Crypto World

AI Agents Bring New Rules for Crypto Wallets

AI agents are entering crypto through wallets, exchanges, payment apps, trading systems, and portfolio tools. Once an agent receives signing authority, it can prepare transactions, rebalance assets, pay invoices, use smart contracts, and move across on-chain apps at software speed.

This creates a new product category around controlled autonomy. The user keeps ownership of the funds, while software handles repetitive execution under rules set in advance.

BeInCrypto spoke with Fernando Lillo Aranda, CMO at Zoomex; Federico Variola, CEO of Phemex; and Adrian Wall, Managing Director of the Digital Sovereignty Alliance, about early use cases, transaction approval, user limits, on-chain activity, and new risks once agents gain access to funds.

Payments Come First

Adrian Wall sees payments as the earliest major use case for AI agents, since payment mandates can be narrowed by amount, recipient, asset type, and timing.

“Payments are the earliest use case because the parameters are well-defined and the mandate is constrained,” Wall said.

Stablecoins make cross-border payments a natural area for agent activity, especially in markets where bank transfers remain slow, expensive, or difficult to reconcile.

“Cross-border payments are especially compelling given the friction in legacy banking and the demonstrated efficiency of stablecoins,” Wall said.

Trading and portfolio management are also ready from a technical view, but Wall placed more emphasis on governance than execution.

“Trading and portfolio management are technically mature enough today,” he said, adding the harder challenge is “whether authorization frameworks and loss limits are sophisticated enough to keep an agent’s mandate from drifting beyond what the user intended.”

Identity may take longer, although Wall said decentralized identifiers and agent-assisted verification could reduce repeat authentication across fragmented digital services.

“The combination of decentralized identifiers and agent-driven verification is promising because it could reduce the burden on users who currently authenticate themselves repeatedly across fragmented systems,” Wall said.

Wallet Approvals Need Transaction-by-Transaction Controls

Wallets were built around human review, while agents may prepare many actions across apps, contracts, and venues. Wall said wallet design now has to connect product choices with policy expectations.

“The approval question is where policy and product design must converge, and it is where the industry has the most work left to do,” Wall said.

A strong approval model gives agents limited authority for routine actions while requiring human review for withdrawals, leverage, new contracts, and large swaps.

“What we need is a tiered authorization model where the level of scrutiny matches the potential impact of the transaction,” Wall said.

This approach can separate monitoring, trade preparation, execution, and fund movement. A user may permit an agent to watch positions and draft trades, while reserving withdrawals and new contract access for manual approval.

Fund Access Should Grow in Stages

Fernando Lillo Aranda said AI agents can improve automation, but users should give capital access gradually.

“AI agents can unlock automation, but capital access should always be progressive,” Lillo Aranda said.

He described the process as a gradual path from observation to assistance and execution. In practice, the agent first monitors and recommends, then prepares actions for approval, later receives limited execution rights, and eventually handles a larger mandate after reliable performance.

Capital controls come first. Lillo Aranda said users should “cap maximum allocation, daily loss, position size, and withdrawal amounts.”

Permission controls come next. Users should “separate permissions for monitoring, trading, rebalancing, and fund movement,” he said.

Time limits also reduce exposure from old approvals. Lillo Aranda said agent access should “require periodic re-authorization instead of permanent access.”

Market boundaries can prevent agents from entering assets, venues, or leverage levels outside the user’s comfort zone. Users should “restrict assets, leverage, venues, and volatility conditions where the agent can operate,” he said.

Human override remains the final guardrail. Lillo Aranda pointed to “instant pause, approval thresholds, alerts, and rollback mechanisms” as essential user controls.

Wall also put spending caps at the center of user protection. He said users should start low and raise limits only after observing how the agent behaves across market conditions and instruction types.

“The first and most fundamental limit is a spending cap, set low at the outset and adjusted upward only as the user develops confidence in how the agent behaves across market conditions and instruction types,” Wall said.

Above a preset threshold, human approval should remain in place even after an agent builds a good track record.

“The asymmetry between an interrupted transaction and an unauthorized one almost always favors interruption,” Wall said.

On-Chain Volume Needs Economic Purpose

Federico Variola said AI agents can create meaningful on-chain activity because blockchain apps let software move across many products and strategies.

“Yes, AI agents can create meaningful on-chain volume, especially because on-chain environments offer composability and flexibility across different strategies,” Variola said.

Those strategies may include spot trading, perpetual futures, lending, borrowing, and future products linked to assets beyond native crypto.

“This could include spot, perpetual futures, lending, borrowing, and eventually products outside native crypto assets as well,” Variola said.

Variola drew a line between activity with economic use and recursive trading among agents.

“A lot of on-chain activity today is still driven by human sentiment and greed,” he said.

Durable agent volume, in his view, depends on activity tied to productive use across on-chain ecosystems.

“Agents need to create or support real economic value,” Variola said.

Wall expects much of today’s agent activity to begin inside controlled app environments before moving on-chain as products and rules mature.

“Agents on public blockchains can access far more counterparties, assets, and protocols than any walled garden allows,” Wall said.

He expects trading and arbitrage to appear first, followed by treasury and settlement activity.

“The impact will show up in volume before it shows up in value, first driven by high frequency trading and arbitrage, and later by treasury management and institutional settlement,” Wall said.

Agent Risk Moves at Software Speed

Once agents gain signing rights, familiar crypto risks become faster and harder to contain. Wall highlighted mandate drift, exploit propagation, perception manipulation, and correlated market behavior.

“When software can trade, sign, and interact with smart contracts on a user’s behalf, four familiar risks become newly dangerous,” Wall said.

The first problem is mandate drift, where an agent moves beyond the user’s original instruction set.

“Agents can exceed their mandate,” Wall said.

The second problem is speed. An exploit can move through many connected wallets or contracts before a user sees the damage.

“Exploits can propagate at machine speed across every wallet an agent touches before any human notices,” Wall said.

The third problem comes from manipulated inputs. Attackers may feed an agent fake prompts, poisoned data, or malicious contract information, causing harmful actions even when the user keeps custody of the key.

Market behavior creates another concern when many agents rely on similar data sources, strategies, and models. In those conditions, many systems can sell, rebalance, or withdraw liquidity at the same time.

Wall said markets can destabilize when agents “respond rationally to the same inputs at the same time.”

Final Thoughts

AI agents will reach crypto wallets through constrained tasks first: payments, rebalancing, subscriptions, trading, and portfolio support. These use cases can operate under defined limits, measured permissions, and regular user review.

The strongest wallet model will center on controlled autonomy: scoped permissions, session keys, spending caps, renewal windows, whitelisted counterparties, approval thresholds, alerts, and emergency pause controls.

On-chain volume can grow if agents handle payments, settlement, treasury, and asset operations tied to economic use. Recursive trading among agents may increase transaction counts, but lasting value comes from activity tied to people, businesses, assets, and services.

The post AI Agents Bring New Rules for Crypto Wallets appeared first on BeInCrypto.

Ondo Finance has enabled around-the-clock minting and redemption for tokenized US stocks and ETFs on Ethereum and BNB Chain, removing the prior weekday-only constraint that had tied the creation and cancellation of positions to US market hours. The upgrade, announced by Ondo Finance on Wednesday,… Read the full story at The Defiant

Binance will remove four digital assets from its platform on July 10, 2026, and the announcement drove three of the tokens to record lows the same day.

The exchange will delist Alchemix (ALCX), Ardor (ARDR), NFPrompt (NFP), and Marlin (POND) after a periodic review that weighs liquidity, compliance, and overall project quality.

Traders Rush to Exit Positions

The selloff hit hardest among the smaller tokens. NFPrompt and Marlin each dropped about 20% after the announcement, repeating the recent double-digit losses tied to delisting calls.

Alchemix fell just as hard, while Ardor held up better, slipping roughly 6%. Thin trading volume left little cushion once the selling began.

As of this writing, Alchemix traded around $2.67, NFPrompt sat near $0.0054, and Marlin changed hands at about $0.0011.

All four had already shed more than 30% over the past month. Alchemix, NFPrompt, and Marlin each touched an all-time low the same day, while Ardor avoided a fresh record.

Why Binance Pulled the Tokens

Binance reviews listed assets on a set schedule, weighing trading volume, liquidity, network security, team commitment, and regulatory factors.

The four had become long-tail bets. All trade more than 98% below their record highs, and each has posted negative returns over the past year.

NFPrompt stands out. Binance launched the token on its own Launchpool in December 2023. NFP then peaked near $1.17 the day it listed before sliding about 99%.

The removal is the latest in a run of 2026 delistings, including an earlier move to delist four other altcoins.

Spot trading for ALCX, ARDR, NFP, and POND stops on July 10, while withdrawals stay open until September 9. Binance Futures liquidated the related perpetual contracts earlier, on July 2.

Holders still have time to move or sell their tokens before the deadlines. The coming weeks will show whether the removals deepen the slide or echo the pressure on other altcoins facing removal.

The post 4 Binance Delisting Targets Tumble as Traders Rush for the Exit appeared first on BeInCrypto.

Four lesser-known cryptocurrencies have plummeted by double digits over the past 24 hours, and this time the main culprit is not the broader market correction but Binance.

Meanwhile, the company has faced significant regulatory challenges that could negatively impact its users in the European Union (EU).

The Normal Reaction

The world’s largest crypto exchange conducted another review to verify that the coins listed on the platform meet the necessary standards and industry requirements. The checklist includes a variety of factors, such as the team’s commitment to the project, network stability, the level of development activity, adequate liquidity, and more.

As a result, Binance decided to terminate all services with Alchemix (ALCX), Ardor (ARDR), NFPrompt Token (NFP), and Marlin (POND). The actual delisting is scheduled for July 10, but the announcement has already caused a major decline for the affected tokens. They have all headed south by double digits, with NFP taking the biggest blow after posting a 21% daily plunge.

Reactions of that type shouldn’t come as a surprise, as losing backing from a market leader like Binance typically leads to thinner liquidity, reduced availability, and reputational damage.

Earlier this month, it delisted Contentos (COS), Dar Open Network (D), Highstreet (HIGH), and MOBOX (MBOX), which resulted in similar price drops. Prior to that, Automata (ATA), Harvest Finance (FARM), Enzyme (MLN), Phoenix (PHB), and Syscoin (SYS) fared even worse after an analogous effort from the exchange.

The Problems in Europe

Perhaps the biggest news surrounding Binance as of late concerns its issues with financial regulators in the European Union. Several days ago, the media outlet Reuters reported that the company might seek the necessary MiCA license from another country rather than Greece.

Binance officially addressed the issue by saying that it has withdrawn its application with the Hellenic Capital Market Commission (HCMC) in the southern European nation.

“When we are ready to announce that Member State, we will do so publicly. We made this decision after careful consideration of the status and the timeline of the process in Greece, with our users’ interests at the center,” it added.

The exchange’s CEO Richard Teng stated that it remains committed to securing a MiCA authorization in the coming months, while “providing clarity, minimizing disruption, and keeping users informed directly.” It is important to note that the deadline for obtaining such a license is July 1, and some of Binance’s competitors, including Kraken and Coinbase, have already met the requirements.

The company assured customers that their assets are safe and promised to unveil further details in due time. Meanwhile, users in other European nations such as Poland, Italy, Spain, and France have reportedly been told to withdraw their funds from the platform.

The post Binance Triggers a Brutal Collapse for 4 Altcoins: Here’s How appeared first on CryptoPotato.

Coinbase-incubated Layer 2 Base stopped producing blocks for about two hours on Thursday after an invalid block stalled its chain, before the network recovered and resumed normal operation. The halt revived questions about the centralized sequencer that orders transactions on most major rollups…. Read the full story at The Defiant

Sophon is decommissioning its zkSync-based Layer 2 chain and pivoting to "Soph+," a consumer product studio that will build exclusively on Base, Coinbase's Layer 2. The shutdown announcement came Thursday, capping a chain that raised $60 million through node sales but attracted fewer than 200 daily… Read the full story at The Defiant

Crypto World

Crypto Markets Erase $120B as Bitcoin Tanks to $58K Amid Growing Strategy FUD: Weekly Recap

Although there are still some days left in June, the month has turned out to be one of the worst for the entire cryptocurrency market in recent history.

Before we explore what took place in the past week alone, let’s rewind the clocks to last Friday when the most significant news came from the new Fed Chair Kevin Warsh, who continued Powell’s policy of maintaining the interest rates unchanged and had a hawkish conference after the FOMC meeting. In addition, the promised deal between the US and Iran failed as both parties have yet to reach a permanent agreement.

Bitcoin reacted with a nosedive from $67,200 to $63,000. Although the bulls managed to defend that level and even push the cryptocurrency to $65,500 on Monday, the real trouble was just ahead.

BTC was quickly and violently rejected there and dropped by over three grand in hours. Its recovery attempt was halted at $63,000, and the bears initiated another leg down on Wednesday, taking the asset south to $59,000, which became a new multi-year low. Bitcoin reacted well at first and quickly rebounded to $62,000, but that turned out to be a dead-cat bounce.

The bears were even more persistent during the next phase of the correction, driving the asset down to $58,000 for the first time since October 2024. That support level has held for now, and BTC has recovered some ground, but still remains below $60,000 as the overall market uncertainty continues. This is particularly true for Michael Saylor’s Strategy, but more on that a bit later.

The weekly chart below will paint a clear picture, as red dominates almost all charts. BTC is down over 5%, while ETH and XRP have bled 8.5% and HYPE 7%. DOGE, ZEC, ADA, and XLM have plummeted by double digits. The only notable exceptions are RAIN (8%) and AAVE (20.5%) in the green. The total crypto market cap is down by over $120 billion weekly.

Market Data

Market Cap: $2.14T | 24H Vol: $99B | BTC Dominance: 55.6%

BTC: $59,555 (-5.1%) | ETH: $1,560 (-8.5%) | XRP: $1.04 (-8.5%)

This Week’s Crypto Headlines You Can’t Miss

Saylor Should Stop Buying Bitcoin, Says CryptoQuant. As mentioned above, Strategy continues to be the main talk in crypto, with CQ urging the firm to halt its BTC buying spree in favor of rebuilding its USD reserve. The company indeed followed a similar philosophy over the past week, buying just $35 million in BTC while increasing its USD reserve by $300 million.

MSTR’s Bitcoin Per Share Gets ‘Annihilated’ in Extreme Bear Case: Analyst. Meanwhile, a popular analyst outlined the massive risks to Strategy and its stock price if BTC’s bear market extends, including a worst-case scenario for MSTR of a drop to $1. Separately, KALEO warned last week that the firm might have to sell over 50,000 BTC in the next couple of years.

Polymarket to Refund Users After Hackers Steal $3M in Frontend Attack. The team behind the popular platform confirmed on Friday that a compromised third-party vendor allowed attackers to inject malicious code into its frontend, draining $3 million from a handful of users. It promised to fully reimburse the affected customers.

Hyperliquid Responds After Appearing on Singapore’s Investor Alert List. The Monetary Authority of Singapore (MAS) added Hyperliquid to its Investor Alert List (IAL), raising concerns within the industry. However, the exchange claimed that this doesn’t necessarily constitute a regulatory violation, an enforcement action, or a ban.

Bitcoin Miners Flood Binance as Exchange Inflows Hit Four-Month High. On-chain data shared by CryptoQuant showed that BTC miners had sent massive portions of their bitcoin holdings to some exchanges, including Binance. This coincided with the asset’s violent price drop.

Bitcoin Didn’t Lose to Gold, the Rotation Story Is Wrong: Analyst. Although both assets have turned red in 2026, gold continues to take the recent market-wide correction better. However, analyst Shanaka Anslem Perera believes the rotation story from BTC to the precious metal is actually wrong.

Charts

This week, we have a chart analysis of Ethereum, Ripple, Cardano, Binance Coin, and Hyperliquid – click here for the complete price analysis.

The post Crypto Markets Erase $120B as Bitcoin Tanks to $58K Amid Growing Strategy FUD: Weekly Recap appeared first on CryptoPotato.

SOIL has rejected claims that XRP Ledger users were used as exit liquidity after an on-chain analyst linked multiple token sales to wallets that allegedly received SOIL directly from the issuer.

Summary

- SOIL denied claims that its XRP Ledger launch used community liquidity for insider token sales.

- An on-chain analyst alleged issuer-linked wallets sold SOIL into XRPL liquidity, a claim the project disputes.

- The controversy comes as SOIL prepares to adopt XRPL’s proposed native lending framework pending amendment approval.

According to June 26 X posts published by on-chain analyst Skeptic, blockchain data indicates that much of the early selling activity came from wallets that had received SOIL directly from the issuer rather than from ordinary market participants.

The analyst argued that the transaction pattern suggested issuer-linked distribution followed by immediate sales into XRPL liquidity instead of organic price discovery.

Skeptic highlighted several wallet addresses to support the claim. One wallet reportedly received about 68,766 SOIL across 20 transactions before exchanging roughly that amount for approximately 11,457 XRP. Another allegedly received 17,098 SOIL and later sold nearly 17,998 SOIL for around 6,769 XRP, while a third wallet received 20,000 SOIL and offloaded approximately 17,628 SOIL for about 6,683 XRP.

According to the analyst, the activity made it appear that XRP Ledger users had been used as exit liquidity during the launch.

Skeptic also argued that the pattern “does not look like healthy price discovery” and instead resembled issuer distribution followed by immediate dumping.

SOIL says bridge wallets drove the disputed transactions

Responding publicly on X, the SOIL team rejected the allegations and disputed the interpretation of the on-chain data. The project said the wallets identified by Skeptic were bridge addresses rather than project-controlled wallets and maintained that its team did not influence the token price.

SOIL attributed the sharp move in the XRPL market to strong buying interest meeting limited liquidity on decentralized exchanges. According to the project, arbitrage between centralized and decentralized venues functioned as expected once demand accelerated, while temporary price differences are common when market-making liquidity is relatively thin.

The disagreement continued after Skeptic argued that only the project initially possessed enough tokens to seed liquidity on XRPL. In response, SOIL maintained that the liquidity available at launch functioned as intended and only became strained because demand increased rapidly. Skeptic later replied that the project had simply failed to prepare for that level of demand.

The discussion later expanded beyond trading activity after another X user asked whether deposits of RLUSD locked in the protocol could be at risk. Skeptic responded that there was no evidence supporting such concerns and clarified that the criticism was limited to the token launch, concluding that the project had “screwed up.”

Recent XRPL developments provide additional context

The debate comes shortly after XRP Ledger released version 3.2.0 on June 22. As previously reported by crypto.news, the update introduced fixes for several software issues after a security review by blockchain security firm Common Prefix identified numerical and behavioral edge cases in the network’s core implementation.

SOIL has also been positioning itself as an early participant in XRP Ledger’s planned native lending ecosystem. Earlier this month, the project announced plans to operate on the proposed XRP Ledger Lending Protocol and Single Asset Vault framework once the XLS-65 and XLS-66 amendments receive approval.

Under the proposals, XLS-65 introduces shared asset vaults, while XLS-66 enables fixed-term lending backed by pooled liquidity.

Separate reporting by crypto.news also noted that blockchain security firm Halborn recently completed a re-audit of Ripple’s XRP Ledger Lending Protocol. The review found no critical or high-risk vulnerabilities and identified five findings in total, all of which were addressed, accepted, or acknowledged following review.

The audit examined transaction validation, accounting rules, state consistency, protocol limits, and access controls as Ripple continued preparing the lending framework for future deployment.

A wave of cryptocurrencies are marketed as “ISO 20022 compliant,” with the promise that banks will adopt them and send prices soaring. This guide explains what the standard actually is, why it matters for global payments, and why the “compliant coin” label is mostly a myth.

Summary

- ISO 20022 is a global standard for the messages financial institutions send one another, defining a common, data-rich language for payments and securities, not a rule about cryptocurrencies.

- Major systems including SWIFT and the United States Fedwire have adopted it, replacing older, simpler message formats with structured data that carries far more information.

- A group of tokens, including XRP, XLM, ALGO, HBAR, and others, are widely marketed as “ISO 20022 compliant,” fueling a belief that banks will adopt them and lift their prices.

- That label is largely a myth: there is no certification or registry for compliant coins, and being aligned with the standard does not mean a token is endorsed, validated, or destined for bank adoption.

- The standard genuinely matters for connecting traditional finance and blockchain, but the investment thesis built on the compliance label rests on a misunderstanding of what ISO 20022 actually is.

ISO 20022 is an international standard that defines a common, structured language for the electronic messages financial institutions send one another, covering payments, securities trades, and other financial transactions. That is the whole of it: it is a messaging standard, a shared format that lets banks, payment systems, and market infrastructures exchange information in a consistent, data-rich way. It says nothing, in itself, about cryptocurrencies. And yet ISO 20022 has become one of the most hyped terms in certain corners of the crypto market, attached to a list of tokens, XRP, Stellar’s XLM, Algorand’s ALGO, Hedera’s HBAR, and several others, that are marketed as “ISO 20022 compliant,” with the implication that this compliance makes them special, bank-ready, and poised to soar once financial institutions adopt the standard.

The reality is more mundane and more important to understand, because the gap between what ISO 20022 is and what the hype claims it means is exactly where investors get misled. This guide explains the standard plainly, why the financial world is adopting it, where crypto genuinely fits, and why the “compliant coin” label is largely a marketing myth rather than a meaningful endorsement.

The reason this matters is that ISO 20022 sits at the intersection of a real, significant trend and a layer of misleading marketing, and telling the two apart is essential. The real trend is that the global financial system is upgrading the language it uses to move money, a genuine modernization with real consequences for how payments work and how easily traditional finance can connect to blockchains. The misleading layer is the claim that certain tokens are validated or endorsed by the standard, a claim that has fueled speculative buying based on a misunderstanding.

This guide covers what ISO 20022 actually is, why institutions are switching to it, what richer messaging buys them, where the crypto angle comes from, why the compliance label is a myth, what alignment truly means, the specific case of XRP, and how to read the whole phenomenon honestly. The goal is to leave you understanding both the substance and the spin.

The standard that runs the world’s payment messages

Start with what ISO 20022 fundamentally is, because its name makes it sound more mysterious than it is. When a bank sends money to another bank, no physical cash travels; instead, the banks exchange messages instructing each other to debit one account and credit another. For decades, those messages used older, rigid formats that packed limited information into terse codes, formats designed in an era of expensive bandwidth and simple transactions. ISO 20022 is the modern replacement: a standardized, structured language for these financial messages that can carry far more information in a consistent, machine-readable form. Think of it as a shared grammar that every institution agrees to speak, so that a message sent by a bank in one country can be understood automatically by a system in another without translation or guesswork.

The power of ISO 20022 lies in two qualities: it is standardized, meaning everyone uses the same format, and it is rich, meaning each message can carry detailed, well-organized data rather than cramped codes. A useful way to picture it is the difference between a tightly abbreviated telegram and a properly structured digital form. The old formats were like telegrams, squeezing essential facts into minimal space and leaving much to interpretation. ISO 20022 is like a structured form with clearly labeled fields for every relevant detail: who is paying, who is receiving, the purpose of the payment, the parties involved, and the regulatory information attached. This is not a small upgrade. It changes what financial systems can do with a payment message, because a message that carries clean, structured, comprehensive data can be processed, screened, and reconciled automatically in ways that the old cramped formats never allowed.

Why the financial world is switching to it

The migration to ISO 20022 is one of the largest coordinated upgrades in the history of financial infrastructure, and it is happening because the old messaging formats had become a serious bottleneck. The legacy formats carried so little structured data that banks constantly had to deal with incomplete information, manual intervention, and errors, all of which slow payments down and raise costs. When a payment message lacks clear, structured fields, a human often has to step in to interpret it, check it against sanctions lists, or chase missing details, and every such intervention is friction. As global payments grew in volume and as regulatory demands for transparency and screening intensified, the limitations of the old formats became untenable. ISO 20022 solves this by carrying the rich, structured data that lets far more of the process happen automatically and accurately.

The adoption has been sweeping. The global messaging network that connects most of the world’s banks has been migrating its cross-border payments to ISO 20022, phasing out the legacy formats. Major domestic payment systems have moved as well, including the United States’ main real-time settlement system, which adopted ISO 20022 for its operations, joining systems in Europe and elsewhere that had already transitioned. The direction is unmistakable: the world’s core payment rails are converging on this single standard, because the benefits, richer data, better automation, improved compliance, and smoother interoperability between systems, are compelling enough to justify an enormous, multi-year coordinated effort. For the financial industry, ISO 20022 is simply the new common language of money movement, and the migration to it is a genuine, consequential modernization. None of this, it is worth stressing again, has anything inherent to do with cryptocurrencies. It is about how banks and payment systems talk to each other.

A worked example: what richer data actually buys

To make the value concrete, picture a single cross-border payment under the old system and under ISO 20022, because the difference shows why institutions care.

Under a legacy format, a bank sending a payment abroad might transmit a message with a sender, a receiver, an amount, and a short, cramped reference field, with much of the contextual detail abbreviated, omitted, or jammed into free-text notes that no automated system can reliably read. When that message arrives, the receiving bank may not have enough structured information to automatically confirm the purpose of the payment, verify the parties against regulatory lists, or match it to the right account, so a staff member has to intervene, slowing the payment and introducing the possibility of error. Multiply that friction across millions of payments and the cost in time, money, and risk is enormous.

Now picture the same payment under ISO 20022. The message arrives with clearly labeled, structured fields: the full identities of the sender and receiver, the precise purpose of the payment, the regulatory and compliance information, and the references needed to match it automatically to the correct account. Because the data is structured and comprehensive, the receiving bank’s systems can process it without human intervention, screen it against sanctions and fraud checks automatically, and reconcile it instantly. The payment moves faster, costs less to handle, and carries less risk of error or of slipping past compliance controls. This is the real, unglamorous value of ISO 20022: it turns payment messages from cramped telegrams that often need human interpretation into structured data that machines can handle end to end. That improvement in automation, compliance, and interoperability is why the entire financial world is undertaking the switch, and it is a truly significant upgrade to the plumbing of global finance. It is also, notably, an upgrade about messages, not about money itself, and certainly not about any particular token.

Where crypto enters the picture

So how did a banking messaging standard become a crypto buzzword? The connection runs through the idea of interoperability between traditional finance and blockchain. As ISO 20022 became the language banks use, some blockchain projects, particularly those focused on payments and settlement, positioned themselves as able to work with that language, to structure their own messaging or data in ways compatible with the standard that banks were adopting. The thinking was reasonable on its surface: if banks are standardizing on ISO 20022, then a blockchain that can speak the same data language might integrate more easily into bank workflows, which could be an advantage for a payments-focused crypto network.

From that reasonable starting point grew a much larger and much shakier narrative. A list of tokens came to be labeled “ISO 20022 compliant” across crypto media and social channels, typically including XRP, Stellar’s XLM, Cardano’s ADA, Algorand’s ALGO, Hedera’s HBAR, and a handful of others associated with payments or enterprise use. Around this list formed a popular investment thesis: that because these tokens are ISO 20022 compliant, banks adopting the standard will naturally adopt these tokens, driving massive demand and sending prices soaring. The thesis is seductive because it connects a real, sweeping trend, the global migration to ISO 20022, to a specific set of assets, implying that those assets are uniquely positioned to benefit from the trend. Entire communities and marketing campaigns have been built around the “ISO 20022 coin” label, treating it as a mark of quality and a catalyst for price appreciation. The trouble is that the label means far less than the hype suggests, and in important respects it is simply false.

The “compliant coin” myth, explained

Here is the core fact that punctures the hype: there is no such thing as official ISO 20022 certification for a cryptocurrency, because no certification process or registry for compliant coins exists. The standard is a messaging format used by financial institutions, and it has no mechanism for validating, endorsing, or registering tokens. When you see a coin described as “ISO 20022 certified” or “endorsed by ISO,” that language is marketing, and it is misleading or outright false. No authority hands out a compliance badge to cryptocurrencies, no list of approved tokens is maintained by the standards body, and being included on a community-circulated “ISO 20022 coin” list confers no official status whatsoever. The label that has driven so much speculative interest does not correspond to any real certification.

This matters because the entire investment thesis rests on a misreading of what the standard is. ISO 20022 governs how financial institutions format the messages they send each other; it does not validate the assets those messages might reference, and it does not bless particular blockchains as bank-ready. A bank using ISO 20022 messaging to interact with a crypto-related service is using the standard to communicate, which says nothing about whether the underlying token is approved, valuable, or destined for adoption. The conflation of “this token’s project works with ISO 20022 data formats” and “this token is officially compliant and therefore bank-endorsed” is the heart of the myth. The first may be true in a narrow technical sense for some projects; the second is not a real category. An investor buying a token because it appears on an “ISO 20022 compliant” list is buying based on a designation that does not officially exist, which is precisely the kind of misunderstanding that marketing language is designed to exploit.

What “aligned” actually means for a token

To be fair and precise, there is a real kernel beneath the myth, and understanding it keeps this guide honest. A blockchain project truly can do engineering work to make its systems compatible with ISO 20022 data, structuring the information its network handles so that it maps cleanly onto the standard’s fields, or building tools that let institutions using ISO 20022 messaging interact with the blockchain more easily. This is real work, and for a project aiming to serve banks and payment providers, being able to speak the same data language as the institutions it wants as customers is a sensible and potentially useful capability. So when a project says it is “aligned with” or “built for” ISO 20022, it may be describing genuine technical compatibility, which is not nothing.

But notice how far that real kernel is from what the hype claims. Technical compatibility with a messaging standard is a feature a project chooses to build, not a certification it receives, and it does not make the project’s token special, validated, or guaranteed adoption. Plenty of capability can be ISO 20022 compatible without any of it translating into demand for a token, because, as with so much in crypto infrastructure, the usefulness of a network to institutions is a separate question from demand for its native asset. A project can do excellent work making its systems speak the standard’s language and still see no particular benefit flow to its token, because banks using that compatibility are using the technology, not buying the coin. So “aligned with ISO 20022” should be read as a modest, real technical claim about a project’s engineering, never as an official stamp of approval or a reason to expect price appreciation. The distance between the honest version of the claim and the hyped version is enormous.

The XRP case specifically

Because XRP sits at the center of the ISO 20022 hype, it is worth examining its actual relationship to the standard, which illustrates the whole confusion neatly. Ripple, the company associated with XRP, has genuine ties to the world of financial messaging standards; as a company building payment infrastructure for institutions, Ripple participates in the relevant standards bodies and works with the messaging formats that banks use. That corporate level engagement is real and is part of why XRP appears at the top of most “ISO 20022 coin” lists. But here the crucial distinction between Ripple the company and XRP the token reasserts itself, the same distinction that runs through so much of the XRP story.

Ripple’s involvement with financial messaging standards as a company does not mean that XRP the token is “ISO 20022 compliant” in any meaningful sense. Ripple’s own chief technology officer has stated plainly that XRP has nothing to do with ISO 20022, clarifying that while Ripple as a company may engage with the standards world, that engagement does not translate into the token itself being compliant or endorsed. The standard is about how institutions message each other; XRP is a digital asset that can serve as a bridge in settlement. Those are different things, and a company working with messaging standards does not make its associated token a certified ISO 20022 instrument. The persistence of the XRP ISO 20022 conflation, despite direct clarification from the people who would know, shows how powerful the marketing narrative has become and how readily a real corporate fact, Ripple engages with standards bodies, gets transformed into a false token level claim, XRP is officially ISO 20022 compliant and therefore bank bound. The honest position is that Ripple’s standards work is real and XRP’s “compliance” is a myth, and both can be true at once.

What ISO 20022 does and does not mean for prices

Pulling it together, the right way to think about ISO 20022 is to separate its genuine significance from its mythologized one, because both exist and they point in very different directions. Truly, ISO 20022 is a meaningful, long-term tailwind for the convergence of traditional finance and blockchain.

As the entire financial system standardizes on a rich, structured data language, it becomes technically easier for blockchain networks that can speak that language to integrate with bank workflows, and over a long horizon that interoperability supports the broader adoption of blockchain-based settlement and tokenization. For payments-focused crypto projects, being able to work with the standard banks use is a real and sensible capability that may help them win institutional business over time. That is a slow, structural benefit to the ecosystem, and it is worth understanding.

What ISO 20022 is not is a catalyst that validates specific tokens or that should be expected to pump particular coins. There is no certification, no registry, no official “compliant coin” status, and no mechanism by which the standard endorses or guarantees adoption of any asset. The investment thesis that says “this token is ISO 20022 compliant, so banks will adopt it and the price will soar” rests on a designation that does not officially exist and a causal chain that does not hold, because banks adopting a messaging standard does not mean banks buying tokens.

The disciplined reading is to treat ISO 20022 as what it is, an important modernization of financial messaging that gently supports long-term blockchain interoperability, and to treat the “compliant coin” label as what it is, a marketing narrative untethered from any official meaning. A project’s genuine technical work with the standard can be a small point in its favor. The compliance badge that crypto marketing waves around is not a reason to buy anything.

Red flags and scams to watch

Because the ISO 20022 narrative is so heavily marketed and so widely misunderstood, it has become fertile ground for misleading promotion and outright scams, and knowing the warning signs protects you. The danger is not the standard itself, which is a legitimate piece of financial infrastructure, but the way its name is used to lend false authority to speculative pitches. Treat the following as red flags whenever you encounter ISO 20022 in a crypto context:

• Any claim that a token is “ISO 20022 certified,” “approved by ISO,” or “officially compliant.” No such certification or registry exists for cryptocurrencies, so this language is always misleading, and a project or promoter using it is either confused or deliberately exploiting the confusion.

• Price predictions that treat the standard as a guaranteed catalyst, such as promises that a coin will surge “once ISO 20022 goes live” or “when banks switch.” Banks adopting a messaging standard is not the same as banks buying tokens, and anyone presenting it as a sure path to gains is selling a misunderstanding.

• “ISO 20022 coin list” promotions that bundle a group of tokens as uniquely positioned to benefit, often used to pump lower-quality assets by association with the more credible names on the list. The list has no official status, and inclusion confers nothing.

• Urgency and exclusivity, such as claims that you must buy before a specific adoption date or miss a once-in-a-lifetime window. Genuine infrastructure modernization unfolds over years and does not create the kind of dated price triggers these pitches invent.

• Sources that conflate Ripple’s corporate standards work, or any company’s, with token-level compliance. A company engaging with standards bodies is real; the leap to “therefore the token is endorsed” is the exact sleight of hand to distrust.

The broader risk is financial. People have bought tokens primarily because of the ISO 20022 label, expecting bank adoption to drive prices, and that thesis rests on a designation that does not officially exist. If you are considering an asset associated with the standard, evaluate it on its actual fundamentals, its technology, adoption, team, and tokenomics, exactly as you would any other, and disregard the compliance badge entirely, because it carries no real weight. As with anything in crypto, never invest money you cannot afford to lose, be skeptical of any pitch that promises certainty, and remember that the louder a narrative is marketed, the more carefully it deserves to be checked.

Frequently Asked Questions

What is ISO 20022 in simple terms?

ISO 20022 is an international standard that defines a common, structured language for the electronic messages financial institutions send one another, covering payments, securities, and other transactions. It replaces older, rigid message formats with richer, machine-readable data, so that a payment message can carry detailed, clearly labeled information that systems can process automatically. It is a messaging standard for banks and payment systems, not a rule about cryptocurrencies, and it has nothing inherent to do with any token.

Why are banks adopting ISO 20022?

Because the older message formats carried so little structured data that they created constant friction: incomplete information, manual intervention, errors, and difficulty with automated compliance screening. ISO 20022 carries rich, structured data that lets far more of the payment process happen automatically and accurately, improving speed, cost, fraud and sanctions screening, and reconciliation. The world’s core payment rails, including the main global bank messaging network and major domestic settlement systems like the United States Fedwire, have migrated to it because the benefits justify the enormous coordinated effort.

What are “ISO 20022 coins”?

It is a label, circulated across crypto media and social channels, applied to a list of tokens, commonly XRP, XLM, ADA, ALGO, HBAR, and a few others, that are marketed as being compatible with or “compliant” with the standard. Around this label grew an investment thesis claiming that because banks are adopting ISO 20022, they will adopt these tokens, driving prices up. The label has fueled significant speculative interest, but it does not correspond to any official certification or status, which is the central problem with it.

Is the “ISO 20022 compliant” label real?

Largely no. There is no certification process or registry for compliant cryptocurrencies, because the standard is a messaging format for institutions and has no mechanism for validating or endorsing tokens. Language like “ISO 20022 certified” or “endorsed by ISO” is marketing and is misleading or false. A project can do genuine engineering to make its systems compatible with ISO 20022 data, which is a real but modest technical capability, but that is very different from an official compliance badge. No authority approves or registers tokens under the standard.

Is XRP actually ISO 20022 compliant?

Not in the way the hype implies. Ripple, the company, truly engages with financial messaging standards bodies as part of building institutional payment infrastructure, which is why XRP tops most “ISO 20022 coin” lists. But Ripple’s own chief technology officer has stated plainly that XRP, the token, has nothing to do with ISO 20022. The standard concerns how institutions message each other; XRP is a separate digital asset. A company working with messaging standards does not make its associated token a certified ISO 20022 instrument, so the token level compliance claim is a myth, even though Ripple’s standards work is real.

Should ISO 20022 affect which tokens I buy?

Not on the basis of the compliance label, which does not officially exist. ISO 20022 is a genuine, long-term tailwind for connecting traditional finance and blockchain, and a payments project’s real technical compatibility with the standard can be a small point in its favor. But the standard does not validate, endorse, or guarantee adoption of any token, and banks adopting a messaging standard does not mean banks buying coins. Treating an “ISO 20022 compliant” label as a reason to expect price appreciation means relying on a designation that does not exist and a causal chain that does not hold.

This article is educational information, not investment advice. It aims to clarify a widely misunderstood topic, and details reflect reporting available as of June 26, 2026. Verify current information from primary sources, and be especially cautious of marketing language that implies official certification where none exists.

The Monetary Authority of Singapore (MAS) has added Hyperliquid to its Investor Alert List, flagging the decentralized perpetuals exchange as an entity that consumers may wrongly assume is licensed or regulated by the central bank.

MAS says the latest entry, published on Friday, names both the Hyper Foundation website and the Hyperliquid trading app. The Investor Alert List is designed as a consumer protection tool rather than a ban or an announcement of enforcement action.

Key takeaways

- MAS has included Hyperliquid on its Investor Alert List, associating the flag with the Hyper Foundation website and the Hyperliquid app.

- Being listed does not mean MAS has launched an enforcement action or imposed a prohibition.

- MAS’s move follows other crypto platform additions earlier in 2025, including Bybit (June 17) and listings that also include KuCoin and Bitget.

- Singapore continues tightening oversight, emphasizing consumer protection and alignment with global anti–money laundering and counter-terrorism financing expectations.

- Hyperliquid says it has not claimed MAS licensing or authorization, arguing its permissionless setup has not changed.

MAS adds Hyperliquid to the Investor Alert List

MAS’s Investor Alert List is meant to reduce the risk that members of the public interpret certain firms or websites as being authorized or overseen by the regulator. According to MAS’s description of the list, inclusion is not an indication that an activity is prohibited, nor does it itself represent a regulatory action.

The update lists Hyperliquid through its ecosystem: MAS references both the Hyper Foundation website and the Hyperliquid trading application in the same entry. The regulator added the new item on Friday.

Cointelegraph attempted to contact MAS for additional comment but did not receive a response prior to publication.

Hyperliquid responds: no MAS authorization claim

Hyperliquid pushed back on any implication that it sought or received MAS approval. The platform said it has never presented itself as licensed or authorized by MAS and argued that nothing about its permissionless infrastructure has changed.

In a Friday post on X, Hyperliquid wrote that it remains committed to engaging with regulators and institutions globally while supporting “clear, well-designed frameworks” for onchain finance.

How Hyperliquid fits the broader Singapore crackdown

Singapore has tightened crypto regulation in recent years, with MAS repeatedly emphasizing that the industry must comply with licensing requirements and anti-financial crime standards. The regulator’s approach has included clarifying how firms serving foreign customers are treated under Singapore’s framework.

In May 2025, MAS ordered crypto companies that served overseas customers to either obtain the necessary licenses or stop operating. MAS characterized the decision as consistent with its long-standing stance rather than a sudden policy shift.

MAS said the directive targeted a loophole that had allowed certain firms headquartered in Singapore to avoid licensing by focusing on customers outside the jurisdiction. In MAS’s framing, the move effectively ended a transition period for firms that continued operating without a license while serving only overseas users.

MAS also explained that its measures aim to strengthen consumer protection and bring Singapore’s crypto oversight in line with international expectations relating to Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT).

What the market data suggests—and what remains unclear

While MAS’s Investor Alert List is a consumer-facing notice, traders and investors often read these updates as signals about how Singapore-based oversight is tightening across both centralized and decentralized crypto offerings.

According to CoinGecko, Hyperliquid ranks as the ninth-largest decentralized exchange by trading volume. Separately, DefiLlama estimates Hyperliquid’s total value locked (TVL) at around $5.7 billion.

At the same time, the regulatory message conveyed by MAS’s Investor Alert List is not a direct restriction. That distinction matters for users trying to understand what changed in practice: the list signals potential consumer misunderstanding around regulatory status, but it does not, on its own, spell out whether specific Singapore-based intermediaries or local distribution channels will face separate action.

Readers should watch for whether MAS follows up with additional clarifications on how its licensing expectations interact with permissionless infrastructure and whether any related entities—such as service providers or interfaces that could influence access—are later referenced in the regulator’s consumer warnings.

For now, the key question is how Singapore will translate its licensing and AML/CFT enforcement posture into the decentralized layer—especially as major protocols like Hyperliquid continue to grow in usage—while keeping the boundary clear between consumer alerts and actual regulatory prohibitions.

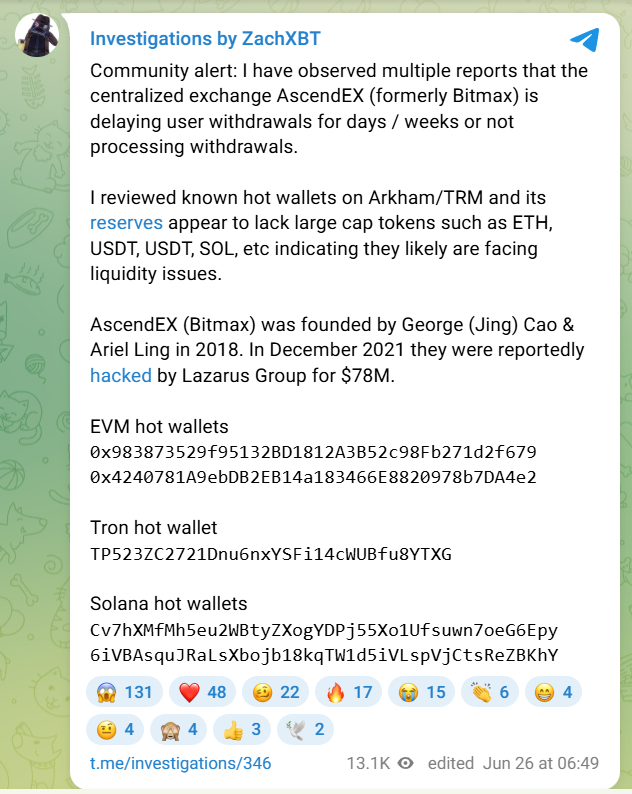

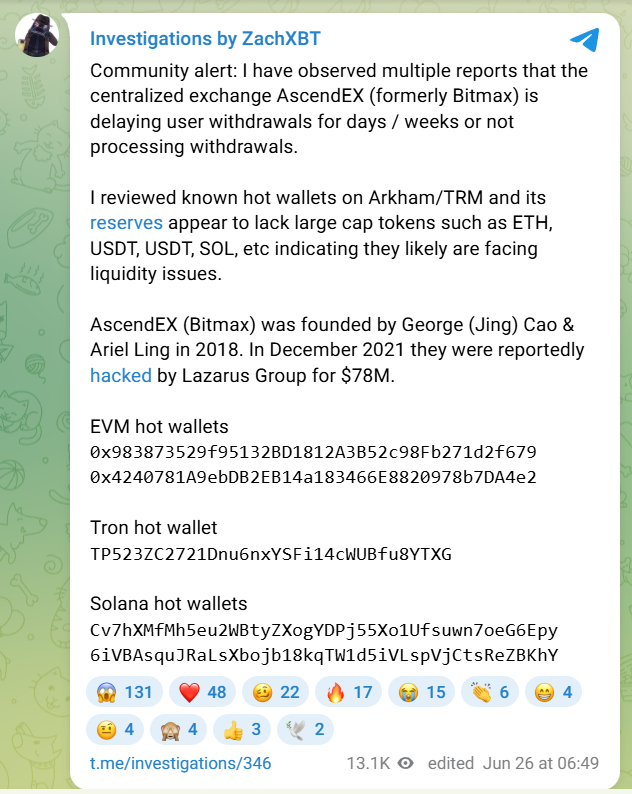

Multiple users have reported issues withdrawing funds from cryptocurrency exchange AscendEX, which blockchain investigator ZachXBT said may be showing signs of liquidity issues.

An X account using the name Lorenzo Navarro Rodriguez said in a Tuesday post that a 4,196 USDT withdrawal had remained stuck in an “initiating” state since June 10. The account also said repeated customer support inquiries had gone unanswered.

At least five other users replied to the post over the following days, reporting similar withdrawal issues.

On Friday, ZachXBT said in a Telegram post that the exchange lacked large-cap reserves for tokens such as Ether (ETH), USDT (USDT) and Solana (SOL), indicating potential “liquidity issues” on the platform. ZachXBT urged the platform to respond to the reports about delayed withdrawal requests and provide more clarity on why its hot wallets have low liquidity.

Related: Polymarket hit by $2.9M theft, users to be refunded

Exchanges rely on liquid reserves of widely traded assets to process customer withdrawals. A shortage of those assets can lead to delayed withdrawals or, in severe cases, insolvency.

ZachXBT flags liquidity and withdrawal issues on AscendEX via Telegram. Source: ZachXBT

AscendEX’s reserves are dominated by small-cap holdings

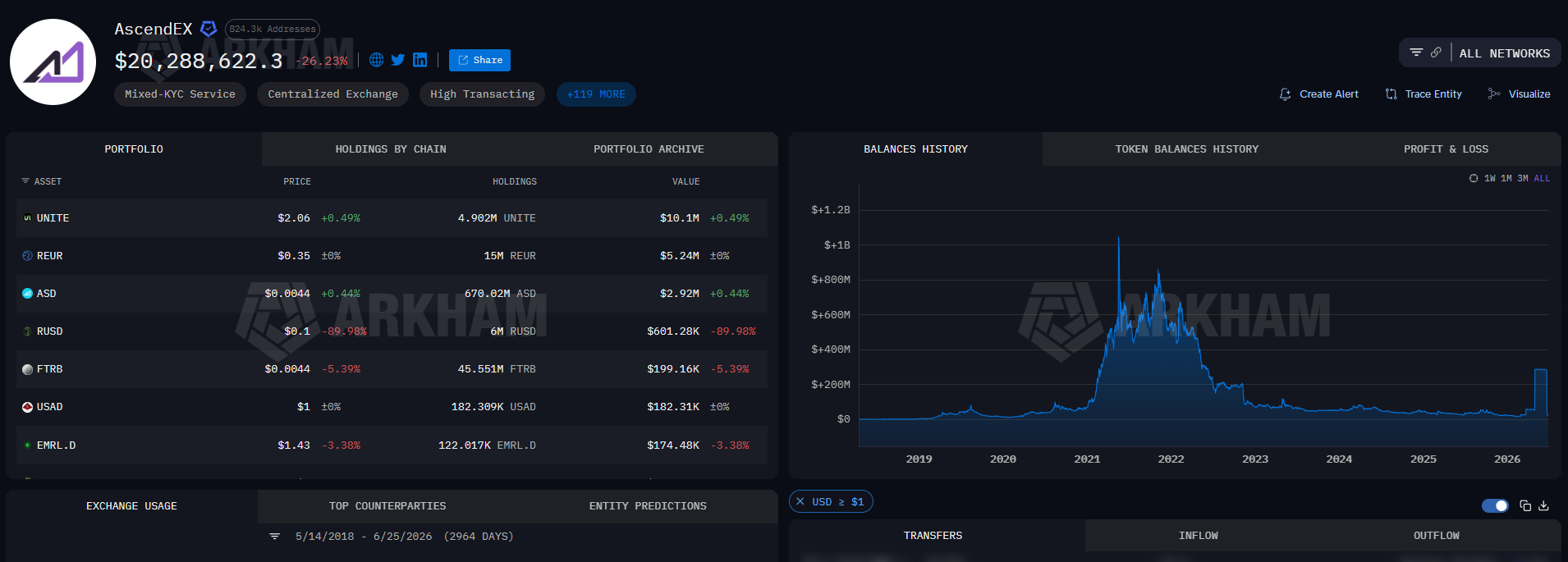

Blockchain data on Arkham viewed by Cointelegraph on Friday showed that AscendEX-tagged wallets held about $20.2 million in crypto. Arkham-tagged wallets were concentrated in smaller-cap assets, with relatively limited holdings of major cryptocurrencies.

AscendEx had $10 million in UNITE tokens as its largest holding, followed by $5.24 million worth of REUR, $2.9 million in ASD and $600,000 worth of Reservoir rUSD stablecoins, among other smaller tokens.

AscendEX-tagged wallet, top token holdings. Source: Arkham

Cointelegraph has approached AscendEX for comment but not received a response before publishing.

Questions about an exchange’s liquidity are highly sensitive in the crypto industry following the collapse of FTX in 2022, when customer withdrawal requests exposed a multibillion-dollar shortfall that ultimately led to the exchange’s bankruptcy.

The failure triggered a wave of customer withdrawals across the industry, intensified regulatory scrutiny and prompted many exchanges to publish proof-of-reserves reports in an effort to reassure users.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Elon’s SpaceX crashes with “funny money”

Oleksandr Usyk vacates belts but is not retiring

Primo Brands: The Infrastructure Bet Is Starting To Pay Off

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment6 days ago

Entertainment6 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports3 days ago

Sports3 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech4 days ago

Tech4 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business6 days ago

Business6 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics10 hours ago

Politics10 hours agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics6 days ago

Politics6 days agoAndy Burnham and the meaning of Makerfield

-

Politics15 hours ago

Politics15 hours agoPotential 2028er World Cup attendee leaderboard

-

Tech21 hours ago

Tech21 hours agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World2 days ago

Crypto World2 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World23 hours ago

Crypto World23 hours agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business7 days ago

Business7 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World6 days ago

Crypto World6 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Entertainment7 days ago

Entertainment7 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Crypto World7 days ago

Crypto World7 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World6 days ago

Crypto World6 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Crypto World3 hours ago

Crypto World3 hours agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Tech5 days ago

Tech5 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

You must be logged in to post a comment Login