Crypto World

Federal Court Shuts Down Custodia Bank’s Master-Account Bid

A U.S. federal appeals court has closed the book on Custodia Bank’s bid for direct access to the Federal Reserve’s master-account program, delivering a setback after years of legal maneuvering. In a 7-3 ruling, the U.S. Court of Appeals for the Tenth Circuit declined to rehear the case, leaving intact the Fed’s long-standing discretion over who receives master accounts and access to the central bank’s payment rails. The decision arrives as crypto firms continue to seek direct lines to Fed services, while other players in the sector push for broader access and clearer regulatory pathways.

Key takeaways

- The Tenth Circuit rejected Custodia Bank’s final challenge in a 7-3 vote, effectively ending the bank’s bid for a Fed master account.

- Custodia originally applied in October 2020; after initial Fed rejection, it argued that the Monetary Control Act entitles state-chartered banks to Fed services, including a master account.

- Multiple courts have upheld the Fed’s discretion in granting master accounts, reinforcing the central bank’s gatekeeping role in access to payment rails.

- Kraken became the first crypto platform to receive a master account from the Federal Reserve Bank of Kansas City on March 4, tying it to Fedwire payments, albeit with a narrower set of services than a traditional bank.

- Disagreeing with the majority, Judge Tymkovich warned that a master account is “indispensable” for a bank’s operations and suggested denial could be viewed as a prohibitive outcome for a crypto-focused institution.

- The case underscores ongoing regulatory debate about “skinny” or limited master accounts for crypto firms, signaling a cautious but evolving approach to central-bank access.

Market context: The ruling lands amid broader regulatory discussions about how crypto-native firms should access traditional financial rails and liquidity. As more players seek direct Fed access to improve settlement efficiency and risk management, regulators have signaled openness to narrower, crypto-specific arrangements, while maintaining the Fed’s discretionary authority over master accounts.

Why it matters

The decision reinforces a foundational policy stance: the Federal Reserve controls who earns entry to its payment system through master accounts. For Custodia, the outcome closes a five-year pursuit that began with ambitions to settle digital-asset transactions with direct Fed support, reducing the likelihood of a direct route around traditional correspondent banking relationships. The ruling clarifies that the Fed’s authority to grant or withhold master accounts is not easily trumped by statutory arguments and that courts are unlikely to compel the Fed to provide access in the absence of a clearly defined statutory mandate.

Yet the same period has also seen notable progress elsewhere. Kraken, a prominent crypto exchange, secured a master account from the Fed’s regional arm in Kansas City, marking a pivotal milestone for the sector’s integration with the U.S. central bank’s system. This development demonstrates that the Fed is willing to grant access, albeit selectively, to entities that can demonstrate robustness, compliance, and operational readiness to connect to Fedwire payments. The distinction between “full” access and the more limited services available to nontraditional banks highlights the evolving nature of central-bank engagement with digital-asset firms.

While Custodia’s setback narrows the path for state-chartered banks seeking direct Fed access, the broader ecosystem remains engaged in a pragmatic dialogue about what accommodations crypto firms should receive. Proponents of increased access argue that direct ties to the Fed could reduce settlement risk and improve liquidity management in a sector characterized by rapid custody and settlement needs. Opponents caution against broadening eligibility without stringent risk controls and robust compliance frameworks. The tension mirrors larger regulatory dynamics as policymakers weigh consumer protection, financial stability, and innovation in parallel tracks.

The court’s opinion also underscores a practical reality: the Fed’s discretion has persisted through multiple adjudications. Although some judges have criticized the Fed’s stance, the majority’s analysis emphasizes that, absent a legislative change, master accounts remain a matter of administrative choice rather than automatic entitlement. In this sense, Custodia’s experience serves as a cautionary tale for other applicants that seek to accelerate entry into federal settlement rails without meeting the precise criteria the Fed applies in evaluating risk, governance, and operational readiness.

In the same thread, commentary around “skinny” master accounts—limited types of accounts designed to offer essential access without granting the full suite of services reserved for traditional banks—continues to gain attention. Advocates contend that even a pared-down pathway could substantially reduce the frictions crypto firms encounter when scaling and integrating with regulated financial infrastructure. Critics, however, argue that the integrity of the payment system requires careful calibration of who can participate and under what conditions. The recent disclosures, including Kraken’s march toward Fed-linked settlement capabilities, illustrate a cautious but tangible shift toward more inclusive mechanisms that balance safety with innovation.

What to watch next

- Regulators and the Fed may continue refining criteria for “skinny” master accounts and similar arrangements for crypto firms.

- Other applicants could reassess their strategies in light of the Custodia decision, potentially pursuing alternative means of direct Fed access or partnerships with traditional banks.

- Ongoing regulatory discussions and potential policy guidance could shape how future master-account decisions are communicated and implemented.

- Industry observers will monitor Kraken’s ongoing integration efforts and any further expansions of its Fed-connected capabilities.

Sources & verification

- U.S. Court of Appeals for the Tenth Circuit — Opinion documenting the denial of Custodia’s appeal: https://www.ca10.uscourts.gov/sites/ca10/files/opinions/010111400884.pdf

- Custodia Bank rehearing en banc master account coverage: https://cointelegraph.com/news/custodia-bank-rehearing-en-banc-master-account

- Custodia crypto bank appeal federal reserve master account coverage: https://cointelegraph.com/news/custodia-crypto-bank-appeal-federal-reserve-master-account

- Kraken receives master account and links to Fedwire coverage: https://cointelegraph.com/news/kraken-crypto-exchange-fed-master-account

- Additional context on Fed services not related to central bank digital currencies: https://cointelegraph.com/news/federal-reserve-service-not-related-to-cbdcs

Why it matters

The court’s ruling crystallizes the principle that access to the Fed’s payment rails is not an automatic entitlement for crypto-focused banks. It foregrounds the Fed’s discretion as a central feature of how digital-asset firms can participate in the U.S. financial infrastructure, at least in the near term. For stakeholders seeking to integrate digital assets into mainstream settlement processes, the decision clarifies the legal landscape and raises the bar for establishing the robust governance, risk controls, and compliance frameworks that the Fed expects of applicants.

At the same time, the Kraken milestone demonstrates that meaningful progress is possible even within a system that remains cautious about crypto-adjacent actors. By securing a master account from a regional Fed bank, Kraken has opened a pathway to improved liquidity and settlement efficiency, though with a narrower set of services than those enjoyed by conventional banks. The contrast between Custodia’s unresolved bid and Kraken’s operational foothold suggests that the road to broader access will likely be incremental, tempered by risk, regulatory clarity, and demonstrated resilience in transaction processing and governance.

Sources & verification

To verify the key elements of this story, readers can consult the official court filing and the referenced industry coverage:

- The Tenth Circuit opinion PDF confirming the denial of Custodia’s appeal: https://www.ca10.uscourts.gov/sites/ca10/files/opinions/010111400884.pdf

- Cointelegraph coverage on Custodia’s rehearing and related master-account discussions: https://cointelegraph.com/news/custodia-bank-rehearing-en-banc-master-account

- Cointelegraph coverage on Custodia’s crypto-bank appeal and Fed master account issues: https://cointelegraph.com/news/custodia-crypto-bank-appeal-federal-reserve-master-account

- Cointelegraph coverage on Kraken obtaining a master account: https://cointelegraph.com/news/kraken-crypto-exchange-fed-master-account

What the story means for the crypto ecosystem

As policy discussions evolve, the industry is watching how regulators balance the benefits of direct Fed access—lower settlement risk, faster liquidity management, and greater resilience—with the imperative to maintain safety, transparency, and financial stability. The Custodia ruling reinforces the notion that central-bank access is not guaranteed and that applicants must meet rigorous criteria and demonstrate systemic readiness. Simultaneously, Kraken’s milestone signals real-world progress and a potential blueprint for future entrants who can align with enhanced risk controls and compliance standards while leveraging more direct settlement capabilities. The next chapter will likely hinge on policy direction, the development of “skinny” account frameworks, and continued collaboration between policymakers, banks, and crypto firms to expand access without compromising systemic integrity.

Polymarket has partnered with oracle provider Pyth Network to launch traditional asset markets on its platform.

Summary

- Polymarket partnered with Pyth Network to introduce equity, commodity, and stock-linked contracts.

- The new markets include daily up or down and closing price contracts that reset at the end of each trading session.

- Pyth Network is providing real-time price feeds from trading firms and market makers to serve as the resolution layer for the new contracts.

According to an Apr. 2 announcement, the latest addition brings daily up-or-down and closing price contracts for major equity indexes, alongside commodities such as gold and oil, and US-listed stocks. Outcomes on these contracts are determined using Pyth’s real-time price feeds, and the markets reset at the end of each trading session.

Pyth Network will act as the resolution layer for these markets, replacing manual or exchange-specific references with a standardized data source aggregated from trading firms and market makers.

Simultaneously, Pyth has launched a data interface called Pyth Terminal, allowing users to track live price feeds and the reference values used to settle markets on Polymarket.

Oracle networks like Pyth bring off-chain data such as prices, foreign exchange rates, and commodities onto blockchains. These feeds are widely used across decentralized finance, prediction markets, and tokenized asset platforms, and have seen growing adoption, including by US government agencies.

PYTH price rallied over 70% after the announcement, while its market capitalization moved past $1 billion.

The latest products on Polymarket were launched as the platform continues to cement its position as a leading prediction market operator.

Last month, the project secured a $600 million investment from Intercontinental Exchange, the parent company of the New York Stock Exchange, as part of a broader multibillion-dollar commitment.

Meanwhile, Polymarket made investments of its own by acquiring DeFi infrastructure startup Brahma for an undisclosed sum.

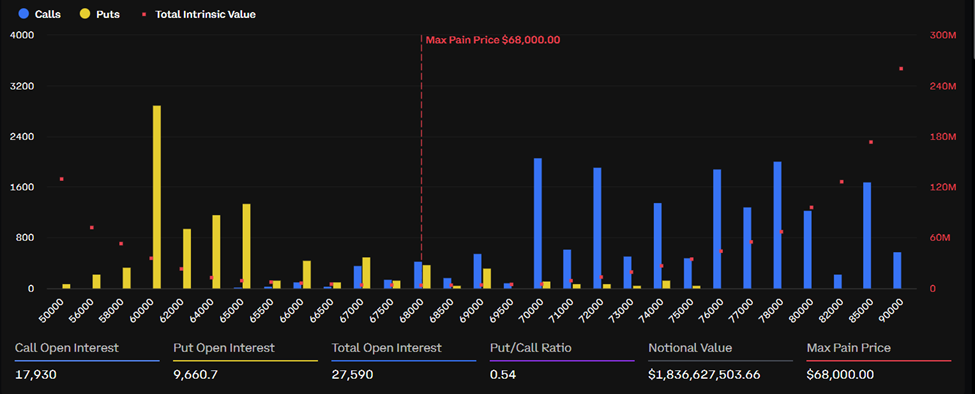

A whale accumulated more than 2,000 Bitcoin (BTC) put contracts overnight, targeting a move below $66,000, just as over $2.15 billion in Bitcoin and Ethereum (ETH) options settle on Deribit today, April 3.

The back-to-back repositioning signals that at least one large player sees downside risk in BTC’s current price range, even as call open interest still outnumbers puts across both assets.

Why the Whale Trade Matters

Options analytics platform Greeks.live flagged the position shift on April 2, noting the same whale had closed a profitable long trade hours earlier before pivoting bearish.

Per the analysts, the whale entered a long position at $66,000 and exited above $68,000, booking a confirmed profit.

Within hours, a trader of comparable size began accumulating put contracts, this time betting on a move lower.

The rapid reversal is notable. A whale exiting a winning trade and immediately loading the opposite direction suggests a view that the $66,000–$68,000 zone is a resistance ceiling, not a launchpad.

With BTC trading at $66,575 and its max pain level set at $68,000, the spot price sits $1,425 below the level where options sellers profit most. If BTC fails to close that gap before settlement at 08:00 UTC, the bearish whale’s puts gain value.

The Expiry Data

Bitcoin accounts for $1.84 billion of today’s total notional value, with 27,590 contracts outstanding. Call open interest stands at 17,930 against 9,600 puts, giving a put-to-call ratio of 0.54.

The call skew still leans bullish in aggregate, but the whale’s 2,000-contract put position adds concentrated downside weight near the $66,000 strike.

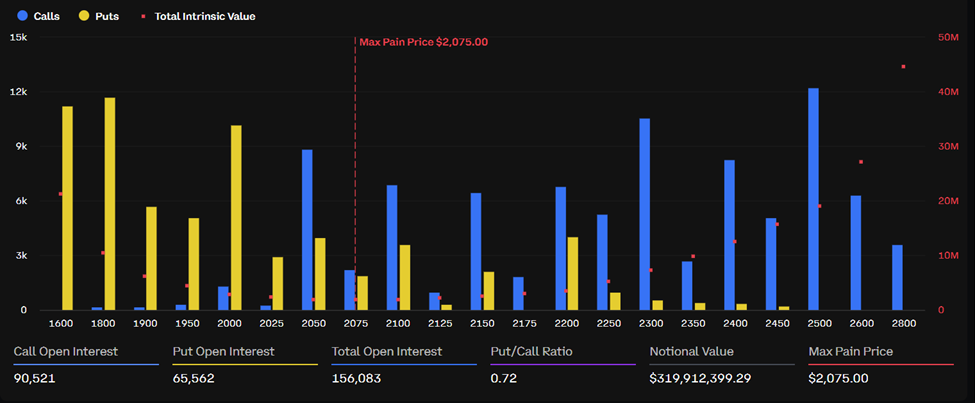

Ethereum’s expiry is smaller but similarly structured. With $319.9 million in notional value and 156,083 total contracts, ETH trades at $2,052 against a max pain level of $2,075. Its put-to-call ratio of 0.72 points to heavier downside hedging than BTC’s.

“Yesterday, the whale closed out the two positions on the right side… The whale entered the position at 66K and closed it out above 68K — this trade was a resounding success. Starting late last night, a whale of similar size began buying put options again, with over 2,000 contracts expiring today, targeting a price below 66K,” the analysts stated.

What Comes Next

Options settle at 08:00 UTC on Deribit. The hours leading up to that window typically generate the sharpest gamma hedging activity, pulling prices toward max pain.

For BTC, that means a potential drift toward $68,000 if bulls hold ground, or a break below $66,000 if the whale’s put bet plays out.

The post Whale Turns Bearish Ahead of $2 Billion Bitcoin and Ethereum Options Expiry appeared first on BeInCrypto.

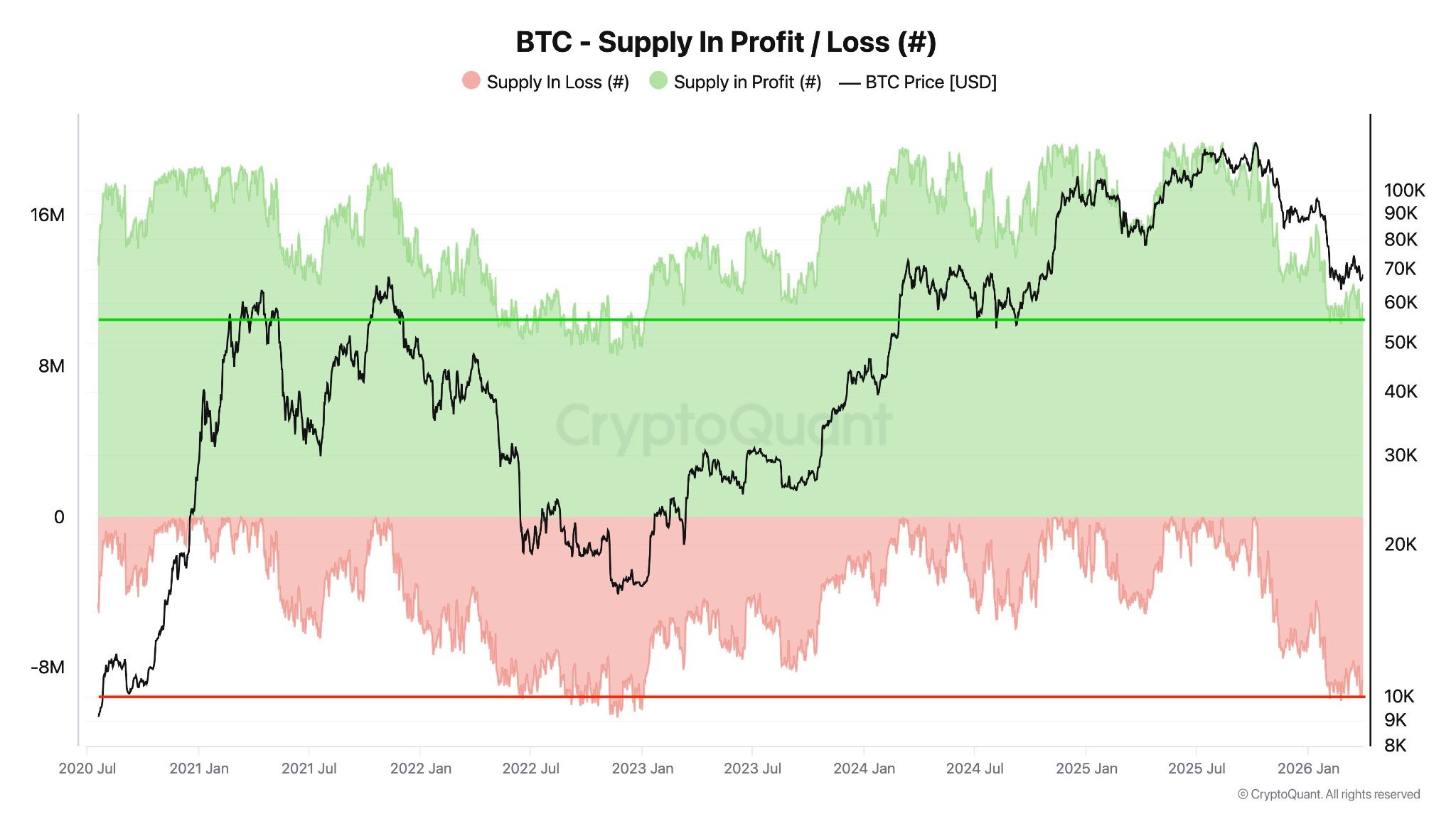

The amount of Bitcoin supply in profit and loss is now getting closer to levels typical of a bear market, according to a CryptoQuant analyst.

There are currently about 11.2 million Bitcoin (BTC) in profit. The previous bear market recorded 9 million BTC in profit at its lowest point, CryptoQuant analyst “Darkfost” said Thursday.

CryptoQuant data also shows there are about 8.2 million Bitcoin at a loss, with Glassnode data confirming it’s at levels not seen since late 2022.

“This is quite significant, considering that during the last bear market this figure reached about 10.6 million BTC,” Darkfost said.

Analysts have been debating whether Bitcoin has further to fall this year amid growing global turmoil. Bitcoin metrics that show a movement toward previous cycle lows could suggest that a market bottom is getting closer.

“This suggests that the market is reaching a notable level of undervaluation, comparable to the conditions observed during the previous bear market,” the analyst added.

Analyst sees increasing market stress, not undervaluation

However, Andri Fauzan Adziima, research lead at the Bitrue exchange, argued the data signals “increasing market stress, not immediate undervaluation.”

True capitulation bottoms saw deeper pain, he told Cointelegraph. The supply in loss in 2022 was greater than 50% and the supply in profit was around 45% or lower, while metrics such as net unrealized profit/loss (NUPL) and market value to realized value ratio (MVRV) were at “extremes.”

“Current data points to early/mid-bear transition (potential structural bottom near $55,000), with more downside or consolidation likely before a full reset.”

Related: Bitcoin’s drawdown is ‘less dramatic’ this cycle, Fidelity says

Data also shows Bitcoin has declined by about 52% from its all-time high this cycle, much less than previous bear markets, which saw 77% to 84% drawdowns from their cycle highs.

Strong dollar hampering recovery

Bitcoin author Timothy Peterson commented on X that Bitcoin “tends to struggle when the dollar is strong, and the Chinese yuan is weak.”

He added that this was due to tighter global liquidity, with higher dollar yields attracting capital into cash and bonds and cautious investor sentiment as China eases policy.

That only changes when US interest rates fall and “dollar yield loses its attractiveness,” which is not likely until the second half of 2026 or more likely 2027, he said.

The US dollar index (DXY) has gained about 5% over the past two months, according to TradingView.

For years, decentralized finance sold a simple, powerful idea: anyone, anywhere, can access financial services without gatekeepers. No banks, no approvals, no identity checks—just code and capital.

But beneath the surface, something is changing.

A growing number of protocols are quietly introducing permissioned layers—KYC-gated pools, whitelisted participants, and compliance-driven infrastructure. It’s subtle. Gradual. Easy to miss.

Yet it may redefine what DeFi actually is.

The Shift No One’s Loudly Talking About

Permissioned DeFi doesn’t arrive with headlines. It slips in through features like:

- KYC Pools – Liquidity pools restricted to verified users

- Whitelisted Access – Only approved wallets can interact with certain products

- Compliance Layers – Protocol-level rules aligning with regulatory frameworks

At first glance, these look like optional features. In reality, they signal a deeper evolution:

DeFi is adapting itself to fit inside the traditional financial system.

Why This Is Happening

Let’s be blunt—pure permissionless systems make regulators nervous.

Institutions want exposure to DeFi yields, but they need:

- Legal clarity

- Counterparty accountability

- Risk controls

Permissioned layers act as a bridge:

- They let institutions participate without violating compliance rules

- They give regulators something to work with

- They reduce the “wild west” perception of DeFi

In short, capital is forcing compromise.

What Changes (And What Breaks)

This shift isn’t just technical—it’s philosophical.

1. Participation Is No Longer Universal

The original promise of DeFi was inclusion.

Permissioned systems introduce exclusion by design.

If access requires:

- Identity verification

- Jurisdiction checks

- Approval from a governing entity

Then DeFi starts to look a lot like the system it aimed to replace.

2. “Open Finance” Becomes Conditional

DeFi assumed:

If you have a wallet, you’re in.

Permissioned DeFi changes that to:

If you meet the criteria, you’re in.

That’s a massive shift. It replaces code-based neutrality with policy-based access.

3. Liquidity Fragmentation

Instead of one unified pool of capital, we get:

- Public pools (permissionless)

- Private pools (permissioned)

This can lead to:

- Uneven yields

- Reduced efficiency

- Insider advantages for approved participants

Basically, the market starts splitting into tiers.

4. Power Starts Re-centralizing

Whitelists don’t manage themselves.

Someone decides:

- Who gets access

- Who gets removed

- What rules apply

Even if governance is “decentralized,”

Control creeps back in through decision-making layers.

The Trade-Off: Growth vs Principles

Let’s not pretend this is entirely bad.

Permissioned DeFi enables:

- Institutional capital inflows

- Regulatory survival

- Scalable adoption

Without it, DeFi risks staying niche—or getting shut out entirely.

But there’s a cost:

- Less openness

- Less censorship resistance

- Less equality

So the real question isn’t whether permissioned DeFi is good or bad.

It’s this:

How much of DeFi’s core ethos are we willing to trade for growth?

The Future: Two DeFis?

We may not end up with one unified ecosystem.

Instead, expect a split:

Permissionless DeFi

- Open to everyone

- Higher risk, higher innovation

- Resistant to control

Permissioned DeFi

- Regulated and compliant

- Institution-friendly

- Controlled access

They’ll coexist—but not as equals.

One maximizes freedom.

The other maximizes scale.

Final Thoughts

Permissioned DeFi isn’t sudden; it’s a slow drift.

No dramatic announcements.

No clear line crossed.

Just small changes… that quietly redefine everything.

And if you blink, you might miss the moment when “open finance” stops being fully open.

REQUEST AN ARTICLE

OpenAI has acquired technology talk show TBPN as it looks to refine how it communicates with audiences beyond its core products.

Summary

- OpenAI has acquired TBPN, a Silicon Valley-focused tech talk show, as it expands its role in shaping public conversations around artificial intelligence.

- TBPN will continue operating with editorial independence while also contributing to OpenAI’s communications and marketing efforts.

According to an Apr. 2 announcement, the deal brings the Los Angeles-based program under OpenAI’s umbrella. Financial terms of the deal were not disclosed.

TBPN, hosted by John Coogan and Jordi Hays, streams live for three hours each weekday and features interviews with founders, venture capitalists, and senior technology executives. Guests in recent months have included Mark Zuckerberg, Satya Nadella, and Sam Altman, underscoring the show’s growing influence within the tech ecosystem.

OpenAI’s leadership framed the acquisition as part of a push to shape how conversations around artificial intelligence unfold.

In an internal memo, Fidji Simo, OpenAI’s chief of strategy, said the company sees a need for “real, constructive conversation” as AI systems become more embedded in society. The company believes TBPN can help create that space while also expanding its reach.

Despite the ownership change, OpenAI has emphasized that TBPN will retain full editorial control.

Behind the scenes, the show is expected to contribute to OpenAI’s communications and marketing efforts beyond its daily broadcasts. Simo noted that TBPN’s track record in brand storytelling and its close view of industry trends played a role in the decision.

Founded in October 2024, TBPN began daily livestreaming in March 2025 and has since carved out a niche audience. Each episode draws roughly 70,000 viewers across platforms such as X, YouTube, and Spotify.

While modest compared to traditional financial media, the show has gained traction among technology leaders who see it as more aligned with industry perspectives than legacy outlets like Bloomberg or CNBC.

The acquisition comes shortly after OpenAI closed a $122 billion funding round led by Amazon, Nvidia, and SoftBank.

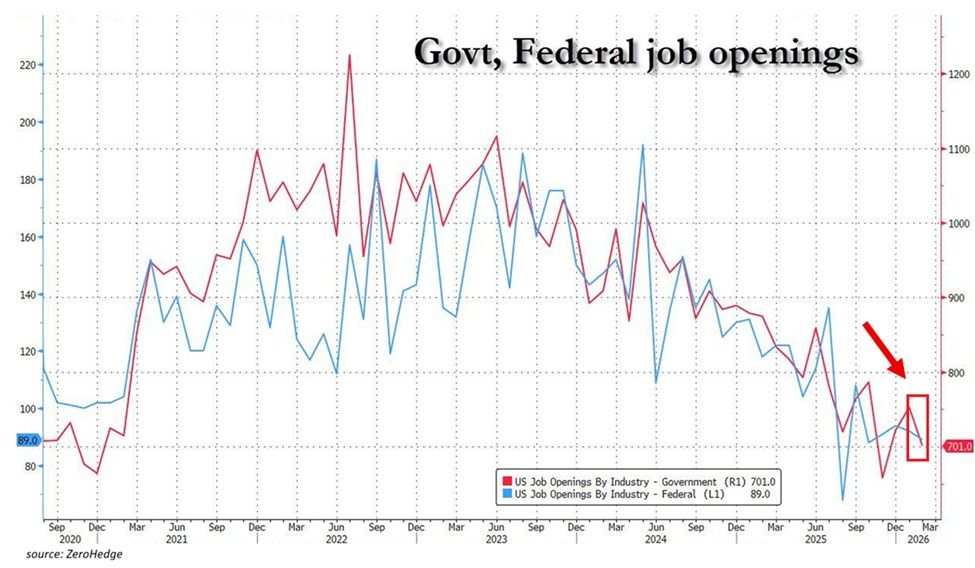

The US job market is showing alarming deterioration. According to The Kobeissi Letter, government job openings dropped 51,000 in February to 701,000.

This marked the second-lowest reading since December 2020. Available government vacancies have fallen 524,000 since their 2022 peak and now sit at pre-pandemic levels.

In addition, federal government openings fell to 89,000, the second-lowest since the pandemic low. This level is also in line with readings from 2017 and 2018.

Follow us on X to get the latest news as it happens

“Meanwhile, the government hiring rate stood at 1.4%, one of the lowest levels since mid-2020 and matching the 2016 and 2017 lows. Government hiring is frozen,” the post read.

Meanwhile, the private sector is shedding jobs at scale. Oracle reportedly laid off up to 30,000 employees on March 31. Amazon cut 16,000 corporate roles in January, and Block eliminated over 4,000 positions. These were just some of the many companies that made job cuts.

Consumer Sentiment Signals Trouble Ahead

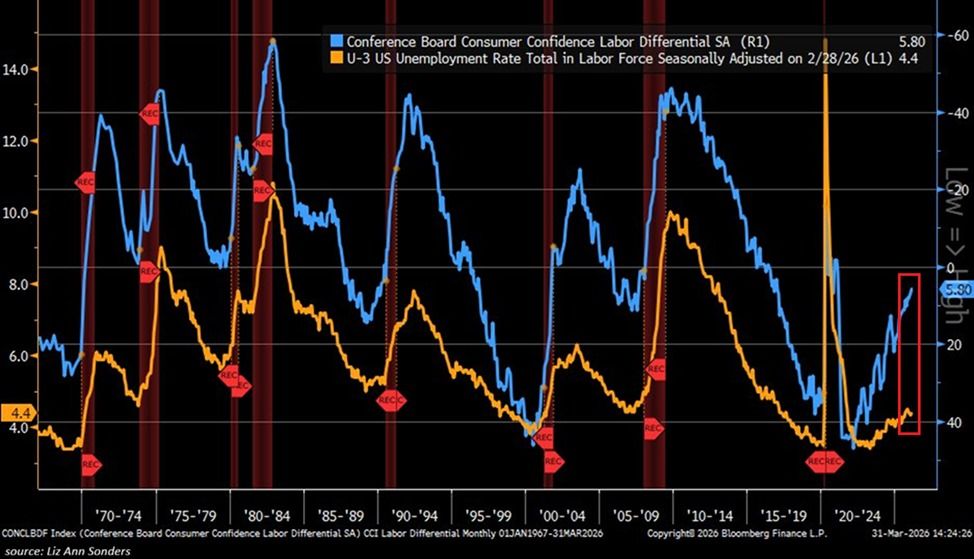

In a separate post, The Kobeissi Letter suggested that forward-looking indicators” point to a further increase in US unemployment.” The Conference Board’s March survey showed that only 27.3% of consumers described jobs as “plentiful.”

This was a marginal uptick from 26.7% in February, but still well below the roughly 55% who felt that way in 2022. At the same time, 21.5% said jobs were “hard to find,” up from approximately 10% over the same period.

The gap between these two readings, known as the labor market differential, fell to just 5.8 points. That represents the lowest level since the 2020 pandemic.

The Kobeissi Letter noted that historically, this indicator has been one of the most reliable leading signals of rising unemployment.

“Furthermore, current levels in this indicator have only been seen prior to or during a US recession since the 1990s. The job market is set for even more weakness,” the analysts added.

With these indicators pointing in the same direction, the March jobs report will be closely watched to determine whether underlying deterioration is cyclical or marks a deeper shift.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US Job Market Flashes Warning Signs Last Seen During 2020 Pandemic appeared first on BeInCrypto.

Circle plans to launch its own version of wrapped Bitcoin on the Ethereum network to target institutional markets.

Summary

- Circle plans to launch cirBTC on Ethereum, a 1:1 bitcoin backed wrapped asset targeting institutional markets.

- Wrapped Bitcoin allows BTC to be used on networks like Ethereum, giving institutions access to decentralized finance applications.

In a Thursday announcement, stablecoin issuer Circle said it plans to introduce cirBTC, a token that is backed 1:1 by bitcoin and aimed at over-the-counter desks, market makers, lending protocols, and other institutional participants, framing the asset as a “highly secure and neutral version of wrapped BTC.”

Wrapping allows a native asset like Bitcoin to be tokenized and used across other blockchains. In this case, wrapped Bitcoin lets BTC be brought onto networks such as Ethereum, which gives users access to decentralized finance applications.

The token will also launch on Circle’s layer-1 blockchain Arc and integrate with the Circle Mint platform.

Circle joins a growing list of participants that have introduced wrapped Bitcoin as demand for decentralized finance continues to expand among institutional users.

The sector is currently led by BitGo’s Wrapped Bitcoin, which currently holds a market capitalization of about $8 billion.

Coinbase also launched its own version, Coinbase Wrapped Bitcoin (cbBTC), in September 2024, which has since grown rapidly to reach a market capitalization of $5.9 billion. Last year, Coinbase launched Wrapped ADA (cbADA) on the Base blockchain to facilitate cross-chain liquidity.

Meanwhile, several other exchanges have released their own wrapped assets, including Kraken Wrapped BTC (kBTC), Binance Wrapped BTC (BBTC), Bitget Wrapped BTC (BGBTC), and OKX Wrapped BTC (okBTC), among others. These offerings are often paired with proof-of-reserve transparency to assure institutional traders that the underlying assets are held in secure, 1:1 custody.

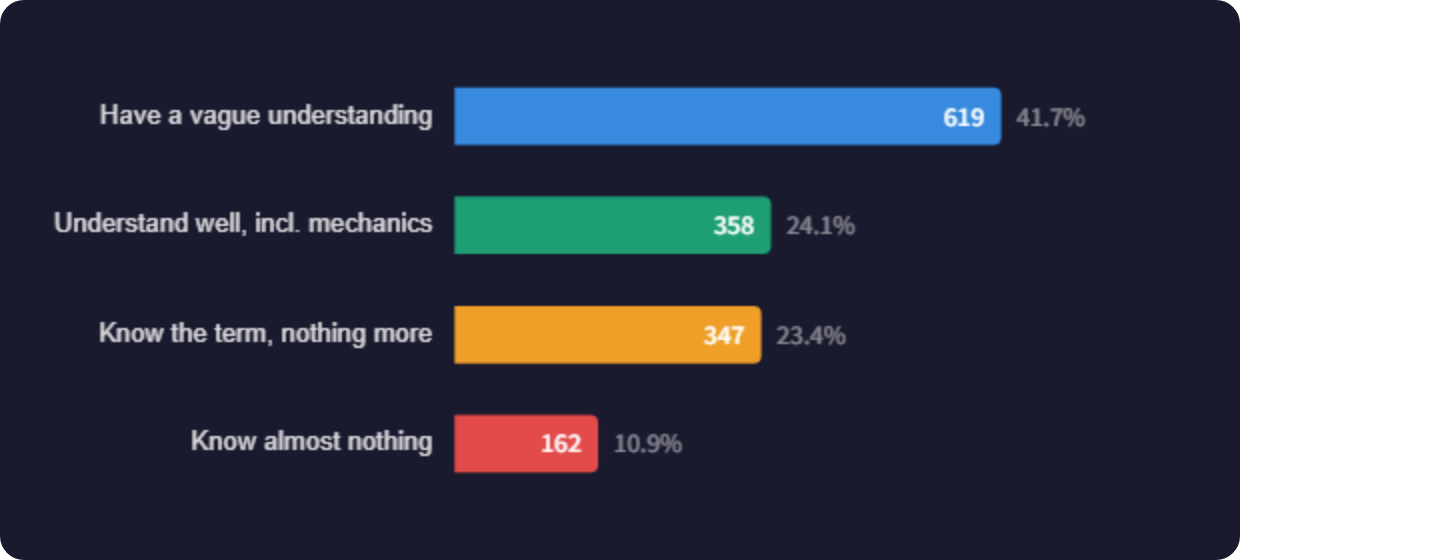

Japanese Gen Z stands out as the most scam-conscious generation when it comes to crypto. A new survey of 1,486 people across Japan found that younger users are far more alert to fraudulent pitches on social media than their older peers.

The gap between generations reveals that Japan’s crypto trust problem is not uniform — it varies by age and online habits.

Gen Z Watches for Scams, Boomers Struggle With Basics

The survey, conducted by Tokyo-based consulting firm Clabo in February 2026, asked respondents why they view crypto as suspicious. The top answer overall was “I don’t understand how it works,” chosen by 23.3% of respondents. Price swings came second at 21.1%, followed by fraud concerns at 19.2%.

But generational breakdowns tell a different story. Gen Z respondents flagged social media scams as their primary worry. They encounter fake giveaways and shady promotions on platforms they use daily. Older cohorts, including Japan’s bubble generation, pointed instead to the complexity of blockchain technology itself.

Millennials showed the highest rate of actual crypto investment among all age groups. They also reported the most active information-seeking behavior.

Across all groups, half of the respondents said they had never invested in crypto. Only 33.7% said they currently hold digital assets. Another 15.7% said they once invested but have since stopped.

YouTube Leads for Investment Decisions

When it comes to where people get crypto news, traditional news sites ranked first at 38.4%. Social media followed at 36.7%, with YouTube at 31.6%. But for actual investment decisions, YouTube jumped to first place at 27%.

The survey suggests that Japan’s crypto industry still faces a basic education gap. Clabo, which offers wallet recovery and security consulting, recommended more accessible educational content tailored to each generation’s specific concerns.

The post Japanese Gen Z Fears Crypto Scams More Than Any Other Generation appeared first on BeInCrypto.

Stablecoin issuer Circle said it plans to launch its own version of a wrapped Bitcoin, which would put it against incumbents Coinbase and BitGo as it targets institutional users.

The asset, called cirBTC and announced on Thursday, is set to launch on Ethereum, backed 1:1 by bitcoin (BTC) and aimed at over-the-counter desks, market makers and lending protocols.

Circle said the asset is designed to provide institutions with a “highly secure and neutral version of wrapped BTC.”

Financial institutions, which have become significant buyers of Bitcoin, have been actively exploring decentralized finance. Wrapped versions of Bitcoin would allow the asset to be used on other chains, such as Ethereum, giving them access to DeFi.

In addition to Ethereum, the new asset will also launch on Circle’s layer-1 blockchain Arc and its Circle Mint platform, said Circle.

Cointelegraph contacted Circle for further details, but did not receive an immediate response.

Circle joins race led by Coinbase and BitGo

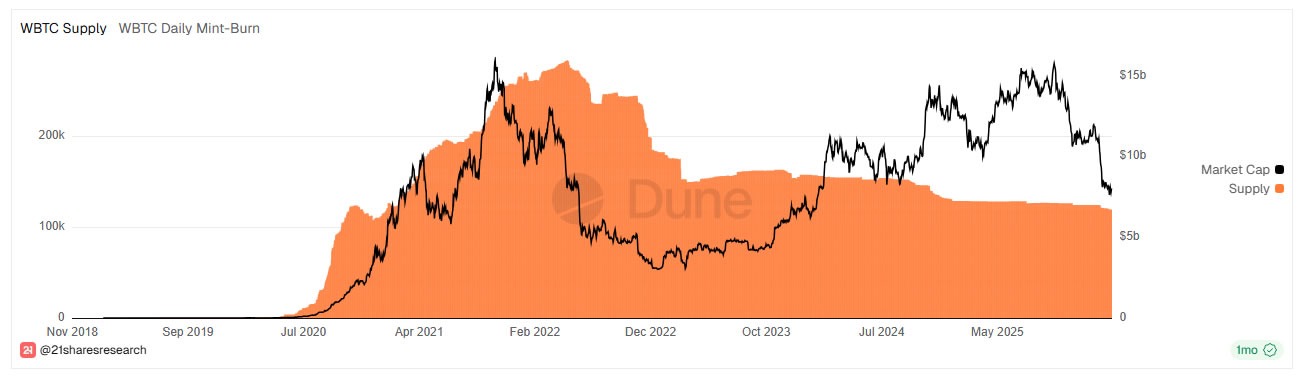

Circle’s new wrapped Bitcoin joins a market currently led by BitGo’s Wrapped Bitcoin (WBTC) and Coinbase Wrapped Bitcoin (cbBTC).

Coinbase’s cbBTC was launched in September 2024 and has a current market capitalization of $5.9 billion and a current supply of 88,800 tokens.

BitGo’s wBTC is the dominant wrapped Bitcoin token, with a market capitalization of about $8 billion and 119,157 tokens in circulation. However, that figure is roughly half its November 2021 peak, when Bitcoin hit its cycle all-time high.

Related: WBTC expands to Hedera as Bitcoin liquidity flows into new DeFi rails

Crypto exchanges launched their own wrapped Bitcoin

Several crypto exchanges have launched variations of wrapped Bitcoin, including Kraken Wrapped BTC (KBTC), Gate Wrapped BTC (GTBTC), Binance Wrapped BTC (BBTC), Huobi BTC (HBTC) and OKX Wrapped BTC (XBTC), but their market caps are a fraction of the two leaders.

The total combined supply of wBTC and cbBTC stands at roughly 208,000 BTC, according to CoinGecko.

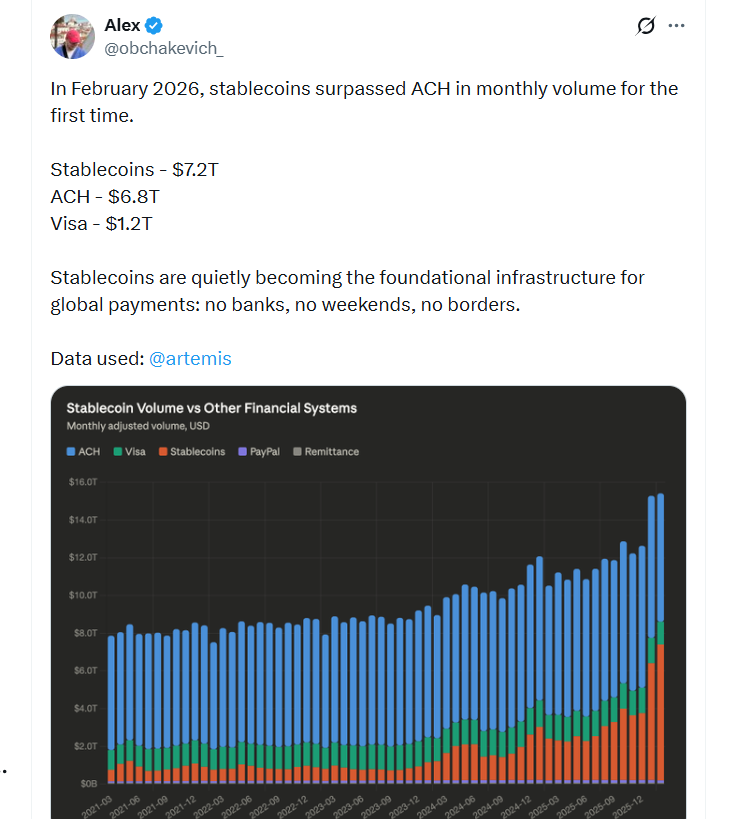

Stablecoin transaction volume surpassed the US Automated Clearing House network for the first time in February, a significant milestone for an asset class that has existed for less than 12 years.

According to data from blockchain analytics platform Artemis, the total 30-day adjusted rolling stablecoin volume hit $7.2 trillion in February, beating the Automated Clearing House network at $6.8 trillion.

The data is based on 30-day rolling adjusted volume of stablecoin transactions in US dollars, excluding MEV activity and intra-centralized exchange transactions, comparing this to the daily average volume of other financial systems.

“Stablecoins are quietly becoming the foundational infrastructure for global payments: no banks, no weekends, no borders,” said analyst Alex Obchakevich in an X post on Friday.

Surpassing the ACH is significant, given that the network functions as the backbone of the US payments system. Data from Nacha, one of the primary forces governing the ACH alongside the Federal Reserve, indicates that the ACH network processes about 93% of salary payments in the US.

The data also shows that stablecoin market volumes have consistently grown over the past few years relative to the other major financial systems, such as Visa and PayPal.

Artemis data for March show that stablecoin volume continued to hit new highs, notching $7.5 trillion for the month and matching the ACH over that 30-day period.

Stablecoin supply continues to surge

Meanwhile, in the first quarter of 2026, total stablecoin supply hit $315 billion, increasing by $8 billion from the first quarter of 2025, according to data from CEX.IO.

Stablecoins also accounted for 75% of total crypto trading volume in the quarter, marking the highest levels on record, Cointelegraph previously reported.

Related: US Treasury seeks public input for state-level stablecoin regulations

An important catalyst for stablecoins has been the growing adoption by institutions amid a warming regulatory climate in the US.

Analysts from major traditional finance institutions such as Standard Chartered have tipped the total stablecoin market cap to hit $2 trillion by 2028, which would mark an increase of over 530% from current levels.

In a post on Tuesday, Frank Chapparo, the content head at trading firm GSR, argued that banks or fintech firms are “toast” if they ignore the explosive growth of the sector.

“The signals are everywhere,” he said, pointing to the total supply growing from less than $30 billion in 2020 to over $300 billion since then. Chapparo highlighted the GENIUS Act as a key piece of regulation that has unlocked institutional adoption.

Magazine: AI agents will kill the web as we know it: Animoca’s Yat Siu

Every TV show canceled so far in 2026, from “Watson” to “Palm Royale”

Shadow Cabinet League Table: Badenoch extends her lead, Timothy holds second

City school to get new unit dedicated to children with learning difficulties

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Tom Lee Just Warned That Bitcoin Will Crash Before It Does Something Nobody Has Ever Seen Before

Next Financial Crisis WORSE Than 2008 – $3T Private Credit Collapsing, $4.6B TRAPPED

IF YOU HOLD XRP ONDO & XLM YOU BETTER SEE THIS (HUGE MOVES MADE)

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat11 hours ago

NewsBeat11 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World1 day ago

Crypto World1 day agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Business6 hours ago

Business6 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Business1 day ago

Business1 day agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

You must be logged in to post a comment Login