Crypto World

Arthur Hayes Buys ETH Above $1,900 Weeks After Selling at $1,700

Ethereum (ETH) has stolen the show in the past few days, posting impressive gains and outperforming the market leader and many of the larger-cap alts.

One of the reasons behind this notable rally that drove it to a multi-week peak could be ongoing accumulation by major players, including BitMEX’s co-founder, Arthur Hayes.

Hayes Buys ETH High

On-chain data provided by Lookonchain indicated that the popular crypto personality spent roughly $2.5 million to acquire 1,293 ETH. Consequently, he continues to display a somewhat controversial approach to Ethereum given his most recent moves.

CryptoPotato reported back in mid-June that Hayes had accumulated a total of 5,900 ETH for $10.58 million in the span of just a few days. However, he disposed of his entire stash (and some more) just a day later for around $10 million, registering a loss of more than $600,000 in hours.

What’s interesting in this situation is that he seems to be buying high and selling low. His most recent accumulation came at prices of well over $1,900, where ETH has stood for the past day. In contrast, the aforementioned offload took place when the asset dipped below $1,700.

Hayes has also exhibited controversial behavior toward other crypto assets. He received substantial backlash over his overpromotion of tokens like HYPE, ZEC, and WLD, as he disposed of his positions weeks after praising them and long before they reached his massive price targets.

Whales, Abraxas Buy Too

With speculation running rampant about ETH’s future following its notable surge past $1,900, the broader Ethereum ecosystem shows that other participants are joining through large acquisitions. Additional data from Lookonchain suggested that three newly created wallets withdrew nearly $58 million in ETH from Coinbase Prime earlier today. The analysts concluded that “whales continue accumulating ETH.”

Moreover, wallets linked to Abraxas Capital deposited $40 million worth of bitcoin into the veteran US exchange Kraken earlier this week. Lookonchain noted that they used a large portion of the capital they gathered to rotate into ETH after withdrawing 8,153 tokens from the platform.

Abraxas Capital is selling $BTC and buying $ETH!

Over the past 3 hours, Abraxas Capital withdrew 8,153 $ETH($15.3M) from #Binance and #Bybit, while depositing 618 $BTC($39.99M) into #Kraken.https://t.co/qwAXChjYvp pic.twitter.com/EdWBYF36Lf

— Lookonchain (@lookonchain) July 15, 2026

The post Arthur Hayes Buys ETH Above $1,900 Weeks After Selling at $1,700 appeared first on CryptoPotato.

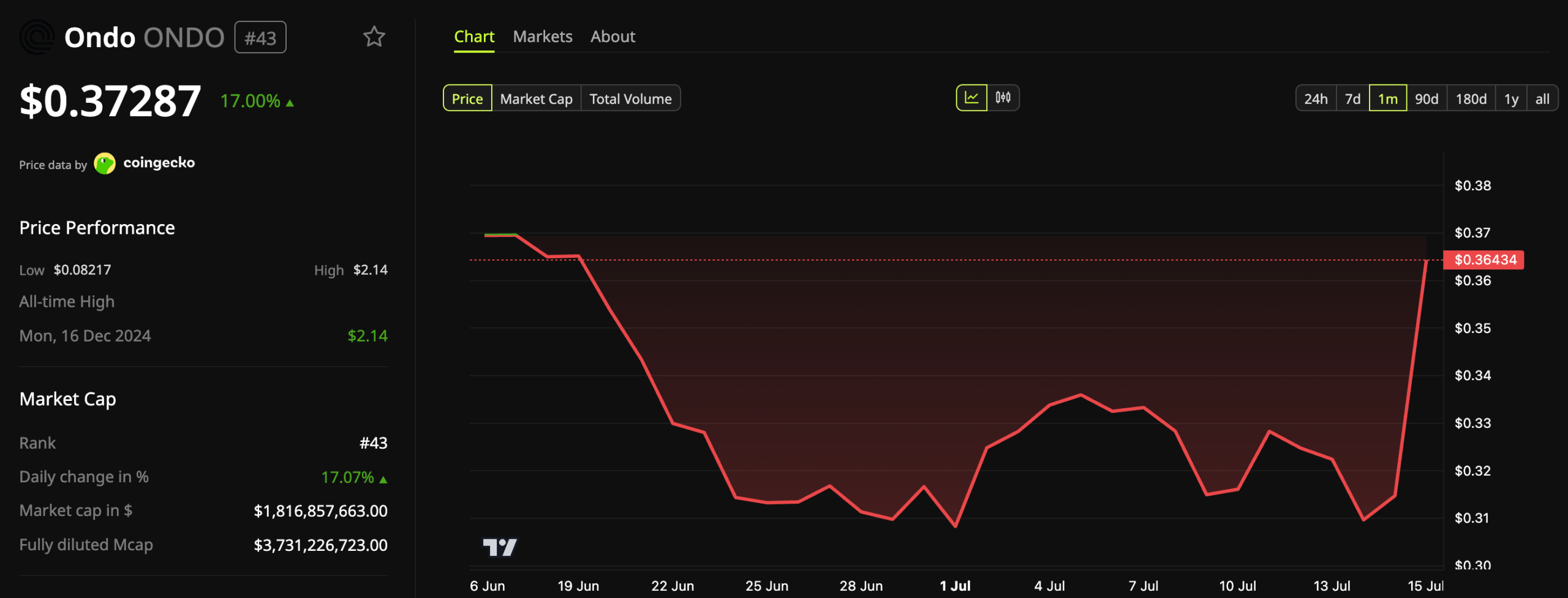

Ondo (ONDO) climbed to a one-month high after a sharp rally driven by the debut of the first tokenized stocks backed by DTC Tokenized Entitlements.

The altcoin surged as much as 17% over the past 24 hours to an intraday high of $0.37. This marked its strongest level since June 18.

The rally also propelled ONDO to the top of CoinGecko’s list of the day’s biggest cryptocurrency gainers. The surge stood out against a flat market, with Bitcoin (BTC) little changed over the same period.

Follow us on X to get the latest news as it happens

Ondo Debuts First DTC-Backed Tokenized Stocks

Ondo’s tokenized stocks are backed by DTC Tokenized Entitlements to securities held at The Depository Trust Company (DTC). The design ties on-chain tokens directly to shares inside Wall Street’s core custody system.

The company called it a first for tokenized equities. The tokens represent Circle (CRCL) stock and the SPDR S&P 500 ETF (SPY) on-chain. Ondo issues them as CRCLon and SPYon, each fully backed by the underlying security.

“Under this model, DTC tokenized entitlements to DTC-held securities are generated through the DTCC Tokenization Service, and the DTC Tokenized Entitlements associated with CRCL and SPY serve as digital twins of the securities underlying existing CRCLon and SPYon tokens (Ondo’s tokenized versions of the stocks),” the team explained.

Ondo is connected to the DTC participant network through Alpaca Markets. The underlying shares stay within DTC custody throughout the process, according to the firm.

“Ondo joins more than a dozen leading TradFi and DeFi firms — including BlackRock, JPMorgan, Goldman Sachs, Nasdaq, and NYSE — participating in DTCC’s largest tokenization initiative to date, representing an important step toward the broader adoption of tokenized securities,” the blog read.

DTCC’s Tokenization Push Gains Traction

The launch comes as the Depository Trust & Clearing Corporation (DTCC) completed the tokenization of assets held at The Depository Trust Company. More than 30 firms participated in the initiative.

The transactions covered collateral pledges, securities lending, and equity settlements. DTCC ran them across its private HyperLedger Besu network and the public Canton network.

The platform plans to launch its full tokenization service in October 2026. That milestone arrived seven months after the SEC granted DTC a No-Action Letter to tokenize custodied assets.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Ondo Hits 1-Month High: Here Is What’s Driving The 17% Surge appeared first on BeInCrypto.

Hyperion DeFi has committed 500,000 HYPE tokens to support institutional perpetual futures listings on Hyperliquid through a new agreement with Skew Technologies.

Summary

- Hyperion DeFi will deploy 500,000 HYPE tokens to support institutional perpetual futures markets on Hyperliquid.

- The agreement gives Hyperion an equity stake in Skew Technologies and a share of revenue from listing services.

- The partnership expands institutional use of Hyperliquid’s HIP 3 framework for launching custom perpetual markets.

According to a Wednesday press release, the Nasdaq-listed company will deploy the tokens under Hyperliquid’s HIP-3 permissionless listings framework while receiving an equity stake in Skew Technologies and a share of the listing-service revenue generated through the platform.

The companies said the partnership is intended to help institutional clients launch custom perpetual futures markets on Hyperliquid, a layer-1 blockchain focused on perpetual futures trading.

Hyperion expands role in Hyperliquid ecosystem

Under Hyperliquid’s HIP-3 framework, developers can create custom perpetual markets by posting HYPE as bonded capital, giving the token a use case beyond staking. The same infrastructure has recently been used to launch synthetic markets linked to assets outside crypto, including pre-IPO companies such as Chinese memory chipmaker ChangXin Memory Technologies.

Commenting on the agreement, Hyperion DeFi chief executive officer Hyunsu Jung said the company continued to receive requests from teams worldwide looking to launch and distribute new markets using Hyperliquid’s infrastructure while evaluating opportunities within HIP-3.

Rather than operating the markets directly, Skew Technologies will provide the listing service, while Hyperion contributes HYPE tokens required to support the permissionless listings under the agreement.

The arrangement also deepens Hyperion’s exposure to the Hyperliquid ecosystem beyond holding the token, with the company set to receive both an ownership interest in Skew and a portion of the revenue generated by the listing business.

Institutional activity around Hyperliquid continues to grow

The latest announcement comes as institutional interest in Hyperliquid has continued to expand across several areas of the ecosystem.

Earlier this month, Bitwise added HYPE to its Bitwise 10 Crypto Index ETF (BITW), placing the token inside one of the industry’s largest diversified crypto index products after its latest index rebalancing.

At the same time, Hyperliquid has been attracting new infrastructure partnerships. Circle and Coinbase recently deepened USDC integration on the network, making USDC the platform’s preferred stablecoin, although JPMorgan said this week that the revised revenue-sharing structure could reduce long-term reserve income retained by Circle and Coinbase even as USDC adoption grows.

Recent HIP-3 deployments have also extended beyond crypto-native assets. Last week, Hyperliquid introduced a synthetic perpetual market tied to ChangXin Memory Technologies ahead of its Shanghai listing, showing how the framework can support custom derivatives linked to real-world and pre-IPO assets without giving traders ownership of the underlying securities.

For fifteen years the loudest promise in crypto was that XRP would replace Swift. Not complement it, not plug into it, replace it: the slow, expensive, pre-funded machinery of correspondent banking swept away by a bridge asset that settles in seconds.

Summary

- Swift’s blockchain ledger went live with 17 major banks and chose tokenized deposits, not XRP.

- The system targets real-time liquidity management and cross-border settlement inside existing bank balance sheets.

- XRP rallied on the headline, but the architecture leaves no public bridge asset in the middle.

- The strongest XRP arguments rely on old artifacts, overlapping relationships, and optional future liquidity use cases.

- The launch weakens the original “XRP replaces Swift” thesis while leaving Ripple’s broader business intact.

It was the thesis that sold the token, filled the conference halls, and outlasted a five-year lawsuit.On July 9, 2026, Swift answered.

The network moved its own blockchain ledger into live operation with seventeen pioneer banks, among them Citi, HSBC, Wells Fargo, UBS, Standard Chartered, and MUFG. The build took nine months. The system runs 24 hours a day across six continents, coordinating cross-border payments on a shared ledger that eliminates the batch windows and cut-off times that made correspondent banking feel like a fax machine. It is, by any fair reading, Swift doing the thing everyone said Swift would never do: shipping blockchain settlement, at scale, with the incumbents, before the disruptor could take the market.

And the asset moving across it is tokenized bank deposits. Not XRP. Not any public token. Banks convert dollars and euros they already hold into digital claims and send those claims to each other directly. No third coin sits in the middle.

That is not a rumor, a leak, or an interpretation. It is the design, and it is the most consequential piece of information the XRP thesis has received since the SEC dropped its appeal.What followed was five days of the loudest argument the XRP community has had in years, conducted almost entirely over a resurfaced slide and a two-word post from a man who no longer works there. That argument is worth walking through, because the way it is being fought reveals more than the thing being fought over.

What Swift actually shipped

The details matter, because the gap between what was announced and what was believed became its own story within hours.

Swift confirmed that its blockchain-enabled shared ledger completed roughly nine months of development and testing and is ready for commercial use. The stated purpose is liquidity management: letting banks monitor and move tokenized deposits in real time, with visibility into cash positions across institutions. The system reportedly runs on Hyperledger Besu with Chainlink’s cross-chain interoperability protocol handling messaging between chains, though that stack detail comes from secondary reporting rather than a Swift technical disclosure and deserves the caveat.

The seventeen pilot banks are not a random sample. They are the tier-one institutions that XRP holders spent a decade naming as future Ripple customers. Citi. HSBC. Wells Fargo. UBS. MUFG. Standard Chartered. When Swift decided how money would move in a tokenized era, it convened exactly the banks the bridge-asset thesis was waiting on, and those banks agreed to test settlement using their own deposits.

The ledger’s economic function is worth stating plainly, because it is where the XRP question actually lives. Its purpose is to let banks see and move their own liquidity in real time across a shared record. Every participant reads the same state. Positions net continuously instead of at end of day. Cut-off times stop existing. Whatever else that is, it is a direct attack on the specific inefficiency that made a bridge asset attractive in the first place, executed by the party that owns the relationships.

Swift has also signaled where this goes next, describing an ambition to become a platform for programmable money and agentic commerce, payments that execute automatically when conditions are met without a human approving each one. That is not a defensive crouch. It is a network that watched the tokenization argument play out for a decade and decided to build the endgame itself.crypto.news covered the market’s immediate reaction, which was, revealingly, a rally. XRP rose on the news that Swift had built a system without it.

Why the rally happened

That reaction is the most interesting thing in this story, because it was not irrational. It was the product of a genuine ambiguity that both sides are now exploiting.

Two of the seventeen banks, Standard Chartered and UBS, already work with Ripple through custody or payment infrastructure on the XRP Ledger. Ripple Treasury entered Swift’s Certified Partner Program in April 2026. Swift’s broader payments framework names more than thirty institutions with existing Ripple relationships, a set that extends beyond the seventeen pilot participants, though the overlap has never been specified. Read those facts quickly and it looks like Ripple is inside the tent.

Then the artifacts arrived. A researcher operating as SMQKE resurfaced a Swift-branded slide that places Ripple explicitly in the middle of a payment flow, positioned between local bank and local bank. A widely shared clip features a former Swift insider, now linked to Euro Exim Bank, predicting XRP adoption within the network. The slide got called a mic-drop moment. The clip got called verbatim proof.

The rebuttal came just as fast and from a more credentialed source. Tom Zschach spent six years as Swift’s Chief Innovation Officer, running the network’s digital asset strategy. He answered the rumor with two words: not happening. A separate analyst urged followers to stop engaging with anyone claiming Swift currently uses XRP, on the grounds that the only public evidence shows adoption of ISO 20022 messaging standards, which is a data format, not an asset choice.

Both sides have a problem. Zschach left Swift earlier this year and has criticized Ripple for years, which makes his read informed but personal and not official policy. The slide is undated, resurfaced rather than leaked, and interpreted through a YouTube channel and an anonymous account. Neither is evidence in the sense that a production integration would be evidence.

What is not ambiguous is the ledger. Seventeen banks. Tokenized deposits. Live.

A decade of the banks saying no

The July 9 launch reads differently once you remember how long the question has been open, because the record is not one of banks failing to understand the pitch. It is one of banks understanding it precisely and declining.

Ripple’s original enterprise product was messaging: a way for banks to exchange payment instructions with better data and fewer errors than legacy rails. Banks bought that. Santander, SBI, Standard Chartered, and hundreds of others signed on across the late 2010s, and RippleNet became a real business. Then came the second ask, the one the token depended on: route your liquidity through XRP instead of pre-funding accounts. That ask went almost nowhere. The company’s own On-Demand Liquidity product reached a fraction of its partner base, and most institutions stayed on the messaging layer and never touched the asset, a divide crypto.news has documented at length across the XRP vertical.

The explanations offered for that gap were always circumstantial: regulatory uncertainty, the SEC lawsuit, accounting treatment, custody immaturity, market depth. Each was legitimate at the time. Each has since been resolved or substantially reduced. XRP is classified as a digital commodity. The lawsuit ended. Custody is a solved product sold by every major bank. Market depth is adequate for the ticket sizes involved.

So the circumstantial explanations have expired, and the behavior has not changed. When the constraints lift and the decision stays the same, the constraints were not the reason. That is the uncomfortable inference available on July 9 and it does not require believing anything bad about Ripple, only accepting that treasurers weighing a volatile bridge asset against a deposit token they issue themselves have a preference, and have had it for ten years, and just spent nine months building infrastructure that encodes it.

The thesis under the argument

Strip away the personalities and one real technical dispute remains, and it is worth stating precisely because it is the only part that could still cut Ripple’s way.

The bridge-asset argument was never about messaging. It was about nostro and vostro accounts, the pre-funded pools of foreign currency that banks must park in every destination country in order to settle. That trapped capital is the actual cost of correspondent banking, running to trillions globally, and it is the problem XRP was designed to solve: instead of pre-funding a lira account in Turkey, a bank buys XRP, sends it in seconds, and sells it into lira at the far end, freeing the capital that was sitting idle.

Ripple’s supporters argue that Swift’s upgrade is a front-end improvement that does not touch this. Tokenized deposits are still deposits. If a bank sends a tokenized dollar to a bank that needs lira, someone still has to bridge the currency pair, and a shared ledger does not conjure liquidity where none exists. On this reading, Swift built a faster pipe and left the plumbing problem intact, which is exactly the gap XRP was built for.

The counter is harder and mostly wins. A shared ledger with real-time visibility across seventeen tier-one banks changes the economics of pre-funding even if it does not abolish it, because the reason nostro balances are so large is uncertainty about position and timing. Netting improves. Buffers shrink. And critically, the tokenized-deposit model gives banks something a public bridge asset never could: settlement in an instrument they already issue, with no exposure to a volatile third token, no market-maker spread, and no question about who is liable when the price moves mid-transfer. The bridge asset solves trapped capital by introducing price risk and a dependency on a token’s liquidity. Banks have been consistent for a decade about which trade-off they prefer, and Swift just built infrastructure that encodes the answer.

There is one more asymmetry the bridge argument tends to skip. A tokenized deposit is a liability of a regulated bank, which means it arrives inside the legal and accounting framework treasurers already operate in. A bridge asset is a bearer instrument on a public ledger, which means somebody has to write a policy for holding it, mark it to market, explain it to an auditor, and answer for it when it gaps. That is not a technology problem and no amount of settlement speed fixes it. It is why the ODL conversion rate stayed low even in corridors where the math worked, and it is the quiet reason Swift’s design was always the likelier winner.

The honest version is that Swift’s ledger does not make XRP technically impossible as a liquidity leg. It makes it commercially unnecessary for the corridors that matter most, which is a slower and more final kind of defeat.

What the artifacts actually show

The evidentiary standard in this argument collapsed almost immediately, and it is worth being precise about what each item is, because the community is treating them as interchangeable.

The Swift-branded slide is the strongest bull artifact and the weakest form of evidence. It is undated. It was resurfaced by a researcher rather than released or leaked. Nobody has confirmed when it was produced, for what audience, whether it described a live integration or a hypothetical architecture, or whether it survived contact with a product decision. Corporate slide decks are full of vendors placed in diagrams during evaluation phases that ended in no. Even read maximally, the slide depicts Ripple as a connector or optional leg inside Swift-adjacent infrastructure, which is a substantially smaller claim than the thesis it is being used to defend.

Zschach’s post is the strongest bear artifact and is also not evidence. He is a former executive stating a personal view, months after departure, about an organization whose current architecture he no longer sets, and he has a documented history of criticizing Ripple. His read is well-informed. It is not policy.

The Euro Exim Bank thread is the strangest of the three. Its force comes from David Schwartz’s court testimony, where Ripple’s chief technology officer initially told regulators that the company’s primary customers were not banks, and later acknowledged failing to mention Euro Exim Bank as a bank customer using XRP. The XRP argument holds that this proves the asset is already in production use at the margins of traditional finance. It does prove that. It also concedes the scale: the reference case, cited in 2026 as evidence of bank adoption, is a trade finance specialist that nobody would mistake for a tier-one institution. If the strongest live example is Euro Exim Bank while the seventeen banks on Swift’s ledger are Citi, HSBC, and Wells Fargo, the argument has answered itself.

The pattern across all three is the same. The bull case runs on interpretation of artifacts. The bear case runs on a live system with named participants. Those are not the same kind of fact.

The case that this changes nothing for Ripple

Now the argument that Ripple’s defenders make, and it deserves a serious hearing, because on the corporate side it is largely correct.

Ripple never needed Swift. The company runs its own corridors, its own bank relationships with Santander and SBI, and its own dollar stablecoin. Ripple Prime, the institutional arm built out of the Hidden Road acquisition, has cleared more than $3 trillion across roughly 300 institutional clients. The company spent the last two years buying its way into prime brokerage, treasury software, and payments infrastructure, and none of that revenue routes through Swift or depends on Swift’s approval. A network that competes with Ripple’s messaging business building a better messaging business is a competitive fact, not an existential one.

The direction of travel also vindicates Ripple intellectually, which is not nothing. Swift spent years dismissing blockchain settlement and has now shipped 24/7 tokenized cross-border payments with an explicit roadmap toward programmable money and agentic commerce. That is Ripple’s thesis, delivered by Ripple’s incumbent. Being right about where finance was heading, and losing the contract anyway, is a real outcome, and Ripple’s supporters are entitled to point out that nobody was building this in 2015 except them.

Ripple is also still in the room. The Certified Partner Program membership is real. The Ripple-linked institutions inside Swift’s framework are real. Standard Chartered and UBS working with both is real. Nothing about the July 9 launch forecloses XRP serving as an optional liquidity leg for exotic corridors where no deep deposit market exists, which is precisely what the resurfaced slide depicts, and which was always the realistic ceiling for a bridge asset anyway.

And Ripple’s institutional business keeps compounding regardless. The XRP Ledger’s credit layer is in validator voting, an effort crypto.news examined in detail in its analysis o what on-chain credit means for XRP. SBI Digital Finance and Doppler announced institutional XRP lending infrastructure for Japan on July 13. Goldman Sachs sits atop the XRP ETF holder table with a $153.8 million position, a fact crypto.news reported when the funds crossed $1.53 billion. The company is fine. That was never the question.

Ripple in 2026 is a payments and prime brokerage conglomerate with a stablecoin, a pending bank charter, and billions in acquisitions behind it, and it would remain all of those things if XRP traded at fifty cents.

The case that it is the end of an argument

The question was always whether Ripple being fine does anything for XRP, and July 9 is the cleanest data point anyone has produced.

Here is the uncomfortable sequence. The bridge-asset thesis required banks to hold and route a volatile public token. The banks said no for a decade. XRP holders explained that the banks were slow, captured, and would come around once the technology proved itself and the regulatory fog lifted. The fog lifted: XRP is a digital commodity, the lawsuit is over, the appeals are dropped. The technology proved itself: Swift just deployed it. And at the exact moment both preconditions were satisfied, the seventeen largest banks in the world adopted tokenized settlement and chose deposits.That is not the banks being slow. That is the banks answering.

The market noticed even while the price rallied. Spot XRP ETFs recorded $7.29 million of net outflows on July 8, the largest single-day withdrawal since March. Open interest fell from $2.58 billion on July 5 to $2.33 billion on July 9 as traders closed positions instead of opening them. The long-to-short ratio slipped to 0.96, meaning bears slightly outnumbered bulls into the news. Retail bought the Swift headline. Institutions sold into it. When those two groups disagree about an institutional-adoption story, the institutions are usually the ones who read the announcement.

That divergence is the tell worth carrying forward. Price reacted to the word Swift appearing next to the word blockchain. Flow reacted to the architecture. Over any horizon longer than a week, flow wins.

The deeper problem is that this compounds with everything else already on the record. Most of Ripple’s bank partners use RippleNet for messaging and never touch the token. The XRP Ledger’s EVM sidechain, built to give XRP a DeFi economy, holds $25,741 and trades nothing. RLUSD, Ripple’s own product, has grown into a business while the ledger’s native asset has not. Each of these is survivable alone. Together they describe a pattern: every route by which value was supposed to reach XRP has been tested, and the value keeps arriving somewhere else.

Swift is the biggest of those tests because it was the original one. The thesis was not that XRP would find a niche. It was that XRP would become the settlement layer of global finance. That specific claim now has a specific answer, delivered by the specific institution the claim was about, using the specific banks the claim named.

What would have to be true for the bulls

Fairness demands stating the conditions under which the bear reading here is wrong, because they exist and they are not absurd.

Tokenized deposits only work between banks that hold each other’s currencies in size. The model is excellent for dollar-euro-sterling-yen, which is most of the volume and nearly all of the profit. It is useless for a Nigerian bank settling with a Philippine bank, where no deposit market exists in either direction and someone must still bridge. If tokenized deposit networks handle the deep corridors and a public bridge asset handles the long tail, XRP has a real business. It is a smaller business than the pitch, and it competes with stablecoins that carry no price risk, but it is real.

The second condition is agentic settlement. Swift has said it wants to be the platform for programmable money and machine-to-machine payments. Those flows are high-frequency, low-value, and permissionless by nature, which is the environment where a neutral public asset with a native ledger has genuine structural advantages over an interbank consortium. Ripple has been building directly at this, and if the agentic economy materializes at scale, the question reopens on different terms.

The third is time. Seventeen banks in pilot is not global adoption. Consortium infrastructure has failed before, repeatedly, and Swift’s ledger could stall in exactly the way that bank blockchain consortia have stalled since 2016. A pilot that quietly does not scale would leave the field open again. R3, Corda, Utility Settlement Coin, and a decade of bank consortia are a real precedent for exactly that failure mode, and Ripple has outlived most of them.

None of those conditions rescue the original claim. They describe a smaller, more plausible XRP: a liquidity instrument for corridors nobody else wants, and a settlement rail for machines. Which is a decent business, and is not what anyone bought.

The answer nobody wanted to hear

Fifteen years of argument reduced to a design document. Swift built the blockchain. It went live with the exact banks the thesis named. And it moves tokenized deposits, because banks would rather settle in money they issue themselves than in an asset whose price can move against them between the send and the receive.

The XRP community will spend this week debating a resurfaced slide and a former executive’s two-word post, and both of those things are more interesting than the ledger, and neither of them matters. The slide is undated. The executive is gone. The ledger is live.

What is left is the smaller question, the one that has quietly been the only real one for two years: not whether Ripple wins, because Ripple is winning, but whether anything Ripple wins reaches the token. On July 9 the largest institution in cross-border payments answered that question in the most expensive way available, by building the future and leaving XRP out of the blueprint.The thesis is not dead. It is just no longer a thesis about Swift.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Swift has not published a technical disclosure of the ledger’s full stack; the Hyperledger Besu and Chainlink CCIP details derive from secondary reporting. The Swift-branded slide discussed here is undated and was resurfaced by a third party, not released by Swift, and no party has confirmed its provenance or current status. Tom Zschach’s comments are his personal view and not Swift policy; he left the organization earlier in 2026. ETF flow, open interest, and long-to-short figures derive from SoSoValue and CoinGlass. Details reflect information current as of July 14, 2026, and are subject to change. Always do your own research.

Crypto World

Crypto News, July 16: All Eyes on Tomorrow’s Clarity Act Hearing as Bitcoin and Ethereum Hold Key Price Levels

South Korea jolted financial markets with an unexpected interest rate hike, sending local stocks sharply lower and even briefly halting trading. Crypto, however, reacted differently. We shifted our focus to tomorrow’s Clarity Act hearing in Congress, while Bitcoin price hovers near recent highs and Ethereum continues to hold above a key support zone.

The House Financial Services Committee will meet on July 17 for a hearing titled “Building the Future of Finance: How the Clarity Act Unlocks Innovation.” With Congress set to begin its summer recess soon after, many in the industry see the discussion as one of the last meaningful chances to move crypto legislation before lawmakers leave Washington.

BREAKING: — Crypto Rover (@cryptorover) July 16, 2026

Tomorrow could decide the ENTIRE future of crypto in the United States.

Tomorrow could decide the ENTIRE future of crypto in the United States.

The House is holding a field hearing on the CLARITY Act:

"Building the Future of Finance: How the CLARITY Act Unlocks Innovation."

Turn on notifications for updates. pic.twitter.com/yjzDSnGUYC

These all explain the current market’s mood. Macro headlines still drive expectations, but they are no longer the only force steering digital assets. This week, the conversation has narrowed around one question. If the Clarity Act can bring enough regulatory certainty to keep institutional money flowing into the sector.

Discover: The Best Token Presales

Bitcoin Price Holds Firm as Clarity Act Gets Closer

Bitcoin price spent Thursday hovering between $64,500 and $65,000, extending a recovery that has carried it to its highest level in about three weeks. After several months of choppy trading, the market finally looks willing to defend higher ground instead of selling at every rally.

Institutional demand remains part of that story, with BlackRock adding another $139 million worth of Bitcoin to its holdings, while the iShares Bitcoin Trust now custodies more than 733,000 BTC. Larry Fink also struck an optimistic tone this week, saying the current price of Bitcoin appears more stable than before and expressing confidence in financial markets over the next year.

Although traders remain cautious, analysts note Bitcoin is approaching the short-term holder realized price, an area that has historically produced resistance as newer investors exit at break-even. At the same time, those levels have often marked the beginning of longer accumulation phases rather than the end of a recovery.

Another signal arrived from a wallet that had been inactive for eight years. About as much as 5,908 BTC, valued near $383 million, moved to a fresh address without touching an exchange. The transfer did little to disturb sentiment, showing that the market viewed it as a reshuffle instead of a liquidation. For now, Bitcoin price remains steady, with tomorrow’s Clarity Act hearing likely to set the next tone.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Ethereum Price Builds on Improving Momentum

Ethereum is trading around the $1,900 price mark after reclaiming an important resistance level and triggering more than $30 million in short liquidations. The move was not explosive, but it continued a steady improvement that has quietly placed Ethereum among the stronger large-cap performers this week. And yes, the Ethereum price has been outperforming Bitcoin with a more than 17% jump in the ETH/BTC ratio.

Investor appetite is also beginning to recover. Spot Ethereum ETFs recorded $84 million in net inflows during the week ending July 11, breaking an eight-week streak of withdrawals. That turnaround has helped stabilize sentiment, while BlackRock’s ETHA has contributed to several of the strongest daily inflows. As a result, the price of Ethereum is once again finding support from institutional investors.

Away from the ETF market, development across the network continues. Robinhood Chain, an Arbitrum-based Layer 2, is attracting activity through tokenized assets, AI applications, and NFT projects, all of which rely on ETH for transaction fees. Growing usage may not move markets overnight, but it steadily strengthens the network beneath the surface.

The next catalyst now sits in Washington. A constructive outcome from the Clarity Act hearing could reinforce confidence, just as ETF flows improve and the Bitcoin price remains resilient. If that happens, we can, once again, believe that the Ethereum price has a realistic chance of reclaiming $2,000 in the weeks ahead.

Discover: The Best Token Presales

The post Crypto News, July 16: All Eyes on Tomorrow’s Clarity Act Hearing as Bitcoin and Ethereum Hold Key Price Levels appeared first on Cryptonews.

Crypto World

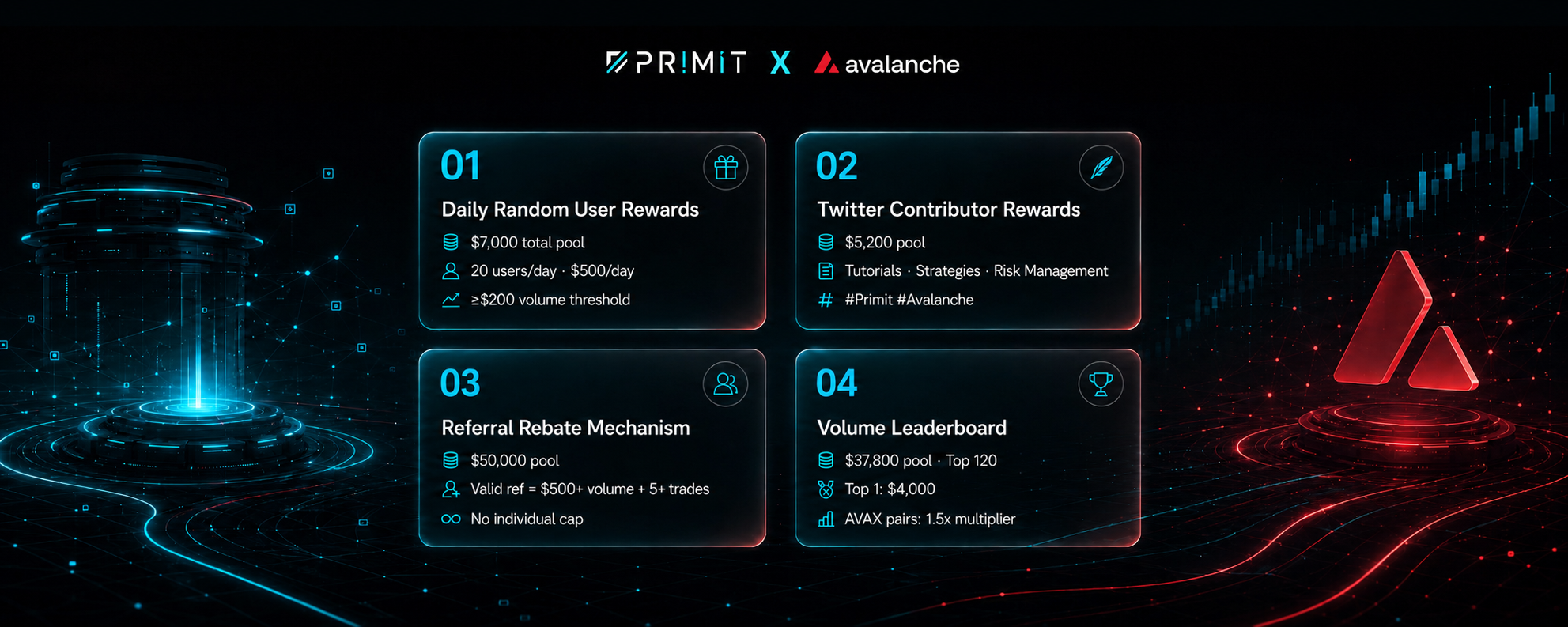

Primit Season 1 Officially Launches: $100,000 Avalanche On-Chain Perp Trading Incentive Event Now Live

Primit × Avalanche Season 1 “On-Chain Perp Frenzy” is now officially live on the Avalanche network. With a total prize pool of 100,000USDT equivalentin AVAX and four simultaneous reward mechanisms, this marks the first large-scale on-chain perpetual trading incentive event in the Avalanche ecosystem.

Full Mechanism Overview

- Daily Random User Rewards ($7,000 pool)

- Every day, 20 users with ≥$200 trading volume are randomly selected to share a $500 pool. 280 total winner slots over 14 days. Draws execute automatically via script daily, with off-chain public verification.

- Twitter Contributor Rewards ($5,200 pool)

- For community content creators. Post high-quality Primit tutorials, strategy analysis, risk management, or reward breakdowns on Twitter/X with #PrimitAvalanche. Human + Agent review. Top contributors earn $300–$500 each.

- Referral Rebate Mechanism ($50,000 pool)

- Every user receives an auto-generated unique Referral Code. A referred user must register via the code and achieve ≥$500 cumulative volume with ≥5 trades during the event to count as valid. After the event, the $50,000 pool is distributed proportionally by valid referral volume. No individual cap.

- Volume Leaderboard ($37,800 pool, Top 120)

- Ranked by cumulative volume after the event:

- Top 1: $4,000

- Top 2: $2,500

- Top 3: $1,800

- Top 4–10: $1,000 each (total $7,000)

- Top 11–30: $450 each (total $9,000)

- Top 31–60: $250 each (total $7,500)

- Top 61–120: $100 each (total $6,000)

- Ranked by cumulative volume after the event:

Avalanche Multiplier

Volume from AVAX-related pairs or using native gas receives a 1.5x weighting. This design directs traders toward Avalanche’s core ecosystem assets while providing quantifiable on-chain activity data for the Avalanche Foundation.

Founder Quote

“Season 1 is not a simple airdrop event. It’s a product stress test. We aim to prove that on-chain perpetual trading is ready to carry real, high-frequency, professional demand. Avalanche’s infrastructure makes this possible.” — Team Primit

About Primit & Avalanche

Primit is a next-generation on-chain perpetual contract trading platform focused on low-latency, low-fee, fully transparent on-chain derivatives. Avalanche is a high-performance Layer 1 blockchain known for sub-second finality and minimal gas costs.

Follow Twitter : https://x.com/primitforall

Event Portal: https://app.primit.io/campaigns

Event Period: July 15 — July 28

The post Primit Season 1 Officially Launches: $100,000 Avalanche On-Chain Perp Trading Incentive Event Now Live appeared first on BeInCrypto.

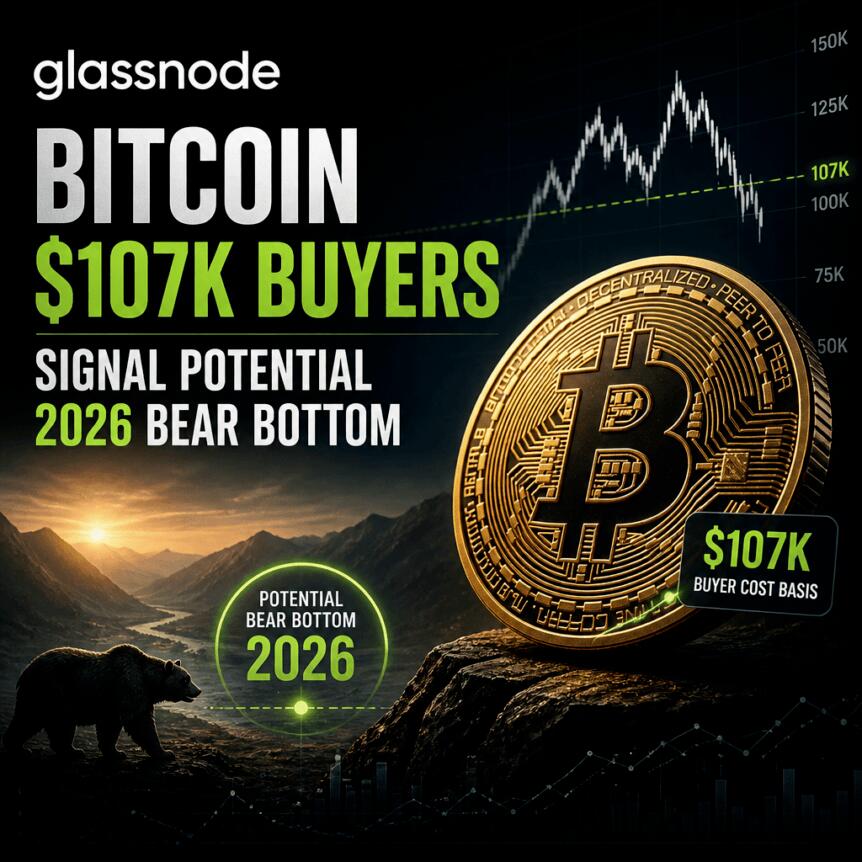

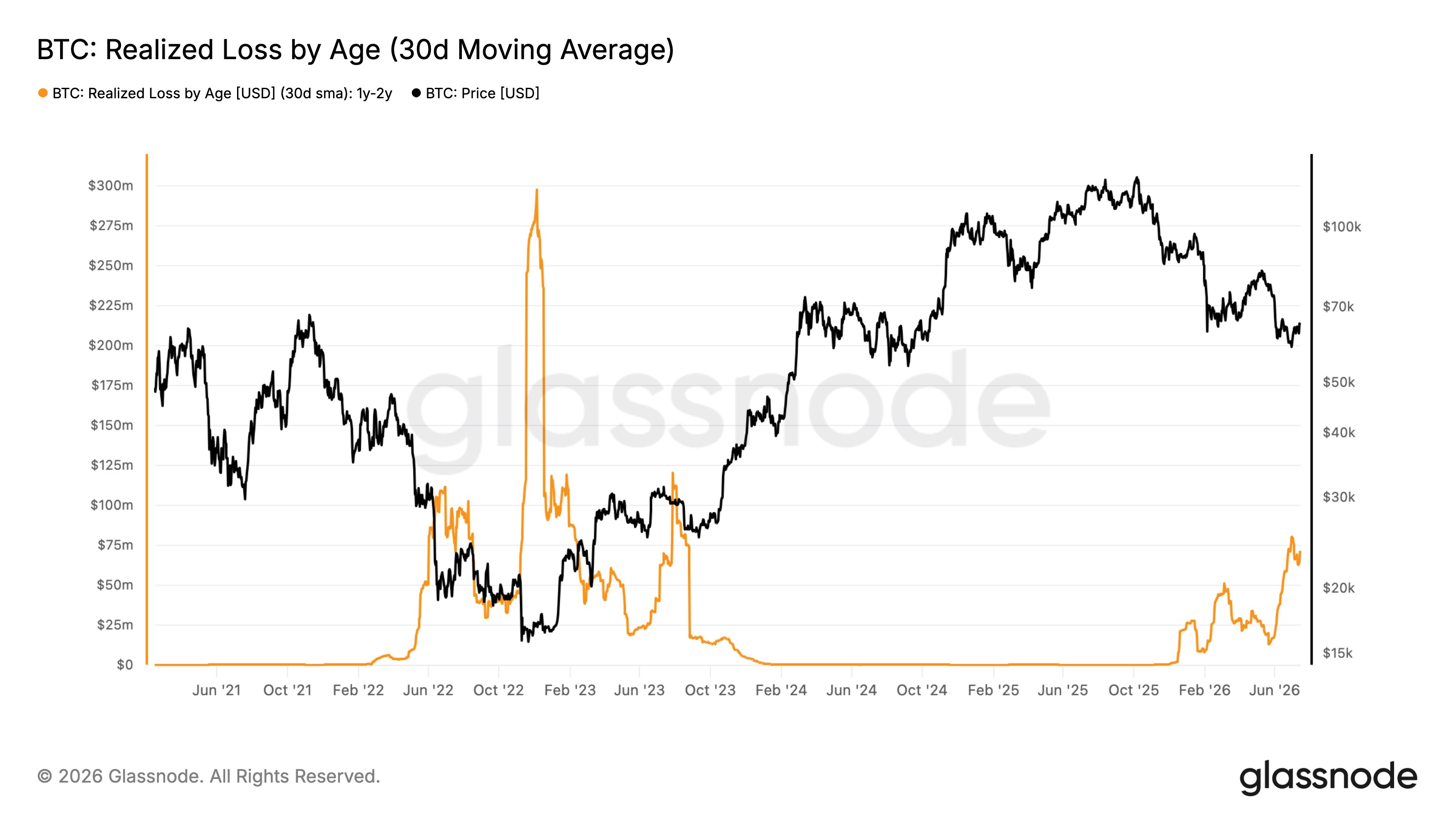

Bitcoin’s “cycle peak buyers”—the investors who accumulated near the latter stages of the last bull run—may be nearing the point where their selling pressure fades, according to new on-chain analysis shared by Glassnode researcher Cryptovizart. The implication is straightforward: if realized losses among one-to-two-year holders keep rolling over, it can mark an early phase of relief from bear-market distribution.

The same report also points to a familiar near-term battleground for price action. Glassnode highlights short-term holders’ aggregate cost basis around $69,000, noting that this level overlaps with old 2021 all-time highs—often a zone where markets either break out decisively or become stuck in a wider range.

Key takeaways

- Glassnode’s realized-loss metric for 1–2 year holders is used as a historical bear-market “endgame” signal.

- Cryptovizart’s chart suggests realized losses recently passed $75 million before beginning a reversal.

- The next potential supply/resistance area centers on $69,000, where short-term holders’ cost basis aligns with former 2021 highs.

- Both signals emphasize shift in cohort behavior—not just price—to gauge whether the market is transitioning out of a bottoming phase.

Why realized losses among 1–2 year holders matter

Cryptovizart, the pseudonymous lead research analyst at Glassnode, laid out the framework in a post on X on Friday. In the analyst’s view, one of the most reliable early checks for whether a bear market has truly started to end is the Realized Loss volume (in USD) by 1–2 year holders.

In on-chain terms, the metric tracks the value of Bitcoin being moved at a loss by coins that have been held for roughly one to two years. When that loss realization rises during a downturn, it often reflects holders giving up after prolonged underperformance. When it starts to cool, it can indicate that the “heaviest distribution” is losing momentum.

According to the post, coins that last transacted at a loss did so during a window spanning July 2024 to July 2025. Over that interval, BTC/USD rose from roughly $62,800 to around $107,000, meaning that a large portion of investors who bought during the latter portion of the bull market are currently underwater on their allocation.

“As frustration builds with sustained price underperformance, this cohort tends to progressively increase loss realization.”

Cryptovizart argues that bear markets have historically lacked durable footing until this specific group begins to exhaust its sell pressure—when realized losses stop climbing and the trend begins to reverse.

The $75 million realized-loss rollover signal

The key visual in the analysis is a spike in realized losses measured on a 30-day moving basis. Cryptovizart notes that realized losses recently climbed to a level above $75 million before the indicator started turning downward.

In the analyst’s framework, the most watchable part isn’t just whether realized losses are elevated—it’s whether the 30D moving average of realized loss begins to cool and roll over. That change, Cryptovizart said, has often appeared among the clearest early signs that the market is moving beyond the phase of concentrated selling.

“When the 30D-SMA of their realized loss cools and rolls over, it has often been among the clearest early signals that the heaviest distribution phase is behind the market.”

For traders and investors, the practical value of this type of signal is that it ties market stress to behavior on-chain. Rather than relying purely on speculative narratives around price, it focuses on whether holders most likely to capitulate are actually doing so—or whether that pressure is beginning to fade.

From on-chain loss exhaustion to the $69,000 price battleground

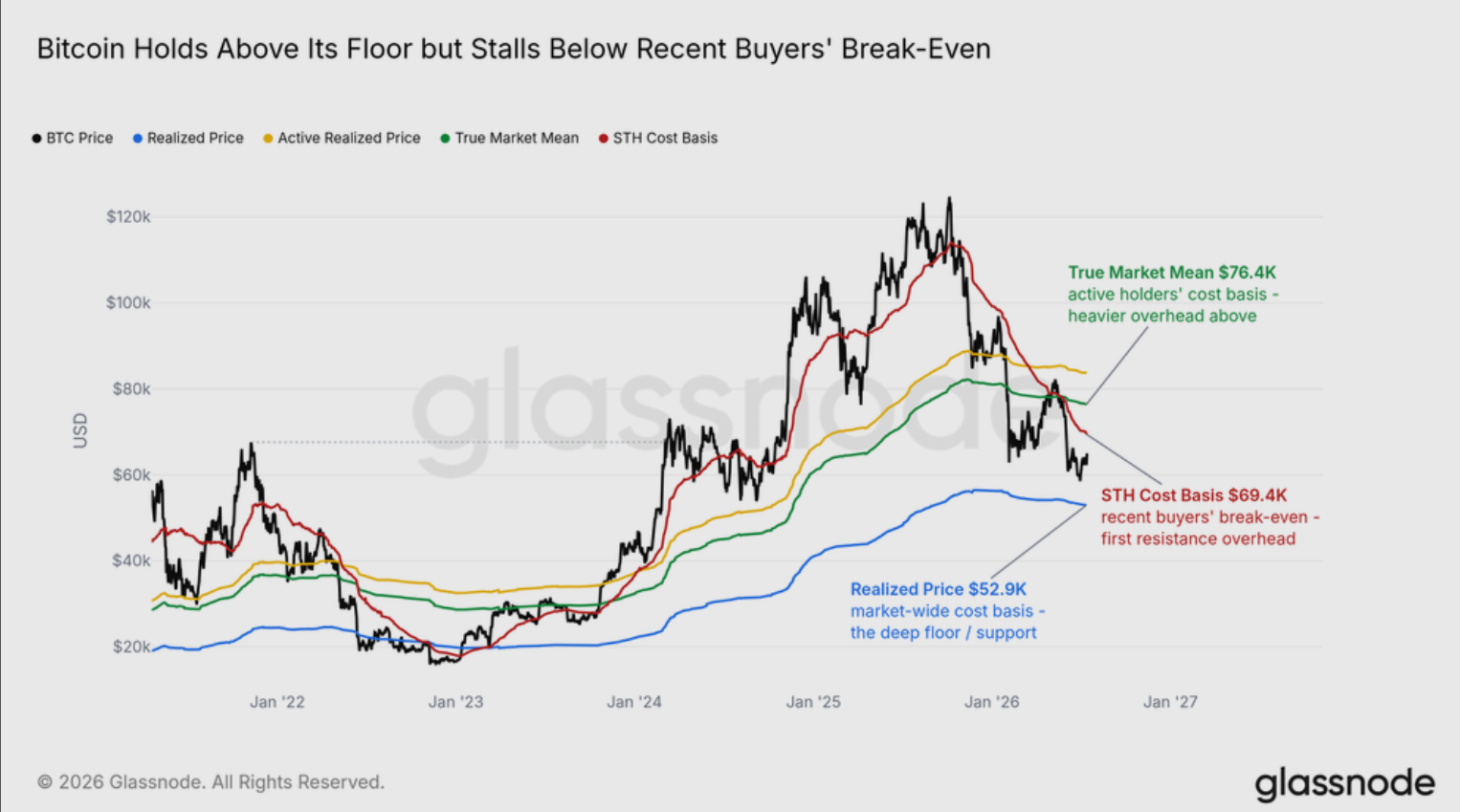

Realized losses are only one piece of the puzzle for bottom-timing. Glassnode’s ongoing work also emphasizes the role of cost basis—particularly for speculators who bought closer to the current price regime.

In its newsletter edition The Week Onchain, Glassnode pointed to Bitcoin speculators’ aggregate cost basis as the next hurdle the market may need to clear for momentum to improve. In the report, that reference level is around $69,000.

Notably, Glassnode says that this cost basis zone also overlaps with old all-time highs from the 2021 bull market. From an order-flow perspective, that overlap matters because it combines two forces that can amplify short-term reactions: sellers who bought at that level (or near it) may be more inclined to exit once price returns, while buyers trying to reclaim prior “breakout” levels may need to overcome earlier supply.

“The first meeting with that level will likely draw a strong reaction, because the people most inclined to sell are the ones about to be made whole.”

Glassnode also framed the scenario in terms of what happens immediately after price approaches the region: a convincing reclaim could open the door for more sustained recovery, while rejection would suggest the market is still negotiating its range rather than transitioning into a new phase.

“A convincing reclaim would give the recovery room to run; a rejection keeps the range intact.”

What to watch next as these signals converge

The most important development implied by Glassnode’s research is the alignment of two different on-chain narratives: (1) realized loss pressure from 1–2 year holders appears to be rolling over, and (2) the market is approaching a widely watched cost-basis resistance zone near $69,000. If realized losses continue to drift lower while price tests that cost-basis level, bulls will likely look for a sustained reclaim rather than a short-lived bounce; if realized losses stop improving or cost-basis resistance holds, the probability of prolonged consolidation increases.

Readers should watch whether the 30-day realized-loss trend continues to cool and whether BTC can hold above or reject the $69,000 region as the next clear confirmation point for market participants.

Veteran trader Peter Brandt has identified a possible bottoming structure on Bitcoin’s chart after the cryptocurrency rebounded from its late-June lows. Brandt stressed that traders still lack enough evidence to confirm the setup.

Summary

- Peter Brandt sees a possible Bitcoin bottom pattern but stresses that confirmation remains far away.

- Bitcoin rebounded from below $58,000, but the recovery remains stalled around the $65,000 resistance zone.

- Recent ETF flows and macro relief support Bitcoin, while weak spot demand keeps analysts cautious.

Bitcoin traded near $64,000 on July 16 after failing to hold above $65,000. It has recovered from below $58,000, but questions remain over whether spot demand can support a broader reversal.

Brandt flags an unconventional Bitcoin bottom pattern

In aJuly 16 post on X, Brandt said Bitcoin’s chart could be developing an inverted head-and-shoulders bottom. He described the structure as “VERY VERY UNCONVENTIONAL” and added, “We do NOT know yet.” He presented the formation as an early possibility rather than a confirmed signal.

An inverted head-and-shoulders pattern includes three price troughs, with the middle decline extending below the surrounding lows. Traders often wait for a break above the neckline before treating the setup as confirmed. Bitcoin has not completed such a move.

Bitcoin rebound meets resistance near $65,000

Bitcoin has gained roughly 12% from its recent swing low below $58,000, but the rebound has struggled around $65,000. The cryptocurrency briefly moved above $65,400 before returning toward $64,000, showing that buyers have not secured a clean breakout.

Notably, Brandt took a cautious view in June when Bitcoin traded near $65,000. His chart showed BTC below its 18-week moving average and outside a rising channel, while on-chain data showed large holders moving coins away from exchanges as selling eased.

Spot demand remains a key question for Bitcoin

Bitcoin’s possible bottom pattern appears as other market indicators send mixed signals. A recent Bitfinex Alpha report said Bitcoin’s recovery relied heavily on changing interest-rate expectations following softer US inflation data rather than sustained Bitcoin-specific buying.

As reported by crypto.news, Bitfinex called the rally “borrowed strength” because spot absorption remained limited, the Coinbase premium stayed negative and ETF demand lacked consistency. US spot Bitcoin ETFs recorded $424.7 million in net outflows on July 13 before attracting $181.1 million the next day.

The pattern therefore appears against a market backdrop that still lacks the steady demand seen during stronger Bitcoin uptrends. Bitfinex identified the $68,000 to $68,300 area as a key decision zone and said stronger ETF inflows and steady spot buying could support acceptance above that range.

Bearish Bitcoin scenarios remain in play

Brandt’s latest observation follows months of cautious Bitcoin forecasts. In January, he said the cryptocurrency could fall toward $58,000 to $62,000, a range Bitcoin later reached during the 2026 downturn. His more recent charts also showed weakness even as whale selling slowed.

Other researchers have kept deeper downside targets in view. A crypto.news analysis of Bitcoin’s bear-market levels noted that some cycle-based forecasts place a possible floor near $38,000, though those projections depend on the current decline repeating older Bitcoin cycles.

Brandt has not declared that Bitcoin has completed a bottom. His chart points to a structure that may develop if price action improves, but his warning leaves confirmation unresolved. Bitcoin’s ability to reclaim resistance, attract steady spot demand and sustain ETF inflows remains central to the recovery.

Vlad.fun, a memecoin launchpad built on Robinhood Chain, has suspended operations after reporting what it called a “serious internal integrity issue” involving members of its team.

Summary

- Vlad.fun halted operations after discovering an internal integrity issue involving members of its own team.

- The launchpad investigates alleged misconduct while consulting legal counsel on possible action against those involved.

- Robinhood Chain’s early growth has been dominated by memecoin trading despite its tokenized finance focus.

The project said it took the platform offline while it investigates the matter and consults legal counsel.

The team has not disclosed the nature of the alleged conduct or identified anyone involved. In its official statement on X, Vlad.fun said it would take appropriate action based on the findings of its investigation.

Vlad.fun takes its platform offline

Vlad.fun said it discovered the issue around the platform’s launch and that members of its team were involved. The project said it would not “gloss over it” and paused operations while reviewing what happened. It has not said whether user funds, token contracts or other parts of the platform were affected.

Hours before announcing the suspension, the project also warned users that a token carrying the Vlad.fun name and appearing on its leaderboard was not official. The team reminded traders through its official X account that its launchpad is permissionless and allows anyone to create tokens. Vlad.fun has not stated whether the token warning and internal investigation are connected.

Robinhood Chain’s memecoin boom forms the backdrop

Robinhood launched its public blockchain mainnet on July 1 as an Ethereum Layer 2 built with Arbitrum technology. As previously reported by crypto.news, Robinhood designed the network to support tokenized real-world assets, decentralized finance applications and around-the-clock trading of stock tokens.

However, memecoin trading quickly became a major source of activity. A recent crypto.news analysis found that Robinhood Chain processed about $570 million in launch-week trading volume against roughly $21.68 million in liquidity, with speculative memecoin activity driving much of the turnover.

Galaxy Digital also reported that memecoins became the network’s most active early use case. Trading volume surged above $560 million on July 8 as interest in tokens including CASHCAT drew more users and liquidity to the new network.

Launchpad disruptions draw closer attention

Vlad.fun is not the first Robinhood Chain launchpad to experience an operational disruption during the network’s early growth. As previously reported, NOXA went offline after becoming a major venue for token launches on Robinhood Chain. Its associated tokens continued trading onchain while its website remained unavailable.

The circumstances are different. NOXA attributed its outage to a Cloudflare problem, while Vlad.fun has cited an internal integrity matter involving team members and said it is consulting lawyers. There is currently no public evidence connecting the two events.

Investigation leaves key questions unanswered

Vlad.fun has not provided a timeline for completing its investigation or restoring the platform. It has also not disclosed whether the alleged issue involved token launches, team wallets, trading activity, platform access or another part of its operations.

For now, the project’s statement remains the main source of information about the shutdown. Users are awaiting more details about the scope of the investigation and any legal action that could follow. The suspension comes as Robinhood Chain continues its rapid expansion, with memecoin trading playing a large role in the network’s early activity.

Bitcoin (BTC) “cycle peak buyers” could already be pointing the way to the next bear-market bottom.

Key points:

- Bitcoin hodlers who bought BTC one to two years ago are cooling selling pressure.

- The cohort’s realized losses have led to market bottoms once their uptrend reverses, Glassnode data shows.

- Speculators’ cost basis reinforces the next BTC price battleground at $69,000.

Glassnode: Bitcoin realized loss reversal “worth watching closely”

In an X post on Friday, Cryptovizart, the pseudonymous lead research analyst at onchain analytics platform Glassnode, showed a classic bottom signal potentially repeating.

The latest in a series of such signals, the latest puts buyers who bought BTC in the latter part of the bull market in focus.

“One of the metrics I watch most closely when trying to gauge a bear market’s end is, Realized Loss volume (in USD) by the 1-2 year holders,” Cryptovizart wrote.

Here, coins moving onchain at a loss last did so between July 2024 and July 2025. During that time, BTC/USD increased from around $62,800 to $107,000, placing the majority of investors underwater on their allocation.

“As frustration builds with sustained price underperformance, this cohort tends to progressively increase loss realization,” the post continues.

“Historically, bear markets have not found durable footing until this specific group exhausts its sell pressure.”

Bitcoin realized losses for 1-2 year hodlers (30-day moving average). Source: Cryptovizart/X

An accompanying chart shows a spike in realized losses on a 30-day rolling basis, with the tally recently passing $75 million before beginning a reversal. For Cryptovizart, that feature is key.

“When the 30D-SMA of their realized loss cools and rolls over, it has often been among the clearest early signals that the heaviest distribution phase is behind the market,” they added.

“Worth watching closely.”

Focus shifts to $69,000 BTC price showdown

Hodler realized losses are not the only onchain metric on the radar when it comes to timing the next macro BTC price floor.

Related: Bitcoin gets new $80K August target: Watch these BTC price levels next

As Cointelegraph reported, stochastic relative strength index (RSI) values on two-month time frames are creating classic market reversal conditions.

In the latest edition of its regular newsletter, The Week Onchain, Glassnode meanwhile flagged Bitcoin speculators’ aggregate cost basis as bulls’ next resistance hurdle.

At around $69,000, the cost basis for short-term holders (STHs) also coincides with old all-time highs from the 2021 bull market.

“The first meeting with that level will likely draw a strong reaction, because the people most inclined to sell are the ones about to be made whole,” it read.

“A convincing reclaim would give the recovery room to run; a rejection keeps the range intact.”

BTC/USD chart with cost-basis levels (screenshot). Source: Glassnode

A Bitcoin wallet that had remained inactive for more than eight years has transferred 5,908 BTC worth about $383 million, reviving another long-dormant holding as traders continue tracking large onchain movements.

Summary

- A Bitcoin wallet dormant for more than eight years transferred 5,908 BTC worth about $383 million to a new address.

- Onchain data showed the coins were not sent to a known exchange wallet, leaving the holder’s intentions unclear.

- The transfer followed another dormant whale move earlier this week, keeping large Bitcoin wallet activity in focus.

According to blockchain analytics platform Lookonchain, citing Arkham data, the wallet identified as “138EM…ReyiT” moved the entire 5,908 BTC balance to a new address at 7:15 p.m. ET on Wednesday. The coins remain in the recipient wallet, with no signs that they have been sent to a cryptocurrency exchange.

Arkham’s data showed the wallet originally received the Bitcoin in December 2017, when BTC traded near $16,800. The holdings were worth about $99.6 million at the time, compared with roughly $383 million at current market prices.

The timing of the original purchase makes the wallet notable. The holder kept the coins through Bitcoin’s nearly 80% decline in 2018, its rally to almost $69,000 in 2021, the subsequent fall to around $15,500 in late 2022, and the record high above $122,000 reached in October 2025, according to market price data. At that peak, the wallet’s balance was worth about $726 million.

While the movement has drawn attention, CoinDesk’s onchain analysis said the Bitcoin was transferred to a newly created, unlabeled address rather than a known exchange deposit address, indicating there is no onchain evidence of an immediate public sale.

The report also noted that the coins moved from a legacy Bitcoin address beginning with “1” to a newer SegWit address beginning with “bc1q.” According to CoinDesk, large holders often reorganize assets to upgrade wallet formats, improve custody, rotate private keys, prepare estate transfers, or arrange over-the-counter transactions that do not reach public exchanges.

Dormant whale activity remains in focus

The latest transfer follows another dormant Bitcoin wallet that became active earlier this week after more than seven years. As previously reported by crypto.news, blockchain intelligence platform Arkham said a wallet moved 2,931 BTC worth about $188 million to a new address after remaining inactive since Bitcoin traded near $6,500.

Although neither transfer has confirmed selling activity, CryptoQuant has reported that whale-sized deposits continue to dominate Bitcoin exchange inflows. Its exchange whale ratio recently stood at 0.99, indicating that the 10 largest transfers accounted for nearly all Bitcoin deposited to exchanges.

According to the firm, elevated readings have historically been associated with higher selling pressure because large deposits are more likely to precede sizable sales.

Iran says ‘we will kill Trump’ in new billboard of US president in a coffin | News World

SKS revives Burswood project

Ondo Hits 1-Month High: Here Is What’s Driving The 17% Surge

-

Fashion7 days ago

Fashion7 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports7 days ago

Sports7 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech7 days ago

Tech7 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics22 hours ago

Politics22 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos2 days ago

News Videos2 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech2 days ago

Tech2 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Sports12 hours ago

Sports12 hours agoNew Cornerback Enters Vikings Trade Rumor Mill

-

Entertainment17 hours ago

Entertainment17 hours agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Tech7 days ago

Tech7 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

NewsBeat7 days ago

NewsBeat7 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos3 days ago

News Videos3 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech3 days ago

Tech3 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Entertainment15 hours ago

Entertainment15 hours agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World2 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

NewsBeat12 hours ago

NewsBeat12 hours agoWatch: Is Donald Trump facing a popular backlash on immigration?

-

Sports10 hours ago

Sports10 hours agoMichigan officials not expected to discuss AD Warde Manuel at Thursday meeting

-

NewsBeat12 hours ago

NewsBeat12 hours agoFirefighters issue update on Dovestone moorland blaze as fire enters fourth day

You must be logged in to post a comment Login