Crypto World

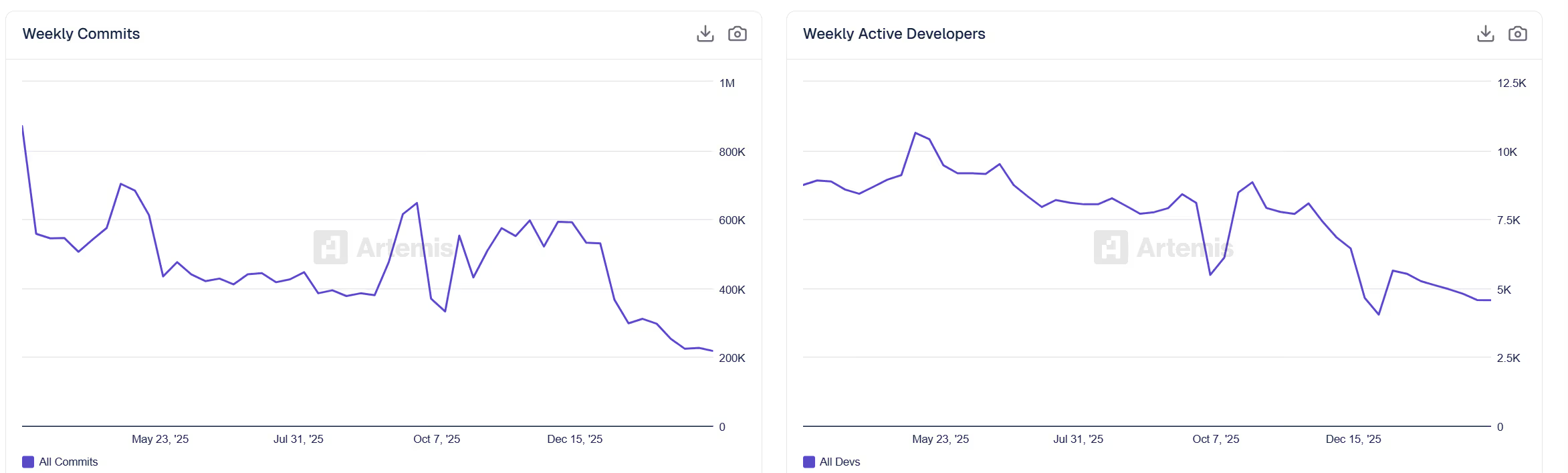

Crypto code commits fall 75% as developers move to AI projects

Blockchain ecosystems are losing developers across the board while artificial intelligence projects dominate growth on GitHub, the world’s largest platform for hosting and collaborating on software code.

Weekly crypto commits (publishing new code) to repositories have fallen roughly 75% since early 2025, dropping from about 850,000 to 210,000, while active developers declined 56% to around 4,600, according to data from analytics platform Artemis.

Repositories track where developers are writing code, building tools and launching new projects, they offer one of the clearest signals of where software innovation is happening.

The contraction stands in stark contrast to the broader software ecosystem. GitHub added about 36 million developers in 2025 alone, bringing its global base to more than 180 million, with platform-wide commits rising roughly 25% year over year, according to GitHub’s Octoverse report.

Much of that growth is flowing into artificial intelligence. GitHub now hosts more than 4.3 million AI-related repositories.

The number of repos importing large language model software development kits surged about 178% to more than 1.1 million over the past year, while generative AI projects now attract more than 1 million monthly contributors.

The numbers suggest developers are reallocating time toward AI infrastructure rather than blockchain.

Repositories using Jupyter Notebooks, commonly used for machine learning experimentation, grew about 75%. Dockerfile repositories used to deploy AI applications jumped roughly 120%. TypeScript, the programming language underpinning much of the modern web and many AI tools, overtook Python and JavaScript to become GitHub’s most-used language after gaining more than 1 million contributors in a single year.

Within crypto, the decline is broad but uneven.

Ethereum’s weekly active developer count fell 34% over three months to 2,811, according to Artemis. Solana shed 40% to 942 developers. Base, the Coinbase-incubated Layer 2 that was among 2024’s fastest-growing ecosystems, dropped 52% to 378 developers.

Newer chains that attracted speculative interest during last year’s bull market are faring worst. Aptos lost about 60% of its developers, BNB Chain commits plunged 85%, and Celo fell 52%.

The only category of meaningful size still growing is wallet infrastructure, which rose about 6% to 308 weekly active developers.

Still, the data suggests crypto may be consolidating rather than collapsing.

Electric Capital’s annual developer report shows the sector peaked at roughly 31,000 monthly active developers in 2022 before falling to about 23,600 in 2024, with estimates suggesting further declines to around 18,000 by mid-2025.

The composition of the remaining workforce is also changing. Developers with more than two years of tenure grew about 27% year over year and now produce roughly 70% of commits. The exodus is concentrated among part-time contributors and newcomers with less than 12 months of experience, a group that declined 58% in one tracking period.

Crypto development has historically followed market cycles, and activity could rebound if another bull market draws builders back.

But previous downturns offered fewer alternatives for displaced developers. In 2025, generative AI represents a rapidly expanding frontier with deep venture funding and immediate commercial demand, raising the question of whether this cycle’s talent drain proves harder to reverse.

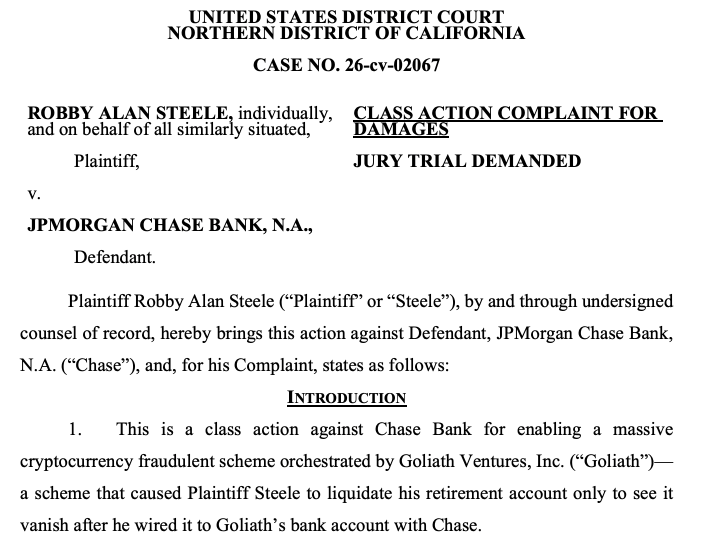

JPMorgan is facing a lawsuit for allegedly enabling a $328 million crypto Ponzi scheme run by now-defunct Goliath Ventures.

Investors on Tuesday filed a proposed class action in the US District Court for the Northern District of California, accusing JPMorgan of ignoring suspicious transactions and allowing Goliath to use its infrastructure to collect investor funds.

The lawsuit notes that despite JPMorgan CEO Jamie Dimon’s repeated criticism of Bitcoin (BTC), the bank allegedly failed to prevent crypto scammers from carrying out fraudulent wire transactions.

“Chase, by virtue of its Know Your Customer actually knew that Goliath was acting as a ‘private equity’ cryptocurrency pool operator investing money for investors, without being licensed at all to sell these investments,” the complaint states.

Complaint focuses on JPMorgan account flows

The US Attorney’s Office for the Middle District of Florida announced the arrest of Goliath CEO Christopher Delgado on Feb. 24. He faces a maximum penalty of 30 years in federal prison if convicted on all counts.

Prosecutors said Goliath Ventures, formerly known as Gen-Z Venture Firm, operated the scheme from January 2023 through January 2026.

The lawsuit claims JPMorgan was the sole banking institution for Goliath from January 2023 to May or June 2025. “Goliath obtained at least $328 million from what are believed to be over 2,000 investors,” the complaint notes.

The complaint also describes money moved from a JPMorgan account to Goliath wallets held at Coinbase.

It alleges that from January 2023 through June 2025, about $253 million was deposited into the bank’s 0305 account, which is nearly two-thirds of the $328 million investors reportedly provided. Of that total, roughly $123 million was transferred to Goliath’s wallets maintained by Coinbase.

US complaint also names Bank of America account

A separate criminal complaint filed by the US government said Goliath also held business accounts at Bank of America.

“Delgado was a co-signatory on the BOA 9136 account in the name of Goliath,” the Feb. 20 complaint states, adding that Goliath directors told at least one investor that Delgado controlled the account.

The complaint further detailed that funds sent by investors were primarily deposited into JPMorgan’s 0305 account or the BOA 9136 account or transferred directly to Goliath’s wallets at Coinbase.

The government said Delgado was the sole signatory on Goliath’s Coinbase wallets.

More complaints are coming as the team is still identifying victims

The complaint was filed by a team of attorneys from Shaw Lewenz, Sonn Law Group and Schwartzbaum. The first named plaintiff, Robby Alan Steele, said he invested a total of $650,000, including retirement funds.

Related: Ex-CFO sentenced to two years for $35M crypto fraud scheme

Shaw Lewenz’ Jordan Shaw said there would be more complaints to come, as the team is still identifying individuals and entities they believe to be complicit.

“We are being purposeful and precise in who we file against, to be complementary to the receiver and his efforts,” Shaw said, adding: “The goal is not to duplicate efforts, but instead to maximize recovery.”

Magazine: Would Bitcoin really be at $200K if not for Jane Street? Trade Secrets

Crypto World

MSTR’s STRC buys an estimated 7,000 BTC this week, but Two Prime CEO warns ‘no free lunch’

Around 7,000 bitcoin are estimated to have been purchased this week through Strategy’s (MSTR) perpetual preferred stock Stretch (STRC), underscoring how quickly the high yield instrument has become a key engine behind the company’s bitcoin accumulation.

But the structure carries risks, according to Alexander Blume, chief executive officer of Two Prime, an SEC registered investment adviser focused on institutional bitcoin yield strategies and bitcoin backed lending.

“There’s no free lunch,” Blume said. “A product that pays more than 6% over Treasuries must come with additional risk.”

Demand for the preferred shares has surged as investors search for higher returns. STRC currently yields at 11.5% and pays monthly cash distributions. Strategy has described the instrument as resembling a short duration, high yield savings instrument, with the dividend rate adjusted to help keep shares trading near their $100 par value while limiting price volatility.

The structure has helped accelerate Strategy’s bitcoin purchases. Market estimates suggest the company has bought more than 11,000 BTC over the past two weeks, bringing total accumulation through the product to roughly 34,000 BTC since it went live, according to STRC.live.

Corporate interest is also beginning to emerge. Asset manager Strive (ASST) recently disclosed a $50 million allocation to STRC, while digital credit firm Apyx said it recently purchased an additional 200,000 STRC shares, bringing its total holdings to 255,000 shares.

Blume said STRC was a major focus at the recent Strategy World conference, highlighting how central the product has become to the company’s capital strategy.

“We have seen a smattering of companies buy STRC,” Blume said, adding that some of the activity appears symbolic or partnership driven for now.

Blume also pointed to early efforts to build decentralized finance products on top of STRC, sometimes marketing them as savings like instruments despite volatility in the underlying asset.

STRC is designed to trade close to its $100 par value, but Blume said that is not guaranteed. A loss of confidence in the company, bitcoin or the preferred shares themselves could push the price below par and cause significant damage, he said.

STRC has on several occasions traded below its $100 par value, prompting the company to raise the dividend to help push the shares back toward par.

Blume added that strong momentum, available funding for interest payments and demand for high yield mean the structure is unlikely to face immediate problems.

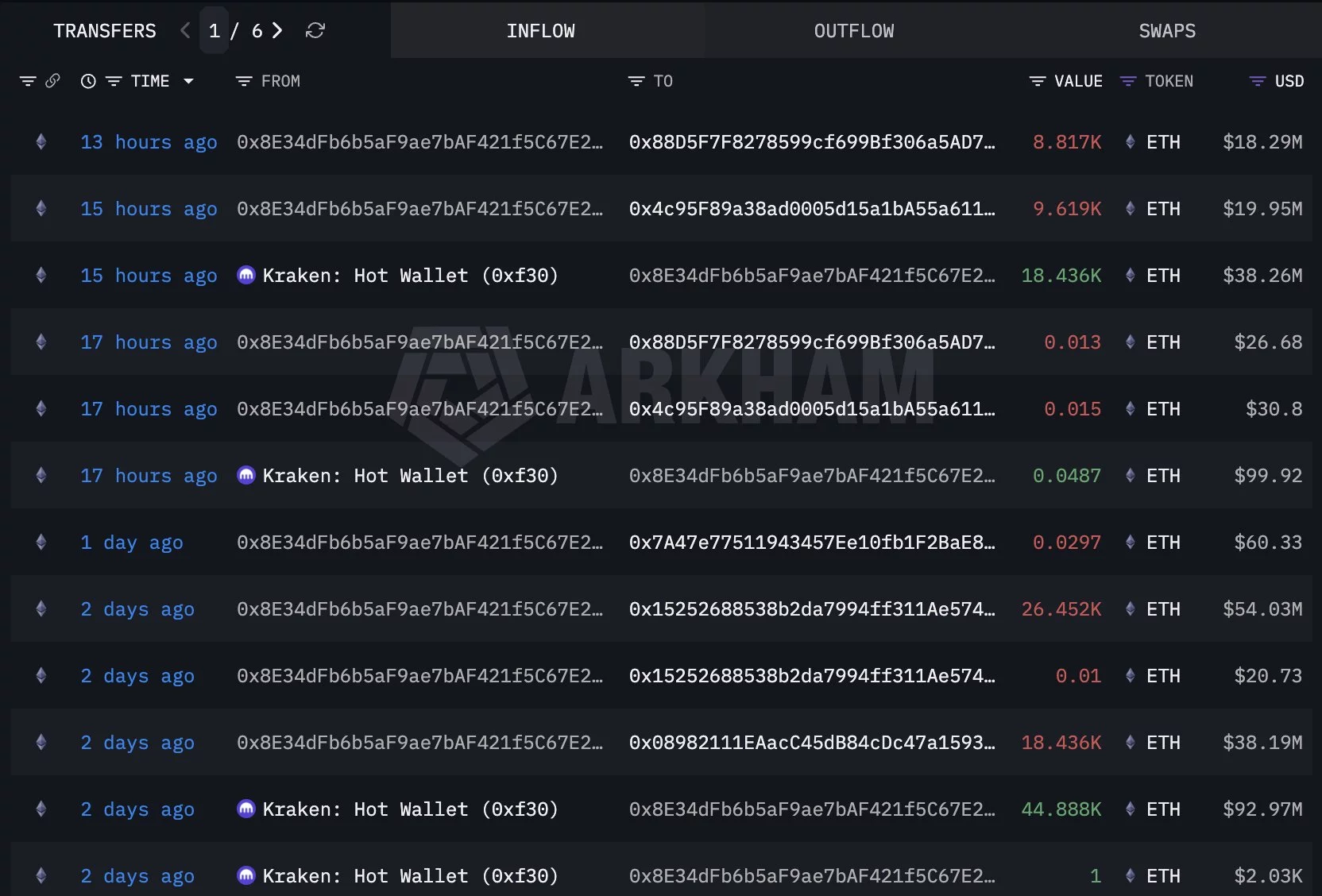

The Ethereum price is showing signs of stabilization as large investors accumulate significant amounts of ETH from major cryptocurrency exchanges.

Summary

- Whale wallets withdrew over 74,000 ETH ($155M) from Binance and Kraken.

- Ethereum price is consolidating near $2,050 after February’s sharp correction.

- A breakout above $2,200 resistance could signal the next bullish move for ETH.

According to blockchain analytics shared by Lookonchain, a newly created wallet withdrew 11,629 Ethereum (ETH) worth about $23.7 million from Binance over the past two days.

In a separate transaction, another whale wallet identified as 0x8E34 removed 63,324 ETH valued at roughly $131.2 million from Kraken during the same period.

Large withdrawals from exchanges are often interpreted as a bullish signal because investors typically move assets to private wallets for long-term holding rather than immediate selling.

The combined withdrawals total more than 74,000 ETH, suggesting that institutional or high-net-worth investors may be positioning ahead of a potential price move.

Ethereum price analysis

Based on the ETH/USDT daily chart, Ethereum is currently trading around $2,050, remaining largely range-bound after a sharp correction earlier in February.

The chart shows that ETH has been consolidating between $1,950 and $2,150 for several weeks, forming a sideways structure after rebounding from lows near $1,800.

The immediate resistance level sits around $2,150–$2,200. A decisive breakout above this zone could trigger momentum toward the $2,400 level, where the previous sell-off accelerated.

On the downside, strong support appears near $1,950, with deeper structural support around $1,800, which marked the February bottom.

The Relative Strength Index (RSI) is currently near 50, reflecting neutral momentum and suggesting the asset is neither overbought nor oversold. This reading typically occurs during consolidation phases before a larger directional move.

Meanwhile, the Accumulation/Distribution indicator is stabilizing after a sharp drop earlier in the month, hinting that buying pressure may be gradually returning.

The recent whale withdrawals could tighten exchange supply if the coins remain off trading platforms. When combined with Ethereum’s current consolidation pattern, such accumulation phases often precede stronger price movements.

However, traders will likely watch for a break above $2,200 to confirm a bullish continuation. Until then, Ethereum may remain trapped within its current range as the market waits for a decisive catalyst.

- TRUMP meme coin slides to $2.86 amid selling pressure.

- The team has moved 5 million tokens to Binance, sparking fears of a sell-off.

- The key support sits at $2.80 with $2.50 as the next downside level.

The price of Official Trump (TRUMP) memecoin has fallen sharply as selling pressure continues to dominate the market.

The politically themed meme coin is trading around $2.86 after losing more ground over the past 24 hours.

This drop extends a deeper slide that has pushed the token down more than 16% over the last week.

The continued decline has left the asset hovering near its lowest levels since its explosive debut rally.

Analysts now believe the current move reflects a broader loss of momentum rather than a brief pullback.

Sentiment around the token has also cooled significantly as the excitement that once fueled its rapid rise fades.

Official Trump team moves $5 million tokens to Binance

The situation intensified after reports emerged that wallets connected to the project moved roughly five million TRUMP tokens to the exchange Binance.

The transfer was valued at more than $17 million at the time it occurred.

Large movements of tokens to exchanges often raise concerns that insiders may be preparing to sell, and such activity can quickly trigger anxiety among traders who fear additional supply entering the market.

That fear alone can be enough to push prices lower as investors rush to exit positions.

In this case, the timing of the transfer has added to the already bearish mood surrounding the token.

The market had already been showing signs of weakness before the transaction became public.

Selling pressure has remained steady for several weeks, preventing any meaningful recovery attempts.

Even brief rebounds have struggled to gain traction as traders continue to reduce exposure.

Lower trading volume in recent sessions also suggests that buying interest has faded.

When demand weakens during a downtrend, sellers often dictate the market’s direction.

This pattern has been clearly visible in the recent price action.

Other micro and macro factors affecting TRUMP meme coin

Bitcoin (BTC) has slipped slightly during the same period, adding to a risk-off environment for digital assets.

Although the wider market declined modestly, meme coins tend to respond more aggressively to shifts in sentiment.

Assets driven largely by hype and narrative often struggle when traders become more cautious.

The TRUMP token is particularly sensitive to sentiment because its appeal is closely tied to the public perception of Donald Trump.

As political narratives shift, investor enthusiasm for the coin can change just as quickly.

This connection between politics and price action has made the token one of the most sentiment-driven assets in the crypto space.

Recent developments suggest that the speculative energy surrounding the project is waning.

Without fresh catalysts or renewed social media hype, the token has struggled to attract new buyers.

That lack of momentum has left the coin vulnerable to extended corrections.

The sharp drop from its peak earlier in the year highlights how quickly meme-driven rallies can reverse.

What once looked like unstoppable momentum has turned into a steady downtrend.

For now, traders appear to be waiting for clearer signals before committing to new positions.

TRUMP price forecast

From a technical standpoint, the most important support level is near $2.80.

Holding above this level could allow the token to stabilise and enter a consolidation phase.

Such a period of sideways movement would indicate that selling pressure is beginning to slow.

However, a decisive break below $2.80 could open the door to another wave of losses, with the next key level traders should watch around $2.50.

A move toward that area would continue the current bearish trend.

On the upside, the first sign of strength would be a recovery back above the $3.00 mark.

Reclaiming that level could signal that the recent downtrend is losing momentum.

Until that happens, the overall market bias remains cautious.

Traders should also pay close attention to Bitcoin’s direction, which often sets the tone for the broader crypto market.

A stronger push from BTC could help restore confidence across altcoins and meme tokens.

If that occurs while the TRUMP meme coin holds key support levels, the chances of a recovery rally would improve.

However, for now, the market remains fragile, with sentiment still leaning bearish.

Key Highlights

- Shares of Nebius Group surged 16.14% Wednesday following Nvidia’s announcement of a $2 billion strategic investment.

- The partnership aims to deliver more than 5 gigawatts of AI computing power before 2031.

- The agreement grants Nebius priority access to Nvidia’s cutting-edge computing platforms and involves joint development of massive AI facilities.

- The AI cloud provider has secured $20.4 billion in commitments from tech giants Microsoft and Meta, targeting $7B–$9B in annual recurring revenue by year’s end.

- Competing neocloud providers CoreWeave (CRWV) and IREN saw gains of 9.4% and 10% respectively following the announcement.

Shares of Nebius Group rallied 16% during Wednesday’s trading session after chip giant Nvidia disclosed a $2 billion investment in the Amsterdam-headquartered AI cloud infrastructure provider. The capital infusion is tied to a strategic alliance focused on scaling AI computing capabilities globally.

Nvidia characterized the investment as a testament to Nebius’s technical expertise and execution capabilities. Under the agreement, both organizations will collaborate on architecting and rolling out next-generation AI data center facilities, with Nebius receiving preferential access to Nvidia’s emerging computing platforms.

The strategic alliance extends to joint development of software infrastructure and management systems designed to operate massive AI computing environments. According to Nebius, this partnership will accelerate the expansion of computing resources across its worldwide network.

Unlike traditional hyperscale cloud providers, Nebius operates as a neocloud—a cloud infrastructure company engineered from the ground up exclusively for artificial intelligence applications. This specialized, efficiency-focused approach has proven attractive to enterprise customers with substantial AI requirements.

Microsoft has committed to procuring $17.4 billion worth of computing capacity from Nebius across a five-year timeframe. Social media giant Meta subsequently signed a separate $3 billion agreement. These contract values indicate serious enterprise adoption.

The company projects it will bring between 800 megawatts and one gigawatt of connected computing power online by late 2026. Power agreements already in place exceed three gigawatts of contracted capacity.

Management forecasts annual recurring revenue will reach the $7 billion to $9 billion range by the conclusion of this year. For an organization that remains relatively unknown to many investors, this represents a dramatic scaling trajectory.

Earlier in the month, Nebius obtained regulatory clearance to construct a 1.2-gigawatt data center complex in Independence, Missouri. The facility is anticipated to generate approximately 1,200 construction positions and 130 full-time operational roles.

The Missouri development also incorporates over $650 million in tax incentive payments distributed across two decades. This structure signals long-term commitment from both the company and local government.

Nvidia CEO Jensen Huang characterized Nebius as constructing an AI cloud infrastructure purpose-built for the agentic intelligence era, with complete integration spanning from chip architecture to application software. Such public validation from Huang carries significant influence within the AI infrastructure ecosystem.

Broader Market Impact

The Nvidia-Nebius partnership triggered gains beyond NBIS shares alone. CoreWeave (CRWV) advanced 9.4% Wednesday in a sympathy move. Nvidia maintains a substantial ownership position in CoreWeave and announced an additional $2 billion investment in January.

Smaller competitor IREN appreciated 10% during the session. Market participants interpreted the Nebius transaction as validation for the entire neocloud business model.

This marks Nvidia’s third $2 billion infrastructure commitment in recent weeks. In the preceding week, the semiconductor manufacturer announced matching $2 billion investments in both Lumentum and Coherent to advance optical networking technologies critical for AI data center operations.

Nvidia’s Infrastructure Push

The Nebius investment announcement arrives concurrent with Oracle revealing it has locked in more than 10 gigawatts of power capacity and corresponding data center infrastructure scheduled to come online within the next 36 months.

Oracle’s infrastructure expansion supports an approximately $300 billion cloud services agreement with OpenAI. Nvidia has separately invested $30 billion directly in OpenAI.

Nebius carried a market capitalization slightly above $24 billion based on Tuesday’s closing price. Nvidia’s $2 billion commitment equals approximately 8% of that valuation.

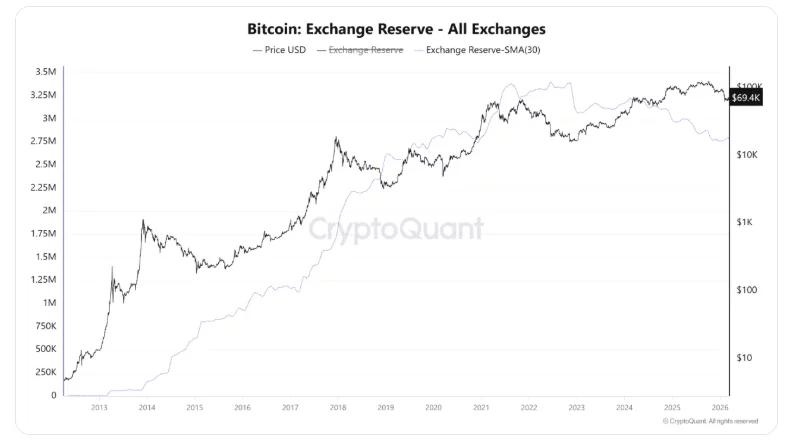

Bitcoin could be approaching a supply shock phase as retail investors sell under pressure while long-term holders keep their coins dormant, according to a new market analysis by CryptoQuant.

Summary

- CryptoQuant says Bitcoin may be entering a supply shock phase as whales remain inactive and retail investors sell at a loss.

- Around 71% of Bitcoin UTXOs remain profitable, while roughly 28% are currently underwater, reflecting stress among short-term holders.

- Bitcoin exchange reserves have fallen by about 204,000 BTC in 2026, potentially tightening supply and setting the stage for a price surge.

At the time of the report, Bitcoin (BTC) was trading around $69,446, with blockchain data showing that 71.41% of all unspent transaction outputs (UTXOs) remain in profit.

UTXOs represent Bitcoin that has not been spent since its last transaction and are often used to gauge investor profitability across the network.

Despite the majority of holders sitting on gains, roughly 28.58% of UTXOs are currently at a loss, signaling that some market participants, primarily short-term traders, are experiencing financial stress.

CryptoQuant analysts say this pressure is largely concentrated among short-term holders rather than large investors.

Retail selling contrasts with whale dormancy

Data from the Spent Output Profit Ratio for short-term holders (SOPR-STH) shows a reading near 0.97, indicating that this group is selling coins at a loss.

This dynamic suggests that the current selling pressure is driven primarily by retail investors exiting positions during periods of market volatility.

Meanwhile, large holders—often referred to as whales—have remained largely inactive, with older bitcoin holdings showing little movement on-chain.

Analysts interpret this dormancy as a sign that institutional or long-term investors remain confident in Bitcoin’s broader market outlook.

Exchange reserves decline as coins move off trading platforms

Another key signal highlighted in the analysis is the continued decline in Bitcoin exchange reserves.

Year-to-date, reserves have dropped from 2.990 million BTC to 2.786 million BTC, representing a reduction of roughly 204,000 BTC across trading platforms.

Such outflows often indicate that investors are transferring coins to cold storage or long-term custody wallets rather than preparing them for immediate sale.

According to CryptoQuant, this trend suggests coins are gradually moving from “nervous hands” to longer-term holders.

The combination of falling exchange reserves and inactive whale wallets could set the stage for a potential supply shock.

A supply shock occurs when sell-side liquidity becomes scarce, meaning fewer coins are available for sale on exchanges. If demand rises during such conditions, prices can move sharply higher.

CryptoQuant analysts argue that the current market environment reflects “fear exhaustion,” where retail capitulation gradually clears excess selling pressure.

If that forced selling cycle ends while long-term holders continue to hold their positions, the market could enter a phase where reduced supply amplifies the impact of new demand on Bitcoin’s price.

Prosecutors asked a federal judge to deny Sam Bankman-Fried’s bid for a new trial, arguing that the former FTX chief failed to meet the legal standard for retrial. The filing arrives as Bankman-Fried continues to press post-conviction appeals while the fallout from FTX’s collapse remains a touchstone for regulators and investors alike. In the February motion, prosecutors contend that testimony from former FTX executives Ryan Salame and Daniel Chapsky does not rise to “newly discovered evidence” and therefore should not warrant another trial, according to court documents cited by Bloomberg. The broader case — which culminated in a November 2023 verdict on seven counts of fraud and conspiracy and a 25-year prison sentence — continues to unfold through procedural challenges rather than fresh courtroom battles. The legal trajectory now centers on whether the retrial motion will proceed and how the Second Circuit will handle ongoing appeals.

Key takeaways

- Prosecutors maintain that the bar for retrial is not met because the witnesses cited by the defense were known to the defense before the 2023 trial, undermining the claim of newly discovered testimony.

- The defense argues that testimony from Salame and Chapsky could alter the government’s portrayal of FTX’s finances, potentially weakening the prosecution’s narrative.

- Judge Ronnie Kaplan has not yet ruled on whether the motion for a new trial will move forward; prosecutors were ordered to respond by March 11.

- Bankman-Fried remains engaged in an appellate battle in the US Court of Appeals for the Second Circuit, separate from the retrial motion.

- Public speculation about possible presidential pardon has accompanied the legal proceedings, though public signals from political figures have varied and progress remains uncertain.

Sentiment: Neutral

Market context: The case sits at the intersection of a high-profile enforcement effort against a failed crypto exchange and broader concerns about market integrity, investor protections, and regulatory clarity in the wake of FTX’s collapse.

Why it matters

The pursuit of a retrial in Sam Bankman-Fried’s case underscores how federal courts handle post-conviction challenges in complex financial fraud prosecutions tied to the crypto sector. The defense’s argument revolving around “newly discovered evidence” hinges on whether testimony from Salame and Chapsky truly represents information that could alter the outcome of the trial, or whether it is something the defense could have anticipated given the broader context of FTX’s finances. The prosecutors’ counterargument, grounded in standard legal thresholds, is a reminder that retrials are far from routine and require tangible, timely facts that could meaningfully shift juror conclusions.

Beyond the courtroom mechanics, the proceedings carry implications for market sentiment, investor trust, and the regulatory posture toward crypto entities. The case has already shaped debates about how closely government witnesses’ accounts align with the realities of a quickly evolving crypto business, and whether retrospective disclosures can meaningfully affect previously admitted narratives. As the Second Circuit review progresses, the crypto industry will watch for signals about how aggressively courts will test witness credibility and financial disclosures in high-stakes prosecutions tied to digital-asset platforms.

On the political front, the possibility of a presidential pardon has lingered alongside courtroom developments. While public comments from figures such as former President Donald Trump have varied, the absence of a clear public commitment to pardon Bankman-Fried leaves the legal avenues—appeal, retrial, or other remedies—as the dominant channels for potential relief. The interplay between criminal rulings and political signals continues to shape expectations about how the sector is treated at the highest levels of government, even as the immediate judicial question remains narrowly focused on the retrial standard and the admissibility of newly presented testimony.

The procedural cadence in this matter remains precise: the defense’s motion was filed in February, prosecutors were directed to file a response by March 11, and the court will then decide whether the retrial request advances to a full consideration. In parallel, Bankman-Fried’s appeal in the Second Circuit proceeds on its own timetable, potentially setting up a long legal saga that could influence how future cases are framed and adjudicated in the crypto space.

What to watch next

- March 11: Deadline for prosecutors’ response to the retrial motion, and any subsequent ruling on whether the motion will proceed.

- Judicial rulings in the Second Circuit regarding the ongoing appeal of Bankman-Fried’s conviction and sentence.

- Any new filings or突inations from the defense that could outline additional grounds for post-conviction relief.

- Related public statements or filings from the parties that could influence the narrative around FTX’s finances and the government’s portrayal at trial.

Sources & verification

- Bloomberg report detailing prosecutors’ response and the status of the retrial motion, including the claim that the witnesses cited by the defense were not newly discovered (Bloomberg: sam-bankman-fried-shouldn-t-get-new-trial-prosecutors-argue).

- Cointelegraph articles covering SBF’s retrial efforts, the government’s response, and related court actions (SBF new trial fraud case; SBF trial court government response; FTX SBF Caroline Ellison Donald Trump; Donald Trump no pardon SBF).

- Public information on Bankman-Fried’s November 2023 conviction on seven counts and the subsequent 25-year sentence (as reported in coverage linked above and related Cointelegraph reporting).

Retrial bid in the SBF case: prosecutors push back as court awaits ruling

The dispute over whether Sam Bankman-Fried deserves a fresh trial centers on the nature of new testimony and what constitutes newly discovered evidence. Prosecutors argue that the proffered witnesses — Salame and Chapsky — were known to the defense before the 2023 trial, calling into question the legal standard for a retrial. This stance is grounded in the procedural framework that governs post-conviction relief, where the bar for presenting new facts that could alter a jury’s verdict is intentionally high. If the court accepts the prosecutors’ reasoning, the retrial request could be dismissed without a full evidentiary hearing.

From the defense side, the motion contends that the witnesses’ testimony could significantly reshape the government’s portrayal of FTX’s financial condition prior to its collapse. The defense argues that Salame and Chapsky could undermine the government’s accounting narrative and, by extension, the jurors’ understanding of the company’s inner workings. The tension between these positions highlights the delicate balance courts must strike between administrative efficiency and ensuring that any potentially exculpatory information is weighed fairly.

Judge Kaplan’s determination will hinge on whether the defense can demonstrate that the testimony constitutes a material discovery that was not reasonably accessible at trial and could have altered the outcome. The government’s response, due by March 11, will likely crystallize the judge’s approach to the motion. If the court signals that it will permit further argument or even a limited evidentiary hearing, the retrial process could extend well beyond a single ruling, prolonging a saga that has already spanned multiple years.

Bankman-Fried’s broader legal journey includes an ongoing appeal in the Second Circuit, adding another layer of complexity to an already intricate case. While the retrial matter is distinct from the appellate path, both avenues collectively shape the fate of one of the crypto industry’s most consequential legal episodes. The conviction and sentencing in 2023 marked a watershed moment, but the post-conviction phase continues to reverberate through courtrooms and industry discourse, influencing risk assessments, regulatory expectations, and the broader narrative surrounding accountability in crypto markets.

Key Takeaways

- Alibaba shares have declined more than 7% in 2026, currently valued at 16x forward earnings — beneath its historical 10-year average of 19x

- The company reports quarterly results March 19, with analysts projecting $1.67 EPS (down 43% YoY) on $42.1 billion revenue

- BABA has been elevated to Morgan Stanley’s premier China technology investment, displacing Tencent from that position

- Mizuho analysts maintain a $195 price objective, while sum-of-parts analysis indicates potential value reaching $213

- Morgan Stanley projects China’s AI chip market will expand to $67 billion by 2030, achieving 76% local production independence

The year 2026 hasn’t been kind to Alibaba shareholders. Shares have tumbled over 7% since January, pressured by competitive threats in artificial intelligence, uncertainty surrounding corporate strategy, and persistent worries about consumption patterns in China.

Alibaba Group Holding Limited, BABA

Yet a mounting chorus of Wall Street voices believes the decline represents an overreaction.

The stock’s current valuation stands at 16 times projected forward earnings. This marks a discount to its decade-long mean of 19x and represents a significant gap compared to Amazon‘s approximately 26.5x multiple. Barron’s observed the shares appear technically oversold based on recent indicators.

Investors will get fresh financial data when Alibaba unveils fiscal third-quarter results on March 19. The Street anticipates earnings per share of $1.67, representing a steep 43% decline from the prior-year period, while revenue is forecast at $42.1 billion — reflecting 9% growth.

While the earnings contraction appears substantial, the revenue trajectory suggests underlying business momentum. Company leadership will have an opportunity to directly address shareholder concerns during the earnings conference call.

A significant area of uncertainty revolves around Alibaba’s Qwen artificial intelligence division. Media reports have highlighted management restructuring and executive exits within that unit, sparking speculation about strategic disagreements regarding AI priorities.

Citigroup’s Alicia Yap acknowledged these reports in her analysis. However, she emphasized that Qwen experienced robust order volumes during the Chinese Lunar New Year holiday period, serving as an important indicator of market demand.

Qwen has been embedded throughout Alibaba’s flagship consumer properties — including Tmall, Taobao, Freshippo, and Alipay. This represents substantial distribution scale for an AI-powered product.

Cloud Division Remains Underappreciated

Mizuho’s Wei Fang contends that Alibaba’s cloud computing segment isn’t receiving appropriate recognition from investors. She characterizes the company’s underlying fundamentals as “incrementally healthier, driven by AI-accelerated growth.”

Fang positions Alibaba’s cloud infrastructure as China’s strongest. The unit competes head-to-head with Amazon Web Services, Google Cloud, and Microsoft Azure on the global stage.

Her formal price objective sits at $195 per share — representing 43% appreciation from present trading levels. When applying a sum-of-parts valuation framework, she identifies even greater potential worth at $213 per share, with e-commerce and cloud operations accounting for the majority.

She additionally calculates that Alibaba’s remaining business segments, combined with its cash holdings and investment portfolio, contribute approximately $25 per share in standalone value.

Morgan Stanley Elevates BABA to Premier Position

Morgan Stanley took a more decisive stance this week, designating Alibaba as its premier investment recommendation within China’s technology sector — supplanting Tencent from that role.

The investment bank emphasized Alibaba’s comprehensive capabilities spanning the entire AI value chain: semiconductor chips, cloud infrastructure, foundational AI models, and consumer-facing applications.

Regarding AI semiconductors specifically, Morgan Stanley asserts Alibaba’s internally developed chips rank among the industry’s best. They position the company as China’s number-one and the world’s fourth-largest cloud infrastructure operator.

The bank also highlights Alibaba’s open-source AI model initiatives, which have achieved extensive international adoption.

Looking forward, Morgan Stanley projects the total addressable market for AI chips within China will expand to $67 billion by decade’s end. Their analysis anticipates domestic production capabilities will satisfy 76% of demand by that timeframe.

Alibaba’s earnings release is scheduled for March 19.

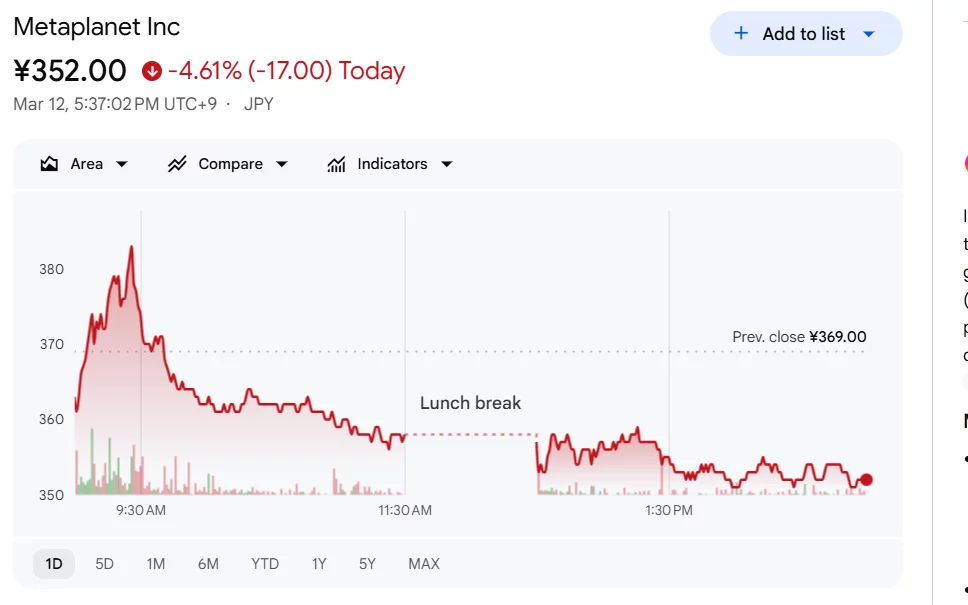

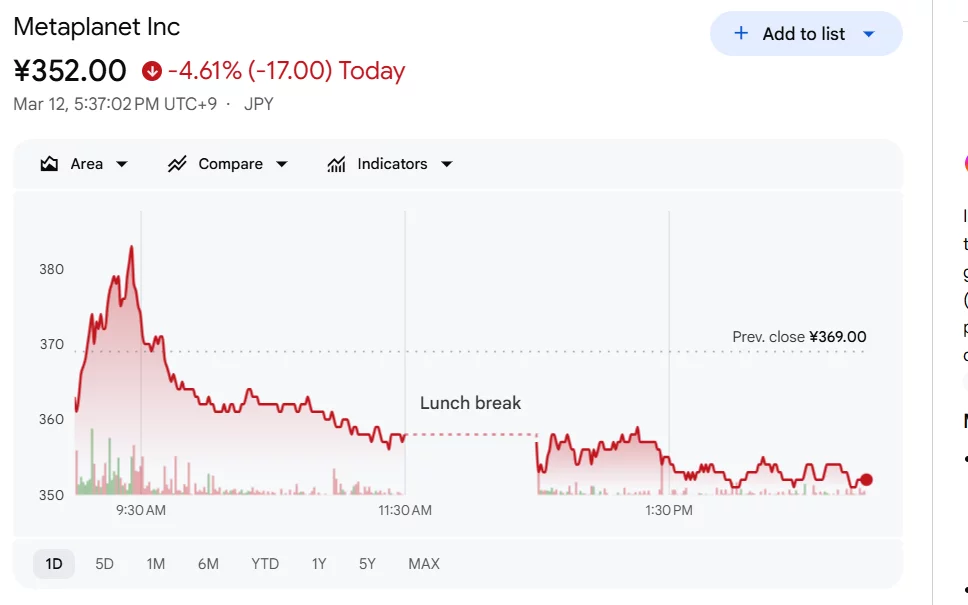

Shares of Japanese investment firm Metaplanet Inc declined Thursday despite the company unveiling a major expansion of its digital asset strategy, including a ¥4 billion venture initiative focused on the Bitcoin ecosystem.

Summary

- Metaplanet Inc shares fell about 4.6% despite announcing two new crypto-focused subsidiaries.

- The company will invest ¥4 billion through Metaplanet Ventures to support the Bitcoin ecosystem in Japan.

- Its first venture investment includes up to ¥400 million in JPYC, Japan’s licensed yen stablecoin project.

The company’s stock closed around ¥352, down roughly 4.6% on the day, according to market data, even as management outlined plans to deepen its involvement in crypto infrastructure and financial services.

In a statement posted by CEO Simon Gerovich on social media, Metaplanet said its board approved the creation of two wholly owned subsidiaries: Metaplanet Ventures and Metaplanet Asset Management.

Metaplanet Ventures will focus on investing in companies building financial infrastructure around Bitcoin in Japan. The firm plans to deploy ¥4 billion over the next several years across sectors such as lending, payments, custody, derivatives, compliance tools and stablecoin infrastructure.

“Metaplanet Ventures is our commitment to Japan’s Bitcoin ecosystem. We’ll be investing ¥4 billion over the next few years into companies building Bitcoin financial infrastructure in Japan,” the post said.

The venture arm will also launch an incubator for early-stage founders and provide grants for open-source developers and researchers working on Bitcoin-related technologies.

Gerovich said Japan already has one of the world’s strongest regulatory frameworks for digital assets but still needs more companies building the infrastructure required for institutional adoption.

The first investment from the new venture unit will be up to ¥400 million into JPYC, which operates Japan’s first licensed yen-denominated stablecoin.

The company is also launching Metaplanet Asset Management, a Miami-based platform designed to connect Asian and Western capital markets through digital credit and Bitcoin-linked investment strategies.

According to the CEO, the new unit will focus on products tied to yield, equity, credit and volatility strategies within digital asset markets.

The expansion reflects Metaplanet’s broader ambition to position itself as a bridge between traditional finance and the emerging Bitcoin capital markets ecosystem.

Metaplanet stock market reaction remains cautious

Despite the strategic announcement, the market reaction appeared muted. The company’s shares fell during the trading session after initially rising earlier in the day.

The decline suggests investors may be waiting for clearer details about the revenue potential of the new initiatives or how quickly the venture investments could translate into returns.

Metaplanet has increasingly positioned itself as a corporate advocate for Bitcoin adoption in Japan, mirroring strategies seen in other publicly traded companies that integrate digital assets into their broader financial strategy.

[PRESS RELEASE – Victoria, Seychelles, March 12th, 2026]

BYDFi announced the integration of its perpetual futures market data into TradingView, enabling traders to access real-time pricing and crypto market signals directly within TradingView charts. The integration supports more efficient workflows by bringing BYDFi derivatives data into a familiar charting environment used by traders worldwide for crypto futures analysis.

Market Signals in View, Strategy in Sync

With BYDFi perpetual futures data available on TradingView, users can monitor price action, volume dynamics, and market structure signals on TradingView while keeping their chart workflow anchored to BYDFi as the data source, ranging from BTCUSDT perpetual futures price action to broader trends across crypto derivatives markets. This reduces context switching for active traders who rely on technical indicators, pattern tools, and multi-timeframe analysis.

BYDFi, Built for Active Derivatives Traders

- Derivatives Depth and Execution: With a derivatives lineup designed for different risk preferences and trading approaches, BYDFi supports 500-plus perpetual contracts with leverage options up to 200x, backed by advanced execution and risk controls for high-leverage crypto trading, helping users approach perpetual contracts trading in a more structured way.

- Global Scale and Responsible Participation: Founded in 2020, BYDFi serves over 1,000,000 users across 190+ countries and regions. BYDFi holds MSB licenses in the U.S. and Canada and is a member of South Korea’s CODE VASP Alliance, reflecting an ongoing focus on operational transparency and responsible market participation.

- Support and Safeguards for Users: Maintaining over 1:1 Proof-of-Reserves with periodic public reporting, BYDFi prioritizes transparency alongside an 800 BTC Protection Fund. 24 by 7 multilingual customer support and timely responses across official channels, including social media, reinforce BYDFi’s user first service standard.

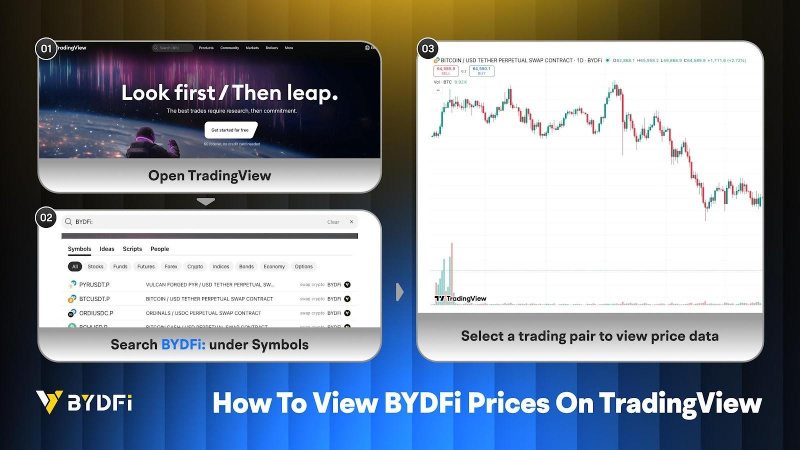

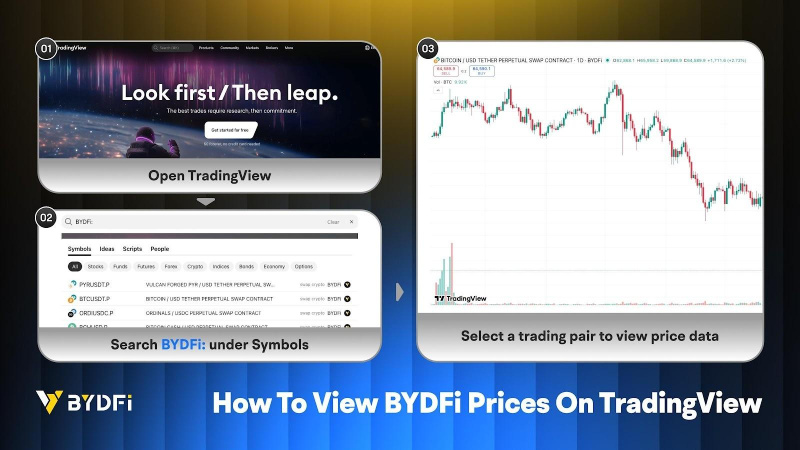

How to Access BYDFi Perpetual Futures Data on TradingView

Users can view BYDFi perpetual futures market data on TradingView in a few quick steps:

- Open Symbol Search on TradingView and enter BYDFi.

- View the full list of available perpetual futures contracts.

- Select a trading pair to view live price data and use TradingView’s analysis tools to refine your market view and timing.

Michael, Co-founder and CEO of BYDFi, commented: TradingView is one of the most widely used charting platforms for traders. Bringing BYDFi perpetual futures market data into TradingView helps traders streamline analysis and stay closer to the signals that matter. BYDFi will continue improving infrastructure, product depth, and user protections to support more informed decision making in fast moving markets.

About BYDFi

Established in 2020, BYDFi is a global crypto trading platform that combines the power of a centralized exchange (CEX) with its on-chain trading engine, MoonX. BYDFi is Newcastle United’s Exclusive Official Crypto Exchange Partner. Recognized by Forbes as one of the Best Crypto Exchanges in Canada for 2026, BYDFi offers intuitive, low-fee trading across Spot and Perpetual Contracts to Copy Trading, and Automated Crypto Trading Bots, empowering both new and experienced traders to navigate digital assets with confidence.

BYDFi is dedicated to delivering a world-class crypto trading experience for every user.

BUIDL Your Dream Finance.

- Website: https://www.bydfi.com

- Support email: cs@bydfi.com

- Business partnerships: bd@bydfi.com

- Media inquiries: media@bydfi.com

Twitter( X ) | LinkedIn | Telegram | YouTube | TikTok | How to Buy on BYDFi

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Stocks Close Mostly Flat as Oil Prices Drop

JPMorgan Sued Over $328M Crypto Ponzi Scheme

Test Your Knowledge With the Collider TV Quiz — March 12, 2026

-

Business6 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

News Videos3 days ago

News Videos3 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Ann Taylor

-

Crypto World3 days ago

Crypto World3 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech1 day ago

Tech1 day agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Sports7 days ago

Sports7 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Politics6 days ago

Politics6 days agoTop Mamdani aide takes progressive project to the UK

-

Business2 days ago

Business2 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Sports4 days ago

Sports4 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

Sports5 days ago

Sports5 days agoThree share 2-shot lead entering final round in Hong Kong

-

NewsBeat17 hours ago

NewsBeat17 hours agoResidents reaction as Shildon murder probe enters second day

-

Tech2 days ago

Tech2 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

NewsBeat7 days ago

NewsBeat7 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Entertainment5 days ago

Entertainment5 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

Business4 days ago

Business4 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business1 day ago

Business1 day agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat2 days ago

NewsBeat2 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech3 days ago

Tech3 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Business3 days ago

Business3 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

NewsBeat20 hours ago

NewsBeat20 hours agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.