Crypto World

Binance’s CZ rejects “fake news” claim of 60,000 BTC BitMEX hedge profits

CZ denies Binance ever traded on BitMEX or booked 60,000 BTC in hedge profits during the March 2020 crash, calling the viral allegation “fake news” and technically impossible.

Summary

- CZ responds to a viral post alleging Binance hedged client flow on BitMEX for over 60,000 BTC in profit during the March 2020 “Covid crash,” dismissing it as fabricated “fake news”.

- He stresses that Binance “never traded on BitMex” and points to the exchange’s once‑daily withdrawal schedule at the time as a practical barrier to real‑time hedging of that size.

- Commentators and BitMEX itself say there are no records of such flows, framing the debate as another example of rumor‑driven FUD and how old anecdotes morph into conspiracy narratives.

Binance founder Changpeng “CZ” Zhao has moved to quash fresh allegations that the exchange secretly booked more than 60,000 BTC in profits by hedging client risk on BitMEX during the March 2020 crash, dismissing the claim as “fake news” and emblematic of the rumor‑driven warfare that still defines much of crypto trading culture.

CZ pushes back on BitMEX hedge narrative

Responding to a viral post from Flood, CEO of fullstack_trade on Hyperliquid, CZ said the allegation that Binance hedged flow on BitMEX for over 60,000 BTC in profit during the Covid‑era liquidation cascade was entirely fabricated. “4. Fake news. They just making things up randomly now. Not sure what their goal is. I feel bad for the people believing this without seeing any proof,” he wrote, adding bluntly that “Binance never traded on BitMex.” Zhao tagged BitMEX co‑founder Arthur Hayes to underline a key operational constraint at the time, noting that “BitMex processes withdrawals only once a day,” a structure that would have made real‑time risk‑hedging of that magnitude effectively impossible.

BitMEX and traders call claim “impossible”

Market participants quickly weighed in to deconstruct the 60,000 BTC storyline. “Exactly. BitMEX’s once-a-day withdrawal window back in 2020 made it impossible for an exchange to use it for a real-time hedge of that size,” commentator Murtuza J. Merchant argued, stressing that “no entity would trap 60,000 BTC in a manual multi-sig during a black swan crash.” He suggested the “60k figure is likely just a garbled memory of old” market anecdotes rather than a verifiable trade record. BitMEX itself has since confirmed that it has no records supporting the alleged flows and pointed to its upgrade from once‑daily batched withdrawals to real‑time payouts as part of broader infrastructure changes since 2020.

FUD, Binance’s legacy, and market context

Not everyone accepted the “fake news” framing. One critic, posting under the handle Broly, countered that “Binance has had a major role in every major downfall of crypto,” citing the exchange’s role in the FTX collapse, its backing of LUNA before withdrawals were halted, and its influence around other major dislocations. The episode has been widely mocked as yet another round of competitive FUD, but it also underscores how opaque cross‑exchange flows, historical grievances, and incomplete memories can quickly harden into conspiracy narratives in a market that still trades on screenshots and hearsay as often as audited disclosures.

Market prices and further reading

This parabolic move comes as digital assets continue to trade as the purest expression of macro risk appetite. Bitcoin (BTC) is hovering around $68,280, with a recent 24‑hour range between roughly $64,760 and $71,450. Ethereum (ETH) is trading near the low‑$2,000 band, with prediction markets clustering key levels between about $1,940 and $2,100 over the near term. Solana (SOL) changes hands around $78–81, roughly flat on the session after a modest pullback from recent highs.

Opinion by: Francesco Mosterts, co-founder of Umia.

Crypto prides itself on being a market-driven system. Prices, incentives, and capital flows determine everything from token valuations to lending rates and blockspace demand. Markets are the industry’s primary coordination mechanism. Yet, when it comes to governance, crypto suddenly abandons markets altogether.

Recent governance disputes at major protocols have once again exposed the tensions inside DAO decision-making. Participation remains extremely low and influence is highly concentrated. A study of 50 DAOs found “a discernible pattern of low token holder engagement,” showing that a single large voter could sway 35% of outcomes and that four voters or fewer influence two-thirds of governance decisions.

This is not the decentralized future crypto originally set out to build. The early vision of the industry was to remove concentrated power and replace it with systems that distributed influence more fairly. Instead, DAO governance often leaves most tokenholders passive while a small group determines the protocol’s direction.

Token voting was crypto’s first attempt at decentralized governance. It is a broken incentive system, and it needs to change.

The promise of token governance

The original “DAO” launched in 2016 as a decentralized venture fund where token holders would vote on which projects to finance. The earliest DAOs were inspired by the idea that organizations could run purely through code.

At crypto’s conception, token voting felt intuitive. It borrowed from familiar concepts like shareholder voting, yet DAOs promised a new form of management called “decentralized governance.” Tokens would represent both ownership and decision rights, meaning anyone who held them could participate in shaping the direction of a protocol.

Related: ‘Raider’ investors are looting DAOs

Token voting was supposed to solve problems seen across many industries, including centralized control, opaque decision-making, and misalignment between teams and users. It offered a simple promise: if the community owned the token, the community would run the project. In practice, however, this miraculous solution hasn’t delivered on its promise.

The reality of why token voting fails

Token voting comes with three core problems: participation, whales, and incentives.

Participation is self-explanatory: most token holders don’t vote. With lots of material to review, particularly when many governance decisions need to be made, governance fatigue is a real problem. The result of this, which we now see every day in crypto, is that most token holders are ultimately passive and a small minority decides the outcomes.

When it comes to whales, it is obvious that large holders are dominating. It’s demoralizing for ordinary voters who feel like their opinions don’t matter, even though the original promise of DAOs was that they would have a real voice. What is the point of voting if whales have the final say?

Finally, there’s an incentive problem. Voting has no economic signal. Votes hold the same weight whether you’re informed or not. There’s no cost to being wrong and no incentive for being right. There’s nothing motivating participants to research and vote according to their beliefs.

Realistically, in current governance, voting simply expresses opinions. It does not express conviction.

The missing piece lies in pricing decisions

Crypto is fundamentally market-driven, and it works remarkably well. Markets aggregate information, price risk, and reveal conviction in ways few other systems can. The industry has built markets for practically everything, including tokens, derivatives, blockspace, and lending rates. They sit at the core of how crypto coordinates economic activity. Yet when it comes to governance, the system suddenly abandons markets entirely.

Decision markets introduce pricing into governance. Instead of merely voting on proposals, participants trade outcomes, pricing the possible decisions and backing their views with capital. This transforms governance from a system of expressed preferences into one of measurable conviction.

By tying decisions to economic incentives, participants are encouraged to research proposals and think carefully about outcomes. The result is a governance process that reflects informed expectations rather than passive opinion.

This matters now

Crypto is reaching a turning point in how it coordinates decisions. Governance conflicts, treasury disputes, and stalled proposals have exposed the limits of token voting. Even major protocols struggle to translate tokenholder input into clear, effective action. This has left governance slow, contentious, and dominated by a small group of participants.

At the same time, interest in market-based coordination is resurging across the ecosystem. Prediction markets have demonstrated how effectively markets can aggregate information, while broader discussions around mechanisms like futarchy are returning to the forefront. These systems highlight markets as powerful tools for revealing conviction and aligning incentives.

If crypto believes in markets as coordination engines, the next step is applying that same logic to governance. The next phase of crypto coordination will move beyond simply trading assets and toward pricing and executing decisions themselves.

Token voting was crypto’s first attempt at decentralized governance, and it was an important experiment. It gave tokenholders a voice, but it didn’t solve the deeper incentive problem.

Markets already power nearly every part of the crypto ecosystem. They aggregate information, reveal conviction, and align incentives at scale. Extending that same mechanism to decisions is the natural next step.

Decision markets also extend beyond governance votes into capital allocation itself. If markets can price decisions about a protocol’s direction, they can also price decisions about what to build and fund. This opens the door to a new generation of ventures built directly on crypto rails, where projects can raise capital and allocate resources through transparent, incentive-aligned mechanisms from day one. Instead of relying on passive token voting, markets can actively guide how onchain organizations form and grow.

Governance without pricing is incomplete. If crypto truly believes in markets as coordination engines, the future of onchain organizations cannot be decided by votes alone, but by markets.

Opinion by: Francesco Mosterts, co-founder of Umia.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

Summary

- Gnosis, Zisk and the Ethereum Foundation unveiled the Ethereum Economic Zone (EEZ) at EthCC in Cannes to unify fragmented Ethereum layer-2 networks.

- The framework targets over 20 L2s securing roughly $40 billion in value, enabling synchronous composability without relying on bridges and standardizing ETH as gas.

- Early backers include Aave and Centrifuge, with developers calling EEZ a “new era” for on-chain applications as Ethereum grapples with slowing fee revenue and a weaker deflationary narrative.

The Ethereum (ETH) ecosystem took aim at one of its biggest structural weaknesses at EthCC 2026, as Gnosis, Zisk and the Ethereum Foundation publicly launched the Ethereum Economic Zone (EEZ), a rollup framework designed to knit together an increasingly fractured layer‑2 landscape. Revealed on March 29 at the Palais des Festivals in Cannes, the initiative seeks to make dozens of Ethereum L2s behave “like one unified system,” in the words of project backers, by restoring synchronous composability between rollups and Ethereum mainnet while keeping security anchored to the base chain.

Ethereum Economic Zone launches

More than 20 operational Ethereum L2s currently secure about $40 billion in assets, yet function largely as isolated ecosystems, each with its own liquidity pools, deployments and bridge infrastructure. “Ethereum doesn’t have a scaling problem. It has a fragmentation problem,” Gnosis co‑founder Friederike Ernst said in comments shared with crypto media, arguing that “every new L2 that goes live has its own liquidity pool and bridging, creating another isolated walled garden.” The EEZ framework instead allows smart contracts on participating rollups to perform synchronous calls with each other and with Ethereum mainnet in a single atomic transaction, using ETH as the default gas token and removing the need for separate bridge protocols.

At EthCC, Ernst and Zisk developer Jordi Baylina presented the EEZ as an explicitly Ethereum‑aligned answer to the user‑experience and capital‑efficiency frictions created by the network’s L2‑centric scaling roadmap. According to coverage from outlets such as The Block and CoinDesk, the collaboration is co‑funded by the Ethereum Foundation and launches with Aave, Centrifuge and a Swiss‑based EEZ Alliance among its early partners, underscoring that DeFi blue chips see value in shared liquidity and cross‑rollup settlement. “The zone will facilitate a new era of blockchain innovation,” Zisk’s CEO Maria Roberts told conference attendees, adding that developers will be able to plug existing applications into the framework “pretty easily.”

The timing is not accidental. Ethereum’s shift of activity toward cheaper L2s has reduced fee revenue on mainnet and softened the narrative of ether as a strongly deflationary asset, with ETH trading near $2,000 even as the network still secures roughly $53 billion in DeFi total value locked and about $163 billion in stablecoins, according to recent market data cited by Phemex. By unifying L2 liquidity and simplifying cross‑network flows, EEZ’s architects are betting that a more cohesive Ethereum stack can keep capital and users inside the ecosystem, even as competing smart contract platforms and modular architectures fight for market share.

Kaiko reports Alameda gap still existsIn separate reporting on EthCC, organizers have described 2026 as “the year of professionalisation of Ethereum and the wider crypto ecosystem,” with the conference’s move to Cannes and the launch of institutional‑focused forums like Kaiko’s Agora strengthening the sense that Ethereum’s next phase will be defined as much by market structure and infrastructure as by new token launches.

Michael Selig, US President Donald Trump’s nominee leading the Commodity Futures Trading Commission (CFTC), said the agency was prepared to oversee the entire $3 trillion crypto industry, with no timeline for Congress to pass a crucial market structure bill.

In a Wednesday statement about his first 100 days as CFTC chair, Selig said that the commission was “ready to take responsibility” for the crypto market and reiterated his claim that it was the sole regulator to oversee prediction markets.

His comments come as the US Senate considers the CLARITY Act, a crypto market structure bill that has been effectively stalled in committee amid discussions over stablecoin yield and other issues.

“The same regulatory clarity being delivered to the crypto industry is being developed for prediction markets, which can serve as powerful tools for information discovery and are regulated by the CFTC under the Commodity Exchange Act,” said Selig.

Under Selig, who was confirmed by the Senate in December, the CFTC has adopted many policies signaling that the agency would soften its enforcement and regulation of digital assets compared to previous administrations. In March, the agency announced a memorandum of understanding with the Securities and Exchange Commission (SEC) as part of efforts to coordinate on regulation, including digital assets.

Related: Crypto exchange KuCoin agrees to $500K settlement, ending CFTC case

Although early drafts of the market structure bill suggested the legislation could give the CFTC additional authority to oversee digital assets, the SEC is expected to continue regulating cryptocurrencies it considers to be securities.

Lawmakers pressing CFTC on insider trading claims over prediction markets

US state authorities and federal lawmakers have been targeting prediction market platforms like Kalshi and Polymarket over alleged violations of gaming laws and claims of politicians using insider information to profit.

While many of the state-level actions continue to be litigated in court, Selig has claimed that the CFTC has “exclusive jurisdiction” over prediction markets and threatened legal action against any challenges to its authority.

In a Tuesday event, CFTC enforcement director David Miller said that the agency’s position was that event contracts on prediction markets were not “gaming” but rather “swaps” that fall under its purview.

Some lawmakers have also proposed legislation to ban elected officials with insider information from profiting from event contracts after suspicious trades on military actions involving Iran and Venezuela.

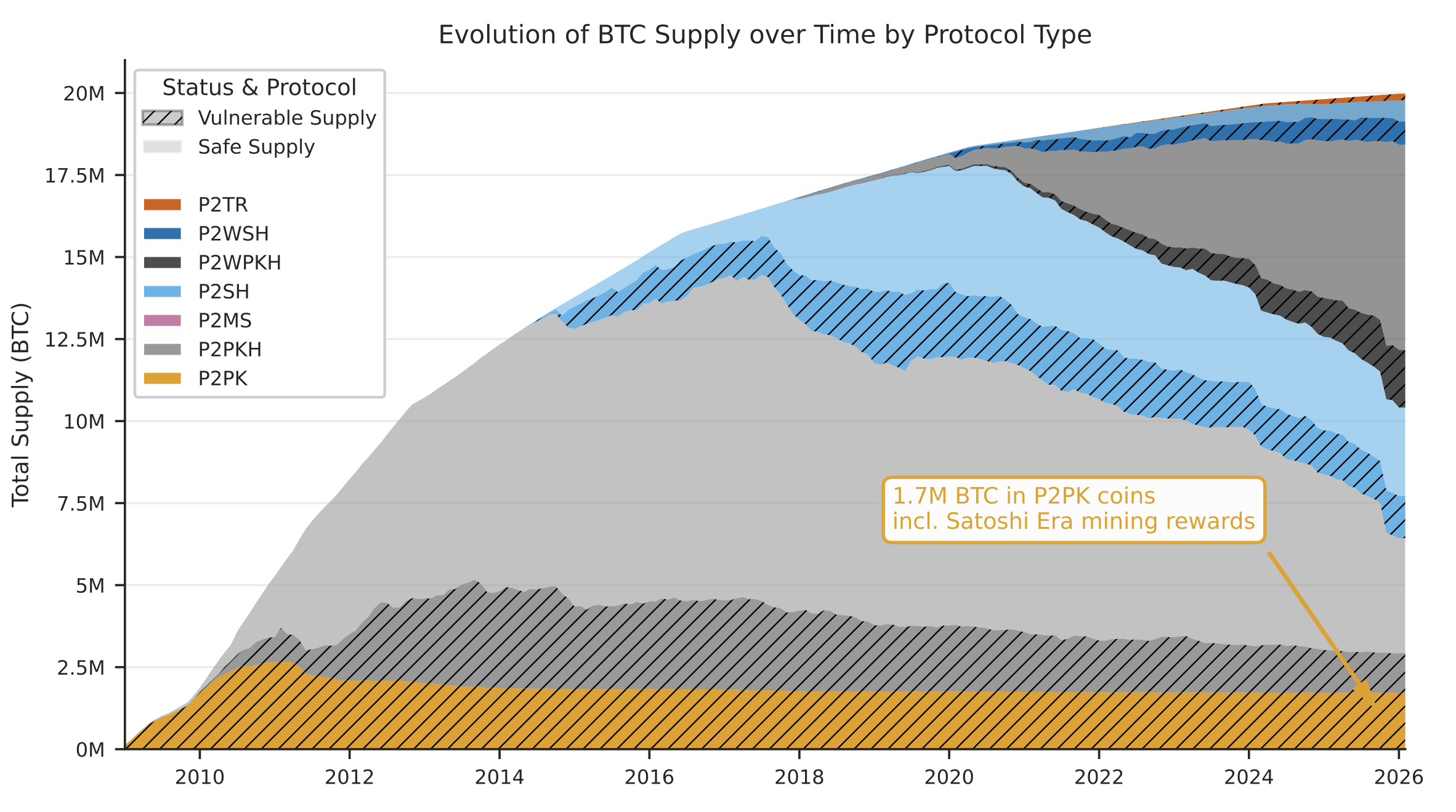

Naoris Protocol has launched its mainnet, introducing a layer-1 blockchain designed to use post-quantum cryptography for transaction validation and network security. The network is live with limited, invite-only participation, allowing early users to run validator nodes and process transactions.

According to an announcement shared with Cointelegraph, it integrates cryptographic standards finalized by the National Institute of Standards and Technology (NIST) to address risks in existing blockchains, where current encryption methods could become vulnerable over time.

Before mainnet, the protocol’s test network processed more than 100 million transactions and identified hundreds of millions of potential threats, according to the project, with activity spanning millions of wallets and nodes.

The system uses a consensus model called distributed proof of security (dPoSec) to verify transactions across nodes, while the NAORIS token is intended to support network operations as the economic model develops.

The rollout begins with a restricted group of validators and partners, with broader access expected to expand in phases.

The project lists advisers with backgrounds in cybersecurity, government and enterprise technology, and is backed by investors including Draper Associates.

Related: Is $450B in Bitcoin vulnerable to the quantum threat? Analysts weigh in

New research suggests quantum computing may arrive sooner than expected

The launch comes as revised estimates for quantum computing, which uses qubits and quantum states to process information differently from classical computers, are driving efforts to move away from current cryptographic standards.

New research from Google released on Monday suggests quantum computers may need far fewer resources than previously thought to break blockchain encryption. The study found fewer than 500,000 physical qubits could crack systems securing Bitcoin (BTC) and Ether (ETH), a roughly 20-fold reduction from earlier estimates.

The findings point to a shorter timeline for quantum risk, with Justin Drake, a researcher at the Ethereum Foundation, estimating at least a 10% chance that a quantum computer could recover a private key by 2032.

Researchers at California Institute of Technology working with Oratomic reached similar conclusions, recently finding that improvements in error correction (which reduce the number of qubits needed to stabilize computations) could lower the requirements for practical systems to 10,000 to 20,000 qubits, down from earlier assumptions of millions.

Based on these reductions, the researchers said a viable quantum computer could emerge by around 2030.

Blockchain developers are beginning to respond. In January, developers in the Solana ecosystem introduced a quantum-resistant vault that uses hash-based signatures to generate new keys for each transaction, reducing the exposure of public keys.

On March 24, developers from the Ethereum Foundation launched a “Post-Quantum Ethereum” resource hub outlining plans to upgrade the network’s cryptography, targeting protocol-level changes by 2029 while also noting the multi-year complexity of such a transition.

Crypto World

Crypto Will Never Die As Iran Signals De-Escalation and Whales Are Quietly Buying Pepeto While Retail Panics

The correction looks like chaos, but the pattern tells a different story. Bitcoin was born in 2009 after the 2008 crisis wiped out trillions, while banks got bailouts. Now, Iran’s president signaled readiness to end the war this week, sending crypto, stocks, gold and silver rallying simultaneously as markets priced in de-escalation for the first time since the conflict began according to Decrypt.

Governments that hold BTC in federal reserves need the price higher to manage $36 trillion in debt, and Fear 8 is designed to move cheap coins from retail into the wallets that understand the cycle.

The crypto news matters because the same forces shaking out retail are the ones that need crypto to explode, and while that shakeout runs, more than $8.69 million flowed into one presale.

Pepeto filled stages during extreme fear with the Binance listing confirmed, and the Pepe cofounder plus exchange tools plus confirmed listing is the rarest combination crypto produces once per cycle, because meme energy plus real utility at the same time is the setup that delivers the return.

The Real Crypto News: Iran De-Escalation Signals Recovery While Governments Need BTC Higher

BTC was added to US federal reserves because the national debt exceeds $36 trillion and holding assets that appreciate helps service it without printing more dollars, according to CoinDesk. Iran’s president signaling willingness to end the conflict sent Bitcoin climbing above $68,000 in hours as traders priced in the possibility of geopolitical stabilization for the first time this year according to Decrypt.

The Fear and Greed Index at 8 is the shakeout that transfers cheap coins from retail to large wallets, and on chain data shows whales continuing to accumulate BTC while retail sold, according to CoinGecko.

The crypto news confirms that the people who control the market are buying what retail is selling, and the presale crossing $8.69 million during that fear proves where the smart capital goes next.

The Exchange the Whales Are Entering Because the Tools Are What Makes the Listing Deliver

Pepeto

The verified exchange keeps filling while the broader market corrects, and more than $8.69 million flowing in during Fear 8 tells you everything about who is buying and why. Pepeto is at the center of the crypto news that matters.

The platform puts every tool in one clean window. No jumping between tabs. Every tool is labelled and one action away from protecting your capital or pointing you toward the entry others miss. PepetoSwap removes every trading fee, and the cross chain bridge moves tokens at zero cost.

More than $8.69 million raised at $0.000000186 with 190% APY staking compounding positions while stages fill. SolidProof confirmed every contract is clean, and the mind behind the original Pepe coin that hit $11 billion on 420 trillion tokens put together the exchange with a former Binance expert directing the tools.

The Binance listing approaches, and the window at current pricing closes fast. After listing, price discovery begins, and the entry disappears permanently. Analysts project 100x, and Pepeto at this level could be the strongest move before the crypto news turns positive and the shakeout ends.

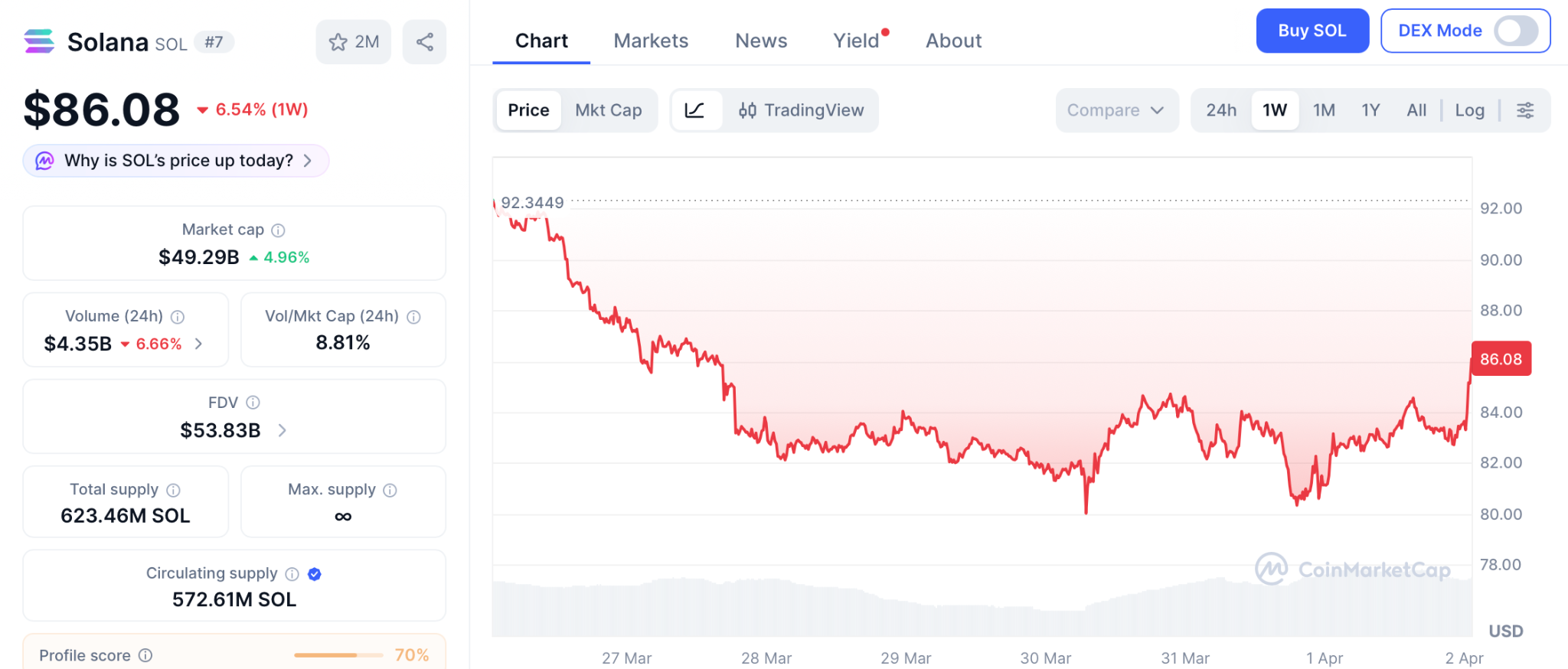

Solana

SOL trades at $86.08 according to CoinMarketCap, after declining from highs earlier this year. Bulls must defend $75 or risk a slide to $65.

Longer term targets point toward recovery, but that requires months of patience and geopolitical relief that is only now beginning to surface with the Iran de-escalation signals, while the presale at 100x from one listing delivers sooner.

River

River climbed 38% weekly after finding support with resistance above and a path higher if buying holds.

Strong weekly numbers, but the verified exchange with $8.69 million raised and a confirmed Binance listing at 100x offers the wider return from one event.

Crypto News Confirms the Pepe Cofounder Plus Exchange Plus Listing Is the Rarest Combination

The crypto news signals a potential turning point as Iran’s president opens the door to de-escalation, and governments that need BTC higher will eventually get what they need, but the 100x potential from the verified presale makes it the strongest move for anyone who wants to be on the right side of the cycle instead of the losing side.

The Pepeto official website is where entering now while whales load and retail panics is how you position alongside the same capital that built the recovery from every crisis, because the Pepe cofounder plus verified exchange tools plus confirmed Binance listing is the combination that delivers returns once per cycle, and the wallets inside already know it.

Click To Visit Pepeto Website To Enter The Presale

FAQs:

What is the real story behind the current crypto news correction?

Governments holding BTC in federal reserves need the price higher to manage debt. Iran signaling de-escalation sent markets rallying. The Fear 8 reading is a shakeout designed to transfer cheap coins from retail to whales.

Why are whales entering the Pepeto presale, according to the crypto news?

The verified exchange raised more than $8.69 million during extreme fear with a confirmed Binance listing. The Pepeto official website is where the same conviction driving institutional accumulation is flowing into the presale.

Will the crypto news improve, and should the reader wait for better conditions?

Iran de-escalation signals suggest the market may be turning, but the presale price disappears when the listing arrives. Waiting means paying the listing price instead of the presale price.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Crypto bull cycles over the past 5 years have been mostly about token speculation and, more recently, institutional adoption. But the next cycle will be dominated by real-world applications, according to Clem Chambers – founder of ADVFN, Europe’s leading stocks and markets website

Speaking at BeInCrypto’s Markets Intelligence Council, Chambers argued that the industry is moving past its trading-driven cycle.

“That era has probably ended and certainly is coming to an end. And then that will be replaced by use cases,” he said, pointing to a structural change in how value is created in crypto.

The Trade Is Crowded, The Utility Isn’t

His comments come as the current cycle shows clear divergence between price action and underlying activity. Bitcoin and Ethereum continue to attract institutional flows, especially in a post-ETF environment.

However, capital is concentrating at the top, while mid-tier tokens struggle to hold attention or liquidity.

At the same time, a different layer of the market is gaining traction. Tokenized real-world assets, stablecoin-based payment rails, and blockchain infrastructure tied to AI and data are seeing steady growth.

These sectors generate usage, fees, and in some cases, real revenue — something most speculative tokens failed to deliver in previous cycles.

Forget Tokens, Think Products

Chambers framed this shift bluntly.

“Forget Fi and look for apps, not Fi, apps, applications of tokens and blockchains,” he said.

Earlier cycles focused on financial primitives — DeFi protocols, yield farming, and token trading. The emerging trend centers on applications that users interact with directly, often without focusing on the underlying token.

This aligns with broader market signals in 2026. Tokenized funds from firms like BlackRock and growing stablecoin usage in payments show how blockchain is embedding into existing financial systems.

Meanwhile, infrastructure sectors such as decentralized physical networks and AI-linked protocols are attracting developer activity and venture funding.

However, this transition is uneven. Speculative trading still drives short-term price moves, and retail participation remains largely momentum-based.

Many application-layer projects also struggle with user retention and monetization.

Even so, the direction is becoming clearer. If previous cycles were driven by narratives around tokens, the next phase may depend on whether blockchain-based applications can deliver consistent utility.

Chambers’ argument reflects a broader reality: the market is starting to reward usage over hype.

Whether that shift fully defines the next cycle will depend on how quickly these applications can scale beyond crypto-native users.

The post The Next Crypto Bull Run Won’t Be About Coins or Viral Hype appeared first on BeInCrypto.

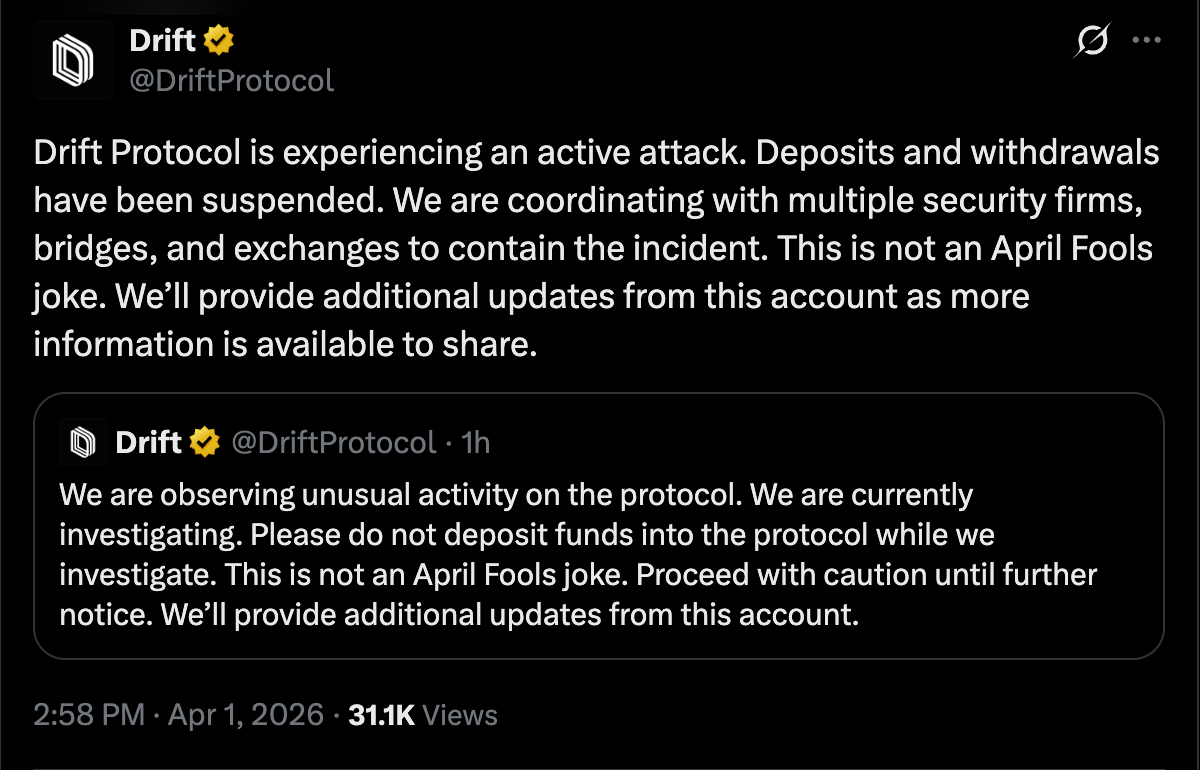

Drift Protocol, a decentralized cryptocurrency exchange (DEX), detected “unusual” trading activity on the platform on Wednesday, warning users not to deposit funds until the issue has been resolved.

The Drift team did not disclose the specific cause of the ongoing incident or the damage in its initial announcement and is currently investigating the issue.

In a subsequent update, the Drift team announced that deposits and withdrawals on the platform have been suspended.

Blockchain cybersecurity threat researcher Vladimir S said the exploit was likely due to a crypto wallet private key leak, and the total funds lost in the incident could be as high as $200 million.

“Admin signer was compromised, or whoever controls it intentionally executed these changes,” he said.

The stolen assets include wrapped versions of Bitcoin (BTC), Jito (JTO), the Fartcoin (FRT) memecoin, other altcoins, and various dollar, euro, and Japanese yen stablecoins, which have since been transferred to multiple wallets, according to Vladimir S.

The exploiter started converting the stolen assets to the USDC (USDC) stablecoin, bridging the funds to the Ethereum network and purchasing Ether (ETH), according to Solana treasury company DeFi Development Corp.

Cointelegraph reached out to Drift Protocol but did not receive an immediate response by the time of publication.

Cybersecurity exploits and hacks were responsible for $49 million in crypto losses during February, a sharp decrease from January, but a reflection of the ongoing security threats users and platforms face.

Related: Resolv temporarily halts protocol to ‘contain the impact’ of 80M USR exploit

Drift token impacted by the exploit

The price of the Drift (DRIFT) token briefly reached $0.68 on Wednesday, but fell by about 18% following news of the exploit, according to data from CoinMarketCap.

About 83% of the native crypto tokens of hacked platforms never recover to pre-hack prices, according to blockchain security company Immunefi.

“The stolen funds are only the first layer of damage,” Immunefi CEO Mitchell Amador told Cointelegraph in March.

“What follows is often more destructive: sustained token price suppression, reduced treasury capacity, leadership disruption, lost development time, and erosion of user trust,” he added.

Magazine: WazirX hackers prepped 8 days before attack, swindlers fake fiat for USDT: Asia Express

Crypto World

Paradigm Is Building a Prediction Markets Trading Terminal Targeting Professional Traders

TLDR:

- Paradigm partner Arjun Balaji has been leading the trading terminal project since late 2025 for pro traders.

- The firm is exploring prediction market indexes by bundling multiple markets into one single tradable product.

- Kalshi, backed by Paradigm, has raised at least $1 billion, pushing its valuation to a record $22 billion.

- Paradigm is raising up to $1.5 billion for a new fund expanding beyond crypto into AI and robotics sectors.

Paradigm, the prominent crypto venture capital firm, is developing a prediction markets trading terminal, sources say.

Partner Arjun Balaji has been leading the project since late 2025. The terminal targets professional traders and market makers. Paradigm has declined to comment on the initiative.

This move comes as mainstream financial institutions rush to capitalize on prediction markets’ growing popularity across sports, elections, and crypto pricing.

Paradigm Eyes Market-Making and Index Products

Beyond the trading terminal, Paradigm is weighing whether to establish an internal market-making desk. Two sources confirmed the firm has actively discussed this possibility. A market-making desk would position Paradigm as a direct participant, not just an infrastructure builder.

Separately, a third source says Paradigm is working with researchers on prediction market indexes. The concept involves bundling multiple prediction markets into one tradable product.

This mirrors how the S&P 500 packages hundreds of stocks into a single instrument. The firm has already started collecting prediction market data into a public dashboard.

Sources familiar with the matter noted that Balaji has been working on the terminal project since late 2025. They spoke on condition of anonymity to discuss private business dealings. Paradigm’s spokesperson declined to comment when approached for a response.

This activity places Paradigm squarely inside a rapidly growing sector. Prediction markets have become one of Silicon Valley’s most discussed areas over the past year. Traditional financial players are also moving in, adding further competitive pressure.

Kalshi and Polymarket Drive Sector Valuations Higher

Paradigm has been a consistent backer of Kalshi, one of the two dominant prediction market platforms. The firm joined three successive Kalshi fundraising rounds in 2025. Paradigm also led a December round that valued Kalshi at $11 billion.

Kalshi has since raised at least $1 billion in new financing, bringing its valuation to $22 billion. Paradigm co-founder Matt Huang sits on Kalshi’s board of directors.

One source confirmed that Paradigm’s trading terminal is “not competitive with Kalshi’s platform,” drawing a clear line between the two products.

Rival platform Polymarket is also seeing sharp valuation growth. The Wall Street Journal reported Polymarket is in talks to raise at a roughly $20 billion valuation.

A new venture firm focused entirely on prediction markets has also emerged, backed by the CEOs of both platforms.

Paradigm’s prediction markets push fits within a wider expansion beyond crypto. The firm is raising up to $1.5 billion for a new fund covering AI and robotics alongside digital assets.

The Wall Street Journal recently reported on the fund’s broader scope, marking a clear shift in Paradigm’s investment direction.

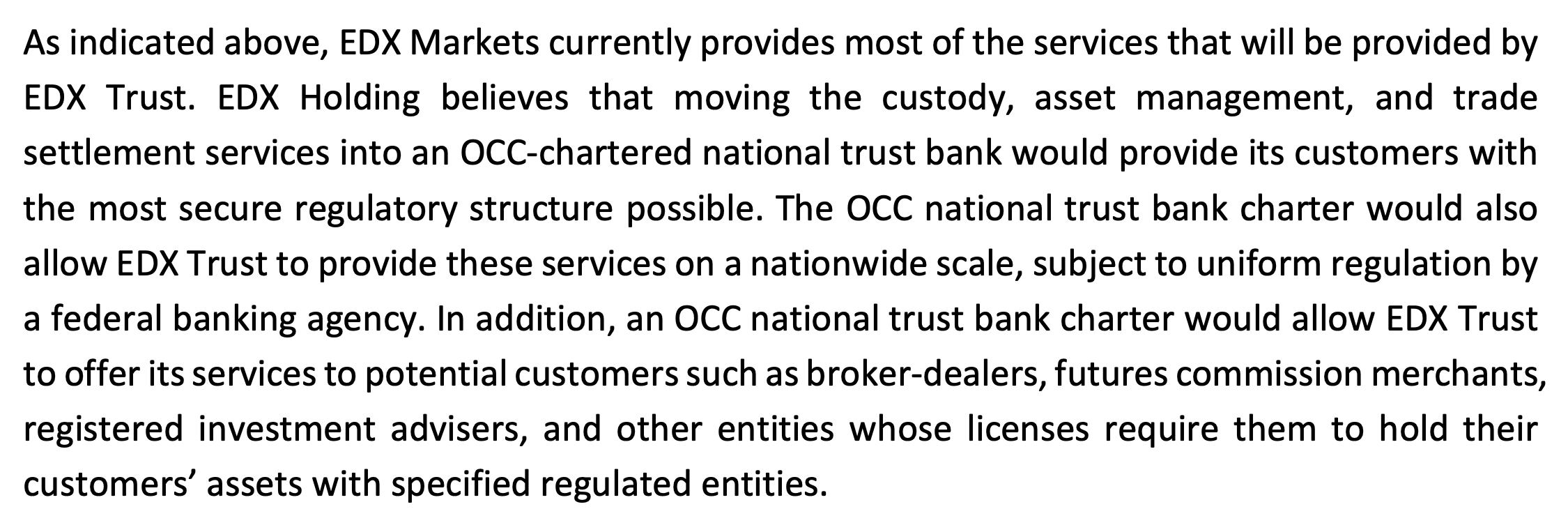

EDX Markets, an institutional crypto exchange, has applied to the US Office of the Comptroller of the Currency (OCC) to establish a national trust bank that would provide crypto custody, asset management and trade-settlement services.

The proposed entity, EDX Trust, would operate as a non-depository national bank, separating custody and settlement from trading while continuing to route order matching through EDX’s existing platform.

In its application, the company said the model is intended to address structural risks in crypto markets, where trading, custody and brokerage are often combined within a single platform, creating potential conflicts of interest and single points of failure.

EDX said the trust bank would provide fiduciary asset management services, invest client cash and stablecoin balances in highly liquid assets, and facilitate trading through a riskless principal model with end-of-day net settlement.

The bank would operate online from Chicago and target institutional clients such as broker-dealers, futures commission merchants and registered investment advisers, according to the filing.

EDX said moving these functions into an OCC-chartered entity would allow it to offer services nationwide under a single regulatory framework while meeting custody requirements for regulated institutions.

Founded in 2022, EDX Markets is backed by traditional market participants including Citadel Securities, Virtu Financial, Fidelity Digital Assets and Hudson River Trading.

Related: Fed’s Barr backs stablecoin clarity but warns of run risks

Crypto companies seek US bank charters

The application comes as crypto and financial companies increasingly pursue national trust bank charters to expand institutional services under federal oversight.

Earlier this month, Zerohash, a blockchain infrastructure company, applied for a US national trust bank charter to expand its stablecoin and custody services for banks, brokerages and fintechs.

Other recent applicants include Coinbase, which applied in October and is still awaiting a decision, as well as Laser Digital and Payoneer, which filed applications earlier this year to expand custody and stablecoin-related payment services.

Traditional financial institutions are also entering the space. In February, Morgan Stanley applied for a de novo trust bank charter to support digital asset services through a separate entity.

At the same time, the OCC has continued approving applicants, issuing conditional licenses last month to Bridge, Stripe and Crypto.com, following approvals in December for Ripple Labs, Circle Internet Group, Fidelity Digital Assets, Paxos and BitGo.

However, the pace of approvals has drawn scrutiny. In February, the American Bankers Association urged the OCC to slow the process, citing unresolved oversight under pending US stablecoin legislation.

Crypto World

Ripple Treasury Becomes First TMS to Offer Native Digital Asset Capabilities for Corporate CFOs

TLDR:

- Ripple Treasury is the first TMS to embed native digital asset capabilities directly into an enterprise platform.

- Digital Asset Accounts support XRP and RLUSD with 15-decimal precision and automated real-time transaction recording.

- Unified Treasury connects multiple custodians via ClearConnect, giving CFOs one real-time dashboard for all positions.

- Ripple’s 2026 survey found 72% of finance leaders say a digital asset solution is now needed to stay competitive.

Ripple Treasury has officially launched Digital Asset Accounts and Unified Treasury. The launch marks the first native digital asset capabilities embedded in an enterprise treasury management system.

CFOs and their teams can now view, hold, and manage both fiat and digital assets in one place. It follows Ripple’s 2025 acquisition of GTreasury, which brought over 40 years of enterprise treasury expertise. Multiple customers completed beta testing ahead of the April 1 global launch.

Digital Asset Accounts Integrate Onchain Balances Into Enterprise Treasury Workflows

Digital Asset Accounts allow treasury teams to create and manage a regulated digital asset account directly within the platform.

No external setup, third-party custody relationship, or separate system is required. XRP and Ripple USD (RLUSD) balances appear alongside cash accounts in real time.

The platform applies live fiat valuation, refreshed within seconds of each transaction. Exchange rates come from leading market data providers and update automatically.

The system also works across multiple data providers simultaneously, maintaining accuracy during volatile market conditions. Teams no longer need manual calculations or separate tools for valuation.

Transactions are recorded with 15-decimal precision, capturing onchain amounts exactly as they exist. This prevents rounding errors that typically cause reconciliation gaps.

An automated audit trail is generated for every transaction, supporting finance and control teams. Treasury managers maintain full control of records without relying on external reconciliation tools.

Each record captures the native notional amount, fiat equivalent, and market price at the moment of the event. This provides a complete, time-stamped transaction history without manual data entry. The automated recording process also supports compliance across multiple reporting frameworks.

Renaat Ver Eecke, SVP of Ripple Treasury, spoke on the shift in how CFOs now approach digital assets. “Digital assets have arrived at the CFO’s desk, and the question has shifted from whether to engage to how to do so advantageously without disrupting existing operations,” he said.

He added that the platform gives the office of the CFO a trusted place to hold and manage digital and fiat assets, with no separate interface or new workflows needed.

Unified Treasury Gives CFOs Real-Time Visibility Across All Liquidity Positions

Unified Treasury consolidates digital asset and cash positions into a single real-time dashboard. Teams holding assets across multiple custodians can connect providers through Ripple Treasury’s ClearConnect connectivity layer.

This layer is the same one already used for existing bank integrations within the platform. No new infrastructure or changes to current banking arrangements are required.

API connectivity to digital asset providers can be completed in minutes through the platform. Once connected, balances reflect automatically as transactions occur onchain.

Treasury teams no longer depend on manual imports or batch data processing to see positions. This also eliminates delays that have made digital asset reporting difficult for corporate finance teams.

Market rates are applied to digital asset balances in the reporting currency of each organization’s choice. No separate data sources or manual currency conversions are required.

The entire process runs automatically within the system, streamlining day-to-day operations. This gives treasury teams in different regions a consistent reporting experience.

Mark Johnson, VP of Global Product at Ripple Treasury, described the core design principle behind both capabilities. “The design principle behind both capabilities is that digital assets should behave exactly like cash within the platform,” he said.

Johnson further noted that treasury teams should not have to think about whether a balance is onchain or in a bank account. “They should simply see their position,” he added.

Ripple’s 2026 survey of 1,000+ global finance leaders found that 72% now consider a digital asset solution a competitive necessity.

Most, however, lack a starting point that fits within current workflows. Stablecoins processed $33 trillion in volume last year, rising 72% from 2024, showing strong demand already in the market.

Talks Church & “New Relationship” With God

RARE Quarter $ 22,000.00 Don’t Spend This Error Coin US Worth Money

Hawaiian Electric Industries (HE): Regulatory Relief Cannot Offset The Dilution Overhang

-

News Videos7 days ago

News Videos7 days agoParliament publishes latest register of MPs’ financial interests

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports1 day ago

Sports1 day agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Crypto World4 hours ago

Crypto World4 hours agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech2 days ago

Tech2 days agoEE TV is using AI to help you find something to watch

-

Tech2 days ago

Tech2 days agoApple will hide your email address from apps and websites, but not cops

-

Entertainment7 days ago

Entertainment7 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Tech2 days ago

Tech2 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech2 days ago

Tech2 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

You must be logged in to post a comment Login