Crypto World

Facing a crisis, Bitcoin treasury companies need to pivot to survive

For much of the last three years, a predictable cycle dominated the market: companies announced their intentions to purchase massive volumes of Bitcoin, watched their stock prices soar to a premium and issued new shares to buy more Bitcoin. This feedback loop made Bitcoin accumulation look like an “infinite money glitch”: a guaranteed way for public companies to manufacture shareholder value out of thin air.

As we move through the first quarter of 2026, that cycle has broken. Recent data shows that roughly 40% of publicly traded Bitcoin treasuries are now trading at a discount to their net asset value (NAV). In plain terms, the market now values these companies as a liability, worth less than the market price of the Bitcoin they hold.

This collapse in valuation has invited blistering criticism from institutional veterans. Jan van Eck, CEO of VanEck, recently dismissed the sector as a publicity-driven trend, while veteran analyst Herb Greenberg has characterized the most prominent player, Strategy, as a “quasi-Ponzi scheme.”

These critiques point to a failure in how many of these firms are managed. To remain viable, Bitcoin treasury companies must accept that accretive dilution is no longer a sustainable strategy. They must move beyond holding passively and operate as disciplined asset managers.

Competing philosophies: the promoter vs. the asset manager

Today, most Bitcoin treasury companies are divided into two camps, representing fundamentally different philosophies of corporate management: “Promoters” and “Asset Managers.”

Promoters treat Bitcoin as a passive asset to be hoarded. In this model, the company’s primary job is two-fold. First, the firm must act as an aggressive advocate for the underlying currency and its ecosystem. By investing in community projects and maintaining a constant presence in public discourse, the Promoter works to drive the token price higher and capitalize on gains from its existing holdings. Second, the Promoter must market its own stock to maintain a high premium. When the market values the company significantly higher than the Bitcoin it actually holds, the company can sell new shares at that inflated price to buy more Bitcoin at the normal market rate. This calculated financial maneuver is called accretive dilution.

Together, these strategies create a feedback loop of hype. The Promoter needs the price of Bitcoin to rise to increase its net asset value, and it needs the equity premium to be maintained to continue its accumulation strategy. However, this model is fragile because it relies entirely on external sentiment. If the price of BTC stalls or the equity premium vanishes — as we are seeing across the board in 2026 — the Promoter is left with an unproductive balance sheet and no internal mechanism for growth.

In contrast, asset managers view Bitcoin as a productive commodity akin to “digital oil.” In the physical world, an oil major like Exxon or Shell does not simply sit on reserves and hope for a price rally. They are sophisticated financial operators who treat their inventory as a productive asset. They trade the futures curve to capture premiums and monetize market volatility.

Asset Manager-style treasuries apply this same industrial rigor to the digital realm. By using their balance sheet to generate real, Bitcoin-denominated returns, they ensure growth is driven by operational skill, rather than a byproduct of crypto market sentiment. By treating Bitcoin as a commodity to be managed, the asset manager generates real yield from the skilled management of the asset, not from the continuous issuance of new stock to the public.

The era of accretive dilution is over

The distinction between these two models is no longer academic. One of them has stopped working.

The Promoter approach — relying on equity issuance to finance Bitcoin accumulation — is no longer a viable growth strategy. What once passed as financial sophistication was, in practice, a tactic that depended on unusually favorable market conditions.

Issuing shares at a premium can temporarily increase Bitcoin per share, but it does not create an economic return. It generates no cash flow, no operational advantage and no durable compounding mechanism. It exists entirely at the discretion of new investors. When that demand weakens, the strategy collapses.

For much of 2025, this reality was easy to ignore. Rising Bitcoin prices and abundant liquidity made accumulation strategies look interchangeable. Capital flowed freely, equity premiums expanded, and dozens of treasury companies adopted the same playbook: buy Bitcoin, promote the narrative, raise more equity, repeat. In that environment, differentiation didn’t matter.

It does now.

As the market matures, Bitcoin treasuries that rely solely on passive accumulation face a hard constraint: they lack an internal mechanism for growth. When every firm owns the same asset, holds it the same way and depends on the same equity-market dynamics, there is no basis for sustained outperformance. The model has become commoditized — and investors are growing sick of it.

Only the most prominent players — those with exceptional scale, brand recognition, and Michael Saylor-level fame — will be able to sustain this approach. For most treasury companies, passive accumulation without active management offers no path to differentiation, resilience, or long-term relevance.

Markets are already reflecting this reality. Nearly half of Bitcoin treasury companies have fallen below mNAV, and most won’t recover without a drastic pivot.

Transitioning from passive storage to active management

To transition from a promoter to an asset manager, companies must move beyond the simple HODL strategy and put the balance sheet to work. This means adopting the tools of professional commodity trading.

One primary tool is the basis trade, in which a firm exploits the price difference between the spot price of Bitcoin and the futures contract price. By capturing this spread, a company can grow its Bitcoin holdings even when the asset’s price is flat or declining. Furthermore, a Bitcoin asset manager uses dynamic options strategies to turn market turbulence into income.

This approach provides a “real yield” that does not rely on selling more stock or finding new investors. It transforms the treasury from a cost center into a profit center. Most importantly, it provides a clear path to increasing Bitcoin-per-share through operational excellence rather than capital market maneuvers.

Treasury companies also need to adjust the way they communicate with investors. Too many treasury CEOs posture as low-budget Michael Saylor impersonators — focusing on narrative amplification, public advocacy and symbolic accumulation. It’s an approach designed to generate hype, not project careful financial stewardship.

As investor scrutiny intensifies, CEOs will need to project credibility by explaining how risk is managed, how exposure is structured, and how returns are generated across a range of market conditions. The market will not reward Bitcoin’s loudest cheerleaders; it will reward the firms that deploy their holdings most productively.

Moody’s Ratings has debuted a system to deliver its credit analysis onchain, bringing its ratings data into blockchain-based financial infrastructure.

The system, called Token Integration Engine (TIE), connects Moody’s traditional ratings data to blockchain networks, allowing permissioned participants to access credit insights within blockchain-based financial workflows. It is built for institutional use, with issuers controlling participation while Moody’s retains oversight of its ratings process.

The company claims it is the first credit rating agency to deliver its credit analysis onchain. In June 2025, Moody’s teamed up with a fintech startup called Alphaledger to run a pilot program to explore how traditional credit ratings could be integrated into blockchain systems.

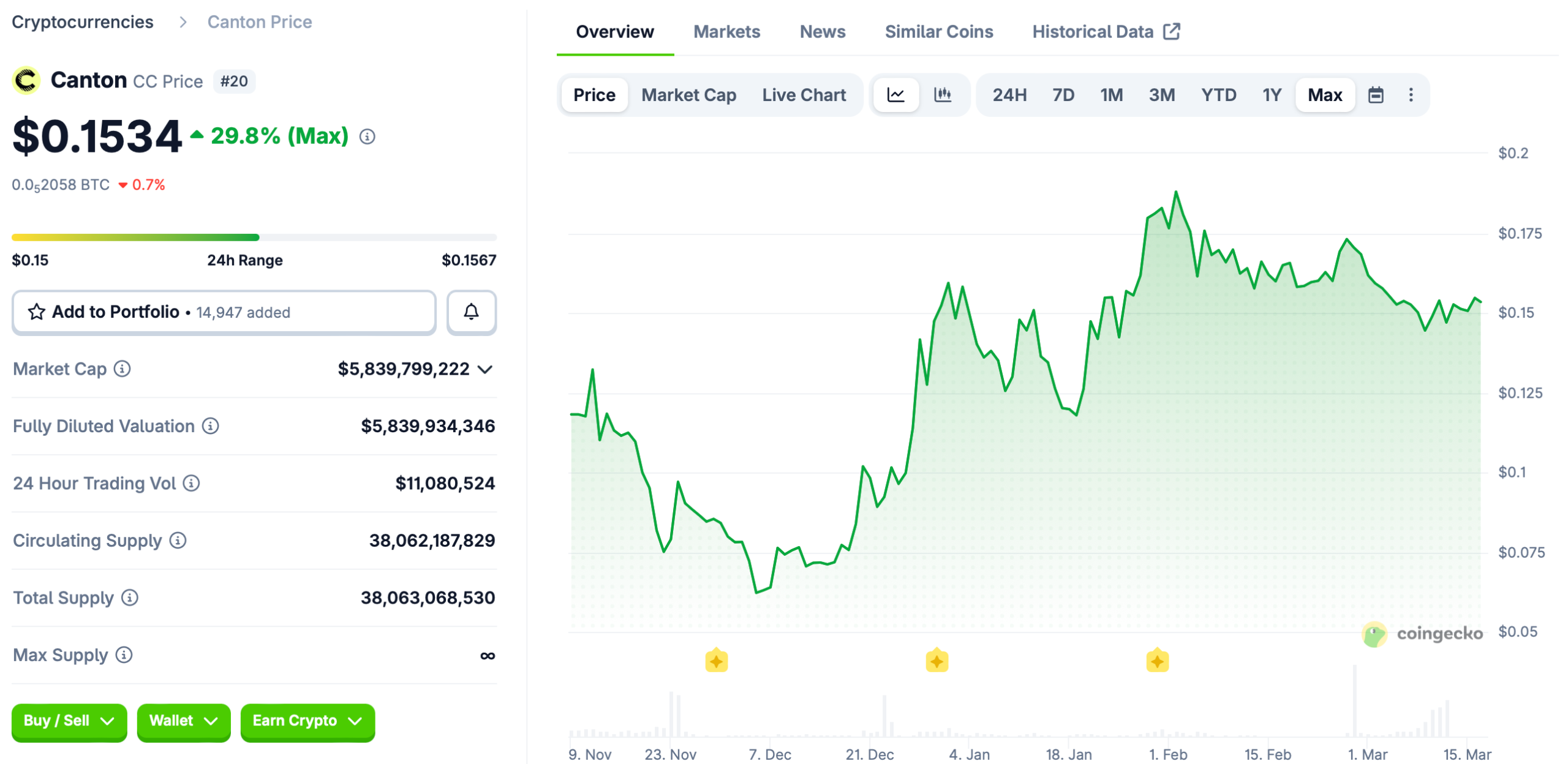

The initial deployment runs on the Canton Network, a permissioned blockchain designed for institutional finance. Moody’s is operating its own node on the network as part of the rollout, and said it plans to expand the system to additional blockchains and asset types.

The system is designed to be network-agnostic, with access controlled by issuers under the company’s existing governance and compliance framework.

Moody’s, a US-based credit rating agency founded in 1909 with operations in more than 40 countries, assesses the creditworthiness of governments, companies and financial instruments, with its ratings widely used by investors across global capital markets.

Related: Crypto accounting startup Cryptio lands $45M as institutions move onchain

The rise of the Canton Network

Moody’s deployment adds to the growing use of the Canton Network as infrastructure for institutional blockchain applications, particularly in tokenized assets and collateral markets.

A growing list of asset managers are integrating tokenized funds into the network. Franklin Templeton expanded its Benji platform to Canton in November, allowing its tokenized assets, including a US government money market fund, to be used as collateral and liquidity within the ecosystem.

Other efforts have focused on market infrastructure and settlement. In December, the Depository Trust and Clearing Corporation (DTCC) said it plans to issue a subset of US Treasury securities on Canton, extending blockchain-based processes into core clearing and settlement systems, with potential expansion to additional asset classes.

Banks and digital asset infrastructure platforms are also building on the network. In January, Digital Asset and Kinexys by JPMorgan said they plan to bring JPMorgan’s dollar deposit token, JPM Coin, to Canton, while Temple Digital Group launched a platform enabling 24/7 trading of digital assets through a central limit order book with non-custodial settlement.

The value of Canton Coin, the network’s native token, has increased about 30% since its launch in November 2025, according to CoinGecko data.

Magazine: China’s ‘50x’ blockchain boost, Alibaba-linked AI mines Bitcoin: Asia Express

For the first time, the U.S Securities and Exchange Commission has sought to clearly define different types of crypto assets and how the regulator will approach them, issuing those new standards Tuesday alongside its sister agency that’s responsible for commodities.

The SEC’s interpretive guidance, which doesn’t yet carry the weight of a formal new rule, has been promised by its new leader, Chairman Paul Atkins, put in place by President Donald Trump. And it was issued in partnership with the Commodity Futures Trading Commission, just days after the two agencies agreed on a formal relationship in which they plan to regulate crypto and other industries as close partners.

“After more than a decade of uncertainty, this interpretation will provide market participants with a clear understanding of how the Commission treats crypto assets under federal securities laws,” Atkins said in a statement.

The previous chairman of the SEC, Democratic appointee Gary Gensler, had declined to commit to tailored policies for the crypto sector, leaving a longstanding gap in its regulator certainty in the world’s most important market.

Atkins said the new “token taxonomy” interpretation on Tuesday takes a stance that Gensler’s agency refused to: “Most crypto assets are not themselves securities.”

He said in remarks at the Digital Chamber’s DC Blockchain Summit that the SEC created four categories of tokens.

“The interpretation then clarifies that only one crypto asset class remains subject to securities laws, namely digital securities, which are traditional securities in new technology,” he said. “This distinction returns the SEC to its core mission and statutory authority of protecting investors involved in securities transactions.”

Additionally, those investment contracts that are securities don’t necessarily keep that status permanently, he said.

“We’re not the securities and everything commission anymore,” he said Tuesday at the Digital Chamber’s DC Blockchain Summit, just minutes after releasing the new standard. The line drew enthusiastic applause from the crypto crowd.

The guidance seeks to define digital commodities, digital collectibles, digital tools, stablecoins and digital securities. It also clarifies how U.S. securities laws should treat airdrops, protocol mining, protocol staking and the wrapping non-security crypto assets.

“For far too long, American builders, innovators, and entrepreneurs have awaited clear guidance on the status of crypto assets under the federal securities and commodity laws,” said CFTC Chairman Mike Selig.

Atkins said that the legislation being devised in Congress to establish new crypto laws will be the only way to guarantee the permanence of pro-digital assets policy shifts.

In the new guidance, the commission is saying that a digital asset becomes a security when its issuer offers it as an investment in a common enterprise that comes with promises of profits based on the management’s efforts. Such an investment contract ends, though, when “either the issuer has fulfilled its representations or promises or the issuer has failed to satisfy its representations or promises,” at which point it wouldn’t be regulated as a security anymore.

The agency says its reach into digital securities does not include airdrops, protocol staking and protocol mining.

The CFTC’s Selig said his agency was also signing on to the same taxonomy, as part of the two agencies’ push toward “harmonization.”

“I think the signal is clear now that it’s time to build in the United States,” he said.

UPDATE (March 17, 2026, 20:35 UTC): Adds additional detail.

The court ordered Google and Apple to restrict Polymarket after investigators flagged unregulated betting and missing identity checks across Argentina.

Argentina has moved to restrict access to the prediction market platform Polymarket after a Buenos Aires court determined it was operating as an unauthorized betting service.

In a ruling issued by Judge Susana Parada, authorities ordered a country-wide block on the website and instructed Google and Apple to remove or limit access to its application on mobile devices.

No License, No Limits

The measure comes after an investigation by Prosecutor Juan Rozas, who oversees gambling-related cases in the city. As part of the enforcement, the telecom regulator Ente Nacional de Comunicaciones (ENACOM) has been directed to ensure internet service providers prevent access to the platform within the country.

The probe concluded that Polymarket allowed users to trade on the outcomes of real-world events without complying with gambling regulations. Prosecutors said accounts could be created rapidly without identity or age checks, which ended up enabling unrestricted participation, including by minors.

They further stated that the platform facilitated payments via cryptocurrencies and credit cards without applying the controls required for regulated betting operations. The case was triggered by a complaint from the Lotería de la Ciudad de Buenos Aires, which alleged that the platform was offering services locally without authorization. Additional verification conducted with the Asociación de Loterías Estatales de Argentina found no record of Polymarket holding a licence in any jurisdiction.

The court’s decision surfaced publicly during a broader controversy linked to Argentina’s inflation data. Shortly before the release of February figures by the national statistics agency INDEC, market probabilities on international prediction platforms moved toward a higher reading.

While analysts had largely estimated inflation between 2.6% and 2.8%, the official figure came in at 2.9%. Activity on Polymarket tied to that data point saw trading volumes rise to roughly $91,000 in the minutes preceding publication, which led some observers to question whether the data had circulated in advance.

You may also like:

The development adds to a growing trend of regulatory crackdowns on prediction market services, with companies like Polymarket and Kalshi increasingly coming under legal or supervisory pressure in a range of jurisdictions, among them France, Germany, Italy, Australia, Singapore, Portugal, Hungary, Thailand, and the Netherlands.

Polymarket Intelligence Misuse

Earlier this year, Israeli authorities formally charged an IDF reservist and a civilian over alleged misuse of classified military intelligence to gain an advantage on the prediction platform. A joint probe by the Defense Ministry, Shin Bet, and national police found that sensitive operational knowledge may have been leveraged to place high-confidence bets on future military developments.

Prosecutors filed serious charges, including security violations, bribery, and obstruction of justice, while a court-imposed gag order limits further disclosures.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

The crypto rally is took a pause on Tuesday ahead of Wednesday’s Federal Reserve decision.

After briefly topping $76,000 overnight, bitcoin pulled back to around $74,000 during the U.S. session, modestly higher over the past 24 hours.

Crypto stocks mostly booked modest gains, with stablecoin issuer Circle (CRCL), bitcoin miner Bitdeer (BTDR) standing out advancing 5% and 12%, respectively. The Nasdaq closed with a 0.5% gain and the S&P 500 rose 0.25%.

It’s almost universally expected that the Fed will leave benchmark interest rates unchanged at 3.50%-3.75% tomorrow. But given rapidly rising oil prices and their possible effect on inflation thanks to the war in Iran, the focus shifts to Jerome Powell’s messaging and policymakers’ outlook for future rates.

Bitfinex analysts said the key question is whether policymakers still signal rate cuts in 2026 or are moving towards the idea of no further monetary ease. A more hawkish outcome could weigh on risk assets by strengthening the dollar, they said.

Powell’s take on the recent oil advance will also be in focus. Treating it as a temporary shock would support sentiment, while a more stagflationary view could limit the Fed’s flexibility.

Also coming on Wedesday is the February Producer Price Index report. Tyically not having nearly the weight of the Consumer Price Index, the PPI will be a bit more closely followed given its timing ahead of the Fed meeting.

“A hot PPI number followed by a hawkish FOMC would be the most damaging combination for equities and risk assets,” the Bitfinex team continued.

That backdrop is already showing up in market expectations toward a higher-for-longer rate path, according to Vetle Lunde, head of research at K33.

The probability of rates staying unchanged through the July meeting has jumped to over 60% from 22% last month, with potential cuts now pushed further into late 2026, he said in a Tuesday note.

For now, price action will likely remain muted. “We expect the $74,000–$76,000 region to cap price momentarily,” Bitfinex analysts concluded.

Crypto World

Next Pepe Coin: Why Investors Are Choosing Pepeto Over AlphaPepe and Other Presales as Exchange Listings Approach

Pepeto is emerging as the strongest point of interest among presale buyers in 2026 as investors become more selective about where they place capital. In a market still full of empty promises and roadmap heavy launches, Pepeto is gaining traction by offering something most meme coins cannot: three real products close to launch, the PEPE cofounder, and $8.1 million in presale funding according to CoinDesk.

That distinction is becoming increasingly important. Early stage crypto buyers are paying closer attention to whether a project has real infrastructure, verified audits, and a team with a track record. On that basis, Pepeto is starting to stand apart from every other presale in the market, including projects like AlphaPepe according to Cointelegraph.

Why Pepeto is resonating more strongly with investors

1. Pepeto

A major part of Pepeto’s appeal is that it does not ask buyers to trust a team with no track record. The PEPE cofounder who built PEPE Coin is behind this project, which gives participants real confidence in what they are buying. The difference may sound minor at first, but it changes the entire investment case. Instead of putting money into a meme coin with nothing behind it, buyers get three real products approaching launch and a SolidProof audited contract.

That makes Pepeto feel more like a real investment and less like a gamble, even though it still sits firmly in the high upside segment of the market where the next Dogecoin will come from. Investors are also responding to the fact that Pepeto has built 196% APY staking directly into the presale phase, compressing supply every single day.

Rather than limiting the experience to buying and waiting, Pepeto has created an ecosystem where PepetoSwap, Pepeto Bridge, and Pepeto Exchange will keep holders engaged long after listings begin.

That makes the ecosystem easier to believe in and gives the presale more momentum than a typical meme coin launch. One reason Pepeto is drawing more attention than competing presales is that $8.1 million raised and three products close to launch present it as an active ecosystem, not a static fundraise.

The broader structure, including PepetoSwap, Pepeto Bridge, Pepeto Exchange, and 196% APY staking, gives buyers the impression that this token is attached to a growing ecosystem instead of a one dimensional meme coin pump.

2. AlphaPepe

AlphaPepe offers instant token delivery and a participation model that keeps buyers engaged after the initial purchase. The project includes features like reward claims and rank progression that give the presale more activity than a typical token sale page.

For investors who want immediate visibility over their position, AlphaPepe delivers on that front. But AlphaPepe does not have the infrastructure depth that Pepeto brings with three announced products, a SolidProof audit, and the PEPE cofounder behind the entire build.

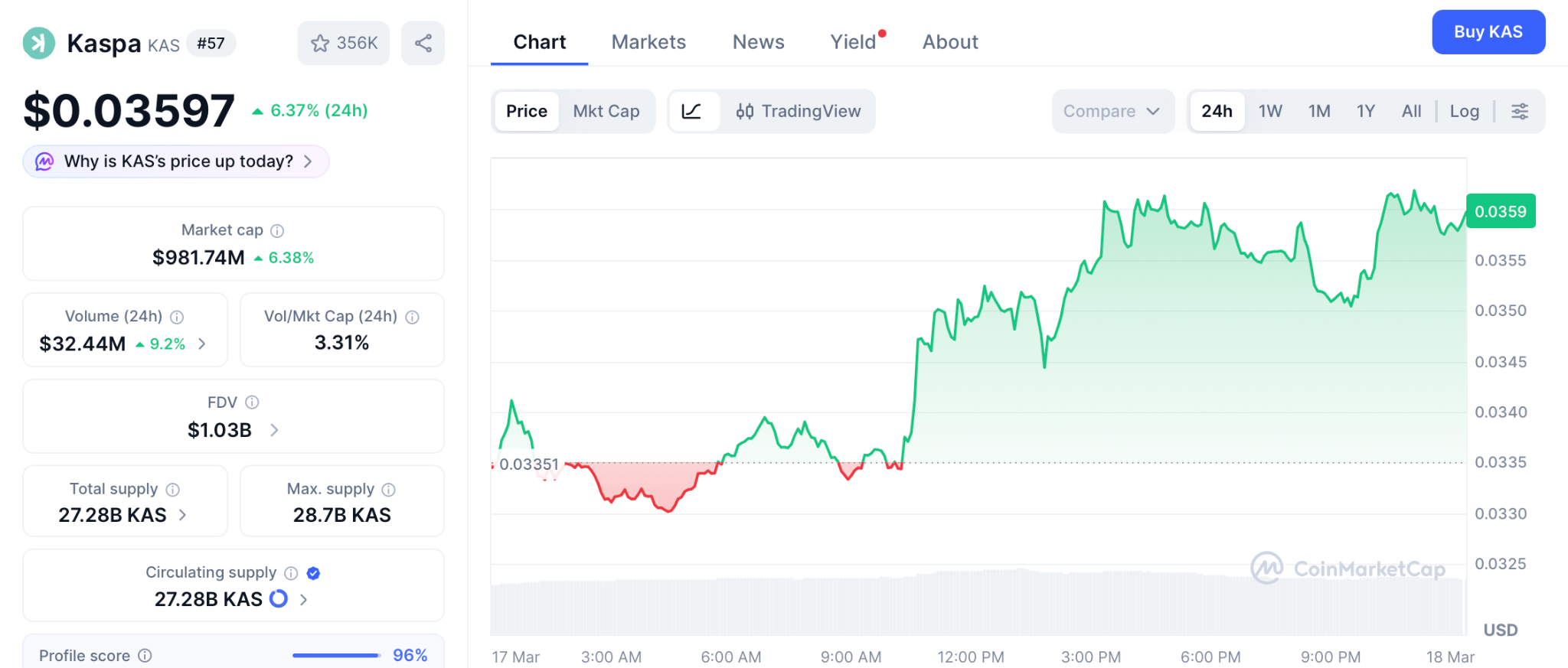

3. Kaspa

Kaspa holds at $0.035 as of March 17 with a loyal community and consistent on chain transaction volumes that reflect real usage. But analysts project a potential dip toward $0.027 by mid April before any meaningful recovery comes through.

The fully diluted valuation already bakes in significant adoption, and the returns from here are measured in modest single or low double digit percentages. For investors looking for the next Shiba Inu level entry, Pepeto at six zeros offers a fundamentally different opportunity category with far more upside potential.

Do not be the person who watches from the sidelines

Pepeto is gaining an edge over every other presale because it offers something no other meme coin has: three real products, the PEPE cofounder, and $8.1 million in proof that investors believe in it. The people who hesitated on DOGE at fractions of a penny and SHIB before it exploded know exactly what it feels like to miss a life changing entry.

That regret is what drives smart investors to act early on projects like Pepeto. They can see the $8.1 million raised, the three products approaching launch, and the SolidProof audit, and they know this is the kind of setup that creates the next wave of crypto millionaires.

Do not be the person who watches Pepeto list on exchanges and realizes they should have bought when it was still at six zeros. Visit the Pepeto official website and enter the presale today.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Why are investors choosing Pepeto over other presales?

Three products close to launch, the PEPE cofounder, SolidProof audit, and $8.1M raised set it apart.

What makes Pepeto the next Pepe coin?

The same cofounder who built PEPE Coin is behind Pepeto, with real infrastructure this time.

Could Pepeto have stronger upside than rival presales?

At $0.000000186 with three products approaching launch, Pepeto has the steepest trajectory in the presale market.

The post Next Pepe Coin: Why Investors Are Choosing Pepeto Over AlphaPepe and Other Presales as Exchange Listings Approach appeared first on Blockonomi.

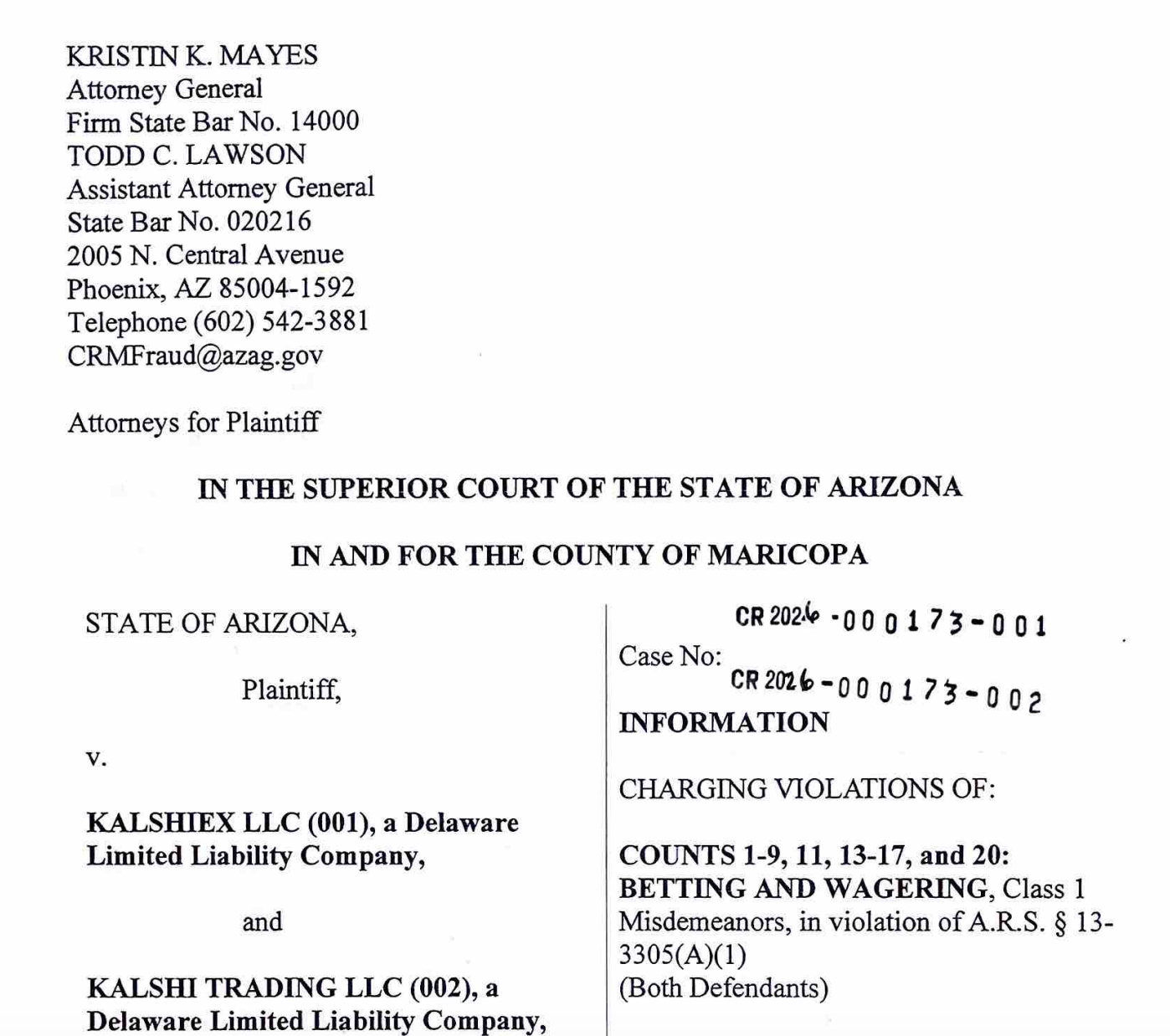

Arizona Attorney General Kris Mayes announced that her office filed gambling and related criminal charges against the companies behind prediction markets platform Kalshi.

In a Tuesday notice, Mayes said that the charges alleged that Kalshi operated an “illegal gambling business in Arizona without a license” and offered election wagering, in violation of state laws. Arizona authorities alleged that Kalshi’s prediction markets platform allowed state residents to bet on event contracts related to sports and state and federal elections.

“Kalshi may brand itself as a ‘prediction market,’ but what it’s actually doing is running an illegal gambling operation and taking bets on Arizona elections, both of which violate Arizona law,” said Mayes. “No company gets to decide for itself which laws to follow.”

According to the AG’s office, the charges followed Kalshi filing its own lawsuit against Arizona “preemptively in an attempt to avoid accountability under Arizona law.” State authorities have filed similar lawsuits against the companies of prediction market platforms like Polymarket and Kalshi.

Related: Kalshi suffers court loss in Ohio over sports betting lawsuit

“Sadly, a state can file criminal charges on paper-thin arguments,” a Kalshi spokesperson told Cointelegraph. “States like Arizona want to individually regulate a nationwide financial exchange, and are trying every trick in the book to do it. As other courts have recognized and the CFTC affirms, Kalshi is subject to federal jurisdiction. It’s different from what sportsbooks and casinos offer their customers, and it should not be overseen by a patchwork of inconsistent state laws.”

Last week, an Ohio judge denied Kalshi’s request for a preliminary injunction in a similar case against state authorities, saying that the company had failed to show that the sports event contracts available on the platform were subject to the “exclusive jurisdiction” of the Commodity Futures Trading Commission (CFTC). However, in February, a federal judge in Tennessee blocked state authorities from enforcing gambling laws against Kalshi.

CFTC chair backs “exclusive authority” over prediction markets

Now the sole commissioner on the CFTC since acting chair Caroline Pham stepped down in December, Chair Michael Selig has publicly said that the federal regulator would defend prediction market platforms from state-level lawsuits.

Last week, Selig opened a proposed rule up to public comment on how the Commodity Exchange Act would apply to prediction markets, potentially changing how the agency approaches regulation and enforcement in the future.

Magazine: Spot Bitcoin ETFs first green week, crypto ATM losses surge 33%: Hodler’s Digest, Mar. 8 – 14

Tether, issuer of the world’s largest stablecoin by market cap, USDT, has released a new AI training framework that it says allows large language models to be fine-tuned on consumer hardware, including smartphones and non-Nvidia GPUs.

According to Tuesday’s announcement, the system, part of its QVAC platform, uses Microsoft’s BitNet architecture and LoRA techniques to reduce memory and compute requirements, potentially lowering the cost and hardware barriers to developing AI models.

The framework supports cross-platform training and inference across a range of chips, including AMD, Intel and Apple Silicon, as well as mobile GPUs from Qualcomm and Apple.

Tether said its engineers were able to fine-tune models with up to 1 billion parameters on smartphones in under two hours, and smaller models in minutes, with support extending to models as large as 13 billion parameters on mobile devices.

Built on BitNet, a 1-bit model architecture, the framework can cut VRAM requirements by up to 77.8% compared with similar 16-bit models, according to the company, allowing larger models to run on limited hardware. It also enables LoRA fine-tuning on non-Nvidia hardware for 1-bit models, expanding support beyond the GPUs typically used for AI training.

The company said the performance gains extend to inference, with mobile GPUs running BitNet models several times faster than CPUs. It also pointed to use cases such as on-device training and federated learning, where models can be updated across distributed devices without sending data to centralized servers, potentially reducing reliance on cloud infrastructure.

Related: Messari’s new CEO is doubling down on AI as firm cuts staff

Crypto companies expand into AI, from mining infrastructure to autonomous agents

Tether’s move into AI infrastructure comes as crypto companies have been expanding into compute and machine learning, with activity accelerating across Bitcoin mining and the rise of AI agents.

In September, Google took a 5.4% stake in Cipher Mining as part of a $3 billion, 10-year deal tied to AI data center capacity. In December, Bitcoin miner IREN said it planned to raise about $3.6 billion to fund AI infrastructure.

The trend has continued into 2026. In February, HIVE Digital Technologies reported record revenue of $93.1 million, fueled by growth in its AI and high-performance computing (HPC) operations, while Core Scientific secured a $500 million loan facility from Morgan Stanley in March, with the option to expand it to $1 billion.

The mining sector’s pivot to AI and HPC comes as AI agents, autonomous programs that can transact, interact with services and execute tasks, are gaining momentum across the crypto sector.

In October, Coinbase introduced wallet infrastructure enabling AI agents to conduct onchain transactions. Last month, Alchemy launched a system allowing agents to access blockchain data services using USDC on Base. Also in February, Pantera and Franklin Templeton joined Arena, a platform from Sentient for testing enterprise AI agents.

On Tuesday, World, the identity network co-founded by OpenAI’s Sam Altman, launched AgentKit, a toolkit that allows AI agents to verify they are linked to a unique human using World ID capabilities while making payments via the x402 micropayments protocol.

Magazine: All 21 million Bitcoin is at risk from quantum computers

GSR is buying its way into the underwriting layer of crypto, spending 57 million dollars to turn itself from a market maker into a full‑stack capital markets and treasury platform for token issuers.

Summary

- GSR is acquiring Autonomous and Architech for a combined 57 million dollars, aiming to control the full lifecycle of digital asset projects from token design and launch to governance, liquidity and secondary‑market trading under one coordinated umbrella.

- Autonomous will keep operating independently to help teams launch and run tokenized organizations, while Architech is being folded into GSR’s advisory arm to anchor its institutional consulting, filling long‑standing gaps between issuance, governance models, listings and treasury design.

- A core focus of the new platform is treasury management, with GSR pitching liquidity planning, risk management and derivatives‑based hedging so projects behave more like mid‑market corporates or funds and less like 2021‑era DAOs that hoarded volatile treasuries and blew up in drawdowns.

Crypto market maker GSR is moving aggressively up the value chain, spending $57 million to acquire Autonomous and Architech in a bid to become a full‑lifecycle capital markets and fund management platform for digital assets. The deal is designed to give GSR direct exposure to everything from token design and launch to liquidity, governance, financing and secondary‑market trading under a single, coordinated umbrella.

According to the announcement cited by ChainCatcher, Autonomous will continue to operate independently, focused on helping teams launch and operate tokenized organizations. Architech, by contrast, will be folded into GSR’s digital asset advisory arm and positioned as a core component of its institutional consulting business. Together, the two acquisitions are meant to plug long‑standing gaps in crypto’s deal infrastructure, where token issuance, governance models, listing strategy and treasury design are often handled by different providers with misaligned incentives.

GSR’s pitch is blunt: crypto projects have grown in size and complexity, but the service stack around them is still fragmented and reactive. By pulling issuance support, advisory, market making, derivatives and asset management into a single framework, the firm wants to offer what it calls a “one‑stop capital market service” for digital assets. That includes help on structuring tokenomics, planning exchange liquidity, sequencing listings, and building governance that institutional allocators can live with over a full cycle.

A key focus of the combined platform will be treasury management for crypto projects. GSR says it intends to offer tools for liquidity planning, cash‑flow forecasting, risk management and asset allocation, pushing projects away from passive token hoarding and toward more diversified, yield‑aware portfolios. In practice, that means using GSR’s existing trading and derivatives capabilities to hedge volatility, manage stablecoin buckets, and smooth runway across market regimes.

Strategically, the move is a bet that the next wave of serious crypto issuers will look and behave more like mid‑market corporates or funds than like 2021‑era degen DAOs. Those issuers want integrated counterparties that can handle launch, liquidity and ongoing risk management without forcing them to stitch together five different vendors. If GSR can execute, it will not just be making markets for tokens; it will be designing, launching and effectively underwriting them across their entire lifecycle. For a space still plagued by ad‑hoc token launches and treasury blow‑ups, that kind of vertical integration is both an obvious opportunity—and a concentration of power that regulators and rival service providers will watch closely.

The Federal Reserve has little choice but to stay on the sidelines this week as it navigates a mix of complicated and conflicting forces playing out in the U.S. economy.

Markets are pricing in a near-zero chance that the rate-setting Federal Open Market Committee will be cutting at this meeting — or any other in the near future. In fact, futures pricing suggests policymakers won’t consider easing until at least September, more likely October, and even then just a single cut this year.

For Wednesday’s decision, Chair Jerome Powell and his colleagues have to wrestle with the Iran war, fears of an inflation spike and mixed signals from the labor market. The combination of factors all but assures the Fed will stand pat, keeping its key interest rate targeted between 3.5%-3.75%. Updates to economic and rate projections also aren’t expected to show major changes.

“The decision itself is almost guaranteed – a rate hold at the March meeting. But any hints Chair Powell might drop about the path of future interest rates will be key,” said BeiChen Lin, senior investment strategist at Russell Investments. “Broadly speaking, the U.S. economy is still on solid footing. This means however that the bar for further rate cuts in the U.S. may be quite elevated.”

Even before the war, traders weren’t expecting a cut at this week’s meeting. Instead, they expected the FOMC would wait until June, then cut at least once more before the end of the year, according to the CME Group’s FedWatch pricing.

However, the attacks — and their impact on oil and inflation — have changed the market’s calculus, even though Fed officials generally look through the types of oil shocks that have accompanied the fighting.

As such, all eyes will be on Powell’s messaging. If things go as planned, this will be Powell’s next-to-last meeting as chair, so even then markets might be wary of reading too much into the chair’s statements.

Forging the future

“With an April cut almost entirely priced out, Powell’s ability to guide markets depends on the extent to which they perceive his comments as representing the committee’s consensus rather than his own views,” Bank of America Fed-watchers said in a note. “Even setting this constraint aside, Powell will have his work cut out for him.”

Former Fed Vice Chair Roger Ferguson told CNBC he expects the committee to be “circumspect” in its post-meeting statement as it characterizes inflation, unemployment, economic growth and the expected path of policy.

“The question in front of everyone’s minds is, what do they say, if anything, about the future and how they think about changing the balance of risks,” he said.

In weighing the labor market against inflation, Ferguson said he’d prefer the Fed focus on prices.

“I’m more worried about higher inflation. You know, the Fed has a 2% target. They’ve been away from that target for multiple years now, actually,” he said. “At some point, it’s going to start to come into question whether or not the 2% target is really what the Fed’s aiming at, and so I am much more worried about that.”

Watching the dot plot

Investors will get a deeper look into the committee’s thinking when it releases updates to the Summary of Economic Projections. Within that release is the Fed’s closely watched “dot plot” grid of individual officials’ expectations for interest rates.

However, most observers expect few changes in the SEP or the dot plot: The Fed could nudge up economic growth and inflation a bit from the last update in December, but the rate outlook is expected to remain largely intact. Officials in December that they see just one cut this year, and the consensus is figured to hold even with the dissents that have accompanied recent Fed decisions.

“Looking at their communications, they will likely emphasize that the conflict in the Middle East has added further uncertainty to the outlook for both inflation and employment. However, their forecasts could look remarkably similar to three months ago,” wrote David Kelly, chief global strategist at JPMorgan Wealth Management.

On top of everything else, there’s also a lingering political air over the Fed.

President Donald Trump for years has been pressing the central bank, and Powell in particular, to cut rates. In an appearance before media members Monday, Trump again lashed out at the chair, saying that Powell should have called a special meeting.

“What’s a better time to cut interest rates than now? A third-grade student would know that,” Trump said.

However, Trump’s own Justice Department is holding up replacing Powell.

His nomination of Kevin Warsh to succeed Powell in May is being held up by a case the U.S. Attorney Jeanine Pirro is pursuing against Powell over the Fed’s headquarters renovation. Until that is resolved, Sen. Thom Tillis, R-N.C., has said he will block the Warsh nomination in the Senate Banking Committee.

This is a “scam coin” that “rugged people,” one analyst claimed.

The meme coin PIPPIN, which was among crypto’s rock stars not long ago due to its staggering price increase, has crashed by approximately 50% over the past day alone.

The big question now is whether a rebound is on the horizon or if this was a textbook rug pull, signaling that things may only get worse from here.

The Scam Revealed Its Real Face?

While the broader crypto market struggled throughout February, the lesser-known meme coin PIPPIN defied the negative conditions, registering a triple-digit price explosion. At one point, the valuation surged to $0.76, whereas towards the end of last month it climbed to an all-time high of almost $0.90.

PIPPIN’s market capitalization briefly reached nearly $900 million, thus entering the elite club of the 100 biggest cryptocurrencies, but that success was short-lived. The beginning of March saw a substantial correction, which intensified after a 52% decline over the last 24 hours. In a matter of a single day, nearly $200 million of the asset’s market cap was vaporized, and it now ranks as the 188th-largest digital asset.

The most evident reason for the crash appears to be the selling spree initiated by certain investors. Some X users reported that the same wallets that accumulated PIPPIN last week recently dumped their holdings en masse.

The meme coin has been the subject of criticism from many market observers, even during its bull run. Last month, X user Dippy.eth described it as “the largest scam of the past year,” while others think the whole project is “a cabal play,” in which a coordinated group of insiders is believed to manipulate the price through their actions. Most recently, Crypto Analyst joined the club of critics, classifying PIPPIN as a “scam coin” that “rugged people.”

How About a Revival?

Despite the overwhelming opinion among industry participants that PIPPIN is a red flag for traders and investors, some remain bullish on the asset. X user Nehal, for instance, envisioned heightened volatility ahead and eventual price increase to a new ATH of $1.

You may also like:

The asset’s Relative Strength Index (RSI) supports the rebound theory. The indicator measures the speed and magnitude of recent price movements, helping traders identify potential reversal points. It runs from 0 to 100, and ratios below 30 are considered bullish territory that could precede a resurgence. On the contrary, readings beyond 70 signal that a pullback might be on the way. Currently, PIPPIN’s RSI stands at around 24.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Newscast – Starmer Turns His Attention To Ukraine (Or Tries To)

General Mills selling food business in Brazil

Moody’s Launches Onchain Credit ratings via Canton Network

-

Tech7 days ago

Tech7 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Crypto World4 days ago

Crypto World4 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Sports3 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

NewsBeat6 days ago

NewsBeat6 days agoResidents reaction as Shildon murder probe enters second day

-

Business2 days ago

Business2 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business7 days ago

Business7 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

Sports6 days ago

Sports6 days agoPWHL, Senators discussing plan to keep Charge in Ottawa

-

Business3 days ago

Business3 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World3 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Tech4 hours ago

Tech4 hours agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

NewsBeat6 days ago

NewsBeat6 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Business3 days ago

Business3 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Business1 day ago

Business1 day agoAustralian shares drop as Iran war enters third week

-

Crypto World1 day ago

Crypto World1 day agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Tech7 days ago

Tech7 days agoClarity as strategy

-

Sports4 days ago

Sports4 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics7 days ago

Politics7 days agoTrump Says Middle East Is ‘Very Lucky’ That He’s President

-

Crypto World6 days ago

Crypto World6 days agoThree Binance Charts May Be Hinting at Bitcoin’s Next Move

You must be logged in to post a comment Login