Crypto World

Fed Seeks Public Feedback on Proposal to End Operation Chokepoint 2.0

The Federal Reserve is moving to enshrine a rule that would remove reputational risk as a driver of banking supervision, a shift crypto advocates say could blunt a pattern of debanking in recent years. The central bank began codifying the change last June, directing its supervisors to stop pressuring banks to sever client ties over reputation concerns and instead assess banking relationships primarily through financial risk management. Now, in a formal rulemaking proposal published on Monday, the Fed is inviting public comment on turning that approach into law, with a 60-day window to hear from stakeholders. The initiative arrives amid ongoing debates about the boundaries of political and ideological considerations in financial services and bears directly on how crypto firms access banking pathways that were once routine.

The Fed’s upward move comes with explicit acknowledgment of the concerns raised by lawmakers and industry observers about how reputation risk has been wielded in ways that affect crypto and other disfavored sectors. In the accompanying release, vice chair for supervision Michelle Bowman framed the issue in stark terms: “We have heard troubling cases of debanking — where supervisors use concerns about reputation risk to pressure financial institutions to debank customers because of their political views, religious beliefs, or involvement in disfavored but lawful businesses.” She stressed that discrimination on these bases runs counter to federal policy and has no place in the Fed’s supervisory framework. The push to formalize this standard reflects a desire to shield legitimate business activity from ad hoc revocation of banking access under the guise of reputation risk.

As the digital asset ecosystem pushes for clearer rules and a more stable banking landscape, political observers weighed in as well. In a post on X, Senator Cynthia Lummis lauded the Fed’s move, arguing that it should not be the regulator’s role to adjudicate who can participate in the crypto economy. She framed the reform as a breaking point that could help “permanently remove ‘reputation risk’ from Fed policy and put Operation Chokepoint 2.0 to rest so America can become the digital asset capital of the world.” The sentiment was echoed by Galaxy Digital’s head of firmwide research, Alex Thorn, who lauded the development as part of the industry’s ongoing push to roll back what supporters call choke points in traditional finance. Thorn signaled via X that the rollback continues, underscoring the ongoing tension between crypto firms seeking direct access to banking services and legacy financial institutions wary of reputational exposure.

Operation Chokepoint 2.0 is a label used within crypto circles to describe what some perceived as a coordinated effort by the Biden administration and the banking sector to restrict crypto firms’ access to essential banking services. The discourse around this concept has included references to previous policy debates and actions that crypto insiders argued were designed to curb the industry’s growth by pressuring banks to sever ties. The Fed’s latest move—aimed at removing reputation-based triggers from supervisory decisions—has been positioned by supporters as a corrective step toward neutral, risk-based decisions that prioritize financial metrics over political or ideological considerations. The discourse surrounding debanking isn’t new: disclosures and investigations have connected the policy debate to broader questions about regulatory overreach, financial privacy, and the U.S.’s stance toward crypto innovation.

The policy questions extend beyond banking practices into the political discourse around regulation. The administration has signaled an intent to curb debanking in the United States, with discussions touching on how regulators should approach crypto-related clients. The public record features a mix of official statements and industry commentary about the proper balance between safeguarding the financial system and enabling a vibrant digital asset sector. The thread linking this initiative to broader regulatory reform remains a focal point for crypto firms seeking greater clarity and predictability in how banks evaluate risk and structure services for digital assets.

In parallel, proponents of the reform have pointed to links between reputational considerations and broader regulatory strategies aimed at safeguarding consumers while not constraining legitimate innovation. The Fed’s invitation for public comment signals a willingness to test the proposed framework against diverse viewpoints before any final rule is enshrined. If adopted, the rule could set a precedent for how U.S. supervisory agencies weigh risk and approach non-financial considerations in decisions that affect access to fundamental banking services for crypto businesses and other sectors that have faced similar pressures.

Beyond the policy debate, the legal and practical implications loom large. Some observers have highlighted how banks may recalibrate due to the clarity this rule would provide or because it reduces discretionary leverage tied to reputational risk. Others warn that a formalized standard would still require careful definition to avoid unintended consequences, such as banks underreacting to financial risk signals or inadvertently channeling risk through opaque channels. In the end, the rule’s success hinges on how well the Fed can translate a principle into a measurable framework that stands up to scrutiny and serves as a reliable reference for bankers, crypto firms, and regulators alike. The Fed’s consultation period will be a key barometer of how broad support is for codifying this approach and what refinements may be necessary to address edge cases and evolving digital-asset landscapes.

The evolving narrative around debanking and regulatory clarity has also intersected with political dimensions, including ongoing disputes over how bank accounts are treated during periods of political or ideological contention. While the Fed’s move is framed as a technical adjustment to supervisory practice, the broader implications touch on the dynamics of financial inclusion, national competitiveness in the crypto space, and the boundaries of regulatory intervention in private-sector decisions. As negotiators and policymakers weigh the future of digital asset markets, this rulemaking could become a touchstone for how the United States balances the need to manage risk with the desire to foster innovation and maintain the country’s pull in the global crypto economy. The public comment period will determine not only the technical shape of the rule but also the degree to which the policy resonates across industry, advocacy groups, and financial institutions that must implement it in the months ahead.

Key takeaways

- The Fed is seeking to codify the removal of reputation risk as a factor in banking supervision, a move crypto advocates view as reducing punitive pressure on banks over political or ideological considerations.

- A 60-day public-comment window accompanies the proposal, signaling an invitation for industry, lawmakers, and the public to weigh in on the formal rule.

- The initiative follows a June policy shift in which the Fed directed supervisors to base decisions on financial risk management rather than reputational concerns.

- Supporters, including lawmakers and industry figures, frame the reform as a step toward restoring access to banking for crypto firms and ending what critics call “Chokepoint 2.0.”

- Opponents may push for careful definitions of “reputation risk” to avoid unintended loopholes or gaps in enforcement that could leave some customers exposed to informal criteria.

Market context: The policy sits within a broader regulatory environment where liquidity, risk sentiment, and clarity around digital assets influence the willingness of traditional banks to service crypto clients. As policymakers push for explicit standards, market participants look for predictable frameworks that reduce opacity in a space historically marked by sudden access changes and reputational triggers.

Why it matters

For crypto companies, the Fed’s potential rule offers a clearer path to banking access that is less contingent on perceived reputational concerns. In a sector where financial infrastructure—payments, settlement, and treasury services—can determine a project’s viability, a formal standard buffers firms against abrupt disconnections from banking rails. The change could also incentivize banks to adopt uniform risk-based criteria, improving consistency across institutions and reducing the likelihood that decisions are swayed by external factors unrelated to financial health.

From a policy perspective, the move indicates an intent to articulate a more transparent governance framework for supervisory actions. If successfully enacted, the rule could help normalize the treatment of crypto firms within mainstream financial services and strengthen the U.S. position as a hub for digital asset innovation. Support from lawmakers who view debanking as a civil-rights or anti-competitive concern further underscores the political resonance of the issue, elevating the debate beyond technocratic risk management into a broader discussion about access to finance and national competitiveness.

Nevertheless, the discussion remains nuanced. Advocates stress the need for precise definitions to avoid softening risk controls or eroding the ability of regulators to intervene when broader financial crime or consumer protection concerns arise. The rule will likely require ongoing refinement to address newly emergent business models and evolving threats, including opaque financial arrangements or non-traditional counterparties that still carry risk. The Fed’s engagement with industry stakeholders, as evidenced by the 60-day comment period, will be a critical litmus test for how quickly and effectively a clearer, more stable regime can take shape.

What to watch next

- Public comments: The 60-day window opens with the formal proposal and should yield a spectrum of views from banks, crypto firms, consumer groups, and policymakers.

- Final rule release: The Fed will publish the final text, outlining definitions, enforcement mechanisms, and transition timelines for banks to align with the new standard.

- Banking industry response: Expect filings, memos, and industry white papers detailing how lenders foresee applying the rule in practice and where they foresee friction or ambiguities.

- Regulatory coordination: Observers will look for alignment with other regulators’ approaches to reputational risk and how the rule interacts with anti-money-laundering and sanctions regimes.

Sources & verification

- Federal Reserve press release: June 23, 2025, announcing changes to supervision focused away from reputation risk

- Federal Reserve press release: February 23, 2026, inviting public comment on turning the approach into law

- Senator Cynthia Lummis (X) post praising the move: https://x.com/senlummis/status/2026060712305365065

- Galaxy Digital Alex Thorn (X) post commenting on the rollback: https://x.com/intangiblecoins/status/2026069012124164150

- Cointelegraph article: Operation Chokepoint crypto banking restrictions

Market reaction and key details

The Fed’s initiative to codify reputation-risk exclusion from supervisory judgment underscores a broader shift toward risk-based banking decisions that foreground financial metrics over reputational considerations. The formal rulemaking process, including a 60-day comment window, invites a wide spectrum of perspectives, ensuring that the final framework balances financial stability with the industry’s push for more straightforward access to banking services. Industry observers note that the policy’s success will hinge on how clearly the Fed defines “reputation risk” and how it handles edge cases where reputational concerns intersect with legitimate risk signals. The conversation also weaves in the historical debate around “Operation Chokepoint 2.0,” a label used by crypto insiders to describe perceived regulatory and banking pressures on crypto firms, which the current proposals seek to reverse or at least diminish in influence over supervisory outcomes. The official narrative aligns with a broader push to position the United States as a competitive, innovation-friendly environment for digital assets while maintaining guardrails that deter illicit activity.

The momentum behind the policy has drawn attention from lawmakers and industry figures who argue it could restore a more predictable banking environment for crypto companies. The ongoing public debate touches on questions of how much regulatory discretion should be exercised based on non-financial considerations and how transparent the decision-making process should be for banks that service digital-asset businesses. With the 60-day window now open, observers will be watching not only for the rule’s final form but also for the evidence of consensus around where the balance should lie between risk control and access to essential banking services.

Ultimately, the Fed’s proposed rule is part of a larger narrative about how the United States intends to steward innovation in the digital asset space while preserving the integrity of the financial system. If the rule stands up to scrutiny and gains broad support, it could reduce the volatility that arises when firms lose access to banking for reasons tied more to reputation than to tangible financial risk. For participants across the industry—from fintech startups to established crypto exchanges—the development represents a potential turning point in the governance of banking relationships and the speed at which the U.S. can keep pace with global peers in the digital economy.

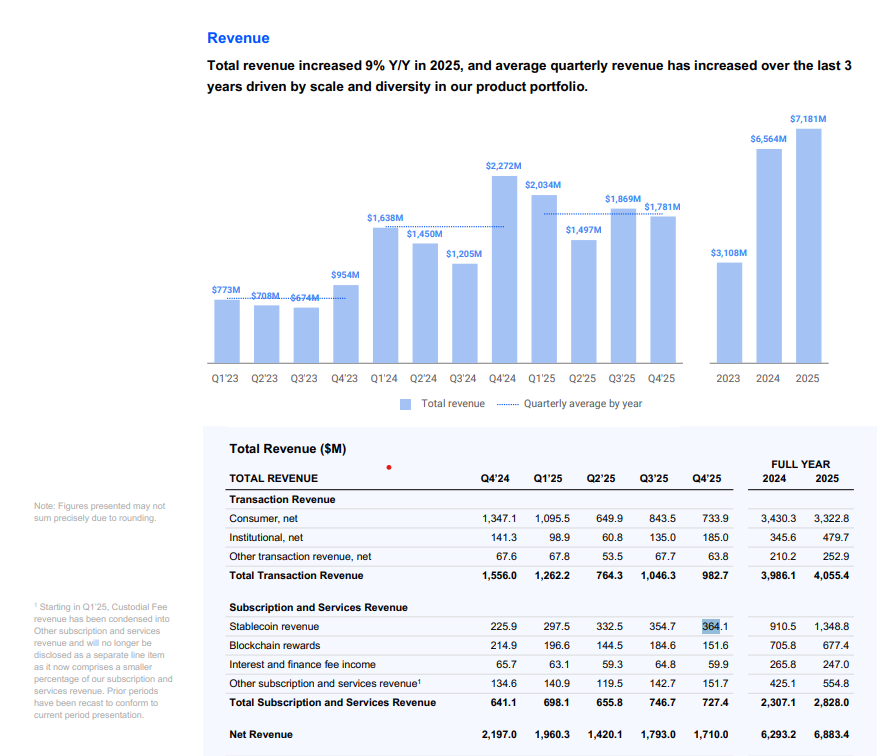

Bloomberg Intelligence estimates that Coinbase’s stablecoin revenue, which is largely tied to its USDC revenue share with Circle and already about 19% of total revenue in 2025, could grow by two to seven times if USDC adoption in payments accelerates.

Despite reporting a net loss of $667 million in the fourth quarter of 2025, according to Coinbase’s Q4 2025 shareholder letter, the company netted around $1.35 billion in stablecoin revenue last year.

That figure was up from $911 million in 2024, with $364 million in stablecoin revenue in Q4 2025 alone, as interest income on USDC (USDC) balances became a high-margin line for the exchange compared to volatile trading fees.

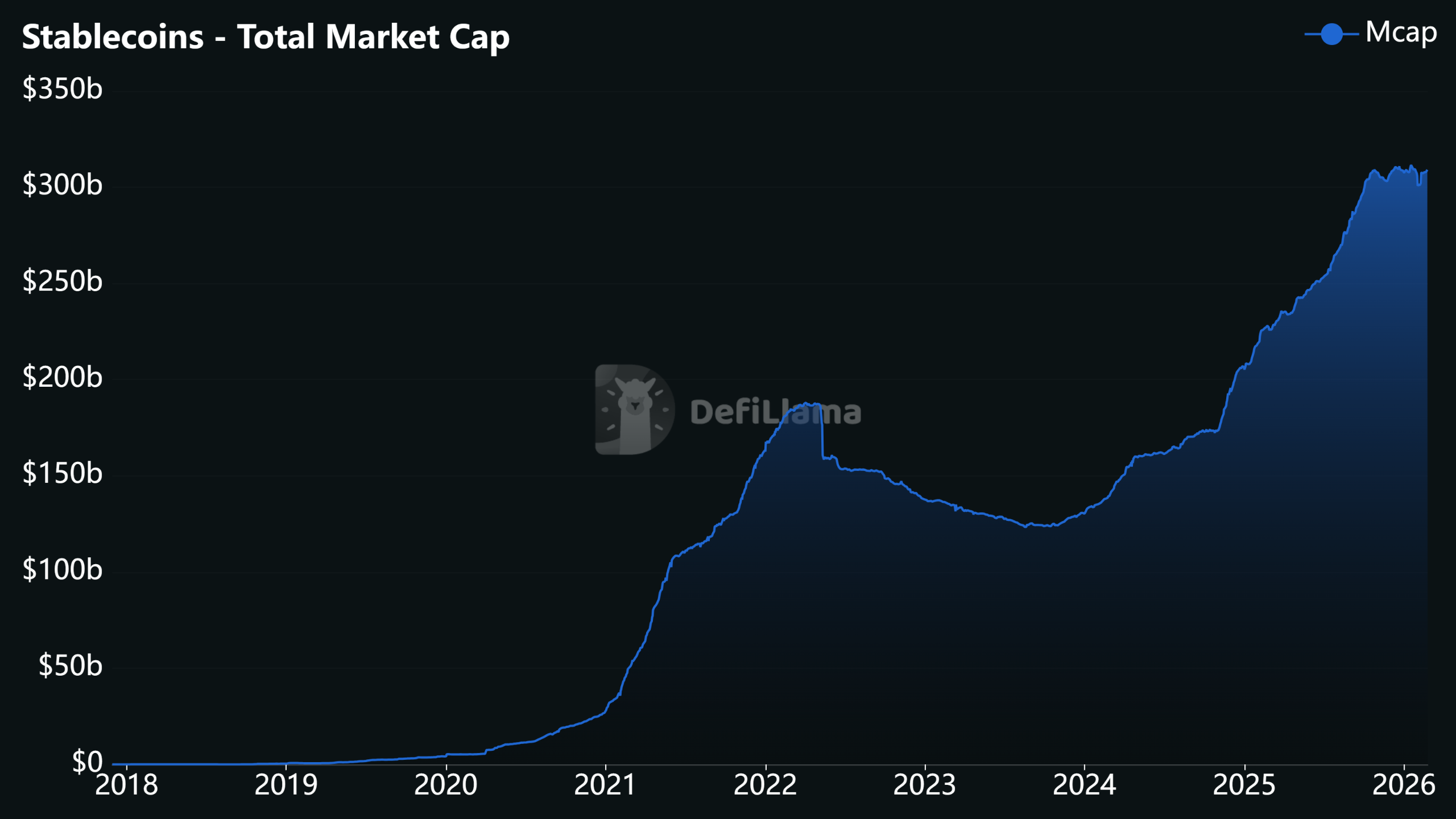

Stablecoins themselves have gone mainstream in usage terms. The total stablecoin transaction volume hit a record $33 trillion in 2025, with USDC accounting for about $18.3 trillion of that, ahead of Tether’s USDt (USDT) by transaction value, even though Tether still leads on market cap.

Politics of stablecoin yield

That growth is exactly why the politics around stablecoin yield have become so fraught. The Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, signed by US President Donald Trump in July 2025, created a federal regime for payment stablecoins and explicitly bars issuers from paying interest or yield to holders.

Related: Who gets the yield? CLARITY Act becomes fight over onchain dollars

That provision is backed by the banking lobby because yield‑bearing stablecoins could siphon deposits from the traditional system.

Banks and their allies now want to go further in the Senate’s Digital Asset Market Clarity (CLARITY) Act of 2025 negotiations by closing what they see as a loophole that still allows non‑issuer affiliates, such as exchanges like Coinbase, to pass some of the interest on reserves back to customers as “rewards.”

Draft Senate language of the market structure bill could extend the yield ban and prevent Coinbase from offering any rewards tied to stablecoin balances.

In January, Coinbase withdrew support for the bill after objecting to provisions that would restrict its ability to offer stablecoin rewards to customers.

Coinbase earns a share of interest income from USDC reserves through its partnership with Circle, and the companies split that revenue based on USDC distribution.

Ironically, Armstrong told investors that if Congress bans rewards, the company would simply keep more of the Circle revenue share, making the stablecoin line more profitable, despite users losing out on yield.

Cointelegraph reached out to Coinbase but had not received a response by publication time.

What’s next for CLARITY?

The CLARITY Act, which bundles a Commodity Futures Trading Commission (CFTC) and Securities and Exchange Commission (SEC) split with tougher language on third‑party stablecoin yield, is currently working its way through the Senate.

Senator Bernie Moreno has said he expected the CLARITY Act to clear Congress as soon as April.

With stablecoins already accounting for nearly a fifth of Coinbase’s revenue and onchain dollar volumes hitting record highs, the eventual shape of those yield rules may matter more for Coinbase’s business model than the next crypto price cycle.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

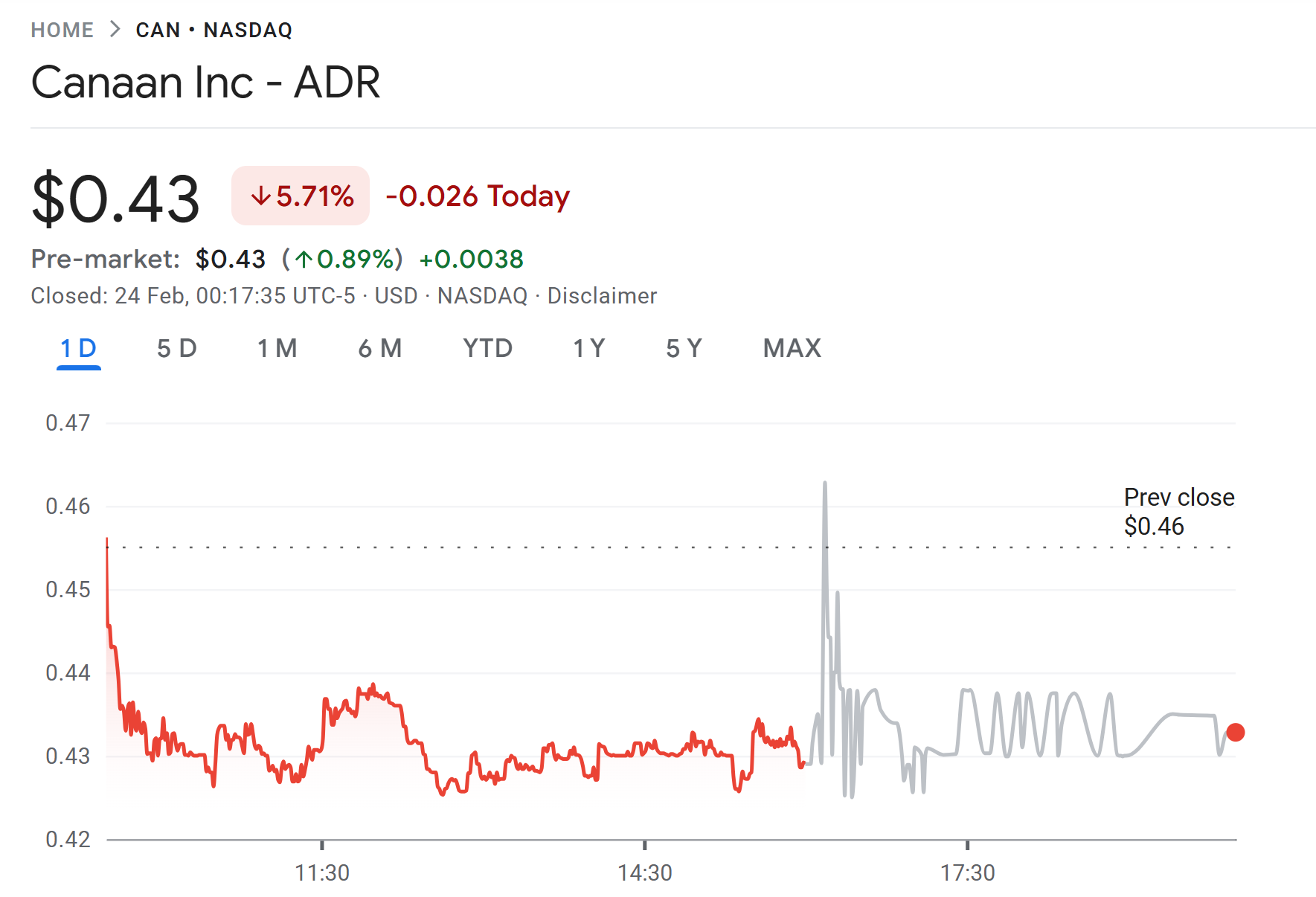

Bitcoin mining hardware maker Canaan has purchased Cipher Mining’s 49% interest in a trio of Texas mining projects for $39.75 million, expanding its mining interests.

The transaction covers joint venture entities Alborz LLC, Bear LLC and Chief Mountain LLC, together known as the “ABC Projects,” according to a Monday announcement. After the deal, Canaan holds a 49% stake while partner WindHQ, a renewable energy infrastructure company, retains 51%.

“By increasing our exposure to high-quality, low-cost operational power assets in Texas, we are aligning our proprietary technology with critical infrastructure to drive long-term efficiency and scale,” said Nangeng Zhang, chairman and chief executive officer of Canaan.

The three facilities are already operational, with a combined 120 megawatts of power capacity and about 4.4 exahashes per second (EH/s) of hashrate. Canaan also acquired 6,840 Avalon A15Pro mining rigs from Cipher. Those machines were previously deployed at Cipher’s Black Pearl location, which is being converted into an artificial intelligence and high-performance computing (AI-HPC) data center.

Related: Bitcoin mining difficulty rebounds 15% as US miners recover from winter outages

Canaan funds deal with $40 million share issuance

The purchase was financed through shares. Canaan issued 806,439,900 Class A shares, equal to 53,762,660 American Depositary Shares (ADS), priced at $0.7394 per ADS and subject to a six-month lockup.

According to the announcement, the Texas sites benefit from electricity costs below $0.03 per kilowatt-hour and include wind-powered generation and grid demand-response capabilities within the ERCOT power market. “ABC Projects feature industry-leading power pricing and offer a strong foundation for growth,” Zhang added.

Canaan reported a strong fourth quarter of 2025, with revenue rising 121.1% year-on-year to $196.3 million, as hardware shipments and mining output improved. Bitcoin (BTC) mining revenue climbed 98.5% to $30.4 million, increasing its treasury to 1,750 BTC. It shipped a record 14.6 EH/s of computing power and expanded installed hashrate to 9.91 EH/s, supported by a large institutional order in the United States.

Related: Bitcoin miners chase 30 GW AI capacity to offset hashprice pressure

Bitcoin miners turn to AI as margins tighten

Bitcoin mining companies are increasingly branching into AI and cloud computing as profitability pressures mount. Last week, MARA Holdings acquired a 64% stake in French infrastructure company Exaion, giving the company a foothold in AI services.

The move came amid a broader industry trend. Companies including Hive, Hut 8, TeraWulf and Iren are converting mining facilities and power capacity into data-center operations, and some players such as CoreWeave have already transitioned fully into AI infrastructure.

Canaan also said the new acquisitions align with its initiative to stabilize power grids amid rising data center demand.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

Crypto World

RedotPay stablecoin payments firm said to consider $1 billion IPO in New York: Bloomberg

RedotPay, a Hong Kong-based stablecoin payments upstart, plans to raise more than $1 billion in a U.S. initial public offering (IPO) that could value it at over $4 billion.

Sources close to the matter told Bloomberg that the company, which achieved unicorn status in September last year, has tapped banking heavyweights such as JPMorgan, Goldman Sachs and Jefferies for a potential New York listing as early as this year.

Details of the IPO, such as the exact size and timeline, are still fluid, and more banks could jump in.

RedotPay raised $194 million in 2025, capped by a Series B in December, and now claims more than 6 million registered users. Backers read like a Who’s Who of crypto venture capital: Accel, Pantera Capital and Blockchain Capital among others.

If it pulls off the IPO, it’d be one of the biggest from Asia’s stablecoin scene.

Stablecoins are digital tokens with values pegged to an external reference such as the U.S. dollar. These tokens are widely used in trading cryptocurrencies and to move capital across borders.

Hong Kong, like other advanced nations, has warmed up to these tokenized versions of fiat currencies and is ready to license its first stablecoin issuers next month.

Doctor Profit compared Saylor’s approach to the 2000 dot-com bubble, and added that buying blindly without strategic selling is a “reckless” trading approach.

Strategy has spent years aggressively buying Bitcoin, pitching the move as a long-term, high-conviction bet, but critics say that the approach has crossed from bold into reckless.

Popular analyst Doctor Profit, for one, drew parallels to the dot-com bubble, while warning that the firm risks repeating history amid today’s AI-fueled frenzy.

Blind Faith vs Market Timing

In a recent post on X, Doctor Profit stated that he repeatedly expressed his concerns with Strategy’s co-founder, Michael Saylor, that nonstop Bitcoin accumulation, financed and backed by issuing company shares, was “playing with fire.” According to the analyst, those warnings were dismissed and even mocked.

He pointed out that since then, Strategy’s share price has fallen by roughly 75% from its highs, while Bitcoin itself is down 50% from its peak. With Saylor’s reported average BTC entry around $76,000 and the asset trading near $63,000, the position sits roughly 17% below cost.

Doctor Profit also argued that, despite accumulating since 2020, the company has never realized meaningful profits or executed serious strategic selling. Meanwhile, its stock has suffered a substantial drawdown, exposing shareholders to extreme volatility with little relief.

Looking back at past cycles, Doctor Profit said Saylor’s experience during the 2000 dot-com collapse offers a warning. He explained that intense excitement surrounding AI today may be creating a similar late-cycle setup, increasing the chance of history repeating itself by 2026.

Rather than de-risking as these signals emerged, Doctor Profit claimed that the executive chairman doubled down, increasing exposure while ignoring red flags.

You may also like:

“I truly wish MSTR and Saylor the best, but I cannot understand how reckless this trading approach is in such a late-cycle environment. Markets reward discipline, not blind belief in Bitcoin. There is always time to buy and time to sell. I hope he will listen next time instead of mocking my warnings.”

The fresh concerns come against the backdrop of Strategy’s latest Bitcoin purchase, which is smaller than its past billion-dollar buys but consistent with its long-standing accumulation plan. The firm spent just under $40 million to acquire 592 BTC at an average price of $67,286, which pushed its total holdings to 717,722 BTC.

The purchase was funded through equity sales. Nearly 298,000 Class A shares were sold via the firm’s at-the-market program over the past week, according to an update cited by Walter Bloomberg. Strategy still has substantial capacity to raise more capital through future ATM sales, as $37.4 billion in securities remain available, including MSTR and STRK stock.

Billions at Risk

As Bitcoin’s price decline deepened, earlier warnings from Michael Burry and Zac Prince drew fresh attention to the fragility of BTC treasury business models. For instance, Burry recently said BTC’s drop increases the risk of broader stress across crypto and related financial markets. “The Big Short” investor had said that further downside could severely impact companies that accumulated Bitcoin at higher prices, potentially leaving firms like Strategy billions underwater and cut off from capital markets.

Former BlockFi CEO, Prince, also questioned the sustainability of BTC treasury models, saying they rely on financial engineering rather than core business fundamentals and may struggle to justify valuations without real operating revenue.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Hong Kong-based stablecoin payments company RedotPay is reportedly weighing a US initial public offering (IPO) that could raise more than $1 billion and value the company at over $4 billion.

The company is working with JPMorgan Chase, Goldman Sachs and Jefferies on a potential New York listing that may occur as early as this year, Bloomberg reported on Tuesday, citing people familiar with the matter. Terms remain under review and could change, while additional banks may join the underwriting group, per the report.

Founded in April 2023, RedotPay provides stablecoin-linked payment cards, multicurrency wallets and international payout services. According to its website, the company has 6 million users and handles about $10 billion in annualized payment volume.

RedotPay declined to comment on the matter.

Related: Binance stablecoin reserves have sunk 19% since November

RedotPay raised $194 million in 2025

The US IPO plans follow a year of fundraising for RedotPay, which raised a total of $194 million in 2025 across three rounds. In March, it closed a $40 million Series A funding round led by Lightspeed, with participation from HSG and Galaxy Ventures.

In September, the stablecoin payment company said it became a fintech unicorn after closing a $47 million strategic round that saw investment from Coinbase Ventures, alongside continued backing from Galaxy Ventures and Vertex Ventures and participation from an undisclosed global technology entrepreneur.

It later closed a $107 million Series B in December. The round was led by Goodwater Capital, with participation from Pantera Capital, Blockchain Capital and Circle Ventures, as well as continued support from HSG.

Related: Standard Chartered sticks to $2T stablecoin call but trims T-bill impact

Stablecoin sector attracts significant funding

Stablecoin-focused companies drew significant investment in 2025 as venture capital continued flowing into payment and infrastructure providers. In August, investors committed almost $100 million to the sector, including a $40 million Series B for Switzerland-based M0 led by Polychain Capital and Ribbit Capital, and a $58 million raise by US startup Rain to build tools enabling banks to issue regulated stablecoins.

Funding activity continued through the year. In October, Chicago-based Coinflow secured $25 million in a Series A led by Pantera Capital to expand cross-border settlement services, while CMT Digital later launched a $136 million fund with allocations for stablecoin startups, including Coinflow and Codex.

Big Questions: Is China hoarding gold so yuan becomes global reserve instead of USD?

As the AUD/USD chart shows, the Australian dollar posted strong performance in January and February. Since the start of the year, the “Aussie” has gained nearly 6% against the US dollar.

Among the bullish drivers:

→ The policy stance of the Reserve Bank of Australia (RBA), which raised its cash rate to 3.85% in February 2026, while many other central banks are considering rate cuts.

→ A resilient labour market. Australia’s unemployment rate remains at 4.1%, giving the RBA room to keep interest rates elevated.

→ Commodity markets. High prices for gold, iron ore and energy exports continue to support Australia’s trade balance.

However, an important CPI report is due tomorrow. Inflation data could inject additional volatility into the market and test the strength of the Australian dollar.

Technical Analysis of the AUD/USD Chart

In early January, we identified an ascending channel that remained valid through February 2026, as bulls managed to break above resistance line R. Note that:

→ The upper boundary of the channel acted as resistance (resulting in the formation of peaks A–B).

→ The median line served as support.

An important observation is that after forming peak B, the market quickly fell back below the level of peak A. This suggests insufficient buying pressure to sustain the advance.

At the same time, the recent candlestick with a long upper wick — a potential bull trap and a bearish signal — may indicate that the AUD/USD reaction to the CPI report could be negative.

In that case, a break below the channel’s median line cannot be ruled out, opening the way for a test of the psychological 0.7000 level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Canaan (EXCHANGE: CAN) has expanded its Texas footprint by snapping up Cipher Mining’s 49% stake in three existing mining operations, broadening its exposure to low-cost, scalable power assets and reinforcing its strategic tilt toward utility-scale mining. The deal covers Alborz LLC, Bear LLC, and Chief Mountain LLC—collectively known as the ABC Projects—and elevates Canaan’s stake to 49% while WindHQ maintains a 51% majority. The trio of facilities already operates with about 120 megawatts of grid-supplied power and delivers roughly 4.4 exahashes per second (EH/s) of Bitcoin (CRYPTO: BTC) mining capacity. In addition to the equity transfer, Canaan acquired 6,840 Avalon A15Pro mining rigs from Cipher, which had been deployed at Cipher’s Black Pearl site, earmarked for conversion into an AI-HPC data center. This move aligns with a broader industry trend of miners diversifying into AI and cloud-based services as margins tighten.

The deal was financed through a significant equity issuance. Canaan issued 806,439,900 Class A shares, equivalent to 53,762,660 American Depositary Shares (ADS), priced at $0.7394 per ADS, with a six-month lockup period. The consideration signals a deliberate capital-structure adjustment to support the expansion of the Texas sites and the ongoing transition of Cipher’s Black Pearl asset. According to the filing, the Texas facilities benefit from electricity costs below 3 cents per kilowatt-hour and include wind-powered generation plus grid-demand response within the ERCOT market. The price tag attached to the acquisition reflects both the tangible hardware upgrade and the strategic value of anchoring a low-cost power profile in a state known for competitive energy economics.

Executive Chairman and CEO Nangeng Zhang framed the move as a step to “align proprietary technology with critical infrastructure to drive long-term efficiency and scale.” The strategic emphasis is clear: gain control of high-quality, affordable power assets that can sustain increased mining activity while positioning the business to capitalize on future opportunities in AI-enabled data center services. The ABC Projects bring with them a proven operational footprint in Texas, a state that remains central to miners’ growth plans given its energy mix, regulatory environment, and capacity constraints elsewhere. While Cipher’s stake transfers to Canaan, WindHQ’s stake remains, ensuring continued governance in the ventures’ direction.

Beyond the specific transaction, Canaan’s financials for the fourth quarter of 2025 augmented the narrative of a company navigating a higher-capacity, higher-visibility mining cycle. The firm reported a 121.1% year-over-year rise in revenue to $196.3 million as hardware shipments and mining activity improved. Bitcoin (BTC) mining revenue reached $30.4 million, contributing to a treasury that expanded to 1,750 BTC. The company shipped a record 14.6 EH/s of computing power during the quarter, lifting installed hashrate to 9.91 EH/s—an uptick buoyed by a large institutional order in the United States. The results underscore a sector that remains sensitive to hashprice dynamics but is able to leverage scale, efficiency improvements, and strategic site selection to sustain growth during a period of consolidation.

Canaan’s foray into AI and broader industry dynamics

As margins compress, several Bitcoin mining firms have started to pivot toward AI, cloud services, and data-center operations. The market has seen a wave of moves where traditional mining capacity is repurposed or expanded to serve AI workloads and HPC tasks. For instance, the company MARA Holdings recently took a 64% stake in Exaion, a move that signaled a broader appetite for AI-enabled infrastructure within the ecosystem. Other players, including Hive, Hut 8, TeraWulf, and Iren, have similarly explored converting mining power into AI-ready capacity, with CoreWeave having already transitioned to a broader AI-infrastructure model. These shifts reflect a strategic emphasis on building diversified, resilient revenue streams alongside traditional block rewards.

In this environment, Canaan’s acquisition strategy and the associated asset mix—low-cost Texas power, wind generation, and ERCOT grid-demand responsiveness—position the company to weather price volatility while scaling operations. The combination of tangible capacity (120 MW, 4.4 EH/s) and tangible assets (6,840 Avalon A15Pro rigs) provides a foundation for longer-term efficiency gains as the AI-HPC data-center conversion progresses at the Black Pearl site and potentially beyond. The emphasis on stabilizing power grids amid rising data-center demand also speaks to a broader industry concern: how miners can contribute to, and benefit from, grid reliability and demand-response programs while maintaining competitive economics.

As the sector evolves, investors are watching how these capital-intensive expansions translate into sustainable cash flow, given the cyclical nature of crypto markets and the sensitivity of mining economics to electricity prices, hardware costs, and BTC price movements. The Texas projects’ economics—anchored by sub-3-cent per kWh power and wind-assisted generation—could provide a durable edge if energy costs remain favorable and the broader demand for AI infrastructure accelerates. In this context, Canaan’s blend of mining capacity with AI-ready hardware represents a notable example of how traditional crypto mining players are recalibrating to operate as diversified data-center operators.

What to watch next

- Close of the Cipher Mining stake transfer and the resulting governance arrangements within the ABC Projects.

- Deployment and operational ramp of the 6,840 Avalon A15Pro rigs within the ABC Projects and the Black Pearl AI-HPC conversion timeline.

- Updates on electricity pricing, ERCOT capacity commitments, and any new wind- or grid-support arrangements affecting Texas operations.

- Canaan’s ongoing quarterly results and how the ABC Projects contribute to revenue, hash rate, and treasury growth going into 2026.

Sources & verification

- Press release: Canaan Inc. acquires Cipher Mining’s interest in multiple operational mining projects totaling 4.4 EH/s in West Texas (PR Newswire).

- Financial performance notes referencing Q4 2025 results, including revenue, BTC mining revenue, and hash rate milestones (as reported and summarized by industry coverage).

- Details of the ABC Projects’ capacity (120 MW) and hash rate (4.4 EH/s) as described in the acquisition announcement.

- Notes on the financing structure, including the share issuance and lockup terms described in the press materials.

Strategic expansion in Texas: Canaan’s ABC projects and AI ambitions

The acquisition of Cipher Mining’s minority stake in the ABC Projects marks a deliberate push by Canaan to anchor its growth in a high-visibility, cost-efficient energy corridor. By taking 49% of the three facilities and leaving WindHQ with 51%, the company gains operational influence while preserving a clear minority stakeholder structure that can support scale without over-leveraging the venture. The combined 120 MW of capacity and 4.4 EH/s of hashrate position the ABC Projects as a meaningful contributor to Canaan’s overall production capacity, particularly as the firm expands use cases for its hardware in AI and HPC environments.

The 6,840 Avalon A15Pro rigs acquired from Cipher bring additional compute power into the fold, with deployment tied to Cipher’s Black Pearl site’s AI-HPC conversion. This move exemplifies a broader miner-led shift from pure crypto mining toward diversified data-center capabilities that can power AI workloads, cloud services, and other compute-intensive tasks. The rationale is grounded in the long-run economics of power efficiency and load diversification, where operators can monetize flexible power usage through grid-demand-response programs while maintaining a robust hardware base to support both mining and AI tasks.

From a market perspective, the deal underscores how miners are reinterpreting their assets in a world where energy costs and hashprice fluctuations can materially affect profitability. Texas remains an attractive destination not only for its competitive electricity rates but also for the regulatory and market infrastructure that supports demand-response programs. The ABC Projects’ wind-powered generation and grid integration through ERCOT are notable features that can help stabilize operating costs even as the broader crypto ecosystem faces cyclical pressures. For investors and builders, the move signals a continued emphasis on scalable, asset-light expansions that couple hardware with strategic power arrangements and diversified data-center economics.

Terraform Labs’ court-appointed bankruptcy administrator has filed a lawsuit against market maker Jane Street for allegedly using non-public information to profit from the 2022 collapse of the Terra ecosystem.

Summary

- Terraform’s bankruptcy administrator has sued Jane Street, alleging the trading firm used material non-public information to front-run trades during the May 2022 collapse.

- The complaint names co-founder Robert Granieri and traders Bryce Pratt and Michael Huang.

- A Jane Street spokesperson has denied all allegations.

The lawsuit was filed on Monday and accused Jane Street insiders, including its co-founder Robert Granieri, and employees Bryce Pratt and Michael Huang of “misappropriating confidential information and manipulating market prices.”

According to the heavily redacted complaint, Jane Street front ran Terraform’s liquidity moves around the Curve 3pool withdrawal and used the information it acquired to unwind hundreds of millions of dollars in UST exposure “that hastened the collapse of Terraform.”

The suit claims that Jane Street and Terraform first connected for over-the-counter trading in 2018, but that trading “did not take off until February 2022” when Jane Street deployed Bryce Pratt, a former Terraform intern, to establish lines of communication with his former colleagues at Terraform.

Pratt allegedly helped set up those channels due to his history as a former Terraform intern, which allowed him to “seamlessly pass information from Terraform to Jane Street.”

“Given Jane Street’s interest in cryptocurrency, Pratt leveraged the relationships he had developed at Terraform to feed material non-public information to Jane Street’s crypto desk,” the complaint said.

“Jane Street abused market relationships to rig the market in its favor during one of the most consequential events in crypto history,” Terraform’s court-appointed administrator, Todd Snyder, said in a statement to the Wall Street Journal.

The lawsuit seeks damages and an order requiring Jane Street to disgorge the profits it allegedly made through insider trading and market manipulation, along with interest, and calls for a jury trial.

In response, a Jane Street spokesperson has denied all allegations and told WSJ that the suit was a “desperate” attempt to “extract money,” and the firm will defend against these “baseless, opportunistic claims.”

“[..] It is well-established that the losses suffered by Terra and Luna holders were the result of a multibillion-dollar fraud perpetrated by the management of Terraform Labs,” the spokesperson said.

Terraform collapsed in May 2022 after its algorithmic stablecoin TerraUSD lost its dollar peg, which resulted in one of the crypto industry’s largest meltdowns as roughly $40 billion vanished from the market. Subsequently, Terraform filed for bankruptcy in 2024, while co-founder Do Kwon pleaded guilty to fraud charges and was sentenced to 15 years in prison.

The bankruptcy administrator also launched a lawsuit against Jump Trading in December and claims the firm entered into secret agreements with Kwon.

XRP price continues to trade under pressure as a persistent downtrend shapes short-term momentum. The token has struggled to break above descending resistance since the beginning of the month. This prolonged weakness has created uncertainty across the broader crypto market.

Despite the downturn, some investors view current levels as strategic entry points, forming the base for a potential recovery.

XRP Bottom In Sight

On-chain data shows XRP’s realized price now sits above the current market price. This metric indicates that the average holder is at a loss. When the market price falls below the realized price, assets are often considered undervalued from a historical perspective, marking a potential bottom.

Past cycles reveal that XRP rarely remains in this zone for extended periods. Similar conditions have preceded swift price rebounds. While no outcome is guaranteed, historical patterns suggest that undervaluation phases often attract accumulation and renewed buying interest.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

How Are XRP Investors Acting?

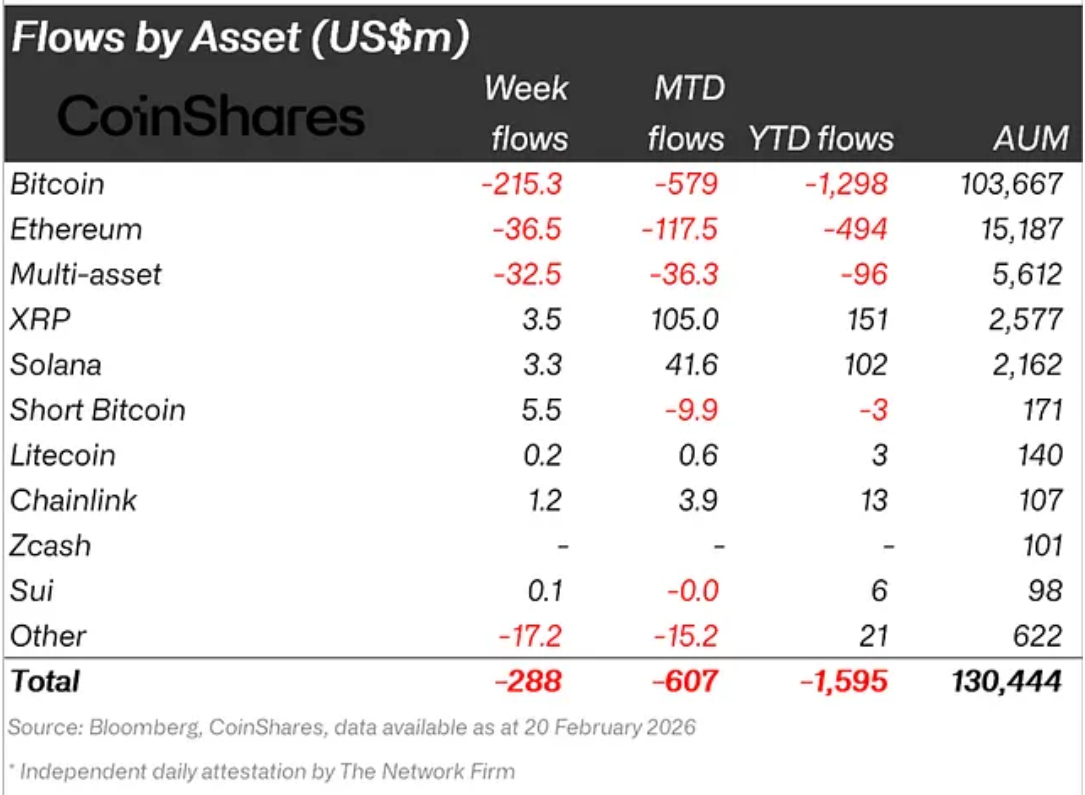

Institutional investors remain notably active despite broader market caution. For the week ending February 20, institutions added $3.5 million worth of XRP exposure. This brought month-to-date inflows to $105 million, a figure unmatched by Bitcoin or Ethereum, which both recorded net outflows.

Sustained institutional demand reflects strategic positioning rather than speculative trading. Professional investors often deploy capital during periods of weakness. Continued inflows may provide liquidity support and strengthen the structural foundation for XRP price stabilization.

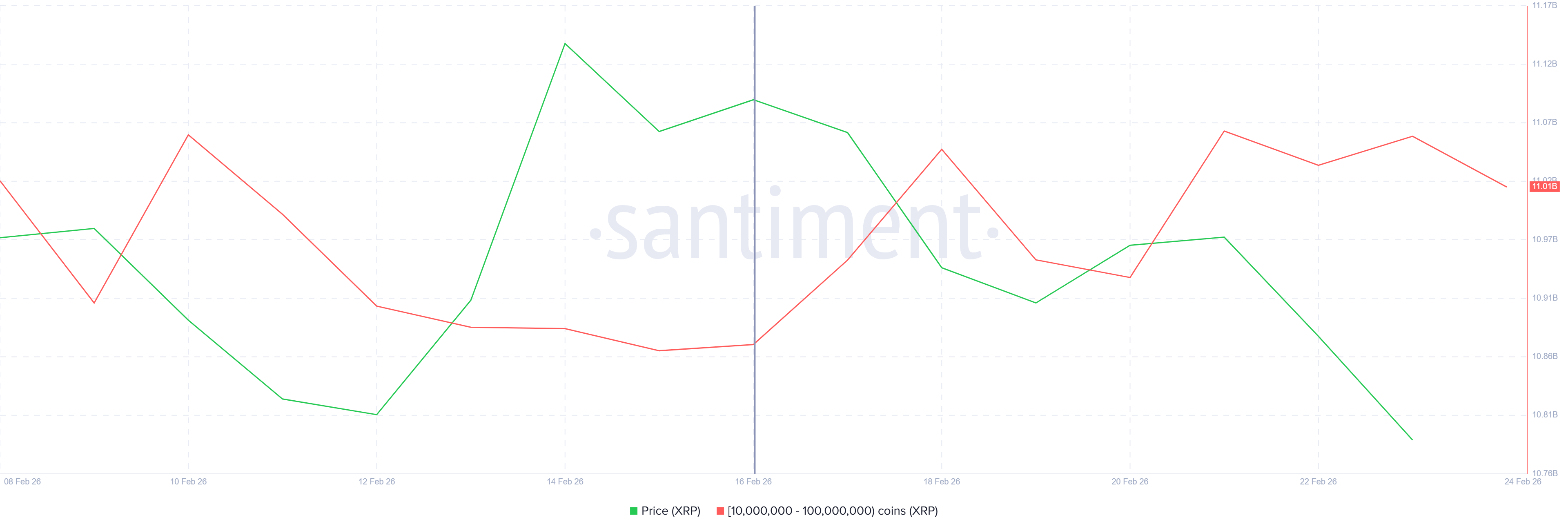

Large XRP holders also appear confident in the asset’s long-term outlook. Addresses holding between 10 million and 100 million XRP accumulated more than 170 million tokens over the past week. This buying activity occurred during a 9% price decline.

Accumulation during falling prices signals conviction among influential wallet holders. While the increase is not historically extreme, timing remains significant. Coordinated accumulation from whales and institutions may reduce circulating supply pressure and contribute to eventual upward momentum.

XRP Price Levels To Watch

XRP price is trading at $1.32 at the time of writing, remaining below a descending trendline established earlier this month. The asset continues to face technical resistance along this barrier. Without a clear improvement in broader market sentiment, XRP may struggle to break higher in the near term.

After losing support at $1.36, XRP now looks toward $1.28 as the next key level. Macro conditions worsened following US President Donald Trump’s 15% global tariff hike. Risk-off sentiment may weigh on digital assets. Continued pressure could push XRP toward $1.28 or even $1.21.

However, stabilization in global markets could shift momentum. Ongoing whale accumulation and institutional inflows may support recovery attempts. A breakout above the descending trendline would signal structural improvement. If XRP clears $1.47 resistance, the bearish thesis would be invalidated, and bullish momentum could reemerge.

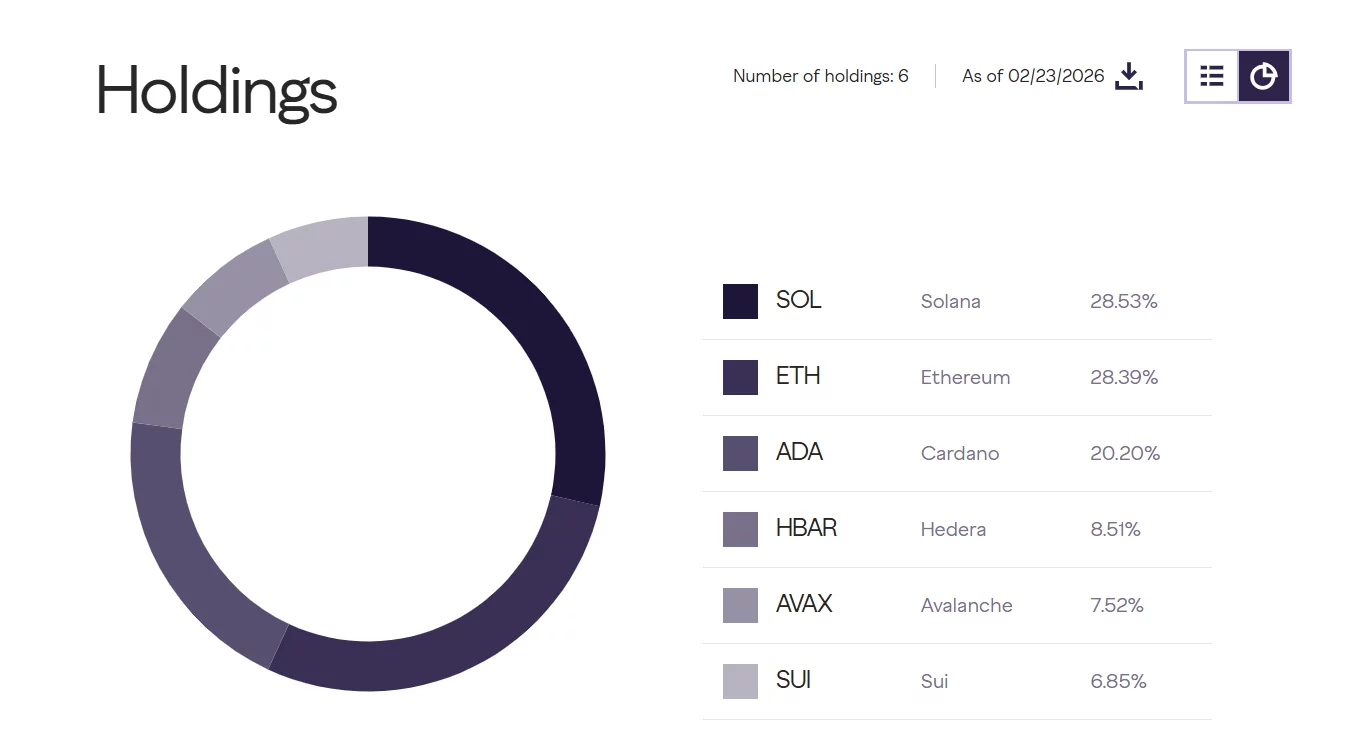

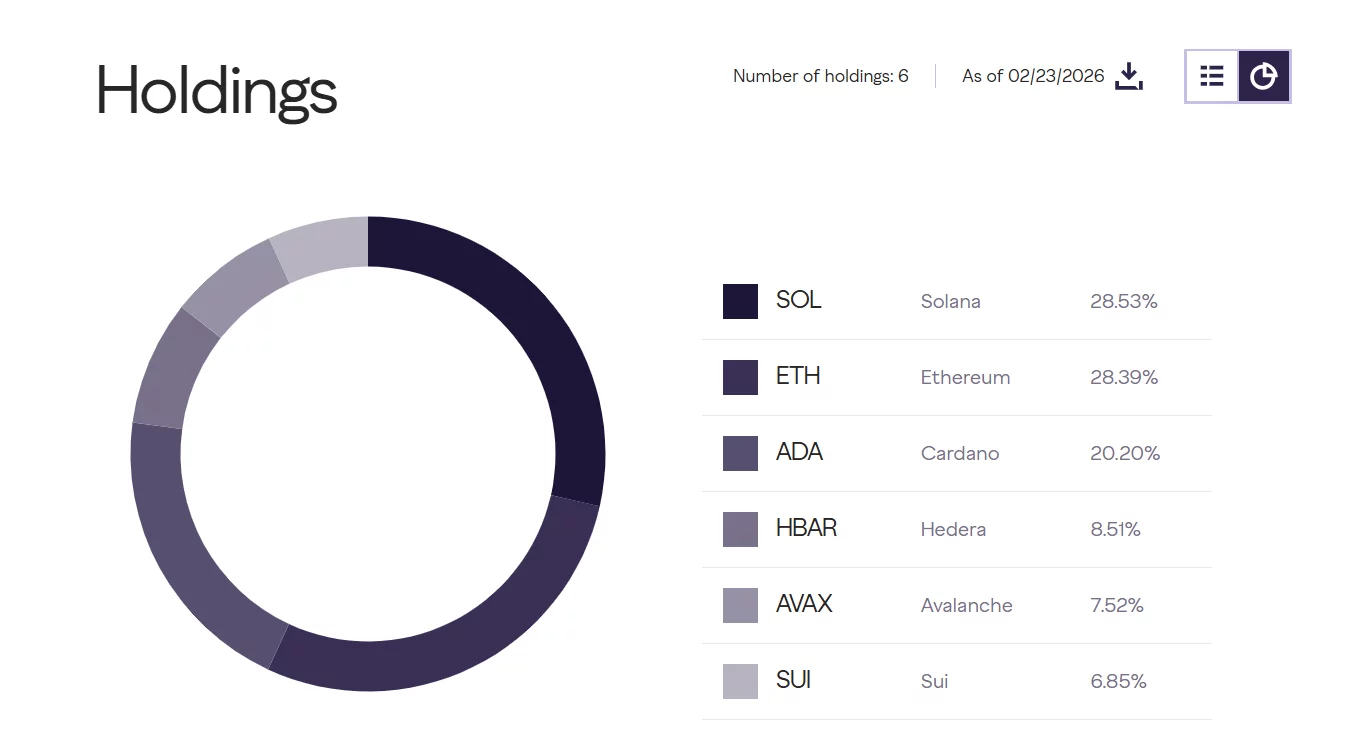

Digital asset manager Grayscale Investments has increased its allocation to Cardano in its diversified crypto holdings, signalling institutional interest in the smart contract platform even as broader market sentiment weakens.

Summary

- Grayscale Investments boosted its allocation to Cardano to about 20.2%, making ADA its third-largest holding.

- The move comes as Bitcoin fell below $65,000 following new tariff measures announced by Donald Trump, dragging the broader crypto market lower.

- Technically, ADA is trading near $0.257, with resistance at $0.30–$0.31 and key support at $0.24, while momentum indicators remain in bearish territory.

According to the latest portfolio breakdown, Cardano (ADA) now accounts for roughly 20.20% of the fund’s holdings, making it the third-largest allocation behind Solana (28.53%) and Ethereum (28.39%).

The adjustment highlights Grayscale’s growing confidence in Cardano’s long-term fundamentals at a time when digital assets are facing macro-driven volatility.

The rebalancing comes amid sharp turbulence across crypto markets. Bitcoin recently plunged below the $65,000 mark following fresh tariff measures announced by Donald Trump, triggering a broad risk-off move.

The sell-off spilled into altcoins, with Ethereum, Solana and Cardano all trading lower on the week.

ADA price analysis

Despite the institutional tailwind, ADA’s technical structure remains fragile. On the daily chart (ADA/USDT), the token is trading around $0.257, down nearly 2% on the session.

Price action shows a clear downtrend from January highs near $0.42, followed by a series of lower highs and lower lows into February.

After a sharp sell-off in early February that pushed ADA toward the $0.23–$0.24 zone, bulls managed a modest rebound toward the $0.30 level. However, that recovery stalled, establishing $0.30–$0.31 as immediate resistance. A sustained break above that zone would be needed to shift short-term momentum.

On the downside, $0.24 remains key support, with stronger structural support seen near $0.22, the recent swing low. A decisive break below $0.24 could open the door to a retest of that lower range.

Momentum indicators remain cautious. The Awesome Oscillator is still in negative territory, though the histogram shows fading bearish momentum as green bars gradually build. Meanwhile, the Balance of Power reading sits below zero, suggesting sellers retain near-term control.

While Grayscale’s increased allocation underscores long-term institutional conviction, ADA’s short-term trajectory will likely depend on whether broader market sentiment stabilizes following Bitcoin’s tariff-driven drop.

Man raped people with dementia at care home and had indecent images of children

Coinbase’s USDC Revenue Could Grow Seven Fold: Bloomberg

Hilary Duff Remembers Lizzie McGuire Co-Star Robert Carradine

-

Crypto World7 days ago

Crypto World7 days agoCan XRP Price Successfully Register a 33% Breakout Past $2?

-

Video4 days ago

Video4 days agoXRP News: XRP Just Entered a New Phase (Almost Nobody Noticed)

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Boden – Corporette.com

-

Politics2 days ago

Politics2 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Sports15 hours ago

Sports15 hours agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics16 hours ago

Politics16 hours agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business6 days ago

Business6 days agoInfosys Limited (INFY) Discusses Tech Transitions and the Unique Aspects of the AI Era Transcript

-

Entertainment6 days ago

Entertainment6 days agoKunal Nayyar’s Secret Acts Of Kindness Sparks Online Discussion

-

Tech6 days ago

Tech6 days agoRetro Rover: LT6502 Laptop Packs 8-Bit Power On The Go

-

Sports5 days ago

Sports5 days agoClearing the boundary, crossing into history: J&K end 67-year wait, enter maiden Ranji Trophy final | Cricket News

-

Business2 days ago

Business2 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business2 days ago

Business2 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Entertainment5 days ago

Entertainment5 days agoDolores Catania Blasts Rob Rausch For Turning On ‘Housewives’ On ‘Traitors’

-

Crypto World2 hours ago

Crypto World2 hours agoXRP price enters “dead zone” as Binance leverage hits lows

-

NewsBeat23 hours ago

NewsBeat23 hours ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Business6 days ago

Business6 days agoTesla avoids California suspension after ending ‘autopilot’ marketing

-

Tech2 days ago

Tech2 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat2 days ago

NewsBeat2 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics2 days ago

Politics2 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Crypto World6 days ago

Crypto World6 days agoWLFI Crypto Surges Toward $0.12 as Whale Buys $2.75M Before Trump-Linked Forum