Crypto World

Does Botanix’s Failure Prove Bitcoiners Don’t Care About DeFi?

For the past two cycles, Bitcoin DeFi has lived more as a promise than a category.

Programmable Bitcoin has remained a vision held by a certain breed of Bitcoin maxi who believes that the world’s largest cryptocurrency can become productive without losing its security or sound money qualities.

Yet the closure of Bitcoin scaling platform Botanix earlier this month has called that vision into question.

If a well-funded, technically ambitious Bitcoin layer-2 with live apps, integrations and competitive yields can’t attract enough usage to survive, does that mean Bitcoiners simply don’t care about decentralized finance?

Bitcoin DeFi remains a niche proposition in 2026, despite years of being touted as the next big thing.

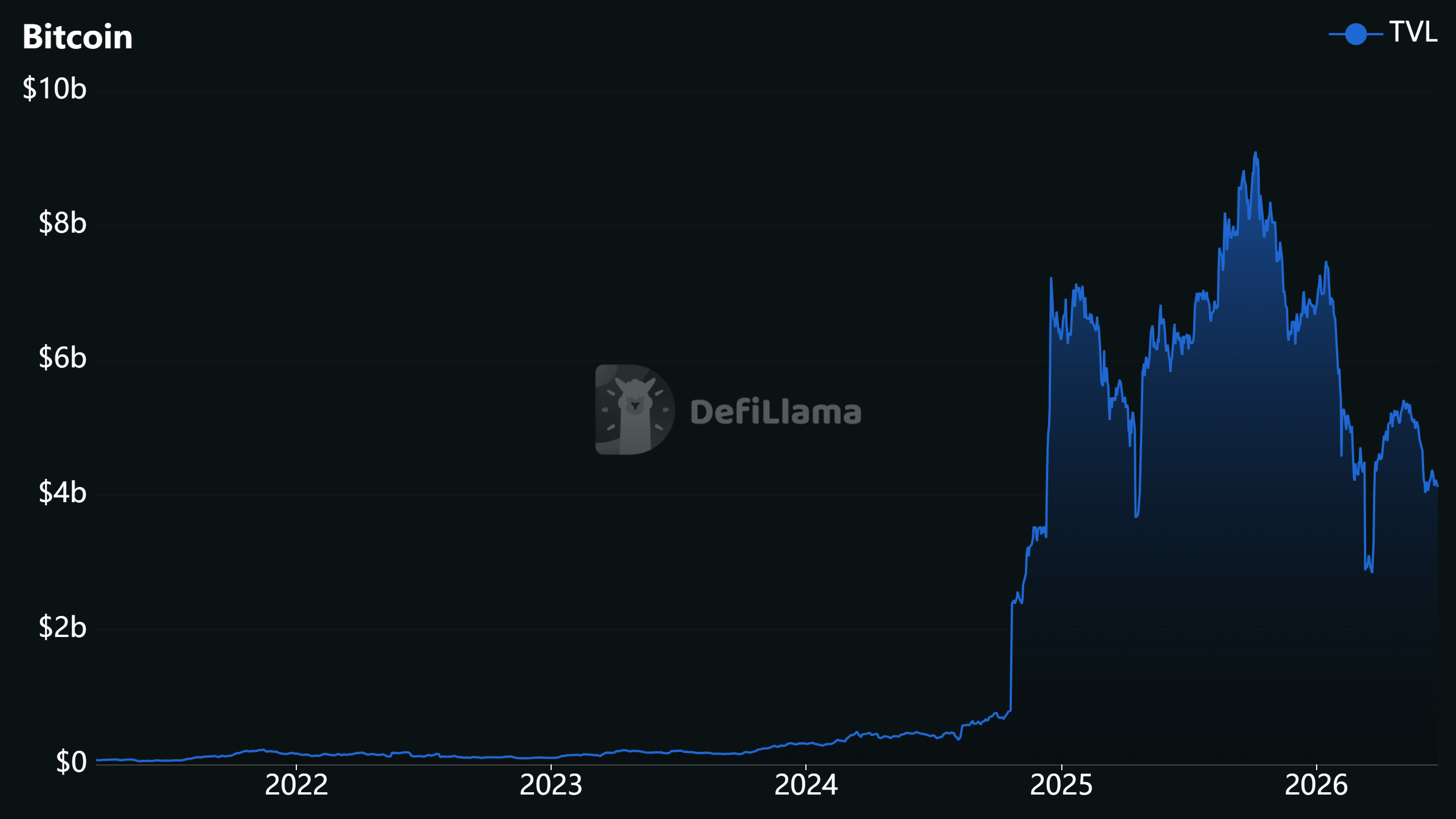

DefiLlama’s dashboard shows just $4.12 billion of total value locked (TVL) across all of the Bitcoin DeFi protocols. That’s a rounding error next to Bitcoin’s $1.2 trillion market cap, and the hundreds of billions held via spot exchange-traded funds, corporate treasuries and custodial accounts.

Andre Dragosch, head of research Europe at Bitwise, told Cointelegraph, “Bitcoin is winning decisively as a monetary asset and as pristine collateral, but the case for Bitcoin as a standalone DeFi execution layer was always structurally weaker than the narrative suggested.”

Botanix closes after four years

When Botanix announced it was winding down after nearly four years of work and a year of mainnet uptime, the team didn’t blame a hack or a regulatory shock; they blamed demand.

Botanix described a chain that “worked” in every technical sense: 25 million transactions, 200,000 wallets, and tens of millions of dollars in bridged funds, yet it never generated the fee volume needed to cover its infrastructure costs.

Users came for the yield, treated BTC as store-of-value collateral, and then largely stuck to passive, buy-and-hold strategies, rather than actively borrowing, trading, or moving funds often enough to generate meaningful fee volume.

Related: Fireblocks to integrate Stacks for institutional-grade Bitcoin DeFi

Like most BTCFi stacks today, Botanix still requires users to bridge their Bitcoin into a tokenized version on a separate Ethereum Virtual Machine (EVM)-based chain before they can access DeFi. That introduces additional bridge and smart contract assumptions that worry many Bitcoiners.

Botanix’s shutdown notice. Source: Botanix

Even so, Botanix co-founder Willem Schroé told Cointelegraph that he wouldn’t have changed the core design. Despite Botanix offering what he described as “the best rates in the industry” and a more Bitcoin-aligned security model than typical wrapped BTC bridges, wrapped BTC on Ethereum still out-competed Botanix.

He attributed that to Ethereum’s “huge infrastructure network and Lindy effect,” as well as a mix of liquidity depth, user experience and regulatory comfort.

What Botanix learned about Bitcoin DeFi

The team concluded that Bitcoin is still viewed as a reserve asset rather than something that has programmable utility.

For most existing use cases like lending, leveraged exposure, or yield, a wrapped BTC position on a large, mature EVM ecosystem such as Ethereum is “genuinely sufficient” for most users. Rather than bridge into a Bitcoin-aligned EVM chain like Botanix, users preferred to stick with wBTC on venues where the liquidity, apps and integrations already exist.

Related: Mercado Bitcoin expands LatAm RWA push with $20M in Rootstock private credit

Botanix also pointed to onchain activity consolidating around venues like Hyperliquid, and major centralized exchanges and retail-facing fintechs that “own the user relationship,” leaving independent infrastructure “rowing upstream” against convenience and branding.

Wilhelm said he hopes Botanix’s wind-down “will definitely be looked at by others,” and framed the process as a professionally managed experiment whose lessons other BTCFi builders should take seriously.

Bitcoiners, DeFi and wrapped BTC

While estimates vary, only a small fraction of Bitcoin’s supply is currently productive in DeFi, and most of that sits in wrapped BTC products on Ethereum and its L2s like Base and Arbitrum, as well as Polygon, Solana and BNB Smart Chain. A smaller percentage is on “Bitcoin L2” chains, with Bitcoin-aligned L2s and sidechains accounting for a modest share of that activity by value.

Tokenized BTC products themselves represent just a sliver of the asset: A May 2026 analysis estimated that roughly $20 billion worth of BTC — less than 2% of the total Bitcoin supply — is circulating on EVM chains in wrapped form.

Total Value Locked (TVL) in Bitcoin DeFi. Source: DeFiLlama

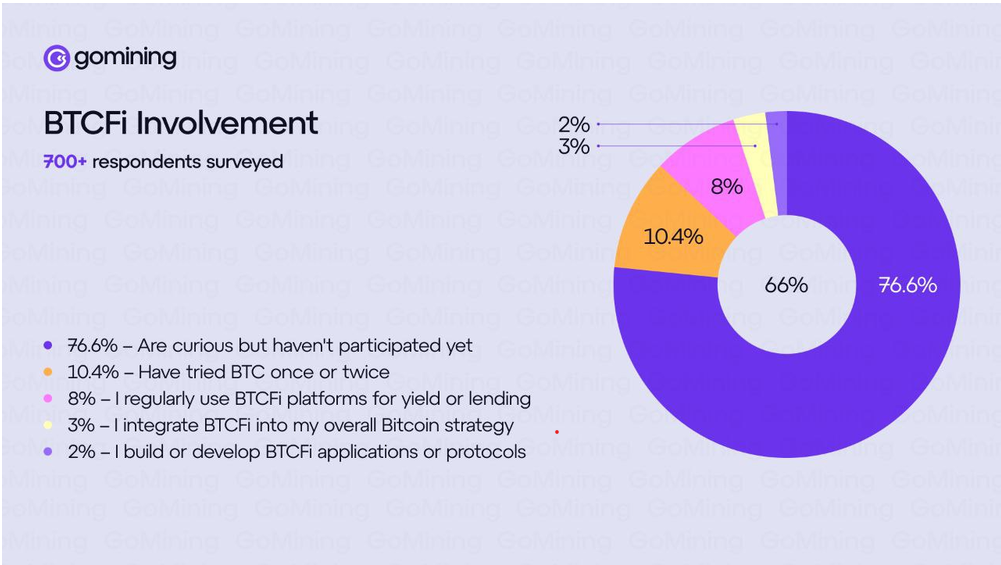

An October 2025 GoMining survey of 730 Bitcoin holders found that 77% of respondents had never used a BTCFi platform, and only 3% integrated BTCFi into their overall Bitcoin strategy.

Even allowing for sample bias (these respondents were plugged-in, survey-answering BTC holders), the numbers show that BTCFi platforms that keep users in Bitcoin-aligned stacks remain a niche activity rather than a mass behavior.

Justin d’Anethan, head of research at crypto private markets advisory firm Arctic Digital, told Cointelegraph, “There is more liquidity and better yields on EVM or SVM [Solana Virtual Machine] native solutions than on BTC solutions, period.”

When clients ask about “putting their Bitcoin to work,” the practical routes, he said, are still centralized desks, exchanges lending out BTC at 2% to 4%, basis trade structures “à la Ethena,” or institutional credit pools like Maple.

Related: Bitcoin recovery meets DeFi tensions as Aave rift deepens: Finance Redefined

He said the big obstacle for most Bitcoiners was the risk of bridging to a less secure Bitcoin L2. For “hardcore BTC maxis,” the default remains cold storage, HODLing and riding price appreciation, rather than trying to “eke out 2-3% with counterparty risk.”

Native BTCFi as a structural mismatch

Dragosch said Botanix’s failure suggested that demand for standalone Bitcoin DeFi execution layers was much weaker than their backers expected.

He argued that capital that “genuinely wants yield has migrated to wrapped BTC on mature, liquid venues rather than bridging into bespoke federations.”

In this view, the problem isn’t just that Bitcoiners haven’t “discovered” native DeFi yet; it’s that the architecture and user base are misaligned. Bitcoin’s base layer is slow, conservative and firmly anchored in the store-of-value narrative.

“Bitcoin as reserve collateral is the durable trade,” Dr. Dragosch said, “the next leg of adoption runs through institutions and balance sheets, not necessarily through onchain execution layers.”

77% of respondents have never used a BTCFi platform. Source: GoMining

Who is still building BTCFi, and for whom?

Diego Gutierrez Zaldivar, chief executive of RootstockLabs, a Bitcoin-secured, EVM-compatible sidechain, doesn’t buy the idea that there’s “no demand” for Bitcoin-backed lending, yield products or broader BTCFi services.

He said the main constraint is trust: putting in place the operational, legal and risk management frameworks that institutions need.

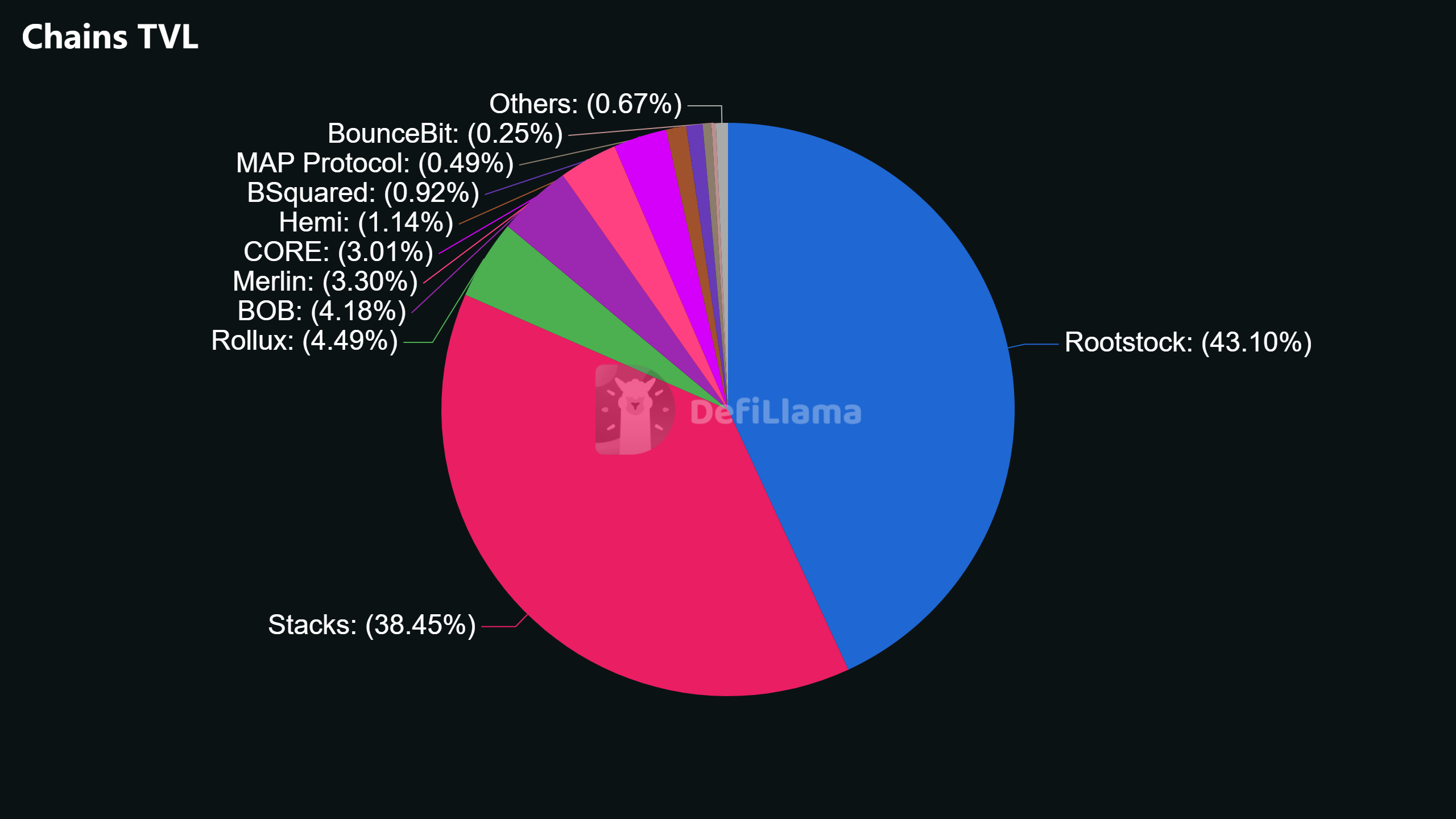

More than 40% of all Bitcoin DeFi activity now runs through Rootstock, he said, including real-world asset settlements and institutional vaults. Over the past year, he said, funds have started asking to deposit hundreds or even thousands of BTC at a time into Rootstock-based products; flows that were almost unheard of two or three years ago.

Chains TVL. Source: DeFiLlama

Orkun Mahir Kılıç is co-founder of Chainway Labs, behind Citrea, a Bitcoin-anchored rollup that keeps user assets inside Bitcoin’s security perimeter and proves its state with zero-knowledge proofs. He argued that cloning EVM DeFi primitives onto Bitcoin is a dead end, and said that Botanix’s experience is a verdict on that model, rather than BTCFi itself.

He told Cointelegraph that “more secure” doesn’t change most people’s behavior.

“People don’t price counterparty risk until something breaks,” he said. ”Where it matters” is for institutions and large holders that need trust-minimized transactions with no custodian to fail.

“For everyone else, the reason to be here isn’t the security guarantee in the abstract; it’s the applications that don’t exist elsewhere.”

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

Bitcoin ended the first half of 2026 near $60,000 after falling about 32% since January, Binance Research reported. Its Half-Year 2026: Macro & Bitcoin report described the decline as a third consecutive quarterly loss across broader financial markets worldwide.

The weak first-half performance also extended Bitcoin’s longer-term drawdown. According to the report, the asset has fallen more than 50% from its October 2025 record high near $126,000. It has also spent 275 days below that peak, underscoring the depth and persistence of the current market downturn.

On-Chain Data Signals Market Stress

On-chain data showed 10.83 million BTC ended the period in unrealized loss, while 9.22 million units remained profitable instead. Binance Research said this marked the first loss-over-profit crossover during the current market cycle, making conditions important for analysts.

The researchers noted similar crossovers have historically appeared near major Bitcoin market bottoms before stronger recoveries eventually followed. However, they cautioned that historical patterns alone cannot confirm the current cycle will produce the same outcome.

Beyond the on-chain signals, Binance attributed Bitcoin’s weak performance mainly to broader macroeconomic conditions rather than crypto-specific developments. The report said markets shifted from liquidity-driven expectations toward economic fundamentals as monetary policy remained restrictive throughout the first half of 2026.

Expectations for interest rates also changed as hopes for aggressive cuts faded. Futures markets instead reflected an 80% probability of another Federal Reserve rate increase before December, adding pressure across financial markets.

Macro Pressures Weigh on Bitcoin

The report also said higher real yields, a stronger U.S. dollar, and tighter liquidity continued to weigh on Bitcoin. While technology stocks rebounded on optimism around artificial intelligence, BTC lagged behind many major asset classes during the same period.

A resilient U.S. economy also reduced expectations that the Federal Reserve would cut interest rates soon. Binance Research said artificial intelligence was a key driver of first-quarter economic activity. At the same time, core PCE inflation rose to 3.4%, its highest level since late 2023, reinforcing concerns that price pressures remain stubborn.

That backdrop also weakened demand for crypto. U.S. spot Bitcoin ETFs recorded $5.4 billion in net outflows during the first half of the year.

The post Down 32% in 6 Months: What Binance Research Says About Bitcoin’s Next Move appeared first on CryptoPotato.

Storj filed for bankruptcy protection on Sunday. The company says its network still works and STORJ tokens still work. Its owner made similar promises nine months ago.

Storj now wants to hand token holders a slice of the rebuilt company. But a judge must approve that. And creditors get paid first.

Why Storj Filed Chapter 11

Storj Labs filed in a federal bankruptcy court in West Virginia. The case number is 5:26-bk-00512.

Follow us on X to get the latest news as it happens

Chapter 11 is not a shutdown. It lets a company keep trading while a court helps it clear its debts.

Storj says those debts are old. They came from an earlier phase of the business. The company cannot grow its way out of them.

“The business underneath is strong and right-sized. What holds it back are legacy obligations from an earlier chapter.”

That was Kaloyan Raev, Storj’s director of software engineering. He also signed the letter to token holders, not Chief Executive Colby Winegar.

What It Means for STORJ Holders

Nothing changes for the token today, Storj says. Data still moves across tens of thousands of storage locations in more than 100 countries.

The company plans to offer holders equity in the new Storj. Equity means part-ownership. The rules for who qualifies have not been written yet.

Those rules will matter. About 143.8 million STORJ trade freely out of 425 million in total. Two-thirds of the supply sits elsewhere.

Bankruptcy also has a payment order. Creditors come before owners. Storj’s letter to token holders admits it can promise intent, not results.

The Warning Sign From October

Inveniam Capital Partners announced it was buying Storj on Oct. 22, 2025. It promised no changes to contracts, pricing, or leadership.

“We’re particularly excited to integrate the STORJ token into our ecosystem, driving greater utility and alignment across our platforms.”

That was Patrick O’Meara, Inveniam’s chairman and chief executive. STORJ traded near $0.1872 that day. It has fallen about 60% since.

A closer warning came this month. MVMT Labs filed Chapter 11 in Delaware on July 15. Its Movement (MOVE) token hit a record low of $0.00964 ten days later.

STORJ has held up so far. It trades near $0.0745, up 1.5% on the day. Volume is $5.6 million and market value is $10.7 million.

The wider sector is soft too. Storage and infrastructure tokens have lagged even as network usage grew.

Storj says it will share court dates as they land. But the fine print of the equity offer will decide what holders actually get.

The post Storj Chapter 11 Raises the Biggest Question for STORJ Token Holders appeared first on BeInCrypto.

Some analysts say Bitcoin (BTC) could reach $200,000 if the CLARITY Act becomes law. That is a very big if. Seven roadblocks now stand between the bill and a Senate vote.

The CLARITY Act would decide which US agency polices crypto. It has sat on the Senate’s to-do list since June 1 without a vote.

Why $200,000 Depends on One Bill

Start with the number. It describes one scenario, not a firm forecast. Research desk FM Intelligence sees Bitcoin between $135,000 and $200,000 over the next year. It gives that outcome one-in-four odds, and only if the bill is signed before the November midterms. Its main case is far lower at $95,000 to $130,000, per its published scenarios.

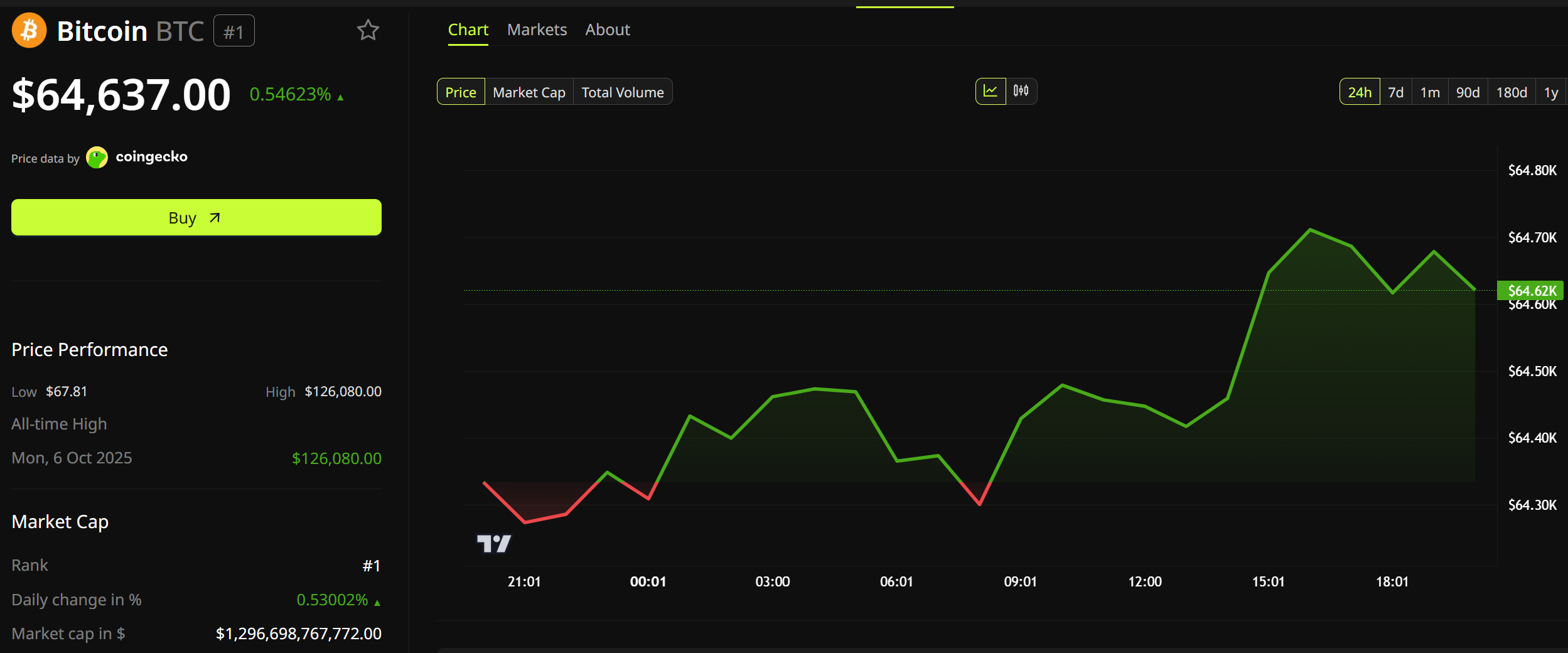

Now look at the gap. Bitcoin trades at $64,671, up 0.48% in a day, with a market value of $1.29 trillion.

Reaching $200,000 means the Bitcoin market price would need to roughly triple. It already sits about 49% below its record of $126,080, set on October 6, 2025.

Sentiment has turned this month, though. Treasury Secretary Scott Bessent said on July 21 that Congress was on the “1-yard line.” Bitcoin jumped toward $67,000, ending roughly 15% above its early July low.

“The formal passage of the Clarity Act into law will be the ultimate catalyst, sparking a new bull market as institutional allocators race to gain exposure out of a fear of missing out,” Forbes reported, citing CK Zheng of ZX Squared Capital.

CK Zheng once ran risk for Credit Suisse. He now runs the hedge fund ZX Squared Capital.

Wall Street Has Already Priced In Some Failure

Big banks have moved the other way. Citi cut its 12-month Bitcoin target to $82,000 on July 1. That was its second cut of 2026. The bank opened the year expecting $143,000, then trimmed that to $112,000 in March.

Its target has fallen 43% this year. Each time, Citi blamed the stalled bill rather than Bitcoin.

Alex Saunders leads the bank’s macro and decentralized finance (DeFi) research. He warned in March that the window for US legislation was closing.

Standard Chartered is warmer but still modest. Geoffrey Kendrick kept its year-end target at $100,000 in mid-July, which would need a 55% climb.

7 Roadblocks in the Bill’s Way

The following roadblocks make the case for what may make the Clarity Act not get the passage analysts are wagering their passage best on.

1. The senators blocking it are not crypto opponents

Seven Democrats rejected the current text in a joint statement on July 22. They are Catherine Cortez Masto, Angela Alsobrooks, Cory Booker, Ruben Gallego, John Hickenlooper, Mark Warner and Raphael Warnock.

Here is the surprise. All seven voted for the GENIUS Act, the stablecoin law, in June 2025.

That bill passed 68-30 with 18 Democrats behind it, Senate records show. Trump signed it into law weeks later.

Elizabeth Warren voted against it and remains opposed today. She was never a winnable vote, so she is not the obstacle.

The wall is built from proven crypto supporters.

2. Republicans cannot reach 60 without them

Senators can stall any bill by refusing to end debate. Breaking that stall takes 60 votes. Republicans hold 53 seats, so seven must come from Democrats.

3. Trump earned $1.4 billion from crypto

Senate Banking’s minority staff reviewed the President’s financial disclosures. They found more than $1.4 billion in crypto income for 2025 alone.

World Liberty Financial, the Trump family’s DeFi venture, supplied $799 million. The $TRUMP meme coin added another $636 million.

4. Only Trump’s Justice Department could enforce the new rules

Republicans released fresh ethics language on July 22, and Trump agreed to it. Ranking Member Warren says it has holes.

State attorneys general could not enforce it, she argues. The rules would also expire once Trump leaves office.

“Donald Trump raked in more than $1.4 billion from cryptocurrency ventures, and this bill does nothing to prevent him from vacuuming up his next $1.4 billion in crypto profits… This bill should be dead on arrival,” said Senator Elizabeth Warren.

Follow us on X to get the latest news as it happens

5. The real deadline is August 7

The Senate’s summer break starts August 10, its own calendar shows. Friday, August 7 is therefore the last working day before members head home.

6. September offers only 14 working days

Senators return on September 14. They leave again on October 5 to campaign for the midterms.

That leaves 14 scheduled working days. It is a thin window for a bill that took a year to negotiate.

7. The House may reject the Senate’s version

Chairman Tim Scott moved the bill through committee 15-9 on May 14. The Senate then swapped in its own text.

The House passed a different version 294-134 in July 2025. It must now accept the 300-page Senate draft text or negotiate a compromise.

The Trap at the Center of the Bill

Traders have turned optimistic quickly. On Kalshi, the odds of passage before April 2027 jumped to 52% from 33% in one week.

Yet the bull case contains a trap. Bitcoin needs the bill signed before the midterms. The unresolved fight is over how much the President may keep earning from crypto.

Passing it would hand Trump a win weeks before voters decide control of Congress. Blocking it costs Democrats little, since the hurdles facing the bill run out the clock anyway.

Seven senators who already backed crypto once must decide whether this version is worth the price.

The post Analysts See Bitcoin at $200,000 on CLARITY Act Passage, But 7 Roadblocks Remain appeared first on BeInCrypto.

Sberbank, Russia’s largest bank, says it plans to roll out cryptocurrency trading infrastructure by Dec. 1, including a “digital depository” designed to record customers’ crypto ownership and handle transactions largely outside the public blockchain.

Interfax reported that the depository will track rights in clients’ cryptocurrency positions and process most transfers off-chain, while Sberbank will also run active wallets for deposits, withdrawals, and client-initiated transfers.

Key takeaways

- Sberbank’s scheduled Dec. 1 rollout would add a regulated-style custody and settlement layer, using a digital depository to record ownership and process transactions off-chain.

- Russia’s crypto market framework is progressing toward an effective date of Sept. 1, 2026, defining regulated participant categories and expanding central bank oversight.

- Regulatory preparation is unfolding alongside intensifying EU and UK sanctions affecting crypto-asset service providers linked to Russia-related activity.

- Investors and market participants should watch how Russia’s central bank sets licensing rules and eligibility for which assets can be offered through intermediaries.

Sberbank’s digital depository: custody and off-chain settlement

According to Interfax, the digital depository will serve as the core component of Sberbank’s planned infrastructure. It is intended to maintain records of customers’ cryptocurrency rights and to account for transactions outside the main blockchain.

The state-affiliated press service quoted Alexander Vedyakhin, Sberbank’s first deputy chairman of the management board, explaining that the depository would also support transfers requested through “active wallets.” In other words, customers’ interactions—depositing, withdrawing, and moving crypto via the bank—would be handled through a banking-operated system that mirrors custody and payment workflows more than traditional on-chain exchange mechanics.

The practical implication is that, if implemented as described, Sberbank could reduce reliance on direct peer-to-peer blockchain settlement for everyday client movements, instead concentrating transaction processing and ownership accounting inside the bank’s infrastructure.

Russia’s regulated crypto framework heads toward 2026

The Sberbank announcement arrives as Russia’s legislators have advanced the country’s first comprehensive crypto market framework. Earlier in the month, lawmakers completed final readings on a bill intended to bring crypto trading, custody, and settlement into a regulated financial system.

Earlier coverage from Cointelegraph noted that the bill would grant the Bank of Russia broad oversight of the regulated market. That oversight would include determining which crypto assets may be offered via licensed intermediaries and issuing implementing regulations.

Cointelegraph’s reporting also highlighted that the central bank has established liquidity thresholds for participating in the regulated market. Those thresholds include an average market capitalization above 5 trillion rubles (about $64 billion) and an average daily volume above 1 trillion rubles (about $12.8 billion) over a two-year period.

Once the framework takes effect, it establishes five categories of regulated market participants: crypto exchanges, brokers, asset managers, custodians, and exchange service providers. The framework is set to define what market participants can do—such as buying, selling, holding, and exchanging crypto assets—as of the effective date, Sept. 1, 2026.

Infrastructure rollout meets tightening sanctions environment

While Russia builds out domestic infrastructure, external compliance pressure continues to rise. The move toward a working crypto system inside Russia is unfolding as the European Union expands sanctions targeting Russia amid its war on Ukraine.

Last week, the EU listed cryptocurrency exchange HTX (formerly Huobi Global) among sanctioned entities. In a Thursday decision, the European Council amended earlier measures “in view of Russia’s actions destabilizing the situation in Ukraine,” adding HTX to a list of 18 entities “providing crypto-assets services or payment services established outside of the Union that are significantly frustrating the purpose of the prohibitions” against Russia.

Earlier, Cointelegraph reported that EU officials said they would prohibit Belarusian nationals and residents from owning, controlling, or managing crypto exchanges and digital asset service providers, aligning the approach with the EU’s Markets in Crypto Assets (MiCA) framework.

The sanctions on HTX were not limited to the EU. The UK government imposed similar measures in May, stating there were “reasonable grounds to suspect” HTX supported Russia’s government by using financial services and funds facilitated by sanctioned entities.

For market participants, the key tension is that Russia is tightening domestic regulation while many foreign-facing crypto service providers remain exposed to sanction risks and compliance constraints. That gap can shape where liquidity flows, which counterparties can operate with certain clients, and how banks and exchanges structure their services.

What to watch next: licensing mechanics and depository operations

Sberbank’s planned digital depository—alongside the broader Russia framework set for Sept. 1, 2026—puts the spotlight on implementation details. Readers should watch how the Bank of Russia operationalizes licensing requirements, how asset eligibility is defined under the liquidity thresholds, and whether bank-operated off-chain custody and transfer accounting becomes a model for other regulated intermediaries.

Outside Russia, the sanctions trajectory suggests that cross-border partnerships and access to international payment rails may remain a moving target for crypto businesses tied to the region.

It was less than a year ago when the Ethereum validator exit queue had stretched for 45 days as millions of tokens waited to be unlocked from staking.

Today, that queue has completely emptied out, while the number of ETH actually staked continues to grow to a new record.

No One Wants to Unstake ETH

Current data from ValidatorQueue shows that there are zero ETH waiting to be unstaked from the network. This means that if anyone decides to unstake their altcoin holdings, they can do so immediately, subject only to the protocol’s normal withdrawal process.

This is a significant turnaround from Q3 last year, when the exit queue had swelled to roughly 2.6 million coins. Validators were forced to wait up to 45 days before they could withdraw their holdings. At the time, Ethereum co-founder Vitalik Buterin defended the extensive period, arguing that it’s an important element of the network’s defense.

The narrative has completely flipped now. ValidatorQueue shows that over 2.5 million ETH is currently waiting to enter staking, translating into an estimated activation delay of nearly 44 days. Investors are willing to wait for a month and a half just to begin earning staking rewards on their ETH holdings.

This shifted imbalance suggests that investors are confident in Ethereum’s long-term outlook to remain strong despite the year-to-date price retracement. It also removes one of the most significant concerns from last year – that millions of staked ETH could suddenly flood exchanges if validators decide to cash out.

Record ETH Is Locked

The broader staking picture has also continued improving as the total number of active validators securing the network has neared 900,000. Almost 41 million ETH is currently staked, which is equivalent to roughly 33.6% of the entire circulating supply. This is the highest percentage in the network’s history, and it means that every one out of three ETH is locked in staking rather than sitting on exchanges or actively circulating.

Tom Lee’s Bitmine remains a leader in this field, having staked over 4.9 million tokens through its institutional platform MAVAN.

Although staked ETH is not permanently removed from supply, it is generally considered less liquid because validators must go through Ethereum’s withdrawal process before they receive access to those holdings.

However, Merlijn The Trader reported a rather intriguing and unexpected twist. The record amount of staked ETH comes even as staking rewards are down to 2.62% per year from 3.05% and issuance has increased from 0.757% to 0.842%.

The post Nobody Wants to Unstake Ethereum Anymore: Here’s Why It’s a Big Deal appeared first on CryptoPotato.

People shared private chats with Claude. Then strangers found those Claude chats indexed by Google, wallet details and all.

The chats also held access keys, CVs and company files. Anthropic, the company behind Claude, had not addressed the matter as of this writing.

Claude Chats Indexed by Google, Explained

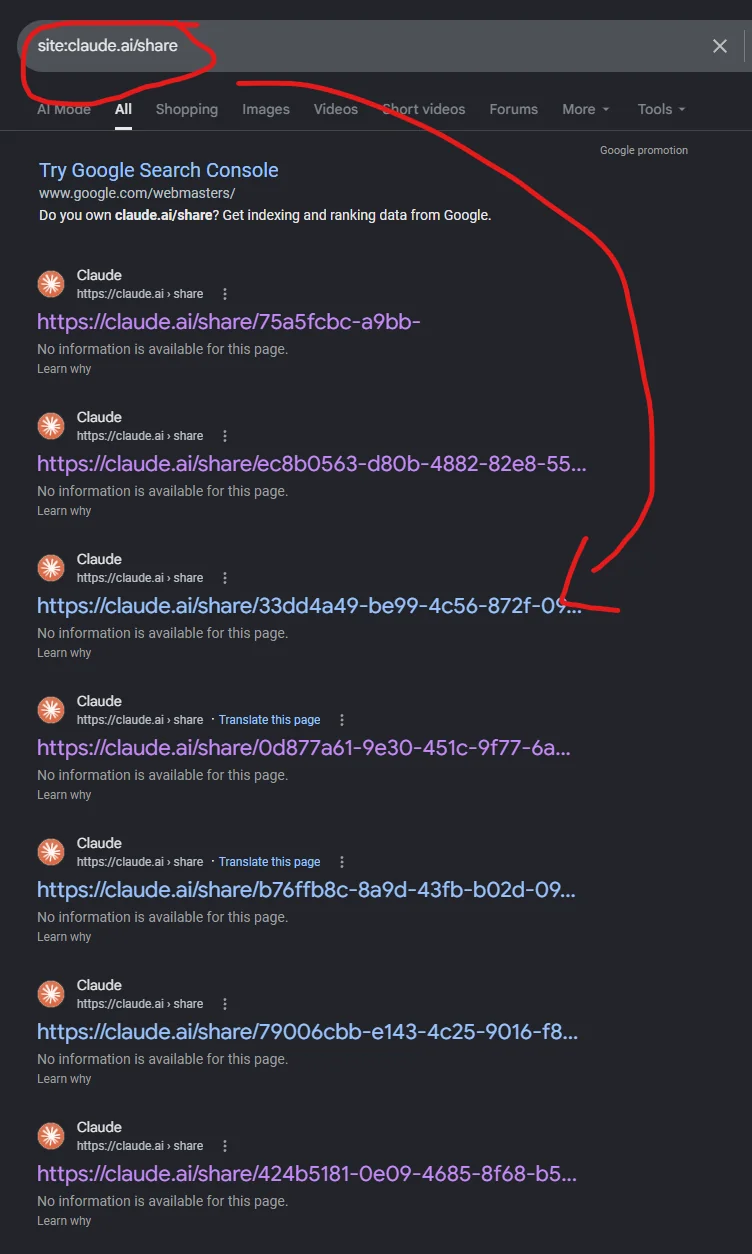

A Reddit thread over the weekend showed the problem. One simple search brought up page after page of shared Claude chats.

People in the thread blamed a missing “noindex” tag. That tag tells Google to hide a page. The real cause looks different. Anthropic’s robots.txt file tells search engines to skip its share pages.

Here is the catch. Google will not open a blocked page. So it never sees the hide tag inside.

Picture a locked door with a note taped behind it. Nobody gets in. Nobody reads the note either.

Google can still show the web address. Other sites link to it, so Google knows it exists. Google just cannot see what sits on the page. Its own guide spells this out.

That fits the screenshots going round on X. Under each Claude link, Google said “No information is available for this page.” Bing showed a similar line.

So the chats never appeared in search previews. But anyone who spotted a link could click it and read the lot.

What the Share Button Really Does

Claude chats are private by default. That changes only when a user clicks Share.

Share builds a public web page. It holds every message sent up to that moment.

Two things stay out, according to Anthropic’s own help pages. Uploaded files are not included. Nor is raw data pulled in by connected tools.

Team and Enterprise accounts cannot share in public at all. This one lands on free, Pro and Max users.

Old links sit under Settings, Privacy, then Shared chats. Click Unshare to kill one.

Why Crypto Users Should Care

Developers flagged it, noting that wallet details and login credentials sat among the results, with some allegedly being able to read strangers’ chats through Brave Search.

For crypto, the stakes differ. A leaked password can be changed. A leaked private key cannot, as BeInCrypto has shown in past private key leak losses.

Small wallets are already the main target. Chainalysis counted 158,000 personal wallet hacks in 2025. Those hit 80,000 people and cost $713 million.

The 2022 figure was 54,000. None of it is tied to AI chats. It simply shows where thieves now spend their time.

More traders also connect AI to wallets to move funds and check code. Researchers have flagged tools that could expose wallet seed phrases as well.

One caution belongs here. Nobody has confirmed a seed phrase or a working key in the indexed chats. Nobody has reported stolen funds either.

Some developers pushed back too. Those pages were public by choice, they argued.

What Happens Next

The pages have gone from search. They have not gone away. Anyone with a saved link can still open the chat. Only the owner can stop that, by unsharing.

This has happened before. Google indexed just under 600 Claude chats in September 2025, as Forbes reported. OpenAI had dropped its own public sharing option a month earlier. It now faces a ChatGPT data sharing lawsuit.

A clean fix exists. Let Google open the share pages, then add the hide tag there.

Whether Anthropic does it will decide if this happens a third time.

The post People Found Crypto Wallet Data in Claude Chats Indexed by Google appeared first on BeInCrypto.

The U.S. Commodity Futures Trading Commission (CFTC) has issued another warning to prediction market operators, urging them to ensure that contract “self-certifications” are detailed and product-specific when event contracts cover a wide range of outcomes.

In an advisory published Friday, the CFTC said that—despite ongoing policy discussions and proposed rulemaking for prediction markets—operators may still certify certain event contracts as compliant with the Commodity Exchange Act and applicable CFTC regulations under the existing self-certification framework, so long as they follow the statutory requirements.

Key takeaways

- The CFTC warned that platforms should not use broad, template-style self-certifications for events contracts that cover many permutations.

- According to the agency, “self-certified” submissions must include the terms and conditions for each proposed variation and a concise explanation of compliance for the product as structured.

- The latest advisory echoes a prior CFTC warning earlier this year about overly generalized filings.

- The guidance arrives shortly before the CFTC’s July 27 deadline for comments on proposed rule amendments tied to public interest determinations for certain event contracts.

Why the CFTC is pushing back on template certifications

The CFTC’s Friday notice focused on how operators describe and certify event contracts under the agency’s jurisdiction. The regulator highlighted concerns with the number of instances where platforms have “self-certified” event contracts without providing sufficient detail for each version of the product.

In particular, the CFTC criticized submissions that do not include, for each proposed permutation of the contract, the terms and conditions and a concise explanation and analysis addressing compliance with respect to the product’s terms, the underlying commodity, and the product’s regulatory compliance.

As the CFTC put it in its July 24 announcement, the guidance “reiterates that broad, template-style certifications should not be submitted.” The agency framed this as a compliance issue rather than a change to the underlying legal concept of self-certification.

A repeat warning earlier this year

This is the second time in 2026 that the CFTC has flagged the same type of problem. In March, the Commission issued an earlier warning about submissions that were “overly generalized,” again indicating that template-level descriptions are not adequate when contracts are structured to cover a broad range of event outcomes.

By issuing a follow-up advisory in July, the CFTC effectively signaled that its concerns are ongoing and that it expects operators to make practical adjustments to how they document certifications—especially for contracts with multiple permutations rather than a single, narrowly defined instrument.

The practical takeaway for platforms is straightforward: if an operator is certifying a wide slate of event outcomes under one certification approach, the filing must still be organized in a way that maps to each contract variation and explains how the design fits regulatory requirements.

Advisory timing ahead of public interest rulemaking

The advisory landed just days before the July 27 deadline for submitting comments on the CFTC’s proposed rule amendments related to public interest determinations for certain event contracts that fall under the Commodity Exchange Act’s enumerated activities.

While the Friday guidance largely addresses self-certification behavior, the timing matters because it underscores that multiple regulatory strands for prediction markets are moving at once: day-to-day product certification practices, and longer-term rules for determining when specific types of event contracts should be evaluated or restricted on public interest grounds.

The CFTC has proposed amendments that outline how it determines whether certain event contracts are contrary to the public interest. In the agency’s proposal, it would apply a three-step analytical framework to evaluate contracts, including those involving activities such as terrorism or assassination, as well as gaming-related considerations tied to the enumerated activities listed in the Commodity Exchange Act.

If those proposed amendments are adopted, the CFTC said they would reshape parts of the regulatory landscape for prediction markets by clarifying the evaluation method used for specific contract types. Legal analysis cited in the source notes that the proposal could represent a meaningful shift in how prediction markets are assessed from a public interest standpoint.

What operators and traders should watch next

For prediction market operators, the CFTC’s warning increases pressure to ensure certification workflows produce filings that are not only legally sufficient but also detailed enough to match each contract permutation and the underlying product structure. Investors and traders should watch for how platforms revise their certification documents—and whether the CFTC’s public interest rule amendments, due to be shaped by the July 27 comment process, later alter the types of event contracts that can be listed or how they are evaluated for regulatory compatibility.

The S&P 500 rose 8.28% this year. However, ten of its own stocks lost more than 40%.

Both things are true at once. Investors are paying almost anything for AI. They are dumping whatever they think AI will kill.

AI Fear Crushed Software and Consulting Stocks

The damage is concentrated. Software, consulting and advertising names fill the bottom of the Slickcharts list.

It started in February. Anthropic released a new AI model. Enterprise software stocks sold off hard. Traders called it the SaaS-pocalypse.

Intuit (INTU) is the clearest victim, down 55.27%. It owns TurboTax, which brings in about a quarter of company revenue and profit.

Then cheap AI tax tools arrived. Goldman Sachs analyst Gabriela Borges cut her price target in June to $276, down from $519.

Intuit moved fast. It cut 17% of staff, roughly 3,000 jobs. It also lowered its TurboTax forecast.

The company is now worth about $88 billion, Forbes reported. A year earlier it was worth more than $219 billion.

Accenture (ACN) tells a similar story, down 45.21%. Clients are spending on AI instead of consultants.

New client orders slipped to $19.3 billion from $19.7 billion. Accenture cut its sales growth forecast to between 3% and 4%. The stock fell almost 18% in one day.

Cognizant (CTSH), Gartner (IT) and The Trade Desk (TTD) each lost 44% to 55%. All three sell work that AI can copy.

But the Two Biggest Losers Had Nothing to do with AI

Here is the twist. The two worst stocks fell for old-fashioned reasons.

CoStar Group (CSGP) is down 58.86%, the weakest in the index. Its problem is spending, not AI.

CoStar owns Homes.com, a property listings site. In January it said the site will not cover its own costs until 2029. Profit is not expected until 2030.

The core business is fine. Revenue jumped 23% to $897 million last quarter. Profit was just $3 million.

Investors lost patience. In February, hedge fund D.E. Shaw told CoStar to quit or shrink Homes.com. It said the move could unlock more than $10 billion. CoStar called the campaign “activism malpractice.”

Shareholders backed the board in June. Nasdaq had already dropped the stock from its Nasdaq-100 index in May.

Boston Scientific (BSX) is down 53.59%. It simply grew slower than promised.

In February it expected sales to grow 10% to 11%. By April it cut that to between 6.5% and 8%.

A rival explains why. Medtronic said its heart device sales rose 124% in the United States. It took “an additional 8 points of U.S. share.”

Then bad news piled up. Boston Scientific recalled its Accolade pacemakers. Regulators tied the fault to four deaths and 2,557 serious injuries. It also agreed to buy Penumbra for $14.5 billion.

Where the Money Went Instead

Chip and memory makers took it. Sandisk (SNDK) is up 505.17% this year. Dell Technologies (DELL) rose 247.55%. Micron Technology (MU) gained 222.68%.

Small investors piled in too, feeding the AI capex boom through chip funds. A narrow group of winners now drives the whole index, as data on AI stocks driving gains shows.

Everything else got punished for any slip. Expensive stocks fell hardest when forecasts came down, a danger flagged in recent earnings bubble warnings.

CoStar and Boston Scientific both report results this week. Those numbers will show whether investors were right or just impatient.

The post 10 Stocks Lost Over 40% in 2026 as Investors Dumped Everything AI Might Kill appeared first on BeInCrypto.

The crypto industry, naturally, is urging passage. The common refrain online is that Clarity includes some investor protection rules and creates some structure for crypto products, while not passing the bill would mean there are no investor protections.

If the bill is to pass the Senate before summer recess begins, the first thing to watch for is a motion to proceed on Monday or Tuesday. This kicks off the formal process. If the motion to proceed is filed by Wednesday, one individual following the process said, that would still give the Senate enough time to vote on the bill before August 7, the last day of the summer session.

If the motion to proceed ripens — meaning it’s been an hour into the second day after the motion is filed, according to the Congressional Institute, a not-for-profit organization — there can be a cloture vote, most likely on the amendment in the nature of a substitute (i.e. the new text of the bill). If that passes, there can be another cloture vote later on for the actual passage of the bill.

“Recess deadlines are powerful tools,” Kristin Smith, the president of the Solana Policy Institute, told CoinDesk.

On a practical note, what this most likely means is we’ll see the motion to proceed Monday or Tuesday, two industry sources told CoinDesk, with a possible vote late next week.

The US Commodity Futures Trading Commission (CFTC) has issued another warning to prediction market operators, urging them to follow its rules when certifying event contracts that cover a wide range of possible outcomes. The regulator said some platforms are submitting “self-certified” listings without providing the specific terms and compliance analysis required for each contract permutation.

In an advisory released on July 24 and published as part of a Friday notice, the CFTC reiterated that—despite ongoing policy discussions and proposed rulemaking—operators may still self-certify certain event contracts as compliant with the Commodity Exchange Act (CEA) and CFTC regulations, as long as they do so within the statutory self-certification framework.

Key takeaways

- The CFTC warned that broad, template-style self-certifications for event contracts are not acceptable for listings under its jurisdiction.

- Operators are expected to submit the terms and conditions for each proposed permutation, along with concise explanations tied to the product and the relevant commodity and compliance requirements.

- The advisory underscores the regulator’s view that generalized submissions have been a recurring issue, with a similar warning issued earlier this year.

- The latest move comes just before a public comment deadline tied to the CFTC’s proposed amendments on public interest determinations for certain event contracts.

Why the CFTC is pushing back on “self-certified” event contracts

According to the CFTC’s July 24 announcement, the agency has observed multiple instances where event contracts are being self-certified by platforms without supplying the full details the CFTC says it needs. Specifically, the regulator criticized submissions that do not include the terms and conditions of each proposed permutation, nor a concise explanation and analysis explaining how the product’s terms and conditions relate to compliance expectations.

The advisory frames this as a compliance execution problem rather than a blanket prohibition on prediction market products. The CFTC emphasized that operators can certify certain event contracts without seeking prior commission approval, but they must do so properly under the self-certification structure established by law and CFTC regulations.

In the regulator’s words, broad, template-style certifications should not be submitted. The CFTC’s concern is that generalized paperwork makes it harder to evaluate whether each individual contract listing complies with the CEA and applicable CFTC requirements—particularly when a contract covers a wide swath of events and permutations.

A warning issued twice in 2026

The July 24 advisory is not the first time the CFTC has flagged the issue this year. The agency referenced a similar warning on March 12, again targeting overly generalized submissions. By issuing the guidance for a second time, the CFTC is effectively signaling that it expects corrective action and that it views continued template-style filings as a repeated compliance failure.

For operators, this matters because self-certification is often treated as a faster path to listing products compared with seeking affirmative approval. If the CFTC continues to find that filings lack the required detail, platforms may face heightened regulatory scrutiny, which can translate into delays, requests for additional information, or more direct enforcement consequences—especially for contracts built around broad event categories.

Regulatory timeline: comments due before rule amendments

The advisory arrives shortly before the CFTC’s July 27 deadline for submitting comments on proposed rule amendments related to how the agency conducts public interest determinations for certain event contracts.

Those proposed amendments aim to clarify how the CFTC determines whether specific event contracts are contrary to the public interest under the CEA. The CFTC described the approach as a three-step analytical framework intended to evaluate contracts based on their involvement in certain enumerated activities—such as terrorism, assassination, or gaming—so that only appropriate contracts are listed for trading.

The proximity between the self-certification warning and the comment period is likely not accidental. For prediction market businesses, the next regulatory phase could change how contracts are assessed for public interest risks even if self-certification remains available in some circumstances. Operators will therefore need to reconcile two parallel expectations: submit sufficiently detailed self-certifications now, while also preparing for potential changes in the CFTC’s public interest evaluation standards later.

What changes for operators: from templates to permutation-specific filings

The practical thrust of the CFTC’s message is straightforward: when an event contract can take many forms—or when it is designed to cover numerous permutations—operators need documentation that matches that complexity. The CFTC’s criticism centered on certifications that do not provide, for each proposed permutation, the terms and conditions and a concise compliance explanation tailored to the product’s conditions, the underlying commodity, and applicable compliance considerations.

That means the template approach that may be common for scaled product development—where only a few parameters are varied across listings—could be viewed by the CFTC as insufficient when the certification is expected to demonstrate compliance for each unique configuration.

For market participants such as traders and liquidity providers, the filing quality issue may not directly change how contracts trade day-to-day, but it does affect listing stability and regulatory risk. If contract certifications are challenged, the availability of products could be disrupted, and participants may face sudden changes in trading access or contract availability.

Legal practitioners have also pointed to how the pending amendments could alter the regulatory landscape. Earlier coverage noted that law firm Ropes & Gray said the CFTC’s proposed changes could “rewrite the rulebook” for prediction market contracts, reflecting how significant the public interest determination framework could be if adopted.

What to watch next

With comments due July 27 on the proposed public interest determinations framework, prediction market operators should expect follow-on developments that could refine what the CFTC considers acceptable contract listings and how self-certification must be documented. The key question ahead is whether operators will update certification practices to avoid template-style submissions and how the CFTC will translate its three-step framework into enforceable guidance if the proposed amendments move forward.

Adam Ramsay-Peaty snubs his estranged family while paying tribute to his wife Holly for supporting him during ‘whirlwind’ 24 hours as she watches him reach 50m breaststroke final after 100m heartbreak

Liv Morgan Reacts To Dominik Mysterio Betraying Major WWE Superstar

Hermes AI agent used to automate attack on Thai Finance Ministry

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech6 days ago

Tech6 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat6 days ago

NewsBeat6 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Business5 days ago

Business5 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

NewsBeat5 days ago

NewsBeat5 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Entertainment5 days ago

Entertainment5 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Tech6 days ago

Tech6 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

NewsBeat6 days ago

NewsBeat6 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World6 days ago

Crypto World6 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Tech7 days ago

Tech7 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

-

News Videos3 days ago

News Videos3 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Sports2 hours ago

Sports2 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Sports3 days ago

Sports3 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion3 days ago

Fashion3 days ago16 Dresses for the High Summer Event

-

Tech6 days ago

Tech6 days agoThe 35 Best Board Games for Family Game Night

-

Entertainment7 days ago

Entertainment7 days agoStephen Colbert Returns to Social Media After Late Show End

-

Crypto World6 days ago

Crypto World6 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

You must be logged in to post a comment Login