Crypto World

CFTC Sues Wisconsin in Response to State’s Lawsuits Against Prediction Markets

The CFTC filed suit against Wisconsin to establish its exclusive regulatory authority over prediction markets, a sector closely tied to crypto and blockchain-based derivatives.

The U.S. Commodity Futures Trading Commission (CFTC) sued Wisconsin on April 28, 2026, to reassert its exclusive jurisdiction over prediction markets. The action challenges state-level regulatory interference in a sector increasingly built on blockchain technology and crypto assets. The lawsuit underscores ongoing federal-state jurisdictional disputes over decentralized and tokenized derivatives platforms.

The CFTC’s enforcement action signals the regulator’s intent to maintain control over derivatives-adjacent products in the crypto space, potentially affecting platforms that tokenize prediction market shares or operate on decentralized protocols.

The CFTC said that its lawsuit is in response to Wisconsin filing civil suits against multiple CFTC-regulated prediction market companies — Kalshi, Polymarket, Crypto.com, Robinhood, and Coinbase — alleging violations of state law.

Sources: CFTC

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

RedStone, a decentralized oracle provider, has launched a new settlement layer for decentralized finance, aiming to make tokenized real-world assets (RWAs) usable as collateral in lending protocols.

The system, called RedStone Settle, is designed to address a long-standing structural issue in DeFi. While lending platforms such as Aave rely on near-instant liquidations to manage risk, RWAs, including tokenized funds and bonds, typically have redemption periods ranging from 60 to 180 days. This mismatch has largely prevented RWAs from being used as collateral.

According to RedStone, the new layer introduces an onchain auction mechanism that is triggered during liquidation events. Liquidity providers can step in to purchase positions immediately, supplying protocols with liquidity while assuming the delayed redemption risk tied to the underlying assets.

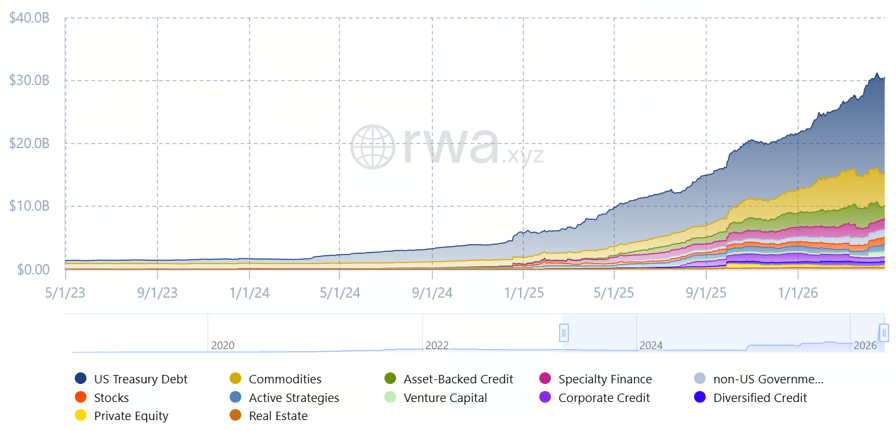

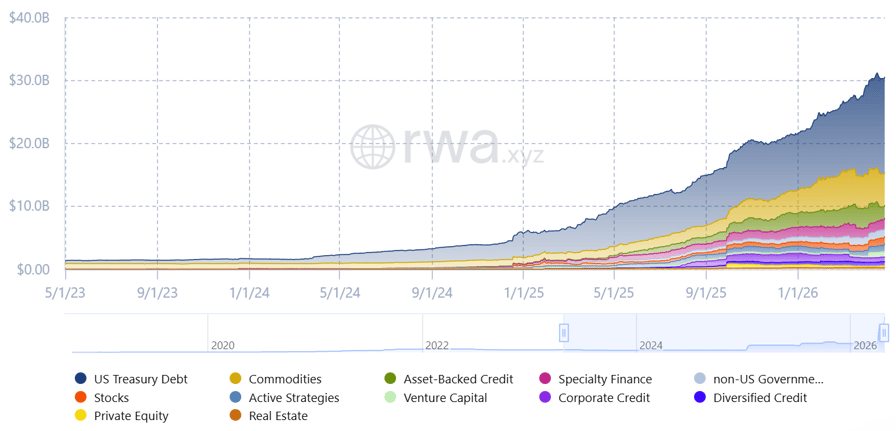

The Baar, Switzerland-based company said the approach could help unlock more than $30 billion in tokenized RWAs currently sitting idle in DeFi, while allowing users to borrow against yield-generating positions more efficiently.

That figure broadly aligns with estimates of the current RWA market. Excluding stablecoins, tokenized real-world assets are valued at over $30 billion, led by products such as US Treasury exposure and private credit, according to RWA.xyz.

Tokenized RWA market. Source: RWA.xyz

Related: Flow Capital plans to tokenize $150M private credit fund via DigiFT: Report

Tokenization alone doesn’t solve liquidity constraints

RedStone’s product launch comes amid growing debate over whether tokenization meaningfully improves liquidity.

As previously reported by Cointelegraph, industry participants at this month’s Paris Blockchain Week said putting assets onchain does not automatically make them tradable or usable in financial markets.

Tokenized real-world assets continue to face structural limitations, particularly in liquidity and settlement speed.

“I think there’s still this idea that tokenizing something illiquid will somehow magically make it a liquid asset, which is just not true,” said Oya Celiktemur of Ondo Finance during a panel hosted by Cointelegraph.

Paris Blockchain Week panel on RWA liquidity. Source: Cointelegraph

At the same time, DeFi lending has expanded alongside growing institutional interest and the gradual adoption of RWAs as collateral. According to Binance Research, the sector grew 72% year-over-year through September, driven in part by institutional use of stablecoins and tokenized assets.

Related: Stablecoin transfer volume drops 19% even as supply keeps rising: RWA.xyz

Across XRP, WeFi, and Hyperliquid, this briefing frames a market expectation: the emphasis is shifting from hype to real use cases and scalable infrastructure. The press release casts XRP, WeFi, and Hyperliquid as three distinct pillars—cross-border settlements, on-chain banking, and decentralized derivatives—whose fundamentals could shape adoption, liquidity, and capital flow in 2026 even as prices consolidate. The material aims to help readers, from users and builders to investors, understand why these tokens are highlighted together and what signals to watch as regulation, product rollout, and real-world usage evolve. This intro previews the themes and what to monitor next.

Key points

- XRP is presented as infrastructure for fast, low-cost international settlements, with a 2025 regulatory settlement and the launch of spot XRP ETFs that may attract institutional capital.

- WeFi merges on-chain accounts with a banking-like UX, has grown rapidly (800% since last year) with 150,000+ users across 80+ countries, and is moving from BNB Smart Chain to its own WeChain.

- Hyperliquid is described as a dedicated infrastructure layer for perpetual futures, handling large volume and revenue (about $2.95 trillion in annual volume and $747 million in revenue) and focusing on liquidity rather than directional bets.

- Institutional interest and ETF filings are noted as a potential bridge to on-chain derivatives (Bitwise updating its S-1 for an ETF, with Grayscale, 21Shares, and VanEck in the queue).

Why it matters

Taken together, XRP, WeFi, and Hyperliquid illustrate how on-chain systems with real products and growing user bases could shape 2026 activity. The emphasis on infrastructure over hype suggests liquidity and adoption may be driven by actual usage, settlement efficiency, and derivatives trading capabilities, rather than headlines. For readers, developers, and investors, the key takeaway is to watch adoption signals, regulatory developments, and the pace at which traditional capital begins to engage with on-chain infrastructure.

What to watch

- Regulatory developments and ETF inflows for XRP (e.g., spot XRP ETFs) and how they affect institutional participation.

- Progress of WeFi adoption (80+ countries, 150k users) and the move to WeChain; potential shifts in user experience.

- Hyperliquid’s liquidity growth and the status of ETF filings by major firms (Bitwise, Grayscale, 21Shares, VanEck) for on-chain derivatives.

Disclosure: The content below is a press release provided by the company or its PR representative. It is published for informational purposes.

XRP, WFI & HYPE: The Trio That Could Surprise the Market in 2026

The crypto market is entering 2026 after a series of sharp fluctuations, reduced risk appetite, and an increasingly clear separation between assets with real products and tokens that are mainly sustained by speculative demand. Despite this, most altcoins are still trading roughly 40–50% below their local highs. Historically, it is precisely these phases that create the most interesting opportunities: the market gradually shifts toward infrastructure, payments, and practical on-chain utility.

In this context, I would highlight three tokens that could potentially not only recover their losses but also break through previous peaks within the current cycle: Ripple $XRP, WeFi $WFI, and Hyperliquid $HYPE. These represent three different sectors – cross-border settlements, on-chain banking, and decentralized derivatives trading – but they share one key factor: their fundamental models continue to strengthen even during periods of price consolidation.

The Post-Overheat Market: Focus Shifting to Fundamentals

There is a recurring pattern that repeats cycle after cycle: the greatest upside potential forms not during moments of euphoria, but during periods of market fatigue, when retail interest fades. The current picture looks exactly like that – most altcoins are correcting from their highs, liquidity is becoming more selective, and capital is moving more cautiously.

At the same time, institutional capital behaves differently: without loud announcements or FOMO, it gradually builds positions in segments where there is a clear product economy and long-term demand. The key difference between this cycle and previous ones lies in the quality of assets attracting attention.

- 2021 was about hype, memes, and retail speculation.

- 2024–2025 is about institutional entry through Bitcoin ETFs.

- And 2026 increasingly looks like a phase of selective growth, where the winners are not the loudest projects but the most functional ones.

At the center of attention are protocols with real products, real users, and real cash flows.

Is XRP Still Undervalued? The Institutional Adoption Case Nobody Prices In Yet

XRP is currently trading around ~$1.42 – on the surface it looks weak, but the picture is more complex. The SEC lawsuit was effectively closed in 2025 through a financial settlement, and the launch of spot XRP ETFs in November has already brought in over $1B in net inflows. This is not just a “legal win” – it opens the door for institutional capital that was previously blocked by regulatory uncertainty.

Fundamentally, XRP is not about “digital gold.” It is an infrastructure asset for fast and low-cost international settlements. Forecasts for 2026 are mostly in the $2.5–$5 range, with average expectations around $3.5–$4. Some models still allow more aggressive targets up to ~$5, but those assume a high level of adoption.

Trading View Source: XRP/USDT Chart – Coinbase

The key driver is simple: whether banks and payment providers will actually start scaling Ripple’s infrastructure. If they do, current levels could look like an early entry phase.

WFI at Scale: Where Utility Starts to Price in Real Adoption

WeFi (WFI) looks like a project operating in a different phase of the cycle compared to most familiar DeFi tokens. And this is the key point: over 800% since the start of last year, more than 150,000 users, and an ATH of $2.75 after consolidating around $2.40 at the end of November – this is no longer an early-stage “pitch,” but rather a sign of established demand. But what matters even more is what’s happening under the hood: an ecosystem that is already starting to scale on its own. According to analysis by TradingView technical analyst CryptoPatel, within his scenario, a potential target level could be around $100.

Trading View Source: WFI/USDT Chart – BingX

The core idea behind WeFi is fairly pragmatic: to merge on-chain accounts with a banking-like UX, where crypto balances can be spent directly via a card – without bridges, manual swaps, or extra steps. The transition from BNB Smart Chain to its own WeChain only reinforces this logic. In such an architecture, WFI effectively becomes the native “fuel” of the system – covering fees, staking, liquidity, and application activity. This starts to look more like an infrastructure layer than a traditional utility token.

At this stage, the market is pricing the project relatively cautiously: a market cap slightly above $200M with a fixed supply of 1 billion tokens still leaves room for revaluation. But the main signal here isn’t the chart – it’s adoption: rapid user growth and real product usage across 80+ countries. And that raises the question – are we looking at another short growth cycle, or at the early phase of a “banking Ethereum effect” that is only just beginning to unfold?

Why Hyperliquid Is No Longer “Just Another DEX”

Hyperliquid no longer looks like just another DEX from previous market cycles but rather as a distinct infrastructure layer designed from the ground up for perpetual futures and high-volume trading. It is not a fork or an attempt to “repackage” an old AMM model – instead, it resembles market infrastructure that has become a concentration hub for derivatives activity. Against this backdrop, the numbers are striking: ~$2.95 trillion in annual volume, ~$747 million in revenue, all within a segment where derivatives already account for roughly 76% of crypto trading. The logic is simple – the platform doesn’t impose a direction on the market; it monetizes the intensity of movement itself.

Trading View Source: HYPE/USDT Chart

At this stage, institutional interest looks less like speculation and more like a natural continuation of the trend. Bitwise Asset Management has already updated its S-1 for an ETF, with Grayscale Investments, 21Shares, and VanEck also in the queue, effectively creating a potential bridge between traditional capital and on-chain derivatives. In such a setup, even price scenarios like Arthur Hayes’ $150 stop looking like hype-driven speculation – they increasingly depend purely on the scale of liquidity inflows and the speed of their integration into the market.

At the end

If this cycle is defined by anything, it’s not broad upside across the board, but a narrowing of attention toward protocols that actually solve distribution, settlement, or trading efficiency at scale. In that sense, XRP, WeFi, and Hyperliquid are less “bets on price” and more different expressions of the same trend: infrastructure starting to matter more than narratives. The real question for 2026 is not which assets can pump, but which ones can justify staying relevant once liquidity stops forgiving everything else.

Crypto World

Bitcoin will bottom at $57,000 in October and will not see an all-time-high this year, says Michael Terpin

Bitcoin has not reached its bottom yet, and a new all-time high is unlikely this year, said Michael Terpin, an early bitcoin investor and author of Bitcoin Supercycle: How the Crypto Calendar Can Make You Rich.

“Before a bull market for bitcoin can be called, the price needs to break back above $100,000 and no support anywhere near has manifested,” according to Terpin, who said the bottom will be seen at $57,000 sometime in October.

“Despite a double-digit gain thus far in April, we are very much still in a bitcoin fall.”

Terpin is often called ‘the crypto Godfather’ for his involvement in the industry around 2013, when the digital asset sector was still small and somewhat misunderstood by the mainstream. Among his many ventures, Terpin founded Transform Group, one of the first PR firms focused on blockchain companies, CoinAgenda, one of the first conferences in the space and BitAngels, a crypto angel investor group.

His bearish view for this cycle stands in contrast to the consensus among analysts that the February low around $60,000 marked the end of the bear market and the beginning of a new bull run. Most of these bullish analysts cited renewed inflows into U.S.-listed spot ETFs and the token’s resilience during the Iran conflict and the oil price spike as part of their outlook.

In an interview with CoinDesk, Terpin said that during Asian trading hours on Monday, “the psychological barrier of $80,000 was strongly rejected, with the high price of oil a factor.” He explained that this is typical at this stage of the bitcoin cycle, with lower highs being rejected until the final capitulation.

While Jason Fernandes, a market analyst and co-founder of AdLunam, agrees with Terpin that the bottom has not yet been seen, he disagrees with the timeline, adding that the market may not have fully capitulated yet. Capitulation is a phase in which long-term holders exit in large numbers, signaling a peak in selling pressure.

“Terpin makes a reasonable case for a later-cycle bottom, but I don’t believe bitcoin has fully capitulated yet,” Fernandes said. “Historically, durable bottoms tend to coincide with a clear exhaustion of both speculative leverage and macro uncertainty, and we’re definitely not there yet.”

Terpin insisted that the fundamentals point more toward a bottom that includes the historical average of the one-year period from each cycle’s bottom.

“That indicates somewhere around $57,000,” he said, predicting that it will happen sometime in October, about the same timeline from last year when BTC first dipped below $100,000, followed by the October 10 crash, when $19 billion in leveraged positions were wiped out in the largest single-day event on record.

Fernandes added that broader macro conditions could continue to weigh on risk assets, including bitcoin.

“Liquidity conditions remain tight, and risk assets broadly are still adjusting to a higher-for-longer rate environment,” he said. “Until we see a more decisive shift in monetary policy or a true washout event in crypto markets, downside volatility remains likely.”

‘Overly bearish’

The author and entrepreneur also said bitcoin will not see an all-time high (ATH) this year.

However, Mati Greenspan, a crypto market analyst and founder of Quantum Economics, disagrees.

“While I’m hesitant to ever disagree with the ‘Crypto Godfather,’ his take seems overly bearish to me,” Greenspan said. “We still have lots of room to run this year, given the level of institutional adoption and growing interest a new all-time-high (ATH) certainly seems plausible.”

AdLunam’s Fernandes also said market sentiment has not yet reached the levels typically associated with cycle bottoms.

“Sentiment hasn’t reached the kind of extreme pessimism that typically marks cycle lows,” he said. “To me, that says we may still need one more leg down – whether or not it aligns exactly with the $57,000 to $59,000 range – before a sustainable base is formed.”

Regarding Terpin’s $100,000 level, Fernandes said it serves more as a psychological signal than a strict technical threshold.

“A true bull market is defined by structural higher highs and strong capital inflows, not just a single price level,” he said. “That said, the psychological effects of hitting $100,000 could trigger exactly that behavior,” Fernandes added.

RedStone, a decentralized oracle provider based in Baar, Switzerland, has unveiled RedStone Settle, a new on-chain settlement layer designed to put tokenized real-world assets (RWAs) to work as collateral in DeFi lending protocols. The move targets a persistent structural hurdle: RWAs such as tokenized funds and bonds often carry redemption windows of 60 to 180 days, a timeline that has historically clashed with the near-instant liquidation mechanics that govern most DeFi lending markets. By introducing an on-chain auction mechanism that activates during liquidation events, RedStone aims to provide immediate liquidity while transferring the delayed redemption risk to liquidity providers who step in to buy positions.

In RedStone’s framing, Settle lets liquidity providers purchase positions during a liquidation, supplying on-chain liquidity to the lending protocol and accepting the underlying asset’s longer redemption horizon. If successful, the approach could convert a substantial swath of idle tokenized RWAs—RedStone cites “more than $30 billion” currently sitting on the sidelines in DeFi—into usable collateral, potentially enabling more efficient borrowing against yield-generating positions.

The broader context for this development mirrors the growing but uneven progress of RWAs in crypto markets. Current estimates of tokenized RWAs—excluding stablecoins—hover around the $30 billion mark, led by exposure to U.S. Treasuries and private credit, according to data from RWA.xyz. The figures align with industry observations that a sizable portion of tokenized assets remains underutilized within DeFi, constrained by liquidity frictions and settlement timelines rather than a simple lack of demand.

Key takeaways

- RedStone Settle introduces an on-chain auction mechanism triggered by liquidation events to bridge the liquidity gap for tokenized RWAs used as collateral in DeFi lending.

- The system envisions liquidity providers stepping in to buy positions, delivering immediate liquidity while bearing the risk of delayed redemption associated with the underlying RWAs.

- RedStone claims the approach could unlock more than $30 billion of tokenized RWAs currently idle in DeFi, aligning with broader market estimates for tokenized real-world assets not including stablecoins.

- Industry voices caution that tokenization alone does not guarantee liquidity; a Paris Blockchain Week panel highlighted the persistence of liquidity and settlement constraints, underscoring the need for robust mechanisms beyond mere tokenization.

- DeFi lending activity continues to rise, with institutional interest and RWAs as collateral contributing to a 72% year-over-year expansion through September, according to Binance Research via a TradingView report.

How RedStone Settle works and why it matters

At the core, RedStone Settle is a specialized settlement layer intended to unlock collateral potential for RWAs within DeFi lending protocols. When a loan or position is tested against risk parameters and approaches liquidation, an on-chain auction is triggered. Liquidity providers can participate by purchasing the position, thereby supplying immediate liquidity to the protocol. In exchange, these providers assume the delayed redemption risk tied to the underlying RWA asset. By internalizing this risk and aligning it with a structured on-chain auction, RedStone aims to minimize abrupt liquidations while preserving the utility of RWAs as collateral.

RedStone’s framework is designed to address the fundamental mismatch between the fast-moving cadence of DeFi risk management and the slower, real-world settlement cycles that characterize tokenized assets. If liquidity providers can efficiently bridge the gap during liquidations, borrowing against RWAs could become more practical for lenders and more attractive for borrowers seeking to leverage yield-generating positions. The emphasis on an on-chain auction mechanism also offers a transparent, auditable pathway for price discovery and settlement, which could help reduce counterparty risk during stressed market conditions.

Industry observers note that even with tokenized assets, the liquidity story is not uniformly compelling. The emergence of Settle comes as part of a broader debate about the liquidity implications of tokenization. A Paris Blockchain Week panel, which Cointelegraph covered, featured voices arguing that simply tokenizing illiquid assets does not automatically render them tradable or readily usable in financial markets. The panel underscored ongoing liquidity and settlement constraints that persist despite on-chain representations of real-world assets.

“I think there’s still this idea that tokenizing something illiquid will somehow magically make it a liquid asset, which is just not true,” said Oya Celiktemur of Ondo Finance during a Paris Blockchain Week panel hosted by Cointelegraph.

These observations help frame RedStone Settle as a targeted attempt to resolve a specific friction point—improving liquidity access during forced liquidations—rather than claiming tokenization alone will solve all liquidity challenges. The approach could complement existing collateral frameworks by creating a credible on-chain pathway for RWAs to participate in DeFi lending markets even when redemption cycles lag behind lenders’ risk-management timelines.

RWA liquidity, market size, and adoption dynamics

RedStone’s projections sit within a landscape where tokenized RWAs are steadily growing in visibility and ambition, even as liquidity remains uneven. Data from RWA.xyz indicates a market worth north of $30 billion when stablecoins are excluded, with the largest segments concentrated in U.S. Treasury exposure and private credit. These assets reflect a broad appetite among traditional issuers and investors to tokenize real-world cash flows, while DeFi protocols seek durable, yield-generating collateral beyond crypto-native instruments.

Industry commentary during Paris Blockchain Week adds another dimension to the debate. Tokenization, while enabling on-chain representation of RWAs, does not automatically unlock tradability or deep liquidity across markets. Liquidity providers, market makers, and risk underwriters must still navigate custody, settlement, and regulatory considerations that govern real-world assets, even when they are tokenized. The discourse highlights why new settlement mechanisms—like Settle—are essential to translating tokenization into practical DeFi utility.

Meanwhile, DeFi lending remains buoyant, with research from Binance indicating continued growth driven in part by institutional interest in RWAs and stablecoins. The research shows a 72% year-over-year expansion in DeFi lending through September, underscoring the sector’s ongoing appetite for diversified collateral and onboarding of traditional finance players. This backdrop helps explain why RedStone is pursuing a settlement layer that could unlock additional liquidity channels for tokenized RWAs without waiting on gradual redemption schedules.

Beyond Settle, the broader ecosystem has seen related tokenization activity that signals growing experimentation with RWAs in crypto markets. For example, Flow Capital has publicly discussed plans to tokenize a $150 million private credit fund via DigiFT, illustrating how market participants are combining tokenization with institutional-grade asset classes to broaden DeFi’s collateral base. Such developments, while at different stages, collectively point to a trend toward more sophisticated ways of incorporating real-world yield into crypto lending and liquidity provision.

What changes for users, lenders, and builders

If RedStone Settle reaches meaningful adoption, several implications could emerge across the ecosystem. For lenders, the ability to collateralize tokenized RWAs more effectively could expand the universe of eligible collateral, potentially enabling larger borrowing capacity or more favorable terms for yield-oriented strategies. For liquidity providers, Settle offers a structured mechanism to deploy capital in exchange for exposure to the delayed redemption risk associated with RWAs, potentially creating new yield opportunities tied to safer liquidation outcomes.

For builders and DeFi protocols, Settle could offer a practical blueprint for integrating RWAs into lending markets without forcing a wholesale redesign of risk models. However, the approach also introduces new layers of risk—primarily around price discovery, settlement finality, custody, and regulatory compliance—that projects must model and monitor. The on-chain auction dynamic, while transparent, requires robust governance, clear settlement rules, and resilient oracle and data feeds to withstand market stress.

Regulatory and operational considerations will likely shape how quickly Settle scales. Tokenized RWAs sit at the intersection of traditional finance, asset custody, and crypto markets, where custody solutions, KYC/AML requirements, and cross-border settlement protocols often influence deployment timelines. As more institutions explore tokenized collateral, the market will be watching how on-chain settlement protocols align with existing compliance frameworks and risk management standards.

What readers should watch next

RedStone Settle represents a notable attempt to translate tokenized RWAs into practical, tradable collateral within DeFi. The coming months will reveal whether the on-chain auction mechanism can deliver the claimed liquidity lift without introducing new forms of risk or friction. Investors and developers should monitor how Settle interacts with existing lending protocols, the quality and diversity of RWAs brought into the frame, and the regulatory guidance that could shape custody, settlement, and disclosure requirements for tokenized assets used as collateral.

In the near term, the market will also weigh broader adoption signals for tokenized RWAs, including continued growth in DeFi lending, the volume and velocity of RWAs tokenized through various platforms, and the willingness of liquidity providers to engage with RWAs that carry longer redemption timelines. As industry research and independent coverage continue to dissect tokenization’s real liquidity impact, RedStone Settle adds a concrete mechanism to bridge the gap between on-chain execution and off-chain asset settlement—an issue that remains central to unlocking RWAs’ full potential in DeFi.

As the ecosystem tests Settle’s value proposition, market participants will closely observe the balance between immediate liquidity during liquidations and the risk transfer to providers. The outcome could influence future designs for DeFi primitives seeking to incorporate real-world yields, shaping the trajectory of RWAs in crypto markets in the months ahead.

Further reading and related coverage include Flow Capital’s tokenization plan for a private credit fund via DigiFT, as reported by Cointelegraph, and analyses of liquidity dynamics around tokenized assets presented at Paris Blockchain Week. For background on market sizing, RWA.xyz provides ongoing data on the scale and composition of tokenized RWAs beyond stablecoins.

Institutional crypto allocation depends on a small group of firms producing ratings, risk scores, and benchmark rates. These firms provide the evaluative layer behind capital decisions.

Best Digital Asset Ratings & Analytics Provider is an award category within The BeInCrypto Institutional 100, an annual research-driven program recognising institutional digital asset excellence across 26 categories and six pillars.

This category sits in Pillar 2: Capital Markets & Infrastructure. The 15 firms below are its longlist. A shortlist will be named in May 2026, and the winner will be announced at Proof of Talk in Paris on June 2–3, 2026.

- Longlist: 15 firms, covering traditional credit rating agencies, specialist benchmark and stablecoin raters, blockchain intelligence with risk scoring, DeFi risk managers and credit raters, and security-and-ratings hybrids

- Candidates screened: Starting pool of more than 30 ratings and analytics providers across the institutional digital asset stack; 15 advanced to this longlist, with 5 additional firms held in the outreach pool

- Scoring (Track C): Editorial quantitative 20%, Expert Council 80%

- Criteria assessed: Coverage and scale, methodological discipline, institutional adoption, regulatory standing, on-chain integration, track record, and market impact

- Sources: Regulator filings (SEC NRSRO register, ESMA CRA register, EU BMR registry, IOSCO compliance statements), firm-published methodologies, oracle integration disclosures, audited financial filings, and private-market data platforms including PitchBook, Tracxn, and Crunchbase, supplemented by mainstream financial press

| # | Firm | Sub-Segment | HQ | Scale Signal | Core Ratings Product | Representative Work |

|---|---|---|---|---|---|---|

| 1 | Moody’s Ratings | TradFi CRA | New York / London | NRSRO and ESMA registered 20+ stablecoins covered |

Stablecoin ratings, DAM, DIRA | Stablecoin methodology launched (2026) Canton Network node enables on-chain access |

| 2 | S&P Global Ratings | TradFi CRA | New York | NRSRO and ESMA registered 10 stablecoins on SSA scale |

Stablecoin assessments, indices | Chainlink DataLink integration (2025) On-chain ratings via Base network |

| 3 | Fitch Ratings | TradFi CRA | New York / London | NRSRO registered Active digital asset research |

Credit research, stablecoin risk | Institutional risk coverage across crypto exposure Referenced in DeFi lending analysis |

| 4 | Chainalysis | Blockchain Intelligence | New York | $8.6B valuation 1,500+ institutional clients |

KYT risk scoring, investigations | Industry benchmark for transaction risk scoring Integration with on-chain compliance systems |

| 5 | TRM Labs | Blockchain Intelligence | San Francisco | $1B valuation (2026) $300M+ assets frozen |

Risk scoring, transaction monitoring | Dynamic risk scoring engine T3 Financial Crimes Unit partnership |

| 6 | Elliptic | Blockchain Intelligence | London | 1,100+ networks tracked 2B+ labeled addresses |

Risk analytics, screening tools | Stablecoin issuer due diligence framework Cross-chain analytics coverage |

| 7 | Kaiko | Benchmark Administrator | Paris | EU BMR registered Clients include CBOE, Gemini |

Reference rates, indices | Regulated crypto benchmark rates On-chain rate publishing via oracles |

| 8 | Bluechip | Stablecoin Rater | United States | SMIDGE rating framework A+ to F scale |

Stablecoin safety ratings | Independent stablecoin grading system Public ratings across major issuers |

| 9 | Particula | Tokenization Rater | Berlin | 200+ risk assessments On-chain scoring across networks |

Digital Asset Risk Passport | PDARP launched (2026) Programmable on-chain risk scores |

| 10 | Gauntlet | DeFi Risk Manager | New York | $1B valuation Compound engagement through 2026 |

Risk modeling, parameter tuning | DeFi risk parameter frameworks Institutional yield strategy curation |

| 11 | Chaos Labs | DeFi Risk Manager | US / Israel | Multi-protocol coverage Aave engagement ended 2026 |

Risk-aware oracle systems | Chaos Oracles risk-aware feeds Protocol-level risk simulations |

| 12 | LlamaRisk | DeFi Risk Manager | Decentralized | Aave primary risk provider Ethena committee member |

Risk assessments, NAV oracle | LlamaGuard NAV for RWAs Expanded Aave risk coverage |

| 13 | Credora (RedStone) | DeFi Credit Rater | Global | Live on Morpho, Spark Oracle-integrated ratings |

Credit scoring, risk analytics | Default-probability rating system Integrated oracle + rating infrastructure |

| 14 | Exponential.fi | DeFi Rating Platform | United States | A–F rating framework Published methodology |

Pool-level risk ratings | DeFi pool risk scoring model Composability-based risk framework |

| 15 | CertiK | Security + Ratings | New York | 5,500+ audits completed $300B+ assets secured |

Skynet Score, audits, monitoring | Real-time project risk scoring Cross-chain evaluation system |

About This List

The BeInCrypto Institutional 100 — Ratings & Analytics (2026 Long List) identifies firms whose core output is evaluative: ratings, risk scores, benchmark rates, and credit assessments used by institutions when allocating capital in digital assets.

Methodology

This category is evaluated under Track C of the BIC 100 methodology: 20% quantitative metrics and 80% Expert Council scoring.

Assessment spans six criteria: coverage and scale, methodological rigor, institutional adoption, regulatory standing, on-chain integration, and market impact.

Data was verified using regulatory registers, firm methodologies, and private-market sources including PitchBook and Tracxn. Figures reflect the most recent available data at publication.

The post BeInCrypto Institutional Research: 15 Firms Rating Digital Asset Risk for Investors appeared first on BeInCrypto.

Imagine a tireless analyst who works around the clock, cross-referencing a company’s onchain purchasing patterns with satellite imagery of its warehouses, correlating its job postings with its patent filings, and mapping its entire supply chain by watching the flow of smart contract payments. This analyst never sleeps, never loses focus and costs almost nothing to run.

That analyst is coming. It’s an AI agent, and your competition will have one.

The rush to build agentic commerce is well underway. The combination of decision-making AI with smart contracts on blockchains is genuinely powerful. Consumer-facing agents will go bargain hunting and close deals autonomously. Enterprise agents will forecast demand and execute procurement at scale through onchain contracts. The efficiency gains are enormous.

But this technology works in both directions. The same infrastructure that lets an enterprise agent negotiate better deals also broadcasts a remarkable amount of information about how that enterprise operates. Public blockchains have no native privacy. And “security by obscurity” — the hope that nobody will bother to piece together all those scattered data points — collapses completely when automated agents can spend their nights reverse-engineering a competitor’s operations, for pennies.

This is not new. It is about to get much, much faster.

Companies have always leaked intelligence. iFixit has built a business around tearing apart every major new electronics product within days of launch, exposing components, likely bill-of-materials costs, and manufacturing approaches for anyone to study. Satellite imagery firms already track everything from warehouse activity to crop yields to oil tanker movements, selling the insights to hedge funds and competitors alike. Specialized competitive intelligence firms have long mapped supply chains and reverse-engineered pricing strategies.

What’s different now is the synthesis. Each of these data streams, taken alone, tells a partial story. An agentic system can pull them all together — public filings, onchain transaction flows, satellite data, job postings, patent applications, shipping records — and deliver not just raw data about your competition but a coherent picture of their strategic road map, updated continuously.

The question this forces is not whether competitors will know more. They will. The question is: what should companies do about it?

Start by admitting what was never really secret

The first step is a clear-eyed audit, from first principles, of what needs to be confidential — because sensitive information is not always treated as such.

Take business strategy. Companies have to tell shareholders so they’ll buy the stock. They have to tell employees so they’ll pull in the same direction. They need to tell partners so they’ll invest alongside them. And once they’ve told all those audiences, they’ve effectively told the competition too. Strategy has not been a real secret for a long time.

The best companies already know this. Apple doesn’t hide that it’s building an ecosystem play. Amazon doesn’t disguise its obsession with logistics efficiency. They don’t win by surprise. They win by execution.

And even execution, at a high level, is more transparent than most people admit. Anyone can walk into a Walmart store and catalog every product on the shelves. Anyone can unscrew the back of any piece of electronics and identify every component. Any analyst can read the 10-K and map out the cost structure.

What’s genuinely left to protect

Strip away strategy, strip away the broad strokes of execution, and what remains is operational detail. Not what components are in a product, but what the company is paying for them. Not that a company has a supply chain, but the specific terms, conditions, volume commitments, and quality management processes that make one supply chain faster or cheaper than the next. The granular, day-to-day mechanics of how the machine actually runs.

This is the data that creates a durable competitive advantage. And in an era of agentic commerce, it’s precisely the data most at risk — because it’s flowing through the same blockchain infrastructure that agents use to transact.

The privacy imperative

If enterprise agents are executing procurement contracts, managing supplier relationships, and orchestrating logistics on public blockchains without privacy, those enterprises are broadcasting their operational playbook to every competitor running an analytical agent. The very system designed to drive efficiency becomes the system that strips away the competitive moat.

The answer isn’t to avoid blockchains — the efficiency and automation benefits are too significant. The answer is to demand privacy as foundational infrastructure, built in from the start, not bolted on as an afterthought.

And the rethinking won’t stop at blockchain transactions. Enterprises will need to examine every digital touchpoint — email metadata, web server configurations, government disclosures, DNS records — with fresh eyes, asking not “could someone find this?” but “what could an agent synthesize from this combined with everything else it knows?”

The new competitive landscape

The world is entering an era where the floor of competitive intelligence rises dramatically for everyone. Agents will make the kind of analysis that once required dedicated teams and significant budgets available to any company willing to deploy them.

The companies that will thrive aren’t the ones that try to hide everything — that’s a losing game. They’re the ones that will clearly distinguish between what can’t be secret (strategy, product design, market positioning) and what must be (operational mechanics, pricing terms, supplier relationships), and then invest seriously in the infrastructure to protect what matters.

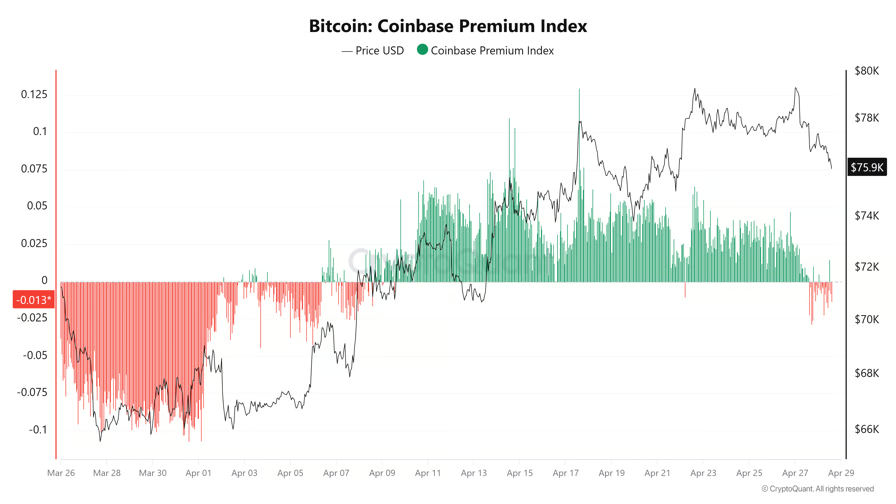

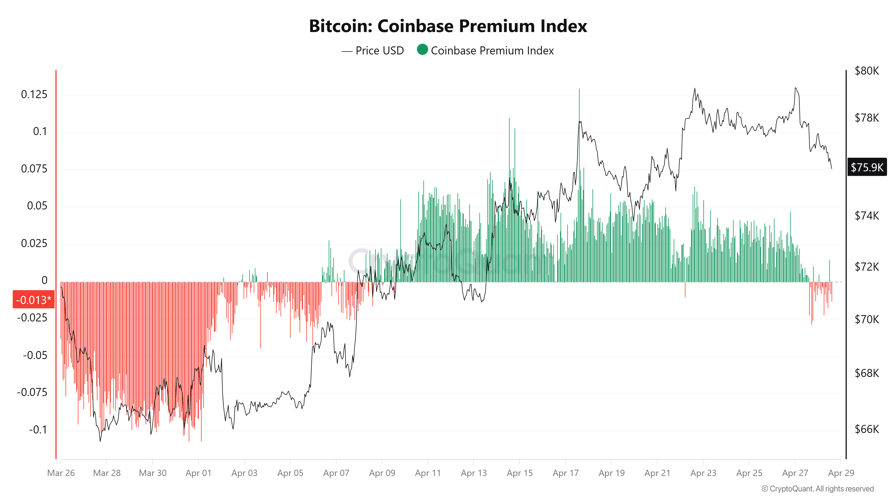

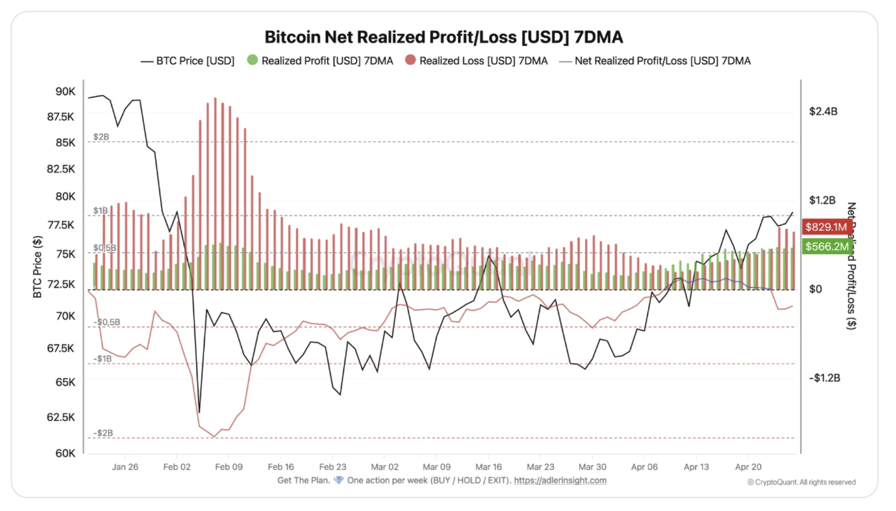

Bitcoin’s (BTC) Coinbase Premium Index has turned negative at -0.008 for the first time in three weeks, signaling a sharp reduction in US spot market demand and aligning with BTC’s current price drop. The signal held across hourly readings through the next 48 hours, showing consistent selling pressure from US-based buyers. The shift comes as the net weekly average of BTC realized losses climbed to $829 million, suggesting reduced investor conviction.

Bitcoin Coinbase Premium Index. Source: CryptoQuant

Crypto trader Ardi highlighted a break in both trendline support and the $77,300 liquidity zone. The trader linked the move to weakening spot demand, noting that the premium has posted consecutive red readings for the first time since BTC was near $67,000.

Ardi said that price action during the Federal Open Market Committee (FOMC) meeting window could remain volatile, with rapid moves in either direction. Traders could place focus on the $74,500–$75,500 range as a key downside area tied to demand exhaustion.

Onchain data adds to this view. Crypto analyst Darkfost noted that the weekly realized losses reached $829 million on a seven-day average, compared to $566 million in realized profits. The net realized profit briefly turned positive on April 9, then reversed within two weeks.

Bitcoin net realized profit/loss [USD] 7DMA. Source: CryptoQuant

The share of supply in profit stands at 64%, a level that has not historically supported sustained upside. This indicates weaker conviction among holders despite the recent rebound.

Related: Bitcoin price hits one-week low as $100 oil sparks fresh Asia crisis fears

Bitcoin sell volumes at Binance reach $828 million

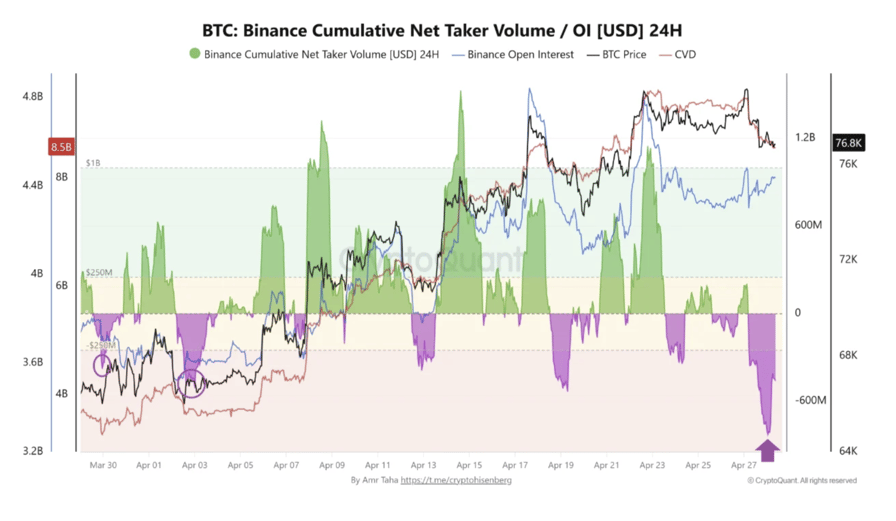

Derivatives data shows strong sell-side activity on Binance. Crypto analyst Amr Taha noted that the 24-hour cumulative net taker volume dropped by $828 million on April 27, the lowest reading since late March.

BTC cumulative net taker volume on Binance. Source: CryptoQuant

Negative net taker volume indicates that the market’s sell orders exceed its buy orders. The Binance taker buy/sell ratio has also fallen to 0.89, a level last recorded on March 29.

That earlier reading aligned with a local pivot when Bitcoin tested $66,000, then recovered by 15% over the past 30 days.

The current readings place both metrics back near prior exhaustion zones. Taha described the setup as closer to a short-term capitulation than a larger trend breakdown.

Related: Can Bitcoin hit $250K this year? Traders say it may be time to ‘sell in May’

Crypto World

XRP Price Outlook: How Bank Adoption and Token Scarcity Could Drive Long-Term Value Growth

TLDR:

- Banks integrating Ripple’s DLT are expected to grow XRP Ledger transaction volumes massively over time.

- Payment providers like Finastra and Volante are adding transaction volume through XRPL’s Cross-Currency RTGS functions.

- XRP cannot be mined and a portion is burned per transaction, meaning circulating supply will keep falling.

- XRP targets the $180 trillion international payments market, positioning it as a top bridging currency asset.

XRP is drawing renewed attention from the crypto community as Ripple’s distributed ledger technology gains traction among global banks.

Analysts and long-time observers point to a combination of rising network adoption, a shrinking token supply, and a massive addressable market.

Together, these factors are expected to push XRP toward higher and more stable valuations over time. The case being made is straightforward and grounded in market mechanics.

Banking Adoption and Payment Providers Fuel XRP Network Activity

As more banks integrate Ripple’s distributed ledger solution, transaction volumes across the network are expected to grow.

Each new institutional participant adds meaningful activity to the XRP Ledger. This growing participation directly increases the utility of XRP as a functional asset.

Payment service providers are also entering the picture. Companies like Finastra, Volante, and CGI are tapping into the XRPL’s Cross-Currency RTGS functions.

They are also using the Neutral Liquidity Marketplace that the XRP Ledger provides. This adds another significant layer of transaction volume on top of banking activity.

A recent post from crypto commentator SMQKE on X laid out the case clearly. The post stated that “the transaction volumes of the network will grow massively” as banks and payment providers deepen their integration with Ripple’s infrastructure. More network activity directly translates to greater XRP utility.

Greater utility, in turn, supports a stronger case for price appreciation. This is not speculative reasoning. It follows a basic supply-and-demand framework that has held across multiple asset classes over time.

Decreasing Supply and a $180 Trillion Market Position XRP for Long-Term Value

XRP cannot be mined, which makes its supply dynamics fundamentally different from Bitcoin and similar assets. A small amount of XRP is permanently burned with every transaction processed on the ledger. Over time, this means the circulating supply will only continue to fall.

As the SMQKE post noted, “everything that exists in a limited amount and is actively used is becoming more expensive.”

This principle applies directly to XRP as network usage climbs. A shrinking supply base against rising demand creates natural upward pressure on price.

The addressable market adds further weight to this outlook. XRP is positioned to serve international funds transfers, a market with an annual volume of $180 trillion.

Even a fraction of that volume flowing through the XRP Ledger would represent enormous demand for the token.

On the question of price volatility, Ripple has addressed this directly. The company expects volatility to ease as demand becomes more constant.

A steady flow of transactions using XRP as a bridging currency is expected to support price stability over time.

Crypto World

A crypto coalition releases technical proposal to save Aave users from a massive token exploit

A $300 million hole doesn’t usually come with a neat repair manual. This time, the group spearheading the Kelp DAO recovery effort is trying to write one.

DeFi United, a coalition of multiple blockchain projects and crypto ecosystem individuals, has laid out a detailed, step-by-step plan to restore the backing of rsETH after this month’s Kelp DAO hack sent shockwaves through DeFi lending markets, releasing more than 116,000 tokens that weren’t properly accounted for.

The proposal, circulated on Aave’s official X account, reads like a coordinated cleanup operation, one that leans heavily on Aave’s infrastructure to unwind the damage and get markets back on a stable footing.

The incident traces back to April 18, when an attacker exploited a vulnerability in rsETH’s bridge. By forging a message that appeared legitimate, the attacker tricked the Ethereum side of the system into releasing 116,500 rsETH, making the system believe the funds had moved when they hadn’t, allowing a large batch of rsETH to be created without backing.

Those tokens didn’t just sit idle. They were spread across multiple wallets and deployed across DeFi, with a significant portion used as collateral on Aave and other lending platforms.

That’s where the problem became systemic: protocols like Aave suddenly found themselves holding collateral that, at least temporarily, wasn’t fully backed.

According to the proposal, most of the exploited funds are still in play. Roughly 107,000 of the original 116,500 rsETH remain tied up in active positions across Aave and Compound.

That leaves two problems to solve at once: restoring the actual backing of rsETH itself, and unwinding the loans created using those extra tokens.

DeFi United’s proposal aims to tackle both sides of that equation simultaneously.

On the backing side, the group says it has already lined up enough ETH commitments to fully re-collateralize rsETH. The plan is to feed that ETH back into the system in stages, converting it to rsETH and depositing it back into the system so the token is once again fully backed.

At the same time, attention shifts to the lending markets where the damage is most visible.

Instead of letting things play out chaotically, the plan is to step in and carefully unwind the mess.

A big part of that involves dealing with the positions the attacker opened on Aave. These are essentially loans backed by rsETH that shouldn’t have existed in the first place. Rather than waiting for those loans to collapse on their own — which could cause more market disruption — the proposal suggests nudging the system so they can be closed out in a more controlled way.

In practice, temporarily adjusting how rsETH is valued inside the system will enable those bad positions to be liquidated or closed more smoothly. As those positions are unwound, the underlying assets (like ETH) can be recovered. The proposal estimates this could free up around 13,000 ETH from Aave alone.

Once that collateral is back in hand, it gets converted into ETH and used to cover the shortfall created by the exploit — essentially filling the hole left behind.

The process isn’t risk-free. It hinges on governance approvals across multiple chains, the successful deployment of committed funds and a smooth execution of the unwind.

Still, the plan reflects a more coordinated response than DeFi has often managed previously. If executed as intended, the end goal is straightforward: “rsETH backing is fully restored, and all affected markets are stabilized,” as the proposal says.

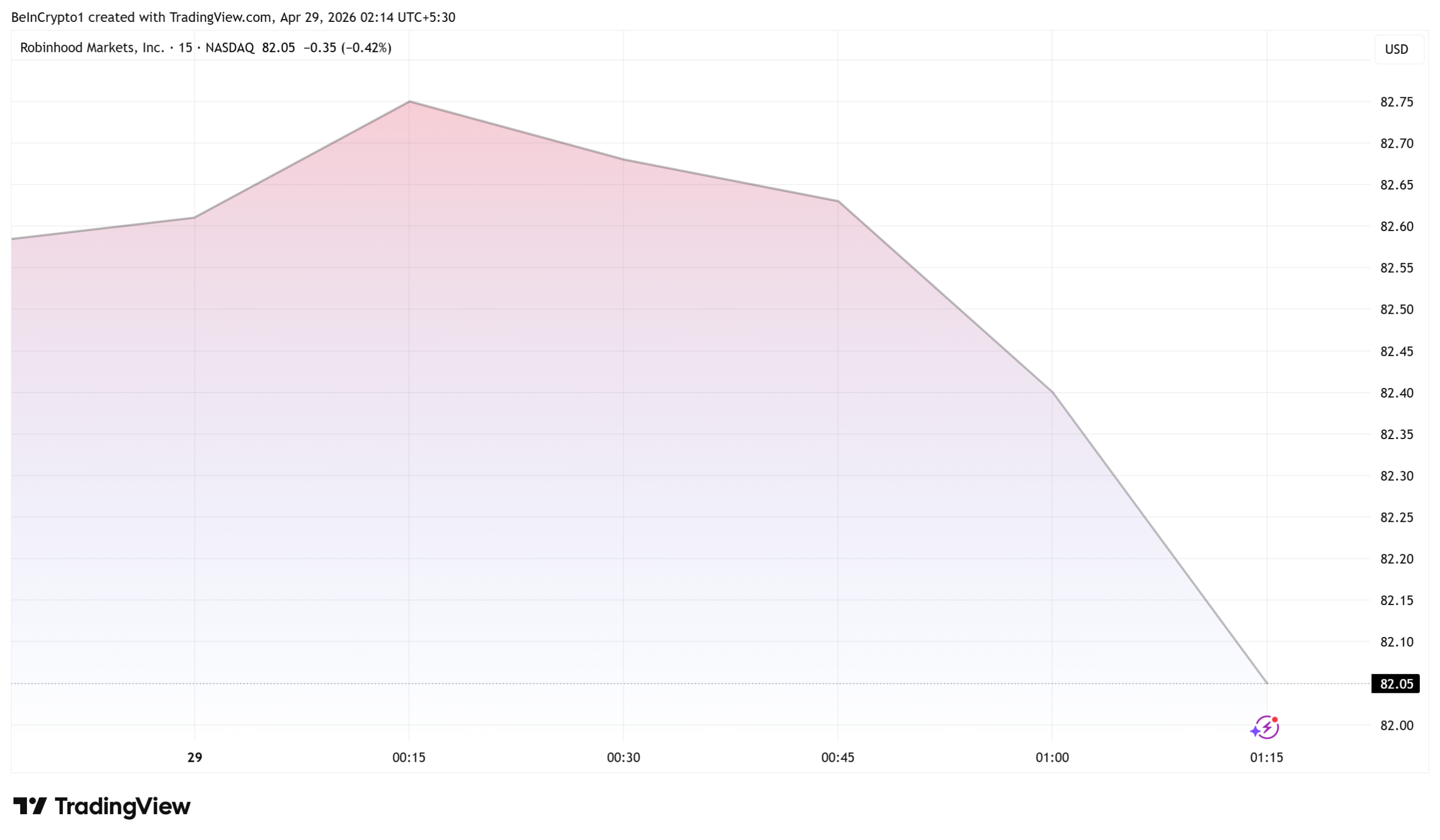

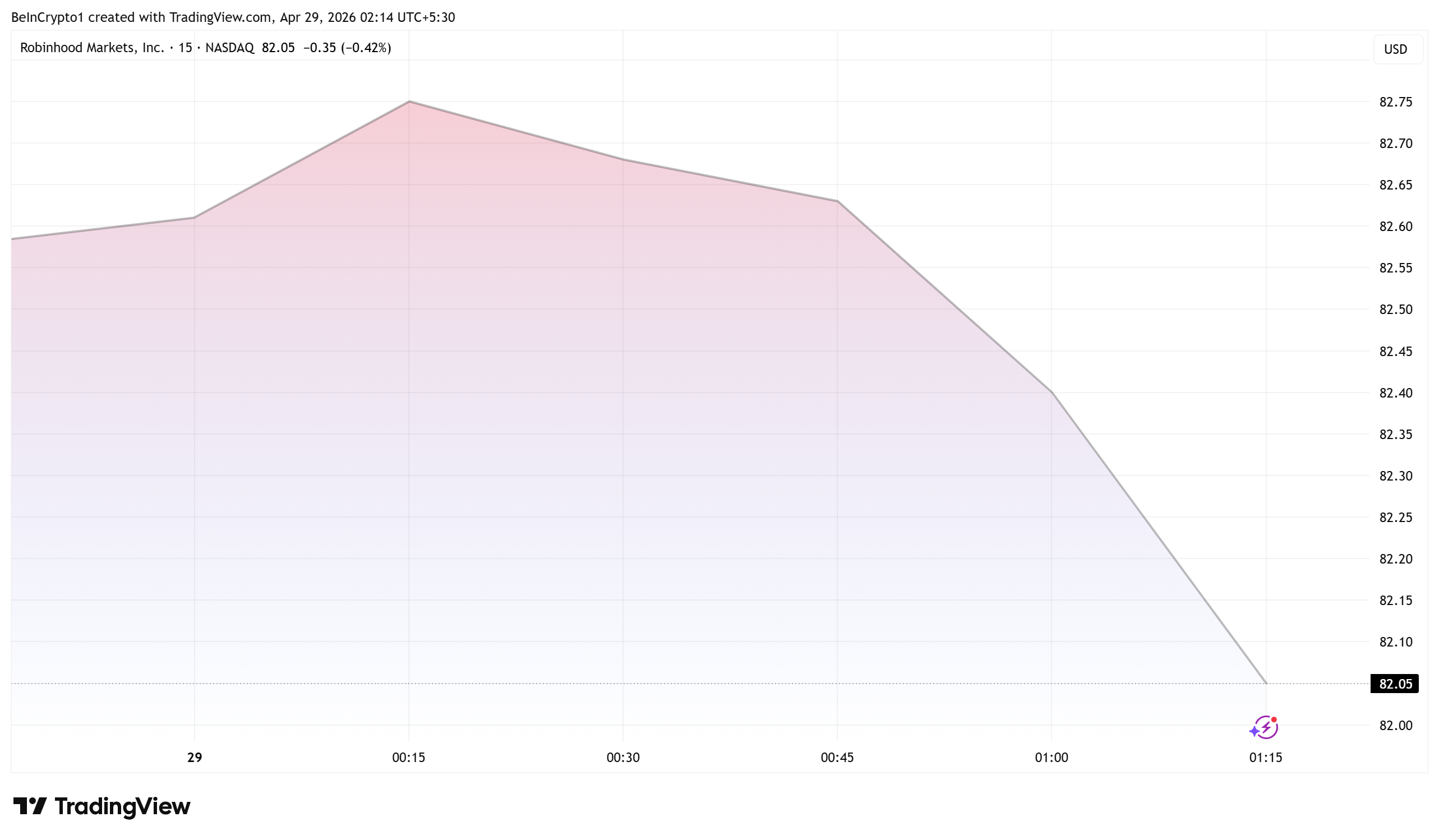

Robinhood Markets shares slipped about 6% in after-hours trading Tuesday after the retail brokerage reported a 47% year-over-year drop in cryptocurrency revenue, dragging overall first-quarter results below Wall Street expectations.

The Menlo Park firm posted $346 million in first-quarter profit, or $0.38 per diluted share, narrowly missing analyst estimates of $0.39 even as net income rose 3% from a year earlier.

Crypto Revenue Slides as Bitcoin Cools

Crypto transactions generated $134 million in revenue during the quarter, down 47% year-over-year as digital asset trading activity cooled across the platform.

Total revenue reached $1.07 billion, up 15% year-over-year but short of the $1.14 billion analysts had projected. The miss arrived even as equities, options, futures, and prediction markets posted double-digit growth or record volumes, the company said.

Trading fees drove much of the platform’s gains last year, when HOOD stock peaked at $153.86 in October alongside crypto’s broader run.

Robinhood stock dipped on this report, and was trading for $82.05 as of this writing.

Prediction Markets and Tokenization Cushion the Slide

Chairman and CEO Vlad Tenev pointed to the firm’s expanding role across customer finances in a statement.

“Robinhood is increasingly positioned at the center of our customers’ financial lives,” he stated in the broadcast.

Wagers routed through Kalshi-powered prediction markets logged record volumes, supported by a one-cent transaction fee.

Robinhood also launched the public testnet for Robinhood Chain, an Ethereum (ETH) layer-2 network built around tokenized assets.

Total platform assets stood at $307 billion, up 39% year-over-year on the back of net deposits and higher equity valuations.

The firm’s European tokenized stocks product continues to offer customers exposure to private companies including OpenAI and SpaceX.

The after-hours sell-off pushed HOOD to roughly $82, well off the October peak. The path forward depends on whether prediction markets and tokenization can offset the cooling in digital asset trading.

The post HOOD Stock Topples After Robinhood Earnings Reveals 47% Decrease in Crypto Revenue appeared first on BeInCrypto.

OpenAI Really Wants Codex to Shut Up About Goblins

Five takeaways from the King’s historic address to US Congress

Ken Griffin slams NYC Mayor Mamdani over ‘personal attack’

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Tech1 day ago

Tech1 day agoRegister Renaming | Hackaday

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread – Corporette.com

-

Crypto World3 days ago

Hyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Politics6 days ago

Politics6 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics6 days ago

Politics6 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Business5 days ago

Business5 days agoPatterson-UTI Energy, Inc. (PTEN) Q1 2026 Earnings Call Transcript

-

Business7 days ago

Business7 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Sports2 days ago

Sports2 days agoIPL 2026: Ruturaj Gaikwad registers slowest fifty of the season, enters all-time unwanted list | Cricket News

-

Politics1 day ago

Politics1 day agoDrax board avoid their own AGM, accused of greenwashing & environmental racism

-

Politics6 days ago

Politics6 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Politics6 days ago

Politics6 days agoZack Polanski responds to home secretary’s taser threat

-

Politics6 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Politics6 days ago

Politics6 days ago‘Iran is still a nuclear threat’

-

Business7 days ago

Business7 days agoHCL Tech share price tank over 9% after weak Q4. JPMorgan, HSBC & 3 others cut target price

-

NewsBeat3 days ago

NewsBeat3 days agoLK Bennett closes all stores after entering administration

-

Sports6 days ago

Sports6 days agoTim Bradley names the current best in the world: “Better than Inoue and Usyk”

-

Crypto World5 days ago

Crypto World5 days agoMichael Saylor says BTC winter is over. Market analyst disagrees, says bitcoin was in a pullback

-

Crypto World7 days ago

Crypto World7 days agoEthereum Price News: ETH Flashes a Bullish Setup No Holder Should Miss While Pepeto Nears Its Binance Listing

-

Business7 days ago

Business7 days agoThe Job Benefits Most Men Don’t Know to Negotiate

-

Business6 days ago

Altimmune prices $225 million public offering at $3 per share

You must be logged in to post a comment Login