Crypto World

Accenture (ACN) Stock Plunges 3% Despite Q2 Earnings Beat on Weak Revenue Outlook

Key Highlights

- Q2 adjusted earnings per share of $2.93 surpassed the Street’s $2.84 expectation

- Quarterly revenue reached $18 billion, topping the $17.84 billion projection

- Q3 revenue outlook’s midpoint fell short of Wall Street expectations

- Annual earnings forecast tightened to $13.65–$13.90, with midpoint below consensus

- ACN shares declined more than 3% before the bell, adding to a 27% year-to-date slide

Accenture (ACN) exceeded Wall Street expectations for both earnings and revenue in its fiscal second quarter, yet shares tumbled Thursday as the market zeroed in on underwhelming forward-looking guidance and persistent worries about enterprise client spending patterns.

Accenture, $ACN, Q2-26.

Solid growth, steady margins.

Adj. EPS: $2.93 Vs. $2.85 (est.)

Revenue: $18B Vs. $17.8B (est.)

Net Income: $1.83B

Bookings hit $22.1B with AI-led demand building.

Margin expansion remains modest in competitive environment.

Thread below pic.twitter.com/ucLPnbT3Up

— EarningsTime (@Earnings_Time) March 19, 2026

The consulting giant delivered adjusted earnings per share of $2.93 for the quarter, topping analyst expectations of $2.84. Quarterly revenue reached $18.04 billion, representing an 8.3% year-over-year increase and exceeding the consensus forecast of $17.84 billion.

The company secured new bookings totaling $22.1 billion during the period, marking a 6% uptick. CEO Julie Sweet highlighted “strong AI-driven growth” as a central theme, emphasizing advancements in artificial intelligence deployment across enterprise customer bases.

However, the positive quarterly results failed to impress Wall Street. ACN tumbled more than 3% in pre-market activity Thursday, dramatically outpacing the modest 0.3% decline in Nasdaq futures.

The negative market response reflects a challenging year for ACN shareholders. The stock has plummeted 27% year-to-date and 35% over the trailing twelve months—substantially underperforming the Nasdaq Composite, which has only retreated 4.7% in 2026.

Investor anxiety centers not on historical performance but on future prospects. Accenture’s third-quarter revenue guidance spanning $18.35 billion to $19.00 billion places the midpoint at $18.675 billion, trailing the $18.72 billion analyst consensus.

Client hesitation is mounting. Management indicated that enterprise customers are postponing major digital transformation initiatives while emphasizing near-term cost reduction measures.

Government Sector Headwinds Intensify

Accenture identified its federal business as creating a 1% revenue headwind for fiscal 2026, attributable to government agency budget cuts and spending reallocations.

This represents a meaningful challenge considering Accenture’s substantial public sector footprint. The deceleration in federal IT expenditures is impacting numerous large government contractors, with Accenture feeling the pressure.

For the complete fiscal year, Accenture refined its adjusted EPS guidance to $13.65–$13.90, narrowing from the previous $13.52–$13.90 range. The updated midpoint of $13.775 remains beneath the FactSet consensus estimate of $13.86.

The firm also marginally improved its full-year revenue growth projection, now anticipating 4%–6% growth in local currency compared to the earlier 3%–6% range.

Wall Street Maintains Cautious Stance

Industry analysts acknowledge that artificial intelligence could bolster long-term expansion for the company, though sluggish near-term demand isn’t expected to fully recover until 2028, based on current forecasts.

That timeline presents a prolonged waiting period for shareholders already grappling with substantial year-to-date losses. The investment community has remained skeptical about Accenture’s AI-driven growth narrative, partially because the very technology expected to fuel demand might simultaneously disrupt the high-margin consulting services the company provides.

Accenture acknowledged that its fiscal 2026 projection incorporates potential ramifications from Middle East geopolitical tensions, introducing additional uncertainty into the forward outlook.

ACN stock began Thursday’s trading session with a 27% year-to-date decline, and the Q2 earnings release provided little momentum to reverse that downward trend.

The post Accenture (ACN) Stock Plunges 3% Despite Q2 Earnings Beat on Weak Revenue Outlook appeared first on Blockonomi.

Opera, a Nasdaq-listed web browser company, is proposing to change how it is compensated by the Celo ecosystem, opting to receive native tokens instead of cash as it deepens its involvement with the network.

The company said Thursday it has proposed restructuring its commercial agreement, moving from US dollar-denominated quarterly payments to an allocation of 160 million CELO (CELO) tokens, subject to approval by Celo’s onchain governance community.

If approved, the shift would more directly align Opera’s financial incentives with the network’s performance and make it one of the largest institutional holders of CELO.

Celo is an Ethereum-aligned protocol focused on mobile-first payments, particularly for stablecoin transfers in emerging markets. Last year, it transitioned from a standalone layer-1 blockchain to an Ethereum layer-2 network.

Opera said the proposed change reflects its “belief in the long-term value” of the Celo ecosystem. The two have worked together since 2021, when Opera integrated Celo-native stablecoins into its browser wallet.

The partnership has increasingly centered on Opera’s MiniPay wallet, a self-custodial app built on Celo, which the company says has grown to 14 million users and focuses on stablecoin payments in emerging markets. MiniPay initiated connections with Latin America real-time payment platforms PIX and Mercado Pago in November.

To be sure, Opera isn’t the only company to accumulate tokens tied to a blockchain protocol. Ethereum software company ConsenSys has exposure to Ether (ETH) through its work on core infrastructure, such as MetaMask. Blockstream, a Bitcoin infrastructure company, holds Bitcoin (BTC) while developing products and services around the network.

Related: US ban on stablecoin yield could see others fill the void: Ledger exec

Opera reports revenue growth, announces buyback

Opera’s deeper integration with Celo comes on the heels of stronger-than-guided results, as the company reported growth across its core browser business and newer product segments.

In February, Opera reported fourth-quarter revenue of $177.2 million, up 22% year-over-year. Adjusted earnings came in at $41.9 million, representing a 24% margin.

For the full year, revenue reached $614.8 million, with adjusted earnings of $142.5 million.

The company also announced a $300 million share repurchase program, which reduces the number of outstanding shares and can increase earnings per share.

Opera’s Nasdaq-traded shares are up more than 21% over the past month and currently trading at around $15 a share, giving the company a market capitalization of roughly $1.3 billion.

Related: Abra targets Nasdaq listing in $750M deal with New Providence SPAC

Ripple keeps broadening its reach outside the US, while whales have shown notable interest in XRP.

Ripple remains one of the most talked-about projects in the crypto space, driven by constant developments across its ecosystem.

Despite the ongoing market correction, XRP (the company’s native token) has posted weekly gains, whereas some key indicators suggest a more substantial rally could be on the horizon.

The Global Expansion and More

In the last several months, the American-based entity expanded its footprint in the Middle East, while earlier in March, it announced plans to secure an Australian Financial Services License. Such a permit would allow the firm to operate a fully licensed payments platform in Australia and offer services under a recognized regulatory framework.

Just a few days ago, Ripple widened its reach across Brazil by becoming “the only solution in the region capable of serving institutions across the full spectrum of financial needs – from cross-border payments and digital asset custody to prime brokerage and treasury management.” Additionally, the company applied for a Virtual Asset Service Provider (VASP) license with the nation’s central bank.

It also made strides in the North American market by teaming up with i-payout to help the latter enable fast, transparent cross-border payments.

Another major news related to Ripple is Evernorth’s step forward to listing on the Nasdaq. The venture that focuses on accumulating, managing, and providing institutional exposure to XRP filed a Form S-4 registration statement with the US SEC in connection with its planned merger with Armada Acquisition Corp. II. Last year, the entity revealed that it had raised over $1 billion in gross proceeds from major institutions such as Ripple Labs, Pantera Capital, Kraken, SBI Holdings, and others.

The ETF Front

2025 was pivotal for Ripple, not only because its long-running legal battle with the SEC finally ended, but also due to the launch of the first spot XRP ETF, which offered full exposure to the asset. This happened in November, and the company behind the product was Canary Capital.

You may also like:

Some renowned firms, including Bitwise, Franklin Templeton, 21Shares, and Grayscale, followed suit, and the investment vehicles have so far generated a cumulative total net inflow of more than $1.2 billion.

However, over the past week, outflows have dominated inflows, indicating that institutional appetite for Ripple’s native token has been declining. After several consecutive red days, the netflow finally flashed green on March 17, and we have yet to see whether the interest will pick up in the short term.

XRP Outlook

As of this writing, Ripple’s cross-border token trades at around $1.44 (per CoinGecko), representing a 4% weekly increase. This contrasts with the losses that many other altcoins have posted during that timeframe.

The broken negative streak on the ETF front, as well as the recent whale accumulation, suggest XRP may record additional gains in the near future. As CryptoPotato reported, large investors purchased 200 million coins in the past two weeks, showing strong confidence in the asset and setting the stage for a possible move north.

The USD equivalent of the stash is roughly $290 million, and this group of market participants now controls 11.1 billion tokens, or 19% of XRP’s circulating supply.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

The European Central Bank (ECB) said it is looking for experts to help draft rules about how a digital euro would work in everyday payments in anticipation of legislation approving a central bank digital currency (CBDC) and a decision by the bank’s governing council to issue one.

The ECB opened applications for experts to help draft parts of the digital euro rulebook relating specifically to ATMs and card payment terminals used in stores, it said Thursday.

ECB President Christine Lagarde said in December the bank had completed its technical and preparatory work on the digital currency and it was now up to political institutions to act. The project, which aims to create a public digital means of payment, is under review by the European Council and the European Parliament. If approved, the central bank has signaled a potential rollout by 2029.

One workstream will define how ATMs and point-of-sale terminals process digital euro payments. This includes how devices connect, how they support offline transactions and how current payment standards can support the new currency. The goal is to ensure people pay with a digital euro at checkout or withdraw it from cash machines across the eurozone.

A second group will design a certification process for payment tools and infrastructure. It will set how providers test and approve systems used to accept digital euro payments in stores and payment networks.

While the central bank is working on the project, a group of 12 European banks are moving forward with their own version of a euro-pegged token. The banks, including BBVA, ING, PNB Paribas, have formed the Qivalis project, a plan to roll-out a euro-pegged stablecoin in the second half of 2026, aiming to offer blockchain payments without relying on dollar-backed tokens.

OpenClaw developers on GitHub, a platform for collaboration and version control, are being targeted in a phishing campaign using fake token giveaways to lure victims into connecting crypto wallets that can then be drained.

The attackers created bogus GitHub accounts and tagged developers in issue threads, claiming they had been selected to receive roughly $5,000 worth of CLAW tokens, Tel Aviv-based cybersecurity company OX Security said in a blog post on Wednesday.

The attackers’ posts link to a near-identical clone of the OpenClaw website, but with a key addition: a prompt to connect a crypto wallet. Once a wallet is connected, malicious code can trigger transactions or approvals that allow attackers to siphon funds. The phishing page supports major wallets including MetaMask, WalletConnect and Trust Wallet, widening the potential impact, OX said.

The campaign highlights an increasingly common attack vector in crypto: social engineering paired with wallet connection requests, often disguised as airdrops or developer rewards. By targeting GitHub users who interacted with OpenClaw-related repositories, the attackers made the outreach appear more credible.

OpenClaw is an open-source AI agent framework and developer tool that has recently attracted attention, and controversy, over crypto-related scams exploiting its name.

Peter Steinberger, the founder of OpenClaw, said last month he was about to delete the entire codebase because of crypto. “I didn’t know that they’re not just good at harassment, they are also really good at using scripts and tools.”

His statement followed a blanket ban he imposed on any mention of crypto, including bitcoin , in the project’s Discord after scammers in January hijacked OpenClaw’s old accounts. The hackers promoted a fake CLAWD token that briefly hit a $16 million market cap before collapsing after Steinberger When Steinberger publicly denied any involvement.

- Animoca Brands has announced a strategic investment in Avalanche.

- The move aims at promoting the adoption of projects built on Avalanche.

- Could the strategic investment boost AVAX price?

The Avalanche (AVAX) price has slipped below $10 as cryptocurrencies experience sell-off pressure.

AVAX could extend the decline to below $9, but is the announcement that Animoca Brands has partnered with Ava Labs to help expand adoption across the Middle East and Asia bullish for the token?

Animoca Brands partners with Ava Labs

Animoca Brands is one of the most influential entities in the web3 ecosystem, boasting notable traction globally and particularly in the East.

The announcement shared today, March 19, revealed that Animoca has signed a strategic partnership with Ava Labs, a company focused on advancing the Avalanche blockchain ecosystem.

While Animoca Brands did not disclose the amount invested, its leadership has termed the investment as a major one.

The focus will be on the deployment of capital in AVAX-based projects, as well as supporting product integrations and offering advisory support.

The Ava Labs team noted that Animoca brings a portfolio of over 600 investments and deep expertise across real-world assets, gaming, and digital identity.

With the collaboration, Ava Labs will target expansion across Asia and the Middle East.

“Avalanche combines scalable subnet architecture with EVM compatibility, which makes it particularly well suited for sovereign and institutional deployments — areas where we see growing demand globally,” said Omar Elassar, Animoca’s head of global strategic partnerships and managing director for the Middle East.

Avalanche RWA and DeFi markets

Avalanche (AVAX) ranks 22nd among the largest cryptocurrencies by market capitalisation, with a valuation of about $4 billion as of March 19, 2026.

However, the layer-1 network remains significantly smaller than leading altcoins in terms of overall market size and ecosystem activity.

Data indicates that Avalanche lags major chains across decentralised finance and real-world asset (RWA) adoption.

According to RWA.xyz, the total value of tokenised assets on Avalanche stands at roughly $1.3 billion, compared with about $15.7 billion on Ethereum.

Similarly, Avalanche’s DeFi total value locked (TVL) is around $1.9 billion, well below Ethereum’s $136 billion and the more than $18 billion recorded on Solana.

Despite this gap, the network’s on-chain finance footprint is showing signs of expansion.

The backing from Animoca Brands could help accelerate growth, while the AVAX token may benefit from further integrations and ecosystem adoption.

AVAX price outlook

AVAX trades around $9.41, down 3% in the past 24 hours.

From a technical perspective, AVAX is trading in a broad downtrend trajectory, with prices constrained within a tightening Bollinger Bands formation.

Currently, AVAX is near the technical indicator’s middle line after recent rejections from the upper band.

Meanwhile, the relative strength index (RSI) has flipped downward and hovers near 48 as bulls risk losing the neutral outlook to the momentum.

However, while sellers show resolve, they are not dominant.

If AVAX holds above $9, a broader recovery could allow for a breakout above $10 and a potential short-term retest of year-to-date highs near $15.

On the downside, failure to defend support zones could drag AVAX to lows of $8.20.

Key Takeaways

- XRP broke above $1.426 resistance after months of consolidation, jumping to $1.47 on surging volume

- Trading volume spiked over 250% during the move, indicating strong participation in the breakout

- Activity on the XRP Ledger continues climbing, with tokenized real-world assets approaching $1.14 billion in value

- Traders are watching if the $1.43-$1.44 level holds as support, with potential targets at $1.50-$1.55 if momentum sustains

XRP cleared a significant technical hurdle Thursday, breaking above $1.426 resistance that had capped the token’s rallies for several months. The move lifted XRP from approximately $1.41 to $1.47, marking the first decisive push above this ceiling since early 2026 and shifting short-term momentum decisively in favor of buyers.

The breakout came on dramatically increased volume, with trading activity spiking roughly 250% during the move. Roughly 170 million tokens traded during the latest 24-hour session, providing the liquidity needed to clear overhead resistance with conviction.

Technical Breakout Gains Traction

The key development was XRP’s decisive close above the $1.426 zone, which had repeatedly acted as a ceiling throughout the token’s multi-month consolidation range. Once cleared on strong volume, price action accelerated quickly toward the $1.47 level, with short-term charts now showing a sequence of higher lows forming below the breakout point.

This pattern suggests buyers are attempting to transform the former resistance zone into support. Momentum remains constructive as long as XRP maintains support above the $1.43-$1.44 area, where the initial breakout occurred. The next technical barrier sits near $1.48-$1.50, where previous rallies have stalled.

Ledger Activity Provides Backdrop

While the latest price advance lacked a clear XRP-specific catalyst, activity on the XRP Ledger has continued climbing steadily. Tokenized real-world assets on the network have risen sharply, with the value of tokenized commodities approaching $1.14 billion during the first quarter. This growing on-chain activity provides a constructive backdrop for the token’s technical breakout.

What’s Next for XRP

Traders are now focused on whether XRP can maintain support above the $1.43-$1.44 breakout level. If this zone holds, the token could extend the move toward $1.50 and potentially reach the $1.55 region as momentum builds and more buyers participate in the rally.

However, a failure to hold above $1.43 would weaken the breakout’s credibility and could pull XRP back toward the previous consolidation range near $1.39-$1.40. Such a move would likely reset technical momentum and require another consolidation period before buyers could regroup for another attempt at resistance.

The breakout’s sustainability will depend on maintaining strong volume participation and the broader bitcoin-led rally that sparked the initial move higher.

Summary

- Deribit data shows $20k Bitcoin put options are now the third most crowded strike by open interest, with about $596m notional, behind $125k and $75k calls heading into the quarterly expiry.

- Despite the doomsday optics, much of the $20k put exposure likely reflects traders selling tail-risk insurance for premium rather than betting on a 70%+ crash from spot.

- With max pain clustered around $75k and fear gauges elevated after macro and geopolitical shocks, the positioning highlights a split market: structurally bullish but acutely aware of low‑probability blow-up scenarios.

As Bitcoin’s largest quarterly options expiration of the year approaches on Deribit, a striking data point has emerged from the derivatives market: $20,000 put options have become the third most popular strike price by open interest, with a notional value of approximately $596 million. The figure reflects a market gripped by uncertainty — one in which traders are simultaneously betting on recovery and hedging for catastrophe.

According to data cited by CoinDesk, the top three strike prices by open interest ahead of the quarterly expiry are: $125,000 call options ($740 million), $75,000 calls ($687 million), and $20,000 put options ($596 million). The total notional value of the expiration stands at $13.5 billion, comprising 120,236 BTC in call contracts and 75,482 BTC in put contracts — a put/call ratio of 0.63, which, despite the elevated put activity, still leans modestly bullish in aggregate.

The surge in $20,000 put interest has raised eyebrows across the derivatives community, but analysts caution against reading it as a straightforward crash prediction. With Bitcoin currently trading below $70,000, the $20,000 strike represents a more than 70% decline from current levels — placing these contracts deeply out of the money.

Deribit’s global head of retail sales, Sidrah Fariq, noted that much of the positioning in deeply out-of-the-money puts likely reflects option selling for premium income rather than genuine expectation of such an extreme decline. Traders collect upfront premiums by selling low-probability puts, a common yield-enhancement strategy during periods of elevated implied volatility.

Still, the sheer scale of the position — which has been reported at close to $800 million in some analyses earlier this month — has drawn scrutiny. Whalesbook analysts noted that the concentration “warrants closer examination than simple hedging,” particularly as it coincides with a broader backdrop of geopolitical stress, rising energy prices, and macro uncertainty stemming from the Middle East conflict.

Indeed, market context matters. The Fear and Greed Index plunged to extreme fear territory in early March following the escalation of the Middle East crisis and effective closure of the Strait of Hormuz. Bitcoin briefly fell toward the $67,000–$69,000 range, with put/call ratios for near-term expirations spiking to as high as 1.70. Against this backdrop, the accumulation of $20,000 puts — even if primarily driven by premium selling — signals that at least some market participants are not ruling out tail-risk scenarios.

The maximum pain point for the quarterly expiration sits at $75,000, a level that market-makers may be incentivized to push toward before settlement — potentially creating a near-term magnetic effect on spot prices.

For now, the presence of nearly $600 million in $20,000 puts underscores the defining tension of this market cycle: institutional optimism on one end, and a deeply uncertain macro and geopolitical landscape on the other.

The line between Wall Street and Web3 just disappeared.

On March 18 2026, S&P Dow Jones Indices officially agreed to list the S&P 500 on the Hyperliquid blockchain. The first time the global equity benchmark has been sanctioned for decentralized perpetual trading.

These are not synthetic approximations running off oracle price feeds. They use direct institutional data feeds with sub-second settlement and 24/7 execution.

HYPE climbed 2.2% in 24 hours on the news. The token is already up 35.5% on the month.

Hyperliquid has cleared over $100 billion in total volume since inception. Now it is giving non-US investors a way to hedge American equities outside traditional banking hours, bypassing the liquidity monopoly of centralized exchanges entirely.

Institutional capital just trusted decentralized infrastructure with its most valuable intellectual property. That is not a small moment.

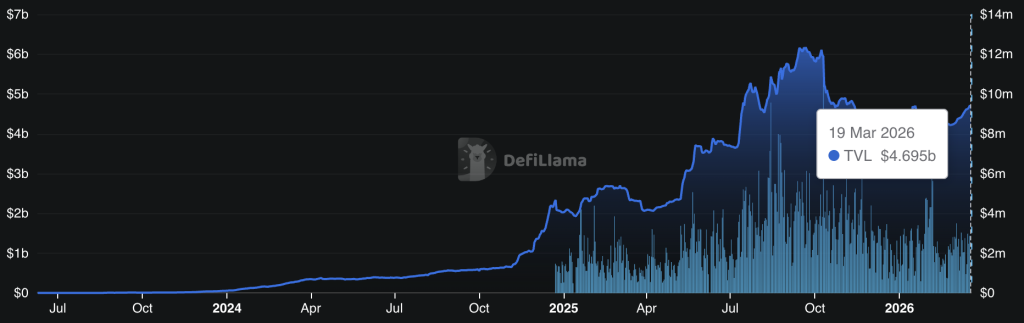

Can Hyperliquid (HYPE) Sustain Momentum as TVL Hits $4.7 Billion?

The S&P 500 listing is already moving Hyperliquid’s numbers in a meaningful way.

TVL has swelled to approximately $4.7 billion. Open interest across perpetual markets now exceeds $1.43 billion, surpassing the staking market cap of entire L1 chains like BNB Chain. Annualized volume is running at $1.5 trillion.

The structural advantage here is real. The always-on nature of the S&P product lets traders front-run macroeconomic data releases that drop while New York is sleeping. No waiting for markets to open. No gap risk sitting overnight on a centralized exchange.

HYPE is holding its gains despite broader market chop. Analysts are watching whether the 35.5% monthly run establishes a new support floor or gets faded.

The bull case is a full re-rating to match legacy clearinghouse valuations. The risk is the same as any heavily leveraged derivatives market. An unexpected geopolitical shock triggers a liquidation cascade and the momentum unravels fast.

The infrastructure is impressive. The leverage underneath it demands respect.

Bitcoin Hyper Targets Early Mover Upside as L2 Demand Spikes

Hyperliquid proves the appetite for high-performance decentralized trading is massive. But the bottleneck remains Bitcoin itself.

That is exactly the gap Bitcoin Hyper is building into. The first Bitcoin Layer 2 to integrate the Solana Virtual Machine. Low-latency programmable smart contracts without sacrificing Bitcoin’s security. Reportedly faster than Solana itself.

The presale has raised exactly $32,017,754.62. Current price is $0.0136772.

The Decentralized Canonical Bridge handles BTC transfers seamlessly, moving Bitcoin into a high-speed DeFi environment without the usual wrapping tricks or sketchy shortcuts.

While macro traders watch the S&P 500 and FOMC policy, infrastructure investors are betting on the picks and shovels of the next cycle. Bitcoin Hyper is positioning itself as exactly that.

Visit the Official Bitcoin Hyper Website Here

The post S&P 500 Launches on Hyperliquid via First Officially Licensed Perpetual Contracts appeared first on Cryptonews.

In today’s newsletter, Dumpling Bullish, independent digital asset commentator, writes about the growing influence of bitcoin’s derivatives stack on its price.

Then, in Ask an Expert, Leo Mindyuk from ML Tech, answers questions about the evolution of bitcoin investment products.

Bitcoin price discovery: no longer just a demand story

For most of its history, bitcoin had a simple pricing logic: limited supply, growing demand and the occasional panic in between. That logic still exists. It just no longer runs the show.

What runs the show now is the derivatives stack sitting atop the asset.

From spot market to leverage system

Over the past decade, bitcoin has moved from a predominantly spot-driven market into a layered derivatives ecosystem. Futures, perpetual swaps, options, exchange-traded funds (ETFs), structured products and prime brokerage lending have transformed the way price discovery occurs.

CME futures launched in December 2017, giving institutions a regulated, scalable way to short bitcoin for the first time and providing a mechanism to express bearish views at the top of what had been a 19x run. The asset saw an 80% drawdown. That did not kill bitcoin. It allowed disagreement to be priced more efficiently.

Then came the 2024 ETF approvals, acting as the foundation for a new derivatives layer inside U.S. equity markets.

Each addition didn’t change what bitcoin is. It changed where and how its price gets discovered.

Three variables that now matter most

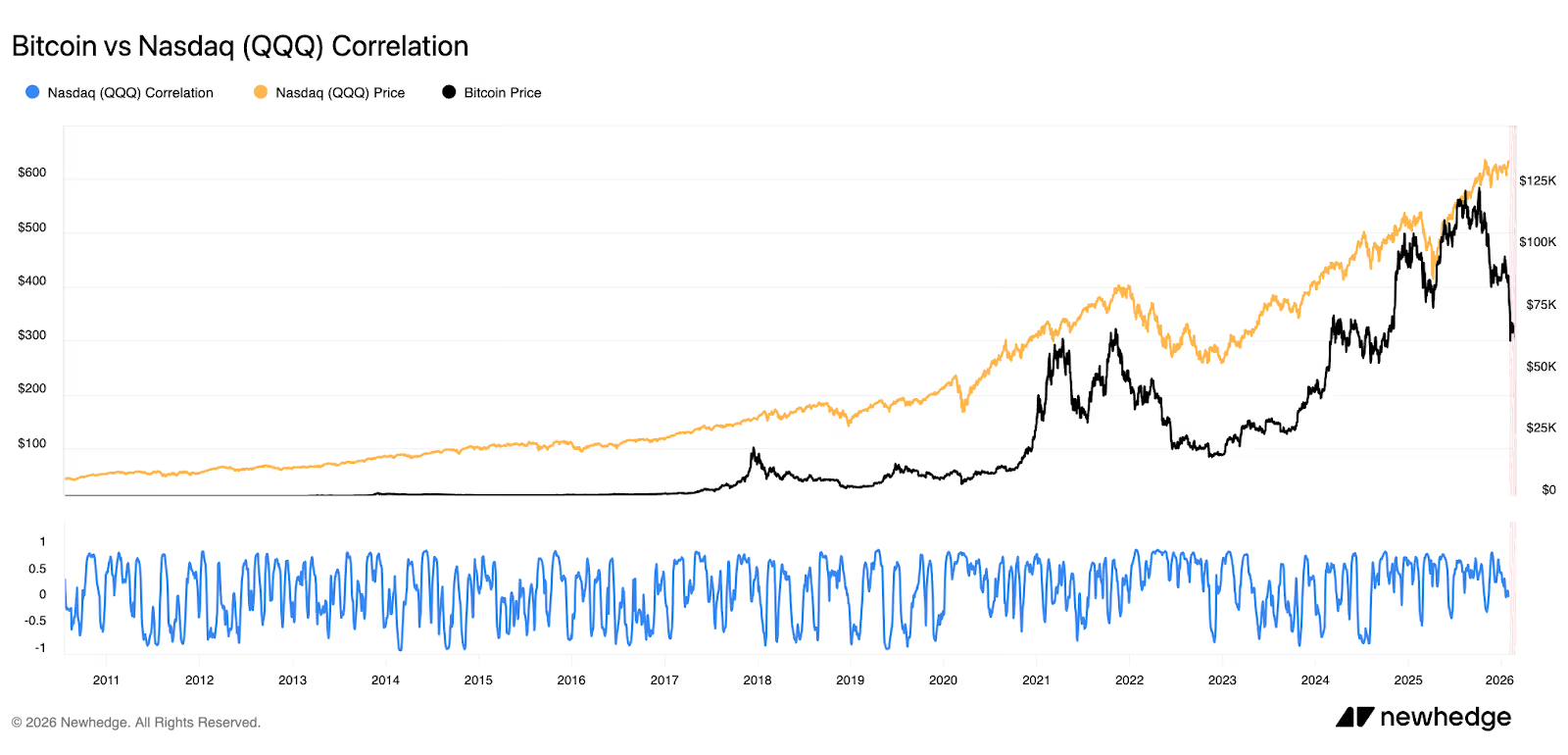

Real yields and dollar strength set the macro backdrop. Bitcoin has increasingly traded as a high-beta liquidity asset and when global risk appetite contracts, it sells off alongside equities and other risk assets, regardless of what the blockchain is doing.

Bitcoin 30-day rolling correlation with Nasdaq (QQQ), 2011 – present

Source: Newhedge

Derivatives positioning tells the short-term story. CME open interest and perpetual funding rates reveal whether a price move is built on genuine new demand or on leveraged speculation that will eventually unwind violently. When funding rates run persistently positive, the market is paying a premium to be long — and that premium is a fragility signal.

Bitcoin CME futures open interest and price, Dec 2017 – present

Source: CME Group via TradingView

ETF options mechanics have introduced a new transmission channel. When institutional investors buy calls or puts on the iShares Bitcoin Trust ETF (IBIT), dealers who sell those options must hedge by trading the underlying ETF and, in some cases, related futures or spot exposure. This hedging is procyclical. When Bitcoin rises, dealers must buy more; when it falls, they must sell. Modest directional moves get mechanically amplified. The result is that a meaningful share of Bitcoin’s short-term volatility is now generated mainly by equity market structure.

Financialization is not extinction

Gold offers a useful parallel. The development of futures and ETFs did not eliminate gold’s scarcity. It integrated gold into global macro portfolios and amplified its volatility during liquidity cycles. Bitcoin is undergoing a similar integration process at a faster pace. It is being absorbed into the global risk budget system. That absorption brings institutional capital, liquidity, and legitimacy. It also brings correlation, reflexivity, and the occasional violent unwind driven by forces that have nothing to do with the protocol.

Scarcity remains intact at the protocol level. But its influence on price is increasingly subordinated to the cost of capital and the mechanics of the derivative stack. Bitcoin is not losing its scarcity narrative. It is gaining a liquidity identity.

Scarcity anchors the asset. Liquidity sets the marginal price.

– Dumpling Bullish, independent digital asset commentator

Ask an Expert

Q: Over the past few years, bitcoin investment products have expanded from spot exposure to futures, options and ETFs. How do you see the evolution of bitcoin financial products shaping the way investors access the asset?

The evolution of bitcoin investment products mirrors the path we’ve seen in traditional asset classes. Early participants primarily accessed bitcoin through direct ownership — buying and holding the asset itself on crypto exchanges. Over time, as institutional interest increased, the market began developing a broader toolkit: regulated futures and options, structured products and regulated fund structures and more recently, spot ETFs.

This expansion is important because it changes bitcoin from simply being a speculative asset to something that can be integrated into portfolio construction and risk management frameworks. Different investors have different needs. Some want direct exposure to the asset’s price movement, while others want regulated vehicles, derivatives for hedging or ways to express more nuanced market views.

As the ecosystem matures, financial products make Bitcoin easier to access through familiar structures, which lowers barriers for institutional investors and broadens the ways the asset can be incorporated into diversified portfolios.

Q: In traditional markets, financial products often evolve from simple exposure to more complex structures like leveraged, inverse, and derivatives-based strategies. Are we starting to see a similar progression in the bitcoin ecosystem?

Yes, and it’s a natural progression. In most asset classes, markets begin with simple spot exposure and gradually develop layers of financial instruments that allow investors to manage risk, hedge positions or express different market views. Bitcoin is following that same trajectory.

Initially, the focus was simply on gaining exposure to the asset itself. Today, we’re seeing a more developed ecosystem that includes derivatives, volatility trading and structured products. These tools allow investors to do much more than just speculate on price appreciation. They can hedge downside risk, trade volatility or construct market-neutral strategies.

What’s interesting is that crypto markets often evolve faster than traditional markets because the infrastructure is digital and global. As liquidity deepens and regulatory frameworks become clearer, we’ll likely see even more sophisticated products emerge that resemble strategies commonly used in equities, commodities and fixed-income markets. For example, I expect growth in various income-generating ETFs — instruments for inversed, leveraged or broader crypto factor-based exposure. Moreover, we will likely see a tremendous growth in crypto option markets.

Q: With the growth of futures markets and the introduction of spot ETFs, how might the next generation of bitcoin products expand investor use cases, whether for hedging, leverage, or more sophisticated portfolio strategies?

Futures markets already allow investors to hedge exposure or express directional views without holding the asset directly. ETFs have made bitcoin accessible through traditional brokerage accounts. The logical next step is products that focus on portfolio outcomes.

As that happens, bitcoin starts to look less like a standalone trade and more like a portfolio building block. That’s ultimately where the market is heading: giving investors the flexibility to express views on the market in much more nuanced and sophisticated ways with the ease of access.

– Leo Mindyuk, CEO & CIO, ML Tech

Keep Reading

Key Takeaways

- Opera proposes replacing cash arrangement with 160M CELO token allocation

- Request represents approximately 27% of current circulating supply

- MiniPay’s 14M+ registrations justify expanded network participation

- Voting power capped at 10% to preserve decentralized governance structure

- Strategic pivot reflects Opera’s deepening commitment to blockchain payments

Opera Limited (OPRA) stock traded around $14.40 following a minor pullback, while the browser company unveiled plans for a substantial cryptocurrency arrangement with Celo. The firm has submitted a governance request to exchange its existing cash-based agreement for a significant token position. This transition could establish Opera among Celo’s most influential network participants.

Browser company transitions from cash payments to long-term token ownership

Opera has presented a formal governance petition requesting 160 million CELO tokens distributed across a three-year timeline. The arrangement would eliminate quarterly cash disbursements in favor of direct token ownership. This structural change creates stronger alignment between Opera’s financial interests and the blockchain’s success.

The proposed allocation accounts for approximately 27% of CELO’s currently available circulating tokens. Additionally, it comprises roughly 16% of the cryptocurrency’s maximum capped supply. The substantial size of this request demonstrates Opera’s intention to establish a meaningful presence within the ecosystem.

CELO was trading near $0.07 during reporting hours, significantly below its 2021 all-time highs. Despite current valuations, the token allocation provides considerable upside potential should market conditions improve. Consequently, Opera’s strategy balances forward-looking opportunity with present-day market realities.

Decentralization safeguards and treasury mechanics structure token distribution

The governance proposal details a single transfer from Celo’s unreleased token reserves to an Opera-managed wallet. This arrangement formalizes the browser company’s transition to long-term ecosystem participant. The mechanism replaces ongoing payments with consolidated token ownership.

The framework restricts Opera’s governance participation to maximum 10% of total staked CELO under standard circumstances. This limitation safeguards the network’s decentralized decision-making processes. Emergency situations may permit temporary adjustments to these restrictions.

Token holder consensus remains essential before implementation, as community members will evaluate the proposal through established governance procedures. Stakeholder feedback will determine whether the allocation magnitude receives approval. The final decision will establish Opera’s authority and influence within Celo’s governance framework.

Wallet platform success drives Opera’s strategic positioning within payment network

Opera grounded its token request in MiniPay’s demonstrated performance, its self-custody digital wallet developed on Celo infrastructure. The application enables peer-to-peer stablecoin transfers using simple phone number identification. It further accommodates regional payment systems across diverse geographical markets.

MiniPay has accumulated over 14 million user registrations following its 2023 introduction. The platform has facilitated more than 420 million transactions spanning across 66+ countries worldwide. These metrics underscore its significance in generating network engagement and activity.

Opera intends to enable over 50 million users to convert rewards into USDT directly through MiniPay. This feature integration may accelerate wallet adoption and transaction throughput. Through these developments, Opera reinforces both operational and economic ties with Celo.

Opera shares registered near $14.60 during recent trading following a modest decline. The organization continues broadening its cryptocurrency involvement through product development and direct token ownership. The pending agreement could fundamentally transform its standing within blockchain-powered payment systems.

Ashley Furniture cuts hundreds of jobs in Mesquite, Texas plant consolidation

Hegseth: Iran War Not ’Forever War’

Pistons’ Cade Cunningham reportedly diagnosed with collapsed lung

-

Crypto World5 days ago

Crypto World5 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech4 days ago

Tech4 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Sports5 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business4 days ago

Business4 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business5 days ago

Business5 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World5 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business3 days ago

Business3 days agoAustralian shares drop as Iran war enters third week

-

Business5 days ago

Business5 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World3 days ago

Crypto World3 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports6 days ago

Sports6 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics1 day ago

Politics1 day agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Business7 days ago

Business7 days agoTrump demands Powell cut rates as Iran conflict raises energy prices

-

Fashion3 days ago

Fashion3 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos23 hours ago

News Videos23 hours agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World7 days ago

Crypto World7 days agoSenate Votes to Include CBDC Ban in Bipartisan Housing Bill

-

NewsBeat7 days ago

NewsBeat7 days agoDeane Road crash near Bolton colleges and university

-

Crypto World23 hours ago

Crypto World23 hours agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

News Videos7 days ago

News Videos7 days agoTom Lee: The 100x Opportunity EVEN Bigger Than Bitcoin (New Ethereum Prediction 2026)

You must be logged in to post a comment Login