Crypto World

Dragonfly Launches $650M Fund IV as Co-Founder Reveals the Blueprint Behind Building a Crypto VC Firm

TLDR:

- Dragonfly Capital launched a $650M Fund IV, bringing total assets under management to approximately $4 billion.

- Co-founder Qureshi credits geographic arbitrage between Asia and the US as the firm’s earliest competitive edge.

- Dragonfly avoided trending crypto deals like Terra and Axie, instead backing Ethena and Polymarket at low-interest periods.

- Qureshi argues that non-consensus investments drive the majority of venture returns, making contrarian discipline essential.

Dragonfly Fund IV, a $650 million crypto venture capital fund, has officially launched amid widespread skepticism about the industry.

Dragonfly Capital now manages approximately $4 billion in assets across offices in New York, San Francisco, and Singapore, with around 45 staff members.

Co-founder Haseeb Qureshi recently shared a detailed account of the lessons behind building the firm, offering rare transparency into the mechanics of crypto venture capital.

Starting From Zero: Reputation and Finding a Niche

Dragonfly Fund IV’s story begins long before the launch announcement. Qureshi entered crypto in 2018, just as the ICO bubble collapsed and most participants were exiting the space.

He later partnered with Bo to launch Dragonfly Capital at a time when dominant players like Polychain, Pantera, and a16z controlled the market.

According to Qureshi, first-time fund managers must stake their personal reputation to get started. He wrote that raising from friends, former bosses, and wealthy connections is non-negotiable for a debut fund. Without putting everything on the line, he argued, there is little to no chance of success.

The firm’s early edge was a geographic arbitrage strategy. Qureshi was based in the United States while his partner, Bo operated in Asia.

This east-meets-west positioning helped Dragonfly earn allocations in early rounds, even without leading deals. The approach was demanding, requiring long hours and constant coordination across time zones.

Talent Management and Brand Building as Competitive Advantages

As Dragonfly grew, Qureshi identified talent retention as a major differentiator. He noted that VC firms are notoriously poor at corporate management, including basic practices like mentorship, clear responsibilities, and open communication. Poor management often goes unaddressed because power law returns mask internal dysfunction.

Dragonfly took a different path. The firm invested in giving junior team members stability, voice, and independence.

Qureshi credited this approach for helping retain people who could have joined larger platforms. Over time, those individuals became central to the firm’s performance.

Brand distribution was another focus area. Qureshi stressed that every team member should build a personal audience. He encouraged public writing, social media presence, and individual thought leadership.

Firms that discourage employees from engaging publicly, he wrote, are making a strategic error.

Investment Philosophy: Non-Consensus Bets and Long-Term Discipline

On investment strategy, Qureshi outlined a clear framework. Most returns in venture come from a small number of deals, often just two or three per fund. He pointed out that consensus deals are usually overpriced, leaving little room for outsized returns.

Dragonfly’s biggest wins came from avoiding popular trends. The firm passed on Terra, Axie Infinity, and Yuga Labs during their peaks.

Instead, it backed Ethena shortly after the Terra collapse and invested in Polymarket before the 2024 election cycle drew mainstream attention.

Hsseeb wrote on X: “Every cycle has a narrative that feels irresistible…most of those themes turn out to be a waste of money.” He tied this discipline directly to portfolio construction, warning that trend-following produces a portfolio of “what was popular 18 months ago.”

Qureshi also addressed fundraising timing, noting that the best window to raise capital rarely aligns with the best time to deploy it. Managing that tension, he concluded, is one of the defining skills in venture.

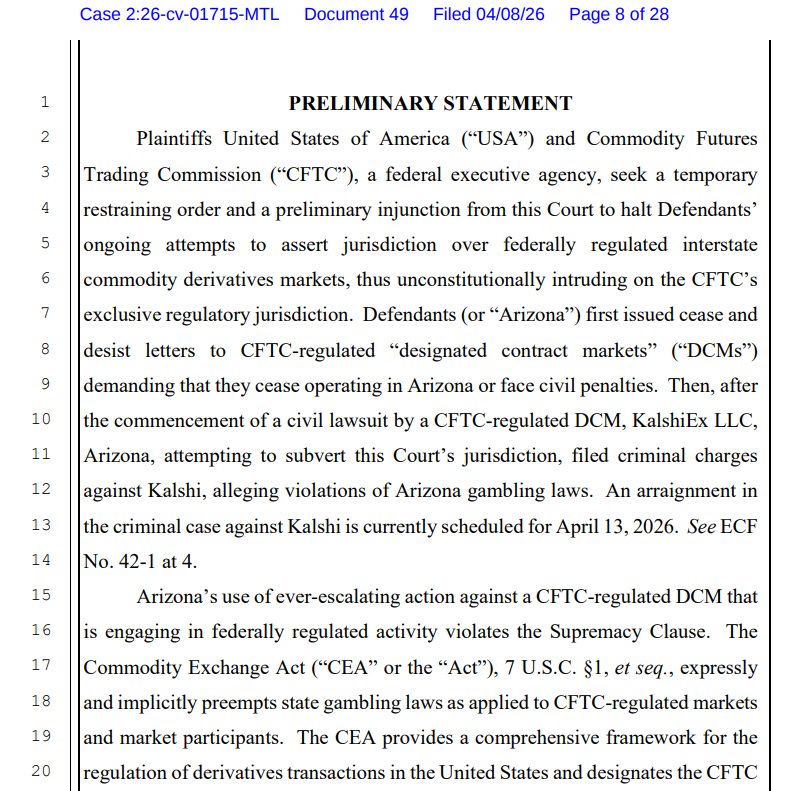

The US Department of Justice (DOJ) and Commodities and Futures Trading Commission (CFTC) asked a federal court to block Arizona from enforcing state gambling law against Kalshi’s event contracts, arguing that they fall under the CFTC’s exclusive authority over swaps markets.

The Wednesday filing argues that event contracts listed on federally regulated platforms such as Kalshi are swaps under the Commodity Exchange Act and therefore fall within the CFTC’s exclusive jurisdiction.

The filing says Arizona’s enforcement effort unlawfully intrudes on the CFTC’s exclusive jurisdiction over federally regulated event-contract markets.

If granted, the order would block Arizona from applying its gambling laws to prediction markets that are listed as federally regulated event contracts. An arraignment in the criminal case against Kalshi is currently scheduled for Monday.

Arizona Attorney General Kris Mayes announced charges against the companies behind Kalshi on March 17, accusing them of operating an “illegal gambling business in Arizona without a license” and offering illegal election wagering.

Kalshi co-founder and CEO, Tarek Mansour, claimed the charges were a “total overstep” and “not about gambling.”

Federal and state regulators clash over prediction markets

The dispute has become a major test of whether prediction market contracts belong under federal commodities law or state betting rules.

On April 2, the CFTC filed three separate lawsuits against the gaming regulators of Illinois, Connecticut and Arizona, claiming that the event contracts offered by the platforms violated state gambling laws and licensing requirements.

In those suits, the CFTC says it has exclusive jurisdiction over CFTC-registered designated contract markets that list lawful event contracts. Kalshi is the clearest example in the current litigation.

Related: Kalshi, Polymarket face trading halt in Nevada after court rulings

Prediction markets are facing growing regulatory pressure in the US, where 11 states have pursued legal action against them.

Prediction market activity has been rising since the beginning of the US and Israeli military conflict with Iran, fueling renewed insider trading allegations, after six Polymarket traders netted $1 million by accurately betting when the US would strike Iran.

In response to insider trading concerns, Democratic Party Senator Adam Schiff has introduced legislation seeking to ban prediction markets on war, death and terrorism.

Magazine: Train AI agents to make better predictions… for token rewards

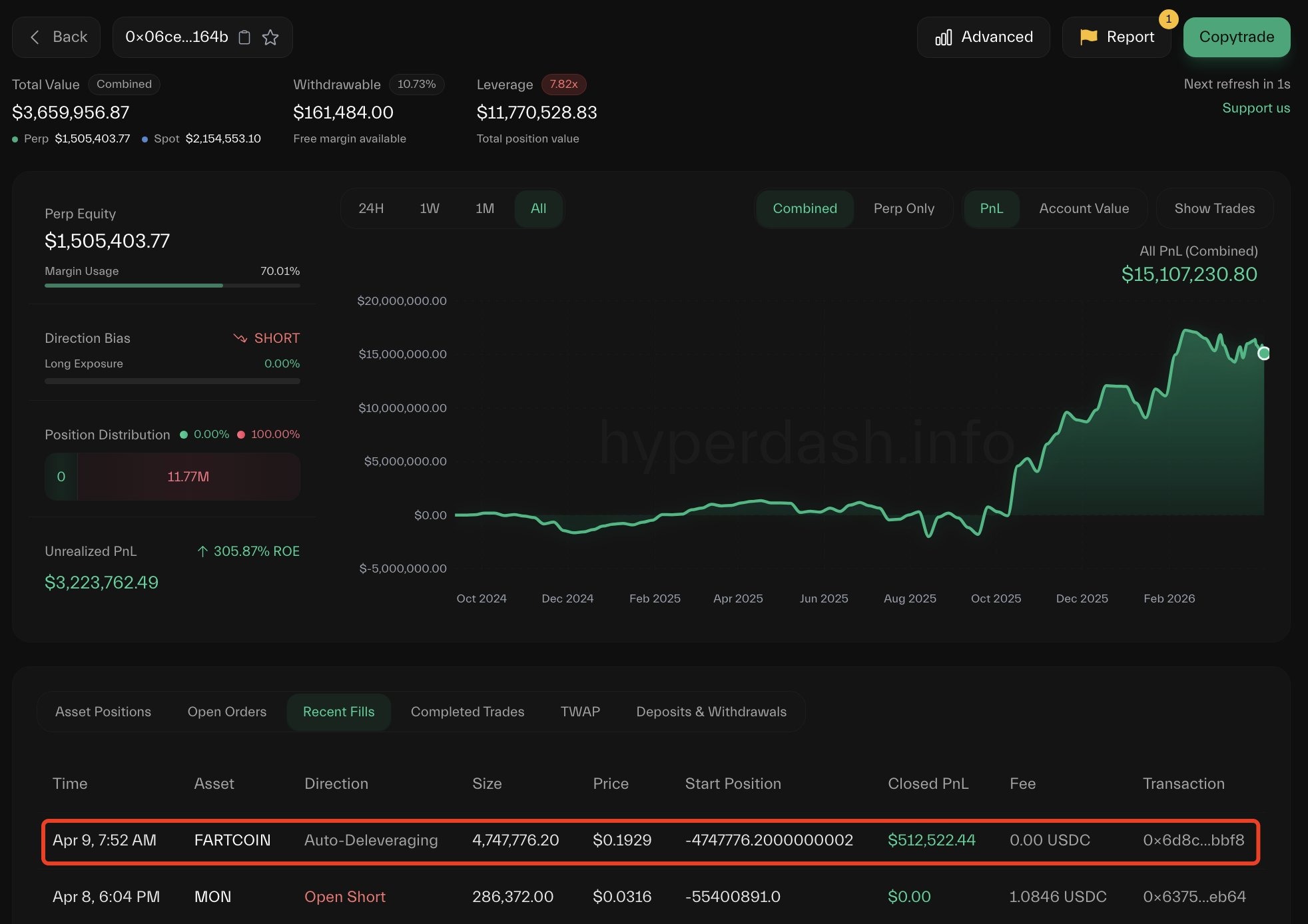

A trader lost about $3 million after building a large leveraged Fartcoin position on Hyperliquid that unraveled in thin liquidity, triggering the platform’s auto-deleveraging (ADL) mechanism.

Hyperliquid data flagged by Lookonchain shows that the trader accumulated about 145 million tokens across multiple wallets before being liquidated. The liquidation redistributed gains to opposing traders, with at least two wallets seeing around $849,000 through ADL.

PeckShield said the unwind produced about $3 million in accounting losses and left Hyperliquid’s HLP vault down roughly $1.5 million over 24 hours, though Hyperliquid had not publicly confirmed those figures by publication.

The episode highlighted how ADL can crystallize gains for traders on the other side of a collapsing position, while raising fresh questions about how Hyperliquid’s liquidation and vault structure behave in low-liquidity markets.

PeckShield said the activity appeared structured to trigger liquidations in low-liquidity conditions, potentially pushing losses onto Hyperliquid’s liquidity pool while being offset by positions elsewhere.

Cointelegraph reached out to Hyperliquid for comments, but had not received a response before publication.

Past trades exposed similar pressure on Hyperliquid’s liquidity system

This is not the first time Hyperliquid’s liquidity system has come under pressure from large, concentrated positions.

On March 13, 2025, the platform’s Hyperliquidity Provider (HLP) vault took a roughly $4 million hit after an oversized Ether (ETH) position was unwound, triggering liquidations under thin market conditions. After the incident, the team said that losses stemmed from market dynamics rather than a protocol exploit.

Related: Onchain perp DEX volumes fall for five straight months after October peak

A similar episode occurred later that month involving the JELLY memecoin. On March 27, 2025, a trader used multiple leveraged positions to exploit the platform’s liquidation system.

However, the final outcome remained unclear, with Arkham saying the trader withdrew about $6.26 million but may still have ended up down nearly $1 million.

On Nov. 13, 2025, a similar pattern occurred when a trader built large leveraged positions in the POPCAT market, triggering cascading liquidations that left a $5 million hole in the HLP vault. Community members said the strategy appeared designed to create and then remove liquidity to force the vault to absorb the impact.

Magazine: Solana exec trolls crypto gamers, Pixel tackles play-to-earn issues: Web3 Gamer

Authorities in the United States, United Kingdom and Canada have frozen millions of dollars tied to crypto scams in a joint enforcement operation called Operation Atlantic.

The operation, focused on phishing attacks, took place in March and was coordinated by the UK’s National Crime Agency (NCA), the US Secret Service, the Ontario Provincial Police and the Ontario Securities Commission.

Operation Atlantic identified more than 20,000 victims across the US, Canada and the UK, securing and freezing more than $12 million in suspected criminal proceeds, the NCA said Thursday. It also identified “more than $45 million stolen in cryptocurrency fraud schemes,” the agency added.

“Operation Atlantic is a powerful example of what is possible when international agencies and private industry work side by side,” NCA Deputy Director of Investigations Miles Bonfield said.

The operation involved assistance from major cryptocurrency exchange Binance, according to a separate statement by the company.

What is an approval phishing scam?

Approval phishing scams trick users into signing malicious permissions that allow attackers to access and drain crypto wallets.

Unlike typical scams, where perpetrators trick victims into sending them crypto, approval phishing misleads victims into unknowingly authorizing malicious transactions that allow scammers to spend specific tokens inside the victim’s wallet.

“Approval phishing is one of the most damaging types of scams targeting crypto users today,” said Flavio Tonon, Binance’s senior regional advisor for the Europe, Middle East and Africa region.

Related: Drift explains $280M exploit as critics question Circle over USDC freeze

He noted that the operation underscores how effective crime fighting is possible when private and public partners work together, adding that blockchain transparency makes it difficult for criminals to get away with phishing exploits.

No funds were frozen on Binance as part of the operation

Operation Atlantic included on-site investigations at the NCA’s London headquarters, where Binance said its Special Investigations team provided support, including live account screening and scam intelligence.

The company also provided insights on potential bad actors in order to assist with asset seizure efforts, and conducted research that identified scam websites that were still actively defrauding victims at the time of the operation.

Binance said no funds were frozen on Binance accounts.

Magazine: AI agents will kill the web as we know it: Animoca’s Yat Siu

Stablecoins are on track to become a foundational layer of global finance, with adjusted transaction volumes projected to reach $719 trillion by 2035, according to a new report by blockchain research firm Chainalysis on Wednesday.

The growth, driven by organic adoption alone, signals a structural shift in how value moves across borders and through everyday commerce, the research firm added.

Stablecoins moved more than $35 trillion on blockchain rails last year, noting that only roughly 1% was for real-world payments, according to a March report by McKinsey and blockchain data firm Atermis Analytics.

A key catalyst is the looming generational wealth transfer, with as much as $100 trillion expected to pass from Baby Boomers to Millennials and Gen Z over the coming decades. These younger cohorts, far more likely to use crypto as a financial instrument by default, are set to redefine payment preferences at scale, embedding digital assets into mainstream economic activity.

“When crypto becomes the default for the next generation of capital, the question is no longer if stablecoins compete with traditional rails, but how quickly they replace them,” Chainalysis said in its report.

At the same time, stablecoin transaction volumes are quickly converging with traditional payment networks. Chainalysis said that current trends suggest onchain payments could match Visa and Mastercard’s volumes no later than 2039, placing direct competitive pressure on legacy rails long defined by intermediaries, fees and delayed settlement.

Unlike card networks, stablecoins enable near-instant, 24/7 settlement and programmable transactions, reducing friction across remittances, business payments, and treasury operations. As merchant adoption expands, paying with stablecoins is increasingly shifting from a deliberate choice to invisible infrastructure, the firm added.

Chainalysis is also introducing a new category of blockchain intelligence agents, aimed at helping institutions navigate and operationalize this transition as digital assets move from the margins to the core of global finance.

“The institutions that build for onchain payments now will define the next era of global finance, while those that wait risk settling on someone else’s rails,” Chainalysis said.

In today’s newsletter, Joshua de Vos from CoinDesk breaks down cryptos performance in the first quarter, highlighting shifting institutional demand and new regulatory clarity setting the stage for Q2.

Q1 2026 Digital Asset Review

Digital assets closed Q1 2026 under meaningful pressure, extending a downturn that began in late 2025. As presented in CoinDesk’s latest “Quarterly Review and Outlook,” the quarter was shaped by escalating geopolitical tensions, a cautious Federal Reserve, and institutional flows that turned sharply negative before partially recovering into month-end.

Q1 in review

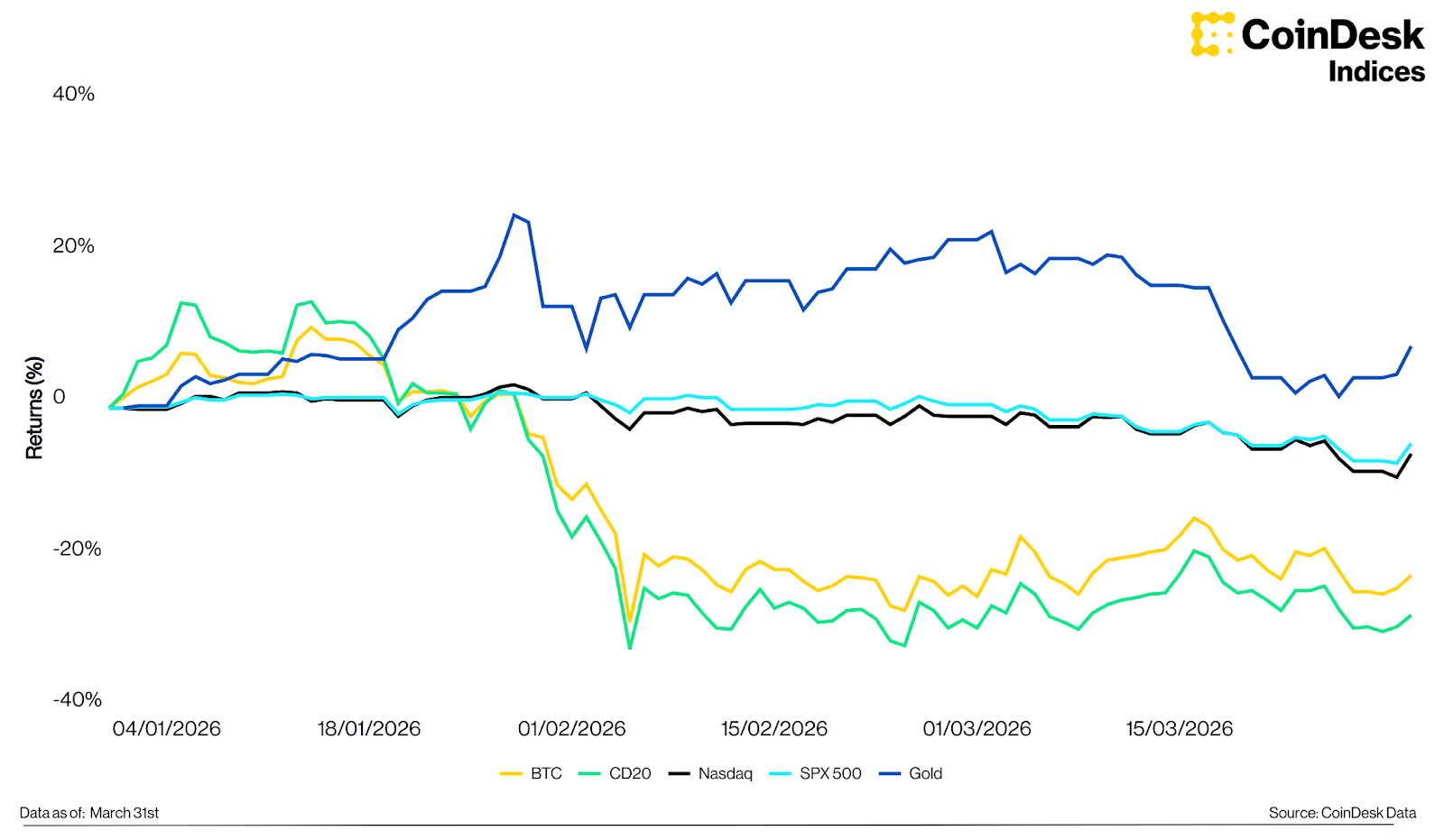

The CoinDesk 20 Index declined 27.4% to 1,952, while bitcoin fell 22.1% to $68,228; its second-largest quarterly decline since Q2 2022. Escalating tensions in the Middle East pushed crude oil above $100 per barrel, while the Federal Reserve held rates steady at 3.5%–3.75% following its March meeting. The S&P 500 and Nasdaq declined 4.63% and 5.98% respectively; gold was the standout, rising 8.19% to $4,671.

BTC vs gold vs SPX vs Nasdaq vs the CD20 Index, Q1 2026

A notable dynamic emerged in the quarter’s second half. Bitcoin had already declined roughly 30% from its February peak before geopolitical tensions escalated sharply in late February, suggesting much of the fear and forced liquidations had been priced in before the event. Since tensions intensified, bitcoin returned 3.54%, while the S&P 500 and Nasdaq fell 5.09% and 4.89%. The CoinDesk Memecoin Index was the weakest performer at -41.7%; the CoinDesk 80 outperformed bitcoin, declining 16.5%, with Hyperliquid (+43.8%) and Morpho (+40.9%) leading positive returns among its constituents.

BTC and CD20 Index vs selected assets, returns since Feb 28th

Institutional flows in focus

Among U.S. spot bitcoin ETFs, net outflows of $1.81B across January and February erased much of the institutional demand built during the prior year. Although March saw a recovery of $1.32B in inflows, Q1 closed with net redemptions of approximately $496M. Bitcoin’s stabilisation in March coincided with the return of positive net inflows, suggesting institutional positioning had begun to rebuild before the quarter ended.

Bitcoin ETF flows and BTC price, Q1 2026

In the spot ETF era, institutional flow data provides a real-time signal of sentiment unavailable in prior cycles. The March recovery sets a baseline worth watching for Q2, particularly as Morgan Stanley reportedly prepares a spot bitcoin ETF ($MSBT) at a 0.14% fee, designed to integrate into its network of over 16,000 advisors.

The regulatory picture clarifies

A joint SEC–CFTC ruling on March 17 designated 16 assets, including SOL, XRP and DOGE, as digital commodities and thus outside the securities definition. This removes a key regulatory overhang and opens the pathway for spot ETF approvals across a broader range of assets. Basket and index-based ETPs now rank second only to bitcoin-focused products by number of pending filings, with CoinDesk indices including the CD20 and CD100 increasingly referenced as natural benchmarks for these vehicles.

Number of pending crypto ETP applications, 2025

Looking ahead to Q2

Market direction in Q2 will be shaped by two variables: the trajectory of the Middle East conflict and the Federal Reserve’s response to inflation data. A de-escalation would ease energy price pressure and creates conditions for recovery; prolonged conflict would keep financial conditions tight. Bitcoin’s October 2025 peak near $126,000 and the subsequent correction are broadly consistent with the historical halving cycle, which typically produces an 18–24 month post-ATH drawdown. This cycle’s structural difference is institutionalised ETF demand; on peak days in 2024, inflows topped $1 billion, equivalent to absorbing over 30 days of mining supply in a single session. Combined with a more supportive regulatory environment and a deepening institutional product suite, the structural foundation entering this correction is meaningfully more durable than in prior cycles.

Constituent highlights

Ether declined 29.1% in Q1, with U.S. spot ether ETFs recording net outflows of $758 million. The more significant forward-looking development is Ethereum’s structural position in tokenised assets; 59.4% of total real-world asset supply resides on Ethereum as of Q1 2026. BlackRock’s ETHB staking ETF, launched on March 12 with a projected 3–7% annual yield, introduces an income-generating dimension to ETH that could broaden its appeal to yield-oriented allocators.

Solana declined 33.2% but registered a notable milestone: peer-to-peer stablecoin transaction volume reached a new all-time high of $832 billion in Q1 2026, reflecting a shift toward payments infrastructure. Solana’s real-world asset holder count also surpassed Ether for the first time, driven by platforms such as Ondo Global Markets and xStocks.

XRP declined 27.1%, but the narrative is increasingly centred on Ripple’s expanding institutional infrastructure. RLUSD reached a market capitalization of $1.42 billion by quarter-end, and Ripple’s acquisition strategy, spanning prime brokerage through Hidden Road ($1.25 billion, clearing $3 trillion annually) and treasury management through GTreasury ($1 billion), points toward a comprehensive financial ecosystem built around XRP and RLUSD. The key catalyst for Q2 is whether these integrations translate into measurable on-chain activity.

This summary was created based on CoinDesk Research’s latest report “Digital Assets: Quarterly Review and Outlook, Featuring CoinDesk 5 and CoinDesk 20.”

– Joshua de Vos, research team lead, CoinDesk

Keep Reading

- JP Morgan CEO Jamie Dimon says the bank must “move faster” with its blockchain efforts due to the threats banking faces from blockchain technology.

- Morgan Stanley’s own bitcoin ETF opened this week creating competition on Wall Street.

- The U.S. Treasury is pitching new rules for stablecoin issuers to treat them like every other financial firm that must maintain armor against illicit uses.

Bitcoin (BTC) circled $71,000 at Thursday’s Wall Street open after US inflation data conformed to expectations.

Key points:

-

Bitcoin waits for new catalysts as US PCE inflation data conforms to market expectations.

-

Friday’s CPI release will be the first to show any impact of the US-Iran war.

-

$80,000 remains in play as a BTC price target, a trader says.

PCE data avoids surprises for risk assets

Data from TradingView showed cooling BTC price volatility after local highs near $73,000 the day prior.

Relief over a US-Iran ceasefire combined with favorable readings from the Federal Reserve’s “preferred” inflation gauge, the Personal Consumption Expenditures (PCE) index.

Core PCE year-on-year came in at 3% for February. On a monthly basis, core PCE was at 0.4%, per data from the US Bureau of Economic Analysis (BEA).

Reacting, trading resource The Kobeissi Letter noted that the impact of the US-Iran war and oil-supply squeeze were not yet reflected in PCE.

“This marks the final pre-Iran War PCE inflation datapoint,” it wrote on X.

Markets remained cautious about future Fed policy, with data from CME Group’s FedWatch Tool continuing to show no expectations of interest-rate cuts in 2026.

While Bitcoin offered no obvious reaction to the latest data, meanwhile, economist Mohamed El-Erian argued that Friday’s March Consumer Price Index (CPI) release was more important.

“While PCE inflation is widely regarded as the Fed’s favorite measure, the bigger inflation focus this week will be on tomorrow’s CPI data, as PCE covers February and not March,” he told X followers.

As Cointelegraph reported, CPI is particularly susceptible to fallout from oil-price swings.

Trader: $80,000 BTC price push “on the horizon”

BTC price action thus left traders guessing as to when and where the next move would be.

Related: Bitcoin RSI ‘nearly perfectly’ copying end of 2022 bear market: Analysis

In their latest market commentary, pseudonymous trader LP leveraged liquidation clusters to give potential targets.

“On the HTF, some upside low-leverage liquidation clusters have been cleared, but sizeable liquidity still remains around 73K and above the highs near 76K. Meanwhile, liquidity is starting to build on the downside, mainly around 69K and 64K,” an X post stated.

“With price still range-bound, both sides remain in play. If the 69–68K level holds, price is likely to push higher and target the remaining upside liquidity around 73K.”

Crypto trader Michaël Van de Poppe was more optimistic, keeping the $80,000 mark in play.

“As long as Bitcoin continues to hold these ranges, there’s a strong new upwards leg on the horizon towards $80K,” he summarized on the day.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Crypto World

Bitmine Immersion (BMNR) uplists to NYSE and boosts share buyback program to $4 billion

Bitmine Immersion Technologies (BMNR) began trading on the New York Stock Exchange on Thursday, moving from the NYSE American as it scales its crypto-focused treasury strategy.

The company paired the uplisting with an increase in its share repurchase program, raising the authorization to $4 billion from $1 billion. The buyback ranks among the largest announced this year, according to the company. BMNR’s stock has plunged roughly 90% since peaking last summer amid the height of the digital asset treasury mania. Shares are lower by 2.8% in early Thursday trading.

Bitmine now holds about 4.8 million ETH, equal to 3.98% of total supply, and continues to target 5%, or what it calls the “Alchemy of 5%.”

The macro backdrop could play a role. Fundstrat co-founder Tom Lee, who also chairs Bitmine, has argued that U.S. equities may have found a bottom following a ceasefire tied to tensions in Iran. Stocks, oil and volatility shifted sharply in response, a pattern that has also lifted crypto markets.

Bitcoin recently moved above $72,000 alongside gains in equity futures, reflecting a broader “risk-on” trade. Ether may benefit as well, with recent inflows into spot exchange-traded funds and increased staking activity reducing selling pressure, according to Lee.

For Bitmine, the link is direct. Each 1% rise in ether’s price adds roughly $100 million to the value of its holdings. A sustained rebound in crypto could support its balance sheet and stock.

Crypto World

Polymarket Just Hit $4 Billion in Volume on 5-Minute Markets: Is Chainlink the Infrastructure Behind the Next DeFi Explosion?

$153 million in daily volume. $4 billion total. $200 million in the first week alone. Polymarket’s 5-minute prediction markets have gone from experimental product to one of the highest-velocity trading venues in DeFi – and Chainlink oracles are the reason any of it works.

The volume surge, confirmed by on-chain data shared across crypto analytics channels, represents a roughly 400% increase from earlier baseline figures, with the 3x weekly growth rate still accelerating as of the latest reporting window.

Discover: The best pre-launch token sales

Why 5-Minute Prediction Markets Break Standard Oracle Architecture

Standard oracle infrastructure built for hourly or daily market resolution can tolerate latency. A price feed delayed by 30 seconds is noise when a contract settles in 48 hours.

In 5-minute prediction markets, that same 30-second delay is the difference between a valid settlement and a manipulated one, exactly why Polymarket’s architecture required a fundamentally different oracle setup.

Chainlink’s Data Streams integration, deployed on Polygon where Polymarket settles, delivers timestamped price reports at sub-second intervals.

Combined with Chainlink Automation handling the on-chain settlement triggers, the system processes the full cycle, price confirmation, contract resolution, USDC payout, without human intervention and without the manipulation vector that centralized price feeds introduce.

The oracles provide the official price feeds that trigger contract settlements, removing the need for a centralized authority entirely.

The scale of what’s now running through this infrastructure is significant. Over 3,000 traders are actively using Chainlink Data Streams across integrated platforms, and the Dashlink dashboard tracking oracle demand shows a direct correlation between the Polymarket volume surge and a decline in LINK exchange reserves – whales are pulling supply off exchanges as network utilization hits new highs for prediction market settlements.

Native USDC collateral adoption within these markets has further accelerated institutional participation by improving capital efficiency.

The appeal is obvious: a platform already under scrutiny for insider trading patterns on longer-duration markets now offers a format where information asymmetry has a 5-minute shelf life.

The risks are real and shouldn’t be buried. Short timeframes amplify volatility, HFT-dominated order flow can crowd out retail, and oracle delays, however rare, carry outsized consequences when resolution windows are measured in minutes.

But the volume data doesn’t lie: the format is capturing demand that didn’t have an instrument before.

Convergence Hackathon Closes – Liquid Chain Takes the Grand Prize on CCIP

Liquid Chain built a Unified Liquidity Layer that aggregates capital across multiple Layer-2 networks using Chainlink’s Cross-Chain Interoperability Protocol (CCIP) as the messaging backbone.

The core problem it solves is real and expensive – assets stranded on individual L2s require manual bridging, creating slippage, delay, and trust assumptions that institutional allocators won’t accept.

Liquid Chain’s architecture lets users move assets seamlessly across chains without manual bridge interactions, with CCIP handling the verification and message-passing layer beneath the surface.

The project has been pitching its Layer-3 DeFi buildout as a credible answer to the fragmentation problem, and the Convergence judges agreed.

Other notable hackathon submissions concentrated on Real-World Asset tokenization and DeFi automation – a consistent signal that Chainlink’s developer community is orienting toward institutional-grade infrastructure rather than consumer speculation. The CCIP adoption rate implied by the hackathon submissions validates Chainlink’s cross-chain positioning at exactly the moment demand for tamper-proof oracle settlement is breaking records on Polymarket.

Explore the LiquidChain presale and current allocation terms here.

The post Polymarket Just Hit $4 Billion in Volume on 5-Minute Markets: Is Chainlink the Infrastructure Behind the Next DeFi Explosion? appeared first on Cryptonews.

- Bitcoin trades above $70,700 as derivatives data shows $80,000 calls dominating on Deribit.

- BTC rebounded to near $72,900 on Wednesday as a US-Iran ceasefire eased oil pressures.

- Analysts see end of stress cycle, targeting $80,000 if $75,000 breaks.

Bitcoin’s resurgence to above $70,000, with intraday highs of $72,900, has crypto enthusiasts in an upbeat mood. The cryptocurrency hovers near $70,800 as of writing, off highs seen on Wednesday, but bulls are upbeat as fresh market signals point to a potential breakout.

Traders bet on next leg up for Bitcoin

Bitcoin is well off its year-to-date highs and has struggled since breaking lower in late January 2026. Bears are therefore still on the hunt.

However, this week has investor sentiment shifting bullish, fueled by the US-Iran ceasefire and key activity in Bitcoin derivatives. Data suggests investors are eyeing a potential rally to $80,000.

Options data from Deribit, the platform that accounts for the lion’s share of the global crypto options market, shows bullish bets on prices surging to $80,000 have increased.

Call options betting on BTC climbing beyond the $80k strike price have hit $1.6 billion. This is a stark reversal from recent months when $60,000 puts, which outline wagers on price drops, dominated the outlook.

On-chain data also supports the bullish case, with Morgan Stanley’s ETF debut netting over $34 million in volume.

Allyson Wallace, global head of ETFs at Morgan Stanley, commented ahead of the launch: “The demand, especially from the high-net-worth investors, has been quite high. Viewed at the firm level, this is an asset class that is not going away.”

Bitcoin price prediction

The crypto market began the week with all eyes on Bitcoin. Notably, BTC bounced to highs near $72,900, hitting levels last seen since March 18. The uptick saw buyers push from lows near $67,700 overnight Tuesday, April 7, amid news of a ceasefire between the US and Iran.

Investors buoyed by the prospect of an easing in oil prices helped BTC higher. With broader inflation concerns dissipating, a further strengthening in the ceasefire could see Bitcoin prices break to $75,000. If this happens, the next target will be $80,000 or higher.

However, geopolitical risks remain amid a likely fragile ceasefire. If fresh attacks begin and an escalation occurs, a surge in oil prices could send risk assets plummeting.

Key Takeaways

- NVDA slipped between 0.2%–0.5% Thursday, settling around $181.75 following Wednesday’s 2.2% rally

- Shares have remained confined within a $165–$195 trading channel for several months

- Market analysts identify $185 as a critical breakout threshold; $200 viewed as confirmation level

- Wednesday’s surge followed news of a two-week U.S.-Iran ceasefire, though durability concerns persist

- Technical analysts warn that breaching $170 support could trigger a decline toward $150

Nvidia’s recent price action reflects a prolonged period of consolidation. Despite its status as the market’s artificial intelligence powerhouse, NVDA shares have languished in a holding pattern since September 2025, oscillating within a $165–$195 corridor as traders await a meaningful catalyst.

Signs of a potential breakout emerged recently. The chipmaker mounted an impressive rally spanning six consecutive sessions—delivering gains exceeding 10% and marking its longest winning streak since October—before momentum stalled on Thursday.

The Wednesday surge of 2.2% followed President Trump’s announcement of a temporary two-week ceasefire agreement with Iran, which included the reopening of the strategically vital Strait of Hormuz. This development eased concerns about potential economic disruption. Nvidia emerged as one of the S&P 500’s top performers during that session.

Thursday’s trading painted a contrasting picture. Shares retreated approximately 0.5% to $181.75 as market participants expressed skepticism about the ceasefire’s sustainability. The broader S&P 500 index also traded relatively flat.

Geopolitical dynamics continue to influence risk sentiment across markets. Iran’s continued capability to disrupt shipping through the Strait of Hormuz maintains a degree of unease among investors.

Beyond geopolitical concerns, a fundamental question persists: will major cloud providers—including Microsoft, Google, and Amazon—realize meaningful returns on their substantial artificial intelligence infrastructure investments? This uncertainty has effectively capped NVDA’s upside potential in recent months.

Ishan Majumdar, founder of Baptista Research, shared his perspective with Barron’s, emphasizing that core AI demand dynamics haven’t changed. “Nothing about the cease-fire alters the structural AI demand story,” he noted. “If anything, removing macro volatility allows the market to refocus on those fundamentals.”

Technical Analysts Flag $185 as Pivotal Threshold

Jonathan Krinsky, chief market technician at BTIG, has identified the $185 price point as particularly significant. “If Nvidia sustains above $185, I would say the money is ready to run back in,” he explained. “The long-term trend remains positive.”

Buff Dormeier at Kingsview Partners believes a higher confirmation is necessary. He suggests NVDA must break through $200 to establish a convincing bullish trajectory. “If we started to get a signal of that, we could easily be back to the races,” he indicated.

Dormeier also highlighted improving valuation metrics. NVDA currently trades at approximately 20 times forward earnings—significantly below its historical 10-year average multiple of around 36—and now trades in line with the broader S&P 500. This represents a meaningful valuation compression for a stock that traditionally commanded a substantial premium.

Support Breakdown Could Trigger Further Weakness

Both technical strategists emphasize meaningful downside risks. The $170 price level represents crucial support. A sustained breach below this threshold could signal additional selling pressure ahead.

“If we were to break under there, I think shares could fall down to $150,” Dormeier cautioned.

Krinsky shared similar concerns about the sustainability of the recent bounce. “It doesn’t strike me as an all-clear that we recovered the $170 level so quickly,” he observed. “If it moves back to that level and closes under it again, that would be a more telling signal that Nvidia is likely to continue lower.”

For the immediate term, Dormeier frames the trading range as $165 representing the floor and $180 marking near-term resistance. NVDA settled Wednesday’s session at $182 before trading around $181.75 on Thursday.

DOJ and CFTC Seek Halt to Arizona Action Against Kalshi

What To Remember Before the Final Season of HBO’s Stellar Comedy

Rise in take up of large industrial space in Wales

-

NewsBeat7 days ago

NewsBeat7 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business5 days ago

Business5 days agoExpert Picks for Every Need

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics6 days ago

Politics6 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoCoffee Break: Santa Croce Tote

-

Politics6 days ago

Politics6 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech6 days ago

Tech6 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

You must be logged in to post a comment Login