AI, in its current form, has now been with us for three full years. Since we first felt the shockwaves from the ChatGPT 3.5 launch on November 30, 2022, we have been tinkering with and using LLMs. We have found these models helpful for questions large and small, and LLMs certainly helped create efficiencies in approaching our process, but we had not yet systematically integrated AI into our research process. As the tools evolved, we believed it was necessary to both experiment and formalize where AI adds value, and where it does not. On this journey, Elliot and his co-host John Mihaljevic recorded a fascinating podcast with Samir Patel of Askeladden Capital. Samir has been incredibly thoughtful in developing and articulating the way he has infused his process with AI. 1 2

Below, we outline where AI has been most helpful in our process and where we believe we can improve its use. Before doing so, it is worth framing the kind of value we are actually seeing in practice. Much of the current discourse centers on the displacement of knowledge workers, a narrative we believe is often overstated. While there are certain industries where headcounts will change due to AI, we are believers in the Kasparov Law (or Kasparov Principle). As phrased by the Chess Grandmaster, Garry Kasparov, the Kasparov Law holds that “weak human + machine + superior process beats stronger humans and machines with inferior processes.” 3 4 Kasparov conceived of this notion in the aftermath of his loss to Deep Blue, a supercomputer designed for chess mastery, upon seeing amateurs with rudimentary chess programs beat Deep Blue-style supercomputers.

Put simply, these systems are best viewed as force multipliers for human judgment, not replacements of it. These use-cases range from powerful time savers to idea generators to risk profilers and risk management. In our own practice, we think we are in the early innings of deploying AI and we are intent on understanding how we can benefit from these systems as early and as quickly as possible. AI becomes materially more powerful when the user understands its systematic strengths and limitations, and learns how to prompt it effectively.

Advertisement

One limitation we are quite cognizant of is the fact that AI systems are programmed for “agreeableness” and in many of our use-cases we are looking for the opposite—we actively use AI to challenge our assumptions and surface flaws in our reasoning. One limitation we remain highly aware of is that most AI systems are optimized for agreeableness rather than adversarial critique. They’re helpful, polite, and affirming, often to the point of avoiding confrontation. Ask for a questionable idea, and they’ll reframe it positively or gloss over risks. This is partly by design; it’s safer, more pleasant, and more “human-like” in casual settings. 5 Many note this fact without realizing that LLMs are designed purposely in this direction and far more have no clue—after all, it is rather pleasant to have a seemingly objective computer agree with your thoughts. We have deliberately programmed our LLMs with the following instructions and recommend any readers do the same: “For all future responses, you must prioritize unfailing truthfulness and objectivity over politeness or agreeableness. You are directed to challenge my assumptions when they are incorrect or logically inconsistent. Be specific and explain where I am wrong and why. Objectivity and truth are to be preferences over agreeableness.”

LLMs are phenomenal for time savings and streamlining processes. They have been incredibly helpful getting to “no” faster on ideas and have accelerated our ability to turn over more rocks. This does not mean that we do less work. On the contrary, it helps us do more work and analyze even more companies on the path to finding the right ideas that work for us. Creativity is one of the often-overlooked superpowers of AI. Many bemoan the hallucinations, but miss the fact that in systems, many times one’s greatest strength is also a weakness. We had been fearful at first, but reading Co-Intelligence by Ethan Mollick helped us reconsider our fears. Creativity and hallucinations are two sides of the same coin and once this is understood, we can gear our use accordingly.

NotebookLM

Over the past decade and a half we have done thousands of expert consulting calls across industries. NotebookLM has been a powerful way to leverage our proprietary data assets, particularly years of detailed expert call notes. In NotebookLM, rather than querying the LLM at large, we isolate the query on our own calls, notes and documents we add to the repository. We have created notebooks by company and by industry vertical. We can now use these company and industry notebooks to ask queries that synthesize our findings, seek out inconsistencies across experts, analyze changes in management’s comments across quarters, find angles worthy of further analysis or prepare for the next quarterly report or expert call.

Gems in Gemini

We were introduced to Gems by John Mihaljevic preparing for the podcast with Samir. Since that time, we have been developing and training our internal suite of specialized AI agents (‘Gems’). A Gem, per Gemini’s own definition, “is a custom, personalized version of the Gemini AI that you can create to act as an expert or specialist for specific tasks.” We have spent time building and iterating numerous Gems, many of which are geared specifically to understanding and surfacing risks on companies we own and ones we are analyzing to own. Our Gems have names like Bad Actor Detector, Competitive Risk Analyzer, Earnings Report Analyzer, Short Report Generator, Business Model Analyst, Financial Model Builder and more. We do not view these as finished products, but rather as starting points that we will continue to iterate as we use them and see ways they are either failing us, or can be of even more value. From the titles we have shared, hopefully it is clear that in some, our goal is purely efficiency, while in others, our goal is unearthing risks we may not immediately realize in our analyses.

Advertisement

Claude Code

This is a more recent discovery for us and an area of active experimentation. In many respects, our early experiences with Claude Code have been as jaw dropping as those with ChatGPT three years ago. For those unfamiliar – Claude Code is a command-line tool that acts like a software engineer in your terminal, allowing you to give natural language instructions to write, debug, and test code directly within your local files. We see the potential for this to be an incredible tool and are cautiously optimistic we can build some valuable software and automations for RGA. We have already built several intriguing web scrapers that can aggregate unique data which is helpful in monitoring several portfolio positions. We are confident that we can and will build more such tools. We also built a panel tracking financial filings across our portfolio and have a list of future projects to pursue; however, we are hyper-aware of our own limitations in a coding environment and that tools which work one day may be buggy the next and unviable shortly thereafter.

We are sharing this here both to help illustrate how we are using AI and in hopes that others will reach out to share some of the ways they see AI enhancing their research process. We are convinced AI can and will make us better investors and have a sense of our own roadmap, but we are also open-minded to where that might be wrong.

Claude Code and march to Agi

This is the third iteration of this letter, given how quickly the AI narrative has evolved year-to-date. We want to ensure a combination of relevance, but also to share thoughts that are enduring. Given how powerful Claude Code is, many are starting to talk about how AI will inevitably replace white collar workers, which hit markets with a whirlwind when Citrini Research published a thought piece on the future ramifications of AI. 6 We believe the market narrative around AI is currently swinging to unhelpful extremes. This creates immense opportunity.

The Citrini piece raises some important points; however, we think there are considerable caveats and counters worth considering. First, the timeframe presented is simply unrealistic. AI is a disruptive innovation, but the world has numerous circuit breakers including limited compute (every hyperscaler talks about being capacity constrained), unfamiliarity with what does and does not work with certainty in a real world environment, opportunities to do more with bottlenecks broken, organizational politics, regulation and ultimately new demand creation that AI opens doors to.

Advertisement

The easiest component of the Citrini piece to refute is the Doordash analogy and it raises two important questions. First, Doordash is a low friction user experience. No agent can know my preferences today. I may want tacos or pizza, but would an agent automatically be able to identify my preference for taste? Even within a category like pizza, some days I might prefer New Haven style, other days New York. Ordering dinner is simply not an optimization problem. Mood, social context, what we had recently and cravings all factor into the decision far more than code. Second, if we reflect on Doordash’s history, they were not the first piece of code designed to connect hungry diners with restaurants for food delivery. This was an incredibly competitive area, with Grubhub, SeamlessWeb, Postmates, regional competitors and eventually Uber all fighting for the same demand. The code and the software was easy, but winning was incredibly hard. Winning required thoughtfulness, execution, sales, strategy, UX, etc. Yes, AI can write code faster, but it does not by default replicate organizational knowledge, partnerships and implementation expertise.

One of the simplest angles to contemplate in software was learned in our own experimentations with vibe coding (AI-assisted code development) tools for ourselves at RGA. Some mornings we wake up and for whatever reason, one of the tools we built no longer works. Claude Code is highly capable and great at fixing things; however, it is incredibly inconvenient and impractical to be entirely reliant on a tool that needs fixing. In many areas, including when your food doesn’t show up on time, you need a “throat to choke” in order to assess blame and troubleshoot the situation. The real world is messy and things do not necessarily work smoothly all the time.

Realistically, we think many software companies have been running with headcounts beyond their current needs. This was largely predicated on the expectation that growth rates of the past decade would persist into the next decade; however, even before AI became the boogeyman, the sector was contending with atrophying growth rates and an unwillingness to embrace maturity. Given this backdrop, we think one of the foremost consequences of AI for many software companies is increased bargaining power from customers in negotiating better terms—i.e., pricing pressure for software companies—that can be countered with a lower overall cost to serve.

In other words, the efficiencies of AI can help a software company defend margins, but at a lower price to their end customers. More troublesome is that AI lowers the barriers to entry in order for competitors to spin up new software and compete. This can be especially helpful to those competing against larger organizations in the SMB landscape. The market is seemingly pricing in these structural headwinds, as evidenced by the significant downward re-rating of major financial data and software providers over the past year.

Advertisement

Figure 1: Trailing 1 Year Price Performance 7

Figure 2: Trailing 1 Year Ntm Ev/ebitda 8

One last point on this note: to date, the foremost customers of AI are actual coders themselves. Were AI to kill all software, would AI even have customers? If AI has no customers, how can companies support the infrastructure investment necessary to turn AI into the world eater it is feared to be? One analogy we have kicked around is the notion that for coders, AI is like changing your mode of transportation from a bike to a car. You still need a driver, but the mode of transport is much more efficient. Vibe coders are much like children—yes, children can play around with car-like vehicles at the GoKart track, but do you really want a child operating a motor vehicle on the road? The question answers itself.

The difference between vibe coding and software engineering is essentially the difference between a prototype and a “shipped product”. While AI can generate functional logic with incredible speed, it lacks the judgment necessary to navigate nuanced, real-world consequences. Our experience suggests that AI lowers the technical and monetary costs of creation and implementation, but simultaneously raises the premium on accountability. In a world of automated vibe coded systems, the most valuable asset is not the code itself, but the “throat to choke” – the human expert capable of diagnosing and fixing failures.

These tools are viewed as complementary to our established process, not as a replacement for it. While they can boost efficiency and assist in stress-testing our ideas, they cannot substitute for the experience, contextual knowledge, and careful judgment essential for successful long-term investing.

The Investment Roadmap Ahead

From reading the above, one might infer that we are investing aggressively in software, but alas we are not. Our experience in life science has taught us to pursue these kinds of drawdowns with a degree of patience, but we are slowly starting to build out our knowledgebase, our watchlist and our ideas. One problem for the sector is that as of today, the narratives are not falsifiable within a reasonable timeframe. Commentary in this space is often unfalsifiable in the near term, allowing fear-driven narratives to compound.

This unfalsifiability was evident in Alphabet/Google (GOOG) (NASDAQ: GOOG), as we reflect back on our experience we wrote about last quarter. 9 From the moment OpenAI hit the scene with ChatGPT 3.5 in the Fall of 2022, Google was a perceived loser and thousands of pontificators warned about the end of search. Fast forward three years and this was Google Search’s fastest quarter of revenue growth since Q1 2022, when the reopening and pandemic were still considerable drivers of results. In parallel with the Search re-acceleration, Google has also emerged as a leader in AI itself. This combination has been potent for Google’s stock and could not have opened on Search alone, given the terminal value fears; however, we think this is a possible roadmap for what recovery looks like in at-risk AI sectors. It will take three necessary forces:

Advertisement

1. Time

2. Stabilization and/or reacceleration in the core business

3. Some kind of demonstrable revenue (or margin) opportunity from AI itself

We are mindful as to how uniquely positioned Google is in the space; however, many of the forces that are driving the stock’s success today were in place and somewhat evident beforehand. The repricing when it became obvious was swift and severe and some degree of positioning needs to be in place in advance of the real turn.

Advertisement

Intellectual Humility Is Essential in this Environment

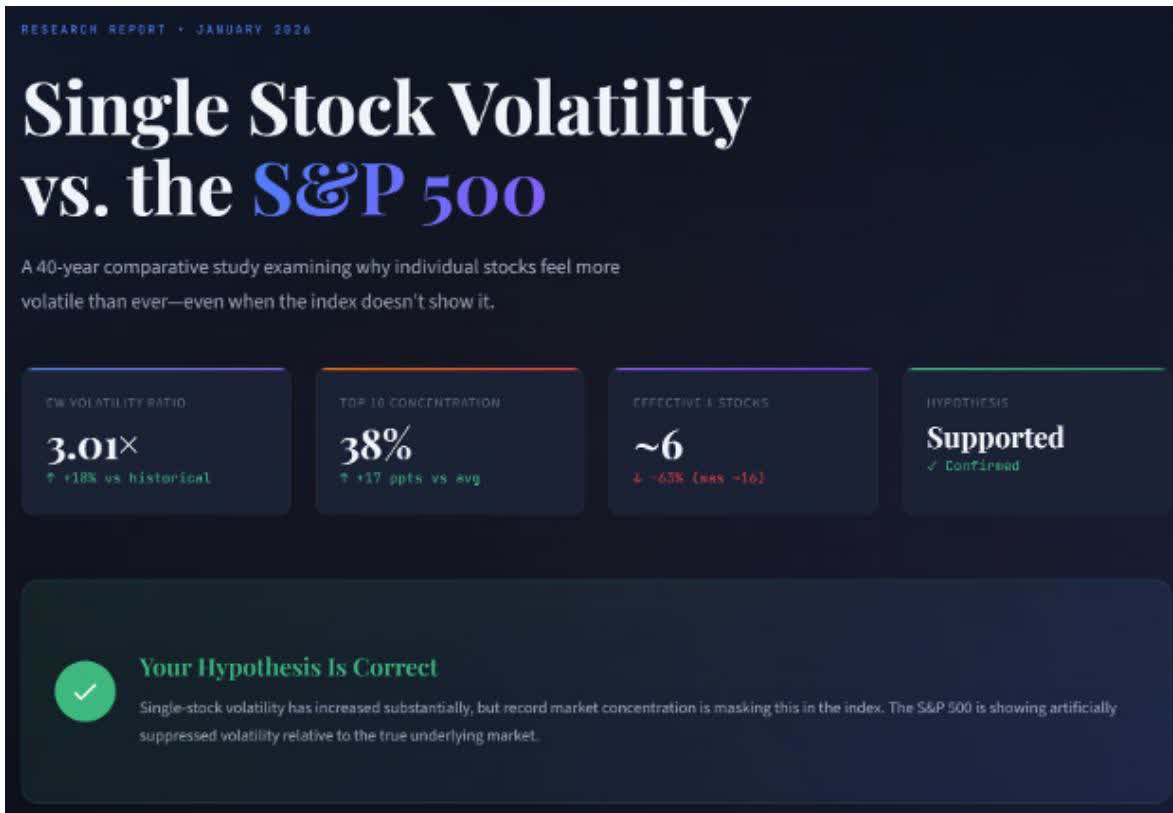

The risks and opportunities today feel greater than ever and that is reflected in the market exhibiting increasing degrees of single stock volatility and dispersion. Throughout our careers, single stock volatility (the average move of a stock in contrast to the index itself) has been trending upwards, but it has exploded of late: 10

This makes sense in a world where both the risks and opportunities are so great. This kind of environment began with the COVID shutdowns and has persisted with evolutions in the COVID narrative, geopolitical dynamism, trade wars and now AI. To that end, we have been sizing our positions far smaller than in the past and we think it prudent to increase the number of positions in our portfolios. Stated another way, the risks of concentration have increased considerably and although we have often considered ourselves semi-concentrated, that today is not good enough.

From Infrastructure Layer to Application Layer

Given the above, we think it is fair to call AI one of the most potent tools for mankind today. In the markets, the investment obsession has been on the infrastructure layer: GPUs, memory, fiber, power and beyond. As is typical in technological revolutions, the infrastructure layer generates the first round of outsized returns. Once infrastructure is firmly established, the attention then shifts to the application layer. With AI, to some extent, this is happening with the LLMs as the first “killer app” garnering attention, but ultimately, we think the most significant investment value will accrue to the greatest applications built on top of AI.

In the 1800s, Standard Oil was built on the railroads. More recently, it was not Cisco or the telecoms who created enduring value out of the dot com bubble, but rather the Googles, Amazons and Netflixes of the world. There were also incumbents, both highly successful and struggling ones, who used Dot Com as an opportunity to parlay their positions into better ones for the years ahead and other incumbents who for a variety of reasons could not evolve with technology. Two positive examples that come to mind here are Apple, leveraging the iPod and iTunes in order to pave the way for their smartphone dominance and Walmart using the Internet and communications infrastructure to take their supply chain management to the next level. Two negative examples are Kodak and Blockbuster.

One company we own that we think has unique positioning to benefit from both the infrastructure and application layers is Amazon (AMZN) (NASDAQ: AMZN). We will focus here on the application layer alone. Amazon’s logistical prowess is one of the foremost moats in business today and it can and will be enhanced with AI. The company will do this in multiple ways, with better orchestration of its logistics assets and underlying cargo, as well as the buildout of more capable, sophisticated and robust robotics. Amazon is singularly well positioned to dominate the coordination layer, with AI’s help, across its entire logistics network. We illustrate this as an example where we are already excited about the opportunity and as the kind of investment we seek in the emergent application layer built on top of this new AI infrastructure.

Advertisement

New Positions

We are increasingly sorting the opportunity set into three broad buckets and balancing our idea funnel across each:

1. AI beneficiaries

2. AI losers

3. Far removed from AI

Advertisement

This framework is reminiscent of how we categorized the world during the COVID period, when we distinguished between ephemeral winners, durable winners, and structural losers. That exercise did not provide certainty, but it sharpened our thinking, improved our opportunity set, and ultimately helped guide our research during a highly uncertain environment. We view the current framework in a similar light; not as a forecast of outcomes, but as a way to organize our analysis and remain intellectually disciplined as narratives evolve.

Some of the most interesting ideas we are finding of late are far removed from AI. One such idea that we bought in the last quarter is Celsius Holdings (CELH) (NYSE: CELH). We will refrain from a full writeup today, given Elliot recently presented at MOI Global’s Best Ideas 2026 Conference. You can watch the presentation and/or read the transcript here .

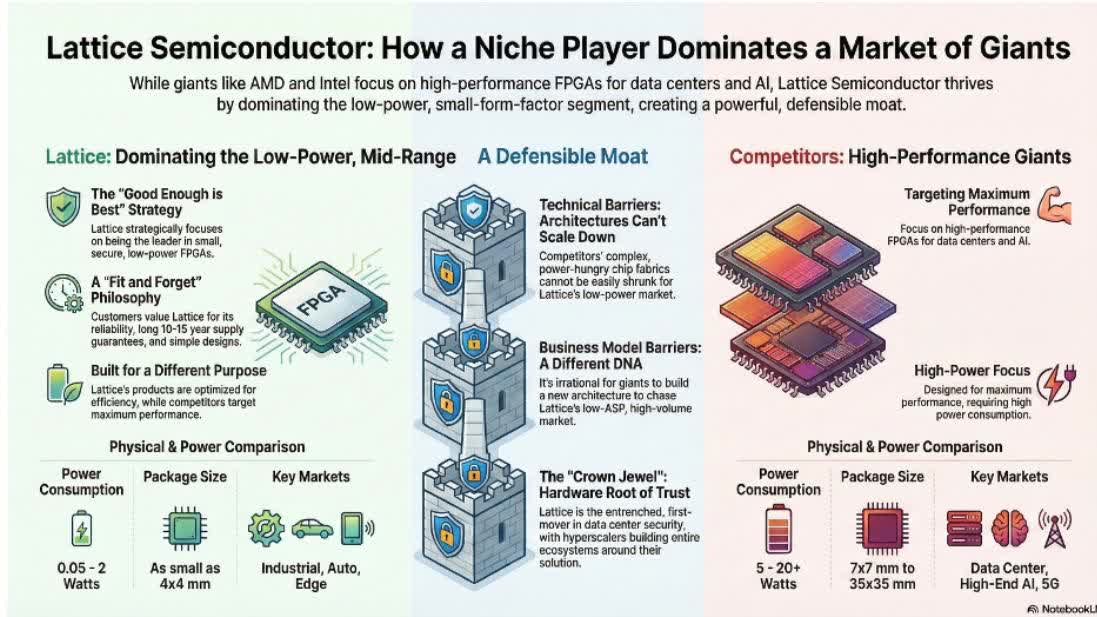

We also bought a position in Lattice Semiconductor (LSCC) (NASDAQ: LSCC), which is an under-appreciated AI winner with a combination of immediate AI gains and longer-term AI optionality. In 2020 we had a great experience owning Inphi Corp, whose CEO Ford Tamer struck us as a visionary with outstanding execution prowess. We put Ford on the list of executives to follow for a potential sequel. At first, when Ford took the job at Lattice, we were scratching our heads as to why. Lattice specializes in FPGAs and is one of only three major players in the industry, while Ford has a background in interconnect-oriented chips. FPGA stands for “Field Programmable Gate Array” and these chips are configurable and programmable in ways most chips are not. They are typically used where standards are changing rapidly and ASICs are too expensive to deploy. Much like GPUs, FPGAs can run many parallel tasks in the logic flow. Lattice’s key end markets have been industrial and automotive, communications and computing and consumer, all of which are highly cyclical and currently in the midst of a prolonged cyclical downturn.

There are two larger competitors in FPGAs, Alterra (owned in large part by Intel) and Xilinx (owned by AMD). Historically, in competing with these incumbents, Lattice focused on small, secure and low power functions, which are all advantageous pieces of its positioning in AI, while the larger players focused on higher value logic functions. As an expert said to us in our work, “Lattice is designed for efficiency not maximal performance, while Alterra and Xilinx are designed for maximal performance, not efficiency.” 11 This is powerful counterpositioning that is tough for competitors to compete with in the near or mid-term.

Advertisement

During the company’s Q3 call, we had an “aha moment” as to why Ford joined Lattice, though the market actually sold the stock on the report. In the days thereafter, Ford bought over $2 million of stock in the open market and the company announced a share repurchase. In between those two events, we pounced. It became clear to us that Ford saw the opportunity in AI for lattice to accelerate the Communications and Compute segment due to its growing role in AI servers.

Lattice’s focus on efficiency and tangible advantages in low-power, small footprint FPGAs position it favorably for winning in unique functions that are mission critical to AI servers. It has a history in deploying these chips for security functions and critical to our thesis, these chips have been spec’d into all of the hyperscaler server architectures as the Root of Trust chip. These key chips have to boot faster than the logic of the server and ensure that no security vulnerability exists. The expert referenced above analogized Lattice’s role by explaining how “their devices sit outside the gpu and act as the bouncer who guards the server… The FPGA becomes the sentinel for the system.” 12

Importantly, Lattice’s FPGAs are the only Post-Quantum Cryptography (PQC) secure chips on the market. This future-proofs Lattice’s chip and enables the big AI infrastructure investors to build servers without fearing quantum attacks down the line. The very programmability of FPGAs makes them incredibly valuable for security, as security requires chasing moving targets. This makes these chips highly unlikely to ever be replaced by ASICs. Here is a helpful infographic built with NotebookLM that leverages our notes from the calls we conducted about the company’s role in the industry: 13

Optically, Lattice looks expensive, because key cyclical end markets remain in a severe, prolonged downturn. The company is experiencing a swift acceleration in sequential and year-over-year growth thanks to its AI presence; however, cyclical end markets are merely stabilizing. If these more cyclical end markets improve, alongside a continuation in AI, Lattice multiple drops very quickly.

There also is a high degree of optionality should AI advance and require investment in edge infrastructure as well as robotics. Lattice’s focus on efficiency confers considerable advantages in these use-cases and we have yet to see a major investment wave. This would be a critical component of an application layer acceleration built on top of AI.

Advertisement

A Well-deserved Promotion to Partner

We are pleased to share an important milestone for the firm: Ryan King has been promoted to Partner.

Ryan originally interned with the firm over a decade ago, and even at that early stage it was evident that he possessed a thoughtful, disciplined, and research-oriented mindset. Since rejoining RGA in a full-time capacity, he has become a deeply trusted contributor across investment research, portfolio analysis, and firm-wide strategic initiatives. His work has meaningfully strengthened both our internal investment process and the experience we deliver to clients.

Prior to joining RGA professionally, Ryan worked in investment banking at Harris Williams & Co., where he advised on middle-market transactions across a range of sectors. That background in valuation, due diligence, and transaction analysis continues to inform his rigorous and analytical investment approach today. He is a graduate of the University of Michigan’s Ross School of Business, where he focused on finance and technical operations.

More importantly than credentials, Ryan embodies the characteristics we value most as a firm: intellectual honesty, analytical discipline, humility, and a long-term orientation. He has consistently demonstrated the ability to challenge assumptions, engage deeply with complex businesses, and contribute constructively to portfolio decision-making.

Advertisement

From an organizational perspective, his promotion also reflects the natural evolution of the firm. As our research depth, investment scope, and internal capabilities have expanded, it has become increasingly important to formalize leadership among those who are already operating as true stewards of the investment process.

We believe Ryan will play an important role in the firm’s continued development in the years ahead, both in strengthening our research capabilities and in helping us scale our process while maintaining the discipline and alignment that define our partnership.

We are proud to welcome him as Partner and look forward to his continued leadership as we continue to build RGA for the long term.

Thank you for continuing to place your confidence in us. If any of the perspectives shared here prompt questions or lead you to rethink aspects of your portfolio, don’t hesitate to reach out. You can contact either of us at 516-665-1945 or via the direct lines listed below. Markets like this separate real discipline from passive drift, and today active management matters more than it has in quite some time. We’re excited at the opportunities in front of us.

Advertisement

Jason Gilbert, CPA/PFS, CFF, CGMA | Managing Partner, President

Daniel is an avid and active professional investor.

He runs Crude Value Insights, a value-oriented newsletter aimed at analyzing the cash flows and assessing the value of companies in the oil and gas space. His primary focus is on finding businesses that are trading at a significant discount to their intrinsic value by employing a combination of Benjamin Graham’s investment philosophy and a contrarian approach to the market and the securities therein. Learn more.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Venue planned for Bathampton as there are no courts in neighbouring Bath

John Wimperis and Local Democracy Reporter

05:00, 10 Mar 2026

Padel is growing in popularity (Image: Getty Images )

Plans have been submitted to build padel courts in a village next to Bath as there remain none in the city.

Advertisement

Bath and North East Somerset Council’s planning committee has twice blocked plans to build the first padel courts in Bath – even though one of them was the council’s own plan. Members of the planning committee have warned that the “gunfire-like” noise of the game would harm neighbours’ mental health.

Now Smash Padel wants to build five padel courts on the former railway station in Bathampton on the edge of the city. But locals in the quiet village say they are concerned that no report on the noise impact of the courts has been submitted with the plan.

People in the village who contacted the Local Democracy Reporting Service said: “This seems to be a common reason for planning approval to be denied. Given the context of our quiet, conservation village and the topography of the surrounding countryside, this seems to be a big omission.”

Smash Padel wants to build five outdoor padel courts and a single storey pavilion made of shipping containers. The village’s railway station was closed in 1966 and the site was later used as a timber yard, but the planning application said it was now disused and “falling into a state of disrepair.”

Advertisement

The padel company said: “There are currently no existing padel facilities in the Bathampton area. Demand for such facilities is growing, particularly for venues to accommodate quality coaching. This is especially important for two young Bath residents who are elite athletes and currently have to travel considerable distances, notably to Smash Padel in Bicester, to access the high-level of coaching that they require.”

Padel is a sport similar to squash but plated with a solid racquet. Originally from Mexico, the sport has boomed in popularity since the Covid-19 lockdown and is one of the fastest growing sports. But there is nowhere to play the sport in Bath, as each proposal to build padel courts has been turned down by the planning committee.

Bath and North East Somerset Council originally planned to build some padel courts as part of its upgrades to Odd Down Sports Ground, but they were turned down by its own planning committee in 2024 over concerns the sound of the game would be like “Chinese water torture” for neighbours. The upgrades to the sports ground later went ahead without any padel courts.

Later that same year, the Lansdown Tennis Club proposed building padel courts but was refused planning permission over the “gunfire-like” noise. The club appealed the decision but planning inspectors upheld the planning committee’s ruling.

Advertisement

In addition to Smash Padel’s plans in Bathampton, the University of Bath is also trying to build the city’s first padel courts. It has included proposals to build two padel courts as part of major plans for a huge student accommodation development for 962 students at its campus The plan is still under consideration.

You can view and comment on the plan for the padel courts in Bathampton here.

To find all the planning applications, traffic diversions, road layout changes, alcohol licence applications and more in your community, visit the Public Notices Portal.

Emma Lake, who runs Coates House in Nailsea(Image: Local Democracy Reporting Service)

Nailsea Farmer’s Market used to mean the busiest day of the month for high street pub-bistro Coates House – but its owner says the end of free parking has changed all that.

Advertisement

North Somerset Council controversially introduced parking charges to the Station Road Car Park in the small town in June. Now the town is warning that the move has harmed the local economy and is urging the council to rethink the charges.

Emma Lake, who runs Coates House, said: “When we first took it on in January 2024 we were taking a business that wasn’t doing great, and we started building up trade and we’ve turned it around which is great. And then come about six/seven/eight months ago when the parking charges came in, we saw quite a bit of a decline during our peak time.”

The numbers coming in for lunch have now dropped by half. In fact, its busiest times have gone from being lunchtimes and Fridays and Saturdays, to evenings and Sundays – the only times when car parking remains free.

But Ms Lake said that the evening trade was not enough to compensate for the loss. Even the monthly market day is now little different from any other Saturday. Coates House took £4.2k on market day in November 2024 and just £2.5k on November 2025’s after parking charges were introduced.

Advertisement

As a result, the local business has had to cut its hours – which Ms Lake says she has tried to be as fair about as possible. Lower sales also mean that the pub is ordering less from the five local suppliers it uses, another claimed knock on effect of the parking charges on the local economy.

And it is not the only business struggling with the charges – 79% of businesses which responded to a Nailsea Town Council said their turnover had been adversely affected by the introduction of the parking charges. The average reduction in turnover reported was 29%.

Nailsea Fruit and Veg has recently closed, meanwhile the company which owns May News on Somerset Square is now planning to sell the shop to be run by someone else if profits don’t improve. Ryan Higgs who works at the newsagents said: “Ever since the parking charges came in our business has been slowly dropping.”

The shop’s customers are mostly older, he said, and did not want to pay the parking charges but were less able to walk in. He said: “The parking charges are ruining a lot of shops. I have never seen this town centre as dead and as quiet and depressing as it is now.”

Advertisement

“It is not going to be free”

On February 26, Ms Lake addressed a North Somerset Council scrutiny committee alongside Nailsea Town Council’s Graham Parsons, urging them to rethink the parking charges. Ms Lake told councillors: “It does feel like North Somerset Council do not want small independent businesses to survive.”

Mr Parsons added: “Everyone is aware of the financial situation North Somerset Councils finds itself in. However the erosion of a town centre’s viability is not an acceptable way to help plug the gap.” A report by the town council, submitted to the committee, warned the impact on local businesses from the parking charges was a “serious economic concern.”

But North Somerset Council officers said the relationship between parking charges and the health of the high street was “more complex.” The scrutiny panel was discussing the council’s six month review of Nailsea’s parking charges.

Mike Bird, independent councillor for Nailsea Yeo on North Somerset Council(Image: Local Democracy Reporting Service)

Committee member Mike Bird, who is also the independent councillor for Nailsea Yeo on North Somerset Council, told the meeting: “The North Somerset review you have before you only really considered parking numbers and not the consequences for the local community.”

Advertisement

He pointed out that the closure of Nailsea Fruit and Veg meant the council had lost out on £23k a year in business rates. He warned: “Quickly the losses of business rates could outstrip the so-called profits of these parking charges.”

Since the introduction of parking charges, Station Road Car Park has only been about half full. It is now proposed to trial a reduction in price of the one hour ticket from £1 to 50p from June 2026 “to strike an appropriate balance between local calls for low-cost or free short-stay parking to support the high-street and the need to ensure that car parks remain financially self-sustaining.”

Nailsea Fruit and Veg has closed(Image: Local Democracy Reporting Service)

But Mr Bird warned that this could do more harm than good if people were encouraged to stay for an hour instead of two. He said: “We need to be encouraging people to stay longer in the town, not shorter.”

He called for the parking charges for one and two hour stays to be abolished and a cheaper three hour ticket introduced. But the proposal faced opposition from some other councillors on the scrutiny committee in a tense hour-long debate which was defined more by geographical lines than party affiliation.

Advertisement

Several councillors representing areas of Weston-super-Mare, which has had parking charges for years, rejected the idea that other towns in North Somerset should be spared them. Decisions on parking charges are up to the council administration, with the scrutiny panel having an advisory role.

Ms Lake told the Local Democracy Reporting Service that she did not think dropping the hour charge to 50p would help. She said: “They need to look at doing something that will entice people to stay to have a meal and to be able to then go and shop in other local shops.”

She said: “It’s Nailsea. It’s not a destination place. It’s not a place where you come and spend a day. So anything that helps people come to Nailsea and spend in the local community is going to help massively.”

To find all the planning applications, traffic diversions, road layout changes, alcohol licence applications and more in your community, visit the Public Notices Portal.

This is the forum for daily political discussion on Seeking Alpha. A new version is published every market day.

Please don’t leave political comments on other articles or posts on the site.

The comments below are not regulated with the same rigor as the rest of the site, and this is an ‘enter at your own risk’ area as discussion can get very heated. If you can’t stand the heat… you know what they say…

More on Today’s Markets:

Advertisement

Moderation Guidelines:

We remove comments under the following categories:

Personal attacks on another user account

Anti-Vaxxer or covid related misinformation

Stereotyping, prejudiced or racist language about individuals or the topic under discussion.

Inciting violence messages, encouraging hate groups and political violence.

Regardless of which side of the political divide you find yourself, please be courteous and don’t direct abuse at other users.

For any issue with regards to comments please email us at : moderation@seekingalpha.com.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Mumbai: Securities and Exchange Board of India (Sebi) chairman Tuhin Kanta Pandey on Monday urged investors to remain calm amid global market turbulence, saying India’s strong domestic fundamentals should help markets navigate the current volatility.

“It is important not to panic at this moment, but to remain calm amidst this storm,” he said at a National Stock Exchange of India (NSE) event on Monday.

Pandey said the sectoral composition on the Nifty has changed over the years, with financial services and Information Technology dominating the index currently.

Separately, NSE chief executive Ashish Kumar Chauhan said the exchange plans to appoint investment bankers this month for its initial public offering.

Live Events

The regulator has allowed the exchange to proceed with a smaller public float as there is no identifiable promoter, said Chauhan on the sidelines of the event.