Year Zero: How AI Is Reshaping Our Investment Process

In our last commentary, we discussed Claude Code as “a more recent discovery” with “jaw dropping” potential. With the benefit of hindsight, we were too restrained in sharing our enthusiasm for Claude. In many respects, the past few months have felt like “Year Zero” for our research process, reorienting and rebuilding our tools with and around Claude Code. Chatting with LLMs is helpful, but we have learned this year that it only scratches the surface of AI’s real potential. By leaning into these new discoveries, we have not just enhanced our process, we have already generated key investment insights.

The key point is not that AI makes research faster, though it does. The more important point is that it changes the surface area of what we can monitor, test, and revisit. We can now track more companies, more inputs, and more changes without diluting the quality of our attention. For an investment process built around patience, selectivity, and evidence, that is a meaningful change.

In this commentary we will walk you through our workflow and then discuss a few specific investments. We have several goals in sharing some of our discoveries here:

Advertisement

• We want you to share in our enthusiasm for these new tools.

• We hope others will share ideas with us on how we can become more productive and generate even more value.

• We want to hold ourselves accountable and track our progress over time. We cannot yet quantify the ROI of these tools, but we expect to demonstrate their value more objectively over time.

At the outset, we should be clear that we do not view the deployment of AI itself as proprietary, though we have built proprietary tools that we will not share or discuss. AI is the ultimate force multiplier for human thought, it is not a replacement. Our process is fundamental to our ethos and does not change. RGA believes deeply in a low turnover, GARP orientation, with an appreciation for quality. In fact, in our version of Claude’s core memory (Claude. md), we have memorialized our own investment worldview with a memo describing our workflow from idea generation through portfolio management. Stated another way: Claude, as we use it ourselves, is deeply indoctrinated in our worldview and process. The only real change is in the tools we are using. We have replaced Factset (FDS) with a combination of AI models and a handful of APIs.

Advertisement

Our Workflow

The workflow starts with our dashboard that pulls together all of our various projects. At the very top, we see the results of our agentic project manager. If any of our various projects fails to run or launch as expected, we get a large red tile indicating which project we need to troubleshoot and why it failed to run. Given the time we have put into building these projects, those failures are increasingly infrequent, though it is incredibly important to know if what you are looking at is clean, factual information or something is broken.

Next, we have embedded links into each of our projects, sorted by category:

• Interactive Tools

• Expert & Management Calls

Advertisement

• Industry Dashboards

• Consumer Demand Trackers

• Filings and Macro

• Screening and Quantitative

Advertisement

• Live Signals

• Alternative Data

• Company Deep Dives

• Cross-Project Synthesis

Advertisement

Cross-Project Synthesis then leads into the next section: our daily “Cross-Project Memo.” Each day, this memo focuses on the critical changes across all of our dashboards. Change here is the key—we isolate and focus on what new material surfaces and where there are notable deltas across our various projects. In the delta lie the insights and the questions that we need to pursue. The cross-project memo is heavy on bullet points and visuals. It flows into/concludes “What to watch” and “suggested follow-up inquiry” and these are geared to our North Stars. In a similar fashion to all of our workflows—it concludes with a hole finding agent which uses a cross model validation framework we have developed internally to identify gaps and potential data weaknesses and/or misstatements.

Beyond these projects, we have built dozens of skills. These are not skills with AI, but rather ones that we have taught Claude and built into repeatable workflows. We have built dozens of skills ranging from more rudimentary pieces of our own workflows to call prep and synthesis. These skills are not exactly projects per se, but they help feed into them and have been tremendous accelerants in our own process.

Architecture and Structure

Our preferred setup uses the Antigravity IDE, Google (GOOGL)’s AI-native integrated development platform. We leverage a number of tools therein, with Claude Code in the command-line interface, Gemini side agents for efficient planning, large context windows, and efficient token use, and Codex for heavy quantitative validation work. We are also increasingly leveraging Claude Code via the desktop app for simple recurring tasks we share across our team.

Ryan’s background in CLI has been extremely helpful from the outset. As a consequence, early on, we developed an appreciation for building with thoughtful, scalable architectures and optimizing for token efficiency. These are critical points that ultimately have significant investment ramifications, but should also be at the heart of how projects are executed. Although this commentary focuses on what we have built with Claude, most of these projects do not run on Claude. Most of our projects run on Python scripts, rely on APIs that access structured information, and do not use AI during execution. We have simply leveraged Claude to build durable tools. To the extent they do utilize AI, the LLMs are accessed via API calls with specific parameter settings which we have refined internally. We further cache all the resulting LLM outputs in our own databases—allowing for cost efficient future access. These projects use SQL, JSON and MD files and we have chosen to visualize them in locally stored HTML files. ¹ Claude knows our preferred architectures and folder structures, so each project we start immediately builds in exactly the same, organized way.

Advertisement

As mentioned, several of these projects leverage AI along the way, and for that, we tap into the LLM model of our choice. This is an important point that you will hear more of over time. Although we are mainly using Anthropic (ANTHRO)’s Opus model via Claude Code to build, we are carefully selecting the appropriate model for the given task. For more rudimentary operations ((think aggregating numbers, more like data entry)), we are using the cheapest capable model and for more complex analyses that are semantic in nature, we tend to use Gemini. For numerate and internal reconstruction, we use Sonnet or Opus. These simple rules of thumb are subject to change, but model token efficiency aside, we expect our actual use of AI, as measured by the volume of tokens we burn, to level off or even decline once our phase of heavy building is behind us.

What Next?

The beauty of this structure is that our projects are evolving into the RGA Investment Management Operating System. Our thesis is housed in our own words, nested within how our ideas are being tracked. We are building structured datasets across key areas of our work, and while we are already harvesting insights, we expect the output to grow meaningfully over time. This is happening in a variety of ways. Each of our screeners is built with a real-time performance tracker; in other words, we will objectively know which screens generate value and which ones do not.

To share a few small examples—we are acquiring data points on key inputs for our companies, ranging from points of distribution to pricing to sentiment of reviews and tracking the progression over time. We have developed the logic that sits behind these workflows and translates this data into actionable insights with quantifiable signal value.

Soon, we will undertake a critical step forward, which was referenced above. We will be nesting our projects in a private domain, where our key assets are hosted and accessible online. We may instead forego online hosting and use a physical server that we can access directly. If you are reading this and have strong opinions on the functionality and security of either path, please do let us know.

Advertisement

The most important test for these tools is whether they lead to better questions, analysis and insights. Dashboards and agents are only useful if they sharpen the research agenda, reveal changes we might have missed, or help us say “no” faster. We are already seeing clear value from our new tools.

Turning Process Into Insights

In our Q3 commentary, we featured Google (Alphabet (GOOGL)) as an AI stock. We remain convicted in Google’s positioning, but our work has made us increasingly enthusiastic about AWS, Amazon’s cloud infrastructure segment, as a beneficiary of where AI workflows are heading. In that spirit, our obsession is far more about the profit pools and platforms built on and leveraging AI than with the picks and shovels required to build out AI infrastructure. The market is focused on companies seeing a surge in sales as hyperscalers rush to build AI infrastructure, but we think that focus is misplaced.

When capex inevitably levels off at the hyperscalers ((and it will)), growth will evaporate and margins will compress at suppliers. Tier 2 suppliers in particular will see demand fall off a cliff, particularly as Tier 1 suppliers add capacity into a plateau in demand. As this generational buildout matures and growth capex tapers, investors will likely realize that an entire class of companies should never have had their earnings capitalized at such high multiples. Meanwhile, the companies building recurring revenues that will continue for decades receive little attention amidst the hype. The recurring revenues layer on slowly compared to the surge in orders for hot items, but the recurring revenues compound and do so at high incremental margins. Free cash flow is crimped as companies rush to meet growing demand; however, as growth slows, free cash flow will soar. These dynamics are opposite what today’s market obsessions will experience. Herein lies our obsession with the profit pools that are emerging today.

In that very same commentary we featured Google, we gave a brief shout-out to Amazon’s opportunity to thrive in building the “application layer” of AI by deploying smart orchestration across the retail business’ robotics and logistics layers. The orchestration opportunity will take time to play out, but meanwhile, we see AWS at a critical inflection point today. As discussed above, using the right model for the right task matters, and Amazon is uniquely positioned to benefit from a shift toward token efficiency and workflows built by AI but executed largely through non-AI processes. This has become increasingly clear in our own work and there is growing evidence that the most advanced companies deploying AI are moving this way themselves: durable value should accrue to platforms that can orchestrate models, data, compute, storage, security, and workflow execution at scale. Said differently, Amazon’s ability to remain model agnostic, while serving the lowest cost tokens, positions them uniquely to capitalize on AI adoption at scale.

Advertisement

AWS has been the platform that helped launch countless software, ecommerce and digital service companies and has empowered numerous older companies to migrate their digital infrastructure to the cloud. They have done this with a combination of driving down the cost of compute, leveraging their proprietary chips and building an ecosystem of integrations around their offering.

Amazon was an early partner to Anthropic and owns a considerable equity stake in the company and more recently became an owner in OpenAI (OPENAI) with an equity stake alongside a commitment from OpenAI to spend $138 billion “to consume approximately 2 gigawatts of Trainium capacity through AWS infrastructure.” ² Trainium is AWS’ custom AI chip, designed to compete with Nvidia (NVDA)’s GPUs at an industry-leading total cost of ownership. As CEO Andy Jassy explained, “Our Trainium2 chip has about 30% better price performance than comparable GPUs and is largely sold out. Trainium3, which just started shipping at the start of 2026 and is 30% to 40% more price performance than Trainium2, is nearly fully subscribed. And much of Trainium4, which is still about 18 months from broad availability, has already been reserved.”

At the heart of AWS’ AI offering is Amazon Bedrock. This is a hosted environment that can run many of the leading AI models and agents, as well as many of the open-source cost efficient ones. In a world where leading users of AI require a variety of models, alongside the ability to run non-AI programs, AWS is positioned to win because their scale is greater and their cost per unit ((whether we’re talking tokens, CPU or memory)) is lower than anyone else’s. Notably, Amazon is already seeing clear signs that the flywheel between AI workflows and core cloud infrastructure is starting to take hold and accelerate, as explained by Jassy:

And then at the same time, we’re seeing very significant growth in our core business. And some of that are the migrations that have picked up from enterprises from on-premises to the cloud. But a lot of that is also as AI growth is exploding, it turns out that it leads to a lot of core growth as well, all the post-training, all the reinforcement learning, all the agentic actions and tool usage that these agents are using. And it fits with what you’re asking about on the chip side, which is because we have an unusual collection of chips, we have the leading CPU chip in Graviton, and we have the leading price performance silicon AI chip in Trainium. It means that we’re really unusually well positioned for the inflection that we’re seeing and the type of growth that we’re experiencing.

This growth is only just beginning and will accelerate as people move beyond experimenting with AI to running workflows built by AI, but the market has yet to recognize this reality. The opportunity in Amazon today feels similar to Google at this time last year. Due to AWS’ industry-leading scale during the rise of AI, growth rates are slower than other hyperscaler cloud peers; however, the absolute dollar volume of growth is incredible and accelerating today. This acceleration will continue throughout the year.

Advertisement

Saas Risk Tracker

We wanted to share one of our high value panels built by AI. This is a project we built in order to decipher the SaaS landscape and mine for opportunities where the market might be indiscriminately punishing software companies that are relatively inoculated from AI risk. The learnings have been actionable: since quarter-end, we have purchased two companies where this tracker helped us better understand the relevant risks. We will write about these purchases in our Q2 commentary. It has also kept us from acting on other companies that had been high up our watchlist.

Essentially what we have done is use a combination of quantitative and qualitative factors to assign a score that measures the risk a software company faces from AI. We defined the logic behind resilience and identified a key of traits that would be strong indicators of resilience quantitatively. In our benchmarking, a low score is good, while a high score is bad. We have turned our scores into three separate indexes: a high, medium and low risk bucket, each of which we can track on their own. We can also track an aggregate index. Notably, although market performance is not an input in the model, actual market results have aligned strongly with the model’s assessment of risk. While we are still tracking these data points prospectively—the backtested results and early tracking look promising.

We have overlaid fundamental data and given Claude the opportunity, knowing our worldview, to point us to mispriced market opportunities and to alert us to “value traps” w here the fundamentals might appear compelling, but the risk is too great.

Further down the tracker, we have ranked and sorted every company in our SaaS universe based on the quality of their free cash flow. Each company is ranked objectively on free cash flow quality—high contribution from net income, low contribution from stock-based comp, little deferred revenue, etc. We also take note of the companies with the greatest improvements in free cash flow quality over time. We also analyze the composition of bookings. Companies with very short-duration bookings face different risks than those with longer-term contracts locked in.

Advertisement

The tracker mines the transcripts of each company and pulls out the most important quotes as it pertains to AI’s impact on the business and ranks the quality of those insights. Companies who merely speak qualitatively receive less credit than those who quantify the benefits ((and risks)).

Last, we can click into any of the SaaS companies we track and see the key statements relating to AI displacement, renewal pricing, downsell/seat compression, build vs buy questions, profitability, renewal walls and AI monetization, amongst other factors. Everything is sourced and clickable back to the actual filings or transcripts. This has meaningfully accelerated our work in the SaaS space in a way that previously would not have been possible. We can cover more ground, get to “no” faster on certain companies, and develop a deeper appreciation for the persistence of certain businesses in ways that would have required a very different level of effort in the past.

The full quarterly snapshot of our tracker—covering every company in our SaaS universe along with their risk scores, free cash flow quality rankings, and AI-related management commentary—is available here.

We believe this is an environment where disciplined active management matters. The opportunity set is changing, dispersion is meaningful, and the ability to separate durable fundamentals from temporary enthusiasm remains critical. We are excited about the opportunities in front of us and grateful for the trust you continue to place in us.

Advertisement

If anything in this commentary prompts questions, please reach out. You can contact any of us at 516-665-1945 or through our direct lines listed below.

Jason Gilbert, CPA/PFS, CFF, CGMA | Managing Partner, President

Elliot Turner, CFA | Managing Partner, CIO

Ryan King | Partner

Advertisement

References

1. We will soon migrate everything to a secure, virtual host as our primary portal, but that’s not exactly necessary today.

2. OpenAI and Amazon announce strategic partnership

The route will provide a connection for people travelling to the Alps during ski season

An easyJet plane

Budget carrier easyJet has announced its first international flight from Cornwall Airport Newquay.

The route to Geneva in Switzerland will operate once a week – on Saturdays – from January 16 to February 27, 2027, providing a connection for travellers from Newquay to the Alps during the ski season, with dates including February half term.

The seasonal service will be the only direct winter connection between Newquay and Switzerland and follows easyJet’s recent announcement of a summer route between Newquay and London Gatwick.

Kevin Doyle, easyJet’s UK Country Manager, said: “We are delighted to be putting another route on sale from Newquay, our first international service from the region, following the recent launch of our route to London Gatwick.

Advertisement

“Our winter service to Geneva will be perfect for those looking to book a winter getaway whether that’s for a city break or a ski trip in the French Alps. We are committed to providing our customers across the UK with greater regional connectivity at affordable prices.”

Nigel Scott, commercial director at Cornwall Airport Newquay, added: “We’re very pleased to be able to offer travellers in Cornwall a direct connection to the Alps with easyJet this winter.

“We know demand is high for direct ski access from the region, and this route provides an affordable and convenient way for travellers to land on the doorstep of some of Europe’s best ski resorts.

“Building on the success of easyJet’s summer Manchester route, and upcoming London Gatwick connection, we’re delighted to continue strengthening our partnership with easyJet into the winter season.”

Advertisement

Earlier in June, Cornwall Airport announced plans to launch a direct-flight package holiday programme to Tenerife in March next year. The South West transport hub has partnered with Murray Travel on the programme which will offer two direct departures from Newquay to Tenerife on Friday, March 5 and Friday March 12.

The news comes as the airport’s interim managing director, Amy Smith, steps down from the organisation after 11 years to take up a new role within the aviation sector. The transport hub has not announced a new boss yet, but is expected to appoint a new MD in the coming weeks.

FOX Business host Larry Kudlow argues that President Donald Trump’s diplomatic efforts with Iran are facing undue criticism on ‘Kudlow.’

There’s vastly too much hand-wringing over President Trump’s diplomacy and potential dealmaking with Iran, and it’s coming from friends and foes alike. I think it has more to do with America’s crumbling political infrastructure, than it does regarding the merits of Mr. Trump’s efforts.

First of all, the so-called memorandum of understanding is a nonbinding political document which simply outlines topics to be covered in the months ahead for some kind of final deal. Some people are taking parts of this MOU completely out of context for their own political gain. Let’s step back for a moment.

Advertisement

Over the past year, beginning with Operation Midnight Hammer and continuing through Epic Fury and Economic Fury, American and Israeli allied forces have completely decapitated the Iranian leadership, turned their nuclear capacity into rubble, totally buried their enriched uranium, destroyed their navy, destroyed their airforce, destroyed their radar, destroyed much of their missiles, and drones, and destroyed virtually their entire industrial base. Inflation could be running at more than 200 percent. Food and medicine for average civilians are not available. Currency is worthless. The economy essentially shuttered. In other words, Iran’s military and economic capabilities have been decimated. And people know this whether they criticize it or not. General Jack Keane observed that we’re not even seeing Iranian fast boats anymore in the Strait of Hormuz.

Sen. Rand Paul, R-Ky., discusses President Donald Trump’s diplomatic approach with Iran and argues peace is preferable to military conflict on ‘Kudlow.’

Meanwhile, the New York Post’s Miranda Devine writes that Iranian women at Tehran are now going around on motorcycles wearing skirts and without hijabs covering their hair, a crime that used to result in fines, jail, and savage beatings. Yet the morality police may be dead. Another sign that the radical Islamist Republic is crumbling from the inside.

Because of Mr. Trump’s courageous actions, the only president in the last 50 years to go after Iran forcibly and successfully. Its leadership has been decapitated, their military capabilities have been virtually eliminated, and their nuclear operations have been shut down. All reduced to rubble.

Advertisement

In short, their capacity for harm has essentially been eliminated for years to come with no boots on the ground. So, all this gives Mr. Trump the opening for diplomacy in the future. Why not try it? And that leads to at least a temporary suspension of the naval blockade to reopen the Strait of Hormuz and bring down oil prices to sustain the world economy.

It’s a risk worth taking. Indeed I don’t think there’s any risk at all. And not a single dime of money will reach Iran unless the final deal verifiably with inspectors ends their nuclear program and their enriched uranium. That’s the final deal, not some non-binding memo.

Fox News contributor Miranda Devine says international media is neglecting a story about Iranian women wearing skirts in Tehran on ‘Kudlow.’

Even oil money will be put into an escrow account by the United States Treasury. And released only for buying the Iranian people food, farm, and medical help. Mr. Trump had this to say on the matter: “One of the things that we are doing also, and it came up last night, is money that’s being unfrozen is going to be used to buy food, and the food is going to be bought exclusively through the United States from our farmers. And corn, soybeans, all of the things they need are going to be bought from our farmers.”

Advertisement

That is quintessentially a Trumpian approach in deal making. The absolute key point is that the president, as he has said time and again, is going to end Iran’s nuclear capacity, period, full stop, with verification and inspection. Mr. Trump calls it nuclear honesty. And if Iran doesn’t play ball, then… We will go back to military, bombing, and the economic embargoes, and give them even more damage if that’s what it’s going to have to take.

Right now, Mr. Trump is making the right decisions. Opinion polls more and more are showing a favorable attitude towards his diplomacy and deal-making. So I say, let us stop this hand-wringing and let Mr. Trump do what he does best. Which is make a great deal for America.

I’m an economist and data analyst, with academic roots in econometrics, PPE (Philosophy, Politics & Economics), and an MBA, and 20 years of hands on experience across finance and analytics. Active in equity markets since 2018, I apply quantitative and first-principles thinking to hunt for the story hiding behind the numbers, situations where real earnings power diverges sharply from what the market is currently pricing. I’m drawn to overlooked small and mid-cap names where the numbers tell a more interesting story than the market is willing to acknowledge yet!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Oklo CEO Jacob DeWitte joins Mornings with Maria to discuss the rising AI energy demand, a major Meta partnership and President Donald Trump’s nuclear agenda are accelerating America’s nuclear future.

The Department of Energy on Tuesday announced $17.5 billion in conditional loans for utilities and energy companies to buy parts that will strengthen the commercial supply chain for nuclear reactors.

Energy Secretary Chris Wright said that the announcement supports President Donald Trump‘s executive order by boosting the nuclear industrial base, helping to “unleash the next American nuclear renaissance.”

Advertisement

“To accomplish that mission, these conditional loans will play an important role in reviving the supply chain needed for America to once again build large-scale commercial reactors,” Wright explained.

“They will also help accelerate the timeline of building those large-scale reactors by up to three years, lowering construction costs and ensuring the United States is able to deliver on President Trump’s bold and ambitious energy addition agenda,” he added.

The Energy Department is hoping to speed up the development of new commercial nuclear reactors through the conditional loan program. (Fox News)

The conditional loans were provided by the Energy Department‘s Office of Energy Dominance Financing (EDF). The loans aim to help achieve the goal laid out in the president’s executive order, which is to have 10 new large nuclear reactors with complete designs under construction by 2030.

Advertisement

The $17.5 billion in conditional loans will help finance five eligible projects that are sponsored by utilities and energy companies to speed up the deployment of 10 large-scale commercial nuclear reactors across the U.S. by up to three years. Each of the five loans will support two reactors at a project site.

Westinghouse, which makes the API1000 units that are the only licensed large-scale commercial reactors operating in the U.S. today, will partner with the eligible utilities and energy companies on the procurement of long-lead items at a fixed price.

Energy Secretary Chris Wright speaking during a panel, said that more than half a dozen utilities and energy companies have expressed interest in the program. (Anna Moneymaker/Getty Images, File)

Long-lead items are complex components of a nuclear power plant that require the most time to manufacture and deliver, such as reactor vessels and steam generators.

Advertisement

Each of the projects will be jointly owned by Westinghouse and the utility or energy company partner, with both required to fully commit project equity of $500 million each, for a total of $1 billion, up front before they can access the Energy Department’s loan funds.

The U.S. industry has struggled to attract investment because nuclear projects are capital-intensive, prone to cost overruns and face complex regulations – creating a riskier proposition for investors than relatively cheaper, quicker energy projects involving natural gas and renewables.

The Three Mile Island nuclear power plant is due to return to operation in the next few years. (Heather Khalifa/Bloomberg via Getty Images, File)

Wright told reporters that the loans have attracted strong interest from data center hyperscalers, which are tech giants that run cloud and computing infrastructure, as well as energy companies amid the rising demand for electricity due to the buildout of data centers that power artificial intelligence (AI) systems.

Advertisement

“We are confident that these projects will be economic for utility shareholders, ratepayers and hyperscalers,” Wright said. He added that seven utilities expressed interest, but wouldn’t disclose their names or the location of their projects.

Trump’s goal is to quadruple U.S. nuclear power capacity to 400 gigawatts by 2050, which is an aggressive target given that the last reactors built in the U.S. were delayed by seven years and faced billions of dollars in cost overruns.

Three shuttered nuclear power plants are on track to resume operations in the coming years, including Palisades in Michigan, Three Mile Island in Pennsylvania and Duane Arnold in Iowa.

Advertisement

During Trump’s first term, he used what was then known as the Loan Programs Office to help finance reactors for the Vogtle nuclear power plant in Georgia.

Wright said that the Energy Department expects the plants’ timing and cost to “well outperform what was done on Vogtle.”

NEW YORK — Exxon Mobil Corp. shares rose modestly Tuesday as the energy giant pressed ahead with plans to redomicile to Texas and highlighted its long-term growth strategy in a market buoyed by relatively stable oil prices.

The stock traded at $139.16, up 0.53 percent or 73 cents, in morning trading on the New York Stock Exchange. The move came as broader energy markets reflected ongoing attention to global supply dynamics and corporate restructuring efforts by major producers.

Exxon Mobil announced last week that its planned redomiciliation from New Jersey to Texas will take effect July 1. The shift, approved by shareholders in May, aims to align the company’s legal home with its operational heartland and potentially streamline regulatory and tax considerations.

The company has emphasized that the move supports its focus on delivering long-term value. In its first-quarter 2026 earnings release, Exxon Mobil reported earnings of $4.2 billion, or $1.00 per share. Excluding certain items and timing effects, earnings reached $8.8 billion, or $2.09 per share. Cash flow from operations stood at $8.7 billion.

Advertisement

Chairman and CEO Darren Woods has repeatedly stressed disciplined capital allocation and investment in high-return projects. The company continues advancing developments in the Permian Basin and Guyana, where production is ramping up toward significant milestones.

Analysts maintain a generally positive outlook. Bank of America recently upgraded the stock to “Buy,” citing attractive valuation and strong fundamentals. Consensus price targets hover around $163 to $170, implying upside from current levels.

Exxon Mobil’s forward dividend yield stands near 3 percent, supported by 43 consecutive years of increases. The company returned $9.2 billion to shareholders in the first quarter through dividends and buybacks.

The energy sector faces a complex backdrop. Oil prices have stabilized following earlier volatility tied to geopolitical developments and demand concerns. Exxon Mobil and peers continue navigating the energy transition while investing in conventional resources to meet near-term needs.

Advertisement

Strategic Investments and Operational Focus

Exxon Mobil’s strategy centers on leveraging its scale in upstream production, downstream refining, and chemical manufacturing. The company targets annual production growth of approximately 1.8 million oil-equivalent barrels per day by 2026, grounded in value rather than pure volume.

Key projects include expansions in Guyana, where output is expected to exceed 700,000 barrels per day over time. Permian operations also remain a priority, with efficiency gains helping offset cost pressures.

The redomiciliation to Texas aligns with these operational realities. Texas hosts significant portions of Exxon Mobil’s U.S. assets and workforce. Company officials have framed the change as enhancing long-term competitiveness without disrupting day-to-day business.

Advertisement

Analysts note Exxon Mobil’s balance sheet strength and free cash flow generation as key differentiators. Trailing twelve-month free cash flow exceeded $23 billion, providing flexibility for investments, dividends, and share repurchases.

Market Context and Challenges

Global oil markets remain sensitive to supply shifts from OPEC+ producers and demand signals from major economies. Recent reports of potential U.S.-Iran diplomatic progress added some downward pressure on prices earlier in the month, though benchmarks have since steadied.

Exxon Mobil’s diversified portfolio helps buffer such volatility. Its chemical and refining segments provide counterbalance to upstream swings. First-quarter results showed resilience despite timing effects that pressured reported figures.

Advertisement

Environmental and regulatory pressures persist. Shareholder proposals on climate and governance issues featured prominently at the May annual meeting, though management maintained strong support for its board and strategy.

The company continues reporting progress on lower-carbon initiatives while prioritizing core hydrocarbon developments. Woods has described the approach as pragmatic, balancing energy security with emission-reduction goals.

Analyst Views and Valuation

Wall Street largely views Exxon Mobil as undervalued relative to its cash flow potential and asset base. Discounted cash flow models suggest intrinsic value well above current trading levels, with some estimates exceeding $270 per share under conservative assumptions.

Advertisement

Earnings estimates for full-year 2026 reflect optimism around production ramps and efficiency. The stock trades at a forward price-to-earnings multiple in the low 20s, below historical peaks for the sector.

Risks include prolonged low oil prices, execution challenges on major projects, and evolving energy policies. Exxon Mobil’s size and integrated model provide advantages in navigating these uncertainties.

Outlook

As the second quarter progresses, investors will watch for updates on operational milestones and any further details on the Texas transition. Exxon Mobil’s next earnings report is anticipated in late July.

Advertisement

The company maintains its commitment to disciplined investment and shareholder returns. With shares showing modest gains amid broader market rotation, Exxon Mobil continues positioning itself as a reliable energy supplier capable of adapting to changing conditions.

The idea is part of a 10-year strategy aiming to better connect the region

Amy Woodward, Local Democracy Reporter

05:00, 24 Jun 2026

MetroLink tram from Manchester(Image: Local Democracy Reporting Service / NQ)

A tram network could soon be set to revolutionise transport across Bournemouth, Christchurch and Poole.

Advertisement

The proposal forms part of the BCP Growth Plan, a decade-long vision designed to transform Bournemouth, Christchurch and Poole into a better-connected, more environmentally friendly and inclusive area by 2036.

The blueprint was examined by BCP Council’s Overview and Scrutiny Board on June 15.

A central element of the plan involves enhancing transport links and reducing congestion through environmentally sustainable alternatives such as ultra-light rail.

Councillor Lesley Dedman said: “It is a wonderful wishlist and it does push all the right buttons. We all want these things, for example the advanced manufacturing hub and industrial parks, with these three towns we are short of space so it is those things I am interested in how we are going to work that out.

Advertisement

“Another thing I am not quite sure on is ultra light railway, what a fantastic idea, I am not to sure what it is but I think again those things have been tried year after year and I really hope we can get something going this time as there has always been a problem.”

Councillor Richard Herrett said: “Not a single post-war tram system has been delivered without central government funding. Which means for a tram system we are likely to need some government funding. As the devolution agenda moves forward there is potential in that, but I think where we are in that scheme remains to be seen.

“Trams are universally loved but they do take up a lot of space and that is another challenge we have in out area. I think we would love a tram system but that government funding can’t come too soon.”

The blueprint also puts forward reopening the Hamworthy branch line and implementing additional improvements to ease congestion, support commerce and enhance travel choices.

Advertisement

Redevelopment of key locations including Wessex Fields, Bournemouth Airport and Holes Bay also features prominently.

The broader strategy seeks to stimulate job creation, increase affordable housing provision, rejuvenate town centres and strengthen local communities.

It focuses on long-term expansion in established sectors such as financial services, advanced manufacturing and the creative industries.

While councillors generally back the vision, uncertainties persist around practical implementation, funding streams and the plan’s resilience to future challenges.

Advertisement

A comprehensive report on the growth plan will be considered by cabinet and council at a subsequent meeting.

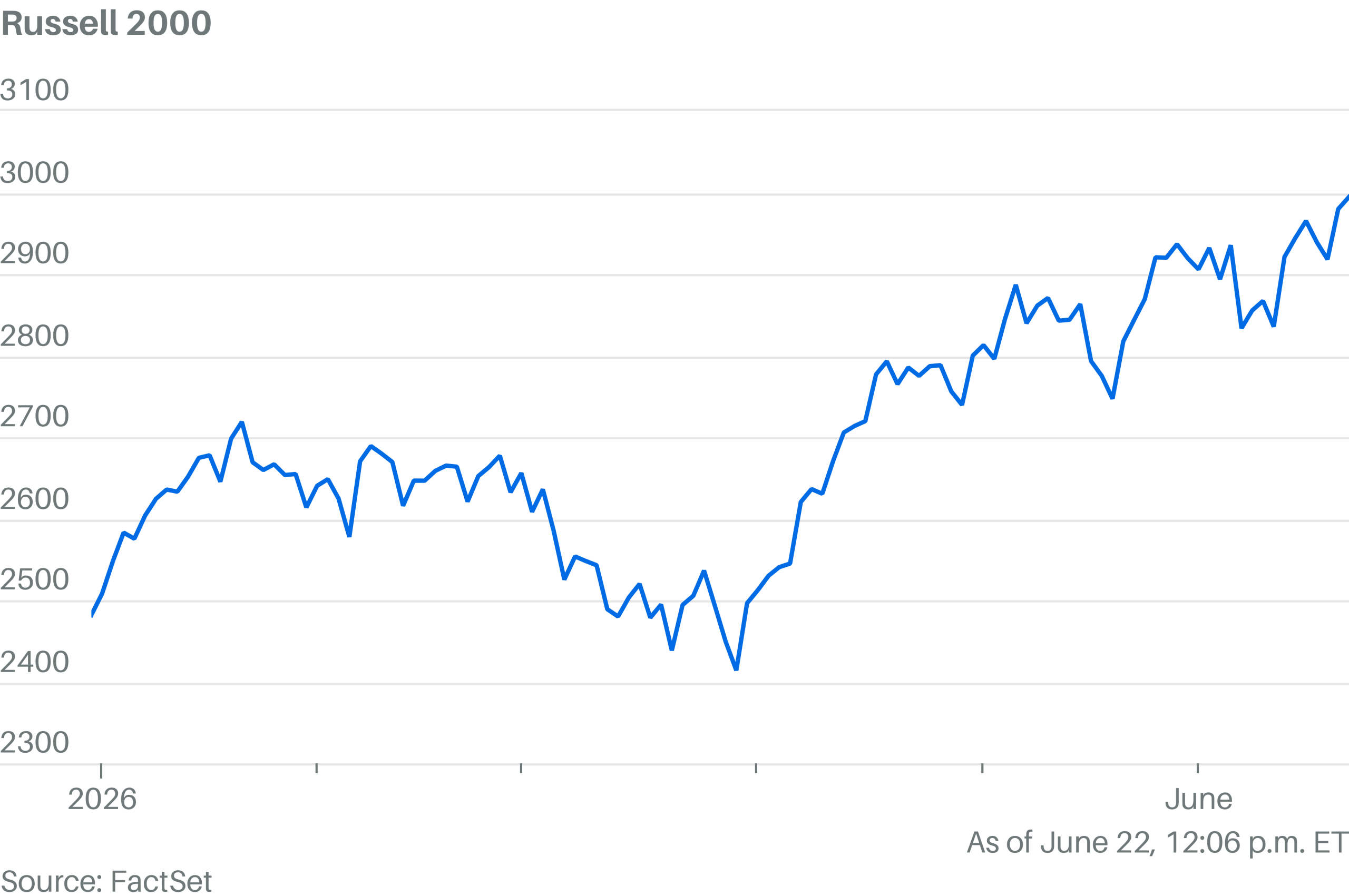

Don’t look now, but the Russell 2000 just hit 3000.

The small-cap index was up 0.7% and trading slightly above the 3000 mark. It first closed above 2000 on Dec. 23, 2020, according to Dow Jones Market Data. It first closed above 1000 on July 5, 2013.

Smaller stocks have been riding a bit of a resurgence this year. The index is up 42% in the past 12 months and 21% this year.

MorningStar Farms is voluntarily recalling two plant-based food products sold in the U.S., Puerto Rico and Costa Rica because they may contain plastic pieces, according to a notice published by the Food and Drug Administration (FDA).

The recall affects MorningStar Farms Buffalo Chik’n Nuggets and MorningStar Farms Hot & Spicy Sausage Patties. The company announced the recall on June 18, and the FDA published the notice Monday.

Advertisement

Consumers who purchased the affected products should not consume them and should instead discard the items and contact the company for a full refund, MorningStar Farms said.

No other MorningStar Farms products are included in the recall.

MorningStar Farms Buffalo Chik’n Nuggets are among the products included in a voluntary recall. (MorningStar Farms / Unknown)

The recalled Buffalo Chik’n Nuggets were sold in 10.5-ounce packages with UPC code 00028989101105 and “Better if Used Before” dates of July 7, 2027, and July 8, 2027.

Advertisement

The recalled Hot & Spicy Sausage Patties were sold in 8-ounce packages with UPC code 00028989100948 and “Better if Used Before” dates of July 5, July 6 and July 7, 2027.

The Chicago-based company said it initiated the recall because of the possible presence of plastic pieces in the food. The products were distributed in the United States, Puerto Rico and Costa Rica, according to the recall notice.

Food recalls involving foreign materials such as plastic can pose a choking hazard or risk of injury if consumed. The FDA classifies recalls involving potential foreign-material contamination among the more common food-related recalls issued each year.

MorningStar Farms Hot & Spicy Sausage Patties are being recalled over possible plastic contamination. (MorningStar Farms / Unknown)

The announcement did not indicate whether any injuries had been reported in connection with the issue or how the possible contamination was discovered.

“At MORNINGSTAR FARMS, our highest priority is protecting the safety and wellbeing of our consumers,” a Mars spokesperson said in a statement to FOX Business. “On June 18, we announced a voluntary recall of two varieties of MORNINGSTAR FARMS products in the U.S., Puerto Rico and Costa Rica because of possible plastic pieces in the food.”

The FDA classifies recalls involving potential foreign-material contamination among the more common food-related recalls issued each year. (Sarah Silbiger/Getty Images, File / Getty Images)

The spokesperson added that the recalled varieties are MORNINGSTAR FARMS Buffalo Chik’n Nuggets and MORNINGSTAR FARMS Hot & Spicy Sausage Patties, and that no other products are affected by the recall.

Consumers seeking additional information can contact MorningStar Farms Consumer Affairs Monday through Friday from 9 a.m. to 6 p.m. ET by calling 800-962-0120 or texting 877-453-5837.

You must be logged in to post a comment Login