Crypto World

Bitcoin trades like growth assets today, Gold tomorrow

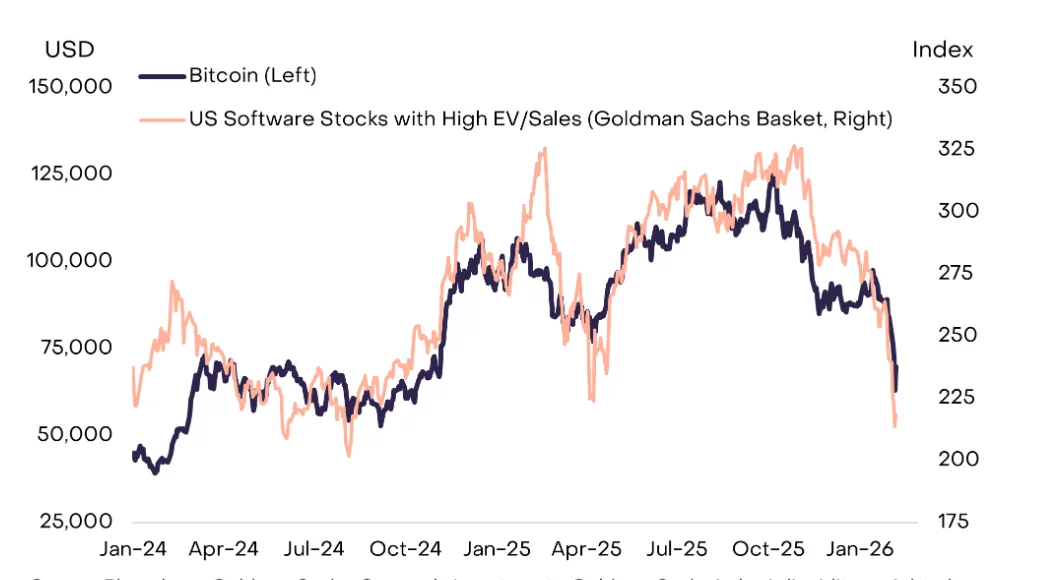

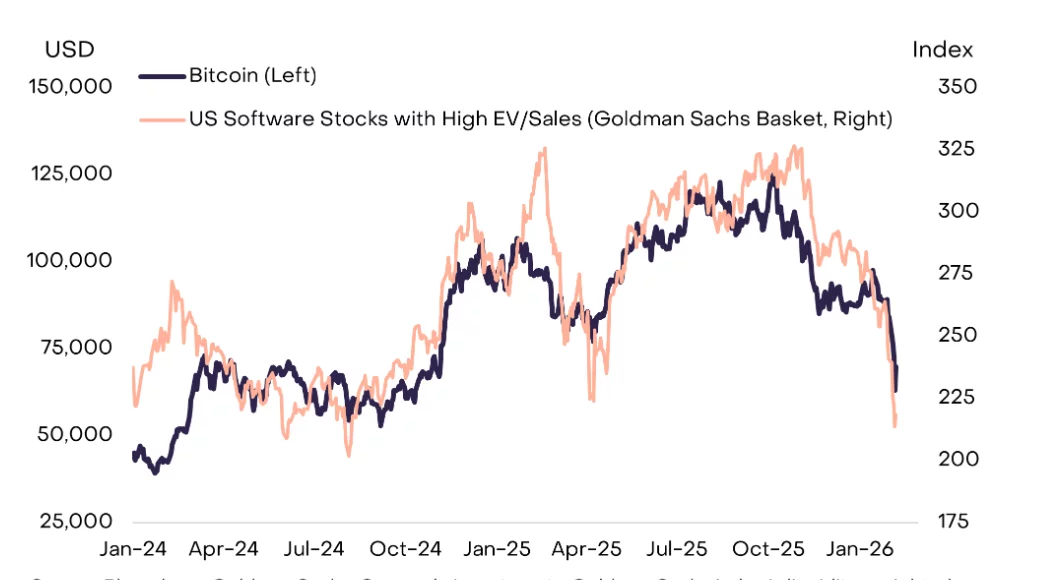

In its latest Market Byte research note, Grayscale Investments highlights a meaningful shift in Bitcoin’s price behavior. Recent BTC trading patterns resemble growth assets more closely than safe-haven commodities like gold, challenging the long-standing “digital gold” narrative.

Summary

- Bitcoin is trading more like a growth asset than gold, with recent price action closely tracking high-growth software stocks and broader risk assets, according to Grayscale.

- Near-term BTC moves are being driven by risk sentiment, not store-of-value demand, limiting its effectiveness as a hedge during equity market drawdowns.

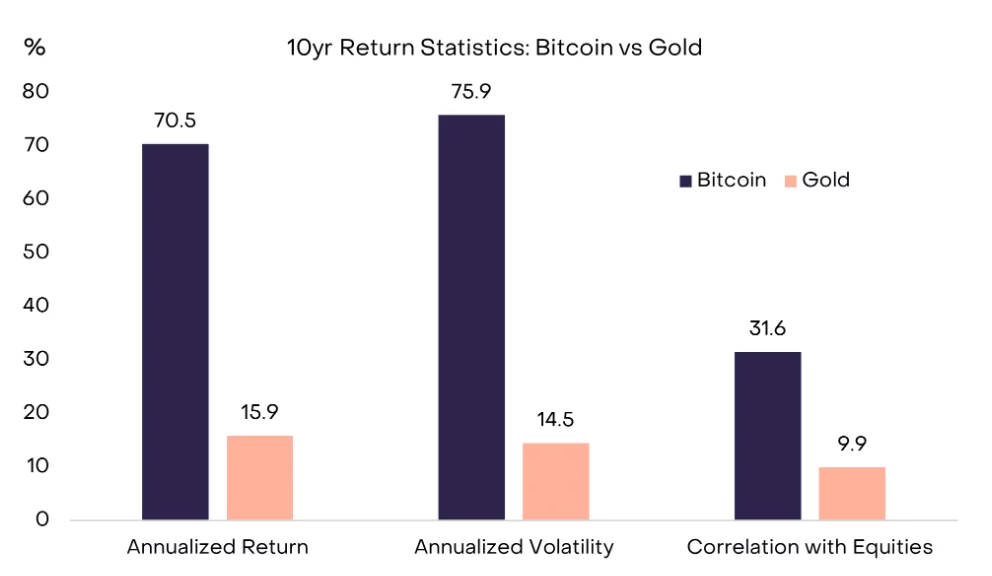

- Grayscale maintains a long-term bullish thesis, arguing Bitcoin could eventually evolve into a gold-like monetary asset with lower volatility and weaker equity correlations if adoption continues.

According to the report’s key takeaways, Bitcoin’s (BTC) sharp move lower in early February — where the price dipped to around $60,000 on February 5 before a modest bounce — was driven by correlation with broader risk assets rather than traditional store-of-value flows.

Grayscale’s research shows Bitcoin’s price movements have tracked high-growth software stocks closely, especially since early 2024, with both falling in sync during recent sell-offs.

This behavior ushows Bitcoin’s sensitivity to market sentiment and cyclical risk appetite, similar to technology or growth equity performance during sell-offs.

What this means for Bitcoin traders

For traders, this means treating BTC more like a beta-driven risk asset in the near term. Rather than acting as a hedge during turbulent markets, Bitcoin has recently declined alongside broader speculative assets and failed to demonstrate the safe-haven characteristics typically associated with gold.

This shift has practical implications for portfolio construction and risk management. Traditional strategies that lean on Bitcoin as a hedge against macro uncertainty or inflation may be less effective when BTC behaves in sync with growth asset risk cycles.

Grayscale stresses that Bitcoin has not yet achieved gold-like status as a monetary asset, and that gap is central to the investment thesis.

However, in a future economy shaped by AI agents, humanoid robots, and tokenized capital markets, the firm argues a digital, blockchain-based commodity like Bitcoin is better suited to become the dominant store of value than physical assets such as gold or silver.

Grayscale adds that if Bitcoin succeeds in this role over the long term, its return profile could eventually shift. Price behavior may begin to resemble gold rather than growth stocks, marked by lower volatility, weaker equity correlations, and more stable — though lower — expected returns.

EUR/USD is recovering losses from 1.1450. USD/JPY is correcting gains from 160.50 and might decline further below 158.00.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

· The Euro struggled to stay in a positive zone and declined below 1.1600 before finding support.

· There is a key bearish trend line forming with resistance at 1.1575 on the hourly chart of EUR/USD at FXOpen.

· USD/JPY rallied significantly before the bears appeared near 160.45.

· There is a major bearish trend line forming with resistance near 159.20 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh decline from 1.1640. The Euro declined below 1.1600 and 1.1520 against the US Dollar.

The pair even declined below 1.1500 and the 50-hour simple moving average. Finally, it tested the 1.1445 zone. A low was formed at 1.1443, and the pair is now recovering losses. There was a move above 1.1500 and the 50-hour simple moving average.

The pair surpassed the 50% Fib retracement level of the downward move from the 1.1639 swing high to the 1.1443 low. On the upside, the pair is now facing resistance near the 61.8% Fib retracement and 1.1575. There is also a key bearish trend line forming with resistance at 1.1575.

The first major hurdle for the bulls could be 1.1605. An upside break above 1.1605 could set the pace for another increase. In the stated case, the pair might rise toward 1.1640.

If not, the pair might drop again. Immediate support is near 1.1520. The next key area of interest might be 1.1480 or the 50-hour simple moving average. If there is a downside break below 1.1480, the pair could drop toward 1.1445. The main target for the bears on the EUR/USD chart could be 1.1400, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a steady decline from well above the 160.00 zone. The US Dollar gained bearish momentum below 159.50 against the Japanese Yen.

The pair even settled below 159.00 and the 50-hour simple moving average. A low was formed at 158.44, and the pair is now consolidating losses. On the downside, the first major support is near 158.45.

The next key region for the bulls might be 158.00. If there is a close below 158.00, the pair could decline steadily. In the stated case, the pair might drop toward 156.80. Any more losses might send the pair toward 155.00.

Immediate resistance on the USD/JPY chart is near the 23.6% Fib retracement level of the downward move from the 160.46 swing high to the 158.44 low at 158.90.

If there is a close above 158.90 and the hourly RSI moves above 50, the pair could rise toward 159.20. There is also a major bearish trend line forming with resistance near 159.20. The next major barrier for the bulls could be near the 50% Fib retracement level at 159.45, above which the pair could test 160.00 in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Wall Street asset management giant Franklin Templeton is launching a dedicated cryptocurrency division as it deepens its push into digital assets, anchored by a planned acquisition of crypto investment firm 250 Digital.

The new unit, called Franklin Crypto, will bring together the 250 Digital team and its liquid crypto strategies — previously managed by CoinFund — under one structure aimed at institutional investors, the firm said Wednesday.

Former CoinFund executive Christopher Perkins will lead the division, with Seth Ginns serving as chief investment officer alongside Franklin Templeton digital assets executive Tony Pecore. The group will report to Sandy Kaul, the firm’s head of innovation.

The move builds on Franklin Templeton’s existing digital asset business, which manages about $1.8 billion, and signals a shift toward offering more active crypto investment strategies alongside its current products.

“This is an exciting addition for Franklin Templeton,” CEO Jenny Johnson said, adding that the deal strengthens the firm’s ability to deliver dedicated crypto expertise to clients globally.

The launch of Franklin Crypto reflects a broader trend among large asset managers that are moving beyond passive exposure, such as exchange-traded funds, toward building in-house capabilities.

Perkins said the effort is aimed at meeting that demand. “Crypto’s institutional moment has arrived,” he said, pointing to growing interest from large investors seeking structured exposure to digital assets.

The transaction also includes an experimental element: part of the consideration will be paid using BENJI tokens, linked to Franklin Templeton’s on-chain U.S. Government Money Fund. The fund uses blockchain infrastructure to process transactions and record ownership.

That approach suggests early steps toward conducting mergers and acquisitions using tokenized assets, with settlement occurring more directly on blockchain rails.

The acquisition is expected to close in the second quarter of 2026, subject to approvals and other conditions. Financial terms were not disclosed.

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 1968.28, up 1.0% (+20.29) since yesterday’s close.

Eighteen of 20 assets is trading higher.

Leaders: AVAX (+4.0%) and HBAR (+3.6%).

Laggards: BCH (-2.1%) and BNB (+0.0%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

Bitcoin (BTC) closed March in green, ending the longest monthly losing streak since 2018. Data suggests that the coming months may prove to be profitable for BTC.

Key takeaways:

-

Bitcoin ended March 2% higher, marking the first green monthly close in six months.

-

A similar streak in 2018/2019 led to an over 316% BTC price rebound over five months.

-

Bitcoin price faces stiff resistance at $70,000-$72,000, where key trend lines converge.

Past multi-month downtrends were followed by 300% price gains

Historical price data from CoinGlass confirms Bitcoin printed its first green monthly candle in six months, closing March 2% higher after five straight months of losses.

“This is a massive dose of hopium,” analyst Ash Crypto said in an X post on Wednesday.

The analyst was referring to a possible shift in momentum, which might lead to a sustained recovery, as seen in previous cycles.

Related: Crypto Fear & Greed Index stuck on ‘extreme fear,’ but is there a silver lining?

The last time this happened was in 2018/2019 when BTC closed February 2019 in green, after six consecutive red months, as shown in the figure below.

This led to a reversal with over 300% returns the following five months, as Bitcoin recovered from the 2018 bear market.

“Last time BTC dumped 6 months in a row, it pumped the following 5 months in a row that came after!” trader Satoshi Flipper said in a Wednesday post on X.

If history repeats itself, the reversal may continue in April, suggesting that BTC price may have bottomed at $60,000.

Bitcoin’s bullish monthly close is a ”catalyst for fresh inflows into early April,” Trader Caleb said, adding:

“April starts with momentum.”

Bitcoin has a well-established tendency for significant price swings in April.

Since 2013, April has been a green month for eight of the past 13 years, with average returns of about 12.2%

However, Bitcoin also tends to move in the opposite direction to March in April, and this is true for nine out of the past 13 years.

In recent years, Bitcoin dropped in April after closing March in green, three out of four times between 2021 and 2024.

Therefore, while the end of past multi-month drawdowns suggests a rebound is due, data demonstrates that BTC price could also slide in April.

Watch these Bitcoin price levels next

Data from TradingView shows BTC price up 2.5% on the day to trade at $68,470 as the $69,000-$70,000 resistance remains in place.

Analysts expect Bitcoin’s range-bound price action to continue for longer, with important price levels to look for in case of a breakout.

These include the $70,000-$72,000 supply zone, coinciding with the 50-day simple moving average (SMA), the 50-day exponential moving average (EMA) and the 1w–1m cohort cost basis.

This is also where investors acquired approximately 650,000 BTC, marking a potential point of sell pressure, according to the cost-basis distribution data from Glassnode.

Breaking above this level could see BTC/USD revisit the $76,000 range high and eventually the $80,000 psychological level.

Zooming out, trader Sheldon Diedericks said Bitcoin could “push into resistance” at $83,000 on the monthly time frame, a key support level from April 2025. The 200-day EMA is also close to this area.

On the downside, the 200-week EMA at $68,300 and the 200-week SMA at $59,400 remain key levels to watch. Below that, the next major level is Bitcoin’s realized price around $54,000.

As Cointelegraph reported, Bitcoin’s bear market bottom could be formed once BTC price drops toward or below its realized price.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Crypto World

OpenAI Secures Historic $122B Investment Round, Reaching $852B Valuation with Amazon and Nvidia Support

Key Highlights

- OpenAI secured $122 billion in funding, achieving an $852 billion post-money valuation

- Major investors include Amazon, Nvidia, and SoftBank, with continued support from Microsoft

- The company reports $2 billion in monthly revenue and serves 900 million weekly active ChatGPT users

- Development underway for an integrated AI “superapp” merging ChatGPT, Codex, and web browsing capabilities

- Credit facility enhanced to $4.7 billion, remaining untapped at present

OpenAI has successfully completed a monumental $122 billion investment round, establishing a new benchmark as the largest private capital raise in corporate history. This extraordinary financing values the artificial intelligence leader at $852 billion following the transaction, positioning it as the highest-valued privately-held company globally.

The investment was spearheaded by technology and investment heavyweights Amazon, Nvidia, and SoftBank. Microsoft, a longstanding strategic partner, maintained its participation in this latest round. SoftBank shared co-leadership responsibilities with a16z, D.E. Shaw Ventures, MGX, TPG, and T. Rowe Price-advised accounts.

The comprehensive investor consortium features prominent names including BlackRock, Blackstone, Fidelity, Sequoia, Temasek, Coatue, ARK Invest, Thrive Capital, and Insight Partners, alongside numerous other institutional backers.

In an unprecedented move, OpenAI made this funding opportunity accessible to retail investors through banking partnerships, successfully securing over $3 billion from individual participants alone. Additionally, OpenAI will gain exposure through inclusion in multiple ARK Invest exchange-traded funds.

The company reports current monthly revenue of $2 billion. This represents substantial acceleration from the $1 billion quarterly run rate recorded at 2024’s conclusion, demonstrating remarkable revenue expansion in a compressed timeframe.

ChatGPT’s user base has surpassed 900 million weekly active participants, complemented by more than 50 million paid subscription accounts. OpenAI maintains that its platform receives six times the monthly web traffic compared to its closest AI application competitor.

Enterprise clients now contribute over 40% of total revenue streams. According to company projections, enterprise revenue is positioned to match consumer revenue contributions by the conclusion of 2026.

The company’s application programming interfaces handle over 15 billion tokens every minute. Codex, its specialized coding assistant, supports more than 2 million weekly users—a fivefold increase achieved within a mere three-month period.

Vision for an Integrated AI Superapp

OpenAI has announced ambitious plans to construct a comprehensive AI superapp platform that consolidates ChatGPT, Codex, web browsing functionality, and autonomous agent capabilities into a singular, cohesive product offering. This strategic initiative aims to simplify widespread adoption and utilization of its artificial intelligence models.

The organization emphasizes computational infrastructure as a critical strategic priority. Cloud computing partnerships span Microsoft, Oracle, AWS, CoreWeave, and Google Cloud. Semiconductor collaborations encompass Nvidia, AMD, AWS Trainium, Cerebras, alongside proprietary chip development in partnership with Broadcom.

Enhanced Credit Arrangements and Market Position

OpenAI has simultaneously expanded its revolving credit arrangement to approximately $4.7 billion. This facility receives backing from leading financial institutions including JPMorgan Chase, Citi, Goldman Sachs, Morgan Stanley, Wells Fargo, and additional major banks. Notably, the entire facility remains untapped as of March 31.

With an $852 billion valuation, OpenAI commands a worth approximately equivalent to Berkshire Hathaway. The company’s value surpasses the market capitalizations of major corporations including Visa, JPMorgan Chase, and Samsung.

OpenAI has recently introduced GPT-5.4 to the market. The company’s API infrastructure continues expanding, processing billions of tokens per minute across both enterprise and consumer deployment scenarios.

BNB is holding a critical psychological price threshold, trading at $614 after a 1.7% gain in 24 hours, and our prediction since last week is getting bullish. As a catalyst, Binance’s newly announced prediction market feature can add enough utility to the equation.

Binance confirmed Yesterday it is rolling out an integrated prediction market directly inside its self-custody wallet, partnering with third-party providers, including Predict.fun, to let users bet on politics, sports, and crypto events without leaving the app.

— BSCN (@BSCNews) March 31, 2026

JUST IN: BINANCE WALLET TO LAUNCH PREDICTION MARKET FEATURE

JUST IN: BINANCE WALLET TO LAUNCH PREDICTION MARKET FEATURE

Binance Wallet (@BinanceWallet) is introducing a new prediction market tool. The feature will allow users to bet on future outcomes. Categories include sports, economics, world events, and crypto.

Binance will not… pic.twitter.com/lmMV53hEyX

The feature may also tie into BNB Chain’s yield-generating staking mechanics, potentially creating new organic demand for the token. Regulatory guardrails around prediction markets remain in flux, which adds a layer of uncertainty, but institutional interest in the sector is clearly accelerating, with Coinbase and Crypto.com both expanding into similar territory in recent months.

Discover: The best pre-launch token sales

BNB Price Prediction: Can It Hit $660 This Week?

BNB is consolidating in a narrow band near its lower Bollinger Bands, with RSI sitting at a neutral-to-weak 41-43, showing convergence but not yet confirmation of a reversal.

Key support sits at $600 level, with a secondary floor at $580. On the upside, resistance clusters at $640, $660, and the upper Bollinger Band at $680.

For the price, prediction market utility drives fresh BNB demand; the price can reclaim the $649 SMA and test the $660–$680 resistance zone within days. But a break below $600 support opens the door to the $420 accumulation zone.

On-chain activity at roughly 1 million active addresses and consistent token burns provide a structural floor. Broader altcoin season dynamics will likely determine whether BNB’s next meaningful move is up or down from here. Watch this current level closely; it has held twice in 48 hours, but a third test rarely ends the same way.

Discover: The best crypto to diversify your portfolio with

Bitcoin Hyper Targets Early Mover Upside as BNB Tests Key Levels

BNB is offering a range-bound trade with meaningful upside capped at $680 in the near term. For traders who want asymmetric exposure during this uncertain window, early-stage infrastructure plays are drawing attention, particularly those targeting Bitcoin’s own scaling limitations.

Bitcoin macro conditions remain a dominant force across the entire market, and projects building directly on BTC infrastructure are positioned to capture that gravity.

Bitcoin Hyper ($HYPER) is positioning itself as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, combining Bitcoin’s security and trust with smart contract performance that exceeds Solana’s own throughput.

The presale has raised more than $32 million at a current token price of just $0.0136, with staking rewards live for early participants. Core features include a Decentralized Canonical Bridge for BTC transfers, sub-second finality, and low-cost transaction execution, targeting the exact bottlenecks (slow speeds, high fees, no programmability) that have historically kept institutional capital off Bitcoin’s base layer.

This article is for informational purposes only and does not constitute financial advice. Cryptocurrencies are highly volatile. Always do your own research before investing.

The post BNB Price Prediction: Can BNB Maintain Momentum With Its New Prediction Market? appeared first on Cryptonews.

The World Foundation sold $65 million in WLD tokens through over-the-counter block trades with four private counterparties at an average price of $0.2719 per token.

Opinion by: Alex Tsepaev, chief strategy officer at B2PRIME Group.

Each generation has its own distinct characteristics, even when it comes to investing. Younger people, for example, show a higher tolerance for risk. More than 64% of Gen Z and 49% of millennials say they are willing to take on more of it.

That appetite naturally includes investing in cryptocurrencies, which is considered one of the riskiest asset classes in modern markets. No surprise, then, that nearly two-thirds of Gen Zs plan to invest in cryptocurrencies like Bitcoin this year. Even more striking is that they are almost four times as likely to own crypto as to own a retirement account.

This might look like pure speculation. These numbers suggest that something more structural is happening.

For Gen Z, crypto is becoming an important part of their portfolios. The question now is whether that bet is mature or premature.

Volatility is the price of admission

Although it is arguable, crypto volatility remains one of the biggest obstacles in investing. Prices can change every millisecond, and trading happens around the clock. This has a significant effect on the final execution price.

The most interesting part here, however, is that Gen Z is fully aware of this. 84% of them acknowledged that cryptocurrencies are risky and volatile, yet continue investing, and participation continues to grow every year. Why?

Gen Z understands that digital assets are a great way to have extra, above-average profits, and volatility is perceived as an entry price. For a generation that has already witnessed two of the biggest economic crises in history, average capital growth in traditional investments can feel too slow or insufficient.

Digital assets also feel native to Gen Z. This is the first generation that has never known a life without the internet, and they are also used to digital wallets and online transactions.

At the same time, their investment behavior is shaped by social media consumption — one in four American Gen Z now gets financial advice from TikTok. Considering that the internet is flooded with so-called “finfluencers,” who help you learnn more about crypto, no surprise that Zoomers tend to invest in it so much.

FOMO and the narrative trap

Beyond risk tolerance, there is another thing that distinguishes Gen Z from previous generations.

It is the fear of missing out (FOMO). This feeling, mostly expressed as the fear of lost profits, is expressed in constant anxiety due to comparing lives with the “perfect” picture on social networks.

FOMO is especially common among Zoomers when it comes to financial matters. In fact, nearly 70% of Gen Z says they feel financial FOMO while scrolling social media. And 50% of Gen Z investors said they have even made an investment driven by this feeling, most often in crypto, in particular, memecoins.

Related: Australia warns of AI, ‘finfluencers’ as Gen Z crypto ownership reaches 23%

Memecoins thrive in this environment. By design, they are made for virality and great coverage in the media and news. The issue is not that they are built on hype, but that they are made to catch the moment and disappear, in most cases. Every memecoin cycle, where it goes up and quickly falls down, strengthens the argument that digital assets are unsafe.

This creates a narrative duality. On one side, crypto is maturing, and institutionals flow in. On the other hand, the industry is still very FOMO-fueled, and this dominates the headlines. And as a result, the loudest crypto stories become more about speculative gains.

Risks that Gen Z underestimate

When Gen Z increasingly invests in crypto, many may be doing so without fully researching the risks. Sometimes they blindly trust TikTok advice without doing their due diligence or reaching out to a financial advisor.

Zoomers mostly feel confident in their decisions. More than 70% of Gen Z saying they are completely sure about their investing behavior. Confidence, however, and especially in crypto, does not mean competence. Younger generations are reportedly more susceptible to the Dunning-Kruger effect. They usually overestimate their knowledge and underestimate risks.

Beyond volatility as a primary risk, Gen Z often neglects the absence of transparency in crypto. Unlike public companies, digital assets have no reporting requirements. A “Wild West” like this, and lack of long-reaching regulation does not bother young crypto enthusiasts. On the contrary, they still trust crypto. They value transparency and direct control a lot. In fact, they should pay more attention to regulation. As it develops, it helps to protect investor rights and turn crypto into a more transparent and trustworthy market.

Investors can also forget that diversification does not simply mean putting 10-20% of your portfolio in crypto. There is the issue of correlation. During periods of systemic stress, crypto has at times moved in line with high-growth equities, weakening its diversification argument. Graphs show that Bitcoin can even correlate with gold, a traditional safe-haven asset.

Or imagine they, for example, choose the wrong coin that is going to fall and put in at least 25%. Without understanding how digital assets work, they risk losing a fourth of their investments.

Still, none of these risks devalues crypto’s role in modern portfolios. On the contrary, crypto might indeed be evolving into a genuine portfolio diversifier.

If that transformation is real, it comes with strings attached.

Opinion by: Alex Tsepaev, chief strategy officer at B2PRIME Group.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

Introduction

Decentralized finance has unlocked something traditional finance never could: permissionless income generation. No bank approvals, no gatekeepers — just you, your capital, and smart contracts.

But there’s a problem.

Most beginners enter yield farming the same way:

They see 100%+ APY, ape in… and learn about risk the expensive way.

This guide fixes that.

Instead of throwing random strategies at you, we’ll walk through a step-by-step “Yield Farming Ladder” — a structured path from beginner to advanced, designed to help you earn sustainably while understanding the risks.

Why Most Beginners Lose Money in Yield Farming

Before we talk profits, let’s talk reality.

Most beginners lose money because they:

- Chase high APYs without understanding the source

- Ignore risks like impermanent loss

- Trust unaudited or hype-driven protocols

- Overcommit capital too early

Here’s the uncomfortable truth:

High yield isn’t free money — it’s risk in disguise.

If you don’t know where the yield comes from, you are the yield.

Level 1: Training Wheels — Stablecoin Lending

Best for: Absolute beginners

Risk level: Low

Typical returns: 3–8% APY

This is where you start.

You deposit stablecoins (like USDC or USDT) into lending protocols, and borrowers pay interest to use your funds.

Why this works for beginners:

- No exposure to price volatility

- No impermanent loss

- Simple mechanics

What you’re learning:

- How DeFi protocols work

- How yield is generated (real demand vs incentives)

Think of this as your DeFi savings account — except it actually pays.

Level 2: Liquidity Pools — Where Real Yield Begins

Best for: Beginners ready to level up

Risk level: Medium

Typical returns: 5–20% APY

Now you step into liquidity provision (LP).

You deposit token pairs into decentralized exchanges, and earn:

- Trading fees

- Incentives (sometimes)

Example:

Provide ETH + USDC → earn fees every time someone trades that pair.

New concept unlocked: Impermanent Loss

This is the “gotcha.”

If token prices move unevenly, you might earn fees… but still lose compared to holding.

Simple analogy:

You’re running a currency exchange booth. If exchange rates swing wildly, your inventory value changes too.

What you’re learning:

- Market exposure

- Fee-based yield vs incentive-based yield

Level 3: Yield Optimization — Work Smarter

Best for: Intermediate users

Risk level: Medium

Typical returns: Variable (often higher due to compounding)

At this stage, you stop doing everything manually.

You use yield aggregators that:

- Automatically reinvest your rewards

- Optimize across pools

- Save time and gas fees

Why this matters:

Manual farming is like watering plants one by one.

Aggregators?

They install an irrigation system.

What you’re learning:

- Capital efficiency

- Compounding strategies

- Protocol diversification

Level 4: Advanced Strategies — The Danger Zone

Best for: Experienced users only

Risk level: High

Typical returns: 20%–100%+ (with serious risk)

This is where things get spicy — and risky.

Strategies include:

- Leveraged yield farming

- Farming new/high-incentive protocols

- Looping (borrow → farm → repeat)

The trade-off:

Higher returns = higher chance of:

- Liquidation

- Smart contract exploits

- Total loss

Let’s be blunt:

This is where people either multiply their capital… or become a Twitter warning thread.

Proceed with caution.

The Risks You Cannot Ignore

If you skip this section, you’re basically speedrunning losses.

1. Smart Contract Risk

Bugs or exploits can drain funds instantly.

2. Impermanent Loss

LPs can underperform simple holding.

3. Protocol Risk

Not all platforms are audited or trustworthy.

4. Market Volatility

Crypto moves fast. Your yields can vanish just as quickly.

5. Overexposure

Putting everything into one strategy = one point of failure.

The Perfect Beginner Yield Farming Path

Here’s the roadmap that actually works:

Step-by-step progression:

- Start with stablecoin lending

- Move into ETH or major asset exposure

- Try stable liquidity pools

- Explore volatile LPs

- Experiment (carefully) with advanced strategies

The key principle:

Start simple. Scale with understanding — not hype.

Example: A Beginner-Friendly $1,000 Yield Portfolio

Let’s make this practical.

Sample allocation:

- $500 (50%) → Stablecoin lending

- $300 (30%) → Stable LPs

- $200 (20%) → Experimental strategies

Why this works:

- The majority of low-risk yield

- Some exposure to higher returns

- Limited downside if experiments fail

This isn’t about maximizing gains.

It’s about staying in the game long enough to learn.

Final Thoughts

Yield farming isn’t a shortcut to wealth.

It’s a system — one that rewards:

- Patience

- Understanding

- Risk management

The real edge isn’t finding the highest APY.

It’s knowing:

- Which yields are sustainable

- Which risks are worth taking

- When to scale… and when to step back

Because in DeFi, survival is the strategy.

And once you survive long enough?

That’s when the real compounding begins.

REQUEST AN ARTICLE

- Solana (SOL) price consolidates near $80 support amid strong fundamentals.

- Institutional staking and brokerage access boost Solana adoption.

- Key resistance at $87.65, and a breakout could target $97–$107.

Solana’s native token, SOL, has been showing signs of consolidation as it struggles to break through key resistance levels.

Despite a slight bounce today, the price remains confined below the $88 range.

At the same time, traders should closely monitor the altcoin which is currently hovering near the critical support at around $80, which has acted as a short-term floor for buyers.

On the surface, Solana’s technical structure appears cautious, with short-term momentum indicators showing weak buying pressure, but underneath this, Solana’s ecosystem is growing at a remarkable pace.

Solana’s fundamental strength fuels long-term confidence

One of the most compelling aspects of Solana’s recent performance is the surge in institutional and real-world adoption.

The network now hosts more than $2 billion in tokenized real-world assets according to rwa.xyz.

This milestone underscores Solana’s role not just as a blockchain for decentralized applications, but as a platform capable of handling complex financial instruments.

Institutional interest has also taken a significant step forward.

Staking products offering competitive yields have been launched, allowing both retail and institutional investors to earn returns on their SOL holdings.

These developments provide additional utility and financial incentives for participants, reinforcing Solana’s position as more than a speculative asset.

Adding to this, several traditional brokerage platforms including Galaxy now offer custody and trading services for SOL.

This integration reduces barriers for institutional investors and opens the door for mainstream adoption.

With access to regulated platforms, capital inflows could increase steadily, strengthening the network’s financial layer and liquidity.

On-chain activity remains robust as well, and the blockchain continues to see high transaction throughput, and its dominance in tokenized equity markets demonstrates that adoption is moving beyond hype-driven speculation.

Taken together, these factors highlight a token with real-world utility and strong growth potential.

Technical resistance holds back SOL’s price

Short-term market sentiment remains cautious, with recent outflows from Solana-focused ETFs reflecting institutional hesitancy despite the network’s improvements.

While the fundamentals are building, the price is still confined by technical hurdles.

SOL has found immediate resistance near $87.65, with historical data suggesting further caps at $97.56 and $106.95.

On the downside, the support zone at $75.85–$80.00 is critical for near-term stability.

A daily close below these zones could trigger a sharper decline toward $63.72, which has historically acted as a longer-term support.

Solana price outlook

Overall, Solana (SOL) is at a pivotal point where its fundamentals are strong, but the market has yet to fully recognize them.

Price action will likely depend on whether buyers defend support and whether institutional capital begins flowing into the network.

In the short term, traders should closely watch the near-term support zone between $80 and $77.32, since holding this level is crucial to prevent further selling pressure.

In case of a rebound, the immediate resistance is at $87.65, which if cleared could open the door to a rally towards higher targets at $97.56 and $106.95.

Mohsin Naqvi-Led Pakistan Cricket Board Blasted By Younis Khan After 20 Million Rupees Fine On Naseem Shah

Claude Code leak exposes how Anthropic’s AI really works

Learning the value of money | financial literacy | Ubongo Kids #financialeducationforkids

-

News Videos7 days ago

News Videos7 days agoParliament publishes latest register of MPs’ financial interests

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World1 day ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports21 hours ago

Sports21 hours agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Fashion7 days ago

Fashion7 days agoHow to Style Spring Like WeWoreWhat: Easy Outfit Ideas for 2026

-

Tech2 days ago

Tech2 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Entertainment6 days ago

Entertainment6 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Tech1 day ago

Tech1 day agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Sports2 days ago

Sports2 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech1 day ago

Tech1 day agoFlipsnack and the shift toward motion-first business content with living visuals

You must be logged in to post a comment Login