Up to US$600 million of shares to be repurchased pursuant to amended normal course issuer bid

US$605 million return of capital and share consolidation expected to be completed in May

TORONTO, Feb. 25, 2026 /PRNewswire/ — Thomson Reuters (TSX/Nasdaq: TRI) today announced that it plans to repurchase up to US$600 million of its common shares under an amended normal course issuer bid (NCIB) that has been approved by the Toronto Stock Exchange (TSX) and that it plans to return US$605 million to shareholders through a return of capital transaction.

Amended Normal Course Issuer Bid

Advertisement

Shares will be repurchased for the new US$600 million repurchase program under an amended NCIB. The amended NCIB, which has been accepted by the TSX, will become effective on February 27, 2026. The amended NCIB will increase the maximum number of common shares that may be repurchased by an additional 6 million. Under the amended NCIB, up to 16 million common shares (representing approximately 3.55% of the company’s 450,687,724 issued and outstanding shares as of August 12, 2025) may be repurchased between August 19, 2025 (the Effective Date) and August 18, 2026. The NCIB, as originally approved in August 2025, contemplated the repurchase of up to 10 million common shares. To date under the current NCIB, Thomson Reuters has repurchased 6,022,437 common shares for a total cost of approximately US$1.0 billion, representing an average price of US$166.05 per share.

Under the amended NCIB, shares may be repurchased on the TSX, the Nasdaq Global Select Market (Nasdaq) and/or other exchanges and alternative trading systems or by such other means as may be permitted by the TSX and/or the Nasdaq or under applicable law. Based on the average daily trading volume on the TSX of 364,105 for the six months preceding the Effective Date (net of repurchases made by TR during that time period), daily purchases are limited to 91,026 common shares, other than block purchase exceptions. Any shares that are repurchased will be cancelled.

Prior to its next regularly scheduled quarterly blackout period, Thomson Reuters intends to enter into an automatic share purchase plan (ASPP) with its broker to allow for the purchase of shares under the NCIB during pre-determined times when the company would ordinarily not be permitted to purchase shares due to customary blackout periods or other regulatory restrictions. Purchases under the ASPP are made by the company’s broker based upon parameters set by Thomson Reuters when it is not in possession of material non-public information relating to the company or the shares. The ASPP will be entered into in accordance with the requirements of the TSX and applicable Canadian and U.S. securities laws, including Rule 10b5- 1 under the U.S. Exchange Act of 1934, and will terminate when the NCIB expires, unless terminated earlier in accordance with its terms. All purchases made under the ASPP are included in computing the number of shares purchased under the NCIB. Outside of pre-determined blackout periods, shares may be purchased under the NCIB based on management’s discretion, in compliance with TSX rules and applicable securities laws.

Decisions regarding any future share repurchases will depend on certain factors, such as market conditions, share price and other opportunities to invest capital for growth. Thomson Reuters may elect to suspend or discontinue share repurchases at any time, in accordance with applicable laws.

Advertisement

Return of Capital

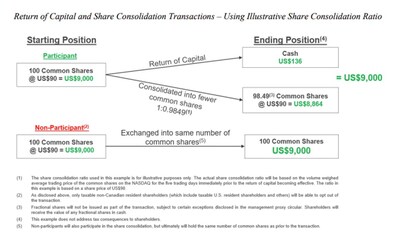

Thomson Reuters will return gross proceeds derived from the May 2024 sales of London Stock Exchange Group shares through a return of capital consisting of a special cash distribution of US$605 million in the aggregate, or approximately US$1.36 in cash per participating share (estimated based on the number of common shares issued and outstanding as of February 24, 2026 and assuming no shareholders opt-out of the return of capital transaction), followed by a share consolidation, or “reverse stock split”, which will reduce the number of common shares on a basis that is proportional to the special cash distribution. To that end, the share consolidation ratio will be based on the volume weighed average trading price of the common shares on the Nasdaq Stock Market LLC for the five trading days immediately prior to the transactions becoming effective.

The proposed return of capital is intended to distribute cash on a basis that is generally expected to be tax-free for Canadian tax purposes. Taxable non-Canadian resident shareholders (which include taxable U.S. resident shareholders and others) will be able to opt out of the return of capital. This right to opt out is being provided to those shareholders because in jurisdictions other than Canada the tax consequences of not participating in the return of capital may be preferable to those associated with participating in the return of capital. A taxable non-Canadian resident shareholder that chooses to opt out will not receive the special cash distribution and will continue to hold the same number of Thomson Reuters shares that they currently hold. Taxable non-Canadian resident shareholders are strongly urged to read the management proxy circular and other related materials carefully and to consult with their financial, tax and legal advisors prior to making any decision with respect to the return of capital and share consolidation transactions.

Advertisement

Shareholders will be asked to approve the proposed return of capital and share consolidation transactions at a special meeting of shareholders of Thomson Reuters to be held on Tuesday, April 28, 2026 at 12:00 p.m. (Toronto time). The proposed transactions require approval by at least two-thirds of the votes cast at the shareholder meeting. The board of directors of the company is unanimously recommending that shareholders vote in favor. Woodbridge has indicated that it plans to do so and, accordingly, it is expected that the shareholder vote will pass. The proposed transactions also require the approval of the Ontario Superior Court of Justice (Commercial List). If shareholder and court approval are obtained, Thomson Reuters expects to effect the proposed transactions in early May.

Full details of the proposed return of capital and share consolidation transactions will be described in the company’s management proxy circular and other related materials. Those documents are expected to be mailed or otherwise distributed to shareholders, filed with applicable Canadian securities regulatory authorities and made available without charge on SEDAR+ at www.sedarplus.ca and made available without charge on EDGAR at www.sec.gov, and posted on the company’s website at tr.com, in mid-March.

Thomson Reuters Thomson Reuters (TSX/Nasdaq: TRI) informs the way forward by bringing together the trusted content and technology that people and organizations need to make the right decisions. The company serves professionals across legal, tax, audit, accounting, compliance, government, and media. Its products combine highly specialized software and insights to empower professionals with the data, intelligence, and solutions needed to make informed decisions, and to help institutions in their pursuit of justice, truth and transparency. Reuters, part of Thomson Reuters, is a world leading provider of trusted journalism and news. For more information, visit tr.com.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Advertisement

Certain statements in this news release are forward-looking statements within the meaning of Canadian and U.S. securities laws, including statements relating to the company’s plans to repurchase up to US$600 million of its common shares; the timing for the approval and implementation of the return of capital and share consolidation transactions, and the filing of materials related thereto; and the anticipated tax treatment for shareholders participating in the return of capital and share consolidation transactions and those opting out of the return of capital. These forward-looking statements are based on certain assumptions and reflect our company’s current expectations. As a result, forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations, including other factors discussed in materials that Thomson Reuters from time to time files with, or furnishes to, the Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission. There is no assurance that the return of capital and share consolidation transactions will be completed or that other events described in any forward-looking statement will materialize. Except as may be required by applicable law, Thomson Reuters disclaims any obligation to update or revise any forward-looking statements.

Rachel Reeves has been told by one of the world’s most influential economic bodies that Britain’s tax system is holding the country back and needs urgent surgery if the Chancellor is serious about reigniting growth.

In a pointed intervention, the Organisation for Economic Co-operation and Development (OECD) has urged the Treasury to launch an “in-depth tax review to make the tax system more efficient and growth-friendly”, arguing that decades of tinkering have left Britain with a patchwork of distortions, loopholes and outdated valuations that penalise enterprise and deter investment.

The Paris-based think tank’s latest assessment will make uncomfortable reading in Downing Street. It concludes that the UK economy is being dragged down not only by the familiar headwinds of elevated borrowing costs and sluggish productivity, but by a tax code that businesses have learned to game and that ordinary taxpayers increasingly struggle to understand.

At the heart of the OECD’s recommendations is a call to broaden the VAT base, stripping out a thicket of reliefs and exemptions that economists describe as “largely inefficient and regressive”. It is the sort of reform that could finally consign to history the long-running absurdity of HMRC having to rule on whether a Jaffa Cake is a biscuit or a cake, the kind of grey area that has generated decades of tribunal cases and column inches. The OECD suggests that any additional receipts raised by closing such loopholes could be recycled to shield low-income households through targeted transfers.

Property tax comes in for similarly sharp criticism. The OECD notes that council tax bands still rest on property valuations taken in 1991, a state of affairs no government has dared to touch for fear of triggering a political backlash among homeowners whose rateable values no longer reflect the modern housing market. Successive chancellors have kicked the revaluation can down the road, leaving a levy that economists regard as one of the most distortive in the developed world.

Advertisement

For small and medium-sized businesses, the case for reform has long been obvious. Entrepreneurs, accountants and owner-managers have complained for years about the sheer complexity of the HMRC code, the punitive £100,000 to £125,000 tax trap that penalises aspiration, the interaction of income tax with student loan repayments, and the cliff edges that plague stamp duty. Each has become a case study in how good intentions, bolted on year after year, can produce a system nobody would design from scratch.

Britain once had a body specifically charged with addressing these frustrations. The Office of Tax Simplification, an arms-length outfit set up to cut administrative burdens, survived for 13 years before being abolished by Kwasi Kwarteng during his short-lived tenure as Chancellor. Its recommendations were frequently ignored even while it existed, and its closure was widely seen at the time as a signal that Whitehall had lost interest in serious structural reform.

The OECD’s warning lands at an awkward moment for Reeves. Several think tanks, including the Institute for Government, urged the Chancellor to pursue wholesale tax reform ahead of last year’s Budget, when she was scrambling to fill a fiscal black hole running into billions. She now faces similar pressures later this year, with the war in Iran weighing on global growth, interest rates stubbornly elevated and borrowing costs showing little sign of easing.

The report also strays into more politically charged territory, criticising the government over conflicts of interest in its dealings with business — a swipe that will inevitably be read in Westminster as a reference to the recent controversies surrounding Lord Mandelson and Labour Together, as well as the steady stream of former MPs moving into private sector roles that have raised eyebrows on both sides of the House. The OECD recommends that legally binding commitments on violations be extended to cover politicians’ post-public careers as well as their periods in office.

Advertisement

Among its other prescriptions, the think tank calls for a rethink of employee training subsidies funded through the apprenticeship levy, suggesting resources be redirected towards young people who are struggling to get a foothold in the labour market.

Responding to the report, a Treasury spokesperson said the government was “already reforming the tax system to make it more efficient, modern and fair”, adding that it was “tackling reliefs that are now costing far more than intended and are disproportionately benefitting the wealthy”.

Whether that amounts to the kind of root-and-branch overhaul the OECD is demanding, or simply more of the piecemeal tinkering that has brought the system to its current state, will become clearer when Reeves stands up at the despatch box later this year. For Britain’s SMEs, who bear a disproportionate share of the compliance burden, the hope will be that she finally grasps the nettle.

Jamie Young

Jamie is Senior Reporter at Business Matters, bringing over a decade of experience in UK SME business reporting.

Jamie holds a degree in Business Administration and regularly participates in industry conferences and workshops.

When not reporting on the latest business developments, Jamie is passionate about mentoring up-and-coming journalists and entrepreneurs to inspire the next generation of business leaders.

NEW YORK — Ivanhoe Electric Inc. shares rose sharply in morning trading Friday, gaining about 7.77% to $13.87 as investors bet on the company’s role in bolstering domestic supplies of copper and other critical minerals amid growing demand from electrification, data centers and national security initiatives.

Ivanhoe Electric

The Phoenix-based exploration and development firm, listed on the NYSE American as IE, added $1.00 by 10:00 a.m. EDT. The move came as broader sentiment toward copper-related stocks improved and the company continued to highlight progress at its flagship Santa Cruz Copper Project in Arizona, along with a strengthened balance sheet from recent cash inflows.

Ivanhoe Electric specializes in using its proprietary Typhoon™ geophysical surveying technology — paired with advanced data analytics from its majority-owned subsidiary Computational Geosciences Inc. — to detect deeply buried mineral deposits that traditional methods often miss. The system generates powerful electrical signals capable of penetrating up to 1.5 kilometers or more, accelerating discovery while reducing exploration risks and costs.

The company’s portfolio centers on copper but also includes nickel, cobalt and other metals essential for batteries, renewables and high-tech applications. Its core asset is the Santa Cruz Copper Project near Casa Grande, Arizona, where it aims to build a modern underground mine and heap-leach facility to produce high-purity 99.99% copper cathode domestically.

A preliminary feasibility study released in mid-2025 outlined strong economics for the project: an underground operation processing 20,000 tonnes per day, with average annual production of approximately 72,000 tonnes of copper cathode in the first 15 years at low all-in sustaining costs around $1.36 per pound after by-product credits. The study supports a potential 23-year mine life, with initial construction targeted for the first half of 2026 and first cathode production by late 2028, subject to permits and financing.

Advertisement

In November 2025, Ivanhoe Electric completed final land acquisition payments totaling $39.3 million, clearing a key hurdle ahead of major construction activities. The project sits on private land, which is expected to streamline permitting compared to federal ground. The company has already secured various permits for exploration and land use, positioning it for a smoother development path in a state with a long mining history.

Financially, Ivanhoe Electric entered 2026 with solid liquidity. As of Dec. 31, 2025, it held $173.3 million in cash and equivalents. In February 2026, it received $82.6 million from the exercise of warrants tied to a prior equity financing. In March, the company stood to receive approximately $58.4 million from its 59.6%-owned subsidiary Cordoba Minerals Corp., stemming from Cordoba’s $128 million sale of its remaining interest in the Alacrán Project in Colombia. The cash distribution of $1.01 per Cordoba share was payable around late March.

An undrawn $200 million senior secured bridge facility, closed in December 2025, provides additional near-term flexibility as the company pursues longer-term project financing for Santa Cruz. Ivanhoe Electric received a Letter of Interest from the U.S. Export-Import Bank in 2025 for up to $825 million in debt financing under the Make More in America initiative, with the full application process ongoing. Executives have signaled expectations to finalize project financing by mid-2026.

The stock’s Friday gain built on recent volatility. Shares had traded around $12.87 at Thursday’s close after pulling back from earlier 2026 levels, with a 52-week range spanning roughly $4.50 to $21.55. Analysts maintain a generally bullish outlook, with consensus price targets near $18 to $21.50 and some high-end forecasts reaching $28.50. JPMorgan recently reaffirmed its overweight rating, though it trimmed its target slightly to $21.

Advertisement

A key differentiator for Ivanhoe Electric is its Typhoon™ technology, which has already shown promise in joint ventures and alliances. In January 2026, the company signed a collaboration agreement with Sociedad Química y Minera de Chile (SQM) to explore 2,002 square kilometers of mining concessions in northern Chile for copper deposits hidden beneath electrically resistive caliche layers. SQM is funding an initial $9 million program, with Ivanhoe Electric supplying a new-generation Typhoon system and advanced inversion software. The deal includes options for joint ventures on discoveries.

In Saudi Arabia, Ivanhoe Electric operates a 50/50 joint venture with Maaden covering about 50,000 square kilometers of the underexplored Arabian Shield. Three Typhoon systems are active there, and early drilling at the Umm Ad Dabah prospect intersected encouraging copper mineralization. Additional surveying and drilling continue across multiple targets.

The company also maintains an exploration alliance with BHP in the southwestern United States, where BHP funds initial work and Ivanhoe Electric acts as operator during the exploration phase. Typhoon surveys have been completed in areas of interest in Arizona and Utah, with drilling underway targeting porphyry copper systems.

Other U.S. assets include the Hog Heaven project in Montana, where expansion drilling has intersected significant copper-gold-silver mineralization and a new porphyry system called Battle Butte was identified, and the Tintic project in Utah, focused on precious and base metals in a historic district.

Advertisement

Executive Chairman Robert Friedland, a prominent figure in the mining industry, has emphasized the strategic importance of domestic critical minerals production. In February 2026, he joined President Donald J. Trump at the White House for the announcement of a $12 billion U.S. minerals stockpile initiative, underscoring Ivanhoe Electric’s alignment with national efforts to reduce reliance on foreign supplies.

The broader copper market provides tailwinds. Analysts forecast structural deficits driven by surging demand from electric vehicles, artificial intelligence data centers, renewable energy infrastructure and grid modernization. Some projections see copper prices potentially climbing significantly if supply lags, benefiting developers like Ivanhoe Electric with high-quality, low-cost projects in stable jurisdictions.

Challenges persist. As a development-stage company, Ivanhoe Electric reports operating losses — posting a net loss of about $105.9 million for 2025 — while investing heavily in exploration and project advancement. Quarterly revenues remain modest, primarily from limited early-stage activities. Permitting timelines, construction execution and final financing terms will be critical to meeting the aggressive Santa Cruz schedule.

The company faces typical mining risks, including commodity price volatility, geopolitical factors affecting global supply chains and potential delays in regulatory approvals. However, its focus on private land in Arizona and access to advanced technology are seen as mitigating factors.

Advertisement

With Q1 2026 financial results scheduled for release in early May, investors will watch for updates on cash usage, exploration results and any progress on Santa Cruz permitting or financing. Management has highlighted a disciplined approach to capital allocation, balancing aggressive exploration with de-risking the flagship project.

Founded with a vision to revive and modernize mineral exploration through technology, Ivanhoe Electric has assembled a portfolio that spans high-potential development assets and early-stage discovery opportunities across multiple continents. Its dual listing on the NYSE American and TSX broadens its investor reach.

Friday’s trading volume appeared elevated as the stock tested recent resistance levels. Technical observers noted the potential for continued momentum if copper prices hold firm and positive news flows from exploration or financing emerge.

As global industries race to secure critical metals for the energy transition and technological advancement, Ivanhoe Electric positions itself at the intersection of innovation, domestic production and strategic partnerships. Success at Santa Cruz could mark a significant step toward establishing new U.S. copper cathode capacity, while Typhoon-driven discoveries elsewhere offer upside potential.

Advertisement

Analysts and industry watchers will continue monitoring execution on the 2026 construction timeline and international exploration programs. For a company blending cutting-edge geophysics with real-world development ambitions, the coming months could prove pivotal in determining whether it delivers on its promise as a key player in the critical minerals supply chain.

Weardale Lithium is hoping to extract the key material from brines under the North Pennines

Weardale Lithium has secured planning permission to build its lithium extraction facility at the former Eastgate cement works.(Image: Weardale Lithium)

A bid to extract the key material of lithium from the ground beneath the North East has received a boost from the Government.

Weardale Lithium has secured grant funding through the Government’s DRIVE35 Scale-Up: Feasibility Studies competition, supporting the next phase of development at its geothermal lithium project in County Durham. The project aims to produce battery-grade lithium carbonate – a key material for the UK’s net zero ambitions – from geothermal groundwaters under the North Pennines, and could create between 20 and 50 jobs.

The grant funding will enable Weardale Lithium to undertake a £700,000 feasibility study to map its geothermal lithium-bearing brinefield within the North Pennine Orefield. The feasibility study represents an important step towards establishing a domestic source of battery-grade lithium carbonate, reducing reliance on imported raw materials and strengthening the resilience of the UK’s EV manufacturing base.

Stewart Dickson, CEO of Weardale Lithium, said: “Securing support through the DRIVE35 Scale-Up programme is an important milestone for Weardale Lithium and for the development of a secure, domestic lithium supply in the UK. This funding enables us to undertake critical subsurface mapping and technical analysis of our geothermal brine resource in County Durham, providing the data needed to inform commercial scale-up and future investment decisions.

Advertisement

Stewart Dickson, CEO of Weardale Lithium(Image: Weardale Lithium)

“Our project aligns directly with the UK Critical Minerals Strategy and wider UK Battery Strategy. By developing low-carbon Direct Lithium Extraction integrated with on-site conversion to battery-grade lithium carbonate, we are positioning the North East at the forefront of the UK’s emerging

battery materials supply chain while creating high-value jobs and long-term economic benefits for the region.”

The grant to Weardale Lithium – which has planning permission for an extraction facility at Eastgate – is part of a wider investment package into the UK automotive industry.

Ian Constance, CEO of Advanced Propulsion Centre UK, said: “The projects announced today demonstrate the UK’s determination to lead the shift to zero-emission mobility. By facilitating the UK Government’s DRIVE35 grants, we are turning world-class innovation into industrial capability. With our partners in DBT and Innovate UK, we are backing manufacturers, empowering SMEs, and strengthening the UK’s sovereign supply chain.

Advertisement

“This multi-million pound support package is more than an investment in technology; it is an investment in the people, skills, and companies that will define the future of clean transport. Together, we are building the foundations of a competitive, resilient, and sustainable automotive industry.”

Fox News chief national security correspondent Jennifer Griffin reports on the state of Strait of Hormuz traffic, Irans demand for a toll on passing ships and ceasefire negotiations on Varney & Co.

This story on the March 2026 CPI inflation report is developing and will be updated with further details.

Inflation surged in March as consumer prices jumped amid the economic disruptions caused by the Iran war’s impact on the energy market.

Advertisement

The Bureau of Labor Statistics on Friday said that the consumer price index (CPI) – a broad measure of how much everyday goods like gasoline, groceries and rent cost – rose 0.9% from a month ago and is 3.3% higher than last year. The annual figure jumped from last month’s 2.4% reading, while the monthly increase also rose markedly from last month’s 0.3% reading.

Expectations vs. reality

Both the 0.9% monthly increase and 3.3% annual rise were in line with the expectations of economists polled by LSEG.

So-called core prices, which exclude volatile measurements of gasoline and food to better assess price growth trends, were up 0.2% on a monthly basis and 2.6% from a year ago. Both of those figures were slightly cooler than economists’ predictions of 0.3% and 2.7%, respectively.

The core CPI figures were slightly hotter than February’s readings, which showed prices rose 0.2% on a monthly basis and 2.5% from the prior year.

Advertisement

Economists have noted that inflation data from December 2025 through April 2026 will be affected due to data collection interruptions resulting from last fall’s 43-day government shutdown.

During the shutdown, the BLS wasn’t able to gather data and used a carry-forward methodology to make up for the lack of an October CPI report and missing data in November’s report. Economists say this is likely to impart a downward bias on inflation data until this spring, when fresh data will negate the discrepancy.

The cost of living breakdown

High inflation has created severe financial pressures in recent years for most U.S. households, which are forced to pay more for everyday necessities like food and rent. Price hikes are particularly difficult for lower-income Americans, because they tend to spend more of their already-stretched paychecks on necessities and have less flexibility to save.

Food prices were flat on a monthly basis in March, and were up 2.7% from a year ago. The food at home index declined 0.2% for the month and is up 1.9% over the last year, while the food away from home index is 3.8% higher than a year ago after a 0.2% increase on a monthly basis.

Advertisement

Meats, poultry and fish prices were down 0.5% for the month but remain 5.6% higher than a year ago. Beef and veal prices fell 0.6% in March and are 12.1% higher than last year. Egg prices continued to decline following an avian flu outbreak that impacted supply, with prices down 3.4% for the month and 44.7% from a year ago. The fruits and vegetables index rose 1% in March and is up 4% on an annual basis.

You must be logged in to post a comment Login