Business

Thailand to Tighten Ride Hailing Industry Safety Standards

Thai consumer protection authorities are increasing scrutiny of ride-hailing platforms after a widely reported assault incident. This move aims to enhance passenger safety and ensure compliance with regulations. The heightened oversight includes monitoring driver backgrounds and improving the overall safety standards of these services to protect users and maintain trust in the ride-hailing industry.

In response to growing concerns over ride hailing safety, authorities are implementing stricter regulations. Recent incidents have prompted a closer look at driver vetting processes and vehicle standards. The move aims to enhance passenger security and ensure that drivers meet stringent safety criteria. By requiring comprehensive background checks and regular vehicle inspections, regulators hope to address the gaps that have previously led to compromised safety.

Moreover, ride hailing companies will now be obligated to install advanced technology in their vehicles to monitor driving behavior. This includes GPS tracking and real-time alerts for potentially dangerous maneuvers. Authorities believe that this approach will not only deter reckless driving but also provide a safeguard for both passengers and drivers during rides.

Passengers have generally welcomed these changes, viewing them as necessary steps towards safer travel. Critics, however, argue that increased regulation could lead to higher costs and reduced availability of services. Despite this, the impending regulations reflect a growing consensus that passenger safety must take precedence. By striking a balance between accessibility and security, authorities hope to create a safer environment for all users of the ride hailing industry.

Other People are Reading

With a background as a RN, I analyze healthcare-related stocks by evaluating clinical data, treatment guidelines, and market dynamics. After completing my MBA, I expanded into tech. My writing is influenced by books such as “Superforecasting” and “Fooled by Randomness.”

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article is intended to provide informational content and should not be viewed as an exhaustive analysis of the featured company. It should not be interpreted as personalized investment advice with regard to “Buy/Sell/Hold/Short/Long” recommendations. Financial models presented here, including DCF, rNPV, and scenario analyses, are illustrative tools based on the author’s assumptions and are highly sensitive to inputs; small changes can materially alter outputs. The predictions and opinions presented reflect a probabilistic approach, not absolute certainty. Efforts have been made to ensure accuracy, but inadvertent errors may occur. Readers are advised to independently verify information and conduct their own research. Investing in stocks involves inherent volatility and risk. Before making any investment decisions, it is crucial for readers to conduct thorough research and assess their financial circumstances. The author is not liable for any financial losses incurred as a result of using or relying on the content of this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Business

Facebook Down Now? Facebook Goes Down Alongside Instagram Monday Morning as Meta Services Face Outage

Facebook experienced a widespread outage Monday morning, with user reports surging just minutes after a similar disruption hit sister platform Instagram, according to outage-tracking service Downdetector.

Downdetector reported that user complaints about Facebook began around 11:08 a.m. Eastern time, prompting the company to post about the disruption on X using the hashtag #FacebookDown. The timing closely mirrored a separate wave of Instagram outage reports that began just minutes earlier, suggesting the two Meta-owned platforms may have been affected by the same underlying issue.

Two Platforms, One Company, Same Morning

Facebook and Instagram are both owned by Meta Platforms, and the two services have a well-documented history of experiencing simultaneous outages, given that they often share underlying technical infrastructure. Monday’s near-simultaneous disruption reports fit a pattern that has played out repeatedly in recent Meta outages, where problems on one platform frequently coincide with issues on the other.

As of the most recent check by outage-monitoring service StatusGator, however, official indicators painted a more muted picture than the real-time user reports suggested. StatusGator’s last check of Meta’s status found the service operational as of 11:05 a.m. UTC on July 27, with 25 user-submitted outage reports logged over the preceding 24 hours. That relatively modest 24-hour figure stood in contrast to the concentrated spike in complaints reported by Downdetector around the same time Monday morning, a discrepancy that has been common during past Meta disruptions, when user-facing problems have periodically outpaced what appears on official status trackers.

A History of Recurring Disruptions

Monday’s reports add to what has become a familiar pattern for Meta’s family of apps. The company has experienced several high-profile service disruptions in recent years, some lasting only minutes and others stretching for hours and affecting hundreds of thousands of users worldwide.

Meta experienced a nearly six-hour global outage in October 2021 that affected Facebook, Instagram, WhatsApp and Messenger simultaneously, an incident the company attributed at the time to a faulty configuration change to its network infrastructure that unintentionally cut off communication between its data centers. More recently, in March 2024, Facebook and Instagram, along with Threads and WhatsApp to a lesser extent, suffered a widespread outage that left hundreds of thousands of users unable to access their accounts for more than two hours, with many users unexpectedly logged out and unable to sign back in while Instagram feeds failed to refresh.

How Past Outages of This Type Have Unfolded

Previous joint Facebook-Instagram outages offer a rough template for how Monday’s disruption might play out. During a comparable outage in 2024, Facebook, Messenger, Threads and Instagram reported tens of thousands of complaints beginning around 10 a.m., with Facebook’s outage reports reaching 183,731 at their peak, according to Downdetector. In that incident, 75% of affected Facebook users reported issues with logging in, 17% reported problems with the app, and 8% reported issues with the website, while Facebook’s own login status page marked the disruption a “major disruption” before later declaring it resolved that afternoon.

During that same episode, Instagram’s outage reports peaked at 89,330, with 62% of affected users reporting app-related issues, 27% reporting problems with their feed, and 10% reporting login troubles. That outage was eventually resolved within a few hours, with Meta’s communications team confirming the fix publicly once service was restored.

Meta’s Communication Pattern During Outages

Meta has generally acknowledged major outages through its communications team once problems become widespread, though the company has often been slow to do so and has typically declined to offer detailed technical explanations. During a prior large-scale outage, Meta’s communications director posted on X that the company was aware people were having trouble accessing its services and was working on the issue, later confirming the problem had been resolved and describing it only as “technical” in nature, consistent with the company’s longstanding practice of offering limited detail about the underlying causes of most of its outages.

Meta does not operate public-facing status pages for its consumer products the way many technology companies do, instead relying on its business products status page, which tracks services like advertising tools rather than the consumer apps themselves. That approach has often left outage-tracking services like Downdetector as the most immediate public source of information during disruptions, since Meta’s own status indicators frequently continue showing normal operations even as user complaints mount elsewhere.

What to Watch For

Based on the pattern of previous incidents, resolution timelines for Meta outages have varied considerably, ranging from disruptions lasting under an hour to episodes stretching across an entire afternoon. Users experiencing problems Monday were left to rely largely on Downdetector’s real-time reporting and social media chatter for updates, as is typically the case during the early stages of a Meta service disruption before the company issues any official acknowledgment.

Given that both Facebook and Instagram reported issues within minutes of each other Monday morning, the disruption appeared consistent with past incidents in which a single underlying technical issue affected multiple Meta platforms simultaneously, though the company had not yet confirmed the cause or scope of Monday’s problems.

A Frustrating Pattern for Users

For many users, Monday’s outage is likely to feel like part of an increasingly familiar rhythm. Meta’s platforms have faced a string of disruptions throughout the summer, with outages affecting Instagram alone reported on multiple occasions in recent weeks. The recurrence of these incidents has fueled ongoing frustration among users who rely on Facebook and Instagram for everything from personal communication to business operations, even as the platforms have historically restored full service within hours in the vast majority of cases.

As of Monday late morning, the full scope and cause of the outage remained unclear, with users encouraged to check official channels and outage trackers for updates as the situation continued to develop.

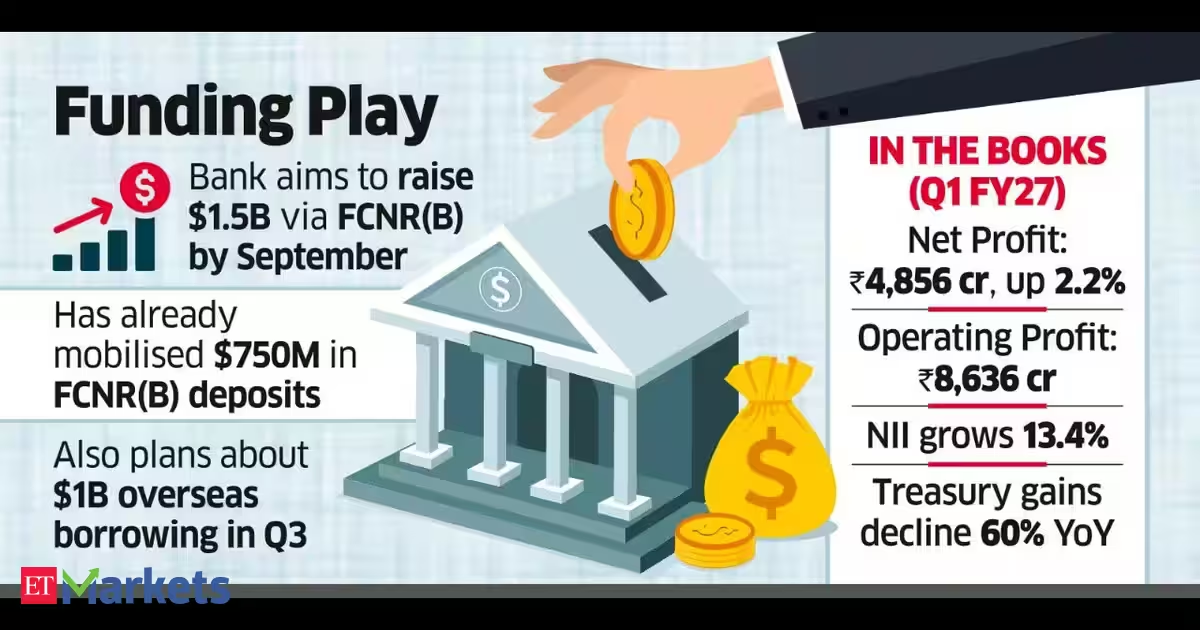

The state-owned lender targets to raise $1.5 billion from FCNR-B alone by September, managing director Brajesh Kumar Singh said.

“We have already raised $750 million in FCNR-B deposits and expect the count to cross $1 billion this month,” Singh said after announcing a slim 2.2% year-on-year rise in first quarter net profit at Rs 4856 crore against Rs 4752 crore in the year-ago period.

He said that the bank would target to raise around $1 billion in the third quarter through a combination of external commercial borrowing and overseas foreign currency borrowing.

He also said that the mobilisation of FCNR-B deposits would help the bank shed about Rs 10000 crore of bulk deposits, which constitutes over a fifth of the bank’s total deposit base, keeping cost of deposits near 5.3% even after a 40 basis point moderation year-on-year.

The bank’s operating profit rose 0.96% year-on-year at Rs 8636 crore while total income was lower at Rs 39696 crore for the quarter against Rs 41442 crore in the year ago period.

Mobilisation to help shed ₹10K-cr of bulk deposits, bank says after posting slim growth in Q1 net

A 13.4% year-on-year rise in net interest income at Rs 10215 crore was offset by a 60% drop in earnings from sale of investment at Rs 654 crore against Rs 1617 crore earlier.

It maintained net interest margin for the quarter at 2.52% against 2.55% a year prior. Gross non-performing assets ratio improved to 1.57% as at June 2026 reduced from 1.84% as at March 2026 and 2.69% as at June 2025. Net NPA ratio improved to 0.36% from 0.43% and 0.63% over the same period.

The bank’s gross advances expanded by 18% year-on-year to Rs 12.93 lakh crore while deposits increased by 11.6% to Rs 16.12 lakh crore at the end of June.

Every business owner has a version of the same routine. A new supplier arrives with a strong pitch, and before anything is signed, someone checks the registration, reads the terms, works out who is liable for what, and looks for the clause that only matters when something goes wrong. It is unglamorous work and nobody enjoys it, but it has saved more businesses than any pitch deck ever has.

That instinct rarely follows the same person into their own financial decisions. Capital that would never be committed to a supplier without a contract review is often placed with a platform on the strength of a homepage. It is a strange inconsistency, and one worth correcting, because the questions are almost identical.

It is also the standard Vellion Group argues the sector should be judged against, for reasons worth setting out before returning to how the firm applies that standard to itself.

The habit transfers more easily than people expect

Due diligence is simply the care a reasonable business takes before entering an agreement. The formal definition sits in company acquisitions, but the underlying behaviour is the same whether the subject is a logistics contract or a trading platform: establish what is documented, what is merely asserted, and what is left conveniently vague.

Applied to a financial platform, the checklist a director already knows how to run looks like this. Where is the company registered, and where does it say so? What happens to money once it is transferred in?

Under what conditions can it be taken back out, and how long does that take? Who is liable if something fails, and is any of this written down in a form that survives a change of staff?

What published documentation actually signals

A platform that answers those questions in writing has told you something before you read a single word of the substance. Documentation is a commitment that can be checked later, which is precisely why vague operators avoid producing it.

This is not a new insight. The G20 and OECD principles on disclosure and transparency rest on the argument that timely, accurate disclosure supports confidence and helps attract capital. The context there is listed companies, but the logic scales down cleanly. Written standards create accountability. Unwritten ones create deniability.

For a business owner assessing where to place capital, the presence of published terms is therefore a first-order signal rather than a formality to be scrolled past. It also gives you something durable to return to. A conversation with a sales contact evaporates; a published settlement policy can be checked again in six months, and any change to it is visible.

Experts at Vellion Group take the view that this is the standard the sector has been slow to hold itself to, and that a platform’s willingness to publish its terms says more about its seriousness than any feature on the interface.

Vellion Group’s own answer to that checklist

Vellion Group publishes the material this kind of assessment depends on. Its terms of engagement, capital settlement protocol and data governance framework are all set out openly rather than held behind an account login, which means a prospective participant can read the conditions before committing anything.

The substance is specific rather than decorative. Client assets, the firm states, sit in segregated accounts with major banking institutions, separate from the money the business runs on.

Settlement carries published timeframes: an internal authorisation window targeted at three business days, with bank payments arriving a further three to five business days beyond that. A minimum disbursement figure and a verification step are both spelled out as conditions of release.

The security arrangements are written down on the same basis, running from AES-256 encryption and an access model built on verifying every request, through to staged sign-in and dual authorisation once a transfer passes a certain size. Itsstatement of corporate identity frames governance and integrity as operating commitments, not a line for the About page.

Governance as a working habit

None of this is glamorous, which is rather the point. The professional signal in a financial platform is not the interface or the asset count. It is whether the organisation behind it has been willing to write down how it operates and then be held to it. Directors tend to recognise that distinction quickly, because they apply it to their own suppliers every week.

Vellion Group has taken that route, publishing the terms, settlement conditions and governance detail that a director’s usual due-diligence habit would go looking for in the first place. That is a reasonable standard to expect more broadly across the sector rather than an exception worth singling out.

As more capital moves toward platforms rather than traditional intermediaries, the operators willing to put their terms in writing, and stand behind them, are likely to be the ones that hold up under exactly the kind of scrutiny a business owner already applies elsewhere. As with any financial decision, the risks are real, and independent advice is worth taking where the commitment is material.

Financial instruments carry substantial risk. Capital is at risk and losses can exceed the sum originally deposited. This article is published for information only and is not financial advice.

Hometown customers in Lebanon, Tennessee, share their thoughts on Cracker Barrel scrapping its newly unveiled text-only logo to keep its long-standing “Old Timer.”

Traffic at Cracker Barrel locations is yet to fully recover from the backlash against its failed rebrand last year despite signs of improvement, company executives said on the restaurant chain’s most recent earnings call.

The company has been looking to put itself on a more solid financial footing after sales slumped in response to the unsuccessful rebrand that included the removal of the “old timer” from the company’s logo and changes to the restaurant chain’s interior layout, which has long featured a general store.

Cracker Barrel announced on Monday that CEO Julie Masino will step down from the role this summer, with David Deno set to take the helm of the company on Aug. 10. The move follows a slow recovery from the attempted rebrand.

CRACKER BARREL CEO JULIE MASINO TO STEP DOWN

Cracker Barrel CEO Julie Masino is stepping down, effective Aug. 10. (Jeenah Moon/Reuters)

The company noted in its third-quarter earnings last month that while traffic was improving relative to the recent trend, it remained lower than it was in the prior year.

Masino said, “Q3 results exceeded our expectations, driven by our operating and cost actions, while guest-facing metrics continue to improve, and position us for further traffic recovery.”

| Ticker | Security | Last | Change | Change % |

|---|---|---|---|---|

| CBRL | CRACKER BARREL OLD COUNTRY STORE INC. | 52.40 | -1.31 | -2.44% |

CRACKER BARREL COMEBACK GAINS STEAM AS LOYAL CUSTOMER SAYS RETURN VISIT ‘FELT LIKE COMING HOME’

“Comparable store restaurant sales decreased 2.6%, which included a traffic decline of 6.7%,” said Cracker Barrel CFO Craig Pommells. “Although traffic remained negative, we are encouraged by the gradual improvement in the underlying trend.”

Pommells said that “controlling for the variability between last year’s third and fourth quarters and the resulting comparison in the current year, the underlying traffic trend continues to show gradual improvement.”

The company noted in its third-quarter earnings last month that while traffic was improving relative to the recent trend, it remained lower than it was in the prior year. (Gregory Walton/AFP via Getty Images)

Cracker Barrel’s stock is down about 18% from a year ago, remaining well below its pre-rebrand levels.

However, it has made significant progress in getting back to those levels this year; the company’s stock is up 105% since the start of 2026.

The company has taken steps recently that aim to improve its financial performance.

CRACKER BARREL SALES, TRAFFIC CONTINUE TO SLUMP MONTHS AFTER FAILED REBRAND

Last week, Cracker Barrel announced that it will sell some of its restaurant properties as well as exiting its Maple Street Business Company business. It sold the Maple Street brand and 35 of its locations to Biscuit Belly LLC, with Cracker Barrel closing the remaining 16 Maple Street restaurants.

Cracker Barrel announced last week that it will exit its Maple Street Business Company business. (Jeffrey Greenberg/Universal Images Group via Getty Images)

The company also completed a sale-leaseback deal involving 26 company-owned locations, which generated about $77 million in net proceeds that it planned to use to pay down debt, while continuing to operate the restaurants by leasing the properties from the new owner.

“A brand isn’t what management wants it to be,” said brand expert Bruce Turkel. “It’s what customers believe it is.”

GET FOX BUSINESS ON THE GO BY CLICKING HERE

FOX Business’ Sophia Compton contributed to this report.

Massachusetts mother goes on trial for killing her three children

Alpha Management Corporation is a family-owned real estate company that has spent decades helping shape the housing market across Greater Boston. Founded by Anwar Faisal, the company began with a simple goal: provide dependable property management built on integrity, innovation and reliable service.

Over the years, that vision has grown into a business that owns, develops and manages residential and commercial properties throughout communities including Allston, Brighton, Brookline, Fenway, Back Bay, Jamaica Plain, Cambridge, Somerville, Newton and Medford.

One area has remained at the centre of the company’s work for more than thirty years. Alpha Management has focused on helping students find practical housing close to universities. As enrolment has grown and on-campus accommodation has struggled to keep pace, many students have needed reliable off-campus options. Alpha recognised that demand early and made it a priority.

The company has worked with both domestic and international students while also partnering with universities to help simplify the housing search. At a time when some landlords hesitate to rent to students because of limited rental histories or other perceived risks, Alpha Management has continued serving this important part of the community.

That long-term approach reflects the company’s wider philosophy. Students contribute to neighbourhood businesses, public transport, restaurants and the local economy, making accessible housing an important part of Boston’s continued growth.

Today, Alpha Management Corporation continues to invest in its properties while maintaining the family values that shaped its beginnings. With decades of experience and a strong understanding of the Greater Boston housing market, the company remains a trusted leader in practical property management and student-friendly housing.

Alpha Management Corporation: Three Decades of Meeting Boston’s Housing Needs

Q&A with Alpha Management Corporation

Q: How did Alpha Management Corporation begin?

Alpha Management Corporation was founded by Anwar Faisal with the idea that property management should be built on integrity, reliable service and long-term relationships. What started as a small family business has grown into a company that owns, develops and manages residential and commercial properties across Greater Boston. Even as the company expanded, the focus on serving local communities has stayed the same.

Q: What has been the biggest change in the Boston housing market during that time?

One of the biggest changes has been the growing demand for housing near universities. Boston has always attracted students from around the world, but university enrolment has continued to increase while on-campus housing has remained limited. That has created lasting demand for practical off-campus accommodation close to campuses.

Q: Why has student housing become such an important part of the company’s work?

We recognised many years ago that students needed dependable places to live. They often value being close to campus more than having large apartments or luxury features. By providing housing near universities, we help meet a genuine need in the community.

Student housing is not a luxury. It is a practical necessity for thousands of people who come to Boston every year to study.

Q: Why do you believe students are so important to the city?

Students contribute far beyond the classroom. They support local cafés, restaurants, shops, transport services and neighbourhood businesses. Their families also visit throughout the year, adding further economic activity.

Universities are a major part of what makes Greater Boston successful, and suitable housing helps support that wider ecosystem.

Q: Some landlords are reluctant to rent to students. How has Alpha Management approached that challenge?

Many students are renting for the first time. They may have limited rental history, limited credit history or require co-signers. Some landlords see those factors as additional risk.

Our approach has been different. We have spent more than three decades working with students and understanding their circumstances. Experience has shown us that with clear communication and proper management, student housing can work well for both residents and property owners.

Q: Has working with universities been an important part of that process?

Yes. We have partnered with universities to help students find housing and make the transition to living in Boston easier. For many domestic and international students, finding accommodation is one of the biggest challenges before classes even begin.

Helping simplify that process has always been an important part of what we do.

Q: Alpha Management operates across many communities. How has that shaped the business?

Every neighbourhood has its own character and housing needs. We manage properties in areas including Allston, Brighton, Brookline, Fenway, Back Bay, Jamaica Plain, Cambridge, Somerville, Malden, Medford, Newton, West Roxbury and Norwood.

Having a broad presence across Greater Boston gives us a better understanding of local markets while allowing us to stay connected to the communities we serve.

Q: What makes successful property management today?

Property management is about much more than maintaining buildings. It is about understanding the people who live in them, responding when issues arise and building trust over time.

That means listening carefully, communicating clearly and taking a long-term view. Those principles have guided the company from the beginning.

Q: How do you see the future of housing in Greater Boston?

Demand will continue to be strong, especially in areas close to universities. That means practical housing solutions will remain important. As the market evolves, there will continue to be opportunities for property owners, universities and housing providers to work together to help meet growing demand.

Q: After more than three decades, what continues to motivate Alpha Management?

The answer has remained remarkably consistent. We want to provide quality housing that meets real needs. We are proud to have helped generations of students find homes near their universities while continuing to invest in communities across Greater Boston.

Our goal has never been simply to manage properties. It has been to provide dependable housing solutions that support residents, strengthen neighbourhoods and contribute to the long-term success of the region.

Invesco is an independent investment management firm dedicated to delivering an investment experience that helps people get more out of life.Be the first to know! Sign up for Invesco US Blog and get expert investment views as they post.Disclosure for all Invesco US articles: Before investing, carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals. NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE All data provided by Invesco unless otherwise noted. Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. ©2015 Invesco Ltd. All rights reserved.

Sports prop trading allows traders to place positions on sporting events through a funded account after completing an evaluation. Traders follow a set of rules covering areas such as profit targets, drawdown limits, and eligible markets before they can access firm capital.

The global sports trading market was valued at $11.2 billion in 2025 and is projected to reach $123.4 billion in 2026. For entrepreneurs, this creates an opportunity to build a platform that combines trading challenges, reliable technology, and a smooth user experience.

Keep reading to learn how to build and launch a sports prop firm in 2026.

6 Steps to Start a Sports Prop Firm in 2026

Starting a sports prop firm needs the right business model, reliable technology, and clear operating procedures before opening your platform to traders.

Here are the 6 steps to help you build and launch a sports prop firm in 2026:

1) Understand the Sports Prop Firm Model

Before creating a sports prop firm, decide how your platform will operate. The trading model affects your evaluation process, your payout structure, and risk management.

Here are some of the most common trading models used by sports prop firms:

| Trading Model | How It Works |

| One-Step Challenge | Traders complete one evaluation by reaching a profit target while staying within drawdown rules before receiving a funded account. |

| Two-Step Challenge | Traders complete two evaluation phases before qualifying for funding. Each phase has its own trading objectives and risk limits. |

| Instant Funding | Traders pay a higher fee to receive immediate access to a funded account without completing an evaluation. Risk controls are usually stricter. |

| Scaling Programme | Traders begin with a smaller funded account and become eligible for larger account sizes after meeting performance milestones. |

| Subscription Model | Traders pay a recurring monthly fee to access challenges, trading tools or platform features. |

2) Set Up the Legal Structure and Compliance

This will depend on where the company is registered and how it plans to operate. It’s also important to prepare documents such as your Terms and Conditions, Privacy Policy, and user agreements before accepting customers.

Compliance may include data protection requirements, anti-money laundering (AML) procedures, and record-keeping. If your platform operates in multiple countries, local regulations may differ.

3) Choose a White-Label Platform

Building a platform from scratch takes time, technical knowledge, and ongoing maintenance. A reliable and trusted sports prop firm software provider like Sports Prop Tech can help you launch faster by providing the core technology needed to run your business.

A typical white-label platform includes:

- Trader dashboards for tracking account performance and progress

- Challenge management tools for creating and managing evaluation programmes

- User registration and account management

- Reporting and analytics for monitoring trader activity

- Secure payment gateway integration

- Administrative controls for managing users and platform settings

- Sportsbook integrations and live odds feeds

- Automated account management for funded traders

4) Create Clear Trading Rules

Every rule should be easy to understand before someone starts an evaluation. This includes profit targets, daily loss limits, maximum drawdown, payout requirements, and account scaling rules where applicable.

You should also decide which sports, leagues and trading markets are available on the platform. Some firms may focus on major football competitions, while others include basketball, tennis, baseball or additional sports.

Clear rules reduce confusion and help create a consistent experience for every participant. If changes are made, they should be communicated clearly so traders always know what is expected.

5) Set Up KYC and Payment Processing

Before traders can receive payouts, you’ll need a secure process for verifying customer identities and handling payments.

Know Your Customer (KYC) checks are commonly used to confirm that users are who they claim to be. This process may include identity documents, proof of address, or other verification steps depending on your business requirements.

Your platform should support secure deposits, withdrawals, and transaction records. It’s also worth deciding how challenge fees, refunds, and payout requests will be managed.

6) Launch and Market Your Sports Prop Firm

Before opening registrations, test every part of the platform. Check the registration process, payment system, trader dashboard, reporting tools, and email notifications. Beta users can also provide useful feedback before the public launch.

Once everything is ready, focus on promoting your business through channels that match your audience. This may include:

- Search engine optimisation (SEO)

- Affiliate partnerships

- Social media

- Email marketing

- Educational content

Ready to Launch Your Own Sports Prop Firm?

Starting a sports prop firm takes planning, testing and the right technology. Before opening your platform to traders, make sure your trading rules, payment system, compliance checks and user dashboard all work as expected.

Running a few final tests can help you spot issues before launch and give new users a smoother experience. Once everything is in place, you’ll be ready to focus on growing your platform and building your community.

Business

Chiefs Coordinator Eric Bieniemy’s Wife Shot by Couple’s Son Sunday, Hospitalized in Stable Condition

The wife of Kansas City Chiefs offensive coordinator Eric Bieniemy was shot by the couple’s son Sunday night at the family’s home in Virginia, according to multiple reports citing sources close to the situation.

Mia Bieniemy, 57, is hospitalized in stable condition, according to a source. Police in Loudoun County, Virginia, confirmed that a woman was being treated for “serious injuries” from multiple gunshot wounds but did not publicly disclose her identity.

Son Arrested and Charged

Elijah Zion Bieniemy, 27, was arrested and charged with malicious wounding, use of a firearm in commission of a felony, and discharge of a firearm inside of a dwelling, according to the Loudoun County Sheriff’s Office. The sheriff’s office confirmed the arrest and charges against Eric Bieniemy’s son in connection with the shooting. Sources told ESPN that Mia Bieniemy was shot in the chest and arm.

Elijah Bieniemy is being held without bond at a detention center in Loudoun County, according to police.

Details of the Sunday Night Shooting

Loudoun County Sheriff’s Office spokesperson Leah Paul said Monday that police responded to a report of a shooting at a home located on the 20000 block of Northpark Drive in Ashburn, Virginia, at 7:32 p.m. Eastern time on Sunday. Deputies who responded found an adult woman suffering from multiple gunshot wounds, and she was taken to a nearby hospital with serious injuries.

The home is located in Ashburn, Virginia, near Washington, D.C., in an area close to the Washington Commanders’ practice facility, where Bieniemy previously served as offensive coordinator.

Bieniemy Was at Training Camp When Shooting Occurred

Eric Bieniemy left the Chiefs’ training camp and was not in attendance for Monday’s practice. He had been with the Chiefs on Sunday in St. Joseph, Missouri, at the campus of Missouri Western State University for the team’s second practice of training camp, when the shooting occurred hundreds of miles away at his family’s Virginia home.

Bieniemy was with the Chiefs for training camp in Missouri when his wife was reportedly shot at their Virginia home.

Team Confirms Awareness, Offers Few Details

The Chiefs said in a statement they are “aware of the incident involving Eric Bieniemy’s family,” but did not provide further details. The team has not indicated whether Bieniemy plans to return to training camp or take any leave of absence while the situation unfolds.

A Long Coaching Career Across the League

Bieniemy’s coaching career has spanned some of the most notable stretches in recent NFL history. He has long been regarded as one of the best assistant coaches in the league, having served as the Chiefs’ running backs coach from 2013 through 2017 before taking over as offensive coordinator from 2018 through 2022, a period that coincided with the emergence of quarterback Patrick Mahomes and two of the franchise’s Super Bowl championships.

After that run in Kansas City, Bieniemy spent the 2023 season with the Washington Commanders before serving as UCLA’s offensive coordinator in 2024. He then joined Chicago Bears head coach Ben Johnson’s staff, where he was instrumental in helping the team finish third in the league in rushing last season. He returned to the Chiefs as offensive coordinator this year after Kansas City parted ways with former Bears coach Matt Nagy.

Bieniemy rejoined the Chiefs earlier this year as their offensive coordinator, a position he previously held from 2018 to 2022.

Family Ties to the Region

The location of Sunday’s shooting adds a notable layer to the story given Bieniemy’s coaching history in the Washington, D.C., area. His stint as the Commanders’ offensive coordinator under head coach Ron Rivera in 2023 placed him in the same region where his family’s home is located, near the team’s practice facility in Ashburn.

What Comes Next

As of Monday, authorities had not released additional details about what led to the shooting, and the Loudoun County Sheriff’s Office had not commented further beyond confirming the location, timing and charges against Elijah Bieniemy. Mia Bieniemy remained hospitalized in stable condition, according to sources cited by multiple outlets, though her exact prognosis and expected recovery timeline had not been publicly disclosed.

The Chiefs are in the midst of training camp as they prepare for the upcoming NFL season, and it remains unclear how the situation involving Bieniemy’s family will affect his participation in camp in the coming days. The team’s brief statement acknowledging awareness of the incident suggests further details may be forthcoming as the situation develops, though the organization has so far declined to elaborate beyond confirming it is aware of what happened.

This is a developing story, and additional details are expected to emerge as the investigation into the shooting continues and as Mia Bieniemy’s condition is further updated by medical officials or family representatives.

MapLight Therapeutics’ Lead Candidate Falls Meaningfully Short In Schizophrenia (MPLT)

Securitize Registers as SEC Investment Adviser Through Capital Unit

Nic Vansteenberghe Breaks Silence On Olandria Carthen Split

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

FINANCIAL FUTURE: STARTING. YOUR BUSINESS, GOVERNMENT WORK OR CORPORATE

This is for educational purposes only, not financial advice #cryptocurrency #tradingtips #market

Has your account ever been debited with NO Credit alert? #BankingXperience #Finance #bank #shorts

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat6 days ago

NewsBeat6 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech20 hours ago

Tech20 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Tech7 days ago

Tech7 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech7 days ago

Tech7 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics10 hours ago

Politics10 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

NewsBeat7 days ago

NewsBeat7 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Sports24 hours ago

Sports24 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

Politics1 day ago

Politics1 day agoSpain sweeps the board at 2026 World Cup with individual awards

-

Crypto World7 days ago

Crypto World7 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

-

Entertainment3 days ago

Entertainment3 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos24 hours ago

News Videos24 hours agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

You must be logged in to post a comment Login