Crypto World

3 US Stocks Heavily Affected by Trump’s Iran Speech This Week

President Trump’s April 1 address on the Iran war promised two to three more weeks of intense military strikes, reversing a two-day stock market relief rally and sending oil above $110 per barrel.

The speech divided US stocks into clear winners and losers. BeInCrypto analysts identified three stocks where the impact was most visible. The list includes one energy name riding the war premium higher.

The list also has two oil-dependent companies whose recoveries were cut short within hours. The selection is based on price reaction, chart structure, and the degree to which each business model directly connects to sustained oil prices.

APA Corporation (NASDAQ: APA)

APA Corporation (APA) is among the US stocks that have benefited most directly from the Iran conflict. As a pure-play oil and gas exploration and production (E&P) company, every dollar increase in crude flows almost directly to APA’s bottom line.

Trump’s pledge to continue strikes and his threat to target Iran’s energy infrastructure signal sustained supply disruption, which supports elevated crude prices for the foreseeable future.

The daily chart shows that APA has rallied approximately 96% since early January, forming a clear pole-and-bull-flag pattern. Since March 30, prices have consolidated inside a flag.

Chaikin Money Flow (CMF), a proxy for institutional buying and selling pressure, has been consistently making higher highs throughout the rally, currently reading 0.18.

That persistent institutional inflow confirms that big money is backing the move rather than fading it.

On April 2, APA’s share price peaked at $43.93 but failed to break the upper trendline of the flag. A clean close above $43.98 would confirm the breakout and target $49.80 initially, followed by $55.63 and $65.06 on the extended projection.

However, a break below $40.38 would end the flag prematurely, though a full invalidation of the bullish structure would require a move below $31.56.

Carnival Corporation (NYSE: CCL)

Carnival Corporation (CCL) sits on the opposite end of the oil price chain. As the world’s largest cruise operator, fuel represents one of its highest variable costs.

Rising oil compresses margins directly, while sustained geopolitical uncertainty dampens consumer willingness to book voyages, creating a double headwind that few sectors absorb as severely.

Since peaking at $34.05 on February 6, Carnival stock has been trading inside a bearish descending channel on the daily chart. It fell approximately 10% over the past month as oil prices climbed.

A bullish divergence had been forming from mid-November to late March, in which the price made a lower low while the Relative Strength Index (RSI), a momentum oscillator, made a higher low.

That divergence suggested weakening sell-side momentum and triggered a bounce as de-escalation hopes lifted markets earlier in the week.

Trump’s speech reversed the setup. The bounce stalled, and prices fell 3.54% on April 2 as the two-to-three-week war extension reignited fears of prolonged $110 oil.

The bullish divergence technically remains intact, meaning a recovery is still possible if de-escalation resurfaces. However, the path of least resistance points lower as long as oil stays elevated.

A move above $26.77 would begin to shift momentum, with $30.13 as the level that turns the structure neutral. On the downside, $23.80 acts as immediate support.

A break below $21.45 would confirm a pattern breakdown and open the path toward $20.19 and $18.41.

United Airlines Holdings (NASDAQ: UAL)

United Airlines Holdings (UAL) experienced perhaps the most dramatic whiplash among US stocks this week. Jet fuel typically accounts for 25-35% of an airline’s operating expenses, making airline stocks among the most oil-sensitive equities in the market.

When oil rises, margins compress immediately because airlines cannot pass fuel costs to passengers fast enough through surcharges.

Between March 27 and April 1, UAL’s share price surged 14%. De-escalation hopes pushed oil lower and lifted the entire travel sector. That rally brought the price back above the 20-day Exponential Moving Average (EMA), a short-term trend indicator that gives greater weight to recent price action, at $93.71.

Trump’s speech erased the recovery. UAL fell approximately 8% from its April 1 high, closing at $92.21 on April 2, a 3% daily loss. The drop pushed the stock back below the 20-day EMA, which matters because the last time UAL reclaimed it on February 3, it preceded a 9% rally. Losing it now removes that short-term floor.

The broader damage is substantial. Since early February, UAL has fallen 28%. Right from $118.88 to its March 30 low of $84.62. The dip was driven entirely by oil-related margin fears.

If markets reopen on Monday with positive developments, reclaiming $93.71 would restore the 20-day EMA floor.

Above that, $97.71 and $101 become the next targets, with $101.75 aligning closely with the 50-day and 100-day EMAs. A move above $101.75 would place UAL above every major moving average for the first time since early February.

However, if oil stays above $110 and the war timeline extends, $84.62 remains the floor. A break below that level exposes deeper downside.

The post 3 US Stocks Heavily Affected by Trump’s Iran Speech This Week appeared first on BeInCrypto.

Key Highlights

- Reed Hastings, Netflix’s co-founder and board chair, offloaded $40.1M worth of NFLX shares on April 1, 2026

- The transaction involved 393,950 shares executed at prices spanning $95.02 to $96.66 per share

- Simultaneously, Hastings exercised stock options for 420,550 shares priced at merely $9.44 apiece

- Earlier in March, Hastings liquidated approximately $39M in Netflix stock, bringing his 2026 total to over $79M

- Wall Street maintains confidence with 41 analysts rating NFLX a Strong Buy and targeting $113.97 per share

On April 1, 2026, Reed Hastings—the visionary co-founder and current board chair of Netflix (NFLX)—executed a substantial stock divestiture worth $40.1 million. The transaction encompassed 393,950 shares distributed across several trades, with individual share prices fluctuating between $95.02 and $96.66.

Records filed with the Securities and Exchange Commission (SEC) confirm the shares were sold through open market transactions.

Concurrent with this divestiture, Hastings leveraged pre-existing stock options to purchase 420,550 NFLX shares at the remarkably low exercise price of $9.44 per share, representing a total outlay of roughly $3.97 million. Additionally, he obtained 654 shares through Non-Qualified Stock Options at $95.55 per share.

This marks a continuing pattern. Earlier on March 2, Hastings divested 410,000 Netflix shares, generating approximately $39 million in proceeds. Combined, his equity liquidations in 2026 have already surpassed $79 million within just one month’s timeframe.

These stock sales follow Netflix’s strategic withdrawal from its ambitious $82 billion acquisition attempt of Warner Bros. Discovery (WBD). After an extended competitive bidding process that included Paramount Skydance (PSKY) as a contender, Netflix ultimately abandoned its WBD takeover pursuit.

In the wake of that decision, Netflix implemented subscription price increases throughout its U.S. market.

Subscription Price Adjustments Catch Wall Street’s Eye

The ad-supported Standard subscription tier now carries an $8.99 monthly price tag. The ad-free Standard option has increased to $19.99, while the Premium tier has risen to $26.99 monthly.

Analysts from Needham project these pricing adjustments could generate approximately $1.7 billion in additional revenue, potentially accelerating North American growth metrics by roughly 300 basis points throughout fiscal 2026.

Major financial institutions including BofA Securities, Bernstein, and Needham have maintained bullish stances on the streaming giant, establishing price targets of $125, $115, and $120 respectively.

NFL Programming Expansion on the Horizon

Netflix is currently negotiating to double its NFL game package from two to four games annually. The streaming platform is pursuing additional time slots, including a Thanksgiving Eve broadcast and an internationally-based matchup.

These negotiations unfold as Netflix nears the conclusion of its three-year Christmas Day game agreement, which commanded approximately $75 million per game.

Citizens Bank recently launched coverage on NFLX with a Market Perform designation, acknowledging Netflix’s standing as the world’s second-largest streaming service provider.

Current analyst consensus reveals 41 Wall Street professionals covering NFLX maintain a Strong Buy recommendation—comprising 30 Buy ratings and 11 Hold ratings published within the preceding three months. The consensus price target stands at $113.97, suggesting potential upside of approximately 16% from present trading levels.

Opinion by: Ido Sofer, founder and CEO at Sodot.

The crypto industry is normally well ahead of its game when it comes to pure innovation and functionality, but security is a different matter.

For years, custody risk in crypto was defined by a single fear: the theft of private keys. The industry responded by hardening storage with cold storage, air-gapped systems, MPC and other methods. It then recognized that protecting only the keys is not enough, introducing transaction security and policies to prevent malicious transactions that steal funds, although the keys remain safe. Both of these remain a serious threat, but focusing solely on private keys obscures a deeper shift.

Custody itself has expanded far beyond private keys.

“Custody” once meant protecting private keys. That definition no longer reflects reality. Custody has evolved into a complex, automated system that operates different kinds of transactions, across multiple venues, custodians, vendors and internal systems. Modern trading firms operate across exchanges, staking platforms, liquidity venues and infrastructure providers, each with API keys, validator keys, deployment credentials and system-level secrets that can move capital directly or indirectly.

Many of these credentials are stored in secret managers that, by design, return the full key to any authenticated process. Convenient, yes, but structurally fragile. If the execution environment is compromised, either by an external attacker, an employee that was threatened or a malicious dependency, the full key is compromised. Custody risk has expanded beyond dormant on-chain keys into a live execution layer, where capital moves in milliseconds and exposure happens in real time.

The evolution of custody security

Custody security evolved in stages. First, the industry secured private keys in storage. It then moved beyond storage, embedding policy and multi-party controls to govern how those keys were used in execution. The next step is inevitable: apply the same zero-exposure and policy-driven discipline to every key and credential. In modern crypto operations, API keys, deployment credentials and execution secrets carry significant risk. Extending private key best practices across this broader surface is no longer optional; it is the defining challenge of execution risk.

In recent years, the execution risk has emerged as the single biggest vector for large-scale exploits. Cybercriminals are bypassing onchain security mechanisms in favor of the soft underbelly, namely the API keys, server credentials and other off-chain secrets needed to facilitate trading, code deployment, staking and custodial actions. Recent major breaches, including the Bybit hack, started with an off-chain hack and compromised credentials, which later led to on-chain loss of funds.

How big is the execution risk?

It’s big and structural. Asset managers, trading firms, custodians and payment companies connect to dozens of CEXs, DEXs, liquidity providers and other vendors simultaneously. Each integration introduces its own credentials, access controls and operational dependencies. Managing these spans across development, ops, trading, risk and security teams, which creates complexity that compounds over time.

Securing these operations is a never-ending struggle. Maintaining consistent security policies and multi-vendor access is a massive headache that’s largely manual, resulting in inevitable security gaps and configuration drift.

Related: Bitcoin is infrastructure, not digital gold

Execution risk is not inherent toautomation. It is a byproduct of how trading systems have historically been designed. In many centralized exchange environments, API keys and operational credentials are placed directly inside trading infrastructure to eliminate latency. For market makers and trading firms, speed is not a feature, it is the business model. Even marginal delay affects revenue.

Over time, full-key availability inside live systems became normalized as the simplest way to achieve high-performance execution. Credentials sit in a constant state of readiness so transactions can be authorized instantly. The issue is not that capital moves quickly. It is that unilateral authority is embedded inside operational infrastructure. And when authority is concentrated where execution happens, it becomes the most predictable attack vector.

Existing controls fall short

Existing tools fall far short of what’s required, considering the complexity of modern execution environments.

While crypto exchanges, custodians and over-the-counter trading desks certainly employ robust security policies for specific operations, it’s incredibly difficult for them to synchronize those controls across such a fragmented ecosystem. In fact, it’s almost impossible to maintain consistent governance across forty-odd exchanges for any length of time. Since it’s done manually, in silo, errors are inevitable, and a single mistake can put millions of dollars in value at risk.

There’s also the counterparty risk to consider. Exchanges and custodians may have their own vulnerabilities in the shape of bugs, misconfigured infrastructure and inconsistent policy enforcement mechanisms. If a trading firm’s internal security code requires geofencing, but one of the exchanges it’s connected to has a buggy implementation of that control, it creates a risk at the point of execution.

The risk is intolerable

The lesson the industry learned from private key security is clear: eliminate full key exposure and enforce strict policy controls around usage. Those principles must now extend beyond on-chain private keys to every credential capable of authorizing value movement.

The solution is not simply better secret storage. Secret managers were built for convenience; they return the full key to any authenticated process. In live execution environments, that model distributes authority to multiple components of the system at the very moment capital is in motion.

What is required is zero key exposure architecture systems where no single machine or employee ever holds unilateral control, combined with enforceable, context-aware policies governing how credentials are used. Multi-party computation (MPC) is one way to implement this model, but the principle is broader — expand private-key security best practices across the entire crypto execution layer.

Opinion by: Ido Sofer, founder and CEO at Sodot.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

What does it take to get corporations into digital assets? According to Brad Garlinghouse, the formula is surprisingly simple.

The Ripple CEO just broke down the “secret sauce” behind Ripple Treasury. It’s an enterprise treasury management platform that lets businesses view and manage both fiat and digital assets (including XRP and RLUSD stablecoins) in a single, unified dashboard.

The Two-Ingredient Formula

Garlinghouse laid it out clearly. No complicated onboarding, no new systems to learn, and no juggling between separate platforms for fiat and crypto. Just one unified solution.

Fun Fact: Ripple Treasury facilitated $13 trillion in payments last year. That’s roughly half of the entire US GDP processed through a single treasury platform!

What Changed

Ripple Treasury just launched as the first Treasury Management System (TMS) with native digital asset capabilities. For CFOs, this means a single place to hold and manage both digital and fiat assets.

Renaat Ver Eecke, who leads Ripple Treasury (formerly GTreasury), explained the vision:

“From the moment GTreasury became Ripple Treasury, we’ve been building to this, giving Corporates a clear, trusted entry point into digital assets.”

The new features include Digital Asset Accounts and Unified Treasury. Corporate treasurers no longer need separate systems, separate logins, separate workflows. Everything lives in one place.

Ver Eecke outlined the roadmap: connecting to Ripple’s regulated payments network and prime brokerage. This will allow corporates to use digital assets and stablecoins for cross-border intercompany payments, earn yield on idle cash around the clock, and much more.

The key insight: Corporations don’t want to become crypto companies. They want to use crypto rails without changing their operations. Ripple Treasury meets them exactly where they are.

Ver Eecke summarized it bluntly: “Corporate treasury has never had a solution like this before.”

Ripple Has a Unique Value in the Enterprise Segment

Traditional treasury management is fragmented. Fiat accounts here, digital assets there, cross-border payments somewhere else. Every system requires its own processes, its own compliance checks, its own headaches.

Ripple Treasury collapses all of that into a single platform. Trusted. Regulated. Embedded in existing workflows.

For CFOs who have been watching crypto from the sidelines, waiting for an entry point that doesn’t require rebuilding their entire infrastructure, this is it. The friction is gone.

Garlinghouse called it the secret sauce. Looking at $13 trillion in volume and native digital asset capabilities, the recipe seems to be working.

The post Ripple CEO Reveals the Secret Behind Its Crypto and Fiat Treasury System appeared first on BeInCrypto.

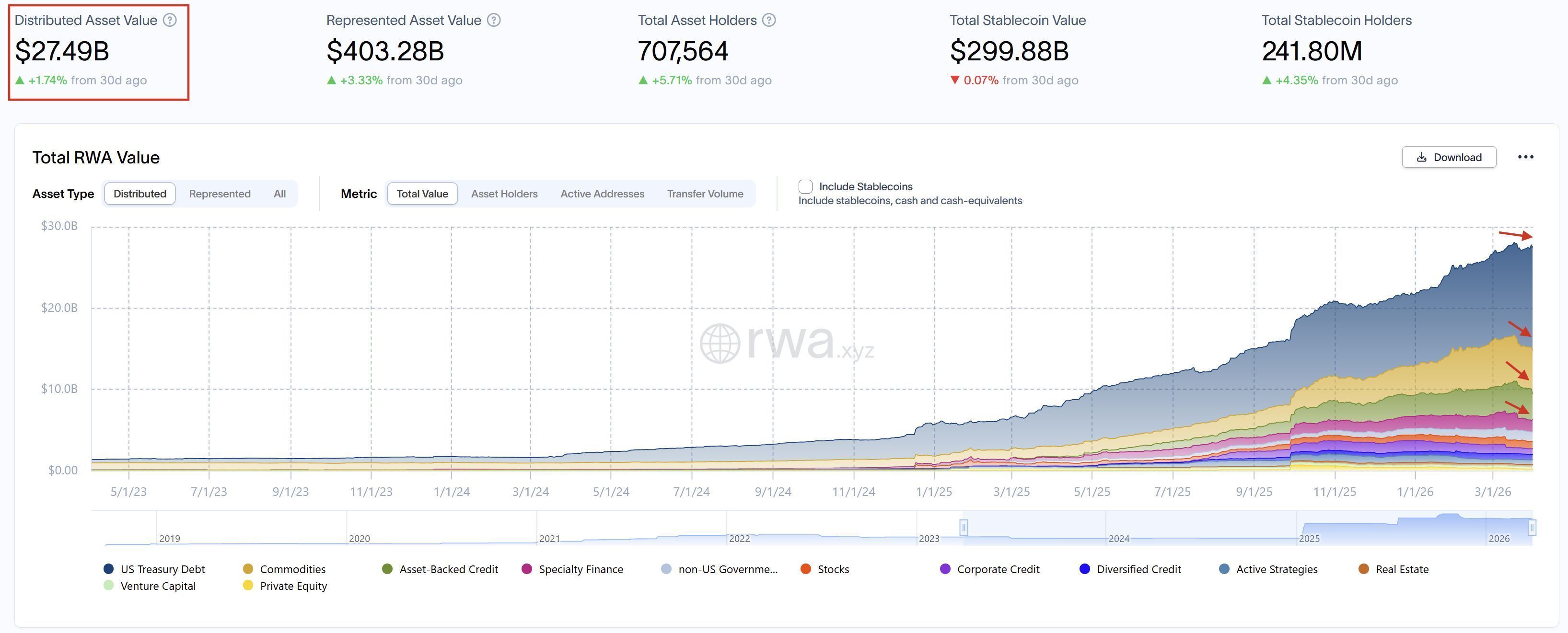

After months of continuous growth, the RWA sector is showing its first signs of a slowdown.

Distributed asset value sits at $27.49 billion with only 1.74% growth over the past 30 days. Stablecoins even recorded a slight decline.

RWA Growth is Dying Out

Current data from RWA.xyz shows the following picture:

- Distributed Asset Value: $27.49 billion, up 1.74% in a month.

- Represented Asset Value: $403.28 billion, up 3.33%.

- Total Asset Holders: 707,564, up 5.7%.

- Total Stablecoin Value: $299.88 billion, down 0.07%.

- Total Stablecoin Holders: 241.80 million, up 4.35%.

The number of holders continues to grow, but the value is not keeping pace. New market participants are entering, but bringing less fresh capital than in previous months.

Fun Fact: Despite the slowdown, RWA distributed value has grown from under $5 billion in early 2024 to nearly $28 billion today. The long-term trend remains intact!

Which RWA Segments Are Cooling

Several asset categories are contributing to the slowdown:

- Commodities: Gold prices have stagnated, and tokenized gold follows the underlying asset.

- US Treasuries: Still the largest segment in the RWA market, but momentum has flattened. Initial demand for tokenized T-bills appears to be stabilizing.

- Stocks and Asset-Backed Credit: Both categories are also showing reduced growth.

The chart from RWA.xyz displays a clear pattern: explosive growth through 2024 and into early 2025, followed by a gradual flattening in recent months.

A monthly growth rate of 1.74% does not constitute a crash. Annualized, that still represents over 20% growth.

However, compared to the triple-digit percentage gains the RWA sector recorded in 2024, the deceleration is clearly visible.

The slight 0.07% decline in stablecoins deserves particular attention. Stablecoins often serve as an entry point into tokenized assets. A shrinking pool may indicate reduced on-chain activity.

On the positive side: asset holders grew by 5.71%. New participants continue to enter the market, though with more cautious capital allocation.

The RWA sector appears to be entering a phase of normalization following a period of strong growth. Whether this represents a temporary consolidation or the beginning of a longer trend remains to be seen in the coming months.

The post Why the RWA Market Is Slowing Down: Is the Boom Over? appeared first on BeInCrypto.

Corporate Bitcoin (BTC) holders are diverging into two distinct paths amid continued market pressure. While Strategy held steady on its massive BTC reserves, Nakamoto Holdings moved in the opposite direction, selling at a loss and trimming exposure as it reworks its balance sheet.

The contrast highlights a growing divide in the corporate Bitcoin treasury model. Some holders have refused to sell, treating BTC as a long-term reserve asset and doubling down through volatility, while others are being forced to unlock liquidity, book losses or rethink capital allocation.

With Bitcoin down 46% from its peak, the risks behind debt-fueled or aggressive buying strategies are becoming harder to ignore.

Elsewhere, a proposed Bitcoin-backed municipal bond in New Hampshire is moving closer to issuance. It has now received a speculative-grade rating from Moody’s, underscoring both the appeal and the risks of tying public financing to digital assets.

Nakamoto realizes losses as Bitcoin treasury model comes under pressure

Bitcoin treasury company Nakamoto Holdings sold roughly $20 million worth of Bitcoin in March, executing the sale at prices well below its prior acquisition costs. The transaction reduced its holdings to just over 5,000 BTC and marked a shift from unrealized to realized losses.

The company sold approximately 284 BTC at around $70,400 per coin, significantly less than its average purchase price. The proceeds were earmarked for working capital and business investments tied to recent mergers.

Alongside the crypto sale, Nakamoto also cut its equity exposure to Japanese company Metaplanet, selling millions of shares at a loss. The moves point to a broader balance-sheet reset as digital asset treasury companies come under pressure.

Strategy pauses Bitcoin buys, keeps its treasury intact

Michael Saylor’s Strategy broke a months-long pattern of steady Bitcoin accumulation, reporting no purchases during the latest weekly disclosure period.

The pause stands out because Strategy has maintained consistent buying as a core part of its corporate identity and capital strategy, especially during the recent market downtrend that has seen Bitcoin fall from $120,000 to below $70,000.

Weekly disclosures have become a signal for institutional demand, and even a temporary halt could suggest squeamishness over market conditions, capital availability or the pace of buying. Strategy still holds roughly 762,000 BTC, maintaining its position as the largest corporate holder of the asset.

New Hampshire Bitcoin-backed bond inches toward reality after Moody’s rating

A proposed Bitcoin-backed municipal bond in New Hampshire has moved a step closer to issuance after receiving a Ba2 rating, below investment grade, from Moody’s. The structure would give investors exposure to Bitcoin-linked returns within a public finance framework, with proceeds expected to support public infrastructure and development projects.

The planned issuance, reportedly around $100 million, would be backed by Bitcoin collateral rather than traditional tax revenues. Repayments would depend on returns from that collateral, introducing a new approach that ties crypto markets to municipal borrowing.

CoinShares debuts on Nasdaq following SPAC deal

Digital asset manager CoinShares launched on the Nasdaq on Wednesday following a merger with special purpose acquisition company Vine Hill Capital, marking another step in bringing crypto-native companies to US public markets.

The deal gives CoinShares access to a broader investor base and deeper capital markets, while offering public market investors exposure to a company focused on digital asset products and infrastructure. SPAC structures have remained a viable route for crypto companies seeking listings despite shifting market conditions.

As Cointelegraph previously reported, the SPAC merger valued CoinShares at roughly $1.2 billion.

Crypto Biz is your weekly pulse on the business behind blockchain and crypto, delivered directly to your inbox every Thursday.

Coinbase got conditional approval from the OCC for its trust, a step toward federal oversight for its offerings to replace the current state by state licensing approach.

Coinbase announced on Thursday that it has received conditional approval from the Office of the Comptroller of the Currency (OCC) to establish Coinbase National Trust Company, a non-insured national trust bank to be headquartered in New York.

The approval marks a step toward Coinbase operating as a federally regulated digital asset custodian — and the latest milestone in a sweeping regulatory shift reshaping how crypto firms interact with the U.S. banking system.

The preliminary green light requires Coinbase to build out compliance systems, hire key staff, pass regulatory reviews, and demonstrate strong risk management and anti-money-laundering controls before it can secure a full charter.

A national trust bank charter gives Coinbase a single federal regulator — the OCC — in place of the patchwork of state money transmitter licenses it currently holds, allowing it to offer custody, safekeeping, and related digital asset services in a fiduciary capacity as a qualified custodian under SEC regulations.

In yesterday’s blog post, the largest U.S. centralized exchange noted that it does not plan to become a commercial bank:

“Coinbase is not becoming a commercial bank. We will not be taking retail deposits. We will not be engaging in fractional reserve banking.”

Looking ahead, Coinbase’s chief legal officer told CNBC that the company plans to explore payment infrastructure products alongside its custody business, with an eye on expanding stablecoin use — particularly USDC — as a mainstream global payment method.

Coinbase joins a crowded field of crypto firms racing to secure federal charters under the OCC’s current leadership.

Circle applied for its own national trust bank license — to be called First National Digital Currency Bank — and received conditional approval in December 2025. Crypto.com similarly secured conditional OCC approval for its Foris Dax National Trust Bank in February.

The trend has not gone uncontested: the Bank Policy Institute, whose members include JPMorgan, Goldman Sachs, and Bank of America, is reportedly weighing a lawsuit against the OCC over what it sees as an uneven regulatory playing field.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

XRP Ledger Chosen to Be the Research Framework

XRP Ledger will be used as the fundamental blockchain platform in the study. In addition, it will discuss how the network assists in payment processing in various markets. In this way, the firms would assess the technical performance under actual conditions. The companies explained that the project does not imply the immediate product rollout, but it will seek to collect technical and regulatory experience to be used in the future. Therefore, the research will guide long-term infrastructure planning.

Japan and South Korea are still working on creating stablecoin and blockchain laws. As a result, there are differences between two systems that should be analyzed in detail. The paper will examine compliance standards in the two jurisdictions. In the study, the researchers will evaluate what blockchain is doing with existing payment infrastructure. It will also compare compatibility with current banking and remittance systems. This will help to ensure that the solutions that will be developed in the future can work within the set frameworks.

The two companies will consider transaction flows and operating models. Therefore, the work will touch upon the stability and performance of the system under real conditions. In addition, it will also analyze some of the risks that may be associated with blockchain-based payments. The project identifies a number of areas of focus on which to analyze. It will look at the issues in the business environment and institutional differences between the two nations. Also, it will determine technical and operational obstacles that influence adoption.

Payments Under Evaluation Use Cases

The companies will consider the real-life uses of blockchain in payments. Therefore, they seek to find feasible applications of cross-border remittances. This will assist in laying down the future implementation directions. This research follows Ripple as it keeps on expanding partnerships with the global payment networks. Furthermore, South Korea has seen more currency being traded on local exchanges, indicating a growth of the stablecoin activity in the country. Such developments give a background to current research. The collaborative research creates a framework for analysing blockchain payments in two regulated markets. In addition, it assists in the planning of cross-border financial infrastructure in the future.

South Korea extradites alleged drug boss Park Wang‑yeol and prepares a blockchain forensics push to trace at least 6.8b won in Bitcoin‑linked drug proceeds.

Summary

- South Korea has extradited alleged drug kingpin Park Wang-yeol from the Philippines and placed him under a joint drug crime task force.

- Investigators will scrutinize Bitcoin wallet activity to trace at least 6.8 billion won (about $5 million) in confirmed proceeds and search for far larger hidden assets.

- The case showcases how Korean law enforcement now leans on blockchain forensics to unwind complex, cross-border narcotics networks.

South Korean authorities have taken custody of alleged “drug lord” Park Wang‑yeol, extradited from a Philippine prison where he was serving a 60‑year sentence for the 2016 “sugarcane field” triple homicide, to face new narcotics and money‑laundering charges at home. Reuters reported that Park, believed to be 47, is suspected of running a drug trafficking ring from inside his Philippine cell, coordinating shipments of “large quantities” of methamphetamine and other narcotics into South Korea via encrypted apps. According to Korean media summaries cited by outlets including the Dong‑A Ilbo, officials estimate he oversaw a monthly drug business worth roughly 30 billion won (around $22 million), turning prison into a command center rather than a constraint.

The Korean Drug Crime Joint Investigation Headquarters — a consolidated task force of prosecutors and police — has made clear that tracing Park’s financial footprint will rely heavily on on‑chain analysis of Bitcoin wallets believed to have received drug proceeds. While confirmed criminal takings in the current indictment stand at roughly 6.8 billion won (just over $5 million), investigators told domestic media they suspect the true scale of assets moved through crypto wallets between November 2019 and July 2024 is “several times larger.

Reporting from Chosun Ilbo details how Park allegedly directed accomplices in Korea to sell drugs sourced from abroad — including at least 4.9 kilograms of methamphetamine and thousands of ecstasy and ketamine doses — then funneled profits through digital channels rather than traditional banking rails. The task force has identified more than 200 accomplices across roles such as suppliers, smugglers and street dealers, underlining the networked nature of the operation and the need for tools that can map complex flows of funds.

South Korea has quietly built one of the more aggressive crypto‑crime enforcement programs in Asia, deploying specialist units that routinely use blockchain analytics platforms to deanonymize wallets and claw back illicit proceeds. A 2024 briefing from Blockchain Intelligence Group noted that Seoul’s joint investigation division recovered roughly 163.87 billion won (about $121 million) in crypto‑linked criminal proceeds in a single year, relying on tools that “identify clusters of wallets,” “track the flow of funds” and link addresses to real‑world entities.

Recent cases underscore both the potential and pitfalls of this approach: DL News reported in February that prosecutors managed to recover $22 million worth of Bitcoin that had effectively gone “missing” in an earlier phishing investigation, even as separate lapses saw police mismanage and temporarily lose more than $1.4 million in seized BTC. In that context, the Park Wang‑yeol probe is emerging as a showcase for how far Korean authorities can push on‑chain forensics to pierce one of the country’s most notorious narcotics empires — and whether they can do so while tightening their own controls over seized digital assets.

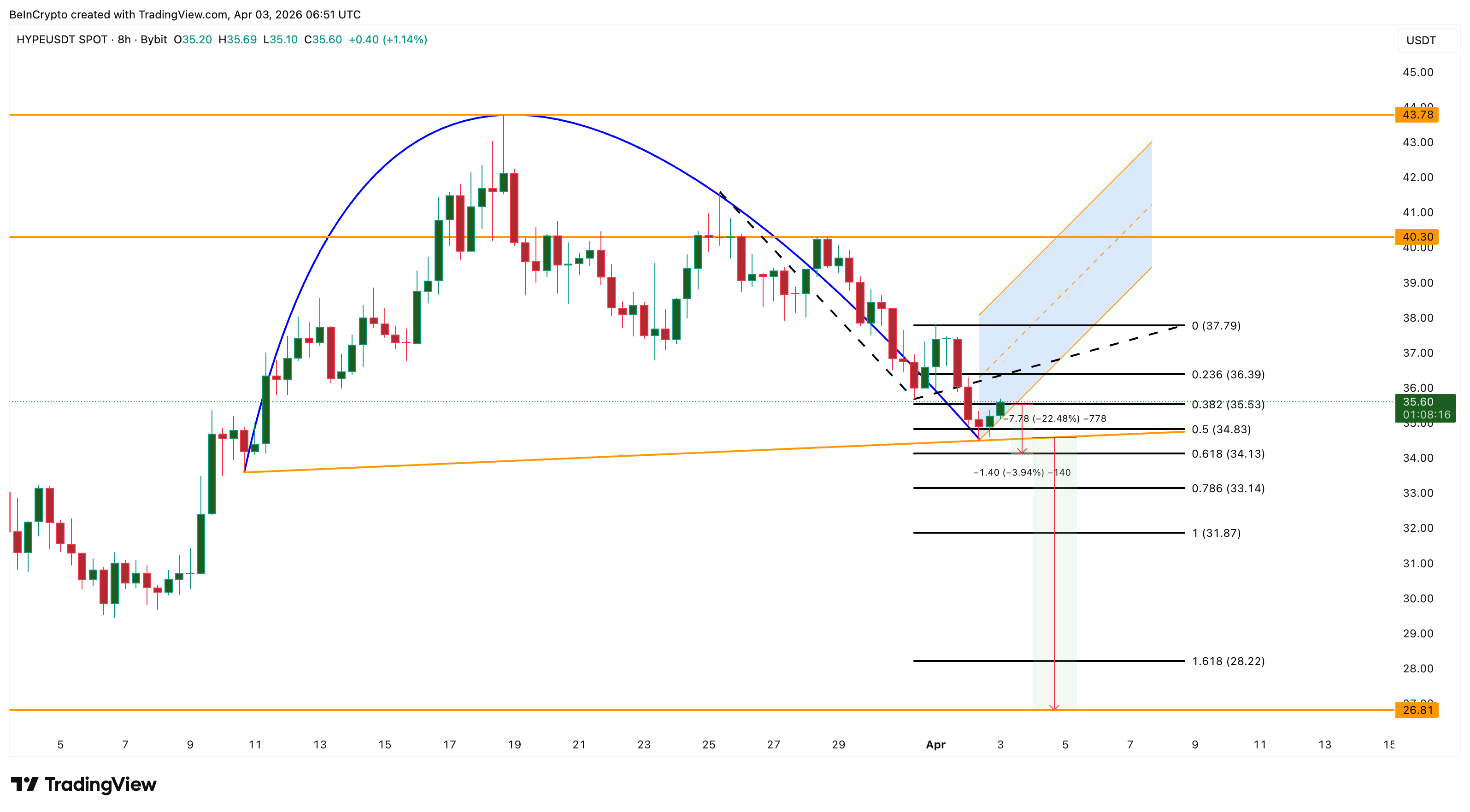

Hyperliquid (HYPE) price trades near $35.60 on April 3, carrying a 13% monthly gain that masks an 8% decline over the past seven days.

On the surface, the monthly performance looks strong for a market under pressure. However, the 8-hour chart is forming a bearish reversal pattern, institutional money flow is diverging from price, and the platform’s own financial metrics show a sharp deterioration in capital commitment. The bounce currently underway may extend further before the structure breaks, but the weight of evidence points toward eventual weakness.

An Inverse Cup Forms as Big Money Quietly Exits

Since March 10, Hyperliquid price has been tracing an inverse cup and handle pattern on the 8-hour chart, a bearish reversal structure. The current bounce is forming what closely resembles the handle, a smaller upward drift within a narrowing channel before a potential breakdown.

The handle remains intact as long as HYPE stays below $40.30. A confirmed break below the neckline would activate the pattern’s measured move, projecting approximately 22% downside from the neckline.

Chaikin Money Flow (CMF), a proxy for institutional buying and selling pressure, confirms the weakness behind the pattern. Since late February, while HYPE price trended higher, CMF trended lower, deepening into negative territory at -0.06. That bearish divergence indicates that large participants have been reducing exposure throughout the rally.

The on-chain data from Dune Analytics possibly explains why. Hyperliquid’s USDC-based assets under management (AUM) on Arbitrum peaked at $4.02 billion around mid-September 2025. By March 30, 2026, that figure had dropped to $1.85 billion, a 54% decline. USDC net flow, which measures the difference between deposits and withdrawals, remains in negative territory, meaning more stablecoins are leaving the platform than entering.

The AUM decline reflects a broader DeFi capital contraction. Total DEX spot volume across all platforms fell to $155 billion in March 2026, its lowest level since September 2024.

As a derivatives-focused platform with spot offering too, Hyperliquid allows traders to generate outsized volume through leverage with relatively small USDC deposits.

When capital commitment shrinks at the platform level while price rises, the rally lacks the financial foundation to sustain itself. The liquidation map now determines whether the bounce extends before the pattern resolves.

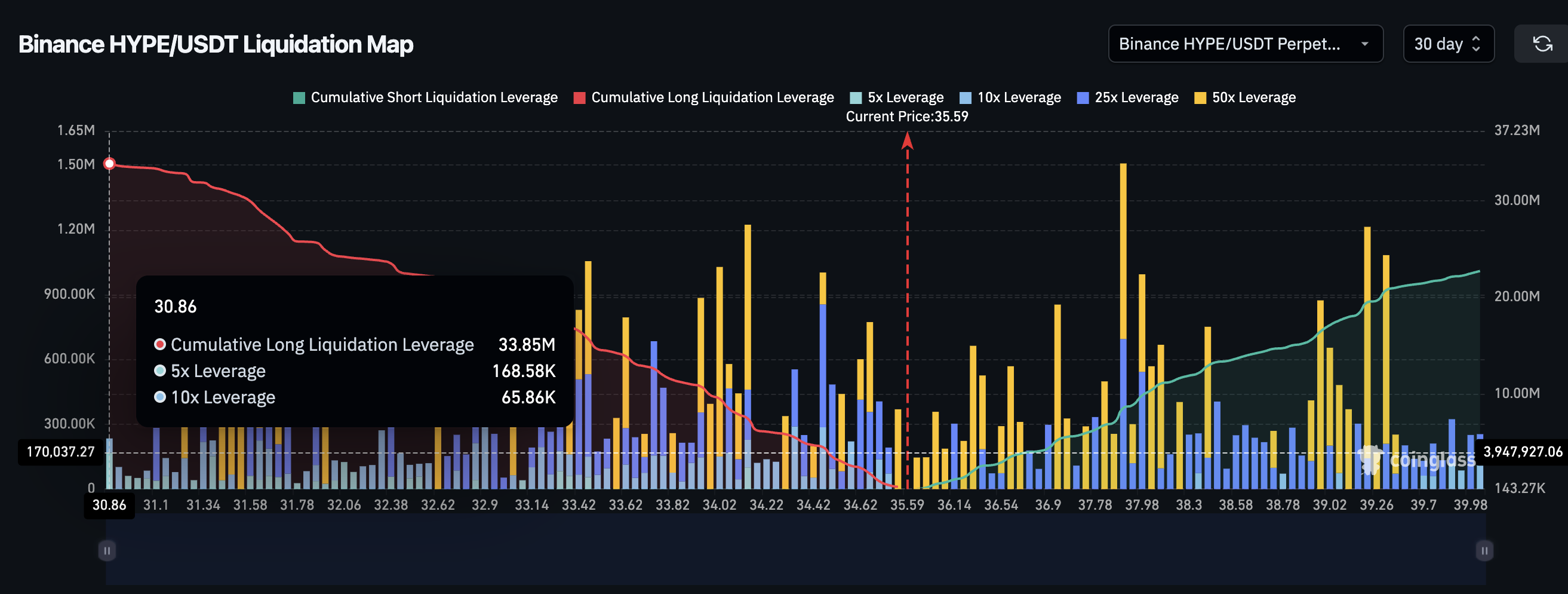

Liquidation Imbalance Could Fuel a Bounce Before the Break

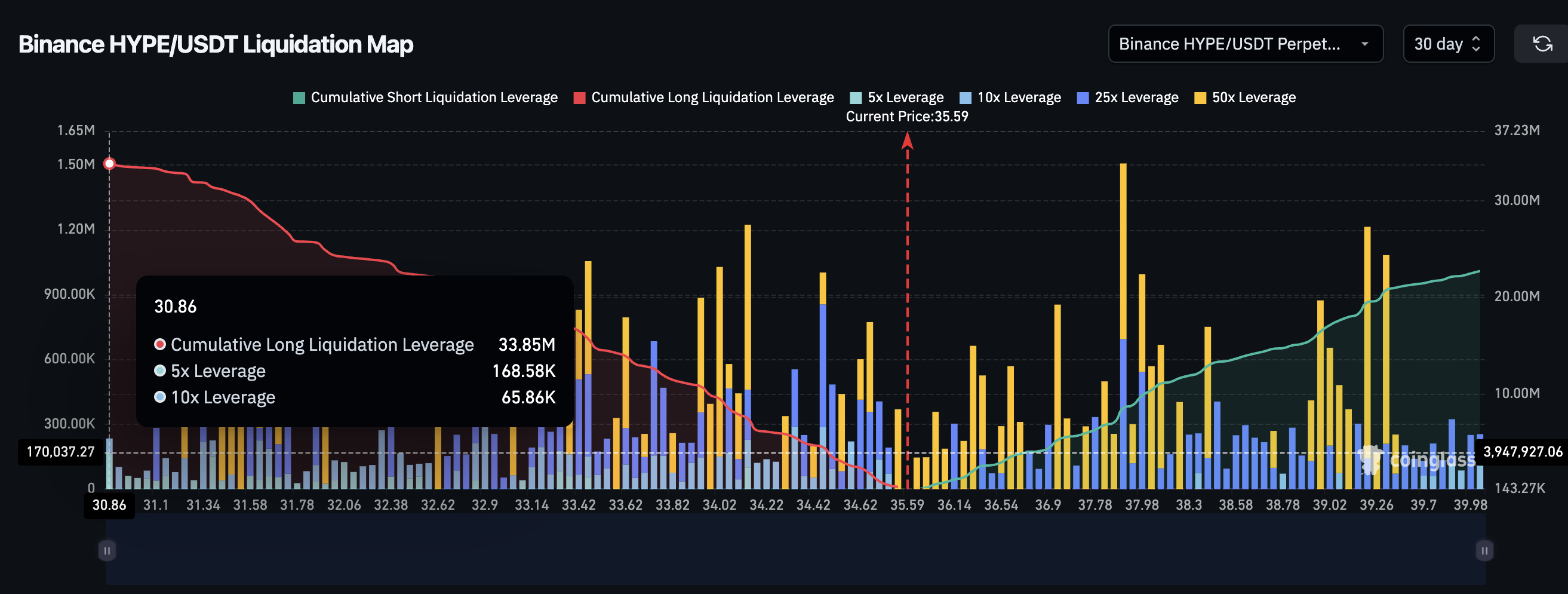

The Binance HYPE/USDT liquidation map adds an important layer that complicates the bearish timeline. Over the past seven days, the HYPE liquidation picture is heavily skewed toward shorts. Cumulative short liquidation leverage stands at $23.92 million, while long liquidation leverage sits at just $7.92 million. That roughly 75% tilt toward shorts means even a modest upward price move could trigger a cascade of forced short closures, temporarily pushing Hyperliquid price higher.

This short-heavy 7-day positioning likely exists because the past week’s 8% decline already flushed most of the recent long positions through liquidations. What remains are new shorts betting on continued weakness.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

However, the 30-day liquidation map flips the picture. Over that timeframe, cumulative long leverage is $33.85 million against $22.73 million in shorts.

The roughly 30% tilt toward longs means the broader positioning still favors upside bets. If the bounce driven by 7-day short squeezes fails to reclaim key levels and price resumes its decline, those 30-day long positions become vulnerable. A move toward the neckline at $34.13 could trigger both the pattern breakdown and a fresh wave of long liquidations, accelerating the sell-off.

The liquidation data therefore supports a scenario where the handle extends higher on short-term short squeezes before the broader structure breaks down under the weight of long-biased leverage and declining capital flows.

Hyperliquid Price Levels That Decide the Pattern

The 8-hour chart with Fibonacci levels frames the path for Hyperliquid price from here. HYPE currently trades at $35.60, sitting between the 0.382 Fib at $35.53 and the 0.236 Fib at $36.39.

For the bounce to gain meaningful traction, HYPE needs to clear $36.39 first, followed by $37.79. A move above $40.30 would weaken the inverse cup and handle structure, and reclaiming $43.78 would invalidate the pattern entirely.

On the downside, $34.83 acts as the immediate floor. A close below $34.13 confirms the neckline break and activates the measured move, projecting a 22% decline that could take HYPE price toward $26.81.

Between $34.13 and $26.81, interim support sits at $33.14, $31.87 and $28.22.

Inverse cup and handle patterns do not always complete. The short-heavy 7-day liquidation setup could produce a squeeze that pushes price above the handle, delaying or invalidating the breakdown. However, the combination of falling CMF, shrinking AUM, negative USDC flows, and a long-biased 30-day leverage structure all suggest the bounce is more likely a pause than a reversal.

A close below $34.13 separates a temporary squeeze-driven bounce from a pattern-confirmed decline toward $26.81. But reclaiming $40.30 would be the first evidence of near-term strength.

The post Hyperliquid Price Rallied 13% but the Money Underneath Tells Another Story appeared first on BeInCrypto.

Nasdaq-listed Bitcoin miner Riot Platforms sold 3,778 BTC in the first quarter of 2026, generating roughly $289.5 million in net proceeds.

Riot Platforms, a major publicly traded Bitcoin mining company listed on Nasdaq, sold 3,778 BTC during Q1 2026, netting approximately $289.5 million in proceeds. The sale represents a significant reduction in the miner’s Bitcoin holdings and marks a notable shift in the company’s position management strategy.

The move aligns with broader selling activity across the Bitcoin mining sector. Multiple publicly traded miners have collectively sold more than 15,000 BTC in recent months, signaling increased liquidation pressure within the industry.

Sources: Riot Platforms

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Reed Hastings Offloads $40M in Netflix (NFLX) Stock: What’s Behind the Sale?

3 steps for mastering the low, spinning pitch shot

Anthropic acquires biotech AI startup Coefficient Bio for $400 million

-

NewsBeat7 days ago

NewsBeat7 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat22 hours ago

NewsBeat22 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports7 days ago

Sports7 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Business16 hours ago

Business16 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Crypto World2 days ago

Crypto World2 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Entertainment6 days ago

Entertainment6 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Tech5 days ago

Tech5 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech5 days ago

Tech5 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Fashion6 days ago

Fashion6 days agoAmazon Sundays: Soft Spring Layers

-

Business2 days ago

Business2 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Fashion7 days ago

Fashion7 days agoWhen Evening Dressing Gets Colorful for Spring

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Crypto World4 days ago

Crypto World4 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Politics4 days ago

Politics4 days agoShould Trump Be Scared Strait?

You must be logged in to post a comment Login