Crypto World

Canton Crypto Network vs. XRP: Breaking Down DTCC’s Infrastructure and Liquidity Needs

A heated debate has erupted over whether Canton Network is quietly positioning itself to replace XRP as the likely onboarder of institutions into crypto technology.

The DTCC processes quadrillions in value annually, and the market is suddenly debating the repercussions of its decision to pivot into real world asset (RWA) tokenization with the help of Canton.

This binary view is flawed. Canton Network builds the private rails for compliance, while XRP provides the liquidity that moves between them.

Key Takeaways

- The Infrastructure: Canton Network is designed for the privacy-preserving Tokenization of real-world assets like U.S. Treasuries, ensuring regulatory compliance on a private ledger.

- The Role: XRP functions as a neutral bridge asset for cross-border liquidity, solving the pre-funding problem rather than the custody problem.

- The Signal: Atomic Settlement on Canton complements the liquidity corridors of the XRP Ledger—they are distinct layers in the Institutional Crypto stack.

Canton Network: The Private Crypto Ledger for Atomic Settlement

The Canton Network, launched in 2023 by enterprise blockchain firm Digital Asset, is not a consumer-facing payment rail.

It is a network of networks designed specifically for regulated financial institutions looking to leverage blockchain while requiring absolute privacy.

Its primary engine is the Daml smart contract language, which allows financial institutions to synchronize data across disparate private blockchains without exposing sensitive trade details to the public.

Canton’s core utility is the Tokenization of real-world assets (RWAs). In pilots involving major players like Goldman Sachs and BNY Mellon, Canton demonstrated the ability to execute atomic settlement, swapping tokenized U.S. Treasuries for cash equivalents simultaneously.

This eliminates settlement risk and manages collateral mobility with a precision that legacy systems cannot match.

That matters because institutions cannot operate on fully transparent public ledgers.

Canton acts as a global synchronizer for these records. Unlike XRP, it does not predominantly seek to be a universal bridge currency; it seeks to be the verified vault where the assets live.

Discover: The next crypto to explode

XRP: The Crypto-Native Liquidity Bridge Canton Cannot Be

While Canton secures the asset, XRP moves the value. The XRP Ledger (XRPL) was designed with a specific friction point in global finance in mind: the dormant capital trapped in pre-funded nostro/vostro accounts. XRP acts as a neutral bridge asset, allowing a bank to swap fiat currencies in seconds without holding reserves in every target market.

The misconception that Canton replaces XRP ignores the difference between settlement logic and liquidity provision.

A private ledger can record a change in ownership instantaneously, but it does not inherently provide the deep, neutral market liquidity required to bridge volatile fiat currencies globally.

Ripple has deployed billions to cement XRP’s role as this connector between the banking world and the crypto economy.

For the DTCC, utilizing Canton for ledger synchronization does not negate the need for a mechanism to move value into and out of those synchronized ledgers efficiently. XRP operates on the liquidity layer, distinct from the asset custody layer that Canton occupies.

Two Layers, One Ecosystem: Why the Replacement Narrative Is Wrong

Essentially, Canton Network functions as the digital notary; XRP functions as the armored transport.

If Canton handles the atomic settlement of a tokenized Treasury bill within a permissioned U.S. network, XRP remains the most efficient tool for a foreign entity to source the USD liquidity needed to buy that bill.

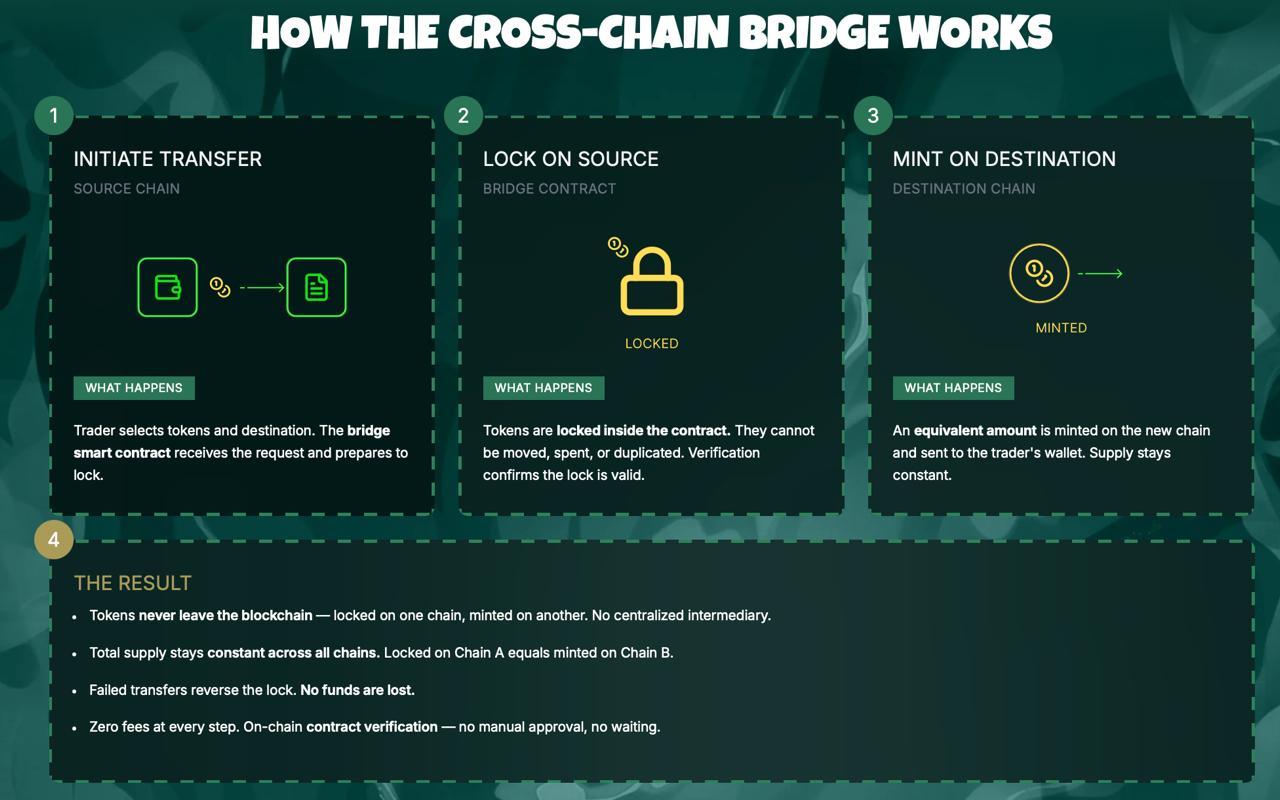

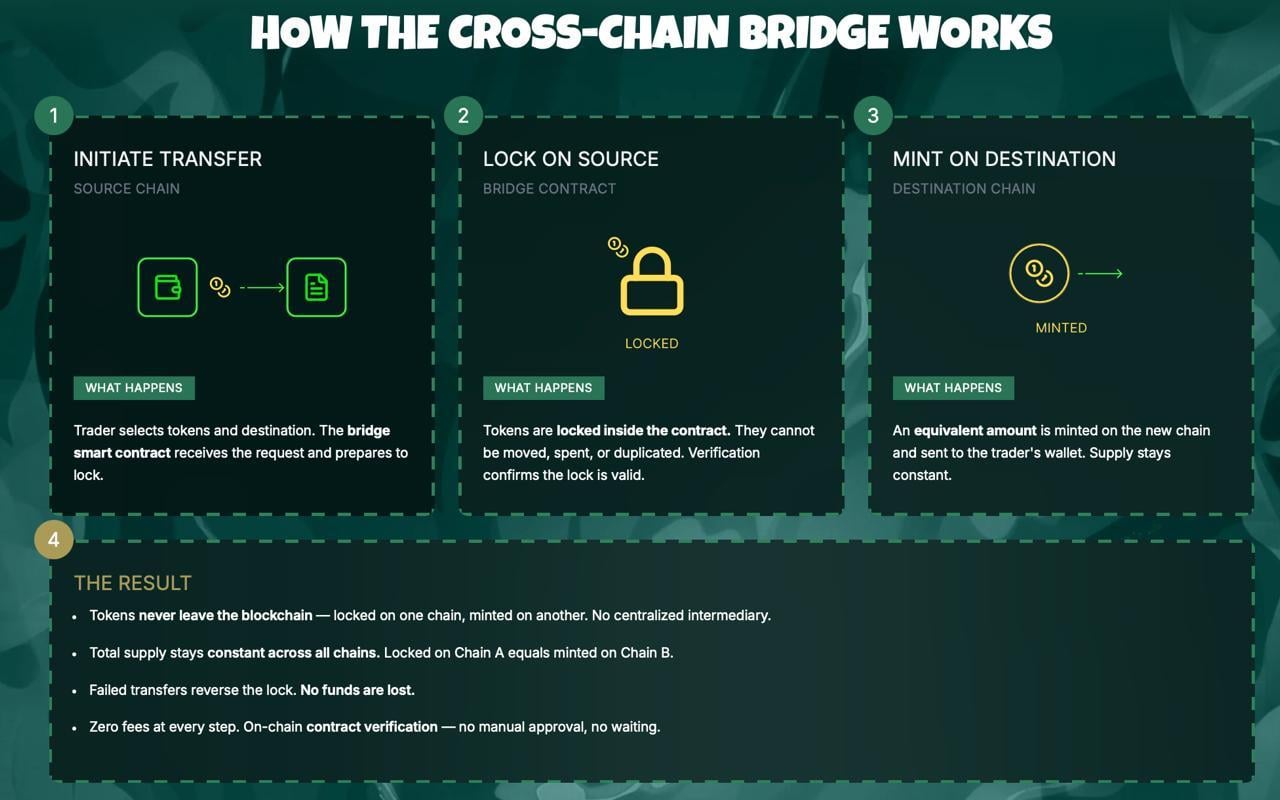

This mirrors the challenge discussed by LiquidChain regarding cross-chain liquidity: distinct ledgers need a neutral connector to function efficiently at scale. Without a bridge asset, liquidity remains fragmented across private chains.

In conclusion, as with many debates in crypto, it’s rarely ever a case of backing the stronger horse when both horses excel at totally different things.

Discover: The best crypto to buy now

The post Canton Crypto Network vs. XRP: Breaking Down DTCC’s Infrastructure and Liquidity Needs appeared first on Cryptonews.

A federal judge in Arizona has temporarily barred state officials from enforcing gambling laws against Kalshi, siding with the CFTC.

A federal judge in Arizona has temporarily barred state officials from enforcing gambling laws against Kalshi, siding with US regulators in a growing dispute over how event-based trading products should be classified.

In an order issued on Friday, Judge Michael Liburdi of the US District Court for the District of Arizona granted a request from the Commodity Futures Trading Commission (CFTC) and the federal government to halt any state-level action targeting contracts listed on CFTC-regulated markets .

The ruling centers on whether Kalshi’s “event contracts” fall under federal derivatives law or state gambling statutes. Last month, Arizona authorities sought to pursue enforcement against Kalshi under local gambling rules, but the CFTC asked a court order on Wednesday to stop the action.

The court said that the CFTC is likely to succeed in arguing that such contracts qualify as “swaps” under the Commodity Exchange Act, placing them within federal jurisdiction. The law grants the agency exclusive authority over swaps traded on designated contract markets.

Related: Prediction market users await Artemis II mission splashdown

Court halts Arizona enforcement against Kalshi

As part of the decision, Arizona officials are temporarily prohibited from initiating or continuing civil or criminal enforcement tied to Kalshi’s event contracts on regulated exchanges .

The restraining order will remain in effect until April 24, while the court considers whether to issue a longer-term preliminary injunction.

The case adds to a broader debate over prediction markets in the United States, particularly as regulators and states clash over whether such products resemble financial instruments or online betting. Last month, Utah lawmakers also passed a bill targeting Kalshi and Polymarket that classifies proposition-style bets on in-game events as gambling, aiming to block such offerings in the state.

Related: US appeals court upholds preventing New Jersey enforcement against Kalshi

Nevada judge extends ban on Kalshi

Last week, a Nevada judge extended a ban preventing Kalshi from offering event-based contracts in the state, siding with regulators who argue the products amount to unlicensed gambling.

The court found that the platform’s offerings closely resemble traditional sports betting. The judge said there is no meaningful distinction between placing a wager through a sportsbook and buying a contract tied to an event outcome, concluding that such activity falls under Nevada’s gaming laws.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

World, a cryptocurrency project founded by OpenAI CEO Sam Altman, announced a significant reduction to the Worldcoin (WLD) daily token unlock rate starting July 24.

The change affects community, team, and investor allocations at different rates. It comes as WLD faces continued market headwinds, having hit a new all-time low earlier this month.

Worldcoin (WLD) Token Unlock Rate To Drop By 43% in July 2026

According to the announcement, the daily unlock rate will fall by 43% on July 24. The largest reduction affects the World Community allocation.

That rate will be cut in half, dropping from 3.2 million WLD per day to 1.6 million. Tools for Humanity (TFH) Investor and Team token unlocks will also decline by 32%, falling from 1.9 million WLD per day to 1.3 million.

In total, daily emissions will fall from roughly 5.1 million WLD to 2.9 million. As of April 10, 4.9 billion WLD tokens are unlocked, representing 49% of the 10 billion total supply. Of this, 3.3 billion are actively circulating.

“In July 2024, a majority of the Team and Investor tokens were made subject to additional extended lock-ups, while remaining on a daily unlock schedule. Importantly, there are no unlock cliffs. A live unlock schedule of all WLD tokens is available on Dune. As a result of these lock-up schedules, on July 24, 2026, the unlock rate for all token allocations will automatically decrease,” the team noted.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

Sell Pressure Meets Structural Headwinds

The announcement arrives weeks after the World Foundation completed a $65 million over-the-counter token sale at roughly $0.27 per WLD.

WLD has lost over 45% of its value since the start of 2026 and trades roughly 97% below its March 2024 peak near $11. At press time, WLD traded at around $0.28, up 4.7% with the broader market.

Follow us on X to get the latest news as it happens

Whether the reduced unlocks will meaningfully ease selling pressure remains to be seen. While the lower emission rate could offer some short-term relief, any meaningful recovery will likely depend on a broader return in risk appetite and improved market conditions.

Until then, WLD’s ongoing downtrend and weak sentiment may continue to weigh on price action, limiting the near-term impact of the reduced token unlocks.

The post Worldcoin Slashes Token Unlocks by Nearly Half, Will It Impact Price? appeared first on BeInCrypto.

Bitwise Asset Management has taken another step toward launching its proposed spot Hyperliquid exchange-traded fund, filing a second amendment with the U.S. Securities and Exchange Commission that specifies the fund’s ticker BHYP and a management fee of 0.67%.

In a post on X, Bloomberg senior ETF analyst Eric Balchunas noted that such filings typically signal that the product is nearing the start of trading, and he highlighted that HYPE has surged over the past year, suggesting Bitwise is “trying to strike” while demand remains strong.

The filing arrives as asset managers press to launch the first spot ETF tied to a crypto perpetual futures protocol and blockchain, a race that also includes Grayscale and 21Shares pursuing similar Hyperliquid products. Bitwise was the first to submit a Hyperliquid ETF filing with the SEC in September, followed by 21Shares a month later and then Grayscale in late March. For context, see prior coverage of those filings here: Bitwise, 21Shares, Grayscale.

If approved, Bitwise’s ETF would trade on the NYSE Arca and provide investors with exposure to the spot price of Hyperliquid. In the December amendment, Bitwise also signaled that the fund would seek to generate additional returns from HYPE staking—a feature not explicitly indicated by Grayscale or 21Shares in their respective filings.

Key takeaways

- Bitwise updates its Hyperliquid ETF to include the BHYP ticker and a 0.67% management fee, signaling a potential near-term launch.

- The Hyperliquid ETF race features Grayscale and 21Shares alongside Bitwise, with Bitwise leading off in September, then 21Shares, then Grayscale.

- If approved, the fund would list on NYSE Arca and track the spot price of Hyperliquid; Bitwise’s staking plan for HYPE marks a notable differentiator.

- Hyperliquid’s native token has shown strong momentum, up about 65% in 2026 to around $41.96 and roughly 182% over the past year, according to CoinGecko.

- CoinGlass data placed Hyperliquid among the top 10 crypto derivatives venues by early April, with Q1 volume at $492.7 billion, trailing Coinbase by about $90 billion in that period.

Regulatory filings and industry momentum

The SEC filings underpin a larger wave of interest in traditional-market vehicles tied to crypto assets. Bitwise’s newest amendment clarifies that BHYP would trade on the NYSE Arca, a critical step toward a potential listing date, should regulators sign off. The December amendment’s staking provision adds a yield-centric angle to the vehicle, positioning the fund as not just a spot exposure tool but also a potential source of staking-driven returns.

Industry coverage traces a clear sequence: Bitwise kicked off the Hyperliquid ETF filings, followed by 21Shares and then Grayscale, each seeking to map the same “spot” exposure to a crypto-derivative ecosystem. This cadence illustrates how sponsors are racing to set precedent in a space where the SEC’s acceptance could unlock broader retail access to crypto-derivative concepts via traditional exchanges.

HYPE’s market trajectory matters beyond token price. A rising price path can attract more investor attention to an ETF that promises direct exposure to the spot market, while staking features introduce a structural difference from peers. The SEC’s eventual decision on these filings remains the central pivot—readers should watch for any updates on the regulators’ stance, timing, and any evolving disclosures from the sponsors.

Market momentum and what it could mean for investors

Hyperliquid’s token, HYPE, has been one of the more notable performers in the crypto space this year. CoinGecko data shows the token gaining roughly 65% since the start of 2026, trading near $41.96 at the time of writing, with a 12-month gain around 182%. While price strength alone does not guarantee ETF success, it contributes to a more compelling case for a spot product that could offer daily settlement and transparent price discovery on a major U.S. exchange.

On the broader derivatives front, CoinGlass reported in early April that Hyperliquid had breached the top-10 derivatives platforms by trading volume, joining heavyweights such as Binance, OKX and Bybit. In the first quarter, the platform processed $492.7 billion in trading volume, trailing Coinbase by roughly $90 billion for the period. These metrics help explain why sponsors are eager to offer a regulated, easy-on-ramp vehicle that could capture a share of ongoing derivatives activity in a compliant wrapper.

The convergence of rising token momentum, active trader interest in derivatives, and the prospect of a U.S.-listed spot ETF creates a nuanced backdrop for Bitwise, Grayscale and 21Shares. The industry is watching not only the SEC’s decision window but also how each sponsor positions the product—whether through staking yield, fee structure, or the depth of liquidity provision at launch.

Bitwise’s historical filings provide additional context: the initial Hyperliquid filing in September started the clock on the race to be first with a spot ETF in this niche. For those tracking the progression, see the prior Cointelegraph coverage linked here: Bitwise filing, 21Shares filing, Grayscale filing.

As the regulatory clock advances, the next milestones—SEC comments, potential approvals, and the final listing date on NYSE Arca—will be critical to gauge how quickly a spot Hyperliquid ETF could debut and what its early liquidity profile might look like.

Readers should watch for updates on the SEC’s review timeline and any refinements in the funds’ disclosures, especially around staking mechanics and yield expectations, which could influence initial demand and arbitrage dynamics once trading begins.

Bitwise’s push, joined by Grayscale and 21Shares, signals a broader push toward regulated crypto-access points that mix spot exposure with product-level incentives. Whether this wave translates into a meaningful market shift or remains a closely watched development will depend on regulatory clarity and the real-world performance of the underlying Hyperliquid ecosystem.

For now, the market is digesting the latest filing details, while investors weigh the potential of a first-mover advantage in an increasingly crowded field of crypto ETFs. The next few regulatory disclosures and any impending launch news will be the key signals to watch in the coming weeks and months.

What’s next: The SEC’s formal review timeline, any additional disclosures from Bitwise and peers, and the evolving liquidity picture on launch will determine how soon investors can actually access a spot exposure to Hyperliquid via an exchange-traded product.

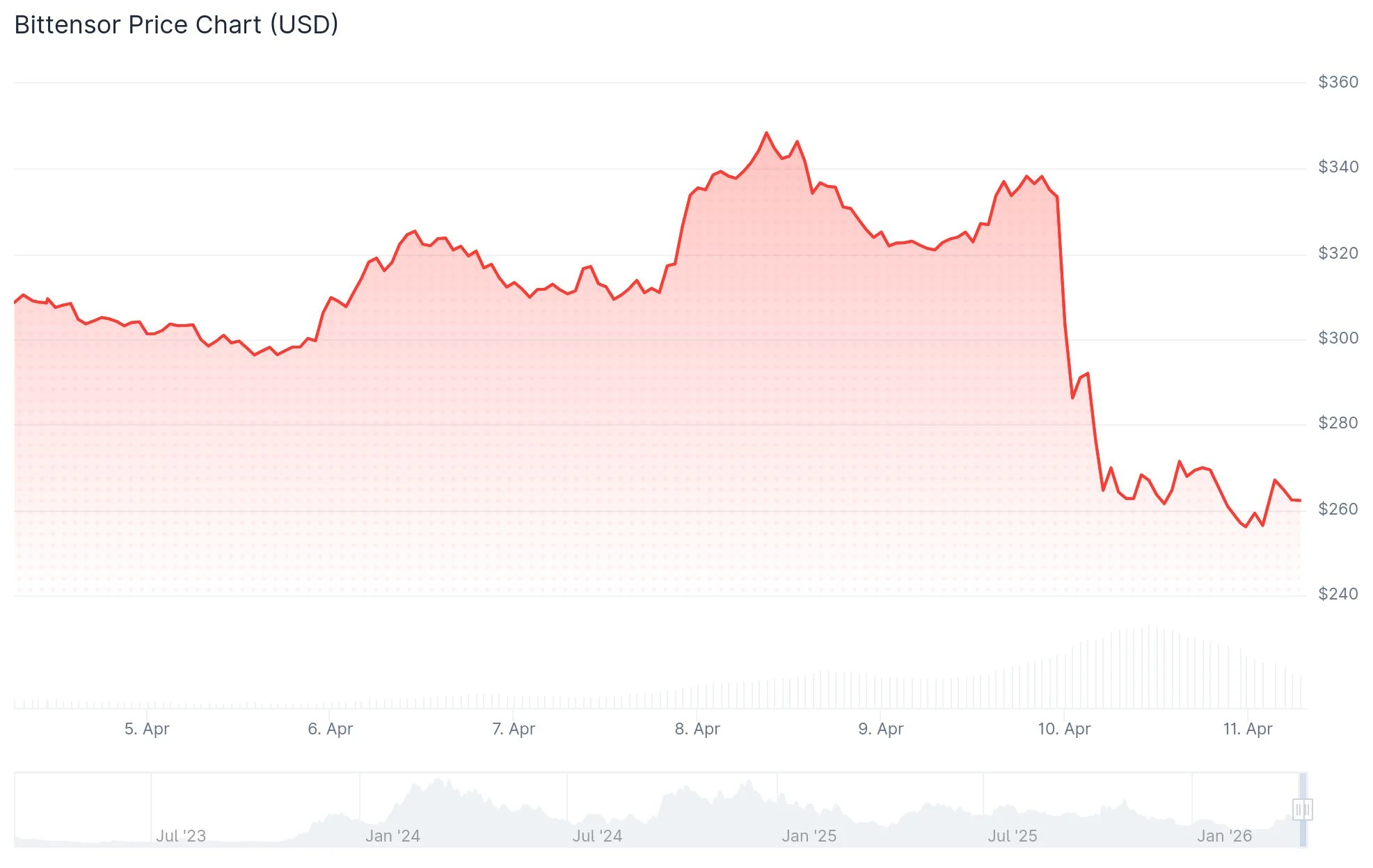

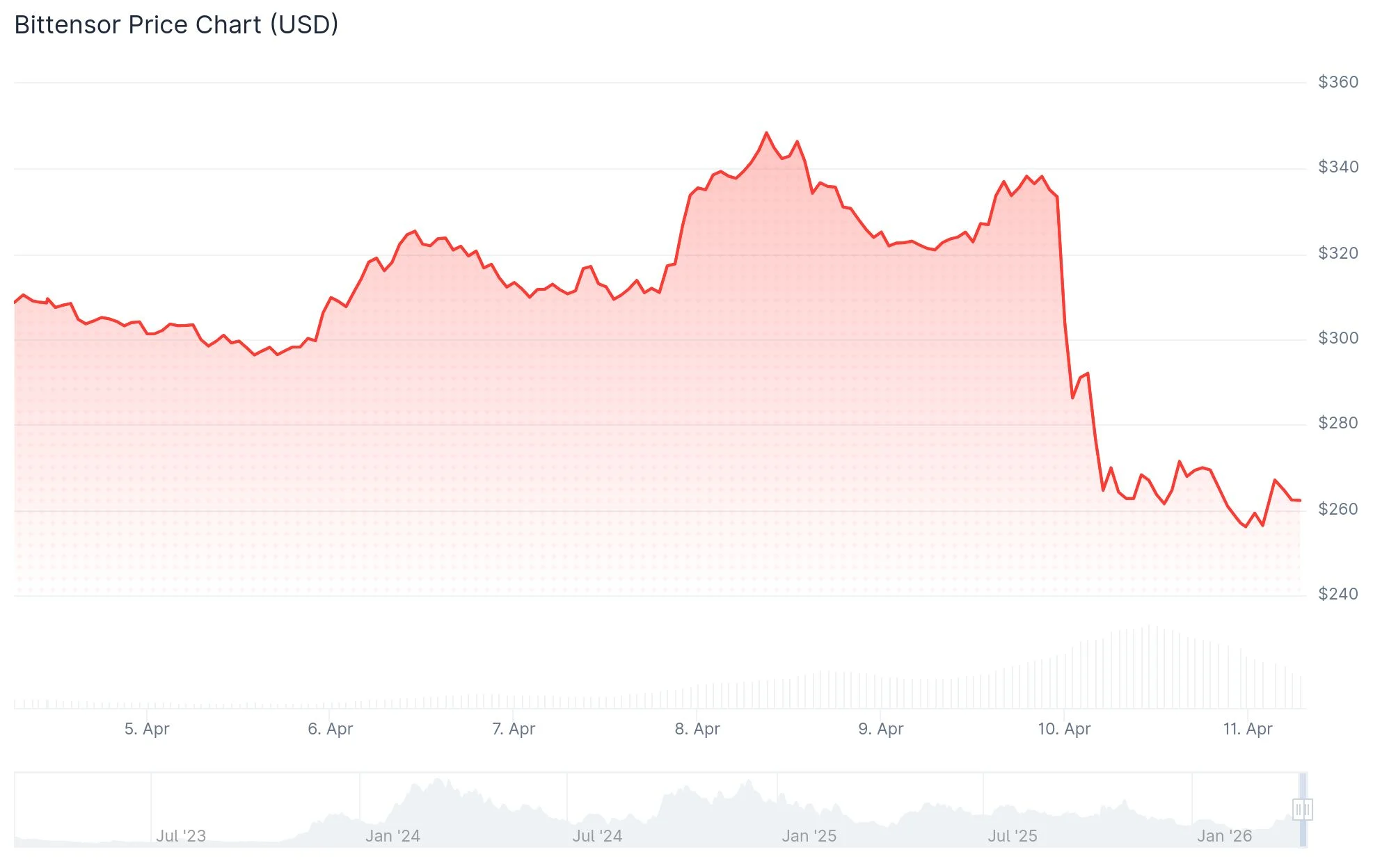

TLDR

- Covenant AI announced its departure from Bittensor on April 8, citing centralized control by co-founder Jacob Steeves

- TAO plummeted approximately 25–30% from weekly peaks, sliding from $337 down to the $249–$253 range

- More than $650 million in market capitalization evaporated, accompanied by $9.1 million in liquidated long positions

- Daily trading activity exploded to $1.72 billion on April 10, compared to roughly $500 million seen in early April

- Chart patterns suggest TAO could face an additional 25–45% correction toward the $144–$230 support zone

The Bittensor network’s native cryptocurrency TAO experienced a dramatic selloff this week following explosive allegations from a prominent subnet operator targeting the project’s leadership structure.

On April 8, Covenant AI declared its complete withdrawal from the Bittensor platform. Two days later, the company’s founder Sam Dare published an extensive explanation detailing the rationale behind this decision.

Dare’s statement accused Jacob Steeves, one of Bittensor’s co-founders, of maintaining unilateral authority over the protocol’s operations. This assertion stands in stark opposition to Bittensor’s fundamental value proposition as a decentralized, permissionless AI infrastructure where competing subnets operate autonomously.

According to Dare’s claims, Steeves independently halted emission distributions to a subnet, overruled subnet administrators within their designated governance channels, and eliminated projects without adhering to documented procedures.

Perhaps most damaging was Dare’s assertion that Steeves weaponized substantial, public token liquidations as “retaliatory” mechanisms to enforce compliance during disagreements. “These weren’t governance actions executed through open consensus mechanisms,” Dare stated. “They represented unilateral decisions by a single individual who never truly decentralized control.”

Dare further suggested that other members of the project’s leadership triumvirate function primarily as “liability buffers” while Steeves operates without accountability.

Market Reaction

TAO experienced a precipitous 25% collapse within six hours following the disclosure, tumbling from $337 to $253. This rapid decline eliminated more than $650 million in market capitalization, reducing the total to $2.57 billion.

Daily trading volume surged to $1.72 billion on April 10, significantly exceeding the approximately $500 million daily average recorded during the month’s opening days. The downturn coincided with a roughly 250% expansion in trading activity, indicating widespread market engagement in the selloff.

Within derivatives markets, long position liquidations totaled $9.1 million, with bullish traders absorbing $9.71 million in total forced closures. Numerous leveraged long positions faced margin calls, intensifying downward momentum through cascading liquidations.

TAO has experienced a modest rebound since bottoming but remains 12.8% lower across the previous seven-day period. Despite recent weakness, the token maintains a 37% gain over the trailing 30 days.

Technical Picture

TAO is presently trading within the 0.382–0.5 Fibonacci retracement zone. Historical precedent shows that in November 2025, a breach below this identical range resulted in losses exceeding 30%. A comparable formation in June 2025 witnessed TAO finding support around the 0.618 Fibonacci level before mounting a recovery.

Price Targets

Should TAO follow the June 2025 trajectory, downside risk extends to the 0.618 Fibonacci support zone approximately $230. If the November 2025 pattern materializes instead, the 1.0 Fibonacci objective resides near $144, representing roughly 45% downside from present price levels.

April 10’s trading volume reached $1.72 billion, marking the month’s peak activity level thus far.

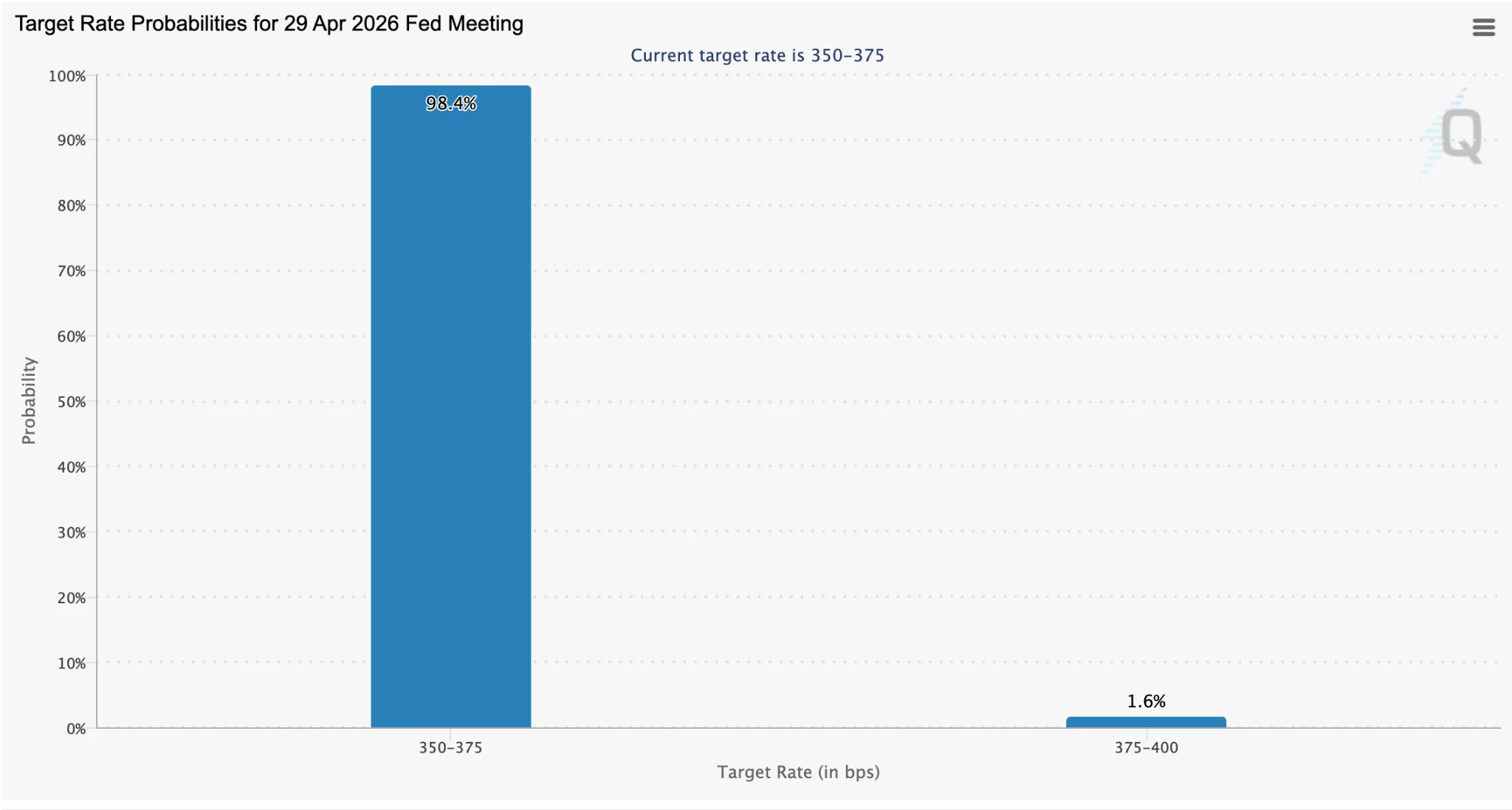

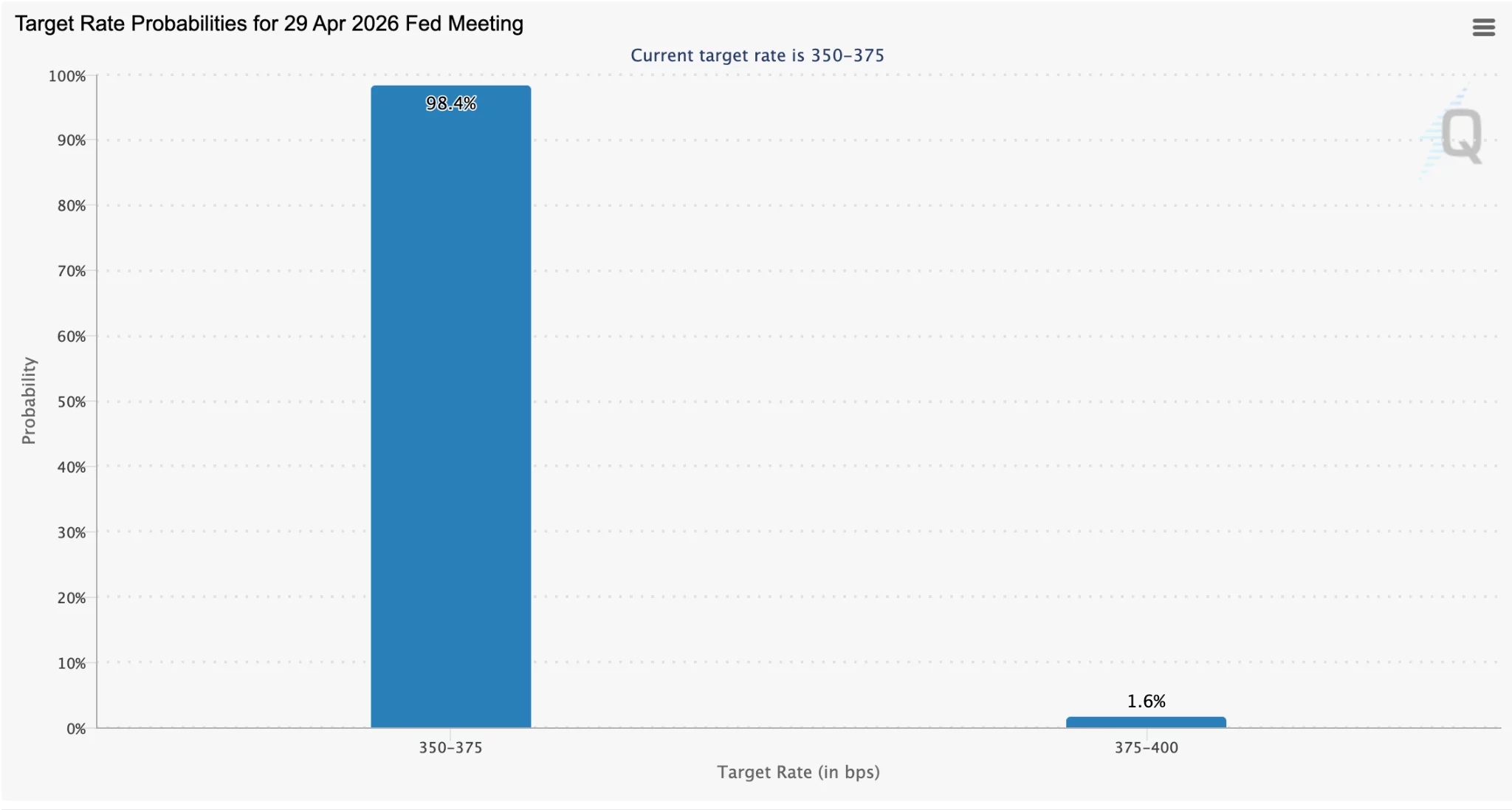

The US Bureau of Labor Statistics reported that headline Consumer Price Index inflation rose 0.9% in March from the previous month.

Summary

- US March CPI rose 3.3% yearly as energy prices surged and gasoline costs jumped sharply.

- Bitcoin climbed above $72,000 after the inflation report despite rising pressure on Federal Reserve policy.

- Traders see a 98.4% chance the Fed will keep rates unchanged in April.

On a yearly basis, CPI increased 3.3%, keeping inflation above the Federal Reserve’s 2% target.

The report showed that energy costs drove much of the monthly increase. The energy index rose nearly 11% during the month, while gasoline prices climbed 21.2%, making fuel the main source of price pressure in the latest reading.

March marked the first full month in which the US-Iran war shaped inflation data. Higher fuel costs pushed the headline number above the pace seen in February, when CPI rose 0.3% on the month and 2.4% from a year earlier.

At the same time, core CPI came in slightly lower than forecast. Core inflation, which excludes food and energy, rose 2.6% on a yearly basis, compared with market expectations of 2.7%. That reading showed that underlying price growth remained more stable even as energy prices surged.

Moreover, the inflation report kept attention on the Federal Reserve’s next policy move. Price stability remains part of the central bank’s dual mandate, alongside maximum employment, and inflation above target has continued to shape rate expectations.

According to CME Group’s FedWatch tool, traders see almost no chance of a rate cut at the April Federal Open Market Committee meeting. Market pricing showed a 98.4% probability that the Fed will leave rates unchanged, while officials have also not ruled out further tightening if inflation stays elevated.

Bitcoin rises after CPI release

Bitcoin moved higher after the CPI data was released, even as the inflation reading pointed to ongoing pressure on consumer prices. The asset briefly touched the $73,000 level and continued to trade above $72,000 later in the session.

At the time of writing, Bitcoin traded at $72,780, up 1 % over 24 hours and 9% over seven days.

Key Takeaways

- The Kingdom of Bhutan has slashed its Bitcoin reserves from approximately 13,000 BTC to just 3,774 BTC since October 2024

- State-controlled wallets have transferred more than $233 million in Bitcoin during 2026

- No significant mining inflows exceeding $100,000 have been detected in Bhutan’s wallets for over 12 months

- Druk Holding and Investments, managing Bhutan’s sovereign assets, has declined to provide public statements

- The Himalayan nation stands alone among sovereign Bitcoin holders in actively liquidating its position

The government of Bhutan has offloaded approximately 70% of its Bitcoin portfolio since reaching peak holdings of nearly 13,000 BTC in October 2024. Current reserves sit at roughly 3,774 BTC, representing a market value of about $272.5 million.

According to blockchain intelligence firm Arkham Intelligence, Bhutan’s Royal Government transferred an additional 250 BTC—valued at approximately $18 million—to a freshly established wallet address this week. This transaction followed a Thursday movement of roughly 319.7 BTC worth $22.68 million.

Cumulatively, the kingdom has relocated more than $233 million worth of Bitcoin from its identified treasury addresses throughout 2026. Approximately $162.6 million flowed into unidentified wallets, while remaining funds moved through addresses historically associated with liquidations via Galaxy Digital and OKX exchange platforms.

Bhutan’s cryptocurrency accumulation stemmed from a hydroelectric-powered mining initiative operated under Druk Holding and Investments, the nation’s sovereign investment vehicle. The program leveraged abundant renewable energy resources to mine Bitcoin while bypassing conventional banking systems.

Evidence Points to Mining Shutdown

Blockchain monitoring reveals no Bitcoin deposits exceeding $100,000 have entered Bhutan’s tracked addresses for more than twelve months. This pattern strongly indicates the mining program has either dramatically scaled back or ceased operations completely.

Druk Holding and Investments has remained silent despite numerous inquiries from journalists, ignoring email correspondence and phone attempts throughout the past week.

The profitability landscape for Bitcoin mining has fundamentally transformed. During Bhutan’s peak mining period, Bitcoin prices exceeded $90,000 while network difficulty remained comparatively moderate. Today, Bitcoin hovers around $72,000 amid record-high mining difficulty levels.

The halving event further reduced block rewards to just 3.125 BTC per block. Combined, these market conditions have squeezed profit margins for smaller-scale mining enterprises.

Another consideration involves electricity export opportunities—selling surplus hydropower to India may now yield superior returns compared to powering cryptocurrency mining infrastructure.

Institutional Buyers Continue Accumulating

Bhutan’s divestment strategy contrasts sharply with behavior among other major stakeholders. Strategy recently acquired 4,871 BTC for $330 million last weekend, expanding its total position to 766,970 BTC.

U.S.-based spot Bitcoin exchange-traded funds accumulated approximately 50,000 BTC throughout March alone. Meanwhile, the Ethereum Foundation staked $93 million in Ether within a 24-hour period rather than liquidating assets.

Bhutan represents the sole sovereign entity currently engaged in visible Bitcoin position reduction.

Bitcoin was trading above $72,000 at press time, registering gains exceeding 1.3% over the preceding 24-hour period. The cryptocurrency remains roughly 43% beneath its peak valuation of approximately $126,000 achieved in October 2025.

Bhutan’s residual 3,774 BTC holding now amounts to less than Strategy’s typical weekly purchase volume.

Key Takeaways

- Tehran is reportedly exploring digital currency payment options for vessels transiting the Strait of Hormuz

- This waterway accounts for approximately one-fifth of worldwide petroleum transport

- Blockchain analysis firm Chainalysis identifies this as potentially unprecedented for state-controlled maritime passages

- Industry experts suggest stablecoins might be favored over Bitcoin given liquidity considerations and Iran’s historical crypto usage patterns

- Maritime companies accepting these payments could face significant regulatory consequences under international sanctions regimes

Reports emerged this week indicating Iran may implement cryptocurrency-based fees for oil tankers navigating through the Strait of Hormuz, a strategically vital maritime corridor. The Financial Times first reported the development on Wednesday, attributing the information to a representative from Iran’s Oil, Gas and Petrochemical Products Exporters’ Union.

https://twitter.com/arkham/status/2042186892465320414?s=20

This narrow passage facilitates the movement of roughly 20% of worldwide petroleum supplies. According to reports, Iran’s Islamic Revolutionary Guard Corps would oversee the fee collection mechanism.

The proposed system would require vessel operators to provide ownership documentation and cargo information prior to fee negotiations. Initial pricing is reported to begin around $1 per barrel, with payment options including Chinese yuan or digital currencies.

Galaxy’s research director Alex Thorn indicated that varying accounts point to possible payment methods including stablecoins or Chinese yuan beyond just Bitcoin. He confirmed Galaxy is actively tracking blockchain networks for evidence of such transactions.

https://twitter.com/coinbureau/status/2042830276913713610?s=20

Thorn’s analysis places potential toll charges in a range from $200,000 to $2 million per vessel. The Financial Times report specified ships would receive mere seconds to complete Bitcoin transfers.

Technical Implementation Questions Remain

Such an abbreviated payment timeframe points toward potential Lightning Network utilization. This second-layer [[LINK_START_0]]Bitcoin[[LINK_END_0]] solution enables near-instantaneous transactions, circumventing the typical 10-minute block confirmation delays.

Yet Thorn highlighted that the highest recorded Lightning transaction stands at $1 million. This capacity limitation may prove insufficient for premium-tier tolls. His assessment suggests Iran would more likely distribute QR codes or Bitcoin wallet addresses following transit authorization approval.

Cryptocurrency proponents emphasize that BTC operates without central issuance and cannot be frozen, contrasting with stablecoins like USDT or USDC that remain subject to smart contract-level blacklisting.

Chainalysis released analysis on April 10 characterizing this development as potentially historic. The blockchain intelligence company stated successful implementation would mark the first documented instance of a sovereign nation requiring cryptocurrency for passage through internationally significant waters.

Stablecoin Payment More Probable, Experts Say

Notwithstanding Bitcoin-focused headlines, Chainalysis indicated Tehran may actually favor stablecoins. The firm referenced Iran’s established track record utilizing stablecoins for petroleum transactions, arms procurement, and large-scale sanctions circumvention.

Stablecoins provide superior liquidity and price stability compared to [[LINK_START_1]]Bitcoin[[LINK_END_1]], rendering them more suitable for substantial commercial exchanges.

International shipping corporations face legitimate compliance exposure. Transferring funds to IRGC-associated wallets could prompt enforcement measures under U.S. Treasury Department sanctions frameworks, irrespective of payment denomination.

Chainalysis emphasized that blockchain forensics capabilities have become indispensable for monitoring these financial flows and supporting global risk management efforts.

Crypto World

Is the Crypto Bull Run Starting as Fundstrat Targets $200,000 BTC and One Presale Nears Listing

Fundstrat’s Tom Lee just placed BTC between $200,000 and $250,000 for this cycle, Goldman Sachs expects two rate cuts in 2026, and Kevin Warsh takes over as Fed chair in May with a track record of pushing for lower rates.

The crypto bull run setup is forming, but the wallets that built generational wealth last cycle did not buy large caps at the top.

Pepeto loaded more than $8.87 million during extreme fear with the cofounder who built the original Pepe coin and a confirmed Binance listing, the kind of entry that previous cycle winners all say they wish they found earlier.

Fundstrat’s Tom Lee placed BTC between $200,000 and $250,000, and Galaxy CEO Mike Novogratz targets $120,000 to $125,000 near term per GlobeNewswire.

Goldman Sachs models two rate cuts for 2026, and Kevin Warsh takes the Fed chair in May with a history of favoring easier money per CoinDesk.

Looser conditions in the second half of the year sit behind every major crypto bull run in history, and the presale entries positioned before that shift capture the widest returns.

How ADA, XRP, and Pepeto Line Up as the Crypto Bull Run Takes Shape

Pepeto: The Presale That Catches the Bull Run From the Lowest Floor

Every crypto bull run makes the same promise, that the early entries win. But most wallets end up buying after the move starts, when prices already jumped and the real gains already got locked in by someone else. Pepeto is the entry that sits at the floor before the move hits, and the confirmed Binance listing is the event that triggers it.

The exchange already runs. Zero fee trading, a cross chain bridge at zero cost, and a risk scanner that catches bad contracts before money goes in are all live and processing real trades. This is not a roadmap promise, it is a working product collecting $8.87 million in presale capital while the Fear and Greed Index stayed pinned in extreme fear territory.

The Pepe cofounder who turned 420 trillion tokens into an $11 billion market cap with zero tools behind it is building a real exchange this time, every contract cleared a SolidProof audit, and 186% APY staking compounds positions while the listing clock ticks. At $0.0000001863, analysts model 100x to 300x when the Binance order book goes live.

Every round closes quicker than the last, and the moment the listing opens this price is gone forever. The crypto bull run rewards wallets that are already inside when the move starts, not the ones scrambling to buy after the headline drops.

Cardano: ADA Waits on ETF Approval With Limited Near Term Upside

ADA trades near $0.255 with ETF filings from Grayscale and VanEck pending SEC approval per CoinGecko. The Midnight sidechain launched with Google Cloud and MoneyGram as validators, adding real enterprise weight.

ADA could ride the crypto bull run higher, but from $0.255 the path to $1 is a 4x that takes quarters, while a presale floor with a confirmed listing delivers a wider gap in one event.

XRP: Regulatory Clarity Helps but Returns Stay Small

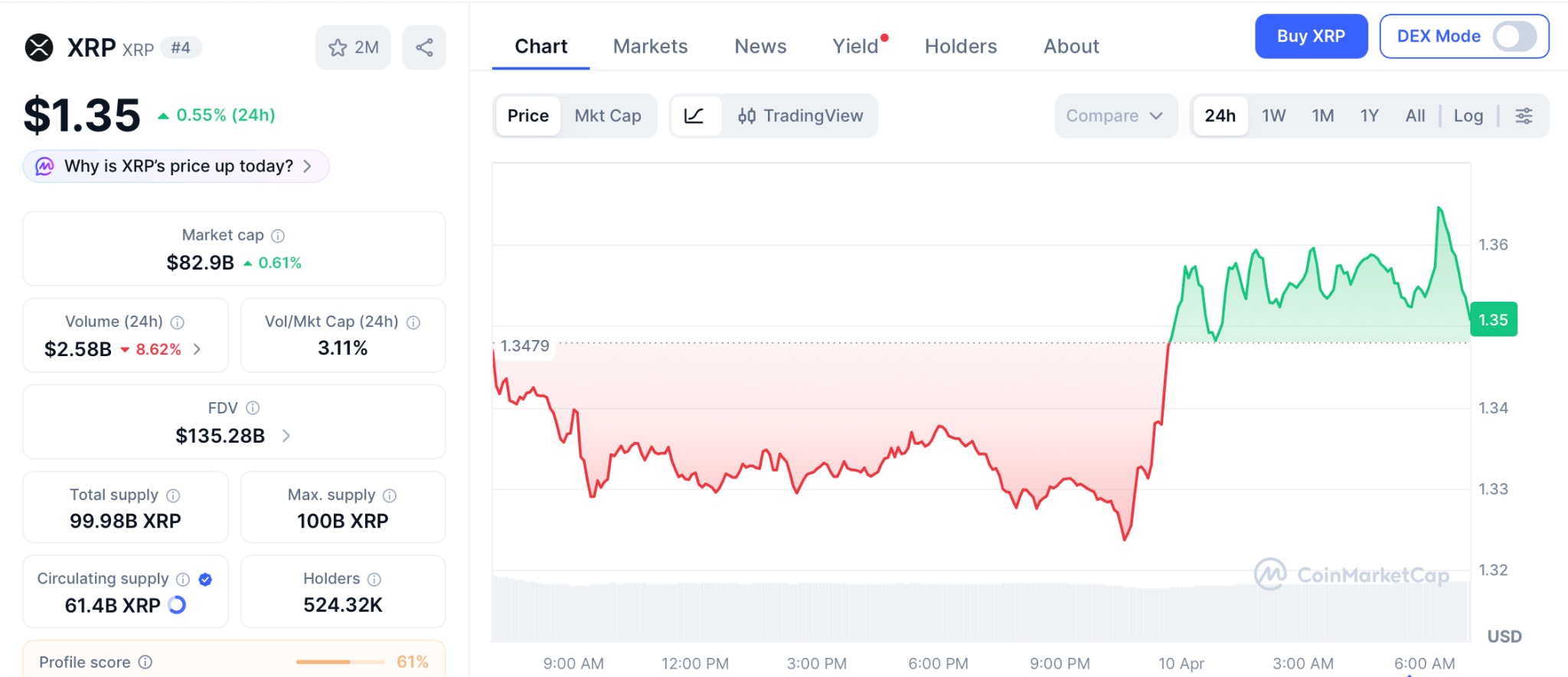

XRP holds near $1.35 after the ceasefire bounce with clearer regulatory standing following SEC settlements per CoinMarketCap. Cross border payment demand supports the long case, and spot XRP ETFs have pulled in over $1.3 billion in cumulative inflows.

XRP could catch the crypto bull run wave, but from $1.35 even reaching $3 is roughly a 2x that most portfolios would not call life changing, and that is why presale floors exist.

Conclusion

Fundstrat and Galaxy signal long term confidence in digital assets, and the wallets getting ready for the crypto bull run are moving past listed tokens toward presale entries with real weight behind them. Pepeto has the live exchange, the Pepe cofounder, and the confirmed Binance listing to back it.

Every major cycle made millionaires from the wallets that committed at the floor, and Pepeto at presale price is that floor right now. The listing is the event that changes everything, and the entry available today disappears the moment it arrives.

Click Here To Position for the Crypto Bull Run Through Pepeto

FAQs

Is the crypto bull run starting in 2026?

Fundstrat targets $200,000 BTC, Goldman expects two rate cuts, and the new Fed chair favors easier money starting May. Every signal points to the crypto bull run forming in the second half of 2026.

Which presale benefits most from the crypto bull run?

Pepeto with $8.87 million raised, a live exchange, SolidProof audit, and confirmed Binance listing captures the widest return from the coming rally. The $0.0000001863 presale floor is where bull run gains start.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Crypto World

CLARITY Act Gains Momentum as Coinbase CEO, Treasury Chief, and White House Push for Passage

Key Points

- Brian Armstrong of Coinbase has reversed his January opposition and now endorses the CLARITY Act

- Scott Bessent, Treasury Secretary, penned a Wall Street Journal opinion piece calling for immediate congressional action

- Senate Banking Committee has scheduled a vote on the legislation before April concludes

- Central dispute centers on stablecoin yield programs and whether exchanges like Coinbase can offer returns to users

- Senator Cynthia Lummis cautioned this represents the final opportunity for passage until 2030 at the earliest

The United States cryptocurrency sector is mounting an intensive campaign to secure congressional approval for the Digital Asset Market Clarity Act, with major industry leaders now rallying behind the proposed legislation following an extended period of legislative stagnation.

In a significant policy reversal, Coinbase’s Chief Executive Brian Armstrong declared on X earlier this week that “it’s time to pass the Clarity Act.” This statement marks a dramatic departure from his January position, when he pulled Coinbase’s endorsement, arguing the legislation was unacceptable “as written.” That withdrawal prompted the Senate Banking Committee to postpone a critical markup session.

Armstrong characterized the current iteration of the bill—refined through extensive negotiations among legislators, banking institutions, and cryptocurrency firms—as a “strong bill” worthy of support.

Treasury Secretary Scott Bessent amplified the administration’s stance through a compelling opinion piece published in The Wall Street Journal this week, urging immediate legislative action. “Senate floor time is scarce, and now is the time to act,” Bessent emphasized in his editorial.

The Senate Banking Committee, where the measure has languished for more than twelve months, has now committed to conducting a vote prior to April’s conclusion.

The Stablecoin Yield Controversy

The primary obstacle impeding progress involves the treatment of stablecoin yield programs. The GENIUS stablecoin legislation, enacted last July, prohibits stablecoin issuers from directly compensating holders with interest. However, the law does not prevent third-party platforms such as Coinbase from providing such rewards.

Traditional banking institutions contend that permitting such yield mechanisms would drain deposits from conventional financial entities, particularly affecting smaller community banks. Cryptocurrency advocates counter that restricting these reward programs would stifle technological advancement.

A White House economic analysis published this week concluded that stablecoin yield programs pose minimal threat to bank lending activities. Banking representatives disputed this assessment, arguing the report failed to adequately measure specific impacts on community banking institutions or deposit migration patterns.

According to a banking industry source who spoke with The Block on Friday, negotiations continue on more precise language governing yield restrictions to address lending sector concerns.

Another insider indicated the current priority involves “getting the banks in line to support the compromise,” noting: “Seems crypto is nearly there.”

Legislative Path Forward

Paul Grewal, Coinbase’s chief legal officer, indicated last week that lawmakers were “very close to a deal.”

Should the measure advance through the Senate Banking Committee, it must then be harmonized with the Senate Agriculture Committee’s competing version. Passage on the full Senate floor would necessitate 60 affirmative votes, requiring bipartisan cooperation with Democratic senators joining Republican supporters.

Senator Cynthia Lummis, among the bill’s most vocal proponents, announced Friday she will not pursue re-election and her tenure concludes in January 2027. “This is our last chance to pass the Clarity Act until at least 2030,” she wrote on X.

The Office of the Comptroller of the Currency recently granted approval for Coinbase’s national bank trust charter application, joining previously approved entities including Paxos, Ripple Labs, BitGo, Circle, and Fidelity Digital Assets.

TLDR

- BTC escaped a bear pennant formation, climbing to a six-week peak of $73,300

- Key resistance territory identified by Glassnode sits in the $78,000-$80,000 range

- Prediction markets on Polymarket now show 26% probability of BTC hitting $80,000 this month

- Institutional Bitcoin ETF buyers accumulated 3,350 BTC valued at $240 million on Friday alone

- Geopolitical developments including U.S.-Iran détente and improving macro sentiment drove BTC up almost 9% weekly

Bitcoin surged beyond the $73,000 threshold on Friday, touching a six-week peak at $73,300 following a decisive breakout from what technical analysts had identified as a bear pennant formation on daily timeframes. The advance occurred alongside elevated trading volumes, suggesting genuine buying conviction rather than thin market manipulation.

The cryptocurrency pierced through the pennant’s upper boundary near $70,000, delivering a 7% single-session gain. During this advance, BTC successfully recaptured multiple significant moving average levels, notably the 200-week exponential moving average positioned at $68,350 and the 50-day exponential moving average sitting at $70,580.

Technicians have also spotted a symmetrical triangle developing on daily charts. Should this pattern complete its typical trajectory, the projected upside target reaches approximately $87,000—representing roughly 20% appreciation from current pricing. Additionally, the Relative Strength Index displays bullish divergence, indicating momentum has been gradually accumulating throughout the previous two months.

The immediate technical obstacle for Bitcoin sits at the 100-day exponential moving average hovering near $75,400. Failure to overcome this barrier could compromise the strength of the present breakout attempt.

What Onchain Data Says About $80K

Glassnode analytics establishes a more defined upper boundary for the near-term advance. The analytics firm’s risk assessment tools highlight substantial resistance clustering between the true market mean around $78,000 and the short-term holder acquisition cost basis approximating $80,000.

“Any rally into this zone is likely to encounter meaningful distribution pressure from recent buyers seeking to exit at or near breakeven,” Glassnode said in its latest Week Onchain report.

Their Entity-Adjusted URPD metrics indicate BTC has penetrated a comparatively sparse zone spanning $72,000 to $82,000, featuring diminished supply overhead throughout that corridor. Nevertheless, over 1.3 million BTC were accumulated within the $82,000-$85,000 band, potentially establishing a formidable ceiling.

Market observer Ali Charts highlighted on X that $75,300 functions as a “magnet” for Bitcoin pricing, observing substantial liquidity concentration positioned just beyond $72,000. He suggested a movement toward $75,300 might eliminate approximately $80 million in short positions, potentially initiating a liquidation cascade.

ETF Demand and Macro Backdrop

Regarding institutional participation, Bitcoin Archive documented on X that spot Bitcoin ETF products absorbed 3,350 BTC worth $240 million during a single trading session. These investment vehicles collectively control 721,090 BTC, representing approximately $56.75 billion in aggregate value.

Broader macroeconomic circumstances also turned favorable for Bitcoin’s trajectory this week. Diplomatic progress toward a U.S.-Iran ceasefire agreement lifted risk-sensitive assets across markets, propelling BTC toward a weekly appreciation approaching 9%—marking its strongest weekly performance since October 2025.

March Consumer Price Index data registered 3.3%, primarily attributable to a substantial 10.9% spike in energy sector costs. Core inflation measurements, however, advanced merely 0.2% month-over-month.

On decentralized prediction platform Polymarket, participants currently assign a 26% probability to BTC achieving $80,000 during April, representing a 5% increase over the preceding 24 hours. Meanwhile, the likelihood of reaching $75,000 stands at 76%.

Bitcoin ETF products maintained holdings of 721,090 BTC valued at $56.75 billion as of Friday’s close.

US, Iran teams in Pakistan for peace talks amid doubts over Lebanon, sanctions

Arizona Judge Blocks Gambling Enforcement Against Kalshi Contracts

Kelly Ripa and Mark Consuelos cheer on son Joaquin in his Broadway debut

-

Business5 days ago

Business5 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports6 days ago

Sports6 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Politics13 hours ago

Politics13 hours agoUS brings back mandatory military draft registration

-

Fashion14 hours ago

Fashion14 hours agoWeekend Open Thread: Veronica Beard

-

Tech3 days ago

Tech3 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business6 days ago

Business6 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion5 days ago

Fashion5 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports14 hours ago

Sports14 hours agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion4 days ago

Fashion4 days agoLet’s Discuss: DEI in 2026

-

Crypto World3 days ago

Crypto World3 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business11 hours ago

Business11 hours agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Business6 days ago

Business6 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Crypto World2 days ago

Crypto World2 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business20 hours ago

Business20 hours agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Tech5 days ago

Tech5 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech5 days ago

Tech5 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech5 days ago

Tech5 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Tech5 days ago

Tech5 days agoSamsung just gave up on its own Messages app

-

Tech5 days ago

Tech5 days agoSave $130 on the Samsung Galaxy Watch 8 Classic: rotating bezel, sleep coaching, and running coach for $369

-

Tech5 days ago

Tech5 days agoItalian court says Netflix must refund customers up to $576 over price hikes

You must be logged in to post a comment Login