Business

Oil price surges towards $100 as Middle East ceasefire begins to unravel

The brief sigh of relief across global markets lasted barely a day. Brent crude climbed sharply back towards $100 a barrel on Thursday after Iran moved to close the Strait of Hormuz, sending a clear signal that the fragile Middle East ceasefire was already fracturing.

The benchmark was trading at $98.61 a barrel in early afternoon dealing, a rise of 4 per cent, having fallen as much as 16 per cent the previous day to below $91 on optimism that a two-week pause in hostilities might pave the way for a lasting peace. That optimism now looks badly misplaced.

Iran’s decision to shut the strait, through which roughly a fifth of the world’s oil and gas passes, came in direct response to Israeli airstrikes on Hezbollah targets in Lebanon, which Tehran condemned as a breach of the ceasefire agreement. It is a move that strikes at the heart of global energy security and one that will alarm policymakers and business leaders in equal measure.

Sultan Al Jaber, chief executive of Abu Dhabi’s state oil company Adnoc, did not mince his words. He made clear that Iran was using passage through the waterway as a tool of political leverage rather than respecting freedom of navigation, a distinction that matters enormously for businesses dependent on uninterrupted supply chains.

Nigel Green, chief executive of the financial advisory group deVere, echoed those concerns, pointing out that a fifth of the world’s oil supply continues to move through a corridor effectively controlled by one of the belligerents. For SMEs already grappling with elevated energy costs, it is a deeply uncomfortable position.

Stock markets reflected the souring mood. The FTSE 100, which had enjoyed its strongest single session since April 2025 with a 2.5 per cent gain on Wednesday, gave back 0.2 per cent to trade at 10,585. On the continent, Germany’s DAX shed 1.4 per cent and France’s CAC 40 fell 0.7 per cent. Across Asia, Japan’s Nikkei, South Korea’s Kospi and China’s SSE Composite all closed lower.

Wall Street, which had rallied sharply overnight with the S&P 500 up 2.5 per cent and the Dow Jones gaining nearly 3 per cent, was expected to open in the red.

President Trump weighed in on social media, confirming that American forces would remain deployed in the Gulf until an agreement was both reached and honoured, warning of severe consequences should it not be.

Meanwhile, Israel intensified its military campaign in Lebanon with its heaviest strikes since the conflict with the Iran-backed Hezbollah militia escalated last month, with more than 250 reported killed.

For British businesses, particularly those in manufacturing, logistics and any sector exposed to energy pricing, the message is stark. The ceasefire may have offered a momentary respite, but the underlying volatility in the Middle East, and its direct bearing on the cost of doing business, is far from resolved. With Brent hovering just shy of triple figures, boardrooms across the country will be revisiting their hedging strategies and bracing for what could be a prolonged period of uncertainty.

Jamie Young

Jamie is Senior Reporter at Business Matters, bringing over a decade of experience in UK SME business reporting.

Jamie holds a degree in Business Administration and regularly participates in industry conferences and workshops.

When not reporting on the latest business developments, Jamie is passionate about mentoring up-and-coming journalists and entrepreneurs to inspire the next generation of business leaders.

BOISE, Idaho — Micron Technology Inc. shares climbed more than 3% Thursday to trade around $420.50 as investors continued to reward the memory chipmaker’s dominant position in the artificial intelligence boom, fueled by sold-out high-bandwidth memory production through 2026 and blockbuster guidance signaling another quarter of record revenue and margins.

The NASDAQ-listed company (MU) rose as high as $425 intraday amid broader optimism in tech stocks following a U.S.-Israel-Iran ceasefire that eased some geopolitical concerns. Micron has delivered staggering gains of more than 300% over the past year and roughly 40-50% year-to-date in 2026, with its market capitalization now exceeding $460 billion as it capitalizes on insatiable demand for advanced DRAM and HBM used in AI data centers.

Micron, a leading producer of DRAM, NAND flash and high-bandwidth memory essential for training and running large AI models, posted explosive fiscal second-quarter results in mid-March that crushed Wall Street expectations. For the quarter ended Feb. 26, 2026, the company reported revenue of $23.86 billion, up 196% from a year earlier and beating forecasts. Adjusted earnings per share surged to $12.20 from $1.56 in the prior-year period, handily topping consensus estimates.

CEO Sanjay Mehrotra highlighted “exceptional” performance driven by tight industry supply, strong AI demand and superior execution. Gross margins expanded dramatically to around 74%, reflecting premium pricing on AI-optimized products. The company also raised its dividend by 30% amid surging free cash flow, which hit record levels in the quarter.

Even more impressive was Micron’s guidance for the fiscal third quarter ending May 2026: revenue of $33.5 billion plus or minus $750 million — a figure that would represent another massive sequential jump and exceed the company’s full-year revenue for many prior years. Non-GAAP gross margin is projected near an eye-popping 81%, with adjusted EPS around $19.15. Management cited higher pricing, lower costs and a favorable product mix as drivers for further margin expansion.

“AI demand far exceeds supply, and we see that tightness continuing into 2027,” Mehrotra told analysts on the earnings call. The company’s entire HBM production for calendar 2026 is already sold out under binding agreements, providing rare visibility in the notoriously cyclical memory industry.

Micron has aggressively ramped production of its HBM3E and next-generation HBM4 products. In mid-March, the company announced it had begun high-volume shipments of its HBM4 36GB 12-high stack, designed for NVIDIA’s upcoming Vera Rubin platform. The new memory delivers more than 2.8 TB/s of bandwidth — a 2.3 times improvement — along with over 20% better power efficiency compared with prior generations.

While some reports have circulated about potential qualification delays or shifts in NVIDIA’s HBM4 allocations for initial Rubin builds, with SK Hynix and Samsung potentially taking larger early shares, Micron executives have pushed back strongly. Management reiterated that its full 2026 HBM supply — including HBM4 — remains fully contracted, with ongoing discussions for pricing and volume on advanced nodes. The company is also shipping samples of even higher-capacity HBM4 48GB 16-high stacks and expanding capacity through new fabs in the U.S., Singapore and Taiwan.

Analysts have responded with a wave of bullish upgrades and price target increases. KeyBanc recently set a $600 target, while UBS raised its target to $535. Consensus price targets now hover around $465 to $500, with some firms calling for $700 or more in optimistic scenarios. Ratings remain overwhelmingly Buy, with Wall Street viewing Micron as one of the purest and most leveraged plays on the AI infrastructure supercycle.

The company’s Cloud and Data Center business unit, which includes HBM sold to hyperscalers and GPU makers, has been the primary growth engine. Demand for memory in AI training clusters continues to outstrip available supply, even as non-OPEC+ producers add capacity elsewhere in the semiconductor chain. Micron’s technological edge in stacking and efficiency has allowed it to command premium pricing while competitors play catch-up.

Beyond HBM, Micron is seeing strength in traditional DRAM and NAND for data centers, PCs and smartphones. The firm highlighted innovations such as PCIe Gen6 SSDs and SOCAMM2 memory modules, further broadening its AI-adjacent portfolio.

Financially, Micron has transformed from a cyclical laggard into a high-margin growth story. Fiscal 2026 revenue is on track for massive expansion, with some analysts projecting full-year figures approaching or exceeding $70-80 billion in optimistic models. Free cash flow generation has enabled both aggressive capital spending — now projected above $25 billion for the year to fuel capacity growth — and shareholder returns via the dividend hike.

Still, risks remain inherent to the memory sector. While AI demand currently masks traditional cyclicality, any slowdown in hyperscaler capital expenditure, resolution of HBM4 technical bottlenecks across the industry or unexpected supply surges could pressure pricing. Micron’s heavy reliance on a concentrated customer base, including major AI players, introduces some concentration risk. Geopolitical tensions, export restrictions and the capital-intensive nature of fab expansions also warrant monitoring.

The stock’s rapid ascent has left valuations elevated by historical standards, though forward multiples remain reasonable given projected earnings growth. Shares have pulled back modestly from recent peaks near $471 but continue to attract momentum and growth-oriented investors.

Thursday’s gains built on a strong session earlier in the week, with elevated trading volume signaling sustained interest. By mid-afternoon, shares traded near $420.50, up about 3.4% on the day.

Micron executives expressed confidence in sustained fundamentals. With new manufacturing sites coming online gradually — meaningful contributions not expected until fiscal 2028 in some cases — supply constraints are likely to persist, supporting pricing power in the near to medium term.

As artificial intelligence spending by companies like Microsoft, Google, Meta and Amazon accelerates, with combined 2026 data center capex forecasts in the hundreds of billions, memory suppliers capable of delivering high-performance, power-efficient solutions are in the spotlight. Micron’s pivot toward AI-optimized products has decoupled it somewhat from broader PC and consumer cycles.

Upcoming fiscal third-quarter results, expected in late June, will be watched closely for further evidence of margin sustainability and any updates on HBM4 ramps or customer diversification. Analysts will scrutinize utilization rates, pricing trends and commentary on 2027 visibility.

For now, sentiment remains firmly bullish. Micron’s record backlog-like visibility in HBM, technological leadership and disciplined execution position it as a cornerstone player in the AI supply chain. Whether the current rally can extend further will depend on continued hyperscaler demand, successful capacity scaling and the broader trajectory of AI adoption.

Micron Technology, founded in 1978 and headquartered in Boise, employs tens of thousands worldwide. Its products power everything from smartphones and servers to the most advanced AI supercomputers. Once viewed primarily as a commodity memory maker, the company has emerged as a critical enabler of the artificial intelligence revolution.

With HBM capacity sold out for the year and explosive guidance pointing to another record quarter, Micron appears poised for what many describe as a multi-year growth phase — provided it can navigate the technical and supply challenges that define the high-stakes AI hardware race.

Julian Lin is a financial analyst. He finds undervalued companies with secular growth that appreciate over time. His approach is to look for companies with strong balance sheets and management teams in sectors with long growth runways.

Julian is the leader of the investing group Best Of Breed Growth Stocks where he only shares positions in stocks which have a large probability of delivering large alpha relative to the S&P 500. He also combines growth-oriented principles with strict valuation hurdles to add an additional layer to the conventional margin of safety. Features include: exclusive access to Julian’s highest conviction picks, full stock research reports, real-time trade alerts, macro market analysis, individual industry reports, a filtered watchlist, and community chat with access to Julian 24/7. Learn more.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of TTD, META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

The BSE Focused IT is a sector index that measures the performance of the 14 companies belonging to the Information Technology sector that are also BSE 500 firms.

The index constituents are Coforge, Cyient, HCL Technologies, Infosys, KPIT Technologies, LTIMindtree, Mphasis, Oracle Financial Services Software, Persistent Systems, Tata Consultancy Services (TCS), Tata Elxsi, Tata Technologies, Tech Mahindra and Wipro.

BSE Focused IT index was launched on October 7, 2024. The index has delivered negative 24% returns between January and March.

BSE shares ended 3% up on the NSE today at Rs 3,260 despite weak markets. Nifty plunged 222.25 points or 0.93% to finish at 23,775.10. Meanwhile, Sensex declined 947.22 points or 1.22% to settle at 76,615.68.

The stock also hit a fresh 52-week high of Rs 3,285.70. The capital market stock has seen a stellar run on the D-Street, delivering 76% returns in the past year. These returns came at a time when Indian markets faced multiple headwinds including rich valuations leading to FII outflows, tariff issues, a falling rupee and weak earnings. The latest setback for global markets including India has been the Iran-Israel war.

BSE shares are currently trading above their 50-day and 200-day simple moving averages (SMAs) of Rs 2,851 and Rs 2,609, respectively.The multibagger counter has delivered 2,070% returns in the past three years.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

Kia plans to release a pickup truck for American consumers in the coming years, as the South Korean automaker plots continued growth domestically and globally.

The company said Thursday it will add a pickup truck that includes hybrid variants by 2030 as a major expansion of its brand into the highly lucrative U.S. market. At least one hybrid variant is expected to be produced in the U.S., according to a presentation from Kia’s CEO investor day.

Detroit automakers General Motors, Ford Motor and Chrysler parent Stellantis dominate U.S. full-size pickup truck sales, however Kia reportedly plans to have its pickup be a smaller, midsize model.

That would position the vehicle against the industry-leading Toyota Tacoma as well as the Ford Ranger and GM’s Chevrolet Colorado and GMC Canyon, among other entrants.

“Accounting for approximately 20% of total demand, the U.S. pickup market represents a key strategic segment. Given its strategic importance, Kia will launch a new Body-on-Frame pickup model to broaden our customer base,” Kia CEO Ho Sung Song said, according to the presentation.

Kia expects to sell 90,000 pickups a year in North America and claim 7% of the midsize pickup segment by 2034, according to Automotive News.

Kia last year entered the global pickup truck market with a vehicle called Tasman. It’s not immediately clear whether the company would use that name or any parts from it for the planned “U.S.-specific” pickup truck or how much its U.S. vehicle would cost.

Kia did not immediately respond for request for comment about the sales targets or whether all variants of the planned pickup would be produced in the U.S.

Its pickup truck plans were announced during the automaker’s 2026 CEO investor day, where it also said it’s anticipating growing annual U.S. sales to 1.02 million vehicles and reaching 6.2% market by 2030. That compares with sales of more than 850,000 units last year and a roughly 5% market share.

Kia CEO Ho Sung Song on April 9, 2026 during the company’s CEO Investor Day in South Korea.

Courtesy Kia

The U.S. is key to Kia’s growth globally. The company said its global sales jumped from less than 2.8 million vehicles in 2021 to 3.14 million last year. Kia on its own is the world’s eighth-largest automaker, but ranks third when combined with its parent company, Hyundai Motor.

Kia said Thursday it’s targeting global sales of 4.13 million units and a 4.5% market share by 2030. That would be up from expectations of 3.35 million units in global sales this year and a 3.8% market share.

The company also announced plans to continue releasing new all-electric vehicles as well as a major push into hybrid and electric extended-range vehicles, or EREVs, including the planned pickup truck for the U.S.

Monthly grocery spend would rise 32% with full adherence, Numerator finds.

Luggage is prepared for an American Airlines flight at O’Hare International Airport in Chicago, Illinois.

Scott Olson | Getty Images News | Getty Images

American Airlines joined other airlines in raising its bag fees Thursday, but the luggage will be even more expensive for customers who buy basic economy tickets.

United Airlines, JetBlue Airways, Delta Air Lines and Southwest Airlines have all hiked the fee to check a bag in the past two weeks as the industry grapples with a jump in jet fuel expenses from the war in the Middle East.

American is raising the cost more for its no-frills option, while the other airlines had across-the-board increases.

The airline will hike the fee by $10 to check a first piece of luggage at the airport on domestic or short-haul international flights starting with tickets booked Thursday. That brings the price for one bag to $50, and a second bag will cost $60 for most tickets. There’s a $5 discount for checking a bag on American’s website or app, making the prices $45 and $55, respectively.

Customers with a basic economy ticket, meanwhile, will have to pay $55 for their first checked bag and $65 for a second bag starting with tickets purchased on May 18. The $5 online discount also applies to those fees, bringing the prices to $50 and $60, respectively, for those who pay in advance.

All customers in basic economy, even those with status, will also have to pay to pick a seat starting on May 18 and will not be eligible for complimentary and system-wide upgrades.

Airline executives have said travel demand is still high, but it’s not clear that carriers will be able to cover the entirety of the fuel price run-up. The effective closure of the Strait of Hormuz is choking off supplies of both crude and refined products like jet fuel, further driving up the price.

Jet fuel is airlines’ second-biggest cost, coming after labor.

Meanwhile, airlines have been leaning into premium offerings and making their basic fares more restrictive as the growth from higher-end options outpaces sales from regular economy. American has fallen behind large rivals Delta and United in seeking out luxury customers, profit and more.

Mane, Arzeda bringing together technologies to scale ViaLeaf Reb M.

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead. We’re sorry we can’t reply to individuals’ comments.Content disclaimer: The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.This publication has been prepared by ING solely for information purposes without regard to any particular user’s investment objectives, financial situation, or means. For our full disclaimer please click here.

Nick Ackerman is a former financial advisor using his experience to provide coverage on closed-end funds and exchange-traded funds. Nick has previously held Series 7 and Series 66 licenses and has been investing personally for over 14 years.He contributes to the investing group CEF/ETF Income Laboratory along with leader Stanford Chemist, and Juan de la Hoz and Dividend Seeker. They help members benefit from income and arbitrage strategies in CEFs and ETFs by providing expert-level research. The service includes: managed portfolios targeting safe 8%+ yields, actionable income and arbitrage recommendations, in-depth analysis of CEFs and ETFs, and a friendly community of over a thousand members looking for the best income ideas. These are geared towards both active and passive investors. The vast majority of their holdings are also monthly-payers, which is great for faster compounding as well as smoothing income streams. Learn More.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BOE, GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Business

Intel Stock Surges Past $60 as Analyst Upgrade, Terafab Partnership and Foundry Momentum Fuel Turnaround Hopes

SANTA CLARA, Calif. — Intel Corp. shares climbed more than 2.5% Thursday, breaking above $60 for the first time in years, as renewed optimism around the chipmaker’s foundry business, a high-profile partnership with Elon Musk’s Terafab project and a fresh analyst upgrade lifted sentiment amid a broader technology sector rebound.

The stock rose as high as $61.08 during the session before settling near $60.44 midday, up $1.49 or 2.54% on strong volume exceeding 60 million shares. That extended a sharp rally that saw Intel gain more than 11% on Wednesday alone and push the shares to a new 52-week high, marking one of the strongest runs in recent memory for the longtime semiconductor giant.

Intel, once the undisputed leader in PC and server processors, has spent years battling manufacturing delays, lost market share to rivals like AMD and Nvidia, and heavy losses in its foundry operations. Under CEO Lip-Bu Tan, who took the helm in early 2025, the company has pursued an aggressive turnaround focused on cost discipline, workforce reductions, improved process technology execution and external foundry customers.

Recent catalysts have accelerated the narrative. On April 7-8, Intel announced it would join Elon Musk’s ambitious Terafab initiative alongside Tesla, SpaceX and xAI to help manufacture advanced AI chips, a move that signaled potential high-volume demand for Intel’s 18A and future process nodes. The partnership sent shares surging as investors bet on renewed relevance in the AI infrastructure race.

Analysts also turned more constructive. Wells Fargo raised its price target on Intel from $45 to $55 while maintaining an Equal Weight rating, citing improved financial flexibility and progress on key nodes. The upgrade helped propel the stock to intraday highs near $59.17 on Wednesday before Thursday’s continuation.

The company’s balance sheet has strengthened noticeably. In early April, Intel agreed to repurchase Apollo Global Management’s 49% stake in its Fab 34 joint venture in Ireland for $14.2 billion, regaining full control over a critical advanced manufacturing facility. The move, financed in part by a healthier cash position, underscored management’s confidence in its long-term manufacturing strategy after years of joint-venture reliance.

Intel’s foundry business remains the centerpiece of the recovery story. The company reported a backlog exceeding $15 billion and is in advanced discussions with hyperscalers including Google and Amazon for advanced packaging services on custom AI chips. CFO Dave Zinsner has highlighted the potential for billion-dollar annual revenue streams from packaging alone, which could deliver attractive 40% gross margins and serve as an earlier bridge to profitability than traditional wafer fabrication.

The Intel 18A process node — a critical bet for regaining process leadership — has shown monthly yield improvements of 7-8% in recent quarters. First 18A shipments occurred in late 2025, with high-volume production targeted for later in 2026. Microsoft and AWS are confirmed customers for custom AI silicon on 18A, providing anchor validation even as the company eyes broader external wins.

Yet challenges persist. Intel’s first-quarter 2026 guidance, issued in January, called for revenue of $11.7 billion to $12.7 billion with breakeven adjusted earnings per share and gross margins around 32-34%, reflecting ongoing supply constraints and the heavy cost of ramping new nodes. Q1 2026 results are scheduled for release April 23, with analysts watching closely for updates on yield progress, supply availability from Q2 onward and any commentary on 14A customer pipeline development.

Data Center and AI (DCAI) revenue showed sequential acceleration in late 2025, growing 15% quarter-over-quarter — the fastest in a decade for that segment. Custom AI ASIC business crossed a $1 billion annualized run rate, though it still represents a small fraction of the overall $100 billion-plus addressable market for such silicon.

The PC client group continues to face headwinds from a maturing market and competition, but Intel is positioning its Lunar Lake and Panther Lake platforms for AI PC leadership, aiming to capture a majority share of next-generation Copilot+ PCs.

Financially, Intel has made progress. Full-year 2025 operating cash flow reached $9.7 billion, and the company expects positive adjusted free cash flow in 2026 despite continued heavy capital spending. Workforce reductions of roughly 30% and disciplined capex have helped stabilize the balance sheet, with cash reserves bolstered by strategic investments and divestitures.

Wall Street’s view remains mixed. Consensus ratings hover around Hold, with average price targets in the mid-$40s to low $50s, though bullish voices see potential for $65 or higher if 18A execution succeeds and foundry external revenue materializes. The stock trades at an elevated forward multiple, reflecting hopes for a multi-year recovery rather than near-term perfection.

Geopolitical tailwinds have also helped. U.S. government support for domestic semiconductor manufacturing, including CHIPS Act incentives, aligns with Intel’s “Made in America” push and has drawn positive attention from the White House. CEO Tan’s engagement with policymakers has reinforced Intel’s role in reducing reliance on overseas foundries.

Longer term, Intel aims to return to 40%+ gross margins as yields improve and higher-value products ramp. Success in advanced packaging, custom silicon for hyperscalers and potential 14A foundry wins could transform the company from a struggling IDM into a competitive player across design and manufacturing.

For investors, the recent surge reflects growing belief that the worst of the process technology crisis may be behind Intel and that Tan’s “time and resolve” approach is yielding tangible results. Thursday’s move lacked major new company-specific news but benefited from carryover momentum, technical breakout above key resistance levels and rotation into beaten-down tech names.

Intel’s market capitalization has climbed back toward $250 billion territory in recent trading, still well below its pandemic-era peaks but reflecting renewed respect for its manufacturing scale and U.S.-based capabilities.

As the April 23 earnings report approaches, focus will center on whether supply constraints are truly easing, any acceleration in foundry customer announcements and updated full-year guidance. Execution risks remain high — yields, competition from TSMC and Samsung, and macroeconomic pressures on capex spending could all influence the trajectory.

Yet for a company once written off as permanently behind in the AI era, the combination of Terafab exposure, regained fab control, packaging momentum and analyst support has reignited the turnaround narrative. Whether Intel can convert that optimism into sustained profitability and market share gains will define its path through the remainder of 2026 and beyond.

UFC 327 — Jiri Prochazka vs. Carlos Ulberg: Fight card, date, odds and more for Miami event

How AI is transforming hospitality operations while preserving human experience

GOLD AND CRYPTO LIVE TRADING || 8 APRIL || Bitcoin Live Trading | Crypto Market Analysis |

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

Business7 days ago

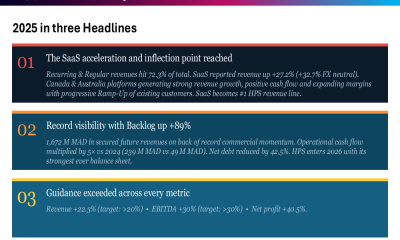

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion6 days ago

Fashion6 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

You must be logged in to post a comment Login