Business

Strengthening ASEAN Currency Resilience: Towards Financial Independence

ASEAN currencies demonstrate resilience through economic fundamentals and integration efforts. Initiatives like local currency frameworks and fintech development reduce reliance on the US dollar, enhancing regional stability and investment opportunities.

ASEAN currencies have shown significant resilience to global economic shocks driven by robust domestic economic fundamentals, effective policy buffers, growth in FDI and investments and global developments, such as geopolitical uncertainties, trade tensions and financial crises.

Key Points

- Resilience of ASEAN currencies

- Strong domestic fundamentals, prudent monetary policies, and large foreign reserves have helped withstand global shocks.

- Growth in exports (US$1.9 trillion in 2024) and FDI (US$234 billion in 2023) supports stability.

- Geopolitical pressures and USD reliance

- Sanctions on Russia and global trade tensions highlight vulnerabilities of USD dependence.

- ASEAN nations are diversifying reserves and promoting intra-regional trade to reduce reliance on the dollar.

Mounting geopolitical uncertainties and trade tensions, exacerbated by sanctions against Russia, have challenged the US dollar’s dominance driving a need for ASEAN countries to deepen integration, diversify currency reserves, and promote intra-regional trade to build resilience against future crises and reduce reliance on external currencies, the US dollar in particular.

At present, the ASEAN nations are developing an independent and more resilient regional financial system through integration and cooperation initiatives such as Regional Payment Connectivity, integrated QR payments, financial safety nets, Digital Economy Framework and Central Bank Digital currencies that aim to strengthen the payment connectivity among these nations while withstanding external shocks and future crises.

The development of fintech and digital banking in ASEAN has brought in stability to the banking system in the region offering broader currency and economic stability. The evolving fintech and digital banking landscape in the region is offering significant investment opportunities for investors in digital payments and lending, neobanking, embedded finance, investment technology and infrastructure.

ASEAN’s Emergence as a Global Powerhouse Supports Financial Resilience

The ASEAN region, with a total population of 682.7 million and a combined GDP of US$3.8 trillion ranks as the fifth-largest economy in the world. The region has evolved into a rapidly growing hub maintaining strong economic resilience driven by robust household consumption, steady increase in foreign direct investment (FDI), economic diversification and access to developed export markets.

Regional integration initiatives

- Local Currency Settlement frameworks (Indonesia, Malaysia, Thailand) encourage trade in local currencies.

- Regional Payment Connectivity (RPC) and interoperable QR payments lower transaction costs and improve cross-border efficiency.

- Chiang Mai Initiative (US$240 billion swap arrangement) provides financial safety nets.

The manufacturing sector continues to play a crucial role as the key driver of economic growth in the region. Manufactured goods such as electronics, automobiles and parts, textile & garments and agricultural products (such as palm oil, rice and rubber) dominate the exports in the ASEAN region.

In 2024, region’s exports reached US$1.9 trillion (7.7% of global exports) growing from US$1.1 trillion in 2016. Over the past decade, ASEAN’s exports to the US alone have increased roughly from 10% to 17%, highlighting the increased role of ASEAN in international trade.

During the last decade, ASEAN also has demonstrated strong performance in services trade, whereas service exports expanded by 8.0% in 2023 to US$554.2 billion.

During this period, intra-ASEAN trade also experienced significant growth with the removal of tariff on most products across the region (through ATIGA) which has helped build an integrated and stable regional market. In 2023, intra-ASEAN trade exports contributed to 22.1% of total ASEAN exports, growing at an average annual growth rate of 7.3% between 2003-2023.

Intra-ASEAN services trade also has experienced sustained growth over the years accounting for 14% of ASEAN’s total trade in services in 2023 (vs 12.6% in 2022). This strong growth in intra-ASEAN services trade further emphasizes the interdependence among ASEAN nations and strong regional integration.

Having a strong export sector and deep intra-regional integration have helped these nations generate significant foreign exchange earnings that have helped currency resilience through building large foreign exchange reserves.

Exports and foreign investments have been key drivers of economic growth in the region and have helped reduce the need for external borrowings in foreign currency. This has paved the way for the development of strong local currency bond markets which has helped build further resilience by reducing dependence on foreign funding.

Prudent monetary policies (such as interest rate and foreign reserve management) aimed at inflation targeting also has offered currency stability in the region. The inflation across most countries in the region has moderated and remains largely within the target.

Source: Source: Board of Governors of the Federal Reserve System (US)

Central banks in countries such as Indonesia and Vietnam have set higher local interest rates which has helped attract foreign investments due to higher yields, driving local currency appreciation.

The inward foreign direct investment flows into ASEAN have shown steady growth over the years (from US$119 billion in 2015 to US$234 billion in 2023) despite seeing a temporary decline in 2020 due to the COVID-19 outbreak. This growth has been driven by a large consumer market, strong economic fundamentals, diversification of supply chains and favorable government policies.

Geopolitical Uncertainties Create a Need for Building Resilience

The US Dollar has been dominating the global trade for decades, and ASEAN has been no exception. The ASEAN nations rely heavily on the US dollar (USD) as the primary currency for trade with the US and other nations including for intra-regional transactions. However, mounting geopolitical uncertainties and trade tension have challenged the USD’s dominance during the past few years, and the economic sanctions levied against Russia in response to its invasion of Ukraine further exacerbated this situation.

This resulted in a need for the countries in ASEAN to further deepen their integration and cooperation to diversify reserves and promote intra-regional trade. Moreover, this created a desire for ASEAN nations to bolster their resilience to weather future crises by reducing their dependence on external currencies.

ASEAN currencies are now less tied to the USD than before, and during the past decade, the exchange rate/USD (weighted average currency index) has shown less volatility compared to other emerging economies.

De-Dollarization in ASEAN: A Collective Effort

Local Currency Settlement Frameworks (LCS): The member states in ASEAN are implementing bilateral and multilateral LCS frameworks to promote the use of local currencies for intra-regional trade and investment. The goal is to reduce exposure to external currency volatility while enhancing efficiency for businesses in the region. At present, operational frameworks exist between Indonesia, Malaysia and Thailand, and as a result, transactions in local currencies within ASEAN have seen tremendous growth during the past five years.

Regional Payment Connectivity (RPC): In November 2022, five ASEAN member states (namely Indonesia, Malaysia, The Philippines, Singapore and Thailand) signed a MoU on cooperation on RPC which aims to strengthen bilateral and multilateral payment connectivity among the nations. This has supported faster, cheaper, transparent and more inclusive cross-border payments in the region. The initiative has now been extended to other member states including Vietnam (2023), Brunei (2024), Lao PDR (2024) and Cambodia (2025). The development of the RPC has also attracted countries outside the ASEAN.

Investment opportunities

- Rising demand for fintech, neobanks, embedded finance, and digital infrastructure.

- Strong manufacturing and services sectors continue to attract investors.

Integration of QR Payments: Having an ASEAN interoperable Quick Response (QR) payment is a key focus area of RPC that aims to encourage integration across participating central banks to standardize national payment systems through a common QR code format, ensuring seamless cross-border transactions. QR code systems of several member states including Cambodia (KHQR), Indonesia (QRIS), Lao PDR (Lao QR), Malaysia (DuitNow), The Philippines (QR Ph), Singapore (PayNow), Thailand (PromptPay), and Vietnam (VietQR) have already been connected. These initiatives are expected to lower transaction costs while mitigating foreign exchange risk. In the meantime, Japan is also reportedly exploring the integration of its QR payment system into RPC, with full implementation expected by end-2025.

Regional Financial Safety Nets: A multilateral currency swap arrangement (The Chiang Mai Initiative Multilateralisation (CMIM)) with a funding size of US$240 billion has been in place among the ASEAN+3 member countries (ASEAN, China, Japan, and South Korea) to address balance of payment and short-term liquidity crises (by enabling rapid financing facilities) in the region.

The regulators and central banks in the region have launched several policy frameworks to facilitate seamless transaction in the region.

The ASEAN Policy Framework is a regional initiative that provides the guiding principles for the implementation of interoperable, real-time payment systems across the region. These include common standards, data security (ISO:20022) and linkages between national QR systems.

The Local Currency Transaction Framework is an initiative by the central banks of Indonesia, Malaysia and Thailand to promote the use of local currencies for trade and investment thereby reducing reliance on USD. This framework was extended in 2025 to include portfolio investments to further strengthen financial cooperation in the region.

The ASEAN Digital Economy Framework Agreement (DEFA) is a comprehensive roadmap negotiated by the countries to create the world’s first comprehensive digital trade rules through harmonizing standards, digital trade, cybersecurity and digital payments. Negotiations are expected to conclude, with the agreement signed by 2026.

In addition to the above, the countries in the region are in the process of adopting international standards such as ISO:20022 messaging standard to facilitate data exchange for regulatory compliance and greater transparency.

Central Bank Digital Currencies (CBDCs) to Further Strengthen Regional Integration

ASEAN Countries are actively exploring CBDCs to further enhance financial inclusion and cross-border payments while further strengthening regional efforts to reduce US dollar reliance. While Singapore (a trial is expected in 2026) is at the forefront, Thailand, Indonesia and Malaysia have already launched pilot projects exploring both wholesale and retail applications as a means of modernizing cross-border payments. The other countries in the region including The Philippines, Cambodia and Vietnam have already initiated several measures (such as receiving training, ongoing research, etc.) related to CBDCs to enhance cross-border interoperability.

CBDCs, if made interoperable with systems of other countries, have the potential to reduce transaction costs by cutting down transaction times and facilitating deeper economic ties with other economies in the region. This offers unique advantages to countries in ASEAN by enabling direct settlement in local currencies thereby reducing US dollar dependency and stability against currency volatility.

Fintech and Digital Banking Further Boost Currency Resilience

The development of fintech and digital banking in ASEAN has further enhanced currency resilience by complementing the regional cooperation initiatives. As countries in the region attempts to interlink economies and financial systems, fintech has offered various measures to achieve the above through streamlining cross-border payments.

Digital transformation

- Fintech and digital banking enhance financial inclusion and stability.

- Central Bank Digital Currencies (CBDCs) are being piloted to strengthen cross-border payments and reduce USD dependency.

Digital banks and fintechs in the region offer services such as mobile money, digital wallets and micro-credit to population which were previously unbanked as well as to SMEs in the region promoting financial inclusion. Strong and inclusive economies are inherently more resilient to external pressures which in turn supports currency strength.

In general, fintech applications leverage big data, AI and blockchain that enable financial institutions to accurately assess risk and manage liquidity in real-time. This offers stability to the banking system and resilience to external shocks which in turn provides the foundation for broader currency and economic stability.

Investment Implications for ASEAN

As fintech firms in the region play a crucial role in developing a robust ecosystem for local currency transactions in the region, there has been strong demand for fintech, digital banks and RegTech (regulatory technology) offerings. The acceleration of digital payment platforms and cross-border payment systems such as the RPC initiative have created a fertile ground for fintech investment in ASEAN. Neobanks are rapidly growing in the region targeting its large underbanked population presenting significant opportunities for innovation and growth. At the same time, embedded finance is also transforming ASEAN’s fintech landscape offering significant opportunities in areas including payments, lending, wealth management and insurance infrastructure. In addition to diversified manufacturing and service hubs in ASEAN offering attractive investment opportunities, investors should also look at companies that stand to benefit from this evolving fintech transition (such as infrastructure and technology providers).

Conclusion

The use of local currencies in cross-border transactions in ASEAN is increasing driven by geopolitical uncertainties and trade tensions. Strengthening macroeconomic fundamentals and deepening regional financial integration and payment connectivity have promoted cross-border settlements in ASEAN, accelerating the move away from the USD. The policy makers and central banks in the region have introduced several policy frameworks to develop an independent financial system thus bringing in further resilience to ASEAN currencies.

An evolving fintech and digital banking landscape in the region have further supported this move by improving the efficiency of cross-border transactions. The investors in ASEAN are increasingly hedging their USD exposures with slowdown in the US economy driving further demand for ASEAN currencies. An attractive bond market in the region (including higher yields compared to other developed markets) also offers investors an opportunity for portfolio diversification.

Despite the cooperation among ASEAN countries and the significant progress made towards building an independent financial system in the region, diverse regulatory landscapes among countries, varied stages of digital infrastructure development and the need to harmonize data protection protocols need to be addressed to achieve an independent financial system. While US dollar’s dominance is expected to continue, ongoing collaboration among ASEAN nations have paved the way for gradual development of an independent financial ecosystem.

This article was written by Smartkarma, in collaboration with ASEAN Exchanges.

Source : Currency Resilience in ASEAN: Moving Towards an Independent Financial System

Other People are Reading

Andrew McElroy is Chief Analyst at Matrixtrade, author of the ebook ‘Fractal Market Mastery’ and producer of the ‘Daily Edge.’ The ‘Daily Edge’ is emailed before each US session and outlines actionable ideas, directional bias, and important levels in the S&P500. It also looks at ‘What’s Hot,’ on any particular day, whether it is commodities, stocks, crypto, or forex. Andrew has developed a top-down proprietary system that starts with his weekend Seeking Alpha article focusing on the higher timeframes. Fractals, Elliott Wave, and Demark exhaustion signals are all incorporated, as are macro drivers and analysis of the market narrative. It is much more than just a few lines on a chart – it is a system developed over 15 years and proven to deliver a consistent edge. An independent trader since 2009, Andrew manages a family portfolio of stocks and ETFs with his wife and fellow Seeking Alpha contributor Macrogirl.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of VOO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

I aim to provide alpha-generating investment ideas. I am an independent investor managing my family’s portfolio, primarily via a Self Managed Super Fund. My articles deliver 5-Minute Pitches focused on the core fundamental and technical drivers of the security.I have a generalist approach as I explore, analyze and invest in any sector so long there is perceived alpha potential vs the S&P500. The typical holding period ranges between a few months to multiple years.I am very much focused on adding value via alpha generation. I always start with a Performance Assessment section for each follow-up article. I publish unusually detailed analytics on my long-only, zero-leverage global equity portfolio performance on my Hunting Alphas website every month. At Hunting Alphas, you can also access the models to all the tickers I publish on.A bit about how I approach research and coverage of a stock:I build and maintain spreadsheets showing historical data on the financials, key metric disclosures, data on the guidance and surprise trends vs consensus estimates, time-series values of the valuations vs peers, data on key coincident or leading indicators of performance and other monitorables. In addition to the company’s filings, I also keep tabs on relevant industry news and reports plus other people’s coverage of the stock. In some cases, such as during times of a CEO change, I will do a deep dive on a key leader’s background and his/her past performance record.I very rarely build DCFs and project financials many years out into the future as I don’t think it adds much value. Instead, I find it more useful to assess how a company has delivered and the broad outlook on the 5 key drivers of a DCF valuation: revenues, costs and margins, cash flow conversion, capex and investments and the interest rates (which affect the discount rate/opportunity cost of capital). In some cases, especially for companies trading at very high multiples on a TTM or 1-yr fwd basis, I do a reverse DCF to make sense of the implied growth CAGR implications.Note: Hunting Alphas is related to VishValue Research on Seeking Alpha.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Germany’s Merz, Brazil’s Lula stress close European-Brazilian cooperation

Ukraine pushes for Europe to build defense system against ballistic weapons

BNY Mellon Appreciation Fund Q1 2026 Commentary

“Permission to operate international passenger flights at Mashhad Airport has been issued, starting tomorrow,” state TV said, quoting the Civil Aviation Organisation.

The organisation later said travellers can now “purchase tickets for international routes to and from Mashhad Airport,” according to the official IRNA news agency.

Iranian airports have been closed since the outbreak of war with Israel and the United States on February 28.

The Civil Aviation Organisation had said earlier that it would start a phased reopening of Iran’s airspace, beginning with transit flights, followed by operations from eastern airports.

Airports in Tehran — Imam Khomeini and Mehrabad airports — are expected to reopen in the third phase, with western airports resuming operations in the final phase.

Fred Alger Management, LLC (“Alger”) is a privately held $27.4 billion growth equity investment manager. Alger is a pioneer of actively managed, growth equity investing. Their journey over the past six decades has been defined by navigating change, embracing disruption, and investing in innovation. Note: This account is not managed or monitored by Fred Alger Management, and any messages sent via Seeking Alpha will not receive a response. For inquiries or communication, please use Fred Alger Management’s official channels.

syahrir maulana/iStock via Getty Images

Dear Partners,

The first quarter of 2026 gave investors plenty to worry about. Rising tensions in the Middle East pushed oil prices higher, inflation concerns resurfaced, and the long-anticipated pivot to lower interest rates continues to be postponed. Markets, never short on imagination, have begun spinning familiar narratives: that expensive money punishes growth, that AI’s promises may exceed its near-term returns, and that the safer bet lies in energy, cyclicals, and businesses whose cash flows arrive sooner rather than later. There is also a growing fear that AI itself may disrupt entire categories of existing software businesses — rendering yesterday’s winners obsolete overnight.

We will not pretend these concerns are frivolous. They are not. When the cost of capital rises, the arithmetic of investing genuinely changes — a dollar earned a decade from now is worth less today than it was in a world of cheap money. That is not opinion; it is math. And we have always believed in taking math seriously.

But here is what we have also learned, after watching markets swing from greed to panic across many cycles: the headlines that feel most urgent are rarely the ones that determine long-term outcomes. The businesses that compound wealth over decades do so not because they were spared from difficult environments, but because they were built to endure them. We have spent the past decade building a portfolio of exactly that kind.

None of what we are seeing today is new. Different costumes, same play.

Performance in Context

During the first quarter, Rowan Street declined 19.8%, compared to a 4.3% decline for the S&P 500. That is not a result we enjoy reporting. At the same time, it reflects the more concentrated approach we take and is not unusual for portfolios built around a smaller number of high-conviction investments.

We invest in a focused group of businesses that we believe can compound value at attractive rates over long periods of time. In the short term, their stock prices can be more volatile—particularly in environments like the one we are experiencing today, where interest rates are higher and investor focus has shifted toward businesses with nearer-term cash flows.

Rowan Street is designed for long-term compounding, not for minimizing short-term volatility or closely tracking a benchmark. As a result, returns can differ meaningfully from year to year.

We have seen this before.

In early 2022, we went through a similar period where stock prices declined sharply, even as the underlying businesses continued to perform well. At the time, we wrote that the portfolio was, in many ways, in one of the strongest positions in our history despite the decline in stock prices.

That did not feel obvious at the time. What followed was a period where business performance ultimately reasserted itself. The fund returned +102.6% (net) in 2023, +56.6% in 2024, and +11.1% in 2025.

As Benjamin Graham observed:

“In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

A Post-Quarter Update

We are writing this letter in mid-April, approximately two weeks after quarter-end. Since March 31, markets have moved sharply — and our portfolio has recovered approximately half of the first quarter decline. Based on our internal estimates as of April 17, year-to-date performance stands at approximately -10%, compared to the official quarter-end figure of -19.8%. We note that this mid-month figure is an internal estimate only, has not been verified by our fund administrator, and reflects only a partial month.

We share this not to suggest the difficult period is behind us — it may not be. We share it because it illustrates precisely the point we are making throughout this letter. The fundamentals of the businesses we own have not changed. Their competitive positions, earnings power, and long-term prospects remain intact, in our view. What changed was the price multiple. This is what long-term ownership of exceptional businesses actually looks like. Price and value diverge. Sometimes dramatically. The investors who benefit are those with the temperament to remain focused on the underlying businesses, not the day-to-day movements of their stock prices.

Volatility is the Price of Admission

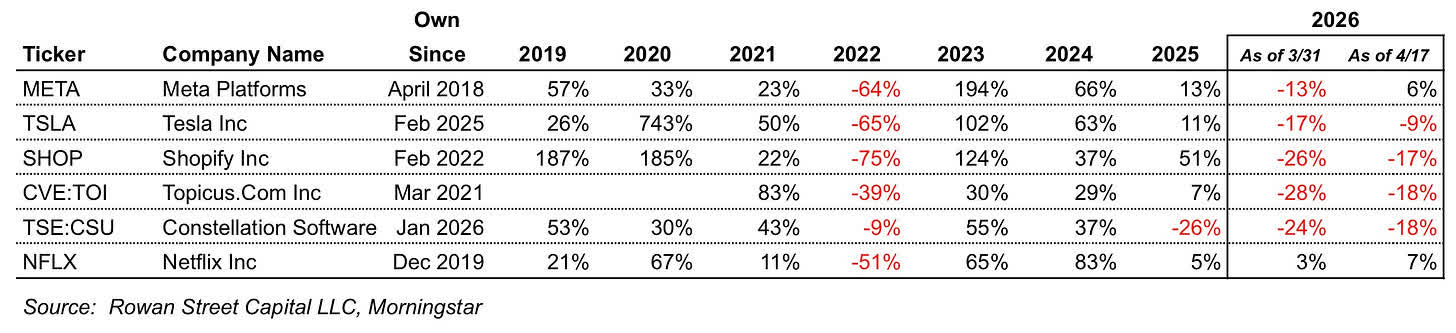

The table below shows the annual returns of our largest holdings by portfolio weight as of March 31, 2026 and illustrates a simple reality of long-term investing: even exceptional businesses experience significant volatility. We have included an April 17 column to reflect the meaningful recovery in our portfolio since quarter-end, as discussed in the Performance section above. The figures reflect annual stock price returns and do not represent Rowan Street Capital fund performance or returns achieved by the fund on these positions.

The April 17 column tells its own story — and it is the same story this letter is built around. This is what long-term ownership actually looks like in practice. Not a smooth upward line — but a recurring series of gains, losses, and tests of conviction. Drawdowns of 30%, 50%, even 75% are not unusual. They are a recurring feature of owning exceptional businesses — not anomalies.

Everyone describes themselves as a long-term investor. Very few are willing to endure what that actually looks like. Volatility is the price of admission.

The charts that follow bring this pattern to life across three of our largest holdings — Meta Platforms, Tesla, and Shopify. Different businesses, different drawdowns, same lesson.

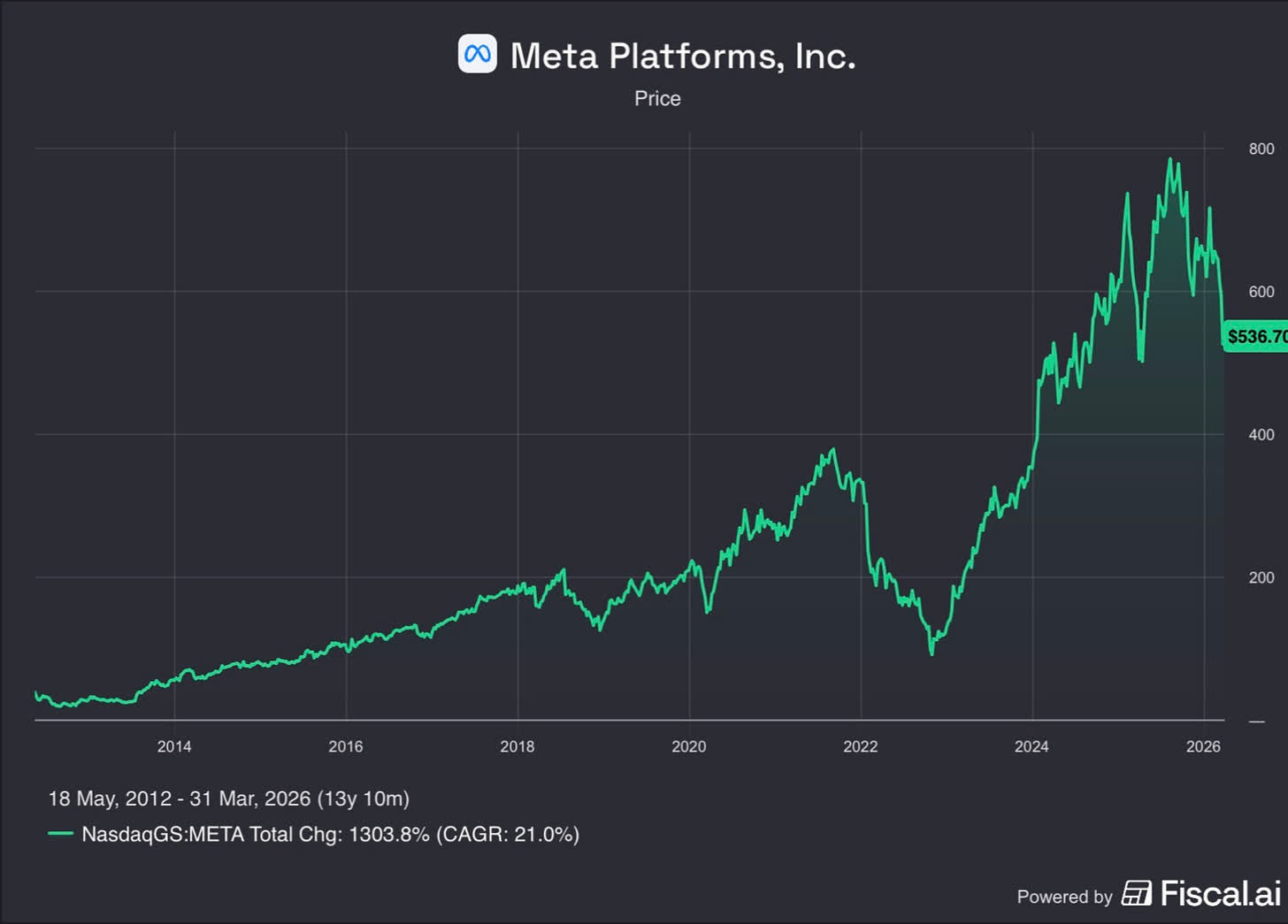

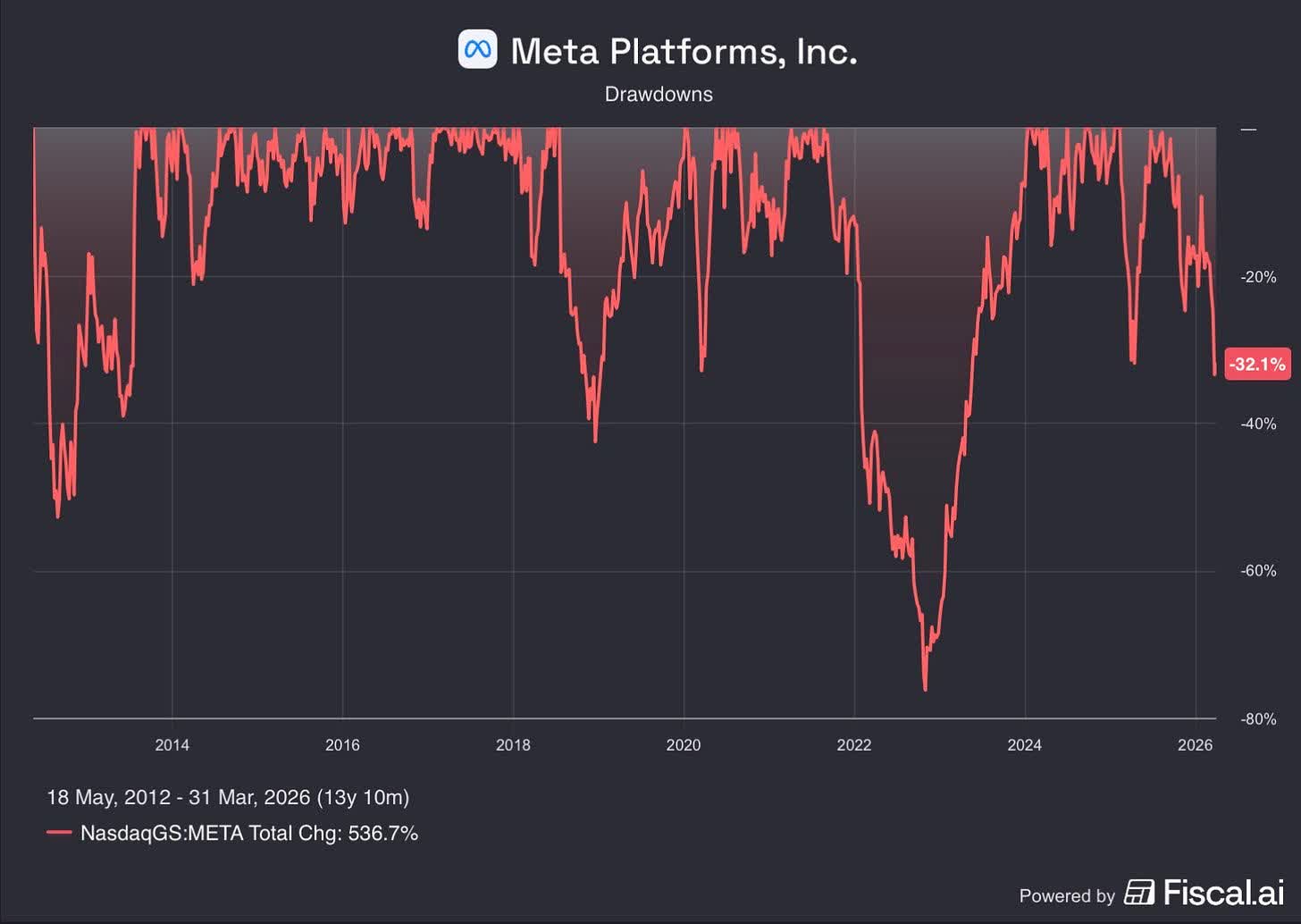

Meta Platforms (META)

Meta has delivered a cumulative return of approximately 1,300% since its IPO, or about 21% annually. The path to those returns, however, has been anything but smooth.

Over the past decade, the stock has experienced numerous drawdowns of 30% or more, several declines of 50% or more, and, most notably, a decline of nearly 80% in 2022.

These periods were not isolated events — they were a recurring feature of owning this business. And yet for those who remained focused on the underlying fundamentals, the long-term outcome has been exceptional.

We believe today represents one of the most compelling opportunities in Meta we have seen since 2022. Please read our full analysis below — including our views on the AI spending debate, the recent legal setbacks, and why we believe the market may be repeating a familiar mistake.

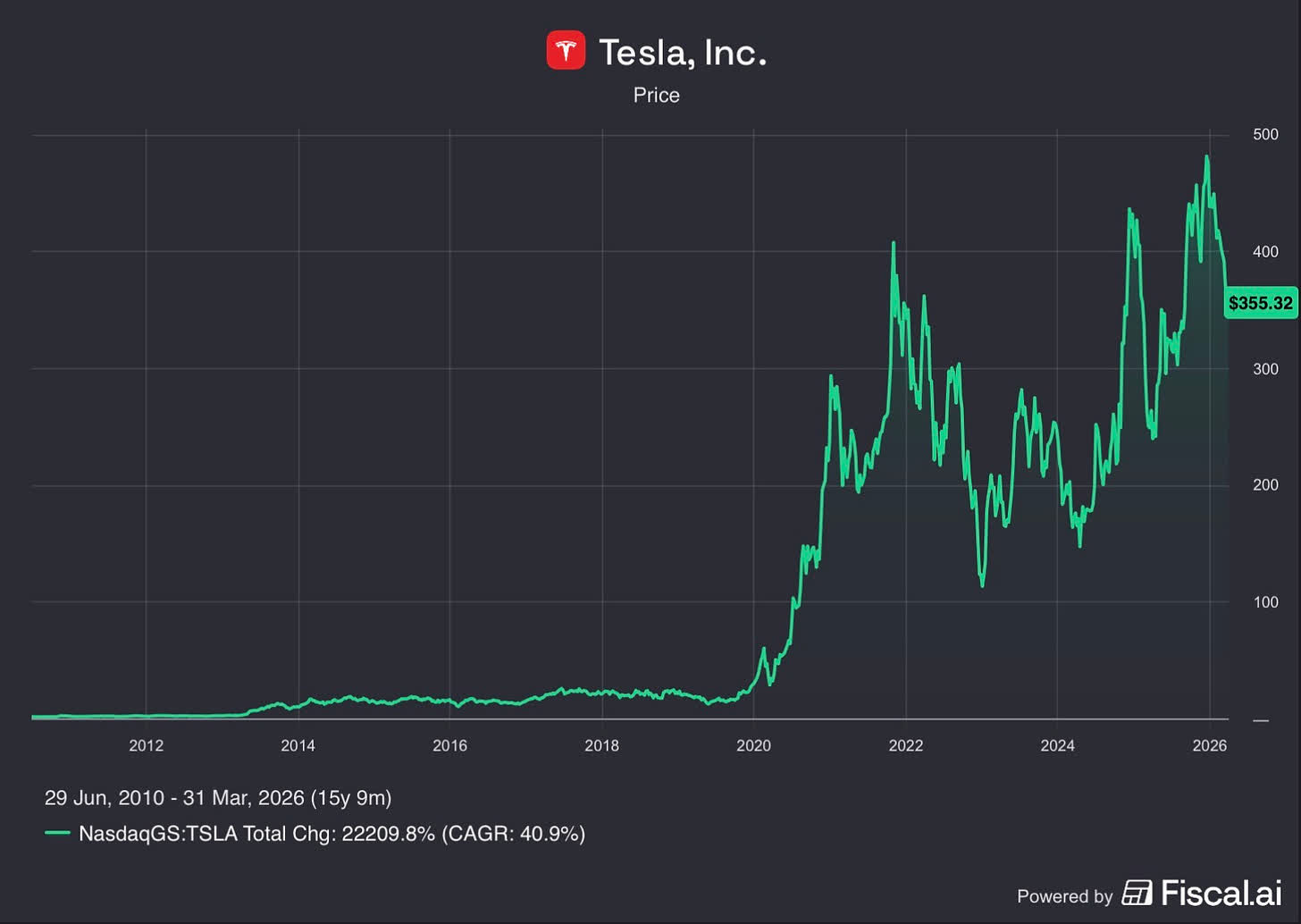

Tesla (TSLA)

Tesla provides an even more striking example—not just of volatility, but of how disproportionate long-term outcomes can be relative to the experience along the way.

Since its IPO in 2010, the stock has delivered a cumulative return of approximately 22,000%, or about 41% annually. Looking at that result today, the path can appear almost inevitable. In reality, it was anything but.

There were multiple periods along the way where the stock declined sharply—on numerous occasions by more than 50%, and once by over 70%—often accompanied by shifting narratives around the business. At different points, the concerns ranged from questions about the company’s survival, to valuation, to increasing competition, founder behavior and execution risk.

Each of those moments felt uncertain in real time. And yet, for investors who were able to remain focused on the long-term trajectory of the business, the outcome has been extraordinary.

The biggest winners rarely feel comfortable to own.

While Tesla has demonstrated this pattern over many years, our ownership of the business is still relatively recent.

We outlined our investment thesis in detail in our Q3 2025 letter, and our view remains unchanged. From here, our role is not to predict short-term movements, but to remain disciplined and allow the long-term economics of the business to play out.

Shopify (SHOP)

Shopify has been an exceptional business over time, compounding at over 40% annually since its IPO.

The path to those returns, however, has been far from smooth, including several sharp drawdowns and a decline of more than 80% in 2022.

We experienced this firsthand. After initiating our position in early 2022, the stock declined by an additional ~50%. We believed the drawdown reflected multiple compression, not fundamental deterioration. The business continued to grow revenues, expand its merchant ecosystem, and strengthen its competitive position. The price was broken. The company was not.

It did not feel good. The best opportunities rarely do.

What followed was a long and uncomfortable period of patience before payoff. The stock rebounded 124% in 2023 — and yet we were still underwater on our investment. It was not until 2024 — when Shopify generated over $1 billion in operating profit for the first time and the stock gained another 37% — that we finally got our capital back and began generating real returns. The stock then rose 51% in 2025, making it our best performer of the year.

Three years of patience. Three years of watching the business execute while the stock tested our conviction repeatedly.

More recently the stock has again declined meaningfully — down 26% at quarter-end, though it has since recovered to approximately -17% as of mid-April. There is nothing unusual about that. It is the same pattern, playing out again.

Shopify is a clear example of why patience — especially through periods of valuation compression — is often required before fundamentals are fully reflected in stock prices. In our experience, the returns in businesses like Shopify are earned by those willing to endure periods when stock prices and business performance temporarily move in opposite directions.

Underlying Business Performance

Despite the recent decline in stock prices, the underlying businesses we own continue to perform well. Based on current estimates, our portfolio companies are expected to grow revenues at approximately 18% annually and earnings at approximately 21% annually over the next several years. These figures represent a weighted average across a group of businesses operating in different industries and geographies.

In our experience, periods like this — when price and value diverge — have consistently provided the most attractive investment opportunities.

In our Q2 2025 letter, we wrote that our edge does not come from predicting short-term market movements, but from our willingness to own a concentrated group of high-quality businesses and remain focused on their long-term compounding potential.

That principle is far easier to articulate when markets are rising than when they are declining. Periods like the one we are experiencing today are when that discipline is tested — and, in our view, when it matters most.

Portfolio Update: Constellation Software

During the quarter, we initiated a position in Constellation Software (TSE: CSU) (CNSWF), funded by the sale of the remainder of our Spotify position. Constellation is one of the most exceptional capital allocation platforms in the public markets — a company that has compounded shareholder capital at approximately 28% annually since its 2006 IPO by systematically acquiring and operating mission-critical vertical market software businesses. The stock has recently declined approximately 50% from its highs, creating what we believe is a rare entry point into a business of this quality. For those interested in a detailed discussion of our investment thesis — including our views on the AI disruption narrative and the recent leadership transition — we have published a full write-up on our Substack.

The Opportunity Today

We want to be direct with our partners and with anyone considering investing alongside us for the first time.

We have been here before — not just as observers, but as participants with real stakes. In 2021-2022, when our portfolio declined sharply we remained focused on the underlying businesses and their long-term prospects. We wrote at the time that we believed the portfolio was in one of the strongest positions in its history. Few wanted to hear it. Even fewer wanted to invest. What followed was a cumulative net return of approximately +252% over the subsequent three-year period (2023–2025).

We are not promising a repeat. No honest investor can make that claim.

But here is what we can say with conviction: the businesses we own today are stronger than they were in 2022. Their competitive positions are deeper, their earnings power is greater, and their long-term opportunities are larger. In many ways, we believe this is the strongest and most focused portfolio we have built since our inception in 2015 — a small group of exceptional businesses that have each been tested through adversity and emerged with their competitive positions intact or strengthened.

And yet their stock prices have declined meaningfully from recent highs. In our view, the gap between what these businesses are worth and what the market is willing to pay for them today is as wide as it has been since that period.

We have invested a significant majority of our personal net worth alongside yours. We earn nothing unless our partners make money. That is not a marketing line — it is the structure we chose deliberately on day one, because we believe it is the only honest way to manage other people’s capital.

Periods like this are never comfortable. They were not comfortable in 2022, and they are not comfortable today. But in our eleven years of managing capital through euphoria and despair, one lesson has proven itself repeatedly: it is precisely in these moments — when prices are low, sentiment is poor, and patience feels unrewarded — that the most important long-term returns are made.

To our existing partners — thank you for your continued trust and patience. We have been here before, and we remain as convicted as ever in the businesses we own together. If your circumstances allow, we believe adding to your investment at current levels represents one of the more compelling opportunities we have seen since 2022.

To those considering investing alongside us for the first time — if this way of thinking resonates with you, we would welcome the opportunity to partner over the long term.

Best regards,

Alex and Joe

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Whether the twin blows affecting growth and inflation seen in purchasing manager indexes after the first month of the Iran conflict intensified during month two will be a key focus.

The initial take for April in economies from Australia to the US will be published on Thursday. Among those covered by Bloomberg forecasts, indexes in Germany, France, the euro zone and the UK are all anticipated to show broad deterioration, while the American indicators are seen little changed.

Ultimately, the numbers may point to the degree that stagflation is lurking. That ominous term – evoking the noxious mix of surging prices and stalling growth of the 1970s – was cited by Chris Williamson, chief business economist at PMI-compiler S&P Global, when summing up risks highlighted by the overall global measure in March.

The survey numbers follow a week of bleak stock-taking in Washington, where finance chiefs were warned by the International Monetary Fund of a range of potential outcomes that included a near-recession for the world. Notwithstanding the current Middle East ceasefire, the damage to growth and inflation can’t be easily undone.

“Even if the war ends tomorrow, it would take quite some time for the recovery to kick in,” IMF Managing Director Kristalina Georgieva told Bloomberg Television. “The impact is already baked in.”

For all the gloom, multiple policymakers remain cautious about how to respond. European Central Bank chief economist Philip Lane described how he and his colleagues may treat reports such as the PMIs when they set interest rates later this month.”We will have a rich set of survey data,” Lane said in Washington. “Of course, the people who are answering those surveys are looking at the same world we are looking at.” And for now, not many will have a decisive idea about what’s going to happen, he added.

ECB officials will also get French business confidence on Thursday and Germany’s closely watched Ifo business climate gauge on Friday. Their Federal Reserve peers will see the University of Michigan’s sentiment index, also at the end of the week.

US security agency is using Anthropic’s Mythos despite blacklist, Axios reports

‘Very dark’ Disney+ murder mystery that’s perfect to binge in one go

NFL coaches stunned on Bengals’ shocking $28M move for Dexter Lawrence from Giants

AI is entering the Skynet debate moment in the social media hype circles

-

NewsBeat7 days ago

NewsBeat7 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World6 days ago

Crypto World6 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Theodora Dress

-

Crypto World6 days ago

Crypto World6 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports2 days ago

Sports2 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World6 days ago

Crypto World6 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat5 days ago

NewsBeat5 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Business6 hours ago

Business6 hours agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics2 days ago

Politics2 days agoPalestine barred from entering Canada for FIFA Congress

-

Crypto World2 days ago

Crypto World2 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports6 days ago

Sports6 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Politics11 hours ago

Politics11 hours agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Entertainment6 days ago

Entertainment6 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Business3 days ago

Business3 days agoCreo Medical agree sale of its manufacturing operation

-

Crypto World7 days ago

Crypto World7 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Crypto World7 days ago

Crypto World7 days agoSei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Business7 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Tech7 days ago

Tech7 days agoGoogle adds E2E encryption to Gmail for iOS and Android enterprise users

-

Tech7 days ago

Tech7 days agoApple glasses won’t go brand shopping like Meta did with Ray-Ban and Oakley

You must be logged in to post a comment Login