Crypto World

Adam Back says Strategy’s Bitcoin sale is a feature, not a flaw

Blockstream CEO Adam Back said concerns over Strategy’s small Bitcoin sale are overblown, framing the move as normal treasury management rather than a warning sign for the company’s Bitcoin plan.

Summary

- Adam Back said Strategy’s small Bitcoin sale showed balance sheet flexibility, not bearish treasury change.

- Strategy sold 32 BTC for about $2.5 million to fund preferred stock dividend payments due.

- Crypto.news later reported Strategy bought 1,550 BTC, keeping its accumulation story active for now again.

Speaking in a Bloomberg interview shared on YouTube, Back addressed questions about Strategy selling 32 BTC to help pay preferred stock dividends. He said the sale showed the firm could meet obligations while keeping Bitcoin at the center of its balance sheet.

Back frames sale as balance sheet use

Back argued that the market should not treat the 32 BTC sale as a bearish signal. In his view, Strategy used a small part of its Bitcoin position to support investor payments and reduce pressure on the capital structure.

He also said the move showed how Bitcoin can function inside a corporate treasury. Rather than showing weak conviction, it showed that a company can hold Bitcoin, raise capital against it and use a limited amount when cash needs arise.

Back’s argument also places the sale inside a larger shift in corporate Bitcoin finance, where companies use BTC alongside preferred shares, debt, common equity, and market tools today.

Strategy’s first sale drew attention

As previously reported by crypto.news, Strategy disclosed on June 1 that it sold 32 Bitcoin between May 26 and May 31 at an average price of $77,135. The sale raised about $2.5 million.

The filing said proceeds were expected to fund distributions on the company’s preferred stock. The sale represented about 0.0038% of Strategy’s Bitcoin holdings at the time, but it drew attention because Michael Saylor had long promoted a “never sell” message around Bitcoin.

Crypto.news later reported that Saylor separated personal investor advice from corporate treasury actions. “I said to YOU never sell your bitcoin,” Saylor said at BTC Prague.

Preferred dividends remain in focus

The debate centers on Strategy’s preferred stock model. Preferred shares can give investors yield, but they also create recurring cash needs that the company must meet through cash reserves, equity issuance or limited Bitcoin sales.

Strategy’s STRC preferred stock has faced pressure after falling below its $100 par value. As crypto.news reported, Saylor defended the company’s Bitcoin-backed strategy and said its Bitcoin and cash reserves still exceeded outstanding debt by about $48 billion.

Some critics argue that dividend obligations could become harder to manage if market conditions weaken. Supporters say the 32 BTC sale showed Strategy has several funding tools and does not need to abandon its long-term accumulation plan.

Strategy remains a net accumulator

The sale did not stop Strategy from buying more Bitcoin. Crypto.news reported that the company later bought 1,550 BTC for $101.3 million, lifting its holdings to 845,256 BTC after the sale disclosure.

That purchase was nearly 50 times larger than the 32 BTC sale. It helped support Back’s view that the transaction was not a broad retreat from Bitcoin.

Saylor has also argued that Bitcoin does not need staking or protocol-based yield. In a separate post covered by crypto.news, he framed Bitcoin as the base layer for credit, money, yield and equity products.

For now, the issue is not whether Strategy still wants Bitcoin. The question is how it funds preferred dividends while keeping investor trust and managing balance sheet risk.

The stablecoin payments company said client funds were unaffected and that the financial impact would be absorbed through its treasury reserves.

Changpeng Zhao (CZ), Binance’s co-founder, told his X followers that they cannot build wealth without understanding Dollar-Cost Averaging (DCA), a basic financial term he said too many crypto investors ignore.

The comment followed a question CZ posted two days earlier, asking whether bull or bear markets offer better entry points for long-term holding. His answer favored a simpler, disciplined approach over market timing.

Why CZ Raised the Timing Question

CZ posed the original question on July 24, asking followers directly whether bull or bear conditions suit long-term investors better. The post drew over 1.8 million views within two days, showing how often newer investors ask this exact question.

Crypto markets swung sharply through 2026. Bitcoin spent months grinding through a bear market before recent signs of stabilization emerged. That backdrop likely shaped CZ’s question, since entry timing feels more urgent during a downturn than during a rally.

CZ has his own record of timing missteps. He recently admitted he misjudged the stablecoin market, dismissing it early before it grew past $300 billion. That history may explain why he now steers newer investors toward a repeatable process instead of one high-stakes decision.

What Is DCA?

Dollar-Cost Averaging means investing a fixed amount at regular intervals, regardless of price. The approach removes the need to predict tops or bottoms, since each purchase averages out over time.

CZ’s underlying point was blunt. Investors who skip basic terms like DCA, he suggested, will struggle to build lasting wealth in volatile markets. CZ’s message pushed back against the instinct to time entries perfectly.

The strategy answers a documented problem. Weak buy-and-hold returns among 2025 token listings showed how badly timed lump-sum entries can underperform. Spreading purchases across both bull and bear phases sidesteps that risk, which is why some investors treat DCA as a long-term retirement strategy rather than a short-term trade.

DCA’s biggest advantage may be psychological rather than mathematical. Regular, automated purchases limit the emotional decisions that often accompany sharp swings, whether markets grind lower or turn toward a new rally.

Some traders currently point to early bottom signals as reason for optimism, while others stay cautious given how long the downturn has lasted. Either way, CZ’s simpler approach offers a middle path that does not depend on guessing which camp is right.

Whether the current stretch counts as bear or bull remains debatable. CZ’s advice suggests investors do not need to settle that debate before they start buying.

The post Changpeng Zhao Warns Investors: You Can’t Get Rich Without Knowing This One Term appeared first on BeInCrypto.

Crypto markets have ticked up this Monday morning as investors brace for a volatile week ahead, with all eyes on the US central bank. Meanwhile, Iran said it will halt its attacks as long as the United States does the same, a senior Iranian official told Reuters on Sunday.

The US paused its bombing campaign on Friday following 13 nights of intensifying airstrikes. The development has caused a dip in oil prices and a jump in US stock futures and crypto markets.

Economic Events July 27 to 31

July’s Consumer Confidence data is due on Tuesday, which reflects how consumers are spending. This is followed by the week’s big event on Wednesday when the Fed announces its rate decision and Fed Chair Kevin Warsh holds a press conference, setting policy direction.

The meeting comes amid growing uncertainty about tech sector valuations, AI infrastructure spending, and economic growth trajectory amid a backdrop of inflationary pressures.

The market “feels very frothy,” Kristina Hooper, chief market strategist at Man Group, told Reuters. “Investors are, to a certain extent, walking on eggshells, and they’re more likely to react negatively to any signs of imperfection.”

Odds of rates remaining the same have fallen to 63.7% on the CME Fed watch tool, which now predicts a 36.3% chance of an increase.

July’s PCE inflation data is due on Thursday, followed by the Michigan Consumer Sentiment data and Inflation Expectations data on Friday.

Key Events This Week:

1. Markets React to US/Iran Pausing Strikes – Today, 6 PM ET

2. July Consumer Confidence data – Tuesday

3. July Fed Interest Rate Decision – Wednesday

4. Microsoft, $MSFT, Meta, $META, Report Earnings – Wednesday

5. July PCE Inflation data – Thursday…

— The Kobeissi Letter (@KobeissiLetter) July 26, 2026

Meanwhile, more than 15% of S&P 500 companies, including Microsoft, Meta, Apple, and Amazon, are reporting earnings this week.

Crypto Market Outlook

Crypto markets have moved higher over the weekend, with total capitalization ticking up to $2.3 trillion on Monday morning in Asia.

Bitcoin moved up 1% on the day to tap $65,500 in early trading before a minor retreat. The asset is still facing heavy resistance above $66,000, which has kept it range-bound for almost two months.

Ethereum has made a bigger 3.5% move to hit a seven-week high of $1,960, but it also faces resistance at this level and hasn’t been over $2,000 since June 2. Only a handful of altcoins were moving, and these included Zcash, Chainlink, and Uniswap, while Monero had lost 4%.

The post 4 Things That May Move Crypto Markets This Week as Fed Rate Hike Odds Increase appeared first on CryptoPotato.

Robinhood Chain has become the leading blockchain by real-world asset (RWA) holder count. This comes less than a month after its public mainnet launch, and it marks a massive milestone in the company’s push into on-chain finance.

The network is an Ethereum layer 2, and it went live on July first. So far, it has surpassed established ecosystems despite its relatively short operating history, at least in this domain.

Retail Distribution Becomes Robinhood’s Main Advantage

Unlike many blockchain projects that first focus on crypto-native users, Robinhood entered the industry with millions of existing brokerage customers. That distribution is obviously translating into rapid adoption of real-world assets (RWAs).

Data from RWA.xyz shows that Robinhood has accumulated almost 330,000 RWA holders, alongside $24.12 million in distributed asset value and over $20 million in represented asset value. The network hosts around 1900 tokenized assets, while monthly transfer volume stands at $750 million at the time of this writing.

Second in line by this metric is Solana, followed by Plume, Ethereum, and BNB Chain.

It’s worth noting, however, that Ethereum dominates when it comes to total value. Almost $18 billion worth of RWA assets are hosted on the network. Second in line is BNB Chain, followed by Solana.

This milestone comes as the platform continuously expands its tokenized stock offering across Europe. The network was designed specifically for regulated financial assets rather than general-purpose DeFi, which allows users to trade tokenized US equities and ETFs around the clock. Transactions are settled on Ethereum through Arbitrum technology.

Early Success Driven Not Only by RWAs

Still, it’s interesting to note that tokenized assets are not yet the chain’s dominant activity driver.

Meme coin trading currently accounts for the majority of decentralized exchange volume. Tokenized stocks represent only a small portion of on-chain value today, although the company views them as the network’s long-term differentiator. Recall the frenzy surrounding the viral meme coin CASHCAT – a cryptocurrency that exploded in value in a few short days only to plummet almost immediately after, leaving stories of overnight millionaires and missed fortunes altogether.

Stablecoins are also growing on the network, noting a 22% increase in their market capitalization, currently pushing $500 million, according to DeFiLlama.

The post Robinhood Chain Becomes Largest Blockchain by RWA Holder Count appeared first on CryptoPotato.

Withdrawals from crypto exchange BitMart appeared to slow after it announced plans to wind down its operations.

On Monday, blockchain analytics account Lookonchain reported that only 58 wallets withdrew about $805,000 in over 24 hours. It added that the exchange had not processed any withdrawals during the latest eight-hour period it tracked.

X users also continued to report withdrawal difficulties. One user said they received an email stating that a USDT withdrawal had been completed even though the transaction had not been processed and their account displayed an “on-chain withdrawal freeze.” Another user said a $30 test withdrawal remained pending for over 30 minutes. These are individual claims and could not be verified.

BitMart’s ability to return customer funds smoothly will be a key test of its promised “orderly” wind-down and could determine whether declining confidence develops into a broader rush for the exits.

BitMart previously said withdrawals remain available but warned that requests may face additional compliance and security checks, including reviews of customer identities, login devices, withdrawal addresses, trading histories and sources of funds. The exchange may also request proof of identity, address, source of funds or ownership of the receiving wallet.

Cointelegraph reached out to BitMart for comments but did not receive a response before publication.

BitMart token extends decline as exchange prepares to close

On Sunday, BitMart announced that it would stop accepting new registrations and deposits while restricting new spot orders and futures positions. Trading services are scheduled to end on Aug. 26, with the platform expected to cease operations entirely on Jan. 31, 2027.

Arkham-identified wallets attributed to BitMart held about $69 million in crypto assets on Monday, down from roughly $102 million on July 6.

Related: Storj files for bankruptcy, explores equity path for tokenholders

BitMart’s BMX token traded near $0.057 on Monday and had fallen about 81.5% over seven days, according to CoinGecko. The token was trading around $0.31 late Friday before the exchange’s shutdown became public.

BMX token’s 24-hour chart. Source: CoinGecko

The closure also prompted discussion about whether larger exchanges could acquire smaller competitors.

Binance co-founder Changpeng Zhao said acquiring a centralized exchange was more complicated than buying other businesses because buyers could inherit security vulnerabilities, including backdoors left by previous teams. He added that acquisitions remain possible but require greater scrutiny.

Magazine: Why Australia’s $17B crypto opportunity depends on regulation

Crypto World

South Korean Traders Push MORPHO Whale Transactions to Highest Level Since October 2025

South Korean demand pushed Morpho (MORPHO) whale transactions, wallet creation, and exchange outflows to multi-month highs on Saturday. The spike landed the same day Upbit opened a won trading pair.

Activity has since cooled across all three metrics. Still, Upbit handles more MORPHO volume than any other venue.

What Happened on Saturday

Santiment recorded 68 whale transactions above $100,000 in a single day. That is the highest daily count since October 2, 2025.

Wallet creation moved with it. 337 new MORPHO addresses appeared, the strongest reading since March 15, 2026.

Exchange balances thinned at the same time. Traders shifted 4.35 million MORPHO off platforms, the largest single-day outflow since February 4, 2026.

Follow us on X to get the latest news as it happens

The simultaneous bullish signal arrived as Upbit opened trading for MORPHO in the KRW market at 6 p.m. KST that evening. The announcement also triggered a price surge.

MORPHO climbed from about $1.93 to an intraday high of $2.17 within hours, and daily volume rose close to 5 times to near $71 million, according to CoinGecko.

Upbit Still Handles More MORPHO Volume Than Binance

Nonetheless, the rush proved short. MORPHO slipped to nearly $1.9 on Sunday and now trades near at $1.99, roughly where it sat a week earlier. Daily volume has fallen back to about $22 million.

Still, the Korean flow did not leave entirely. The Upbit KRW pair accounts for 12.26% of daily MORPHO volume, the largest share of any market, ahead of Binance.

Won pairs across all venues make up about 13% of turnover. That concentration gives Korean retail traders significant influence over short-term MORPHO price movements.

The next few weeks should show whether Korean access turns into steady demand or stays a one-day event.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post South Korean Traders Push MORPHO Whale Transactions to Highest Level Since October 2025 appeared first on BeInCrypto.

Risk-on peace trades are back in vogue after the U.S. and Iran held fire on Sunday, sending oil prices lower.

Bitcoin , the leading cryptocurrency by market value, is back above $65,000, with prices up about 1.2% over 24 hours. Ether (ETH) has risen by over 3% to nearly $1,950 alongside 1% to 2% gains in other top 10 token, including solana (SOL) and XRP (XRP).

Futures tied to WTI gapped lower on Monday, trading around 5% lower at $85 as of this writing, while those linked to Nasdaq and S&P 500 traded half a percent higher. Currency markets also showed risk-on trends, with the Aussie dollar and euro gaining against the U.S. dollar.

The United States and Iran paused military strikes against each other for a second consecutive day, creating room for a diplomatic breakthrough. The war, which began in late February, entered a fragile ceasefire in the second quarter, but it quickly unraveled.

Iran reportedly said that it would continue to halt airstrikes as long as the U.S. did the same, marking a tenous start of what appears to be yet another peace process.

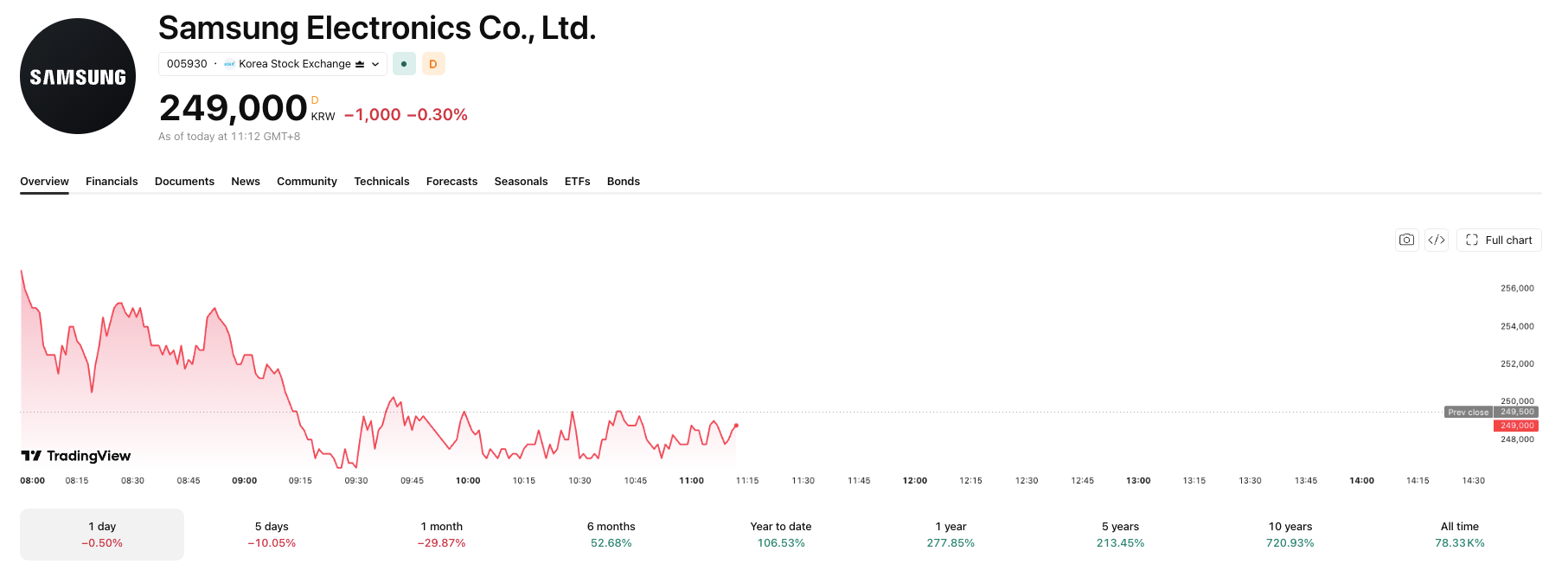

Samsung Electronics and SK Hynix signed a combined $950 billion in artificial intelligence (AI) chip supply deals with Nvidia and Broadcom over the weekend.

Both stocks still fell in Monday trading, a disconnect that shows how much of the AI rally already sits in the price.

A Massive AI Infrastructure Deal

SK Hynix will supply $750 billion in memory chips to Nvidia and other US companies over several years. Nvidia put its own portion of that deal at $500 billion. The agreement covers new data centers targeted for 2027, and SK Hynix affiliate SK Telecom will build a cloud business on Nvidia’s Vera Rubin systems.

Nvidia enterprise vice president Raj Mirpuri said the deal secures a stable supply of high-bandwidth memory (HBM), the specialized chips that power AI processors and graphics cards.

Samsung separately signed a memorandum of understanding worth an estimated $200 billion with Broadcom. The agreement expands their memory and foundry collaboration, the companies said in statements Friday.

Is the AI Boom Already Priced In?

Despite the scale of the announcements, SK Hynix shares traded at 1,752,000 won Monday morning, down a little from Friday’s close, but also down 11.38% over five sessions. Samsung fell 0.50% to 248,500 won, extending its own 10.05% five-day slide. Nvidia closed down 0.92% at $206.84 in Friday’s session before edging higher in overnight trading.

The muted reaction fits a recent pattern. SK Hynix shares have slid even on positive news this month. US investors already pay a premium for its shares compared with Seoul, a gap that opened after its blockbuster Nasdaq listing earlier in July.

Both stocks are up sharply this year on AI demand, so traders appear to be booking profits rather than chasing another AI headline, regardless of the deal size.

The bigger test comes later this week. Samsung and SK Hynix report quarterly earnings that will show whether soaring chip orders are converting into profit. That result will tell investors whether this month’s record deal flow deserves a second look, or whether it is already old news.

The post SK Hynix, Samsung Ink $950 Billion AI Chip Deals, But Stocks Still Slide appeared first on BeInCrypto.

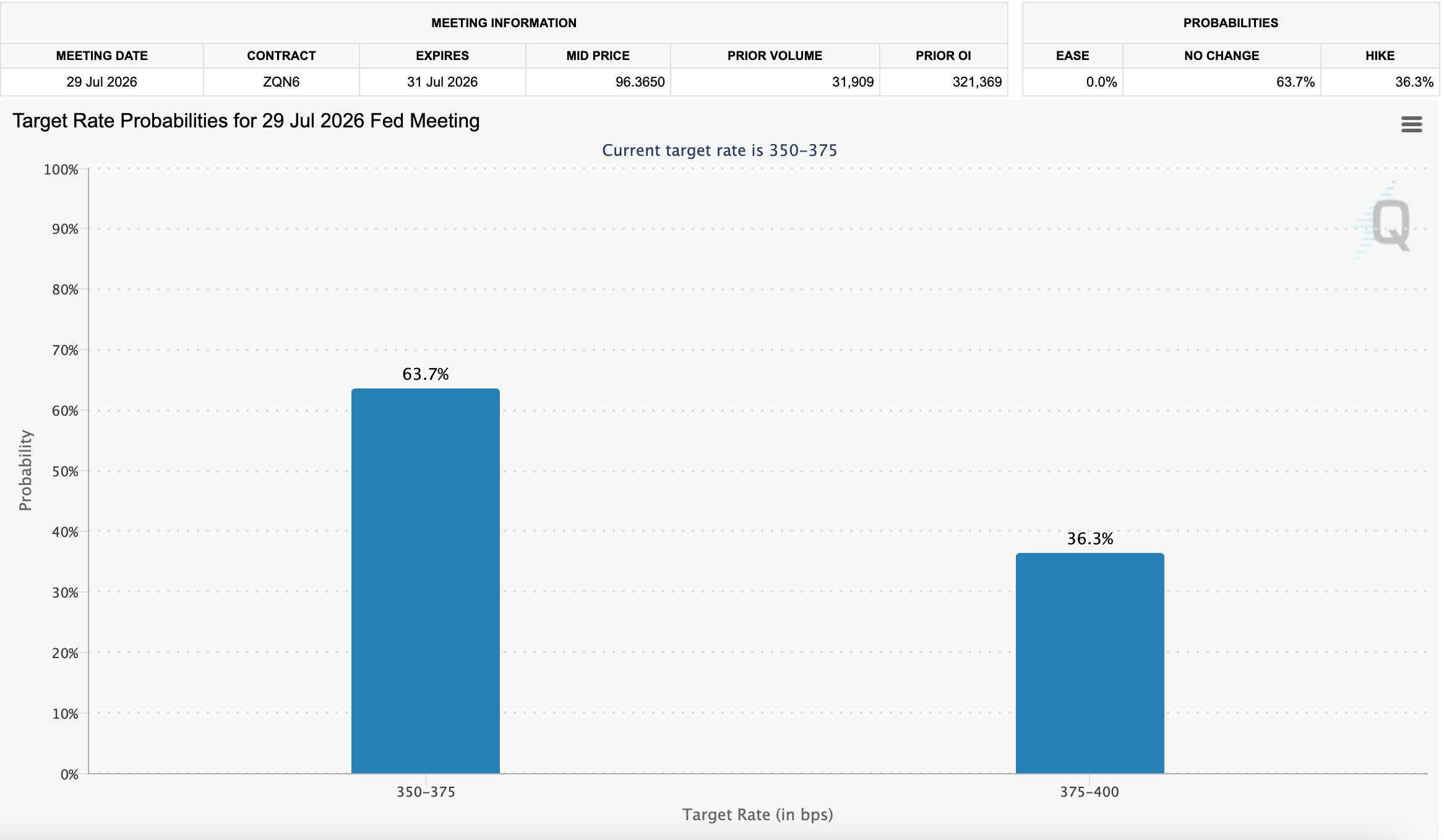

Federal Reserve Chairman Kevin Warsh keeps predicting a Fed “family fight.” Wednesday’s policy meeting could finally deliver a real one, with economists expecting at least two hawkish dissents over interest rates.

Warsh has used the phrase 13 times since his April nomination hearing, according to a CNBC tally. His first meeting as chair ended in a unanimous hold last month.

A Feud That’s Been Building for Months

Wall Street expects a different outcome this week. JPMorgan’s Michael Feroli predicts a contested vote. He names Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan as likely dissenters.

“The July FOMC will be a family feud… just as Kevin Warsh intended.”

Oscar Munoz, TD Securities

TD Securities’ Oscar Munoz agrees. Traders are already repricing the odds. CME Group’s FedWatch tool now shows 34.2% odds of a quarter-point hike, up from 12.8% just a week ago.

Oil and Chips Are Feeding the Feud

A collapsed U.S.-Iran ceasefire has pushed oil prices higher again. Brent crude climbed back above $100 a barrel, undoing the recent oil price relief. But a recent pause in hostilities has brought that price back down for the moment.

Chip shortages tied to the AI boom have raised consumer electronics prices too. Hyperscalers keep spending heavily on AI infrastructure, and that shows no sign of slowing. Fed Governor Chris Waller argues the central bank cannot just watch inflation and hope it fades, echoing Warsh’s own recent complaint about the Fed’s inflation framework mistake.

Cleveland Fed President Beth Hammack has been especially blunt about the stakes. She says businesses and consumers are both losing patience with prices.

“For the first time in my tenure, I’m hearing from businesses who say they think we need to take action to curb inflation, and from consumers who can’t make ends meet about a growing sense of despair.”

Beth Hammack, Cleveland Fed President

A softer June inflation report still favors a hold on Wednesday. The Fed’s next test also lands just as U.S. midterm elections near, adding political weight to the vote. But two hawkish dissents would turn Warsh’s family fight into the real feud he predicted all along.

The post Kevin Warsh Wanted a ‘Family Feud’ at the Fed; At Wednesday’s Meeting He Might Get One appeared first on BeInCrypto.

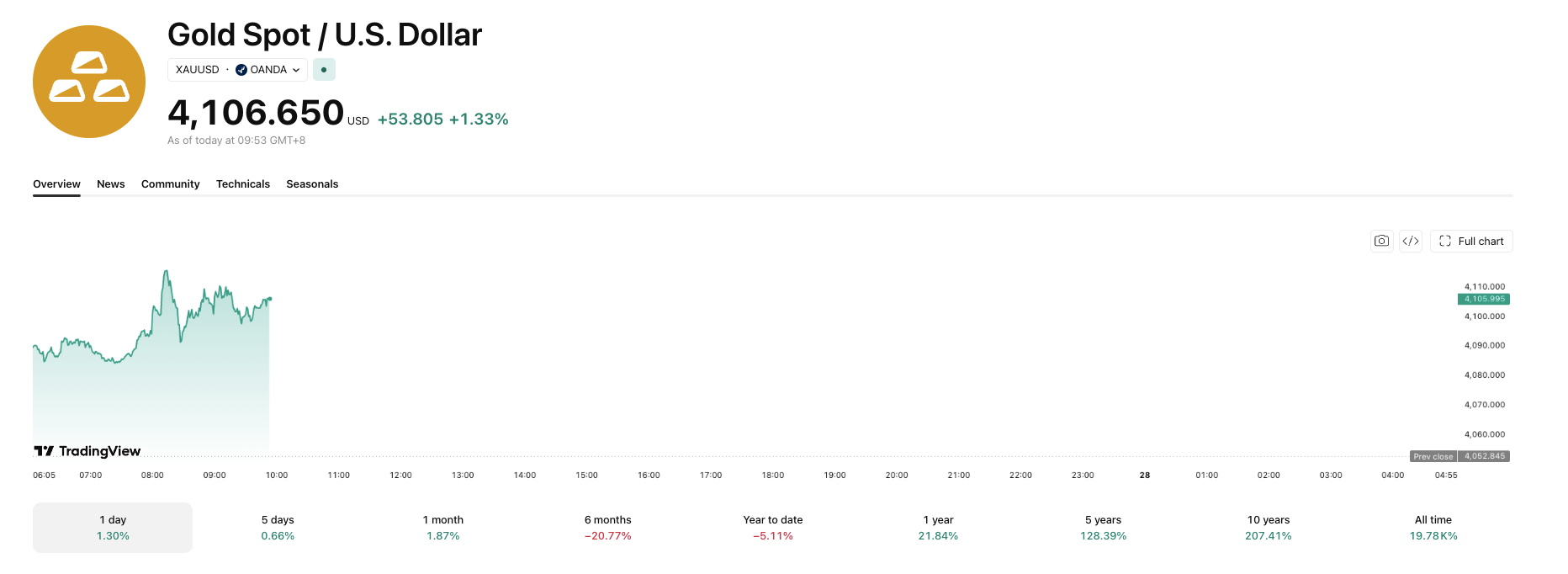

Gold climbed more than one percent in Asian trading Monday. A weekend pause in US-Iran hostilities pushed oil prices lower and eased fears of prolonged high interest rates.

Spot gold traded at $4,106.65 per ounce Monday, up 1.33% on the day, according to TradingView data.

Oil Retreat Lifts Precious Metals

The pause came as advisers reportedly warned Trump that the military was nearing the limit of viable targets in Iran. They also flagged concerns about draining U.S. munitions stockpiles, prompting the pause in strikes. Iran will halt its own attacks as long as Washington does the same, a senior Iranian official told Reuters.

Oil prices tumbled as much as 7% on hopes for a diplomatic resolution. That reverses recent forecasts that Brent crude could revisit its war-era peak near $120 after going above $100 at the weekend. Lower energy costs typically ease inflation, reducing the odds the Fed holds rates high for longer. Gold’s appeal fades when rates stay high since the metal pays no yield.

Traders are still pricing an 80% chance of a rate hike in September, according to the CME Group’s FedWatch Tool, which tracks futures-implied rate expectations.

Gold also Boosts Silver

Other precious metals rallied in tandem. Spot silver climbed 2.7% to $59.74 an ounce, building on a recent breakout above key resistance. Platinum gained 2% to $1,619.75, and palladium rose 2.3% to $1,271.93.

COMEX gold speculators added 4,438 contracts to their net long position in the week to July 21. That brought the total to 123,586 contracts, according to CFTC data.

The Fed’s rate decision this week will test whether the truce holds long enough to sustain the rally. A split among 104 economists over the central bank’s next move shows how uncertain the path remains. That uncertainty deepens if fighting resumes and oil prices reverse.

The post Gold Gains as US-Iran Pause Also Sends Oil Prices Lower appeared first on BeInCrypto.

Who Is Emma Roberts’ Husband Cody John?

TIMOTEO Y LUCIANEKA SE VAN A LA CAMA | CHAPA TU MONEY CON MATEO

Decorating shop to close in Consett due to lack of shoppers

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat5 days ago

NewsBeat5 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech6 days ago

Tech6 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat7 days ago

NewsBeat7 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Tech5 hours ago

Tech5 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Business5 days ago

Business5 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment5 days ago

Entertainment5 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Tech7 days ago

Tech7 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

NewsBeat6 days ago

NewsBeat6 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World7 days ago

Crypto World7 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Tech7 days ago

Tech7 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

-

Sports9 hours ago

Sports9 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos3 days ago

News Videos3 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Politics17 hours ago

Politics17 hours agoSpain sweeps the board at 2026 World Cup with individual awards

-

Sports3 days ago

Sports3 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion3 days ago

Fashion3 days ago16 Dresses for the High Summer Event

-

Crypto World6 days ago

Crypto World6 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

You must be logged in to post a comment Login