Crypto World

Federal Reserve moves to ease capital rules for Wall Street’s biggest banks

Fed unveils a 90-day comment plan to ease Basel III and G-SIB capital rules, modestly cutting requirements for large banks and more for regional lenders.

Summary

- Fed launches a 90-day comment period on proposals that slightly lower capital requirements for large banks and more materially for smaller regionals.

- Bowman’s “four pillars” overhaul spans stress tests, eSLR, Basel III and G-SIB surcharges, aiming to free credit and shareholder payouts without scrapping post-2008 safeguards.

- Industry groups cheer the recalibration as growth-friendly, while critics warn easing buffers amid oil shocks and higher-for-longer rates risks weakening prudential defenses.

The Federal Reserve voted Thursday morning to formally release a sweeping package of proposed bank capital reforms, launching a 90-day public comment period on changes that would modestly reduce capital requirements for the largest U.S. financial institutions — and more substantially ease the burden on smaller regional banks. The proposals, previewed by Fed Vice Chair for Supervision Michelle Bowman in a March 12 speech at the Cato Institute, represent the most significant overhaul of the post-2008 bank capital framework in years and a clear victory for Wall Street institutions that had spent years lobbying against an earlier, more stringent version of the rules.

The package addresses what Bowman described as “the four pillars” of the regulatory capital framework for the largest banks: stress testing, the enhanced supplementary leverage ratio (eSLR), the Basel III endgame rules, and the G-SIB surcharge applied to globally significant institutions. Together, the proposals would produce a net decrease in capital requirements for large banks “by a small amount,” while smaller banks focused on traditional lending would see “slightly larger reductions”. For major institutions such as JPMorgan Chase and Goldman Sachs, the modest increase from revised Basel III calculations would be more than offset by a recalibrated G-SIB surcharge — one Bowman argued had grown disproportionate to the risks these banks actually carry.

The philosophical underpinning of the reform is a conviction that capital requirements imposed after the 2008 financial crisis have gradually overshot their intended purpose. “When capital requirements become excessive, they hinder the banking system’s essential role of providing credit to the real economy,” Bowman said in her Cato Institute remarks. She described the proposals as a “sensible recalibration” designed to remove redundant standards and better align requirements with actual institutional risk profiles, rather than a wholesale rollback of post-crisis prudential safeguards.

The eSLR reforms are particularly significant. A final rule approved by the FDIC and Federal Reserve in November 2025 — effective April 1, 2026 — had already replaced the existing 2% eSLR buffer for global systemically important banks with a buffer equal to half of each institution’s Method 1 G-SIB surcharge, capped at 1% for subsidiary banks. FDIC staff estimated that change alone would reduce aggregate Tier 1 capital requirements by $13 billion, or under 2%, for G-SIBs, and by $219 billion — or 28% — for major bank subsidiaries. The new proposals being voted on Thursday extend that logic across the Basel III and G-SIB surcharge frameworks.

The banking industry responded favourably. The American Bankers Association, Financial Services Forum, and Bank Policy Institute issued a joint statement praising Bowman’s approach as “a thoughtful, bottom-up” resolution to the concerns raised by 97% of commenters on the prior Basel proposal, calling for a capital framework that “reflects the actual risks in the banking system, rather than over-calibrated requirements that impede economic growth”.

The timing carries broader market significance. With the Fed holding rates steady at 3.5%–3.75% and explicitly raising its 2026 inflation forecast to 2.7% on Wednesday, the capital easing offers Wall Street a degree of policy relief that monetary policy itself is not currently providing. Freeing up capital for lending, share buybacks, and dividends — precisely the stated aim of the reform — may inject some flexibility into a financial system otherwise navigating a geopolitical oil shock and a higher-for-longer rate environment.

Critics, however, argue that loosening capital buffers during a period of elevated macro uncertainty runs counter to the spirit of prudential regulation. Bowman indicated no implementation timeline beyond coordinating with other international jurisdictions — leaving the final shape of the rules subject to the 90-day comment process.

RLUSD Minting Activity on Ethereum

Ripple Labs has minted nearly 10 million RLUSD tokens after weeks of heavy token burns across networks. The issuance took place on Ethereum and signals a shift in supply activity. The move follows large-scale reductions that tightened circulation and reshaped recent stablecoin flows.

XRP Ledger and Supply Rebalancing Strategy

Ripple continues to balance RLUSD supply between Ethereum and the XRP Ledger through coordinated minting and burning cycles. This approach supports network efficiency and ensures availability across different blockchain environments. Additionally, it allows the firm to respond quickly to shifting transactional demand.

During late March and early April, Ripple executed several large burns exceeding $230 million within one week. One notable event removed about 180 million RLUSD tokens within a few hours. These actions reduced excess supply and prepared the system for controlled re-expansion.

The recent mint indicates that Ripple has recalibrated its supply strategy following those aggressive burns. It now distributes liquidity more evenly between supported chains and user segments. As a result, RLUSD remains adaptable to both institutional and retail transaction requirements.

Stablecoin Growth and Market Integration

RLUSD continues to expand its presence as a bridge between traditional finance and digital asset markets. Exchanges have begun listing new trading pairs that improve accessibility and increase transactional use cases. This expansion strengthens RLUSD’s role within broader crypto liquidity networks.

Bitrue introduced trading pairs that match RLUSD with tokenized gold assets such as PAXG and XAUT. These assets represent physical gold exposure issued by established providers in the market. Therefore, RLUSD gains additional utility in diversified trading environments.

Meanwhile, Binance has enabled RLUSD support on the XRP Ledger, allowing direct transactions within its platform ecosystem. This integration increases exposure and simplifies cross-platform transfers for users. Furthermore, it aligns with Ripple’s goal of improving cross-border payment efficiency.

Recent reports indicate that RLUSD reserves exceed its circulating supply, reinforcing its backing structure. Reserve holdings reached approximately $1.56 billion, while token supply remained slightly lower. Hence, the stablecoin maintains a surplus-backed position within regulated custody frameworks.

💵💵💵💵💵💵 9,900,000 #RLUSD minted at RLUSD Treasury.https://t.co/UQY0Dx1bZm

— Ripple Stablecoin Tracker (@RL_Tracker) April 8, 2026

Render price is up 3.55% on April 9 as a W pattern develops across the daily chart, with the Supertrend flipping green and the MACD histogram turning positive for the first time in months. The $2.646 resistance is the pattern confirmation trigger and the immediate bull case target.

Summary

- Render price is trading at $2.071 on April 9, up 3.55% on the session, as a W pattern develops across the daily chart with bottoms in September 2025 and February 2026.

- The daily Supertrend (10,3) has flipped green at $1.631 and the MACD histogram is printing a positive 0.077, confirming early upside momentum behind the move.

- The immediate bull target is $2.646 resistance; a daily close below $1.631 Supertrend support invalidates the recovery thesis and risks a return to the February lows near $1.20.

Render (RENDER) price is trading at $2.071 on April 9, up 3.55% on the session, as a W pattern takes shape on the daily chart following a seven-month decline from 2025 highs above $3.50. The token has printed two distinct lows, the first in September 2025 and the second in February 2026, and is now pushing toward the $2.646 resistance level that capped the January recovery attempt. The daily Supertrend has flipped green and the MACD histogram has turned positive for the first time in months, supporting the early recovery case.

The daily chart shows Render forming a W pattern, defined by two successive troughs separated by a brief interim high. The first low appeared in September 2025 during a broader AI token sector sell-off, and the second developed through February and March 2026 after price failed to break the $2.646 resistance ceiling. Price is now rising from the second trough with improving momentum, but pattern confirmation requires a sustained daily close above $2.646.

The Supertrend indicator (10,3) has turned green at $1.631, marking its first bullish reading after an extended bearish period. The MACD (12,26,9) supports the shift: the MACD line sits at 0.023, the signal at 0.100, and the histogram is printing a positive 0.077. The expanding positive histogram bars confirm that buying pressure is building, even as the MACD line has not yet crossed above the signal.

Wintermute, a leading algorithmic market maker, noted in a recent market intelligence update that AI stocks have been siphoning liquidity from crypto-native AI tokens, a dynamic that contributed to RENDER’s slide from the March high of $3.17 before the current base began forming.

Key Levels: Support, Resistance, and Price Targets

The $2.646 level is the immediate resistance and the W pattern confirmation trigger. A confirmed daily close above it opens the extended bull case toward $3.00, the nearest psychological level on the daily chart. If momentum accelerates from there, the March 2026 high near $3.17 represents the next reference point.

On the downside, the Supertrend at $1.631 is the primary support to monitor. A daily close below that level shifts the indicator back to red and invalidates the recovery thesis. The February 2026 lows near $1.20 represent the last structural demand zone before the W pattern collapses entirely.

Invalidation: a daily close below $1.631.

On-Chain and Market Data Context

Render connects GPU providers with users requiring compute power for AI inference and 3D rendering, giving the token direct exposure to AI sector sentiment. RENDER surged 40% to $3.17 on March 11 as AI token sentiment briefly recovered before sector-wide selling resumed. Daily trading volume on April 9 stands at 3.24 million RENDER tokens, reflecting sustained participation as price builds from the second W pattern trough.

According to Coinglass data, funding rates in RENDER perpetual contracts have shifted from negative toward neutral as price recovered from the February base, consistent with short-side pressure beginning to ease and a healthier foundation for a sustained move.

If RENDER holds $1.631 on a daily close basis and volume supports the advance, a test of the $2.646 W pattern trigger becomes the near-term base case, with $3.00 the next level to watch on a confirmed breakout.

Crypto World

Comcast (CMCSA) Stock: Strategic Streaming Bundle Expansion Strengthens Competitive Edge

Key Highlights

- Xfinity bundles now include Disney+, Hulu, and HBO Max subscriptions

- Customers can save up to 45% with new flexible StreamSaver packages

- Enhanced StreamStore platform provides centralized subscription management

- Strategic bundle expansion reinforces Comcast’s streaming market presence

- Integration of internet, TV, and streaming creates unified entertainment ecosystem

Comcast Corp (CMCSA) shares trade at $28.13, gaining 0.64%, following the announcement of significant enhancements to its Xfinity StreamSaver bundle offerings. The telecommunications giant incorporates premium streaming platforms to enhance its competitive stance in the digital entertainment landscape. This strategic initiative aims to improve customer loyalty and drive subscription growth throughout its service portfolio.

Comcast Corporation, CMCSA

The telecommunications provider now incorporates Disney+, Hulu, and HBO Max within its bundle portfolio. These additions complement previously available services including Netflix, Apple TV, and Peacock. Consequently, Xfinity establishes itself as a comprehensive gateway for accessing premium streaming content.

This strategic enhancement addresses increasing consumer appetite for consolidated digital entertainment packages. Subscribers increasingly prioritize affordability and streamlined billing across various platforms. Therefore, Comcast adapts its service structure to match shifting consumption patterns in the streaming sector.

StreamSaver Package Upgrades Deliver Enhanced Subscriber Benefits

Comcast rolls out customizable bundle configurations featuring three to five streaming services. Subscribers can tailor packages according to personal entertainment preferences and financial parameters. These bundled options provide discounts reaching 45% versus individual platform subscriptions.

The provider organizes eight distinct bundle configurations through its StreamStore interface. This digital marketplace enables subscribers to explore and control numerous streaming accounts from a single location. Comcast consolidates access to an extensive library of entertainment options.

Subscribers maintain the ability to select ad-free subscription tiers or incorporate additional services. This adaptability gives users greater autonomy over entertainment expenditures and content choices. Therefore, Comcast elevates its competitive advantage within the crowded streaming marketplace.

StreamStore Platform Updates Deliver Improved User Experience

Comcast upgrades StreamStore capabilities to accommodate the broadened bundle selections. Subscribers can navigate the platform through web browsers, Xfinity hardware, or voice-activated controls. This multi-channel approach ensures smooth interaction across streaming platforms.

The interface provides access to more than 450 applications and thousands of entertainment titles. Customers can complete rentals, purchases, or subscriptions through a consolidated dashboard. Therefore, Comcast minimizes the complexity inherent in managing multiple streaming accounts.

Furthermore, the system facilitates straightforward migration of current subscriptions into bundled offerings. This functionality streamlines the transition process and enhances subscriber satisfaction. Thus, Comcast improves prospects for maintaining long-term customer relationships.

Comprehensive Strategy Integrates Streaming with Core Services

Comcast connects the StreamSaver enhancement with its overarching digital infrastructure approach. Subscribers can merge streaming packages with broadband, wireless, and television services. This methodology delivers an integrated digital entertainment ecosystem across all offerings.

The organization provides supplementary discounts when subscribers consolidate multiple services. These comprehensive packages incorporate high-performance internet access and premium television capabilities. Therefore, Comcast amplifies revenue opportunities across its entire service range.

The platform integration encompasses advanced features including 4K resolution streaming and simultaneous multi-screen viewing. These technological improvements elevate subscriber satisfaction and system functionality. Thus, Comcast establishes Xfinity as an all-inclusive entertainment platform.

Industry Dynamics and Strategic Market Positioning

The streaming industry maintains rapid transformation characterized by intensifying rivalry and content dispersion. Leading platforms aggressively pursue subscriber acquisition and sustained engagement. Bundle-based strategies have emerged as critical tools for competitive distinction.

Comcast capitalizes on its technical infrastructure and content collaborations to maintain competitive viability. The incorporation of premier streaming platforms reinforces its market significance. The organization expands its identity beyond conventional cable television services.

Consolidated billing systems and unified account management resonate with contemporary subscriber preferences. Modern consumers prioritize accessibility and economic efficiency in subscription-based services. Therefore, Comcast refines its business approach to satisfy these evolving demands.

Comcast enhances Xfinity StreamSaver packages to solidify its standing within the streaming entertainment sector. The incorporation of major platforms delivers improved value and customization options for subscribers. The company advances its strategic vision of unifying connectivity infrastructure with content delivery.

This initiative mirrors broader industry movements toward consolidated service offerings and enhanced user convenience. Comcast applies its operational scale and partnership network to compete effectively. Consequently, the organization establishes foundations for continued expansion in digital entertainment markets.

The latest AI video tool to go viral this week is HeyGen’s Avatar V, announced April 8 with 472,000 views on X, which builds a photorealistic digital twin of a user’s face, voice, and gestures from a single 15-second webcam recording and then generates unlimited studio-quality video without any professional equipment.

Summary

- Avatar V captures a user’s specific micro-expressions, lip geometry, facial silhouette, and natural movement from one 15-second clip, then maintains that identity across every video generated regardless of length, angle, outfit, or scene, solving the identity drift problem that has caused most AI avatars to degrade in quality after a few seconds

- Once the digital twin is created, users pick a base photo as their identity reference, apply any outfit or setting via text prompts, and generate video in 175 languages with full lip-sync; voice cloning is a separate optional step the company recommends for maximum realism

- Avatar V is now the foundation all other features in HeyGen’s platform run on, integrated with Seedance 2.0 for cinematic video generation and available across paid subscription tiers

HeyGen’s official launch page describes Avatar V as built on a single belief: the output has to be good enough that users would be willing to put their name on it, not good for AI, just good. The model is trained on what HeyGen calls a temporally grounded identity embedding built from the 15-second clip, capturing the specific gestures and expression transitions that make a person recognizably themselves across different contexts. Wide shots, medium frames, and close-ups all stay consistent from one recording. The process requires no studio lighting and no crew; a standard phone or webcam is enough.

The key design principle is separating identity from appearance. The 15-second clip defines how a person moves. A separate base photo defines how they look. Users can then change the look freely while the motion stays unmistakably theirs.

Most AI avatar systems optimize for a single impressive moment: the screenshot, the short clip, the controlled demo where everything works in the model’s favor. They look sharp in two seconds and collapse in twenty as the face drifts from the source. Avatar V was designed specifically to hold across the full runtime of a video without that drift. HeyGen describes this as identity consistency: the same face, the same micro-expressions, the same presence from the first frame to the last, across a 30-second clip or a 10-minute module.

What Users Can Actually Build With It

The practical workflow is three steps: record a 15-second video, optionally record a standalone voice clone, then choose a base photo as the identity reference for every scene generated afterward. From that base, users write prompts to generate new outfits, settings, and styles, or use the HeyGen library. The finished video can be delivered in any of 175 languages with lip-sync adapted to the target language automatically. HeyGen advises users to be expressive during recording because, as the company put it, “the energy you put in is the energy you get out.”

Why This Matters for Content Creation at Scale

As crypto.news has reported, AI tools that reduce the cost and time of producing professional content are directly reshaping enterprise headcount decisions in 2026. As crypto.news has noted, the proliferation of AI content tools is a key variable in how institutional investors are assessing the durability of AI infrastructure spending. Avatar V is now fully available through HeyGen’s paid plans, with access to the platform’s full suite of templates, translation, and studio tools.

Anthropic revenue surpassed $30 billion on an annualized basis as of early April 2026, the company disclosed alongside a major new compute deal with Google and Broadcom, marking a more than threefold increase from the approximately $9 billion run rate it reported at the end of 2025.

Summary

- The $30 billion figure puts Anthropic ahead of OpenAI’s reported run rate of approximately $24 to $25 billion, with the gap driven by Anthropic’s enterprise-heavy revenue mix: 80 percent of its revenue comes from business customers rather than consumers, producing higher retention and lower churn than a consumer-first product strategy

- Over 1,000 business customers are now each spending more than $1 million annually on Claude services, doubling from 500 when Anthropic raised its Series G at a $380 billion valuation in February 2026; the company says that number doubled in less than two months

- Alongside the revenue disclosure, Anthropic confirmed a new long-term agreement with Google and Broadcom for multiple gigawatts of next-generation TPU computing capacity beginning in 2027, described by CFO Krishna Rao as “our most significant compute commitment to date”

Anthropic’s official announcement states plainly: “Our run-rate revenue has now surpassed $30 billion, up from approximately $9 billion at the end of 2025.” The trajectory behind that figure is striking. The company had a run rate of roughly $1 billion at the start of 2025, $4.5 billion by mid-year, $9 billion by year-end, $14 billion in February when it announced its Series G, and $30 billion in April. Each milestone came faster than the prior one. CEO Dario Amodei has noted repeatedly that he has consistently underestimated his own company’s growth, saying he is “always very conservative” on the business side and has been wrong every time.

Claude Code, the company’s agentic coding platform, has been a particular standout, generating over $2.5 billion in run-rate revenue as of February 2026, with weekly active users doubling since January 1.

The enterprise customer expansion tells the most important part of the story. When Anthropic announced its Series G in February, it noted that over 500 business customers were each spending more than $1 million annually. That number now exceeds 1,000 and doubled in less than two months. This is not organic drift from marketing. It reflects a fundamental shift in how large organizations are deploying AI: not as a search replacement or productivity experiment, but as core infrastructure for legal, finance, consulting, and communications workflows where knowledge worker productivity carries a measurable premium. Claude’s API market share expanded from 12 percent in 2023 to 32 percent by mid-2025, overtaking OpenAI to become the enterprise language model leader by that measure.

What the Google and Broadcom Compute Deal Signals

The timing of the compute announcement alongside the revenue disclosure is deliberate. Anthropic is signaling to the market that it has the demand to justify infrastructure at a scale few companies can access. The deal gives Anthropic access to approximately 3.5 gigawatts of TPU-based computing capacity beginning in 2027, an extension of the $50 billion US AI infrastructure commitment announced in November 2025. Anthropic already runs workloads on AWS Trainium, Google TPUs, and Nvidia GPUs, matching each workload to the chips best suited for it.

What a $30 Billion Run Rate Means for the AI Market

As crypto.news has reported, the revenue signals coming from frontier AI companies are now primary inputs for institutional investors assessing whether the AI buildout justifies current infrastructure spending levels. As crypto.news has noted, the competitive dynamics between Anthropic and OpenAI have direct market effects on AI-adjacent crypto assets and the broader perception of the AI sector’s capital efficiency. Anthropic projects positive free cash flow by 2027 while OpenAI has pushed its breakeven target to 2030, a structural gap that is now visible in revenue terms.

Securitize has appointed Brett Redfearn as its president and as a member of the tokenization platform’s board of directors, underscoring the crypto industry’s growing pull for former regulators and established market veterans. Redfearn, who previously led the U.S. Securities and Exchange Commission’s Division of Trading and Markets, spent over a decade at JPMorgan and later served as Coinbase’s head of capital markets. He has also been a member of Securitize’s advisory board, and the company’s Thursday notice confirmed the leadership change as it continues to push real-world asset tokenization into the crypto mainstream.

The move arrives as tokenization of real-world assets (RWA) gains momentum across crypto markets. Securitize’s boardroom shake-up comes amid a broader surge in on-chain assetization activity, with data from analytics platform RWA.xyz showing $3.85 billion in distributed asset value across platforms in March and tokenized stocks on-chain surpassing $1 billion in total value. The numbers highlight a material shift toward regulated, tokenized exposure to traditional assets within the crypto ecosystem.

Key takeaways

- Brett Redfearn is named president and board member of Securitize, bringing SEC leadership experience, Coinbase capital markets background, and JPMorgan tenure to the tokenization platform.

- Market momentum for tokenized assets remains robust, with March data placing distributed asset value at about $3.85 billion on RWA platforms and tokenized stocks crossing $1 billion in on-chain value.

- The SEC is recalibrating its enforcement leadership, naming David Woodcock as director of the Division of Enforcement, a role that will shape crypto oversight as the space expands.

- Lawmakers are scrutinizing regulator departures, including the exit of former enforcement head Margaret Ryan, amid ongoing questions about crypto enforcement actions and dropped cases.

- The broader trend of ex-government officials entering crypto continues, signaling a convergence of traditional financial governance experience with digital asset markets.

Strategic pivot at Securitize

In its official announcement, Securitize confirmed Brett Redfearn’s elevation to president and a seat on the company’s board. The former SEC official led the agency’s Division of Trading and Markets, a portfolio overseeing market structure and regulatory compliance, before moving to Coinbase as head of capital markets. He also accumulated frontline experience at JPMorgan spanning various roles across a decade. By bringing Redfearn onto the executive team, Securitize signals a continued emphasis on robust compliance, market governance, and scalable tokenization of real-world assets—areas where regulatory familiarity and traditional market discipline can be advantageous for accelerating institutional-grade adoption.

Redfearn’s growing role at Securitize also reflects a broader industry trend: attracting senior figures with public-sector credibility to help bridge crypto innovation with established financial norms. The executive’s transition from public service to private sector leadership dovetails with ongoing investor appetite for regulated pathways to tokenized exposure, especially in tokenized securities, asset-backed tokens, and other RWAs that promise enhanced liquidity and efficiency for traditional instruments.

RWAs and tokenization momentum

The market context for Redfearn’s appointment is favorable to Securitize’s business model. Data from RWA.xyz indicate a sustained surge in tokenized assets, with March totaling roughly $3.85 billion in distributed asset value across platforms. In parallel, tokenized stocks have crossed a notable threshold, with on-chain value exceeding $1 billion. These figures illustrate not only growing demand for tokenized access to mainstream assets but also the viability of regulated tokenization rails that can support larger, more diverse pools of capital.

For investors, the implication is twofold: first, tokenized RWAs offer a potential pathway to diversification and liquidity in traditional asset classes; second, the involvement of experienced financial-services executives in tokenization ventures could help drive scalable governance, risk controls, and compliance frameworks that appeal to institutions wary of regulatory uncertainty. Securitize’s leadership move aligns with a market that increasingly prioritizes both innovation and credible oversight as use cases expand beyond crypto-native tokens.

Regulatory backdrop and leadership reshuffle

Beyond Securitize’s leadership update, the regulatory environment is experiencing a notable transition. The SEC announced that David Woodcock would become director of the Division of Enforcement, with the appointment set to take effect on May 4. The change comes as the agency continues to navigate a contentious policy landscape for crypto-related enforcement, and as lawmakers press for clarity on how the SEC will approach recent crypto cases and policy shifts.

Interest among lawmakers centers on the departure of former enforcement head Margaret Ryan and questions about the SEC’s crypto crackdown strategy, including whether certain cases have been dropped or recalibrated. While authorities have pursued various actions against crypto firms and projects in recent years, the timing and rationale behind high-profile moves have drawn scrutiny from Capitol Hill. The broader takeaway for market participants is a heightened focus on how enforcement direction and regulatory priorities will shape project roadmaps, exchange behavior, and the permitting environment for tokenized assets.

In parallel, industry observers note how the movement of former regulators into crypto companies—such as Caroline Pham’s shift from the Commodity Futures Trading Commission to MoonPay—illustrates a broader willingness among policy veterans to contribute to, and influence, the sector’s development. This trend does not guarantee favorable policy outcomes, but it does signal a convergence of traditional financial governance with crypto innovation, potentially accelerating the adoption of clearer compliance standards and governance practices.

What this means for investors, builders and users

The confluence of leadership experience and tangible market momentum in RWAs points to a maturing segment of the crypto economy. For investors, the combination of seasoned governance acumen and regulatory-aware product design could translate into more credible access points to real-world assets, with improved risk management and reporting. For builders, Redfearn’s appointment may encourage the creation of more transparent issuance and custody solutions, along with stronger tokenization infrastructure that stands up to regulatory scrutiny. For users, the trend could translate into broader ranges of tokenized securities and asset-backed tokens that operate on trusted rails, delivering greater liquidity and on-chain settlement efficiencies.

That said, uncertainties remain. The regulatory posture toward crypto enforcement and the specifics of how RWAs will be treated under securities or commodities regimes will continue to influence product design, listing standards, and cross-border considerations. Market watchers should monitor how Woodcock’s leadership style translates into enforcement priorities and whether the SEC’s approach to complex asset-backed tokens evolves in a direction that reduces friction for compliant projects while preserving investor protections.

As the sector evolves, the next few quarters will reveal how these leadership movements translate into tangible policy signals, partnerships, and capital flows. Expect further commentary from industry participants on how tokenization platforms align with evolving regulatory expectations, and watch for any new data points that illuminate the pace of adoption among institutional participants seeking regulated exposure to tokenized real-world assets.

Readers should keep an eye on Securitize’s strategic execution under Redfearn’s presidency—especially initiatives around onboarding institutions, expanding the RWA toolkit, and advancing governance standards. Concurrently, any developments from the SEC’s enforcement division and congressional inquiries into crypto cases will help frame the risk and opportunity landscape for tokenized assets in the near term.

TLDR:

- Bitcoin continues trading below $72K after repeated rejection, keeping the market inside a tight consolidation range.

- On-chain data shows only 59% of the Bitcoin supply remains in profit, nearing levels seen during past bear markets.

- Traders watch $69,100 support and $72,000 resistance as key zones that could determine Bitcoin’s next move.

- Analysts note that extreme loss levels historically create accumulation opportunities before broader market sentiment improves.

Bitcoin continues to trade within a tight range below $72,000 as analysts track liquidity levels and momentum signals.

At the same time, on-chain data shows the share of BTC supply in profit falling toward levels last seen during previous bear cycles.

Bitcoin Faces Resistance Near $72K as Traders Watch Liquidity Zones

Bitcoin has struggled to maintain momentum above the $72,000 region during recent sessions. The market rejected this level again, keeping price action inside a narrow trading range.

Crypto analyst Lennaert Snyder discussed the setup in a post on X, noting that Bitcoin faced rejection near $72,000 again. As a result, he opened a small hedge short after the failed breakout attempt.

According to Snyder, liquidity around $66,590 remains a potential downside target this week. He also noted that the present zone offers poor risk-reward conditions for long positions.

The analyst explained that long setups may become attractive under two scenarios. One option involves Bitcoin reclaiming the $72,000 resistance zone. The other scenario involves a pullback toward the $69,100 level.

That area contains a four-hour imbalance and marks the lower edge of the recent trading range. If buyers regain control, Snyder expects liquidity around $74,800 to become the next weekly target.

Meanwhile, technical indicators still show moderate bullish momentum. The Relative Strength Index currently stands near 65, which signals steady buying pressure.

However, the indicator remains below the overbought threshold of 70. This suggests room for further upside if demand continues.

The Moving Average Convergence Divergence indicator also remains positive. The MACD line stays above the signal line, while the histogram shows weakening but positive momentum.

These signals suggest consolidation may continue before the next directional move develops.

On-Chain Data Shows Bitcoin Profit Supply Near Bear Market Levels

While price remains near recent highs, on-chain data presents a different picture of investor positioning.

CryptoQuant contributor Darkfost shared new data showing a drop in Bitcoin’s profit supply. The analysis estimates that around 59% of the circulating Bitcoin supply currently sits in profit.

This means nearly one Bitcoin out of every two remains held at a loss. The figure sits close to levels observed during previous bear market conditions.

Historically, the market tends to operate with a higher share of profitable supply. Data shows the long-term average sits closer to 75%.

The gap between current levels and the historical average shows that many investors entered positions at higher prices.

The data also identifies a key threshold around the 50% level. Previous bear markets often reached a bottom near that point. Although the current market has not reached that level, the trend suggests widespread unrealized losses across the network.

Darkfost explained that profitable supply plays an important role in sustaining market momentum. When investors hold gains, they are more likely to continue participating in the market. However, when losses dominate the supply distribution, sentiment often weakens.

For this reason, the analyst described the current environment as more suitable for accumulation strategies. Market participants often increase exposure during periods when losses reach extreme levels.

The strategy aims to position investors before broader market sentiment turns positive again. At the same time, exposure typically decreases when the share of supply in profit approaches 100%.

For now, Bitcoin remains within a defined price range while traders monitor resistance near $72,000 and support levels below $70,000.

The US inflation reading the market has been dreading arrives Friday morning when the Bureau of Labor Statistics releases the March Consumer Price Index at 8:30 AM ET, with economists widely forecasting it will be the hottest monthly inflation print since May 2022, driven almost entirely by the energy shock from the Iran war.

Summary

- Barclays Senior US Economist Pooja Sriram forecasts March headline CPI at 0.9 percent month over month and 3.3 percent year over year, “led by a surge in gasoline prices”; BofA Securities economists project a 10.6 percent monthly jump in energy prices driving a 0.9 percent headline increase; Oxford Economics projects headline CPI above 3 percent in March and above 4 percent in April

- The expected reading would mark a sharp reversal from the 2.4 percent annual inflation rate recorded in the first two months of 2026, and would be the first major inflation data to reflect the impact of the Iran war on consumer energy prices; Pantheon Economics says the US experienced the largest one-month jump in fuel costs since at least 1957

- Core CPI, which strips out volatile food and energy, is forecast to rise 0.3 percent monthly and 2.7 percent year over year, with the Federal Reserve expected to hold interest rates at 3.50 to 3.75 percent at its April 29 meeting; CME FedWatch shows 98.4 percent of respondents pricing in no change

As Kiplinger reported, “How much and how severely depends on just how long the conflict continues to crimp key energy exports. Some degree of inflation is now inevitable.” That framing captures the central tension in Friday’s release: whether the data confirms a one-month spike that fades as oil stabilizes, or signals the opening print of a new inflation regime where the Iran war has durably repriced transportation, manufacturing, and utility costs across the economy.

Consumers have already paid approximately $8.4 billion in additional fuel costs in the month after the Iran war started, according to an estimate from the Joint Economic Committee’s Democratic minority. Gasoline prices have averaged over $4 per gallon nationally, with oil remaining close to $110 per barrel even after the temporary ceasefire announcement caused a brief drop.

Since the post-2009 recovery, only five months have produced a monthly CPI reading of 0.9 percent or higher. Every one of them fell between October 2021 and June 2022, at the peak of the post-pandemic inflation surge. March 2026 is expected to join that short and painful list. The mechanism is straightforward: the Iran war disrupted oil flows through the Strait of Hormuz, the world’s most critical petroleum corridor, causing a supply shock that fed immediately into gasoline, diesel, and jet fuel prices. Energy costs then ripple into transportation, food distribution, and manufacturing, which is why Oxford Economics expects the headline rate to climb above 4 percent in April even after the temporary ceasefire.

What the Report Means for the Federal Reserve

The Fed had penciled in one interest rate cut for 2026 before the Iran war began. The war repricing of energy has caused many economists to remove that cut from their forecasts entirely. Austan Goolsbee, president of the Federal Reserve Bank of Chicago, warned that rising prices could pressure household budgets and derail spending. Some Fed policymakers signaled in March meeting minutes that future rate hikes may need to be considered if inflation accelerates further. Mark Zandi, chief economist at Moody’s Analytics, told CBS News: “We’re going to be paying the price for this through much of the year.”

What to Watch in the Numbers When the Report Drops Friday

As crypto.news has reported, bitcoin and crypto markets have been closely tracking every inflation signal in 2026, with the war-driven energy shock adding a new layer of uncertainty on top of existing tariff and monetary policy pressures. As crypto.news has noted, the March CPI release is one of the most anticipated economic events of the quarter for crypto investors because a number above 3.5 percent would likely extend the Fed pause and suppress the rate-cut narrative that has historically supported risk asset rallies. The report drops at 8:30 AM ET Friday, April 10.

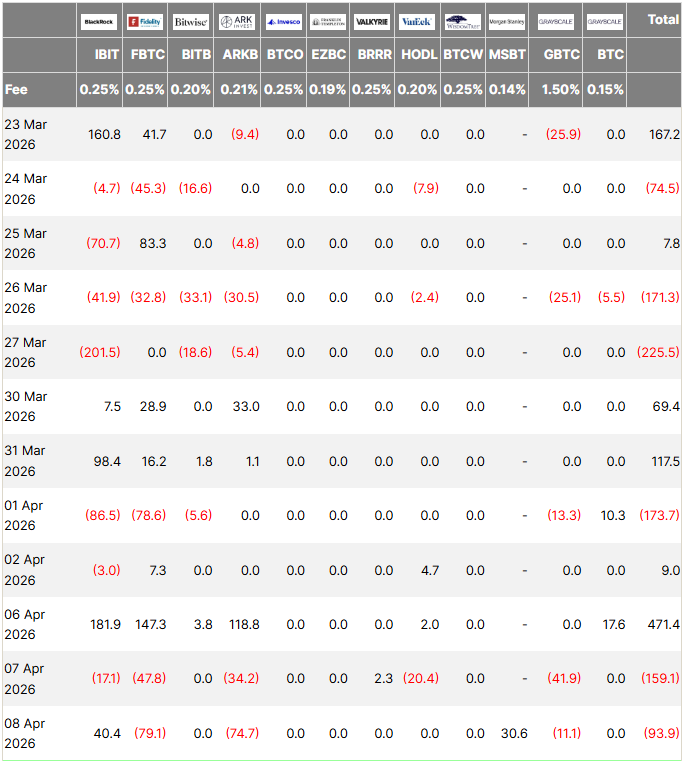

Morgan Stanley Bitcoin Trust (MSBT) launched on April 8 with a 0.14% expense ratio, making it the cheapest US spot Bitcoin ETF and undercutting BlackRock’s iShares Bitcoin Trust (IBIT) by 11 basis points.

Senior ETF analyst Eric Balchunas, however, does not expect BlackRock to respond with a fee reduction. His reasoning centers on IBIT’s liquidity advantage and dominant market position.

This ETF Expert Thinks Otherwise

MSBT pulled in approximately $30.6 million in net inflows on its first day and processed more than 1.6 million shares.

Balchunas placed the debut among the top 1% of all ETF launches. He has also projected $5 billion in AUM for MSBT within its first year.

Still, he made clear that IBIT’s position remains secure for now. IBIT holds roughly $55 billion in assets, making it by far the most liquid spot BTC ETF.

“Prob won’t see any cut from $IBIT. When you are King of the Hill with tons of liquidity, you have pricing power,” wrote Balchunas.

That liquidity moat gives IBIT tighter trading spreads and deeper options market activity, two factors that institutional traders weigh heavily when choosing a fund.

Fellow Bloomberg analyst James Seyffart echoed that view, noting it is unlikely MSBT will compete with IBIT on liquidity anytime soon.

Where the Pressure Falls

Balchunas warned that MSBT’s aggressive pricing could still trigger fee cuts elsewhere. Smaller issuers with less scale may be forced to lower their expense ratios to retain market share.

Because all spot BTC ETFs hold the same underlying asset, fees become one of the few differentiators. MSBT now sits one basis point below Grayscale’s Bitcoin Mini Trust at 0.15% and well below Fidelity’s Wise Origin Bitcoin Fund (FBTC) at 0.25%.

Morgan Stanley also brings a structural advantage most competitors lack. The bank’s wealth management arm employs roughly 16,000 financial advisors overseeing $9.3 trillion in client assets.

Those advisors can now recommend an in-house product rather than directing clients to third-party funds.

Balchunas identified only two scenarios that could force BlackRock to reconsider its pricing.

- The first would be sustained outflows from IBIT toward cheaper rivals.

- The second would be an entry from Vanguard at approximately 0.10%, though he assigned that outcome a 0.01% probability.

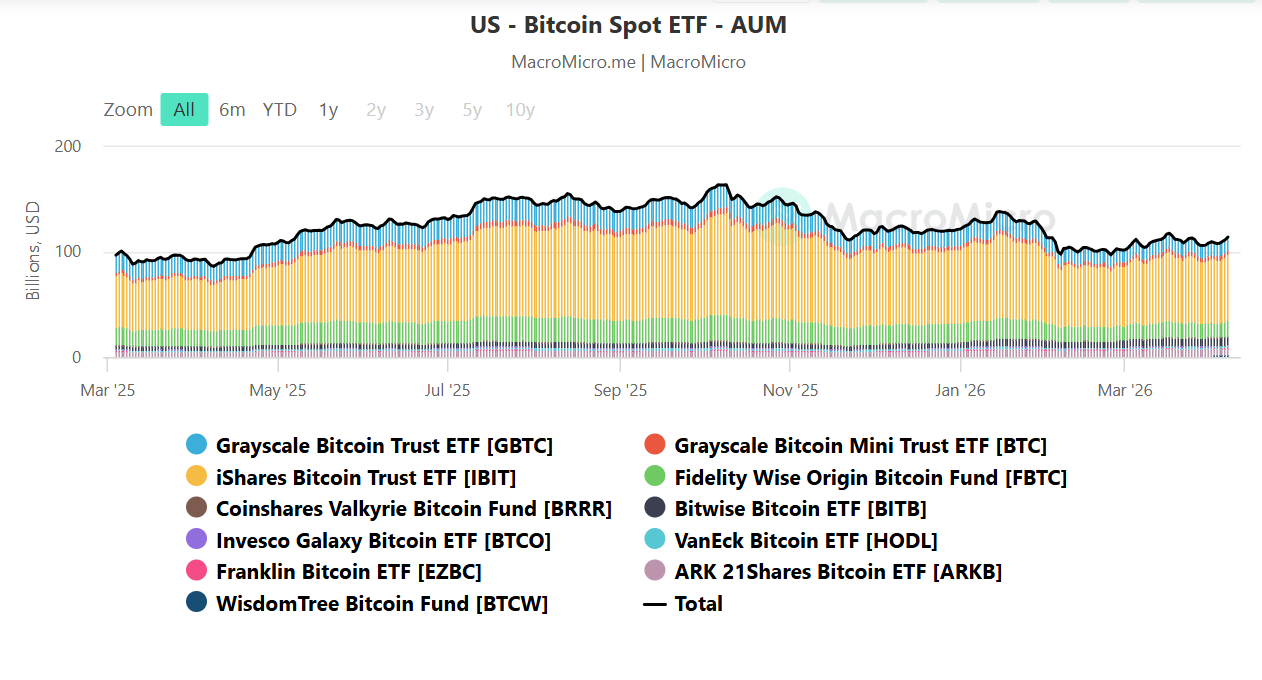

The US spot BTC ETF market has grown past $100 billion in cumulative assets since launching in January 2024.

However, 2026 started slowly, with four consecutive months of net outflows between November 2025 and February 2026.

March reversed that trend with $1.32 billion in inflows. Whether MSBT can sustain its opening momentum and capture a meaningful share of new flows will likely determine how seriously competing issuers treat its pricing signal.

The post 2 Conditions That Could Force BlackRock to Cut IBIT Fees After MSBT’s Undercut appeared first on BeInCrypto.

Binance Wallet has integrated predict.fun prediction markets and is sponsoring all gas fees for users on BNB Smart Chain.

Binance Wallet has integrated BNB Smart Chain-based predictfun as its official prediction market provider. Predictfun is backed by YZi Labs, formerly Binance Labs, the centralized exchange’s venture capital arm.

The integration allows Binance Wallet users to access prediction market functionality directly within the wallet interface without bearing transaction costs on the BNB network.

The move comes amid broader regulatory scrutiny of prediction markets in the U.S., including recent CFTC action seeking to enjoin Arizona from enforcing criminal and civil penalties against prediction market operators. Predictfun operates as a decentralized prediction market platform, and the Binance Wallet integration represents a major distribution channel for the protocol.

Sources: Binance Wallet

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Shortt & Kelly Break Irish Records in Bangor

New VENOM phishing attacks steal senior executives’ Microsoft logins

Appeals court judges question if Sean ‘Diddy’ Combs got too much prison time

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

Business5 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion4 days ago

Fashion4 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics7 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Crypto World12 hours ago

Crypto World12 hours agoCanary Capital Files SEC Registration for PEPE ETF

-

Politics6 days ago

Politics6 days agoThe UK should not pay a penny in slavery reparations

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

Business7 days ago

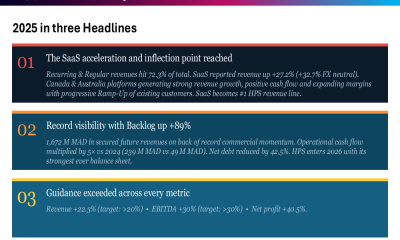

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion7 days ago

Fashion7 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

-

Fashion6 days ago

Fashion6 days agoFrugal Friday’s Workwear Report: Hammered Metallic Button Sweater Vest

You must be logged in to post a comment Login