TORONTO, March 13, 2026 /PRNewswire/ — Thomson Reuters (TSX/Nasdaq: TRI) today filed its management proxy circular and related documents in connection with the upcoming special meeting at which shareholders will be asked to approve the proposed return of capital and share consolidation transactions, among other items. The management proxy circular and related documents are available online and for pick-up, as set out below.

The transactions consists of a special cash distribution of US$605 million in the aggregate, or approximately US$1.36 per common share (estimated based on the number of common shares issued and outstanding as of the record date and assuming no shareholders opt-out of the return of capital) followed by a consolidation of outstanding common shares (or “reverse stock split”) on a basis that is proportional to the special cash distribution. The share consolidation ratio will be based on the volume weighed average trading price of the common shares on the Nasdaq Stock Market LLC (“Nasdaq”) for the five trading days immediately prior to the return of capital becoming effective.

The proposed return of capital is intended to distribute cash on a basis that is generally expected to be tax-free for Canadian tax purposes. Shareholders who are taxable in a jurisdiction outside of Canada (including taxable U.S. resident shareholders and others) (“Eligible Opt-Out Shareholders”) will be able to opt out of the return of capital. This right to opt out is being provided to those shareholders because in jurisdictions other than Canada the tax consequences of not participating in the return of capital may be preferable to those associated with participating in the return of capital. If an Eligible Opt-Out Shareholder chooses to opt out, it will not receive the cash distribution and will continue to hold the same number of shares that it currently holds.

Details of the transaction (including information regarding the opt-out right) are described in the management proxy circular and related materials, which are available on thomsonreuters.com in the “Investor Relations” section. The documents were filed with the Canadian securities regulatory authorities on SEDAR+ and are available at www.sedarplus.com. The documents will also be furnished to the U.S. Securities and Exchange Commission through EDGAR and when filed, will be available at www.sec.gov. The documents will also be available for pick-up, free of charge, at Computershare Investor Services Inc.’s offices in Toronto, Montreal, Vancouver and Calgary. Please contact Computershare Investor Services Inc. using the phone numbers set out below for the addresses of those offices.

Advertisement

The special meeting of shareholders will be held on Tuesday, April 28, 2026 at 9:00 a.m. EDT (changed from the original planned time of 12:00 p.m.). The meeting will be a webcast on thomsonreuters.com in the “Investor Relations” section. Holders of Thomson Reuters common shares as of 5:00 p.m. EDT on March 6, 2026 are entitled to vote at the meeting.

Registered shareholders who have questions or need assistance voting their shares may contact Computershare Investor Services Inc. at 1.800.564.6253 (toll-free in Canada and the U.S.) or at 1.514.982.7555 (outside Canada and the U.S.). Non-registered shareholders who hold their shares indirectly through an intermediary (such as an investment dealer, stock broker, bank, trust company or other nominee) should contact their intermediary if they have questions or need assistance. Shareholders who have questions or need assistance may also contact D.F. King & Co., Inc., who is acting as Information Agent for the transaction, at 1.800.967.5068 (toll-free in Canada and the U.S.) or at 1.212.561.5870 (outside Canada and the U.S., banks, brokers and collect calls) or at the following email address: tri@dfking.com.

About Thomson Reuters

Thomson Reuters (TSX/Nasdaq: TRI) informs the way forward by bringing together the trusted content and technology that people and organizations need to make the right decisions. The company serves professionals across legal, tax, audit, accounting, compliance, government, and media. Its products combine highly specialized software and insights to empower professionals with the data, intelligence, and solutions needed to make informed decisions, and to help institutions in their pursuit of justice, truth and transparency. Reuters, part of Thomson Reuters, is the world’s leading provider of trusted journalism and news. For more information, visit thomsonreuters.com.

Advertisement

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this news release are forward-lookingwithin the meaning of applicable Canadian and U.S. securities laws, including the Private Securities Litigation Reform Act of 1995. These statements relating to the return of capital and share consolidation transactions and the anticipated tax treatment for shareholders participating in the return of capital and those opting out. These forward-looking statements are based on certain assumptions, including shareholder approval of the transactions, and reflect our company’s current expectations. As a result, forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations, including the risk factors discussed in materials that Thomson Reuters from time to time files with, or furnishes to, the Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission. There is no assurance that the return of capital and share consolidation transactions will be completed or that other events described in any forward-looking statement will materialize. Except as may be required by applicable law, Thomson Reuters disclaims any obligation to update or revise any forward-looking statements.

KLA Corporation (KLAC) Analyst/Investor Day March 12, 2026 9:00 AM EDT

Company Participants

Bren Higgins – Executive VP & CFO Richard Wallace – President, CEO & Executive Director Ahmad Khan – President of Semiconductor Products & Customers Brian Lorig – Executive Vice President of KLA Global Services

Conference Call Participants

Advertisement

Atif Malik – Citigroup Inc., Research Division Stacy Rasgon – Bernstein Institutional Services LLC, Research Division Joseph Quatrochi – Wells Fargo Securities, LLC, Research Division Christopher Caso – Wolfe Research, LLC Harlan Sur – JPMorgan Chase & Co, Research Division Sreekrishnan Sankarnarayanan – TD Cowen, Research Division Vivek Arya – BofA Securities, Research Division Christopher Muse – Cantor Fitzgerald & Co., Research Division Shane Brett – Morgan Stanley, Research Division Yu Shi – Needham & Company, LLC, Research Division Melissa Weathers – Deutsche Bank AG, Research Division

Presentation

Unknown Attendee

Advertisement

Please welcome KLA EVP, CFO and Global Operations, Bren Higgins.

Bren Higgins Executive VP & CFO

Good morning. Thank you for being here for our 2026 KLA Investor Day. It’s great to be back in New York. I’m going to make a few comments. First, I’m going to walk through the agenda overall. So I’ll make a few comments, and then I’ll transition to our President and CEO, Rick Wallace, who will talk about compounding sustainable outperformance of the company, where we’ve been and where we’re going, some of the dynamics that are driving the ecosystem and how that plays through to opportunities for KLA relevance.

Advertisement

Ahmad Khan, who’s the President of our Semiconductor Products and Customers business, will then stand up and talk about process control in the AI era, some of the dynamics that are driving our business, how we’re collaborating and engaging with customers that drives our innovation model and ultimately, how we execute. And our strategy is to take advantage of what looks like a very exciting business environment moving forward.

As grain farmers prepare for spring planting, any optimism for the coming season is being tempered by the economic reality that they may face another money-losing year. This was looking to be the case even before the conflict began in Iran, which triggered a surge in fertilizer prices.

Input costs skyrocketed in 2022 after the start of the Russia-Ukraine war and remain elevated, while commodity prices sit under production costs. The American Farm Bureau says many row-crop farmers are looking at four or five straight years of operational losses, even after accounting for crop insurance payments and ad-hoc assistance.

Advertisement

Philip Nelson, a fourth-generation farmer in LaSalle County, Illinois, who was recently elected as Illinois Farm Bureau president, says the profits farmers made when crop prices were high a few years ago have eroded and balance sheets are tight.

“If you adjust for inflation, we’ve got the same commodity prices we had in 1974, and at the same time, the input costs have quadrupled,” Nelson says.

Input costs aren’t the only issue clouding farmers’ outlooks for spring planting. Last year, the U.S. harvested a record corn crop of roughly 18 billion bushels, and that heavy supply continues to weigh on the market, says Sean Lusk, vice president, commercial hedging division for Walsh Trading. In addition, the outlook for soybeans remains mixed as farmers wait on the Trump administration to decide on a potential expansion of the biomass-based diesel program that could offset some of the lost export market share to China amid recent trade tensions.

In a challenging year, risk management tools and fine-tuning marketing plans take on added importance.

Advertisement

Shifting Farmer Sentiment

The Purdue University-CME Group Ag Economy Barometer weakened in December, reflecting farmers’ declining long-term outlook about U.S. soybean export prospects as competition from Brazil increases. More recently, the focus has shifted to tensions between current conditions and future expectations, with farmers more optimistic about the former than the latter.

The U.S. Department of Agriculture’s (USDA) Economic Research Service forecasts net farm income to fall by 2.6% year-over-year in inflation-adjusted terms. The decline is mitigated in part by the Farmer Bridge Assistance Program and the Emergency Commodity Assistance Program, USDA’s aid packages for farmers to offset losses because of the trade environment. However, the American Farm Bureau says most producers likely will still lose money.

University of Illinois agricultural researchers forecast crop prices to be marginally higher in 2026. As of early March, CME Group September 2026 Corn and Soybean futures are trading around $4.55 and $11.32 per bushel, respectively.

Price gains compared to last year will likely be offset by small increases in overall costs with yields at trend levels. Break-even prices to cover all costs without government support are in the $4.70-$4.90 range for corn and $10.80-$11.25 range for soybeans, close to or above current market prices and pricing opportunities for the 2026 crop.

Advertisement

David Iserman, a fifth-generation farmer based in Streator, Illinois, is sanguine about the growing season, based on those figures. “We’re definitely either breaking even, if we’re lucky, or losing money,” he says.

Cost-Cutting Measures

Annual inputs, such as seed, fertilizer and chemicals, are higher than last year. Corn consumes more inputs than soybeans, and that may factor into what U.S. farmers plant this spring – though markets won’t know for sure until the 2026 Prospective Plantings report is released on March 31. However, many farmers typically still stick with a traditional 50/50 corn and soybean rotation for agronomic reasons, which is what Iserman and Nelson plan to do.

Both producers have experienced lean times before and are looking at ways to cut costs. Iserman says fertilizer is his number one cost. He practices no-till farming on his soybeans and strip-till for corn. In strip-till farming, producers till a narrow strip of soil for fertilizer on the corn, which minimizes loss.

Iserman may tweak how much he uses and is studying the cost, using software to gauge his returns on his fertilizer use.

Advertisement

“We’re looking at all of our fertilizer inputs from the standpoint of not yield, but profit. For every dollar I put in, I want to get $1 back. I don’t care about winning a yield contest. I care about return,” he says.

Nelson also says he might cut back slightly on fertilizer use because he has built it up in the soil, giving him an option to cut costs.

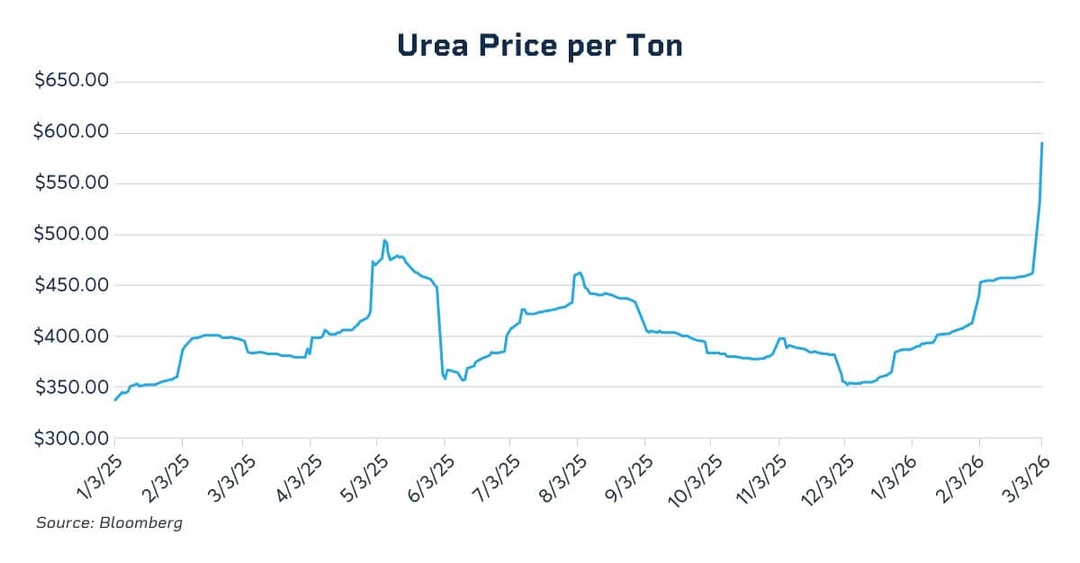

Fertilizer Prices Stay High

Fertilizer remains the most volatile and significant non-land cost, often accounting for 20% to 30% of total production expenses, according to USDA data.

Josh Linville, vice president of fertilizer at StoneX, says prices remain significantly higher than a year ago. In early 2026, a barge of urea at the port of New Orleans traded around $450 per ton, compared to $389 per ton in early 2025. Nitrogen prices are also higher versus a year ago.

Advertisement

Three global factors drive this inflation, Linville says. China, a major global supplier, has indicated it may not export urea until August 2026, removing millions of tons from the global market. In Europe, persistent high natural gas costs have limited nitrogen production to about 75% of normal since the second half of 2022 because of the Russia-Ukraine war. In the Middle East, the Strait of Hormuz is a critical choke point through which three of the top 10 urea exporters must ship their product. As of early March, the Strait of Hormuz is facing a blockade.

To better understand fertilizer costs, some farmers look at the corn-urea and soybean-urea ratio. These ratios position fertilizer costs within the context of crop costs, calculating how many bushels of grain are required to purchase one ton of nutrients.

A lower ratio signals a more favorable time to lock in costs. Currently, with low corn prices and high urea prices, the corn-urea ratio sits near 87 to 90 bushels per ton, a five-year high. To manage this, some farmers are using CME Group’s 10-Ton Urea U.S. Gulf futures contract. Launched last year, this tool allows individual producers to hedge their fertilizer risk in increments more suited to their actual field needs, and options can help limit price risk to the upside. While fertilizer costs were elevated in January, those levels now appear relatively attractive by comparison.

A Changing Approach

“Frankly speaking, we don’t sell all of our grain in one decision. We should be looking at doing the same thing with fertilizer,” Linville says.

Advertisement

He notes that traditionally farmers have looked at their fertilizer purchases annually, but watching prices throughout the year may help them make smarter operational decisions.

Farmers interested in adding the fertilizer ratios as part of their risk management toolkit can start by talking to their local grain elevator, which may give them data stretching back a few years to help them plot trends, he says. With this information, farmers may be able to act on price changes and lock in better prices.

Please welcome Vice President, Investor Relations, Mark Haden.

Mark Haden VP of Investor Relations

Advertisement

Well, good morning, everyone, and thank you for joining us today for Bunge’s Investor Day. We’re pleased to have you with us. I’m Mark Haden, Head of Investor Relations for Bunge.

Before I introduce our first presenter, I’d like to cover a few brief but important items. Today’s presentation includes forward-looking statements that reflect Bunge’s current views regarding future events, financial performance and industry conditions. These statements are subject to a number of risks and uncertainties that could cause actual results to differ materially. We encourage you to review the detailed discussion of these risk factors in our reports filed with the SEC.

Second, a brief safety and orientation reminder. In the event of emergency, please follow the posted exit signage here and then in the rear of the room and the instructions of on-site staff.

Let me now walk you through today’s agenda. Greg Heckman, our Chief Executive Officer, will begin with a company overview and strategy update. Julio Garros, our COO, will then discuss our operations and value chains. And

China, closely monitoring the escalating Middle East conflict, balances its interests while opposing foreign intervention, emphasizing risk mitigation over resolution due to its limited influence and strategic concerns.

Key Points

China observes the escalating Middle East conflict, prioritizing risk management over resolution, while opposing foreign intervention and tracking U.S.-Israeli actions affecting its interests.

Though physically distant at 4,200 miles, China finds itself in a strategically uncomfortable position regarding the U.S. campaign, which challenges its energy security and commercial goals.

Beijing’s muted response reflects its limited leverage and transactional relationship with Iran, emphasizing its opposition to regime change and its focus on preserving national sovereignty while preparing for potential escalation.

As the conflict in the Middle East intensifies, China adopts the role of a concerned observer, attempting to balance its strategic interests with a limited ability to influence events. Situated approximately 4,200 miles from the conflict, Beijing has more room to navigate the implications of the U.S.-Israeli military operations against Iran, which present a challenge to China’s energy security and economic ambitions in a region of crucial significance. The recent escalation is particularly discomforting for China, given that it represents the most substantial military engagement by its primary geopolitical rival, the United States, since the Iraq War.

China’s response has been notably restrained, reflecting its limited leverage over unfolding events and the transactional nature of its relations with Iran. Historically, China opposes foreign intervention, particularly actions like regime change that challenge national sovereignty—a principle that not only shapes its foreign policy but also resonates with its own territorial sensitivities. This fundamental stance underpinned China’s initial reactions to the conflict, as it joined Russia in requesting an emergency session of the United Nations Security Council shortly after the military escalation commenced. During this session, China expressed deep concern over the missile strikes, emphasizing the importance of respecting Iran’s territorial integrity and the need to cease hostilities.

Although Beijing publicly condemned the U.S.-Israeli strikes, its swift focus on risk mitigation suggests a prioritization of preparations for potential escalation over active conflict resolution. This duality underscores China’s dilemmas in responding to the volatile situation, where it must navigate its commitments to sovereignty while safeguarding its substantial economic interests in the region. As a result, China’s approach reflects a broader strategy centered on maintaining stability and controlling risks rather than directly engaging in mediation or seeking immediate resolutions. In essence, while China remains vocal against foreign intervention, its actions indicate a careful calculus aimed at minimizing potential fallout and preserving its interests amidst the upheaval in the Middle East.