Business

Should Investors Centralize Indonesia Operations Within a Holding Company?

Consolidation with a holding company enhances control, tax planning, and efficiency, but sector restrictions and dividend taxes influence foreign ownership limits and repatriation strategies in Indonesia.

Capital Requirements for Consolidation

Consolidation becomes essential when expansion increases a company’s exposure across multiple entities. In Indonesia, a PT PMA typically requires a minimum investment of IDR 10 billion (US$637,000) per business classification. Establishing three subsidiaries in different sectors would demand at least IDR 30 billion (US$1.91 million) in committed capital before operational expenses are considered. This substantial funding highlights the need for careful planning in capital allocation and investment management to support growth and diversification efforts.

Impact of Holding Companies on Tax and Profit Management

Introducing a holding company alters the landscape of equity distribution and profit accumulation. The holding can be either Indonesian or offshore, influencing tax residency, treaty benefits, and dividend routing. The optimal choice depends on the investor’s long-term capital strategy, especially regarding cross-border profit repatriation. Jurisdiction selection is critical, as it directly affects net returns, with tax treaties playing a vital role in reducing withholding taxes on dividends.

Ownership, Control, and Sector Regulations

Ownership placement significantly impacts tax obligations and control rights. Indonesia’s Positive Investment List restricts foreign ownership in specific sectors, meaning a holding company cannot bypass sector-specific limits. Additionally, dividends paid abroad typically face a 20% withholding tax unless reduced by tax treaties. Planning for dividend flows exceeding this threshold makes treaty positioning and jurisdiction choice economically crucial to optimize after-tax returns.

Read the original article : Should Investors Consolidate Indonesia Operations Under a Holding Company?

Other People are Reading

Business

Australia Fuel Prices Ease Slightly After Excise Cut But Iran War Keeps Oil Costs High In AUD

SYDNEY — Australian motorists are seeing modest relief at the petrol pump this Easter long weekend after the federal government’s temporary halving of fuel excise took effect on April 1, yet global oil prices driven by the ongoing U.S.-led conflict with Iran continue to exert upward pressure on costs measured in Australian dollars.

engin akyurt / Unsplash

The government slashed the fuel excise from 52.6 cents to 26.3 cents per litre for petrol and diesel for three months until June 30, delivering an expected saving of about 26.3 cents per litre when fully passed on. Motoring groups reported early price drops across capital cities in the first days of April, with some locations seeing reductions of up to 25 cents per litre for regular unleaded.

In Adelaide, the average price for regular unleaded fell sharply from nearly $2.60 to around $2.34 per litre in early April, according to NRMA data. Melbourne recorded a 16.3-cent drop to about $2.43, while Sydney saw a 12.7-cent decline to roughly $2.44. National averages for regular unleaded had climbed above $2.30 to $2.38 per litre in late March before the cut, with diesel pushing toward or past $3.00 in many areas.

Prime Minister Anthony Albanese announced the measure on March 30 as international benchmark Brent crude surged above $116 per barrel amid disruptions to roughly 20 per cent of global oil supply through the Strait of Hormuz. The tax relief, combined with the suspension of heavy vehicle road user charges, aims to ease cost-of-living pressures on households and businesses hit by the energy shock.

Despite the excise cut, experts warn that the real crunch for Australia’s fuel supply may still arrive in mid-to-late April. Australia imports more than 90 per cent of its refined petroleum products, primarily from Asia, and supply chains have been disrupted by export caps in South Korea, reduced refinery runs and rerouting of cargoes. Some analysts predict potential restrictions or shortages by around April 20 if the conflict persists, as voyage times lengthen and alternative supplies from the U.S. and Europe take time to arrive.

Brent crude, the global oil benchmark, traded around $109 per barrel on April 2 after volatile swings, reflecting a sharp monthly rise but some pullback from recent peaks near $116. With the Australian dollar hovering near 0.69 to 0.691 U.S. dollars in early April, the effective cost of imported oil in AUD remains elevated compared with pre-conflict levels.

The conflict, now in its fifth week, has caused Brent prices to surge dramatically since late February, with some periods showing monthly gains exceeding 30 per cent. Australia’s heavy reliance on imported refined fuels — rather than domestic crude production, which has declined significantly — amplifies the impact. Domestic oil output stands at low levels, with only two operating refineries contributing a small share of national needs.

Retail fuel prices in Australia rose about 40 per cent in the month following the start of strikes on Iran, according to various reports. Diesel prices climbed faster than petrol in many cases, surpassing $3 per litre in several capital cities and adding significant costs for transport, agriculture and construction. Farmers and logistics operators have reported surcharges and supply concerns, with flow-on effects to food prices and broader inflation.

The government has taken additional steps to secure supply, including underwriting spot cargoes, relaxing fuel quality standards to allow more production flexibility and sourcing alternative shipments. Energy Minister Chris Bowen has indicated that deliveries are assured into mid-April, but longer-term stability depends on developments in the Middle East and diplomatic efforts to reopen the Strait of Hormuz.

Motorists are advised to shop around using apps such as FuelCheck or PetrolSpy, as prices can vary by 20 to 40 cents per litre within the same city. Many service stations passed on portions of the excise cut quickly, even before depleting higher-cost stock, but full transmission may take weeks in some regional areas.

Economists note that sustained high oil prices could influence Reserve Bank of Australia decisions. The RBA raised the cash rate in March amid inflation concerns, and further energy-driven pressure may complicate the path back to target. The Australian dollar has shown some resilience but weakened slightly against the greenback in recent sessions as global risk sentiment fluctuated.

For households, the excise cut provides temporary breathing room. Filling a typical 60-litre tank could save around $15 to $16 at current rates, though this benefit may erode if international crude prices climb again or if supply disruptions lead to rationing or higher margins at the pump.

Businesses, particularly in freight and agriculture, face steeper challenges. Diesel, critical for heavy vehicles and machinery, has seen sharper increases, with some operators reporting costs up by $1 per litre or more since February. Construction firms have added fuel surcharges of 8 to 10 per cent in some cases.

Longer-term, the crisis has renewed debate about Australia’s fuel security. Critics point to the closure of most domestic refineries over the past 15 years, leaving the country vulnerable to global shocks. Calls have grown for investment in refining capacity or strategic reserves, though the government maintains that current measures and diversified sourcing provide adequate buffers for now.

As the Easter long weekend begins, with many Australians travelling, fuel availability appears stable but prices remain well above 2025 averages. Public transport usage and fuel-efficient driving tips are being promoted to help manage costs.

Looking ahead, any de-escalation in the Middle East or successful reopening of key shipping routes could ease pressure on oil markets and flow through to lower AUD-denominated prices. Conversely, prolonged disruption risks further spikes, testing the three-month excise relief and broader economic resilience.

The Australian Institute of Petroleum and motoring organisations continue to monitor weekly trends. Consumers should check local prices daily, as volatility persists. For businesses reliant on fuel, hedging or forward contracting where possible may offer some protection.

In summary, while the government’s excise cut has delivered noticeable short-term relief at Australian service stations, the underlying driver of high oil costs — geopolitical tensions affecting global supply — keeps the situation fluid. Australians are paying more in AUD for fuel than they were before the conflict, but the full extent of April’s potential supply challenges remains to be seen.

The coming weeks will be critical as supply chains adjust and markets watch for any breakthrough in Middle East diplomacy. For now, the combination of policy relief and cautious optimism about alternative sourcing is helping to stabilise the domestic fuel situation amid an unpredictable global energy landscape.

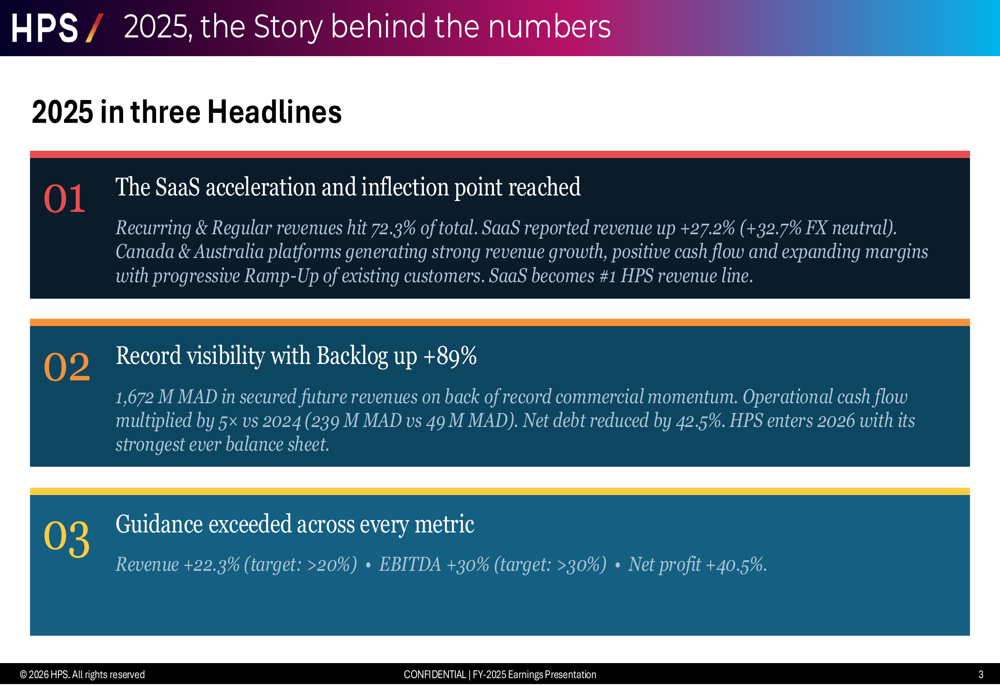

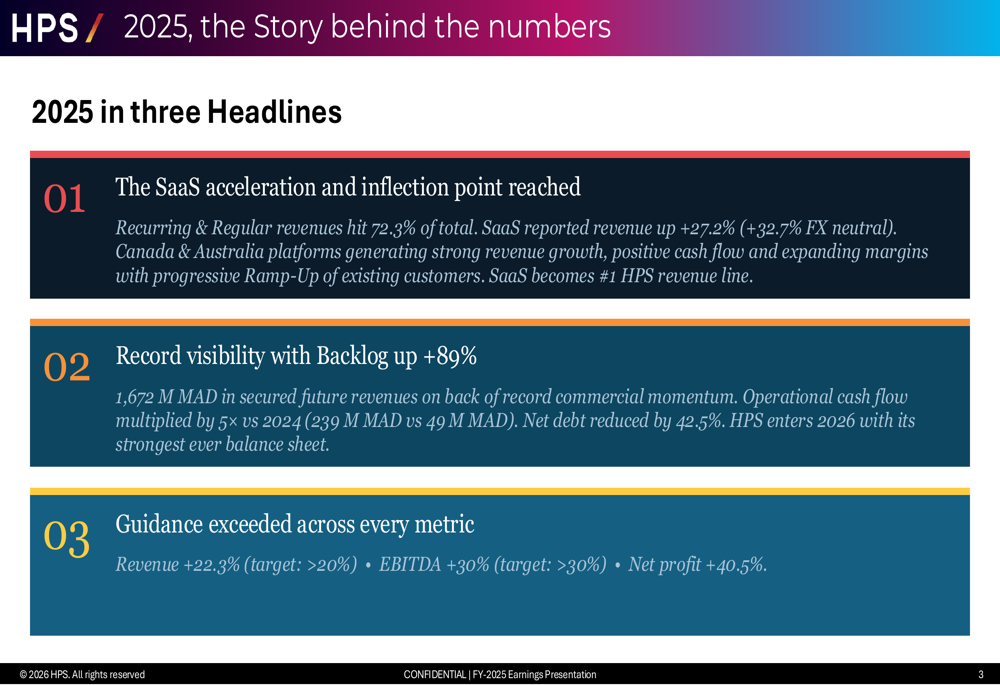

HPS FY 2025 slides: SaaS inflection drives 22% revenue growth

Japan stocks higher at close of trade; Nikkei 225 up 1.21%

The latest penalties follow a series of accountability actions the bank has taken in connection with the AT1 bond controversy. As ET reported on March 21, HDFC Bank had sacked three senior executives — including group head of branch banking Sampath Kumar — along with two others, Harsh Gupta and Payal Mandhyan, following internal findings.

Gupta, executive vice president for the Middle East, Africa and NRI onshore business, and Mandhyan had been suspended in January 2025 after the bank initiated an internal probe into alleged mis-selling of debt products at its Dubai branch. Investigations showed that several AT1 bond investors had alleged they were encouraged to move their foreign currency non-resident (FCNR) deposits from India to Bahrain. The controversy goes back to March 2023, when Swiss authorities wrote down Credit Suisse’s AT1 bonds to zero as part of its emergency takeover by UBS, wiping out investors who held these quasi-equity instruments. AT1 bonds have been written off during bank bailouts in multiple geographies, including India.

Despite the personnel actions, HDFC Bank managing director and CEO Sashidhar Jagdishan has maintained that no fraud was committed.

“In June 2023, the Dubai Financial Services Authority clarified that clients who are continuously engaged in Dubai must also be onboarded there, even if accounts are booked in Bahrain,” Jagdishan told ET on March 23. “Our assessment is that this was a technical lapse in documentation and regulatory interpretation — not fraud or mis-selling. We initiated an internal review and took staff accountability actions through our disciplinary and board-level committees, with a right to appeal. There is no fraud, no misappropriation, and no integrity issue that has surfaced so far.”

HDFC Bank Penalises 12 Execs

“Appropriate remedial actions have been taken in line with internal policies. Personnel changes have been undertaken along with appropriate action as per the bank’s conduct regulation,” it said on March 21.

The regulatory fallout had already become public in September 2025, when HDFC Bank disclosed that the Dubai Financial Services Authority had barred its DIFC branch from onboarding new clients or undertaking fresh business. The prohibition followed non-compliance with regulatory requirements related to servicing clients not onboarded through the DIFC entity, as well as lapses in advisory and credit arrangement practices.The branch remains prohibited from soliciting or conducting business with new clients across financial services including advising on financial products, arranging investment deals, extending or advising on credit, and custody-related activities.

SAN ANTONIO — Victor Wembanyama dropped 41 points and grabbed 18 rebounds in just 29 minutes Wednesday night, leading the surging San Antonio Spurs to a 127-113 victory over the Golden State Warriors and their 10th straight win. It was the second consecutive 40-point, 15-rebound game for the 22-year-old phenom, prompting a familiar question across the league: Is Victor Wembanyama unstoppable now?

The 7-foot-4 Frenchman has elevated his game to historic levels in the 2025-26 season, posting averages of 24.7 points, 11.5 rebounds, 3.1 assists and a league-leading 3.1 blocks per game while shooting 50.9% from the field. His defensive impact remains otherworldly, altering shots from the perimeter to the rim in ways few players in NBA history have matched. Offensively, Wembanyama has added strength, improved footwork and expanded range, turning potential weaknesses into matchup nightmares.

Wembanyama’s recent tear has fueled MVP chatter. He has scored 30 or more points in six of his last 14 games, averaging nearly 29 points, 12.6 rebounds and 3.5 blocks in that span on 53% shooting. Against the Warriors, he went 16-for-22 from the field, showcasing mid-range pull-ups, step-back threes and thunderous dunks that left defenders helpless. The Spurs improved to 58-18 with the win, sitting just two games behind the Oklahoma City Thunder for the top seed in the Western Conference.

Spurs coach Mitch Johnson praised his young star’s growth while cautioning that the journey continues. “He’s doing things we’ve never seen before at his size,” Johnson said postgame. “But Victor is the first to tell you there’s always another level. He studies film, lifts weights and works on his body like a veteran.”

The transformation from a skinny rookie to a dominant two-way force has been remarkable. In his third season, Wembanyama has bulked up while maintaining incredible mobility. His block rate leads the NBA, and opponents shoot significantly worse when he is on the floor. Advanced metrics show the Spurs are roughly 16 points per 100 possessions better with Wembanyama in the game, a massive net-rating swing driven largely by elite defense.

Legends and analysts have taken notice. Former players and coaches describe Wembanyama’s combination of length, skill and basketball IQ as unprecedented. Indiana Pacers coach Rick Carlisle called him a player with “no comparison in the history of the game” for his two-way impact. NBA analyst Brian Scalabrine went further, saying Wembanyama is “on the precipice of breaking the NBA” and compares his influence to Stephen Curry’s revolution with the three-point shot.

Yet Wembanyama remains grounded. After his latest dominant performance, he told ESPN he is squarely chasing the MVP award but emphasized team success above individual honors. The Spurs have gone 26-2 in their last 28 games, a stunning turnaround that has them as legitimate title contenders heading into the playoffs. Wembanyama’s presence has energized the young roster, including emerging talents like Stephon Castle and others benefiting from his gravity on both ends.

Defensively, no one has solved the Wembanyama riddle consistently. Guards and wings struggle to finish over his outstretched arms, while bigger centers get blocked or forced into tough shots. His help defense rotates seamlessly, and his ability to switch onto smaller players adds versatility rarely seen in traditional big men. Some call him the frontrunner for Defensive Player of the Year, with his rim protection anchoring one of the league’s top defenses.

Offensively, progress has been equally impressive. Wembanyama has improved his pick-and-roll efficiency, developed a reliable step-back jumper and become a more willing passer out of double teams. He knocks down 1.9 threes per game at 35%, stretching the floor in ways that open driving lanes for teammates. Free-throw shooting has climbed to 82.3%, reducing a former vulnerability.

Still, questions linger about whether he is truly unstoppable. Some analysts point to occasional lapses in physicality against veteran bruisers or the need for finer details in high-pick-and-roll situations. A minor right ankle issue led to him being ruled out for Thursday’s game against the Los Angeles Clippers, a precautionary move after heavy recent minutes. Durability remains a watchpoint for a player of his frame logging big minutes in a physical league.

Wembanyama has missed only a handful of games this season, a positive sign after early injury concerns in his career. The Spurs have managed his workload carefully, often keeping him around 29-30 minutes per night while prioritizing recovery. His conditioning regimen, inspired by LeBron James-level discipline, has drawn praise from veterans who see him as a potential all-time great.

The broader impact extends beyond stats. Wembanyama has injected competitiveness and excitement into a league sometimes criticized for predictability. His relentless motor and joy for the game have lifted the Spurs from lottery hopefuls to contenders in record time. San Antonio’s offense ranks among the league’s best, averaging nearly 120 points per game, while their defense has tightened significantly with Wembanyama patrolling the paint.

Opponents openly acknowledge the challenge. Warriors coach Steve Kerr, after watching Wembanyama torch his shorthanded team, called the performance “special” and noted the difficulty in game-planning against such unique size and skill. Across the league, coaches experiment with zone defenses, double teams and switching schemes, yet Wembanyama continues to produce at an elite clip.

MVP frontrunners include Wembanyama, Shai Gilgeous-Alexander of the Thunder and others, but many insiders give the edge to the Spurs star for his two-way dominance and team elevation. Recent polls and expert commentary increasingly frame him as the league’s most valuable and impactful player, even if traditional scoring leaders edge him in raw points.

At just 22, Wembanyama’s ceiling appears limitless. He studies greats like Tim Duncan, Kobe Bryant and Kevin Durant, blending their traits into a singular package. His work ethic off the court matches his production on it, with reports of late-night film sessions and rigorous training.

The Spurs’ surprising ascent has rewritten expectations. After years of rebuilding, the franchise sits second in the West with home-court advantage potentially within reach. Wembanyama’s leadership by example has been key, as he mentors younger players and sets a culture of accountability and competitiveness.

As the regular season winds down, attention turns to the playoffs, where Wembanyama will face heightened physicality and scrutiny. Can he maintain this level against elite defenses? Will fatigue or minor injuries derail the momentum? For now, the answer seems to be that stopping him requires near-perfect execution from multiple defenders over extended stretches — a tall order even for the NBA’s best.

Wembanyama himself downplays the “unstoppable” label. “I’m just trying to help my team win,” he said recently. “There are always adjustments to make, always things to improve.”

Those improvements may come in subtle areas, such as finer decision-making in certain sets or sustaining energy through deeper playoff runs. Yet the foundation is already elite: size, skill, smarts and an insatiable drive.

NBA legends have weighed in on podcasts and interviews, predicting Wembanyama could cruise to top-10 all-time status with continued health and development. Some go further, suggesting he has the tools to redefine the center position much like Curry redefined the guard spot.

For Spurs fans and basketball purists, watching Wembanyama evolve has been a treat. From his rookie flashes to this season’s sustained excellence, the progression feels generational. His ability to dominate without forcing shots, protect the rim without fouling excessively and contribute as a connector makes him a coach’s dream.

As April unfolds and playoff seeding solidifies, the narrative around Wembanyama will only intensify. Is he the clear MVP? The best player in the world? Unstoppable? The answers may vary by metric or matchup, but one truth stands out: the NBA has rarely seen a talent quite like this, and at 22, he is only getting started.

The Spurs host more games in the coming days, with Wembanyama expected back soon after ankle management. His absence, however brief, underscores how central he has become to San Antonio’s success. When he returns, expect more highlight-reel plays and winning basketball.

Whether Victor Wembanyama is fully unstoppable remains a debate for analysts and fans. What is undeniable is his rapid ascent into the conversation for the game’s elite. In a league filled with stars, the alien from France continues to rewrite what is possible at his position and age.

NEW YORK — Bitcoin fell modestly Friday morning amid lingering uncertainty from the ongoing U.S.-led military campaign against Iran, with the world’s largest cryptocurrency trading near $66,650 after shedding about 0.36% in early Asian and European hours.

At approximately 6:29 a.m. UTC on April 3, 2026, Bitcoin was priced at $66,647.02, down $241.46 from the previous close, according to major exchanges. The move extended a volatile stretch for the digital asset, which has swung between roughly $65,000 and $69,000 over the past week as investors weighed risks from the five-week-old conflict in the Middle East.

The decline came as President Donald Trump signaled that U.S. strikes could intensify in the coming weeks if Iran does not reopen the Strait of Hormuz, a critical waterway for global oil shipments. Higher energy prices and broader risk-off sentiment have pressured Bitcoin and other cryptocurrencies, which often behave like high-beta growth assets during periods of geopolitical stress.

“Bitcoin is still feeling the heat from macro headlines,” said one analyst at a major crypto trading firm who spoke on condition of anonymity. “Any escalation in the Iran situation tends to drive safe-haven flows into traditional assets like gold or the dollar, leaving risk assets like BTC under pressure.”

Bitcoin’s market capitalization stood near $1.33 trillion, with 24-hour trading volume hovering around $35 billion to $40 billion across major platforms. The cryptocurrency has posted a roughly 2% loss over the past 24 hours and remains down more than 20% year-to-date after a bruising first quarter that saw it drop from highs near $97,000 earlier in 2026.

Broader cryptocurrency markets mirrored Bitcoin’s softness. Ethereum traded down about 1%, while Solana and other major altcoins posted similar modest losses. Total crypto market capitalization sat around $2.3 trillion, with Bitcoin’s dominance holding steady near 58%.

Options activity added to the cautious tone. A large whale reportedly accumulated more than 2,000 Bitcoin put contracts targeting a drop below $66,000 ahead of a significant $2.15 billion options expiry on Deribit on April 3. The max pain level for the expiry sat near $68,000, leaving spot Bitcoin trading below that threshold and potentially benefiting put holders if prices failed to recover.

Despite the short-term dip, some analysts pointed to underlying resilience. Bitcoin has repeatedly defended the $65,000 to $66,000 zone in recent weeks, a level many view as critical psychological and technical support. ETF inflows have remained relatively steady, though not at the explosive pace seen in previous bull cycles, and institutional interest continues to build through spot Bitcoin and Ethereum exchange-traded funds.

“The narrative around Bitcoin as a long-term store of value hasn’t changed,” said another market observer. “But in the near term, it’s caught in the crossfire of oil spikes, Fed policy uncertainty and war headlines.”

U.S. economic data scheduled for release later Friday, including the March jobs report, could provide fresh direction. Analysts expect the report to influence Federal Reserve rate-cut expectations, which in turn affect liquidity and risk appetite across markets. Stronger-than-expected job numbers might push back anticipated cuts, weighing further on Bitcoin, while a softer print could spark a relief rally.

Bitcoin’s performance in April has historically been mixed, but many traders entered the month hoping for a rebound after a difficult Q1. Early April trading has instead been characterized by range-bound action between roughly $65,000 and $69,000, with geopolitical developments overriding seasonal patterns.

On-chain metrics showed mixed signals. Long-term holders have continued to accumulate during dips, while exchange reserves have remained relatively stable. Network hashrate experienced some pressure earlier in the quarter due to elevated energy costs affecting miners, but it has stabilized in recent days.

Regulatory and adoption developments provided a counterbalance to the macro gloom. Several countries and institutions have continued exploring Bitcoin as a reserve asset or payment rail, and corporate treasuries have maintained steady buying in the background. Spot Bitcoin ETFs in the United States have seen net inflows in most sessions, though volumes have moderated compared with 2024-2025 peaks.

Looking ahead, many market participants are watching for any signs of de-escalation in the Middle East. Diplomatic efforts involving multiple nations are underway, and a quicker resolution could remove a major overhang for risk assets. Conversely, prolonged disruption to oil supplies could keep upward pressure on inflation and energy costs, complicating the Federal Reserve’s path and keeping Bitcoin in a defensive posture.

Technical analysts noted key levels to watch in the coming days. Support sits near $65,500 to $66,000, with a decisive break lower potentially opening the door to $63,000 or even $60,000 in a worst-case scenario. On the upside, reclaiming $68,000 would improve sentiment and could target $70,000, a level Bitcoin has struggled to hold consistently in 2026.

“April often sets the tone for the rest of the year in crypto,” one veteran trader noted. “If Bitcoin can stabilize here and push back toward the upper end of the range, it could rebuild confidence. But another leg down on bad war or macro news would test the resolve of even the strongest hands.”

Ethereum, the second-largest cryptocurrency, faced similar headwinds but showed slightly better relative performance in some sessions due to ongoing developments in layer-2 scaling and decentralized finance. Solana and other high-throughput chains continued to compete for developer mindshare and user activity.

For retail investors, the current environment underscores the importance of risk management. Volatility remains elevated, with daily swings of 2% to 4% commonplace. Dollar-cost averaging and holding through cycles have historically rewarded patient Bitcoin investors, though short-term traders face choppy conditions.

As trading continued into the U.S. session, all eyes remained on geopolitical updates from the Middle East and the upcoming U.S. employment data. Bitcoin’s ability to hold above $66,000 could signal that the market is absorbing the latest news without panic, while a break lower might invite more aggressive selling.

The cryptocurrency’s long-term thesis — as a hedge against fiat debasement and a decentralized store of value — continues to attract proponents even amid short-term noise. With institutional infrastructure now more mature than in previous cycles, many believe Bitcoin is better positioned to weather storms than in years past.

For now, however, the market remains on edge. The modest decline observed early Friday reflects a broader risk-off mood driven by uncertainty over the duration and intensity of U.S. operations against Iran. Traders will monitor developments closely over the Easter weekend, with limited traditional market liquidity potentially amplifying moves in crypto.

Bitcoin’s journey in 2026 has been one of sharp contrasts — from early-year highs near $97,000 to the current consolidation phase. Whether the digital asset can regain momentum will depend on macro stabilization and any positive shifts in the geopolitical landscape.

As of early Friday, the crypto market appeared to be taking a cautious breath, digesting the latest headlines while awaiting clearer signals on both war developments and U.S. economic health.

Earnings call transcript: HPS Q4 2025 highlights SaaS growth, stock dips

Business

Extreme poverty in the Asia-Pacific region has declined but inequality remains high, says OECD

Extreme poverty across the Asia-Pacific region has fallen dramatically over the past two decades, according to the OECD, with the share of people living on less than PPP 2.15 a day dropping from more than 21% in 2000 to about 2.6% in 2022 on average across the region.

Key takeaways

- Extreme poverty in the Asia-Pacific dropped from over 21% in 2000 to about 2.6% in 2022.

- India and Timor-Leste still had the highest extreme poverty rates, with more than 10% of people living below PPP 2.15 a day.

- Income inequality declined over the past decade but remained slightly above the OECD average in 2021.

The report says much of that decline was driven by major gains in China, Indonesia, Kyrgyzstan, and Tajikistan, where poverty rates fell by 30 percentage points or more. Still, the OECD said extreme poverty remains highest in India and Timor-Leste, where more than 10% of the population continues to live below the PPP 2.15-a-day threshold.

Among low- and middle-income economies, poverty levels were lowest in Bhutan, China, the Maldives, Malaysia, Mongolia, Thailand, and Tonga, where less than 0.5% of the population was living in extreme poverty.

Growth has reduced poverty, but inequality remains a challenge

The OECD said poverty generally declined faster in countries that posted stronger real GDP growth, with China recording the fastest pace of both economic growth and poverty reduction between 2000 and 2022. However, the report noted that in Armenia, Bangladesh, Georgia, India, and Lao PDR, poverty did not fall as much as expected relative to economic growth.

Income inequality in the Asia-Pacific region remained slightly higher than the OECD average in 2021, even though it has eased over the past decade.

The regional Gini coefficient declined from 0.35 in 2010 to 0.33 in 2021, compared with an OECD average of 0.32 in 2021.

Malaysia and the Philippines recorded the widest income gaps, with Gini coefficients above 0.40, while Tonga and Armenia posted the lowest levels at 0.28. Over the past 10 years, inequality declined in countries including China, Fiji, Georgia, and the Maldives, but increased in Lao PDR, Sri Lanka, and Tajikistan.

The findings point to significant social progress across the region, but also suggest that economic growth alone has not delivered equal gains everywhere, leaving persistent disparities in both poverty reduction and income distribution.

Other People are Reading

Bankers said the gap widened steeply in the longer end as overseas investors and hedge funds were not big sellers of the US currency in the long end. The difference between one-month domestic forward and overseas NDF increased to about 50 paise from about 40 paise on Monday, but was higher at about 180 paise versus 130 paise in the sixmonth basket, currency dealers said. “Banks have all reversed their positions after RBI’s directions yesterday.

RBI clearly does not want banks to be active in this market. Banks and companies are now selling dollars domestically and buying in overseas NDF which is the opposite of what they were doing last month,” said a senior bank treasury official, who did not wish to be identified.

Forwards-NDF Spread

In a late evening notification on Wednesday, the central bank said banks cannot offer NDF contracts involving rupee to resident or non-resident users. Banks and other authorised dealers have also not been permitted to book again any foreign exchange derivatives contract, whether deliverable or non-deliverable, which was cancelled with immediate effect.

No exchange of the underlying currencies happens in NDF contracts, as the parties only settle the difference between the agreed and market rates. The rupee reacted instantly to RBI’s latest action, closing at 93.10 against the dollar, up from the previous close of 94.83, recording the biggest single-day gain since September 2013.

The latest move was a second blow to banks within a week after RBI on March 27 asked banks to cap their net open rupee positions in the onshore deliverable market to $100 million at the end of each business day with effect from April 10, far lower than the current limit of 25% of total capital. The latest change makes it more difficult for banks to pre-vent losses as they cannot even sell their contracts to clients.

“RBI has effectively made the NDF market untouchable for local banks and companies, first by limiting open position limits and then banning new NDF contracts for clients, too. That market will now be dominated by foreigners,” said another treasury official.

RBI first opened the NDF market to Indian banks in June 2020, and to resident Indians three years later, giving them an avenue to hedge their domestic currency positions.However, the central bank has also previously informally curbed trading in that market, particularly when the rupee was weak. But now, with official communication against trade in the market, banks will forever be wary of trading in the derivative instrument, bankers said. The central bank’s moves are aimed at curbing speculative currency trading at a time the West Asia crisis has pushed the rupee to an all-time low against the dollar.

LIXIL Corporation (JSGRY) Analyst/Investor Day – Slideshow

Bogota 2026 Day 5: Women’s predictions ft. Varvara Lepchenko vs Emiliana Arango, Marie Bouzkova vs Darja Semenistaja

99% Don’t See What’s Coming For Bitcoin

Rory McIlroy hopes to emulate greats as he aims to make more history

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat13 hours ago

NewsBeat13 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World1 day ago

Crypto World1 day agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Business7 hours ago

Business7 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Business1 day ago

Business1 day agoLogin and Checkout Issues Spark Merchant Frustration

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion7 days ago

Fashion7 days agoWeekly News Update, 3.27.26 – Corporette.com

You must be logged in to post a comment Login