Crypto World

FDIC, OCC, and NCUA Propose New AML/CFT Rule Updates for Banks and Credit Unions

TLDR:

- FDIC, OCC, and NCUA jointly propose updated AML/CFT rules aligned with FinCEN’s new framework.

- Banks must adopt risk-based programs, focusing resources on higher-risk customers and activities.

- Only systemic or significant compliance failures will trigger formal AML/CFT enforcement actions.

- A new FinCEN consultation framework will strengthen coordination across federal banking regulators.

Federal banking regulators have jointly proposed a rule to update anti-money laundering and countering the financing of terrorism requirements.

The FDIC, OCC, and NCUA are seeking public comment on amendments to AML/CFT compliance programs. These changes align with updates proposed by the Treasury’s Financial Crimes Enforcement Network.

The rule stems from the Anti-Money Laundering Act of 2020, which directed agencies to modernize the existing regulatory framework.

Risk-Based Approach Takes Center Stage

The proposed rule places greater focus on risk-based AML/CFT programs for supervised institutions. Banks would be required to direct more resources toward higher-risk customers and activities.

Lower-risk customers and activities would receive proportionally less regulatory attention under the new framework.

The FDIC shared this update directly, stating:

“The FDIC Board also approved a proposed rule to update requirements related to anti-money laundering and countering the financing of terrorism.”

This approach encourages institutions to align compliance efforts with their actual risk profiles. Rather than applying uniform scrutiny across all customers, banks must assess and prioritize accordingly. The goal is to produce more effective outcomes for financial institutions and law enforcement alike.

The proposed rule also requires that a bank’s designated AML/CFT compliance officer be located in the United States.

That officer must remain accessible to regulators at all times. This provision adds a layer of accountability to institutional compliance structures.

Clearer Enforcement Standards and FinCEN Coordination

The proposed rule also introduces clearer standards around when enforcement actions may be triggered. Only significant or systemic failures to implement a properly established program would qualify. This change offers banks more regulatory certainty around compliance expectations.

Additionally, the rule establishes a new consultation framework between the agencies and FinCEN. This framework applies to certain supervisory and enforcement actions taken by the FDIC, OCC, and NCUA. It is designed to strengthen coordination and consistency across federal regulators.

Banks would also gain explicit authority to share AML/CFT-related information directly with FinCEN. This provision supports more open communication between institutions and federal financial intelligence units. It further reflects the broader effort to modernize information-sharing under the Bank Secrecy Act.

The public comment period gives financial institutions, credit unions, and other stakeholders the opportunity to weigh in.

The agencies intend for these changes to produce a stronger, more consistent AML/CFT compliance environment nationwide.

Oil prices dropped sharply late April 7 while Bitcoin climbed back toward $70,000, as markets reacted to signs that a last-minute diplomatic breakthrough between the US and Iran may be close.

Reports from CNN citing a regional source said “some good news is expected from both sides soon,” with expectations that a deal could be finalized before President Donald Trump’s deadline expires. The shift in tone comes just hours after markets braced for potential escalation in the Middle East.

Bitcoin rebounded to around $69,900, recovering intraday losses, while oil pulled back from earlier highs as traders priced in a lower risk of supply disruption.

Trump’s Deadline Pushes Markets to the Edge

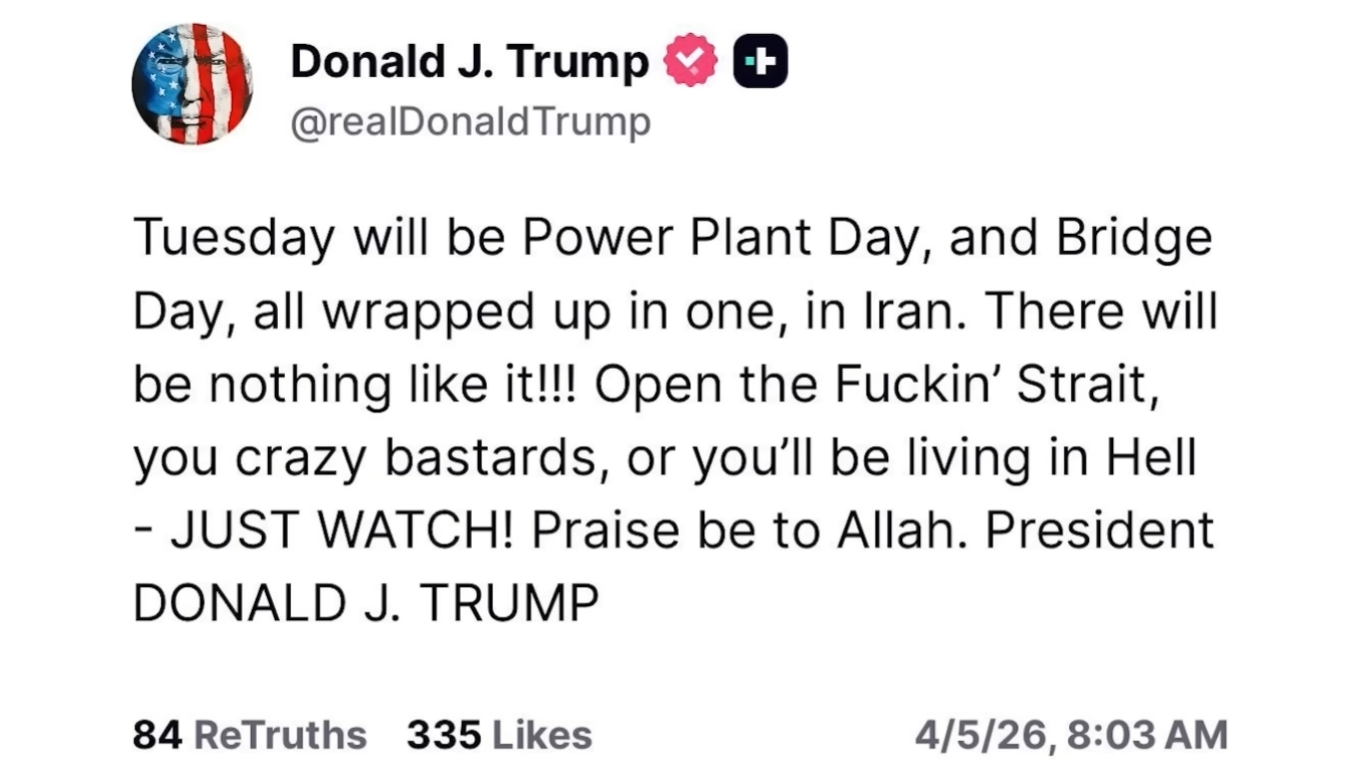

Earlier in the day, Trump imposed a hard deadline of 8 p.m. ET (midnight GMT) for Iran to agree to a US proposal that includes reopening the Strait of Hormuz.

He warned that failure to comply would trigger large-scale strikes on Iran’s infrastructure, including power plants and transport networks.

The rhetoric escalated quickly. Trump said a “whole civilization will die tonight” if no deal is reached, while US and Israeli strikes intensified across Iranian targets ahead of the deadline.

Iran responded with threats of regional retaliation and urged civilians to form human chains around critical infrastructure.

Markets reacted in real time. Oil surged on fears of prolonged disruption to global supply routes, while risk assets, including crypto, saw volatility. Now, on reports of positive diplomatic developments, oil price has sharply dropped.

Pakistan Mediation and Last-Minute Deal Signals

Diplomacy accelerated in the final hours. Pakistan, acting as a key intermediary, formally requested a two-week extension to allow negotiations to continue.

Prime Minister Shehbaz Sharif urged both sides to observe a temporary ceasefire and reopen the Strait of Hormuz as a goodwill measure.

The White House confirmed Trump was reviewing the proposal. At the same time, US officials said negotiations were ongoing, and Iran signaled it was considering the extension.

Now, with reports pointing to a possible agreement “tonight,” markets are shifting from panic to cautious optimism. The drop in oil and Bitcoin’s rebound suggest traders are positioning for de-escalation rather than immediate conflict.

The post Bitcoin, Oil, and Stock Markets Flip as Trump’s Iran Deadline Nears Deal Breakthrough appeared first on BeInCrypto.

Ethereum’s stablecoin supply reached an all-time high of $180 billion, representing 150% growth over three years and 60% of the total stablecoin market.

Stablecoin supply on Ethereum has reached an all-time high of $180 billion, up 150% over the past three years, according to Token Terminal. Ethereum currently holds a 60% market share in the stablecoin sector, dominating the landscape for dollar-pegged tokens across blockchain networks.

Token Terminal projects $1.7 trillion in stablecoin inflows to blockchain networks over the next four years. Assuming Ethereum’s market share gradually declines from 60% to 50%, the network could capture approximately $850 billion in new stablecoin flows by 2030.

Sources: Token Terminal

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

The US Federal Deposit Insurance Corporation (FDIC) is advancing a regulatory framework for stablecoin issuers that operate under its supervision, in line with the GENIUS Act. The FDIC’s board voted to publish a proposal establishing minimum standards on reserves, redemption mechanics, capital requirements, risk management and custody for stablecoin issuers and the insured depository institutions (IDIs) that fall under its purview. Signed into law roughly nine months ago, GENIUS grants the FDIC authority to oversee stablecoin activity within the banks it supervises, with a broad aim of bringing more robust oversight to a fast-growing corner of the digital-asset ecosystem. The agency noted that the proposed rules would apply to reserve-backed payment stablecoins and are scheduled to take effect on January 18, 2027, unless earlier action is taken.

The FDIC underscored that, while the proposed rule would insure reserve deposits backing a payment stablecoin, it would not extend FDIC insurance to stablecoin holders themselves. In its view, treating holders as insured depositors would be inconsistent with GENIUS Act provisions, which limit deposit insurance coverage to traditional deposit accounts rather than tokenized payments. Nevertheless, the FDIC argued that by elevating the regulatory and supervisory standards around stablecoin reserves and governance, the rules would create a more secure environment for users who rely on stablecoins for smoother payments and liquidity needs.

Key takeaways

- The FDIC proposes standards on reserves, redemption, capital, risk management and custody for stablecoin issuers and supervised banks, aligning with the GENIUS Act framework.

- FDIC insurance would cover reserves backing payment stablecoins, but not the stablecoin holders themselves, reflecting GENIUS Act’s limits on deposit insurance for digital-asset tokens.

- The GENIUS Act authorized FDIC oversight of stablecoin activity within its supervision footprint; the regulatory timetable points to a January 18, 2027 effective date for many rules, with potential earlier actions.

- The FDIC’s initiative is part of a broader, multi-agency push to regulate stablecoins, with the OCC also moving to implement GENIUS Act provisions and potentially covering a broader range of activities.

- Public input is invited through a 60-day comment window on 144 questions, signaling an extensive consultation process as regulators shape the regime.

Regulatory architecture under GENIUS Act takes shape

The FDIC’s move represents a meaningful step in translating the GENIUS Act’s broad mandate into concrete, bank-centered standards for stablecoins. By focusing on reserve management and governance, the proposal aims to reduce liquidity and credit risk that could arise if stablecoin reserves are not held in a prudent and auditable manner. The agency’s emphasis on custody and risk management signals a priority on how reserves are held and safeguarded, a critical concern for both issuers and users who rely on the stability of these digital tokens in everyday payments and cross-border transfers.

The GENIUS Act, enacted last year, gave the FDIC new authority to supervise stablecoin activity within the banking system it already oversees. That framework is designed to ensure that as stablecoins grow in breadth and usage, the institutions backing them adhere to consistent, enforceable standards. In the FDIC’s view, this approach should provide greater assurance that payment-stablecoin networks operate with heightened governance and capital resilience, reducing potential shock transmission to the broader financial system.

What would be insured—and what would not

A central nuance in the FDIC proposal is the distinction between reserve insurance and holder protection. The agency confirmed that reserve deposits backing a payment stablecoin would fall under the FDIC’s insured deposits framework, at least for the portion of funds held in its supervised banks. However, this protection would not extend to the token holders themselves. The FDIC argued that treating stablecoin holders as insured depositors would run counter to GENIUS Act limitations on insurance coverage for payment-stablecoin users. In practice, this means that while the rails and buffers supporting a paid stablecoin could be shielded by insurance-like guarantees, the value risk borne by holders would remain separate from traditional deposit protections.

Despite the stance on holder protection, the FDIC stressed that the proposed rules would nonetheless enhance security and oversight for those using payment stablecoins by subjecting reserve management and custody to elevated standards. In its view, that combination should foster greater confidence among users and counterparties who rely on stablecoins for on-chain settlements, remittances and retail payments, especially during periods of market stress.

Feedback, timing and a wider regulatory arc

Public participation is a centerpiece of the FDIC’s approach. The agency invited the public to comment on 144 questions related to how it should regulate stablecoin issuers, with a 60-day window for responses. The consultation process follows a December 19 release detailing an earlier GENIUS Act implementation step that established an application procedure for insured depository institutions seeking approval to issue payment stablecoins through subsidiaries. The current proposal thus sits within a broader, staged effort to codify how financial institutions can participate in the stablecoin economy under federal supervision.

The FDIC’s activity is part of a coordinated federal push on digital-asset regulation. The Office of the Comptroller of the Currency (OCC) is also advancing GENIUS Act implementations, and the OCC’s track is described as broader in scope than the FDIC’s, covering national bank subsidiaries and certain nonbank issuers. The dual-track approach underscores how U.S. regulators are attempting to thread the needle between fostering innovation in digital payments and ensuring they do so within well-defined risk-management and consumer-protection boundaries.

Why this matters for markets, users and builders

For stablecoin issuers and banks alike, the FDIC’s proposal could redefine the cost and feasibility of issuing payment-stablecoins through FDIC-supervised institutions. A set of uniform reserve and custody standards can reduce fragmentation across different banking partners and issuer structures, providing a clearer pathway for compliance and oversight. This, in turn, may affect how quickly issuers can scale, how they structure reserve holdings, and how custodial arrangements are designed to meet heightened standards. While the insurance of reserves could boost confidence among users and counterparties, issuers may face additional capital and operational requirements that influence product design, liquidity management and the speed of settlement in volatile market conditions.

From a risk perspective, the emphasis on robust governance around reserves and redemption mechanics is aimed at mitigating a key class of failure modes that previously rattled stablecoin markets. If implemented as proposed, the rules could help prevent liquidity stress scenarios that arise when reserves are illiquid or poorly controlled, contributing to a more stable on-chain economy at a time when stablecoins have become a central component of on-chain commerce and liquidity provision.

Investors and builders will want to watch how the agencies harmonize their rules, how fast the 2027 effective date approaches, and how the public comment shapes final language. The interplay between the FDIC’s rules and the OCC’s broader GENIUS Act program will be particularly consequential, potentially creating a unified federal approach to stablecoins that could set global benchmarks for custodian standards, reserve transparency and prudential requirements for issuers.

Beyond the technical details, the broader takeaway is that the U.S. is moving toward a more formalized, bank-centric governance model for stablecoins. This shift could influence where stablecoin reserves are held, how issuers structure their corporate and regulatory relationships, and how users evaluate the safety and reliability of digital payment rails in the coming years.

Keep an eye on how the public comments frame the discussion. The 60-day input period will likely surface perspectives from banks, stablecoin issuers, consumer advocates and other stakeholders, shaping the final iteration of these rules and their ultimate impact on the evolving landscape of digital payments in the United States.

As regulators prepare to publish the final rules, market participants should assess potential stress-test scenarios, reserve-management practices and custody structures that could become industry benchmarks. The GENIUS Act’s intent is clear: bring higher standards and greater scrutiny to a sector that touches everyday commerce, while preserving the core benefits that stablecoins offer in terms of efficiency and interoperability across financial rails.

Readers should remain attentive to updates from both the FDIC and the OCC as they expand on their respective GENIUS Act plans, and to how issuers adapt their product designs in response to the evolving regulatory terrain.

The FDIC’s latest step marks a significant milestone in the ongoing effort to codify the security and reliability of stablecoins within the U.S. financial framework. The next few months will reveal how the 144 questions are addressed and how the final rules translate into real-world change for stablecoin participants across banking and digital-asset markets.

Closing perspective: As the regulatory scaffolding around stablecoins thickens, market participants should watch closely how the finalized rules balance innovation with safety, and how the two regulatory tracks converge to shape a more predictable, bank-backed landscape for digital payments.

Crypto World

Polygon Giugliano Hardfork Scheduled for April 8 to Improve Finality and Fees: Polygon Foundation

The Polygon Foundation confirmed the Giugliano hardfork will activate on mainnet at block 85,268,500 on April 8 at approximately 2 p.m. UTC.

The Polygon Foundation confirmed the Giugliano hardfork will activate on mainnet at block 85,268,500 on April 8 at approximately 2 p.m. UTC. The upgrade targets faster finality and improved fee transparency, allowing block producers to announce blocks earlier and reducing transaction confirmation time to finality.

The hardfork is part of Polygon’s broader push toward higher throughput for payments and tokenized assets. The upgrade follows a challenging 2025 for the network.

Sources: Polygon Foundation Forum | Polygonscan | BeInCrypto

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Some past enforcement actions against cryptocurrency companies lacked clear investor benefit and misinterpreted federal securities laws, the US Securities and Exchange Commission (SEC) said on Tuesday.

Since the 2022 fiscal year, the SEC brought 95 actions and $2.3 billion in penalties for “book-and-record violations,” it said in a statement about its enforcement results for 2025.

“Together with seven crypto firm registration-related and six ‘definition of a dealer’ cases, these cases identified no direct investor harm from those violations, produced no investor benefit or protection.”

It also reflected a “bias for volume of cases brought versus matters of investor protection,” a misallocation of resources and a misinterpretation of federal securities laws, the SEC said.

It is the latest example of the regulator’s shift in approach towards enforcement since it came under new leadership under SEC Chair Paul Atkins in April 2025.

His predecessor, former SEC Chair Gary Gensler, has been accused of pursuing a regulation-by-enforcement approach toward crypto. Since his departure, the SEC has adopted a friendlier stance toward digital assets.

SEC said it is shifting its focus to quality over quantity

In the lead-up to Donald Trump’s 2025 inauguration, the SEC enforcement division engaged in an “unprecedented rush” to bring cases and moved ahead with an “aggressive pursuit of novel legal theories,” the agency said.

Atkins said the agency has since shifted away from this approach, ending regulation by enforcement and refocusing on the commission’s core mission by prioritizing cases that provide meaningful investor protection and strengthen market integrity.

“We have redirected resources toward the types of misconduct that inflict the greatest harm—particularly fraud, market manipulation, and abuses of trust—and away from approaches that prioritized volume and record-setting penalties over true investor protection,” he added.

Consulting firm Cornerstone Research reported in November that under Atkins, the number of enforcement actions against public companies, including those involving crypto, decreased by about 30% in fiscal 2025 compared with fiscal 2024.

In connection with 2025 enforcement actions, the SEC said it obtained orders for monetary relief totaling $17.9 billion, comprising $7.2 billion in civil penalties and the remainder in disgorgement and prejudgment interest.

Related: Crypto market safe harbor lands at White House for review

“This year’s enforcement results clarify the flaws of these actions and their respective penalties and re-establish the definition and measure of enforcement effectiveness, grounded in Congress’ original intent and focused on bringing actions that actually prevent investor harm instead of headlines and inflated numbers,” the SEC said.

Some crypto companies are still in the firing line

Despite the SEC’s enforcement shift, several crypto companies were still hit with enforcement actions in 2025.

In May 2025, Unicoin and four of its current and former executives were sued by the SEC for allegedly raising $100 million by misleading investors about certificates that purported to convey rights to receive Unicoin tokens and stock. However, the platform has accused the agency of distorting its regulatory statements to build a case.

The SEC also filed a civil complaint against Ramil Ventura Palafox in April 2025, CEO of Praetorian Group International, for allegedly orchestrating a $200 million Ponzi scheme. A parallel criminal case brought by the US Department of Justice resulted in Palafox’s February sentence of 20 years in prison.

Cardano’s ADA climbs about 4–5% to the mid‑$0.24s on Tuesday as traders rotate into high‑beta majors, but futures data shows churny perps and weak open interest behind the move.

Summary

- Cardano price jumps about 4–5% intraday, outpacing most large‑caps outside Bitcoin and Ethereum.

- Perps volume climbs while open interest lags, pointing to short‑term churn rather than committed longs.

- ADA trades as high‑beta L1 DeFi infrastructure, echoing broader liquidity‑driven flows across majors.

Cardano’s price rallied roughly 4–5% on Tuesday, extending a short burst of outperformance versus most large‑caps outside Bitcoin and Ethereum as traders rotated into higher‑beta names.

ADA (ADA) Spot prices hovered around $0.24–$0.25, up from the $0.23–$0.24 range seen earlier in the week, leaving ADA still far below its 2026 peak but firmly green on the day. The move comes as liquidity conditions across majors improve marginally and traders look for catch‑up plays after focusing on Bitcoin for most of the recent macro‑driven rally.

On centralized venues, Cardano was recently quoted near $0.2417 with a 24‑hour trading volume of about $1.91 million and a market cap of roughly $8.91 billion, representing around 0.44% of total crypto market capitalization.

Historical data from CoinMarketCap shows ADA closing at $0.2479 on April 5, $0.2462 on April 4, and $0.2394 on April 3, underscoring how modest the absolute price move has been even as percentage gains look eye‑catching on the day.

Over the past month, ADA remains down about 5% and roughly 58% over the last year, highlighting the gap between short‑term momentum and longer‑term underperformance.

Derivatives data paints a more cautious picture behind the headline price spike. Cardano futures open interest climbed as high as $416 million in February, according to Coinglass figures cited by MEXC, but has struggled to hold above the $400–$500 million band as speculative interest faded into March and early April. A February report noted total ADA derivatives volume near $669.6 million with funding skewed long, yet that backdrop has since softened, with Yahoo Finance recently flagging open interest stalling below $500 million and slipping toward $431 million.

That mix—rising intraday volume, modest fresh open interest, and funding that has flipped from aggressively long to more neutral—suggests the latest leg higher is being driven by perp churn rather than big structural positioning. From a technical perspective, external trackers show ADA’s daily RSI grinding up from mid‑range toward the low‑60s, a constructive but not yet overbought setup that typically characterizes flow‑driven beta rallies rather than full‑blown breakouts.

As a proof‑of‑stake layer‑1 focused on DeFi and smart‑contract infrastructure, Cardano is trading in line with other L1s that are acting as liquidity proxies rather than idiosyncratic narratives. A recent crypto.news story on Cardano’s price after its rollout across 137 Spar stores in Europe noted that ADA had been locked in a tight $0.26–$0.30 range, with dwindling volatility before today’s nudge higher, while another crypto.news story on ADA’s broader market analysis framed the token’s near‑term path between $0.41 and $0.45 if liquidity conditions improve. In parallel, crypto.news coverage of Bitcoin’s recent drawdown below $70,000 and risk‑off jitters around U.S.–Iran tensions shows how fast flows can reverse across the complex, reinforcing the idea that ADA’s latest beta burst may fade quickly without a durable pickup in open interest and spot demand.

Changpeng “CZ” Zhao became a household name in the cryptocurrency sector after founding Binance, the world’s largest crypto exchange. Following a series of legal and regulatory challenges that culminated in a prison sentence, Zhao has authored an autobiography recounting his rise — and subsequent fallout.

The 364-page manuscript, titled Freedom of Money, presents a first-person account of Zhao’s life and career. The foreword is written by Yi He, a Binance co-founder who has worked with Zhao since 2014.

Zhao writes that his story has been shaped by media coverage, court filings and public commentary. He describes the book as an account intended to provide additional context to those narratives.

Throughout the memoir, Zhao emphasizes the human dimension behind Binance’s rapid ascent — and his personal and professional downfall — which he argues has been lost in soundbite-driven coverage.

The memoir covers his early life and career in finance and technology, as well as the founding of Binance in 2017. It outlines the company’s rapid growth into one of the world’s largest cryptocurrency exchanges.

Regulatory failures and accountability

Zhao served a four-month prison sentence in the United States in 2024 after pleading guilty to violating US Anti-Money-Laundering laws, as part of a broader settlement with authorities that also required him to step down as Binance CEO.

The case marked a major enforcement action by the US Department of Justice, which had initially sought a longer sentence to reflect the severity of the violations. Binance, for its part, agreed to pay billions of dollars in penalties and implement sweeping compliance reforms.

US regulators had for years scrutinized Binance over alleged failures related to anti-money laundering controls, sanctions compliance and operating without proper licensing. The settlement effectively closed one of the most high-profile investigations in the crypto industry.

In the memoir, Zhao reflects on the decisions and missteps that led to these outcomes. He recounts the events surrounding the settlement, his guilty plea and his resignation, describing the tradeoffs made during Binance’s rapid growth.

The book also includes detailed descriptions of his time in federal prison, including the adjustment from leading a global company to living in a confined environment.

Related: Binance led Q1 crypto derivatives as Hyperliquid cracked top 10: CoinGlass

“Freedom of money”

The book’s title reflects a central theme of the memoir. Zhao describes the “freedom of money” as the idea that cryptocurrency can address barriers to financial access, particularly in countries with limited banking infrastructure or strict capital controls.

He links part of Binance’s growth to users in emerging markets who used the platform to move funds across borders, hedge against local currency volatility and access global financial markets.

Zhao also acknowledges that expanding access at scale introduced challenges. He writes that Binance’s rapid growth often outpaced regulatory frameworks, contributing to gaps in compliance and oversight that later drew scrutiny from authorities.

Related: Crypto’s 2026 investment playbook: Bitcoin, stablecoin infrastructure, tokenized assets

TLDR

- Bitcoin’s long-term holder supply has turned positive over the past 30 days.

- More Bitcoin is now being held by investors for the long term rather than being sold.

- The change in supply comes from coins aging past six months and entering the long-term holder category.

- Despite the price dropping below $70,000, long-term holders have increased their supply by 308,000 BTC.

- Currently, 29% of long-term holder supply is in loss, which is still below past cycle bottom levels.

Bitcoin (BTC) has seen a shift in long-term holder supply over the past month. Data indicate that investors are holding onto their assets, with long-term supply rising in recent weeks. Despite recent price challenges, this trend shows a change in investor behavior.

Bitcoin Faces Selling Pressure Despite Increased Long-Term Holdings

On April 6, Bitcoin briefly surpassed the $70,000 mark but was unable to sustain this price level, dropping to around $68,000. Despite the downward price action, Bitcoin’s long-term holder supply has flipped positive over the past 30 days. This increase stems from coins transitioning from short-term to long-term holdings as they age past six months.

The rise in long-term holder supply marks a shift in the market, as more Bitcoin is now being retained in wallets. This trend reflects a decision by investors to hold rather than sell their coins. Data from analyst Darkfost confirms this, highlighting a jump from -674,000 BTC to a positive +308,000 BTC over the past 30 days. This shift indicates a growing number of investors holding onto their Bitcoin.

Data Suggests a Long-Term Holding Trend

The increase in Bitcoin’s long-term supply comes from coins that have not been moved for over six months. Darkfost clarified that this data does not necessarily reflect new buying, but rather coins that have simply aged into the long-term holder category. These coins have remained untouched for a significant period, reflecting a preference for holding rather than selling.

According to the analyst, this shift in behavior is notable, as it signals a growing inclination to retain Bitcoin even during periods of low spot demand. Historically, similar changes in long-term holder supply have preceded price increases, although Darkfost cautioned that it is too early to confirm a lasting trend. The current data suggests that more investors are making the choice to hold Bitcoin in anticipation of future gains.

Bitcoin Long-Term Holder Supply in Loss Still Below Past Cycle Levels

Although long-term holder supply is increasing, a significant portion of this supply remains in loss. At present, 29% of Bitcoin held by long-term investors is in the red. This figure is still well below previous market cycle bottoms, where losses reached 44% to 53%. This suggests that Bitcoin’s market has not yet reached its lowest point, despite the rise in long-term holder supply.

Market analysts, including Ardi, have noted that similar loss levels in previous years, 2015, 2018, and 2022, marked the bottom of market cycles.

While the current loss percentage remains lower, it continues to rise, signaling that Bitcoin may be heading towards new lows. This increase in long-term holders could potentially influence Bitcoin’s price trajectory, but investors remain cautious as the market adjusts.

The US politics news today midterm election Georgia Trump test is live: polls opened this morning in the deeply conservative Georgia-14 district that Marjorie Taylor Greene vacated, where Republican Clay Fuller faces Democrat Shawn Harris in a runoff that analysts say could be the clearest early signal yet of whether the Iran war is beginning to hurt Republicans’ electoral standing.

Summary

- Democrat Shawn Harris, a retired Army brigadier general and cattle farmer, led the March 10 primary with 37% in a district Trump won by 37 points in 2024, prompting Trump himself to urge Republicans to “be careful” and post a personal get-out-the-vote message Monday night

- If Harris wins or comes significantly closer than expected, it would signal elevated Democratic enthusiasm heading into November’s midterms, where Republicans hold a razor-thin 218-214 House majority

- The Iran war has become a central issue: Harris has explicitly tied rising gas prices to the conflict, telling voters “they will have to stop at the pump, and that’ll be the last thing they think about before they go and vote”

The US politics news today midterm election Georgia Trump dynamic arrived at its most visible test yet when polls opened this morning in Georgia’s 14th Congressional District, a stretch of northwest Georgia that runs across 10 counties from suburban Atlanta to Tennessee. Bloomberg reported the race as a direct test of Trump’s standing with his own base amid the Iran war, with Harris, a retired Army brigadier general, running against Trump-endorsed district attorney Clay Fuller in the runoff to replace MTG.

The district is the most Republican-leaning congressional seat in Georgia, according to the Cook Political Report. Trump carried it by 37 points in 2024. Harris won the March 10 all-party primary with 37% against 17 candidates — 12 of whom were Republicans — a result that rattled enough people in Washington that Trump posted a personal appeal Monday night: “I am asking all Republicans, America First Patriots, and MAGA Warriors, to please GET OUT AND VOTE for a fantastic Candidate, Clay Fuller.”

Harris has positioned gas prices as his closing argument. “When they go to the polls, they will have to stop at the pump, and that’ll be the last thing they think about before they go and vote,” he told Fox News. “And they’re going to say, ‘You know what, Shawn Harris is the only one that’s talking about bringing down costs.’” National gas prices now average $4.14 per gallon, up from $2.98 before the war began.

Harris has also used his military background to credibly challenge the war. “We will win this war militarily. However, if we don’t watch it and be clear with the American people, based on these gas prices and diesel prices, we could actually lose this war politically,” he said.

Fuller’s counter: “The voters in Georgia-14 support the president in this endeavor.” He has described himself as a “MAGA warrior” and called voters ready to support the district’s continued representation under Trump’s agenda.

What the Margin Will Tell November’s Candidates

Even a Harris loss by a small margin would carry significant information for both parties. As one analyst noted, the key question is “the margin by which he loses, and whether or not it’s narrower compared to 2024” — and whether Harris can demonstrate that Democratic infrastructure built during the special election translates into broader midterm momentum in Georgia.

The stakes for crypto policy are real as well. As crypto.news reported, the Fairshake crypto super PAC has $116 million set aside for the 2026 midterms, targeting congressional races where candidates’ positions on digital asset legislation will shape November’s outcomes. A House that shifts Democratic in November would significantly change the calculus for the CLARITY Act. As crypto.news noted, Democrats may have little incentive to accelerate crypto legislation if they believe they can regain House control — and tonight’s result in Georgia-14 will be the first data point on whether that scenario is becoming more credible.

“What I’m looking at is the improvement compared to 2024,” one Georgia political analyst told MS NOW. “That improvement suggests enthusiasm among Democrats that could be a harbinger going into the November midterm elections.”

The bitcoin price prediction latest crypto news Iran deadline today tells a familiar story: BTC briefly reclaimed $70,000 on Monday ceasefire hopes before retreating to the $68,000 range on Tuesday as Iran rejected the deal and Trump’s 8 PM ET deadline drew closer, with ETH, SOL, and XRP all posting losses of 2% to 4%.

Summary

- Bitcoin touched $70,200 on Monday on ceasefire optimism, then pulled back to around $68,200 on Tuesday as Iran rejected the 45-day proposal and geopolitical risk overwhelmed bullish sentiment

- Spot Bitcoin ETFs recorded $471 million in inflows on April 6, the sixth-largest single-day total of 2026 and the highest since late February, signaling sustained institutional demand even as price action weakened

- Analysts say a confirmed deal tonight could push BTC toward $75,000, while a major escalation risks breaking the $66,500 support level and opening a path toward $60,000

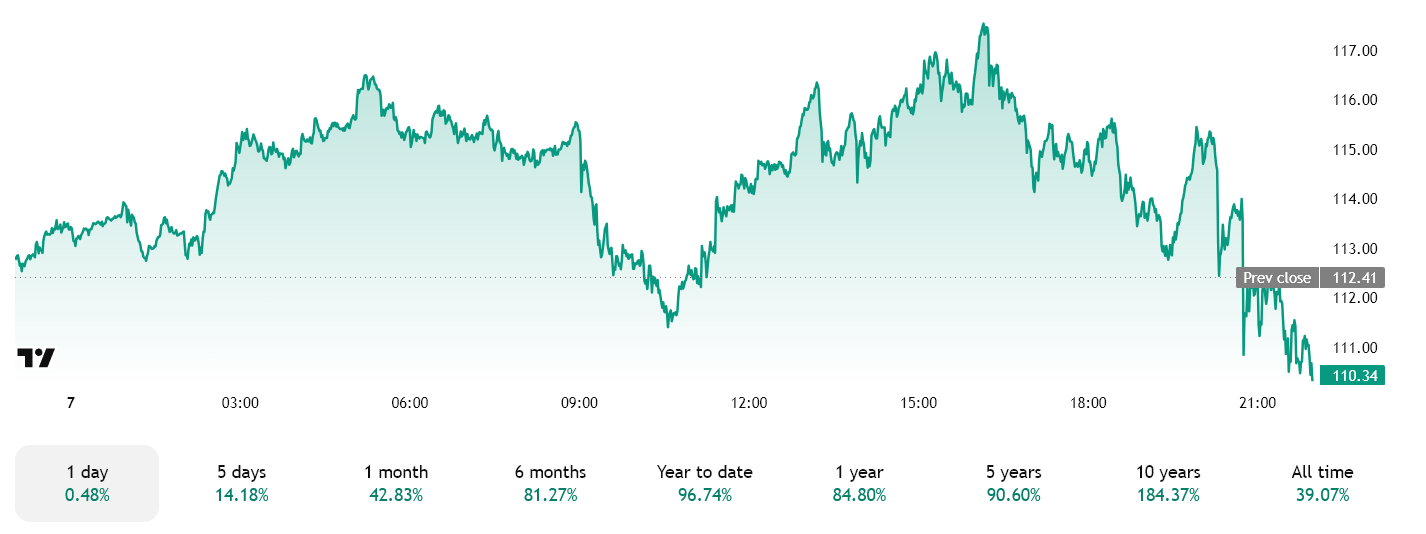

The bitcoin (BTC) price prediction latest crypto news Iran deadline today is being driven entirely by geopolitics. Bitcoin pulled back to around $68,228 on Tuesday morning after Monday’s brief touch of $70,200, as Iran formally rejected the US-backed 45-day ceasefire proposal and Trump confirmed his 8 PM ET strike deadline remained in force. The crypto market cap fell roughly 2% to $2.42 trillion as traders positioned defensively heading into the evening.

Ethereum dropped 2.9% to $2,090. Solana fell 3.8% to $79.44. XRP slid 3.3% to $1.31. The pattern is the same one that has played out across six weeks of this conflict: a de-escalation headline sparks a rally, Iran rejects the terms, and the gains get erased within hours.

The one data point bucking the bearish narrative is spot Bitcoin ETF flows. Monday’s $471 million in inflows marked the sixth-largest single-day total of 2026 and the highest since late February, according to Bloomberg. Binance Research found this month that Bitcoin’s correlation with its Global Easing Breadth Index, which tracks 41 central banks, turned strongly negative after the launch of spot ETFs, suggesting institutional investors are treating dips as accumulation opportunities regardless of short-term price moves.

As crypto.news reported, a confirmed agreement tonight could open the door to a move toward $75,000, as easing tensions would support risk appetite across financial markets. Failure to reach a deal points in the other direction, with $66,500 identified as the key support zone and, below that, a Glassnode-flagged negative gamma setup that leaves BTC exposed to a faster move toward $60,000.

The Two Scenarios Traders Are Pricing

“This move looks less like a shift in fundamentals and more like positioning getting caught offsides,” said Diana Pires, chief business officer at sFOX. “Heading into the weekend, sentiment was heavily skewed bearish and short interest had built up across the market. Once ceasefire headlines hit, that positioning had to unwind.”

The six-week trading range of $65,000 to $73,000 that has defined Bitcoin during the Iran war remains intact. Breaking above it requires either a genuine ceasefire or a significant improvement in the macro backdrop — neither of which looks imminent at press time.

What the Fed Overlay Adds

Oil above $111 per barrel means inflation expectations remain elevated, which reduces the Federal Reserve’s room to cut rates. The market currently prices in little near-term Fed movement. Bitcoin, which performs best in easing liquidity environments, is caught between institutional accumulation demand and a macro backdrop that keeps capital defensive. That tension is precisely why BTC has held its war range rather than breaking either way.

As crypto.news noted, the Strait of Hormuz situation is the single most important variable. Tonight’s 8 PM ET deadline is the clearest binary event Bitcoin has faced in the six weeks since the war began.

“Survivor” star Monica Culpepper breaks silence on son Rex's death at 28: 'Our worst nightmare won't end'

The Drums “Money” (New Single)

US rejects aluminum tariff relief request from Ford, WSJ reports

-

NewsBeat5 days ago

NewsBeat5 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business2 days ago

Business2 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports3 days ago

Sports3 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business4 days ago

Business4 days agoExpert Picks for Every Need

-

Business6 days ago

Business6 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech6 hours ago

Tech6 hours agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business3 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Tech6 days ago

Tech6 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Tech6 days ago

Tech6 days agoDrawing Tablet Controls Laser In Real-Time

-

Crypto World6 days ago

Crypto World6 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion2 days ago

Fashion2 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World6 days ago

Crypto World6 days agoWhy It’s Partnering, Not Issuing

-

Politics5 days ago

Wings Over Scotland | The quality of mercy

-

Business3 days ago

Business3 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoDebenhams Occasion Dresses for Girls 2026 Collection

-

Sports6 days ago

Sports6 days agoSteal Gary Woodland’s subtle power move for longer drives

-

Tech6 days ago

Tech6 days agoBattery Tester Outperforms Cheaper Options

You must be logged in to post a comment Login