Crypto World

CME Sues the CFTC Challenging Crypto Perpetual Futures Rules

The Chicago Mercantile Exchange (CME) Group has filed a lawsuit in federal court challenging the U.S. Commodity Futures Trading Commission (CFTC) over its approvals of cryptocurrency-linked perpetual futures. The complaint, submitted to the U.S. District Court for the District of Columbia, targets the CFTC, its chair Michael Selig, and asks the court to vacate the agency’s actions.

The case highlights an expanding regulatory dispute over how U.S. derivatives rules apply to crypto products that do not fit neatly into traditional futures structures. For crypto exchanges, broker-dealers, market operators, and institutional investors, the outcome could affect product design, compliance expectations, and supervisory oversight of crypto derivatives—particularly where regulatory interpretations hinge on whether a contract is treated as a “futures” product or as a “swap” under the Commodity Exchange Act (CEA).

Key takeaways

- CME filed a D.C. federal lawsuit against the CFTC and chair Michael Selig relating to the agency’s approval of crypto perpetual futures tied to Bitcoin spot prices.

- The complaint centers on a CFTC notice dated May 29 involving Kalshi prediction market products and a no-action position for similar products involving Coinbase.

- CME alleges the CFTC improperly applied the CEA by effectively treating “futures” as “swaps” with expiration dates, and argues Selig acted without a full five-commissioner panel.

- The CFTC, through a spokesperson, rejected the claims as “frivolous” and characterized CME’s litigation approach as “lawfare.”

CME’s lawsuit challenges CFTC approvals for crypto perpetual futures

In its Thursday filing, CME sought judicial review of CFTC actions approving certain perpetual futures contracts linked to Bitcoin’s spot price. The dispute traces back to a May 29 CFTC notice that (1) approved perpetual futures contracts tied to Bitcoin for Kalshi, a platform operating prediction markets, and (2) issued a “no-action” position for similar perpetual products referenced in connection with Coinbase.

CME’s complaint argues that the CFTC’s approach conflicts with directives from Congress, particularly by treating “futures” as “swaps” for purposes of regulatory classification. Under CME’s theory, the classification matters because it determines which statutory and regulatory requirements apply to the relevant derivatives framework.

Beyond the substantive challenge, CME also raised procedural concerns. The exchange contends that Selig acted unilaterally rather than through a full panel of five CFTC commissioners, implying that the agency’s internal governance or decision-making process was not properly followed for the actions at issue.

“With one stroke of his pen, [Selig] overrode Congress’s definition of the term ‘swap’ and circumvented the regulatory regime Congress required for that form of derivative.”

CME further asserted that the CFTC’s handling of these approvals could harm competition and destabilize derivatives markets, arguing the agency failed to apply the CEA consistently and evenly.

Congress, contract classification, and why the dispute matters

At the core of CME’s legal argument is the classification of perpetual futures contracts—contracts that, in typical market practice, can be designed to trade without a fixed expiration date, while still resembling derivative instruments whose regulatory treatment depends on statutory definitions.

From a compliance standpoint, how a product is categorized can determine whether market participants must register, seek approvals, adopt particular operational controls, and comply with specific surveillance or reporting expectations under U.S. derivatives oversight. The lawsuit therefore sits at the intersection of contract engineering and statutory interpretation: market operators and intermediaries may need clarity on whether certain crypto-linked “perpetual” structures fit within futures frameworks or instead trigger swap-like regulatory pathways.

The broader institutional issue is that perpetual crypto derivatives have increasingly blurred lines between legacy derivative categories. That raises practical uncertainty for exchanges and clearing entities, and it can create compliance friction for financial institutions that must meet regulatory expectations for eligible contract types and risk controls. In that context, CME’s challenge is not merely a technical disagreement: it is aimed at shaping the legal boundaries that govern future approvals and market access.

Selig’s position and the CFTC’s response

The dispute escalated publicly shortly before CME’s filing. One day earlier, CME CEO Terrence Duffy said the exchange operator would take legal action against the CFTC. In a subsequent interview, Selig maintained that perpetual futures contracts “trade very similarly” to other derivatives and argued that the CEA does not define the term “futures contract.”

The CFTC rejected CME’s complaint. A CFTC spokesperson told Cointelegraph that CME had engaged in “lawfare” against the agency and the administration’s broader crypto policy approach, characterizing the lawsuit as “frivolous.” The exchange’s response, in turn, underscores a high-stakes policy conflict: if courts accept CME’s reading, it could compel the agency to revisit approvals tied to its prior interpretive stance and potentially adjust how it evaluates similar applications or regulatory notices.

CFTC leadership structure and timing: a procedural and policy flashpoint

CFTC chair Michael Selig was confirmed by the U.S. Senate in December 2025 and, as of the time of CME’s filing, remains the chair and sole commissioner in a leadership panel intended to include five commissioners. The lawsuit comes amid uncertainty about whether the CFTC’s full bipartisan composition will be restored in time for complex contested decisions—an issue that CME highlights through its allegation that Selig acted without a complete panel.

Political context also matters for the regulatory process. As of Thursday, President Donald Trump had not announced nominations to fill the CFTC seats, despite calls from members of Congress to do so. That governance vacuum can become consequential when markets depend on consistent, multi-member commission decision-making for contested interpretations of the CEA.

The dispute also arrives as crypto perpetual derivatives are proliferating across U.S. venues and regulated infrastructure. For example, Kraken announced it would offer perpetual futures to U.S. users through a CFTC-regulated platform, Bitnomial. While that development is separate from CME’s lawsuit, it reflects the practical stakes of regulatory clarity: product expansion continues, but the legal foundations supporting classification and approval pathways are actively contested.

What to watch next

Courts will determine whether CME’s claims succeed on statutory interpretation and whether the challenged approvals can stand procedurally under the CFTC’s decision-making requirements. For market participants, the most immediate watchpoints are how the court frames the futures-versus-swaps classification issue and whether the CFTC revises its approach to approvals of crypto perpetual derivatives pending the litigation’s outcome.

US financial regulators have proposed customer identification rules for stablecoin issuers, aiming to align identity verification practices with requirements applied to banks and other covered financial institutions under federal law. The initiative, issued by multiple agencies, is part of the broader implementation framework for the GENIUS Act, a stablecoin-focused statute enacted in July 2025.

The proposal would require stablecoin issuers to perform “customer identification” in connection with onboarding and account access, alongside related recordkeeping and screening obligations tied to the Bank Secrecy Act (BSA). For regulated firms, the move signals an expectation that stablecoin-related activities will be treated within established AML/CFT compliance structures—raising practical questions around supervision, data handling, and how identity requirements apply across different stablecoin business models.

Key takeaways

- US agencies have issued a proposed rule that would require stablecoin issuers to implement customer identification procedures comparable to those used by banks under the BSA.

- The proposal is positioned as part of the GENIUS Act implementation process and is intended to address AML/CFT obligations for stablecoin providers.

- The notice will be open for public comment for 60 days after formal filing in the Federal Register.

- Regulators cite baseline BSA standards including identity verification, retention of identity information, and screening for potential terrorist affiliations.

- Treasury has already issued related GENIUS proposals on illicit-finance requirements, indicating a multi-agency rulemaking path for stablecoin compliance.

Proposed customer identification requirements under GENIUS

According to the agencies’ notice, the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve, the Office of the Comptroller of the Currency (OCC), the National Credit Union Administration (NCUA), and the US Treasury’s Financial Crimes Enforcement Network (FinCEN) jointly proposed that stablecoin issuers be treated as regulated financial institutions for purposes of verifying customer identity.

The action is linked to the GENIUS Act’s implementation timeline. The law is expected to enter effect 18 months after enactment or 120 days after federal authorities finalize implementing regulations, depending on the administrative schedule for the rulemaking process. In practical terms, the proposal represents regulators translating statutory obligations into operational compliance expectations for stablecoin issuers.

The agencies stated the proposal is designed to meet AML and Countering the Financing of Terrorism (CFT) requirements through GENIUS. In the BSA framework, covered financial institutions are generally expected to verify the identity of a person seeking to open an account, maintain records of identity information, and apply risk-based determinations that include whether the person may be associated with terrorism or terrorist organizations.

For institutional stakeholders, the significance lies in how customer identity and onboarding procedures can affect both compliance operations and product design. Identity verification requirements may necessitate enhanced onboarding controls, clearer definitions of “customer” and “account” for stablecoin use, and more robust governance over identity data retention, access controls, and audit trails.

How the Bank Secrecy Act baseline is likely to map onto stablecoin issuers

The BSA standards cited in the notice provide a concrete benchmark: verifying customer identity, keeping records, and determining potential terrorist connections. While those obligations are familiar for banks, applying comparable expectations to stablecoin issuers introduces implementation questions—particularly where stablecoins are issued or distributed via programs, intermediaries, or digital-asset rails rather than through conventional deposit account structures.

Institutions will likely need to assess how customer identification obligations interact with existing compliance programs. Many stablecoin providers and partners already run onboarding and transaction monitoring processes, but the proposed rule would more explicitly anchor identity verification in the same legal and supervisory logic used for covered financial institutions.

That alignment may also affect compliance risk assessments and regulator expectations regarding accountability. Firms may face increased scrutiny over who performs the verification (issuer versus downstream counterparties), what information is considered sufficient for “verification,” and how firms document and retain records to support investigations and examinations.

Broader GENIUS implementation: AML/CFT rulemaking and related deposit coverage issues

The customer identification proposal is not occurring in isolation. Treasury has previously proposed GENIUS-related AML and CFT requirements targeting illicit finance involving stablecoins. In addition, other GENIUS-linked implementation activity has already touched on the contours of insurance coverage for stablecoin issuers.

Earlier, the FDIC suggested that rules allowing deposit insurance for certain corporate deposits of stablecoin issuers would not automatically extend to holders. That distinction matters because it signals regulators are attempting to define regulatory treatment not only for issuers’ activities but also for how stablecoin users and balances fit into existing consumer protection and prudential frameworks.

While the identification proposal focuses on onboarding and screening obligations, the broader GENIUS implementation path suggests a phased approach: first establishing AML/CFT compliance structure and supervision expectations, then refining other areas such as how stablecoin balances interact with deposit-like protections.

From a compliance monitoring perspective, these parallel threads increase the likelihood that stablecoin programs will be evaluated through multiple regulatory lenses—identity verification, transaction monitoring, illicit finance risk controls, and potentially prudential or insurance-related requirements—depending on how each firm’s activities are classified.

Regulatory landscape beyond GENIUS: CLARITY Act timing remains uncertain

Even as stablecoin-specific rules progress under GENIUS, broader US crypto regulatory clarity remains unresolved. The Digital Asset Market Clarity (CLARITY) Act—intended to reshape roles and enforcement mechanisms across financial agencies—has not yet established a defined timeline.

Coverage of the legislative environment indicates that while many stakeholders expect progress by the August recess, there are unresolved concerns raised within Congress, including Democratic objections related to potential conflicts of interest by lawmakers and elected officials. That political uncertainty can influence how quickly the government can harmonize crypto oversight across agencies, even when stablecoin rules move forward.

For regulated entities, this matters because GENIUS addresses stablecoins specifically, but firms operating in the broader digital asset ecosystem may still need to contend with overlapping or inconsistent regulatory treatment depending on the asset category, the structure of the offering, and the designated regulator under any future CLARITY framework.

As a result, institutions should treat the GENIUS customer identification proposal as part of a longer regulatory process rather than a final endpoint. Compliance programs may need to be designed for iterative updates as implementing rules expand, agencies issue additional guidance, and Congress potentially advances wider statutory frameworks for digital asset regulation.

Closing perspective

With the proposed customer identification rule now open for a 60-day comment period after Federal Register filing, stablecoin issuers and their compliance teams will need to prepare for changes that bring identity verification expectations closer to bank-style BSA requirements. The next key step will be how agencies finalize the rule after public feedback and whether broader crypto oversight legislation—such as CLARITY—clarifies agency roles and enforcement priorities alongside GENIUS implementation.

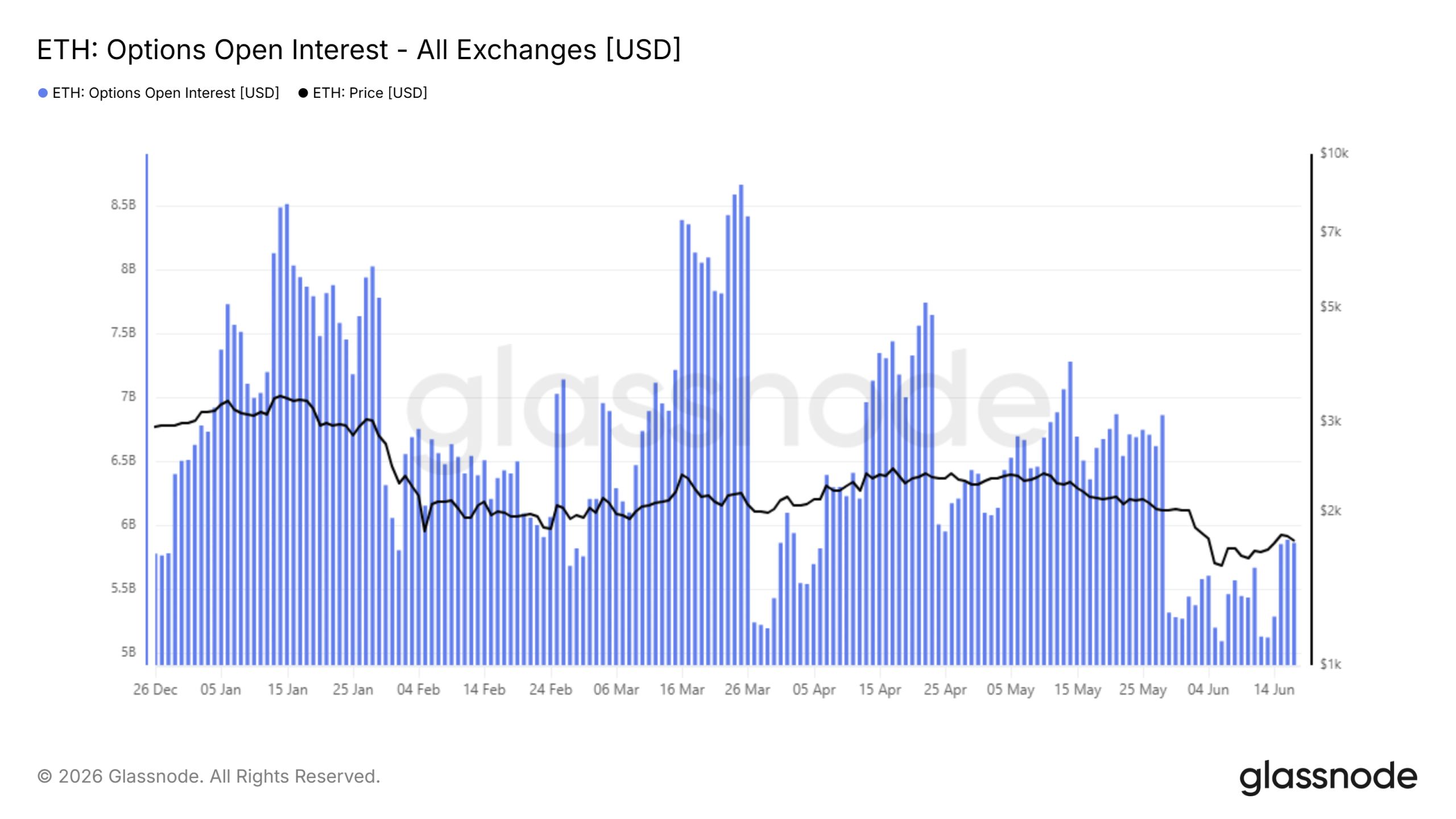

Ethereum (ETH) derivatives and ETF flows have gone quiet at the same time, with options open interest, perpetual funding, and spot inflows all sitting near multi-month lows. Ethereum Price trades around $1,682, down nearly 5% on the day.

That broad calm arrives as the daily chart shows volatility compressing again after a sharp June flush. Quiet conditions like these often precede an outsized move, though the direction stays unresolved.

Derivatives Activity Has Drained Toward Multi-Month Lows

ETH options open interest across all exchanges has fallen to roughly $5.5 billion. That sits well below the $8.5 billion peaks recorded in January and March. Traders have closed out futures positions rather than adding new bets.

Perpetual funding rates tell a similar story. After a brief negative spike near the early-June low, funding has flattened close to zero. Neither longs nor shorts hold a crowded edge right now.

This combination points to washed-out positioning. Low open interest and neutral funding mean less leverage feeding the price. A clear catalyst could therefore move ETH quickly with little resistance.

ETF Flows Hint at Returning Demand

The bearish read has one complication. Spot Ethereum ETF net flows have stopped bleeding after months of steady outflows. June printed a handful of small green inflow days.

The amounts stay modest, well under the $250 million inflow spikes seen in January. However, the shift from persistent selling to mild buying matters. It suggests institutional demand is no longer pointed in one direction.

A sustained return of positive flows would strengthen the case that $1,500 marked a durable floor. Without it, the recent bounce risks fading.

Ethereum Price Prediction Hinges on $1,500 and $1,920

ETH lost two important supports in recent weeks. Price broke an ascending trendline and the $2,150 level on May 17. It then lost the descending channel and support near $1,920.

The decline reached roughly $1,500 before buyers stepped in. Ether has since bounced to retest the lower band of the descending channel near $1,750. That retest now acts as resistance.

Volume contracted through most of the year, spiked on the channel breakdown, then contracted again. The Bollinger Band Width Percentile shows the same pattern. Volatility compressed into June, spiked at the low, and is compressing once more.

A rejection here could send ETH back toward $1,500, about 13% below current levels. Losing that floor would open lower targets and likely revive bearish predictions.

A $1,920 reclaim would flip the structure instead. That path points toward $2,150, roughly 25% above the current price, where prior resistance sits. Until then, the bearish structure holds the edge.

The setup leaves Ethereum coiled between a tested floor and stacked resistance. The next volatility expansion should decide which level breaks first.

The post Ethereum Could be Nearing a Violent Move as Price Drops 6% appeared first on BeInCrypto.

Morgan Stanley has updated its proposed Ethereum and Solana exchange-traded funds with a staking structure that would allow 95% of staking rewards to remain within the trusts while charging a 0.14% annual sponsor fee.

Summary

- Morgan Stanley amended its Ethereum and Solana ETF filings to include staking and a 0.14% annual fee.

- The proposed structure would keep 95% of staking rewards inside the trusts, with 5% paid to service providers.

- Ethereum filing data shows a 3.64 million ETH validator queue, implying a staking activation wait of about 63 days.

According to amended S-1 registration statements filed by Morgan Stanley, both the Morgan Stanley Ethereum Trust and Morgan Stanley Solana Trust would stake portions of their underlying crypto holdings to generate additional income for investors.

The filings disclosed that staking service providers and custodians would receive 5% of staking rewards as compensation, while the remaining 95% would stay in the funds.

Under the proposed structure, Morgan Stanley stated that the sponsor would not receive any staking rewards beyond the management fee. The filings indicate that staking income would accrue to the trusts rather than being redirected to the fund sponsor.

The amendments represent another step in Morgan Stanley’s efforts to expand its digital asset product lineup after entering the spot Bitcoin ETF market earlier this year.

Ethereum filing outlines validator limits and staking delays

Details included in the Ethereum filing provide a closer look at how the staking process would operate. According to Morgan Stanley, custodians would deposit ETH held by the trust into Ethereum staking smart contracts, while third-party staking service providers would operate validators on behalf of the fund.

The filing noted that staked Ether remains exposed to slashing penalties if validators fail to meet network requirements or violate protocol rules. In such cases, a portion of staked ETH could be removed from a validator’s balance.

Morgan Stanley also disclosed network capacity data tied to Ethereum staking. According to the filing, approximately 3.64 million ETH were waiting in the validator activation queue as of May 18, 2026.

The document stated that Ethereum currently limits validator activations to 56 validators per epoch, which translates to roughly 57,600 ETH entering staking each day. Based on those figures, Morgan Stanley estimated that newly staked ETH could face a waiting period of around 63 days before becoming eligible to earn staking rewards.

While the filing focused on operational details, the disclosures come as asset managers continue working with U.S. regulators on ETF structures that incorporate staking alongside direct crypto exposure.

Solana trust follows similar reward-sharing model

A separate amendment for the Morgan Stanley Solana Trust described a similar staking arrangement for SOL holdings. According to the filing, validators operated by staking service providers may act as delegated validators for the trust’s staked assets.

Morgan Stanley stated that custodians involved in the staking process would not control the private keys associated with delegated SOL. Unlike the Ethereum filing, however, the Solana amendment did not specify a daily limit on how much SOL could enter staking.

The filings arrive as Morgan Stanley continues adding crypto-related services across its wealth management division. As previously reported by crypto.news, Morgan Stanley Wealth Management recently partnered with Galaxy Digital to allow eligible high-net-worth clients to convert digital asset holdings into spot crypto investment products through a referral arrangement.

According to the companies, clients can lend assets including Bitcoin, Ether, and Solana to Galaxy Digital and receive shares in regulated crypto investment products, including the recently launched Morgan Stanley Bitcoin Trust.

The firms said the process can reduce crypto-to-ETP onboarding times by as much as 75% while allowing investors to maintain market exposure without first selling their digital assets.

Taken together, the ETF amendments and the Galaxy Digital arrangement add new crypto investment channels for Morgan Stanley clients as the bank continues building products tied to Bitcoin, Ethereum, and Solana through regulated investment structures.

Strategy’s STRC preferred stock has fallen as much as 17% below its $100 par value, prompting Arca Chief Investment Officer Jeff Dorman to argue that selling billions of dollars worth of Bitcoin may be the company’s best path to easing pressure on its capital structure.

Summary

- Jeff Dorman says selling $3–4 billion in Bitcoin could help stabilize Strategy’s struggling STRC preferred stock.

- Dorman assigns a 70% chance that Strategy continues selling MSTR shares rather than reducing Bitcoin holdings.

- QCP and Peter Schiff have separately raised concerns about dividend funding, fundraising costs, and investor risks.

According to a June 18 X post by Dorman, the recent decline in STRC has left Strategy facing increasingly difficult choices as investors question the sustainability of its preferred stock obligations. The preferred security dropped to a record low of $82.53 on June 18 before recovering and closing at $88.59, remaining well below par value.

Describing the situation as the latest stage of the “MSTR pickle,” Dorman said management must decide whether to take direct action to restore confidence in STRC or continue operating under a structure that leaves multiple parts of the company exposed to uncertainty.

Selling Bitcoin could buy Strategy more time

In Dorman’s view, the most effective solution would involve Strategy selling between $3 billion and $4 billion worth of Bitcoin. Assigning a 25% probability to that outcome, he said such a move would provide additional flexibility, support STRC holders, and address concerns surrounding the preferred stock without materially changing the company’s long-term Bitcoin strategy.

While Dorman acknowledged that a large Bitcoin sale could weigh on the asset in the short term, he argued that it would buy the company significant time and reduce pressure on its financing structure.

His most likely scenario, however, points elsewhere. Dorman assigned a 70% probability to Strategy continuing its current approach of selling small amounts of MSTR stock at what he described as non-accretive levels.

Under that outcome, he said STRC investors would retain some hope of recovery while Bitcoin holdings remain largely intact, though common shareholders could face further downside.

The comments arrive as scrutiny surrounding Strategy’s financing model continues to intensify. As reported by crypto.news, Peter Schiff recently accused Strategy co-founder Michael Saylor of misleading investors who purchased STRC after it was promoted as a yield-generating investment.

Schiff argued that retirees and income-focused investors could have grounds for legal action if risks associated with the security were not adequately disclosed. He also warned that the stock’s decline could make future fundraising more expensive if investors begin demanding higher yields to purchase additional STRC shares.

Dividend obligations remain at the center of concerns

Beyond stock sales and Bitcoin disposals, Dorman assigned a 5% probability to what he called a “nuclear option” involving the elimination of payments tied to preferred securities.

According to Dorman, such a move could leave preferred shareholders recovering only 30 to 40 cents on the dollar while effectively shutting Strategy out of capital markets. At the same time, he said the company would eliminate an annual cash obligation of roughly $1.7 billion.

Separate concerns about liquidity have also emerged in recent weeks. Earlier, market maker QCP estimated that Strategy’s available liquidity could support preferred dividend payments for approximately seven and a half months.

QCP added that if existing funding channels become less attractive, the company may eventually need alternative sources of capital, with Bitcoin sales potentially becoming one available option.

Alongside those concerns, Dorman challenged Strategy’s valuation. Based on his calculations, the company holds roughly $35.2 billion in unencumbered Bitcoin collateral against an equity market capitalization of about $40.4 billion, leaving MSTR trading at approximately 1.15 times net asset value.

Given those figures, Dorman argued that MSTR should trade below net asset value and warned that the stock could continue falling unless Bitcoin stages a strong recovery. Even then, he said any upside would depend on Strategy avoiding additional dilution through dividends, asset sales, or future fundraising activities.

MicroStrategy’s biggest Bitcoin financing tool is under pressure. Strategy’s STRC preferred stock fell well below its intended $100 level this week, raising fresh questions about the company’s complex plan to keep buying Bitcoin through Wall Street-style securities.

The selloff drew extra attention because Saylor has linked Strategy’s new preferred-stock products to AI-assisted design.

“When we did STRC, I did it all with AI. I couldn’t have done it myself. I literally sat and used AI, went back and forth for hours,” Saylor said in an interview.

STRC, formally known as Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock, was built to trade close to $100. Strategy can adjust its dividend rate each month to help support that target.

That design is now being tested.

STRC traded near the high-$80s after falling as low as the low-$80s, well below the level Strategy wants it to hold.

For a product sold as a relatively stable, high-yield preferred stock, that drop has become a major signal for investors.

The AI Angle Turns a Selloff Into a Meme

The crash became more sensational because of Saylor’s comments about AI.

Saylor has said Strategy used artificial intelligence to help design some of its preferred-stock products. Critics are now mocking STRC as an “AI-designed” security that is breaking under market pressure.

The line is catchy, but the reality is more complicated. AI likely helped with modelling, structure, or product design. The security itself still went through bankers, lawyers, executives, and market approval.

Still, the optics are bad. STRC was pitched as financial engineering for the Bitcoin era. Its drop below $100 makes that engineering look less stable than advertised.

What STRC Actually Is

STRC is not Bitcoin or a stablecoin, but it’s not a normal company share either.

It is a preferred stock issued by Strategy, the company formerly known as MicroStrategy. Preferred stocks usually sit between common shares and debt. Investors buy them mainly for income.

STRC pays a high dividend. Strategy can raise or lower that dividend monthly to try to keep the stock trading around $100.

That is the core mechanism. If STRC falls too far below $100, the market expects Strategy to raise the dividend to make it more attractive.

Why the Drop Matters

A higher dividend means MicroStrategy must pay more to investors.

That increases the cost of raising capital. It also makes future STRC issuance harder. If investors no longer believe STRC can hold near $100, Strategy may have to offer even higher yields to attract buyers.

For Saylor, that matters because Strategy has used securities like STRC to fund its Bitcoin strategy. The company raises money from capital markets and uses part of that money to buy more Bitcoin.

When that machine works, Strategy can keep expanding its Bitcoin holdings without selling much common stock at unattractive levels.

When it weakens, the choices get harder.

Will MicroStrategy Have to Sell More Bitcoin?

There is no confirmed sign that Strategy will have to sell Bitcoin again because of STRC.

The concern is about pressure, not an immediate forced sale.

If STRC keeps falling, Strategy may need to raise the dividend again. If dividend costs rise, the company needs reliable cash flow or fresh capital to keep paying investors.

That could lead to more common stock issuance, which would dilute shareholders. It could also reduce Strategy’s ability to buy more Bitcoin.

In a more stressed scenario, investors worry the company may eventually face pressure to sell some Bitcoin to meet obligations or defend its balance sheet.

That would hit the core narrative around Saylor’s strategy. Strategy has built its identity around accumulating Bitcoin, not selling it.

The post Saylor Created MicroStrategy’s STRC Stock with AI, and Now It Crashed Below $100 appeared first on BeInCrypto.

Wealthsimple has secured approval to offer roughly 4,000 prediction market contracts in Canada, expanding retail access to event-based trading through a new partnership with Kalshi.

Summary

- Wealthsimple will launch a prediction markets app in Canada with access to about 4,000 Kalshi contracts.

- Kalshi’s crypto perpetual futures platform generated more than $5.5 billion in volume within two weeks.

- Regulatory and legal battles over prediction markets continue to intensify across the U.S. and several international jurisdictions.

According to Wealthsimple, the company plans to launch a standalone prediction markets platform called Wealthsimple Predict this summer, giving Canadian investors access to thousands of contracts listed by Kalshi across categories such as financial markets, economic data, and climate-related events.

The rollout follows authorization from the Canadian Investment Regulatory Organization in March. Under the approval, Wealthsimple became the second investment dealer permitted to offer prediction market contracts in Canada. CIRO said the products will be regulated as derivatives and must carry settlement periods of at least 30 days.

Wealthsimple’s launch arrives as prediction markets continue to attract attention from regulators, lawmakers, and traditional exchanges in several countries. While Canadian authorities have allowed the products under an established derivatives framework, regulators elsewhere remain divided over how such contracts should be classified.

Kalshi expands beyond prediction markets

At the same time, Kalshi has continued pushing into crypto-linked derivatives. The company announced on Thursday that its perpetual futures products are now available for trading, following a May 31 announcement that formally introduced its crypto perpetual futures business.

Earlier this week, Kalshi disclosed that its perpetual futures platform generated more than $5.5 billion in trading volume within two weeks of launch. The company currently offers 11 crypto-linked perpetual futures contracts and has stated that discussions with regulators regarding additional products are ongoing.

Crypto.news previously reported that Kalshi’s rapid growth has intensified a separate political dispute in Washington. According to a Semafor report, a coalition that includes the Indian Gaming Association, the American Gaming Association, and several labor groups has urged the U.S. Senate to amend the CLARITY Act to explicitly prohibit sports and casino-style event contracts from being offered through prediction market platforms.

In a letter to lawmakers cited by Semafor, the coalition argued that sports betting should remain under existing state and tribal regulatory systems rather than falling under the oversight of the Commodity Futures Trading Commission.

The groups also claimed that prediction markets have enabled what they described as the largest expansion of gambling in U.S. history over the past 18 months without direct congressional approval.

Legal challenges continue to grow

Meanwhile, resistance is also emerging from established derivatives exchanges.

On Thursday, CME Group filed a lawsuit against the U.S. Commodity Futures Trading Commission over the regulator’s approval of cryptocurrency perpetual futures contracts offered by Kalshi and similar products introduced by Coinbase. The filing came one day after CME Chief Executive Officer Terrence Duffy said the company intended to challenge the approvals through the courts.

The legal dispute follows a series of regulatory actions supporting onshore crypto perpetual futures trading. In May, the CFTC approved Bitcoin perpetual futures contracts for Kalshi and issued a no-action position that allowed Coinbase to launch comparable products.

Several jurisdictions outside North America have taken a different approach. Spanish regulators ordered internet providers in May to block access to Kalshi and Polymarket while examining whether the platforms violated national gambling laws.

Indonesian authorities have banned Polymarket, while Japanese and South Korean regulators have also taken action against prediction market activity.

Within the United States, at least 11 states have challenged prediction markets in recent months. Speaking at Bitso’s Stablecoin Conference in Mexico City on June 16, Digital Chamber Chief Executive Officer Cody Carbone said the growing dispute between state gambling regulators and the CFTC is likely to reach the U.S. Supreme Court.

Cap Labs has closed its public CAP token auction with 1,002 unique bids, $16.4 million in total commitments, and a 5.5x oversubscription rate, the EigenLayer-backed stablecoin protocol announced Wednesday night. The auction opened June 8 and drew a final clearing price of $0.011 across a total… Read the full story at The Defiant

Key Highlights

- Shares of Take-Two Interactive climbed more than 6% following Rockstar Games’ announcement that GTA VI preorders begin June 25.

- Rockstar confirmed a November 19, 2025 release date, bringing clarity after multiple delays.

- Piper Sandler maintains an Overweight rating with a $280 target, forecasting over 45 million units sold initially.

- CEO Strauss Zelnick projects FY2027 net bookings between $8 billion and $8.2 billion.

- Official box art revealed by Rockstar generated significant buzz across social platforms.

Shares of Take-Two Interactive (TTWO) rallied over 6% Thursday following Rockstar Games’ confirmation that Grand Theft Auto VI will be available for preorder starting June 25, ahead of its November 19 launch. The stock traded near $241.74 during afternoon hours.

Take-Two Interactive Software, Inc., TTWO

Rockstar made the announcement through its verified X account, simultaneously unveiling the game’s retail box artwork. The reveal quickly gained traction online.

For market watchers, this preorder timeline represents more than just a marketing milestone. It provides concrete evidence that the November launch window remains on track — a crucial signal following years of uncertainty and postponements.

The road to GTA VI’s release has been turbulent. Originally targeted for 2025, the launch was subsequently delayed to mid-2026, then pushed again to November 2026. When that final postponement was revealed, TTWO shares tumbled nearly 18% in a single trading day.

By announcing preorders five months before launch, institutional investors are interpreting this as strong indication that additional delays are unlikely.

The franchise’s previous installment debuted in 2013. That represents thirteen years of accumulated anticipation, and market data supports the magnitude of this buildup.

Wall Street’s Expectations

Piper Sandler maintained its Overweight stance on TTWO with a $280 price objective. Their analysis suggests GTA VI could move more than 45 million copies in its initial release period.

To put this in perspective, GTA V generated over $1 billion in sales during its first three days in 2013 and has delivered more than 200 million units lifetime — establishing it as the most successful entertainment launch ever.

FactSet consensus estimates point to Take-Two generating $8.6 billion in revenue for the fiscal year concluding next March, representing a 27% increase from fiscal 2026.

CEO Strauss Zelnick has provided guidance for FY2027 net bookings in the $8 billion to $8.2 billion range.

Preorder Window Opens Late June

The June 25 preorder availability will span PlayStation 5 and Xbox Series X|S digital platforms, alongside physical reservation options at leading retailers globally.

The game’s cultural impact is already extending beyond the gaming sector. Burger Motorsports, an automotive parts retailer, announced it will shut down operations on November 19 — the GTA VI release day — describing it as “an unprecedented cultural event.”

TTWO remains down approximately 6.9% for the year and roughly unchanged over the trailing twelve months. Preorder metrics in the weeks ahead will provide investors with better visibility into whether consumer demand aligns with market expectations.

Strategy's STRC preferred stock extended its slide to a fresh record low on Thursday, deepening the discount on one of the main channels the largest corporate bitcoin holder uses to fund its purchases. The Variable Rate Series A Perpetual Stretch Preferred Stock, known as STRC, traded near $85 on… Read the full story at The Defiant

- Hyperliquid (HYPE) holds a strong uptrend with all major EMAs stacked bullish.

- HYPE price is testing $75.62 resistance after the recent all-time high move.

- RSI neutral at 62, leaving room for a continued momentum move.

HYPE has remained one of the strongest-performing digital assets in recent weeks as growing activity on the Hyperliquid ecosystem continues to attract attention across the crypto market.

The token recently climbed to a new all-time high of $76.70 before pulling back slightly to around $72.50 at the time of writing.

Despite the retracements, HYPE is still up more than 30% over the past seven days and more than 52% over the last month.

The rally comes at a time when Hyperliquid is reporting record levels of trading activity, revenue generation, and derivatives market participation.

Hyperliquid revenue growth continues to accelerate

Hyperliquid’s revenue growth has emerged as one of the biggest talking points surrounding Hyperliquid in 2026.

The platform has generated more than $1.16 billion in cumulative revenue, placing it among the highest-earning crypto protocols in the market.

The growth has been driven by rising trading volumes across its perpetual futures markets, which have attracted both retail traders and large institutional participants.

Notably, trading activity has remained strong throughout the year, with the DEX recording approximately $1.38 billion in 24-hour trading volume, while total value locked on the platform has climbed to roughly $6.38 billion.

The strong revenue figures are particularly notable because they come as Hyperliquid continues expanding beyond its original crypto-native derivatives business, with new markets tied to equities, commodities, indices, and pre-IPO assets broadening the platform’s reach and creating additional sources of trading activity.

Hyperliquid’s open interest surpasses $6 billion

Another major milestone arrived when Hyperliquid’s total open interest crossed $6 billion on June 14.

This places Hyperliquid among the largest perpetual futures venues globally and highlights the platform’s growing influence within the derivatives market.

Earlier in the year, Hyperliquid controlled around 8.3% of global perpetual futures open interest, demonstrating how quickly it has gained market share against established competitors.

HYPE price outlook

While the Hyperliquid price action has cooled slightly from its recently reached all-time high, the broader structure still points to a market that is holding a strong upward trend rather than reversing it.

On the technical side, the short-term setup remains firmly positive.

A majority of the technical indicators are bullish.

Oscillators are showing a buy bias, while moving averages are fully aligned on the upside.

The token is trading above all major daily exponential moving averages (EMAs), including the 10-day, 20-day, 50-day, 100-day, and 200-day EMAs.

This type of full EMA stack typically reflects sustained trend control by buyers rather than short-lived momentum.

The RSI (14) sits at 62, which places it in neutral territory with a slight upward tilt.

The RSI is not in overbought conditions, meaning there is still technical room for continuation if momentum returns.

However, price is now approaching a key decision area, and a daily close above the first major resistance at $75.62 would be required for HYPE to enter the next phase of price discovery.

But if the market becomes overbought and pulls back, the key structural support is positioned at $56.50.

A break below $56.50 would represent a meaningful shift in the current bullish structure.

![[TIKTOK] Lisa Money Trend](https://wordupnews.com/wp-content/uploads/2026/02/1770644804_maxresdefault-80x80.jpg)

[TIKTOK] Lisa Money Trend

Is there an exit poll for the Makerfield by-election?

Who should pay on the first date

![Skilla Baby - GYSM (Get You Some Money) [Official Video]](https://wordupnews.com/wp-content/uploads/2026/06/1781824474_maxresdefault-80x80.jpg)

-

Business4 days ago

Business4 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World4 days ago

Crypto World4 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World6 days ago

Crypto World6 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech6 days ago

Tech6 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech6 days ago

Tech6 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

NewsBeat6 days ago

NewsBeat6 days agoFBI searches office of Ohio voter registration group

-

Tech7 days ago

Tech7 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-

Entertainment7 days ago

Entertainment7 days ago‘The Pitt’s Fan-Favorite Doctor Confirms Noah Wyle Gave His Blessing to Return [Exclusive]

-

Crypto World7 days ago

Crypto World7 days agoRipple and Bitso Bring MXNB Stablecoin to XRP Ledger

-

Tech7 days ago

Tech7 days agoFormer AWS CEO Adam Selipsky to lead new $10B AI data center venture

-

Entertainment4 days ago

Entertainment4 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Business4 days ago

Business4 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Tech4 days ago

Tech4 days agoAs AI companies race to go public, who else is along for the ride?

-

Crypto World4 days ago

Crypto World4 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

Tech7 days ago

Tech7 days agoEuro-Office 1.0 Arrives To Open-Source Infighting: ‘Compatibility Is Not Sovereignty’

-

Politics4 days ago

Politics4 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

Entertainment7 days ago

Ana Navarro unleashes explosive tirade on ex-Trump aide, Disney Channel star in epic on-air fight: 'Have you no shame?'

-

NewsBeat4 days ago

NewsBeat4 days agoWarning of disruption as Cardiff Crossrail works to start

-

News Videos4 days ago

News Videos4 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

You must be logged in to post a comment Login