Business

Okta Stock Soars 18% on Strong Q1 Earnings Beat and AI Identity Security Momentum

NEW YORK — Okta Inc. shares jumped more than 18% in early trading Friday, climbing to $112.01 after the identity security company posted better-than-expected first-quarter results and highlighted growing demand for solutions to secure artificial intelligence agents.

The rally reflects investor confidence in Okta’s execution amid an evolving cybersecurity landscape where identity management has become a top priority for enterprises adopting AI technologies. The company’s fiscal first-quarter 2027 earnings, released after the market close Thursday, showed continued revenue growth and margin expansion.

Okta reported total revenue of $765 million for the quarter ended April 30, up 11% from a year earlier and ahead of Wall Street expectations around $752 million. Subscription revenue, the company’s primary driver, rose 11% to $750 million. Adjusted earnings per share came in at $0.91, beating consensus estimates of $0.85.

Remaining performance obligations, a key forward-looking metric, reached $4.719 billion, up 16% year-over-year. Current RPO, representing revenue expected over the next 12 months, grew 12% to $2.499 billion.

The results underscore Okta’s position as a leader in workforce identity security. CEO Todd McKinnon has emphasized the company’s role in helping organizations manage and secure AI agents, an emerging area that is drawing significant enterprise interest.

Okta raised its full-year fiscal 2027 outlook, now projecting revenue growth of 9% to 10%. The company also guided for strong non-GAAP operating margins and healthy free cash flow generation, signaling confidence in sustained profitability improvements.

Analysts reacted positively to the report. Several firms noted Okta’s ability to maintain steady growth while expanding into high-potential AI-related security use cases. The identity security market has gained prominence as companies deploy more autonomous AI systems that require robust authentication and access controls.

Okta’s performance comes as the broader cybersecurity sector benefits from rising threats and digital transformation efforts. Identity and access management solutions have become critical infrastructure for preventing breaches, particularly as remote work, cloud adoption and AI proliferation expand the attack surface.

The company has invested in product innovation to address these trends. Newer offerings, including solutions for privileged access management and identity governance, contributed to stronger bookings in the quarter. These products accounted for a growing share of new deals.

Financially, Okta continues to demonstrate improving operational efficiency. GAAP operating income reached $56 million, or 7% of revenue, compared to $39 million a year ago. Non-GAAP operating income was $191 million, or 25% of revenue.

The company generated solid cash flow, supporting ongoing investments in research and development while maintaining a strong balance sheet. Okta has also returned capital through share repurchases in recent periods.

Wall Street has grown increasingly bullish on Okta’s prospects. Price targets have risen following recent earnings beats, with some analysts citing potential upside from the AI security tailwind. The stock’s valuation reflects expectations of accelerating growth as AI adoption matures.

However, challenges persist in the competitive identity market. Okta faces rivals including Microsoft, Ping Identity and CyberArk. Macroeconomic uncertainty and cautious enterprise spending have weighed on growth rates compared to the pandemic-era surge.

Okta has responded by focusing on larger deals with existing customers and expanding its platform capabilities. The company reported strong performance in upsells to its workforce identity solutions.

Investors appear to be rewarding Okta’s consistent delivery. Friday’s surge marks a significant rebound from earlier 2026 levels, highlighting renewed enthusiasm for software stocks tied to AI infrastructure and security.

The identity security space is expected to grow rapidly as organizations prioritize securing both human and machine identities. Analysts project the market for AI agent security tools to expand substantially over the coming years, positioning established players like Okta favorably.

From a technical perspective, the stock broke key resistance levels on the earnings reaction, with heavy volume indicating broad participation. Traders will watch whether the gains hold through the session or if profit-taking emerges after the sharp move.

Longer term, Okta’s strategy centers on becoming the essential identity layer for modern enterprises. Its cloud-native platform integrates with major cloud providers and supports hybrid environments, giving it broad applicability.

The company’s leadership has expressed optimism about the AI opportunity. Early pipeline interest for AI-related identity products has been encouraging, though these offerings are still in relatively early stages of contribution.

Okta’s transformation from a high-growth disruptor to a more mature, profitable software company has been closely watched. The current quarter’s results suggest the transition is progressing well, with stable growth and expanding margins.

Broader market sentiment toward technology and cybersecurity names remains constructive. Artificial intelligence themes continue to drive investment flows, benefiting companies that enable or secure AI deployments.

For investors evaluating Okta, key considerations include execution on guidance, competitive positioning and the pace of AI product adoption. The company’s track record of beating estimates has helped rebuild credibility after periods of slower growth.

Risks include potential slowdowns in enterprise IT spending, integration challenges with acquisitions and evolving regulatory requirements around data privacy and security.

Okta has a history of strategic acquisitions to bolster its platform. These moves have expanded its capabilities in areas such as customer identity and access management.

As enterprises navigate complex digital ecosystems, demand for unified identity solutions is likely to persist. Okta’s independence from major cloud providers gives it appeal as a neutral, best-of-breed option for many organizations.

Friday’s market reaction represents a strong endorsement of management’s strategy. With solid fundamentals and exposure to a secular growth trend in AI security, Okta enters the new quarter with positive momentum.

Analysts will monitor upcoming quarters for evidence of reacceleration. If AI-related products begin contributing more meaningfully to revenue, the stock could see further upside.

In the near term, focus remains on operational execution and customer retention metrics. Okta’s net retention rates have remained healthy, indicating strong value delivery to existing clients.

The identity security sector is poised for consolidation and innovation. Companies that can combine scale with advanced capabilities are best positioned to thrive.

Okta’s performance this earnings season adds to a series of positive reports from cybersecurity firms, reflecting resilience in the sector despite economic headwinds.

As trading continues, the stock’s movement will be watched closely by growth investors seeking exposure to both established software platforms and emerging AI themes.

A company of Manulife Investment Management, John Hancock Investment Management serves investors through a unique multimanager approach, complementing our extensive in-house capabilities with an unrivaled network of specialized asset managers, backed by some of the most rigorous investment oversight in the industry. The result is a diverse lineup of time-tested investments from a premier asset manager with a heritage of financial stewardship. Note: This account is not managed or monitored by John Hancock Investment Management, and any messages sent via Seeking Alpha will not receive a response. For inquiries or communication, please use John Hancock Investment Management’s official channels.

Invesco is an independent investment management firm dedicated to delivering an investment experience that helps people get more out of life.Be the first to know! Sign up for Invesco US Blog and get expert investment views as they post.Disclosure for all Invesco US articles: Before investing, carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals. NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE All data provided by Invesco unless otherwise noted. Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. ©2015 Invesco Ltd. All rights reserved.

Manhattan Institute expert Adam Lehodey says NYC Mayor Zohran Mamdani’s outreach to Wall Street leaders signals a recognition that New York cannot fund progressive priorities without keeping businesses and wealthy investors in the city.

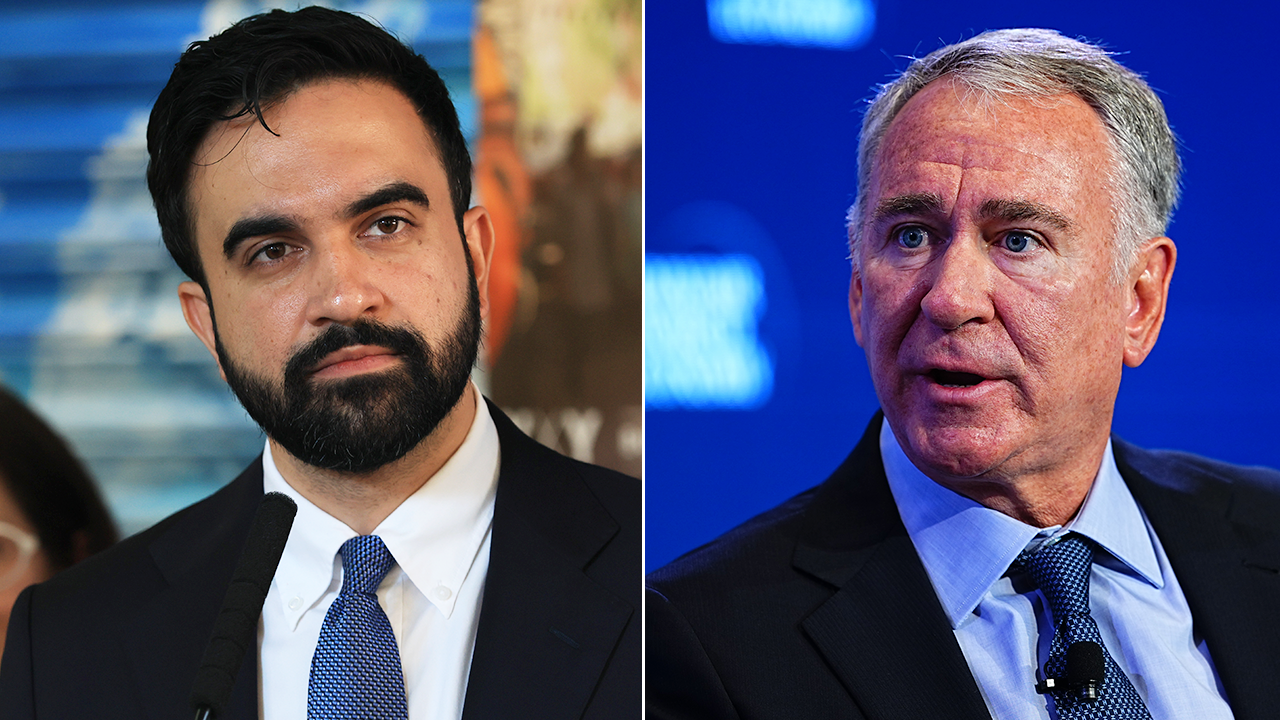

Billionaire Citadel founder Ken Griffin is encouraging New York’s business leaders to take on socialist Mayor Zohran Mamdani, warning that the city’s future could be at risk if employers and investors stay quiet.

“They need to find their voice and fight for their city,” Griffin said Thursday at a Manhattan event, according to Bloomberg.

“My advice is to speak up. What’s the worst that’s going to happen? It will be that New York empties of talent and that’s a catastrophe. If the mayor wants to say a few words about you, your record speaks for itself: You create jobs, you create value and you pay taxes.”

MAMDANI’S WALL STREET COURTSHIP SPARKS CRITICISM OF ANTI-BILLIONAIRE AGENDA

The Citadel founder is clashing with New York City Mayor Zohran Mamdani over taxes targeting the ultra-wealthy and intensifying crime, reviving the same tensions that drove him to pull his business and billions out of Chicago. (Spencer Platt/Aaron Schwartz/Bloomberg/Getty Images / Getty Images / Getty Images)

Griffin’s remarks mark the latest chapter in an ongoing clash between Wall Street’s billionaire class and Mamdani, whose proposals to raise taxes on wealthy New Yorkers and luxury property owners have drawn fierce criticism from business leaders concerned about the city’s economic competitiveness.

The financial titan, whose net worth is estimated at $48.3 billion according to the Bloomberg Billionaires Index, argued that New York’s corporate leaders should focus on the long-term future of the city rather than short-term political battles.

BILLIONAIRE KEN GRIFFIN SAYS CITADEL’S CHICAGO EXODUS WAS ‘NOT HARD,’ CITES CRIME, TAXES

“Everything should be viewed through the lens of, Citadel will be here far longer than he’ll be mayor,” Griffin said.

The comments come as Griffin and Mamdani appear to be cautiously opening a dialogue after months of public sparring over taxes, wealth and the city’s business climate.

The socialist mayor recently reached out to Griffin after previously criticizing the billionaire hedge fund manager over his Manhattan penthouse and personal wealth. Mamdani notably stood outside Griffin’s luxury property to promote his proposal to raise taxes on second homes in New York City worth more than $5 million.

CHICAGO KNOWS WHAT HAPPENS WHEN KEN GRIFFIN TURNS ON A CITY, NOW MAMDANI MAY FIND OUT

New York City Mayor Zohran Mamdani’s “pied-a-terre” wealth tax on luxury properties ignites a contentious debate, drawing strong criticism from Citadel CEO Ken Griffin and hedge fund manager Bill Ackman.

The outreach comes as some business leaders warn New York risks alienating major employers and investors — a concern Griffin has raised before in another major American city.

The tensions have fueled concerns among some business leaders that New York could follow a path similar to Chicago, where Griffin spent years criticizing crime, taxes and public policy before moving Citadel’s headquarters to Miami in 2022. The relocation marked the departure of one of the financial industry’s most influential firms and underscored the economic impact that can follow when a major corporate player leaves a major city.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

Citadel founder and CEO Ken Griffin described New York City Mayor Zohran Mamdani’s “tax the rich” video targeting him as a “creepy and weird” political advertisement. (Krisztian Bocsi/Bloomberg via Getty Images / Getty Images)

Griffin has repeatedly pointed to Florida’s business climate as a model and warned that policies targeting high earners and businesses could make New York less competitive.

Griffin said he plans to talk to Mamdani “at some point in the months ahead.”

“Let’s see where he is on the state of policy at that time,” he said. “Actions speak louder than words.”

Micron's $1,700 Setup Emerges

Cash Builder Opportunities (aka Nick Ackerman) is a former fiduciary and a registered financial advisor with 14 years of investing experience.He is the leader of the investing group Cash Builder Opportunities, where his specific focus is on closed-end funds, dividend growth stocks, and option writing as an attractive way to achieve income. He shares model portfolios and research to help investors make better decisions, via his Investing Group’s active chat room.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of OKE, SOBO, VICI, SBUX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Aaron Chow, aka Elephant Analytics has 15+ years of analytical experience and is a top rated analyst on TipRanks. Aaron previously co-founded a mobile gaming company (Absolute Games) that was acquired by PENN Entertainment. He used his analytical and modeling skills to design the in-game economic models for two mobile apps with over 30 million in combined installs. He is the author of the investing group Distressed Value Investing, which focuses on both value opportunities and distressed plays, with a significant focus on the energy sector. Learn more>>

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Business

Delta Air Lines: My Buy Thesis Played Out, But Growing Risks Are A Real Concern (Rating Downgrade)

Delta Air Lines: My Buy Thesis Played Out, But Growing Risks Are A Real Concern (Rating Downgrade)

Amazon: I'm Buying The Free Cash Flow Collapse

Microsoft: Market Is Missing The Big Picture

Ultragenyx: The Setrusumab Reset Creates A Cleaner Rare Disease Opportunity

Reason Keely Hodgkinson disappeared moments before British final race emerges

John Hancock Multi-Asset Absolute Return Fund Q1 2026 Commentary

Women’s T20 World Cup: India vs South Africa highlights

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Miami – Corporette.com

-

Crypto World7 days ago

Crypto World7 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Business2 days ago

Business2 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Entertainment7 days ago

Entertainment7 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Crypto World2 days ago

Crypto World2 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Business7 days ago

Business7 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Crypto World7 days ago

Crypto World7 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

NewsBeat7 days ago

NewsBeat7 days agowhat doctors are seeing in ebike crashes

-

NewsBeat7 days ago

NewsBeat7 days agoWarning of disruption as Cardiff Crossrail works to start

-

NewsBeat7 days ago

NewsBeat7 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

Entertainment7 days ago

Entertainment7 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Politics7 days ago

Politics7 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

Crypto World7 days ago

Crypto World7 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Tech7 days ago

Tech7 days agoOver 400 Arch Linux packages compromised to push rootkit, infostealer

-

Sports7 days ago

Sports7 days agoDick Advocaat’s Curacao scores first-ever World Cup goal against Germany

-

Business7 days ago

Business7 days agoInvesco Quality Income Fund Q1 2026 Commentary

-

NewsBeat7 days ago

NewsBeat7 days agoSinger Oliver Tree dies aged 32 in helicopter crash in Brazil

-

Tech5 days ago

Tech5 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Tech7 days ago

Tech7 days agoMicrosoft Updates Six Windows’ Apps. ‘Photos’ Gets Watermarks for Copilot Images (Off by Default)

-

Tech7 days ago

Tech7 days agoI tried ASUS’ ROG Xbox Ally X20, and the 171-inch screen changes everything

You must be logged in to post a comment Login