Business

Unlocking Career Success with Gabriel Goldbrain: Your Gateway to Management Consulting

This is a post sponsored by Goldbrain SRL. Goldbrain offers the Goldbrain Success Training which intends to significantly increase graduates’ odds to break into tier 1 and tier 2 management consulting firms like McKinsey, BCG and Bain.

In the competitive landscape of management consulting, landing a position at top-tier firms like McKinsey, Bain, or BCG can be a daunting challenge, especially for freshly graduated students. Navigating the intricate interview processes and intense competition requires not just academic excellence but also strategic preparation and guidance. This is where Gabriel Goldbrain steps in, offering a unique and highly effective service tailored to help new graduates achieve their career aspirations in management consulting.

Gabriel Goldbrain specialises in coaching freshly graduated students to successfully apply to prestigious management consulting firms. Our comprehensive approach includes a variety of services, with our flagship program being the Success Training. This innovative program operates on a “only pay if you succeed” model, ensuring that our clients only invest financially when they secure their desired job offer. This commitment underscores our confidence in the effectiveness of our training and our dedication to our clients’ success.

The cornerstone of our offering is our unparalleled case interview training. Recognized as the best in the field, our case interview training program equips candidates with the essential skills and knowledge needed to excel in the rigorous case interview process used by top consulting firms. Our experienced coaches, many of whom have backgrounds in leading consulting firms, provide personalised mentorship and insights that go beyond generic preparation materials.

What sets Gabriel Goldbrain apart is our holistic approach to coaching. We understand that each candidate is unique, with distinct strengths and areas for improvement. Therefore, our training programs are customised to meet individual needs, ensuring that every candidate can maximise their potential. From mastering problem-solving techniques and developing strong analytical skills to enhancing communication and presentation abilities, our training covers all critical aspects necessary for success in management consulting interviews.

Moreover, our support extends beyond just case interviews. We assist our clients in every step of the application process, including resume and cover letter preparation, networking strategies, and interview coaching. Our goal is to build a robust foundation that not only helps candidates secure their first job in consulting but also equips them with skills and insights that will be valuable throughout their careers.

Joining Gabriel Goldbrain means becoming part of a community of ambitious and talented individuals who are committed to achieving excellence.

For those ready to take the first step towards a successful career in management consulting, Gabriel Goldbrain offers a transformative experience that combines expert coaching, personalised training, and a results-oriented approach. Our Success Training program’s “only pay if you succeed” model ensures that our interests are aligned with those of our clients, providing a risk-free opportunity to invest in your future.

Discover more about how Gabriel Goldbrain can help you achieve your career goals in management consulting by visiting our website at Gabriel Goldbrain’s case interview training. Embark on your journey to success with confidence, knowing that you have the best in the field guiding you every step of the way.

In a world where the right guidance can make all the difference, Gabriel Goldbrain stands out as a beacon of hope and opportunity for aspiring management consultants. Join us and transform your potential into a thriving career.

Goldbrain is independent and not associated in any way with the consulting firms mentioned and discussed in any of our social media content/video. We received no financing for creating our social media content unless and where we explicitly state otherwise.

Readers contacted BBC Your Voice to say they not been able to claim funds from dead family members’ premium bond investments.

Carnival earnings on deck: Fuel costs test cruise rebound

Co-op Group has confirmed that chief executive Shirine Khoury-Haq will step down, following mounting pressure over workplace culture concerns and a difficult year marked by losses and a damaging cyberattack.

Khoury-Haq, who has led the organisation since 2022 and spent seven years with the business, will be replaced on an interim basis by Kate Allum while the board begins the search for a permanent successor.

Her departure comes after reports of a “toxic culture” within senior leadership, alongside claims of falling morale, high-profile departures and operational challenges across the group.

The Co-op revealed that it swung to an underlying pre-tax loss of £126 million in its latest financial year, compared with a £45 million profit the previous year. Revenues also declined by 2.3 per cent to £11 billion, reflecting disruption to trading and changing consumer behaviour.

The group said the results were heavily shaped by its response to a major cyberattack, which forced it to restrict systems in an effort to contain the threat. While necessary, the measures had a significant commercial impact.

The company estimates the attack reduced revenues by £285 million and cut profitability by £107 million, including £86 million in lost margin and £21 million in additional costs.

The food division, the largest part of the business, was particularly affected, with sales falling 2 per cent to £7.25 billion. The disruption led to empty shelves in stores and altered shopping patterns, which continued to weigh on performance even after systems were restored.

Market share also slipped, falling to 5 per cent over a 12-week period, down from 5.3 per cent a year earlier, as the group lost ground to discounters and larger supermarket rivals.

Alongside the financial pressures, the organisation has faced scrutiny over its internal culture. A letter sent to board members, reportedly from senior staff, described an environment of “fear and alienation”, raising questions about leadership and decision-making at the top of the business.

The Co-op said it did not recognise those criticisms as representative of the wider organisation, emphasising its co-operative structure and commitment to inclusive decision-making. However, the reports have added to the challenges facing the group during a period of significant change.

Khoury-Haq said the timing of her departure reflects the next phase of the company’s transformation strategy.

“It has been an honour to lead our Co-op,” she said, adding that the business is now positioned to move forward with a programme of stabilisation and long-term reform that will extend beyond her planned tenure.

Her strategy had focused on rebuilding the group’s financial position, reducing debt and modernising its IT systems — issues that have been central to the Co-op’s operational challenges in recent years.

The company said she had overseen a significant turnaround between 2022 and 2024, including a 95 per cent reduction in debt and a 30 per cent increase in profits over that period, before the latest setbacks.

The Co-op, which employs around 54,000 people and operates more than 2,300 food stores and 800 funeral homes, continues to face intense competition across its core markets.

Discounters such as Aldi and Lidl have expanded aggressively, while established rivals including Tesco and Sainsbury’s have strengthened their positions, leaving the Co-op under pressure to differentiate its offering.

At the same time, the wider economic environment remains challenging, with inflation, shifting consumer behaviour and geopolitical uncertainty affecting demand.

Khoury-Haq acknowledged these headwinds, warning that “trading conditions remain difficult” and that external pressures are likely to persist.

The board now faces the task of appointing a new chief executive capable of navigating the next stage of the group’s recovery and transformation.

Group chair Debbie White thanked Khoury-Haq for her leadership during a turbulent period, particularly in guiding the organisation through the cyberattack and broader restructuring efforts.

For the Co-op, the leadership transition comes at a critical juncture. Restoring profitability, rebuilding trust internally and externally, and adapting to a rapidly evolving retail landscape will be central to its future.

As the organisation seeks to stabilise after a challenging year, the next phase of its strategy will be closely watched by both the market and its millions of members.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

Marwyn Value Investors partner transfers shares between accounts

GEELONG, Australia — The Geelong Cats held off a determined Adelaide Crows side to secure an eight-point victory in a rain-affected contest at GMHBA Stadium on Thursday night, improving to a strong start in the 2026 Toyota AFL Premiership season.

Geelong finished with 9.14 (68) to Adelaide’s 9.6 (60) in Round 3, snapping a potential slide after an undermanned Crows outfit mounted a spirited comeback but fell short in the dying stages. The win keeps the Cats in the mix early in the season while dealing Adelaide a second consecutive narrow loss.

Played in wet and slippery conditions typical of autumn evenings in Geelong, the match featured physical contests, costly penalties and several standout individual performances. Geelong’s greater efficiency in front of goal and ability to win key moments in the final quarter proved decisive.

Match Summary and Quarter-by-Quarter Breakdown

Geelong started strongly in the first quarter, capitalizing on two 50-metre penalties conceded by Adelaide’s Darcy Fogarty. Unlikely goal kicker Tom Stewart converted one from long range, marking just his seventh career major and giving the Cats an early momentum boost. Geelong led 28-14 at the first change after kicking four goals to Adelaide’s two.

Adelaide fought back in the second term, outscoring Geelong and narrowing the gap through slick transition play and individual brilliance. Luke Pedlar’s contested win on the wing set up Zac Taylor for a crucial goal, while Riley Thilthorpe was active around the ground. At halftime, Geelong held a slim advantage.

The third quarter saw both sides trade goals in a tight arm-wrestle. Adelaide briefly threatened to take control, but Geelong’s midfield responded with disciplined ball movement. The Cats entered the final change with a modest lead.

In the last quarter, Geelong steadied under pressure. Oliver Dempsey delivered a clutch goal to seal the result, while Jack Martin produced a moment of magic, gathering a wet football at pace to kick a vital major after an umpiring decision went against the Crows. Adelaide pushed hard late but could not bridge the gap, finishing with fewer scoring shots despite competitive possession numbers.

Key Performances and Statistics

Geelong’s midfield and defense stood tall in the greasy conditions. Mark Blicavs battled effectively in the ruck, while Sam Mannagh earned praise for a strong first-half contribution. Tom Stewart’s early goal and defensive reliability added value, and Oliver Dempsey’s composure late proved match-winning.

For Adelaide, the Crows were without key players including Jordan Dawson, Taylor Walker and Rory Laird, forcing coach Brad Scott to blood debutant Finnbar Maley from North Melbourne. Despite the absences, Zac Taylor and Luke Pedlar provided spark, and Darcy Fogarty remained a focal point up forward despite the early penalties.

Stats reflected a hard-fought contest: Adelaide edged total disposals slightly (around 750 to Geelong’s 742), but Geelong won more clearances (69-67) and tackles. Inside-50 entries were nearly even, yet Geelong’s accuracy in the wet proved superior with 14 behinds compared to Adelaide’s six.

Umpiring came under scrutiny, with one late non-call on a last-touch situation labelled a “farce” by some observers. Adelaide coach Brad Scott expressed frustration post-match over the slow start and several key decisions, while Geelong players celebrated a gritty four-point haul on the ladder.

Context and Implications

The match highlighted Geelong’s resilience at home, where they have historically been difficult to beat. GMHBA Stadium’s conditions favored the Cats’ experienced core, who adapted better to the slippery surface and capitalized on Adelaide’s errors.

For the Crows, the loss extends early-season challenges. Missing experienced leaders hurt their structure, particularly in stoppages and defensive transitions. Scott will likely demand a sharper opening quarter in future games, as Adelaide has now dropped two close encounters.

The result adds early intrigue to the 2026 season. Geelong demonstrated they remain competitive despite roster evolution, while Adelaide showed fight but must address injury concerns and execution under pressure.

Broader AFL talking points included the impact of wet-weather football on scoring and the growing conversation around umpiring consistency. Fans and commentators debated the balance between physicality and rule enforcement in slippery conditions.

Notable Moments from the Highlights

- Darcy Fogarty’s two first-quarter 50-metre penalties gifted Geelong easy scores and set an early tone.

- Tom Stewart’s long-range goal from the penalty provided an unlikely highlight.

- Luke Pedlar’s wing contest and Zac Taylor’s resulting goal showcased Adelaide’s counter-attacking potential.

- Jack Martin’s skillful goal in the wet after a controversial decision lifted Geelong at a critical juncture.

- Oliver Dempsey’s sealer in the final minutes triggered celebrations among the home crowd.

These moments, captured in official AFL highlights, underscored the game’s intensity and the small margins that decide modern AFL matches.

What’s Next for Both Teams

Geelong will look to build on the victory with improved percentage and consistency as the season progresses. Their home-ground advantage remains a significant asset.

Adelaide faces a tough road ahead and must find ways to integrate returning players while maintaining competitiveness. The Crows’ young talent showed promise, suggesting long-term potential if they can tighten defensive structures and improve starts.

For fans unable to attend, the full match replay and extended highlights packages are available on official AFL platforms and broadcasters.

The Cats’ narrow win keeps them in the early-season conversation, while Adelaide will regroup ahead of their next assignment. In a competition where every point counts, Geelong’s ability to grind out results in adverse conditions could prove valuable as the premiership race intensifies.

Britain is heading towards a significant shortage of mechanics trained to service electric vehicles, raising concerns that the country’s transition to cleaner transport could outpace the workforce needed to support it.

New analysis from the Institute of the Motor Industry suggests the UK could be short of 44,000 EV-qualified technicians by the time petrol and diesel car production is phased out, under current government targets.

While ministers have reaffirmed plans to ban the sale of new internal combustion engine vehicles by 2035, only around a quarter of the UK’s mechanics are currently trained to work on electric cars. The gap between policy ambition and workforce readiness is widening, particularly among smaller independent garages.

A key concern is the uneven distribution of EV expertise. A disproportionate number of qualified technicians are employed by larger national chains such as Kwik-Fit, which have the scale and resources to invest in training and benefit from servicing contracts with corporate EV fleets.

By contrast, many smaller, independent garages, which make up a large part of the UK’s automotive repair network, remain hesitant to invest in EV training. Owners cite a lack of local demand, high training costs and uncertainty over the pace of the transition.

In areas where electric vehicle adoption remains low, particularly outside major urban centres, garage operators say the business case for upskilling staff is not yet compelling.

For many workshop owners, the decision comes down to economics. Traditional repair work — such as servicing engines, clutches and fuel systems — remains a core revenue stream, yet these components are largely absent in electric vehicles.

EVs typically require less maintenance and fewer moving parts, reducing both the frequency and value of repair work. Even routine checks such as MoTs tend to involve less labour, further eroding potential income for independent garages.

This structural shift is creating uncertainty across the sector, with some operators concerned that investing in EV capability could fail to deliver sufficient returns in the short term.

The transition is also being shaped by regional disparities in EV uptake. In some parts of the UK, particularly rural areas, demand remains limited, reinforcing reluctance among smaller businesses to invest.

Consumers are already experiencing the consequences. In some cases, EV owners have been forced to travel long distances to access qualified repair services, as local garages lack the necessary expertise or equipment.

This highlights a growing disconnect between national policy and local infrastructure, both in terms of charging networks and servicing capacity.

Broader uncertainty around global EV policy is adding to the hesitation. Shifts in international markets, including changes to electric vehicle targets in the United States and Europe, have made some business owners wary of committing to long-term investment.

At the same time, the UK government has introduced measures such as expanded charging infrastructure and new road pricing proposals for EVs, but these have yet to fully translate into stronger consumer demand.

Despite these challenges, industry analysts believe the transition to electric vehicles is ultimately inevitable.

Even if policy timelines shift, manufacturers have already invested heavily in electrification, and EVs are expected to dominate new car sales within the next decade. Quentin Le Hetet of automotive analysts GiPA suggests that electric vehicles could outnumber petrol and diesel cars on UK roads by the mid-2030s.

However, the pace of that transition will depend heavily on whether supporting industries, including repair and maintenance, can keep up.

Experts warn that without targeted support, independent garages could be left behind, with larger operators and manufacturer-approved service centres capturing a growing share of the market.

Peter Wells, of the Centre for Automotive Industry Research, said the shift could fundamentally reshape the sector, with manufacturers increasingly controlling access to repair data and systems.

This trend raises concerns about competition, pricing and the long-term viability of smaller businesses that have traditionally formed the backbone of the UK’s automotive repair industry.

The Institute of the Motor Industry has called for increased funding to support training and workforce development, warning that without intervention, the skills gap could become a major bottleneck in the UK’s net zero ambitions.

For policymakers, the challenge is clear: ensuring that the transition to electric vehicles is not only technologically feasible, but also economically and operationally sustainable.

For the thousands of garages across the country, the message is equally stark; adapt to the electric future or risk being left behind as the automotive industry undergoes its most profound transformation in decades.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

eMed chief wellness officer Tom Brady and eMed CEO Linda Yaccarino discuss GLP-1 market growth and the company’s latest funding round on ‘Mornings with Maria.’

As the market for GLP-1 weight-loss drugs explodes toward a projected $150 billion, NFL legend Tom Brady is stepping into the arena — not to promote a magic pill, but to infuse the clinical surge with his trademark “TB12” discipline.

“Making a difference in other people’s lives, trying to share some of the things that have been in my mind that I’ve learned from incredible mentors, understanding and trying to inspire through the different people that have come into my life to communicate the messages that I’ve been able to get, that have helped me kind of live my dream, and I want to do that for others,” Brady said in an exclusive “Mornings with Maria” interview that aired Thursday.

The seven-time Super Bowl champion and eMed CEO Linda Yaccarino joined forces to announce a massive $200 million funding round, valuing the digital health company at more than $2 billion. The duo is aiming to revolutionize “population health” by using AI and clinical oversight to provide employers with a sustainable way to offer GLP-1 weight-loss medications like Ozempic and Mounjaro, while slashing corporate insurance claims.

“The raise confirms immense momentum and establishes us as the definitive company for population health and helping employers break the runaway health care costs and break their cost curve,” Yaccarino told Bartiromo.

TOM BRADY SAYS POST-N.F.L. LIFE IS ABOUT ‘BUILDING TRUST’ AS HE MAKES BUSINESS PLAY WITH HERTZ

“When you have overweight or obese people, their health care costs are two times the average employee who’s not obese,” she continued. “So that is the question that hasn’t been answered yet, that finally, eMed steps in, is able to deliver those solutions to employers all over the country.”

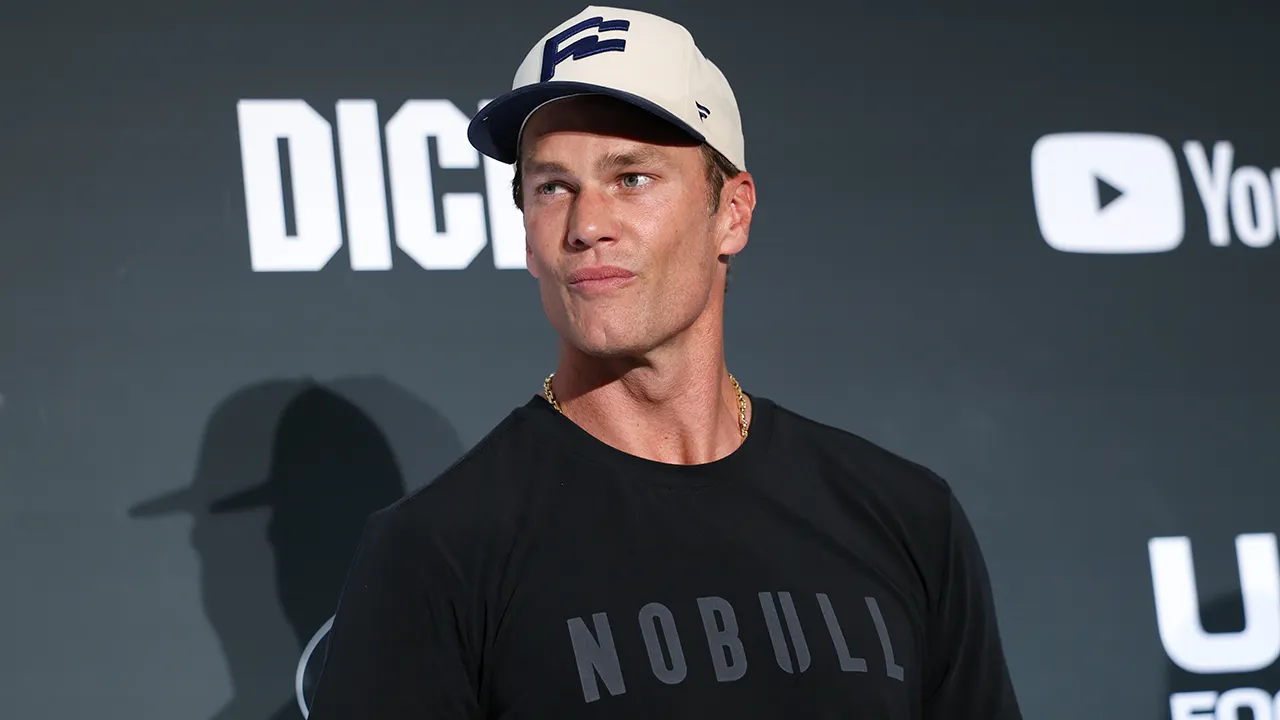

Tom Brady at the Fanatics Flag Football Classic Press Conference & Practice held at BMO Stadium on March 20, 2026, in Los Angeles, California. (Getty Images)

While many Americans use GLP-1s as an easy weight-loss solution, Brady views the eMed platform as a kickstart for those who lack the biological advantage of natural high-willpower. He insists that medication must be based on a foundation of clinical support and personal accountability.

“This isn’t about shortcuts for anybody. This is about a well-delivered program for people to kick-start their health journey in certain ways,” Brady clarified. “I’ve been so fortunate to be around the best professionals, the best doctors, the best trainers, the best nutritionists. And I realized how fortunate I was at having that guidance.”

“I really want to kind of break the stigma around the fact that, you know, discipline and hard work and willpower are something that… we’re born with. I was born with that, and I have the ability to do that. I think there’s a lot of other people that that is something that is more of a struggle,” he added. “But we need to be able to provide support for those people as well.”

Seven-time Super Bowl champion Tom Brady and Aescape CEO Eric Litman discuss the NFL star’s partnership with next-generation AI massage technology on ‘The Claman Countdown.’

Brady further detailed how his most valuable asset required a level of maintenance that is only now becoming mainstream.

“I realized because I was an athlete, my body was my asset,” the former quarterback said. “If I loved playing football and I love being on the field, then I love performing my very best. I had to treat my body, you know, a very certain way. I tried to get a lot of muscle work to repair injured tissue. I hydrated all the time. I tried to eat a low inflammatory diet. I tried to get the proper rest.”

“How can I ever stop? This is my life, I tell you, I’ve been so obsessed with training. I would feel horrible and worse if I didn’t move all the time. I feel like I have a lot of energy… I want to stay active. I have three children. I want to go out there and play basketball and swim and hit the golf ball, and play volleyball with my daughter in the backyard,” Brady said.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

Novo Nordisk President and CEO Mike Doustdar joins ‘Mornings with Maria’ to discuss the launch of the first GLP-1 weight-loss pill in the U.S., the lawsuit against Hims & Hers and talks with the Trump administration on drug pricing.

Yaccarino — the former CEO of X Corp who declined to comment on Wednesday’s social media verdict — explained that the goal of eMed is to take Brady’s “rigor” and apply it to the American workforce and minimize chronic diseases.

“Ninety-percent of people stay on our program. They do two things: First, and most important, what Tom was referencing, they get healthier,” she said. “And when you get people on the program, when you deliver those health outcomes, that’s the secret sauce for employers, for CEOs, CFOs — who you have on your show all the time — because they get their return on their investment.”

IB Acquisition stockholders approve extension of business combination deadline

Travelers across the United States are enduring some of the longest security wait times in TSA history as a partial government shutdown drives high staff call-out rates at major airports, forcing many hubs to warn passengers to arrive three to four hours early for domestic flights.

Houston’s George Bush Intercontinental Airport has reported the most severe delays, with checkpoints showing waits of up to three to four hours in recent days. Hartsfield-Jackson Atlanta International, the world’s busiest airport, has advised allowing at least four hours for screenings amid fluctuating but often extended lines.

The disruptions stem from elevated TSA officer absences — sometimes exceeding 30-47% at affected airports — linked to the funding lapse. This has compounded spring travel demand, creating unpredictable and occasionally chaotic scenes with lines stretching outside terminals or into parking areas.

Here are 10 U.S. airports currently experiencing among the longest TSA wait times, based on recent reports, airport advisories, call-out rates and traveler accounts as of late March 2026. Wait times can shift rapidly within the day and vary by terminal or checkpoint; these reflect the most frequently cited problem spots.

- George Bush Intercontinental Airport (IAH), Houston Waits have repeatedly hit three to four hours at open terminals, with some checkpoints reporting 180 minutes or more during morning peaks. High call-out rates around 36-42% have forced reduced operations, prompting strong advisories and even assistance from ICE agents providing water to those in line.

- Hartsfield-Jackson Atlanta International Airport (ATL) The busiest U.S. airport by passenger volume has urged travelers to allow four hours or more for security. Call-out rates have reached 33-37%, with lines sometimes exceeding two hours during rushes. Officials have removed or suspended real-time wait displays due to volatility.

- John F. Kennedy International Airport (JFK), New York One of the hardest-hit East Coast hubs, with call-out rates near 33% and reports of multi-hour delays. The airport has suspended routine wait-time reporting, warning that conditions can change quickly based on staffing and volume. Long lines have been visible in multiple terminals.

- William P. Hobby Airport (HOU), Houston Often posting even higher call-out percentages than its larger sibling IAH — up to 47% in recent data — Hobby has seen significant delays and reduced checkpoint availability, contributing to the broader Houston-area chaos.

- Louis Armstrong New Orleans International Airport (MSY) Travelers have faced waits stretching to three hours or more, with advisories to arrive at least three hours early. Call-out rates around 34% have strained operations, occasionally pushing queues into parking structures.

- LaGuardia Airport (LGA), New York Reports of 90-minute-plus waits during morning peaks, with lines extending outside buildings. The airport has seen notable staffing pressures amid the regional New York challenges.

- Newark Liberty International Airport (EWR), New Jersey Wait-time reporting has been temporarily suspended due to rapid changes from staffing shortages. Delays have contributed to flight disruptions, with lines frequently extending during busy periods.

- Los Angeles International Airport (LAX) Major West Coast hub experiencing longer-than-normal waits amid nationwide issues, with some reports highlighting multi-hour delays during peak spring travel. High passenger volume amplifies the impact of reduced staffing.

- Miami International Airport (MIA) South Florida’s primary gateway has seen elevated lines, with waits reported in the 30- to 60-minute range or higher during peaks, exacerbated by international traffic and staffing constraints.

- Fort Lauderdale-Hollywood International Airport (FLL) Another busy Florida airport hit by the broader disruptions, with reports of extended security lines during the recent wave of spring and leisure travel.

Other airports frequently mentioned in recent delays include Philadelphia International (PHL), where some checkpoints closed entirely, and occasionally Orlando (MCO) or Austin (AUS) during event-driven surges.

Broader Context and Causes

The ongoing partial government shutdown has dramatically increased TSA call-out rates from a normal level below 2% to double digits or higher at many large hubs. This has occurred while passenger volumes remain robust, particularly with spring break overlapping the disruptions.

TSA Deputy Administrator Ha Nguyen McNeill told Congress that the agency is facing unprecedented wait times in its 24-year history. Some airports have deployed alternative staff or adjusted operations, but capacity remains constrained.

Airports in Houston and Atlanta have been among the most visibly affected, with real-time data sometimes unavailable as officials prioritize safety and flow over precise estimates. Smaller or mid-sized airports have generally fared better, though isolated spikes occur.

Tips for Travelers Facing Long TSA Lines

Authorities and experts recommend the following strategies:

- Arrive early: Plan for three to four hours before domestic departures at affected major airports; allow even more for international flights.

- Check real-time sources: Use airport websites (when available), the MyTSA app for crowd-sourced reports, or third-party trackers. Note that some official displays have been paused.

- Enroll in expedited programs: TSA PreCheck, CLEAR and Global Entry can significantly reduce times where lanes remain open, though they are not immune to overall staffing issues.

- Pack smart: Follow the 3-1-1 liquids rule and minimize carry-on complexity to speed screening.

- Monitor flight status: Delays in security can cascade into gate issues; build in buffers for connections.

- Consider alternatives: Off-peak flights or smaller regional airports sometimes experience shorter lines.

Many airports have added signage, rope lines and support staff to manage crowds, but patience remains essential.

Outlook and Potential Relief

Negotiations to resolve the funding lapse continue, with some lawmakers expressing urgency over the impact on travel and the federal workforce. Until a resolution, variability is expected to persist, particularly during morning and evening rushes at large hubs.

Travelers are advised to verify conditions the day of travel, as wait times can drop dramatically later in the day once initial peaks clear. Those with flexible schedules may benefit from shifting to less busy periods or airports.

The situation underscores the critical role of consistent TSA staffing in maintaining efficient air travel. While some checkpoints have seen temporary improvements when call-outs ease, the underlying pressures remain until broader funding and personnel issues are addressed.

For the latest updates, check individual airport websites, the TSA’s resources or reliable news outlets. Conditions evolve quickly, and proactive planning is the best defense against missing a flight.

Data reflects reports and advisories from March 23-26, 2026. TSA wait times fluctuate hourly and by checkpoint; always confirm with official sources before traveling. This article is for informational purposes only.

M&A Can Be a Big Opportunity. These Stocks Look Like They Could Pop If Deals Close.

Sikorsky’s UH-60MX Black Hawk Helicopter Brings Complete Autonomy to Real World Army Trials

YES!! XRP GOT GREENLIT!? (MAJOR CLARITY ACT SHOCK)

The V&A’s Schiaparelli exhibition is a surrealist delight

-

Crypto World6 days ago

Crypto World6 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Adidas – Corporette.com

-

NewsBeat1 day ago

NewsBeat1 day agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Politics6 days ago

Politics6 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World5 days ago

Crypto World5 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech6 days ago

Tech6 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

News Videos12 hours ago

News Videos12 hours agoParliament publishes latest register of MPs’ financial interests

-

Sports3 days ago

Sports3 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Politics7 days ago

Politics7 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business4 days ago

Business4 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Sports3 days ago

Sports3 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech4 days ago

Tech4 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports6 days ago

Sports6 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Tech4 days ago

Tech4 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

Politics7 days ago

Politics7 days agoScotland’s rejection of assisted dying is a victory for humanity

-

Business7 days ago

Business7 days agoDLocal: Entering 2026 At Escape Velocity

-

Business6 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

NewsBeat7 days ago

NewsBeat7 days agoMissile lands next to presenter during live report

-

Tech5 days ago

Tech5 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

You must be logged in to post a comment Login