Crypto World

From Crypto Treasury to RWA: ETHZilla Retreats and Relaunches as Forum Markets on Nasdaq

TLDR:

- ETHZilla rebrands as Forum Markets and begins trading under the Nasdaq ticker FRMM starting March 2, 2026.

- Shares collapsed roughly 96% from their August 2025 peak despite a 13.3% single-day gain on the rebrand news.

- Peter Thiel’s Founders Fund exited its 7.5% stake in Q4 2025 as ETHZilla’s Ethereum treasury strategy unraveled.

- Forum Markets shifts focus to regulated, tokenized real-world assets, moving away from single-asset crypto exposure.

ETHZilla is pulling back from its crypto-heavy balance sheet strategy after a dramatic share price collapse. The company announced a full rebrand to Forum Markets, with trading set to begin under the Nasdaq ticker “FRMM” on March 2.

The retreat follows months of investor exits, asset sales, and a sustained decline from last year’s highs. In place of Ethereum treasury holdings, the company is now directing its focus toward tokenized real-world assets built on regulated infrastructure.

ETHZilla Scales Back Crypto Holdings After Sharp Investor Exodus

ETHZilla built its identity around holding Ethereum directly on its balance sheet as a public company. The strategy was designed to give traditional investors exposure to Ethereum without directly purchasing the asset.

Shares soared to $107 on August 13, 2025, shortly after the company revealed plans for a $425 million Ethereum treasury. That announcement followed a pivot away from its earlier biotech business model.

The rally, however, proved short-lived as market conditions deteriorated and enthusiasm faded. The company began selling crypto assets to reduce its exposure as the stock continued sliding.

Investor confidence took a further blow when Peter Thiel’s Founders Fund exited its 7.5% stake during Q4 2025. Accounting for a 1-for-10 stock split executed in October, shares had fallen roughly 98% from their effective peak of $174.60.

The retreat from crypto exposure was gradual but deliberate. ETHZilla reduced its Ethereum holdings while exploring alternative business lines to shore up its equity performance.

One move included entering jet engine leasing through a new subsidiary called ETHZilla Aerospace. That unit tokenized equity in leased engines via the Eurus Aero Token I, deployed on the Arbitrum layer-2 network.

Shares climbed 13.3% to $3.91 on the day the rebrand was announced. Despite that recovery, the stock remains down approximately 96% from its August 2025 peak.

The single-day gain reflects cautious optimism around the company’s new direction. Whether that momentum continues under the Forum Markets name remains to be seen.

RWA Strategy Positions Forum Markets for a More Stable Model

The shift toward tokenized real-world assets marks a fundamental change in how the company plans to generate and sustain value.

Forum Markets intends to develop tokenized products backed by tangible assets using regulated infrastructure. That approach moves away from the volatility associated with holding large crypto positions on a public balance sheet. The aviation leasing venture offered an early preview of where the company is headed.

Vincent Liu, chief investment officer at Kronos Research, addressed the structural risks that drove the retreat. “Single-asset treasury strategies are highly dependent on strong market conditions and sustained equity premiums,” Liu told Decrypt.

He added that treasury-focused firms ultimately need revenue-generating businesses and broader asset exposure to remain relevant long term.

His comments reflect a broader concern within the industry about the sustainability of crypto-only balance sheet models.

Liu also pointed to specific weaknesses tied to Ethereum-focused strategies. He described the model as fragile, noting that its value is “tightly linked to network activity,” thereby creating “a correlation trap where purchasing power weakens during ecosystem downturns.”

Fragmentation across Ethereum’s base layer and its layer-2 networks further dilutes the overall narrative and premium.

He added that the model is “further undermined by the absence of a hard supply cap, leaving its long-term scarcity proposition open to question.”

Forum Markets is set to begin trading under the FRMM ticker on March 2, replacing the former ETHZ symbol on the Nasdaq Capital Market.

The rebrand draws a clear line between the company’s failed crypto treasury experiment and its new asset-backed direction.

The transition reflects a growing recognition that public companies cannot sustain themselves on crypto price appreciation alone. Building regulated, revenue-linked products appears to be the model Forum Markets is now betting on.

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Despite the wave of attention RWAs have received over the past couple of years, there’s a sense that everyone is waiting for something to shift. The problem is that many “tokenized” assets are still legal promises dressed up as tokens. Vague token rights, improvised custody and transfer controls, and servicing shortcomings make the whole thing still feel speculative. While the tokenised RWA market sits around $25B (which demonstrates serious growth), it’s still modest in comparison to global markets.

Summary

- Tokens aren’t titles: Many RWAs remain legal promises wrapped in blockchain rails. Without enforceable rights, controlled transfer, and servicing, tokenization stays speculative.

- The UAE is building the legal stack: Through DIFC, ADGM, and the Dubai Land Department, the UAE is treating tokenized real estate as regulated market infrastructure — not a crypto experiment.

- Rights beat throughput: The trillion-dollar RWA opportunity will go to jurisdictions that make token-holder rights unambiguous and enforceable, not to chains with the fastest settlement.

In Dubai, work on this is picking up. The Dubai Land Department has launched Phase II of its Real Estate Tokenization Project, with secondary-market resales scheduled to begin on 20 February 2026. In DIFC, the DFSA’s inaugural tokenization regulatory sandbox drew 96 expressions of interest. In short, the UAE is assembling the regulatory and institutional scaffolding needed to make tokenised real estate scalable – that’s certainly something worth talking about.

The crypto RWA fallacy

The best RWA pitch in crypto happens to be the simplest: take a deed, a fund share, or a receivable, put it on-chain, and let liquidity do the rest. In practice, that often means shipping a minting interface attached to a legal promise that lives somewhere else. The token trades 24/7, but the underlying rights don’t.

When markets tighten, everyone rediscovers the same truth: a token is not a title, nor a court order. Instead, it’s a digital representation recorded on a programmable platform – and it’s notoriously difficult to make it legally and operationally identical to what it claims to represent.

This idea shows up in three places. First, think about enforceability. If token holders can’t clearly understand what they own, what jurisdiction governs it, and how a claim is enforced, the idea of ownership is just branding. As a matter of fact, IOSCO warns that investors may not understand the legal aspects of ownership and transfer rights for tokenised assets, and flags legal uncertainty as a central risk holding back adoption.

Second, consider controlled transfer. Real assets don’t move like meme coins. Eligibility checks, transfer restrictions, and the ability to halt or reverse activity under lawful orders are not optional in institutional markets. OECD research notes that implementing restrictions like forced transfers or trading suspensions can be especially challenging on public, permissionless networks.

Third, there’s servicing. Real estate is an operating system: taxes, insurance, maintenance, tenant issues, distributions, valuations, reporting, audits. Tokenization can streamline records and transactions, but it doesn’t eliminate the admin layer that makes cash flows real and disclosures defensible. Until projects address these issues, RWAs are a bit stuck.

The UAE’s blueprint

If the UAE wins the real estate tokenization boom, it will be because it treated tokenization as a regulated financial product, a market-structure upgrade, and has built rules and institutions around that assumption.

- In DIFC, the DFSA launched a dedicated tokenization Regulatory Sandbox and drew 96 expressions of interest. This is an early indicator that serious firms are looking for a supervised pathway.

- In Abu Dhabi, ADGM has been explicit about positioning itself as a comprehensive regulatory home for digital assets, and it went further by introducing a DLT Foundations regime designed for token issuance and on-chain organisational structures.

- In 2025, the DIFC reported 8,844 active companies, demonstrating rapid year-on-year expansion.

- In Dubai, the Dubai Land Department is running a controlled pilot that explicitly tests governance, investor protection, and operational readiness while enabling secondary-market resale from 20 February 2026.

- The UAE also hosts pools of dry powder that can fund compliant issuance once the infrastructure is credible. Mubadala reported AED 1.2 trillion in assets under management, and Reuters notes Abu Dhabi’s major funds together manage around $1.7 trillion.

The UAE is building something of a regulatory SDK for RWAs — standardized rules, venues, and counterparties that make tokenized real estate deployable.

The winning stack

The projects that scale in the UAE are likely to be regulated market infrastructure that happens to use blockchain. Starting with licensing. In DIFC, the DFSA’s tokenization Regulatory Sandbox provides a supervised route where selected firms can test in a controlled environment and, if successful, transition toward full authorisation.

Next, the packaging has to be familiar. DIFC SPVs (Prescribed Companies) are designed to ring-fence and isolate assets and liabilities (something institutions already understand and can underwrite). Tokenization then simply becomes a distribution and settlement upgrade.

Then comes the hard constraint most crypto-native RWAs avoid – controlled transfer and custody. Institutional markets require governance, safe custody, and clear oversight. ADGM’s FSRA guidance is clear about addressing safe custody, market abuse, and related controls via a thorough regulatory framework.

Finally, the winning stack anchors to the registry. The Dubai Land Department is currently testing tokenization on title deeds within a regulated model, in collaboration with VARA, and moving into a phase that activates secondary resale under a controlled framework focused on governance and investor rights.

Put together, the archetype that wins looks license-first, SPV-based, compliance-native, and obsessed with issuance plus servicing.

The implication for crypto

Here’s the part crypto needs to internalize — the trillion-dollar RWA upside will be won by the players that can make token-holder rights unambiguous, transfers compliant, and cash flows serviceable at scale.

IOSCO makes a good point — investors can end up unsure whether they hold the underlying asset or merely a digital representation, with risks concentrated around legal structure and intermediaries rather than chain throughput.

That’s why the UAE matters to the broader market. The Dubai Land Department is running a controlled tokenization pilot that moves into secondary resale from 20 February 2026, framed around governance, operational readiness, and investor protection. DIFC’s regulator is doing the same at the market-structure level.

For crypto, the chain becomes the settlement, transparency, and automation layer (inside this regulated perimeter). It’s useful precisely because it is programmable, auditable, and interoperable. But pay attention to the jurisdictions and infrastructure providers building enforceable rights – that’s arguably more important right now.

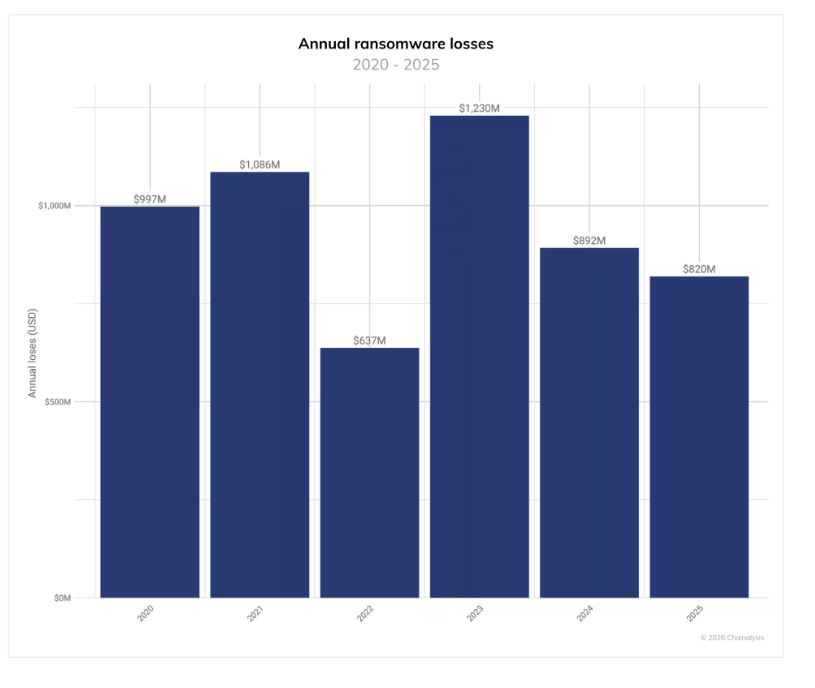

The number of ransomware attacks rose 50% in 2025 as hackers shifted their focus from large-scale attacks to small and medium-sized targets, according to blockchain analytics firm Chainalysis.

In an annual report published on Wednesday, Chainalysis said there were nearly 8,000 total leak events in 2025, a 50% increase from 2024. However, total on-chain ransom payments amounted to $820 million, marking an 8% decrease from 2024.

Chainalysis said increased regulatory scrutiny, enforcement actions targeting laundering network infrastructure, and a general refusal by big firms or organizations to pay ransoms all contributed to lower overall payments in 2025, forcing attackers to go after smaller targets.

“We’re seeing a structural shift in targeting: fewer large, headline-grabbing intrusions and more volume focused on small and medium enterprises. The assumption is simple — smaller victims pay faster,” eCrime.ch founder Corsin Camichel said in the report, adding:

“However, Chainalysis’ data shows payments trending downward despite an all-time high in public claims. That divergence is important. It suggests attackers are working harder for diminishing returns.”

Meanwhile, the increase in attempted attacks was attributed to a continued decline in the average “price for victim access” on the dark web, from $1,427 at the start of 2023 to $439 at the start of 2026.

A flood of cheap software and ransomware strains on the market, combined with AI integrations to streamline attacks, has resulted in increased output by hackers, Chainalysis said.

“We are seeing industrialized access pipelines, AI-assisted tooling, and a proliferation of infostealer logs that lower the barrier to entry, which has resulted in an oversupply of cheap but operationally constrained inventory that floods the market and depresses pricing.”

Hackers and scammers causing crypto chaos

Despite a modest reduction in blockchain ransomware payments last year, 2026 has kicked off with some big losses from crypto exploits and scams.

Related: Why address poisoning works without stealing private keys

According to a recent report from cybersecurity company CertiK, a whopping $370.3 million in crypto was stolen in January through exploits and scams. The lion’s share of funds was stolen via phishing scams, which accounted for $311.3 million.

Magazine: South Korea gets rich from crypto… North Korea gets weapons

Crypto markets are in retreat during U.S. morning hours on Thursday, rapidly reversing yesterday’s strong gains.

Just under $67,000, bitcoin has pulled back more than 4% after touching $70,000 late on Wednesday. Ether (ETH) and solana (SOL) are showing similar declines.

The selloff comes alongside a 2% decline in the Nasdaq following Nvidia’s (NVDA) earnings last night. While Nvidia didn’t disappoint, investors are selling the news after the stock’s sizable run higher into the earnings event. NVDA is lower by 4.8%, with related names like Broadcom (AVGO), Micron (MU) and Intel (INTC) also sharply lower.

Curiously, the software names are nicely higher today, with the Software Sector ETF (IGV) ahead more than 2%. Bitcoin’s correlation with this embattled group has been well documented, but to BTC bulls’ chagrin, they apparently only move together when IGV heads lower.

A check of stocks finds Coinbase (COIN) down 1%, Strategy (MSTR) down 2.3%, and Galaxy Digital (GLXY) down 3%. Outperforming is stablecoin issuer Circle Financial (CRCL), up another 3.3% today, and bringing its two-day post-earnings advance to about 40%.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

As the Crypto Fear and Greed Index plummets, Bybit is doubling down on stablecoin yield and fixed-income-style products to help users generate steady returns amid volatility.

While the Crypto Fear and Greed Index plunges to historic lows and Bitcoin pulls back sharply from its highs, the crypto exchange Bybit is expanding new opportunities, strengthening fixed-income-style products.

“We believe stability is what our users want most right now,” said Helen Liu, Co-CEO at Bybit. “The market will recover, we have no doubt about that. But in the meantime, our job is to help ease the pressure, offer real opportunities to earn stable income, and make sure our community knows that Bybit is right here with them.”

The company is accelerating access to stablecoin yield opportunities and capital-efficient tools designed to help users preserve value and earn predictable returns during uncertain times.

“We want to find every opportunity for our users to earn stable income,” said Helen. “Whether it is on-chain yield through Mantle Vault or capital efficiency through BYUSDT, the goal is the same, make every dollar work harder so that our community can weather this period with less stress and more confidence.”

Bybit believes the current market is also revealing a deeper structural change in investor behavior. They stated that this cycle is different, and that users are not chasing 100x returns, they are looking to protect capital and generate sustainable yield. Bybit reiterates that the shift is structural, not emotional.

Bybit will roll out up to $10 million in fixed-income opportunities backed by stablecoins, giving users more ways to earn predictable returns during volatile markets.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Circle stock price popped by over 35% on Wednesday, its best day since going public, after publishing stronger revenue and USDC stablecoin growth than expected.

Summary

- Circle stock price soared after publishing strong financial results on Wednesday.

- Canaccord Genuity analysts maintained a bullish outlook for the stock.

- They slashed their CRCL stock target to $160, a 93% upside from the current level.

Circle Internet Group jumped to $83, its highest level since January 15, and 66% above its lowest level this year. This surge boosted its market capitalization to nearly $20 billion.

Canaccord Genuity slashes Circle stock forecast

Analysts at Canaccord Genuity, a firm with more than $110 billion in assets under management, maintained the bullish view on the company, even as they reduced the price target. They slashed their Circle stock forecast by 35% from $247 to $160.

In a note, the analysts praised Circle for another solid quarter in which its stablecoin holdings and revenue jumped. Its stablecoins in circulation rose by over 100% to $75 billion, a figure that Circle expects to have a CAGR of over 40%.

Canaccord Genuity also identified other potential catalysts. The most notable one is Circle Payment Network, which aims to disrupt how money moves globally.

Instead of using the expensive and time-consuming Swift network, banks and other fintech companies can use its stablecoin-powered platform. CPN costs are negligible, while transactions are completed in seconds. Its annualized volume has jumped to over $5.7 billion, with 55 institutions in the network.

Most notably, Circle is building Arc, its layer-1 network, which has attracted hundreds of developers. Canaccord believes that CPN will ultimately run on Arc, leading to higher revenues in the future.

Circle named the “Switzerland of stablecoins”

Additionally, Canaccord believes that Circle is the “Switzerland of Stablecoins” since stablecoins are its only business, and that USDC is the biggest GENIUS-Act compliant coin. As such, it can gain more adoption from companies seeking to leverage stablecoins to cut transaction costs. The report added:

“The launch of competitive stablecoins from eCommerce or financial services giants could be more problematic in terms of their widespread adoption. For example, would Amazon really want to accept WalMart’s stablecoin?”

Meanwhile, John Todaro, a top Needham analyst, slashed Circle’s target from $190 to $130, while William Blair reiterated its outperform rating on the stock. The consensus estimate among Wall Street analysts is $131, up by about 57% above the current level.

Vitalik Buterin has outlined a four-pronged plan to harden Ethereum against quantum threats, identifying four areas most vulnerable: validator signatures, data storage, user account signatures, and zero-knowledge proofs. As headlines spotlight quantum risk across crypto, including discussions around Bitcoin (CRYPTO: BTC) and other chains, the Ethereum co-founder argues that a careful, long-horizon upgrade path is essential. In a Thursday post, he described a roadmap that hinges on selecting a post-quantum hash function for all signatures—an issue that could determine the network’s security stance for years. The discussion echoes prior proposals, including Justin Drake’s Lean Ethereum idea proposed in August 2025.

Key takeaways

- Buterin identifies four pillars for quantum resistance: validator signatures, data storage, user account signatures, and zero-knowledge proofs, framing a holistic upgrade rather than piecemeal fixes.

- The plan contemplates replacing the current BLS signatures with lean, quantum-safe hash-based signatures, with the choice of hash function carrying long-term implications for the network.

- Data storage would transition from KZG to STARKs, a move that aims to preserve verifiability while enhancing quantum resistance, albeit with significant engineering work ahead.

- User accounts would shift from ECDSA toward signatures compatible with lattice-based, quantum-resilient schemes, though heavier gas costs are a concern.

- A long-term solution centers on protocol-layer recursive signatures and proof aggregation to keep on-chain verification costs in check, potentially enabling vast scalability for quantum-resistant proofs.

- The conversation nods to ongoing research, including ETHresearch discussions on recursive-STARK approaches and the broader Strawmap effort to accelerate finality and throughput.

Sentiment: Neutral

Market context: The push toward quantum-resistant primitives sits against a backdrop of ongoing network upgrades and a broader move toward scalable zero-knowledge proofs, with developers weighing security, efficiency, and long-term viability as they plan multi-year transitions.

Why it matters

The four-pronged approach to quantum resistance is more than a theoretical exercise; it signals how Ethereum intends to preserve user trust as quantum threats loom on the horizon. If effective, a hash-based signature layer could become the de facto standard for post-quantum security, shaping how users interact with wallets, smart contracts, and validator participation for years to come. The decision on the hash function is particularly consequential: once a standard is chosen, it tends to anchor the protocol for a generation, influencing tooling, hardware requirements, and compatibility with future cryptographic advances.

On data storage, the plan to replace KZG with STARKs reflects a subtle shift in cryptographic assumptions. STARKs are lauded for being quantum-resistant and transparent, but integrating them into Ethereum’s data availability and verification stack would demand substantial engineering effort, optimization, and rigorous security audits. Buterin has framed it as “manageable, but there’s a lot of engineering work to do.” The move would balance the need for robust post-quantum guarantees with the practical realities of a live, globally used network.

Account signatures represent another frontier. Ethereum currently relies on ECDSA, a staple of today’s cryptographic ecosystem. Moving to a system that can accommodate lattice-based or other quantum-safe schemes may impose heavier computational loads and gas costs in the near term. Yet the long‑term payoff could be a network that remains secure even as quantum computing capabilities grow. Buterin points to a longer-term fix—protocol-layer recursive signature and proof aggregation—that could dramatically reduce gas overheads by verifying many signatures and proofs within a single frame. If realized, that approach could unlock scalable, quantum-resistant transactions without sacrificing usability.

A central theme across the discussion is the balance between immediate practicality and enduring security. Quantum-safe signatures are not a cosmetic upgrade; they alter core data paths, from how validators validate blocks to how users sign transactions and how proofs are verified. The blockchain community increasingly recognizes that a “one-size-fits-all” cryptographic choice may not suffice; instead, a layered strategy—where traditional primitives coexist with post-quantum alternatives and where recursive techniques optimize verification—could define Ethereum’s security posture for years to come.

Beyond the cryptographic specifics, the conversation is anchored in ongoing academic and developer experiments. For example, researchers have explored recursive-STARK concepts to compress bandwidth and computation, including discussions on a bandwidth-efficient mempool that leverages recursive proofs. This line of inquiry mirrors Ethereum’s broader push toward scalable, verifiable computation that remains tenable in a post-quantum world. The discussion also nods to real-world upgrade planning, such as Lean Ethereum, which Justin Drake proposed in August 2025 as a pragmatic framework for accelerating quantum readiness without destabilizing current operations.

In parallel, governance and roadmap conversations continue to unfold within the Ethereum Foundation and the wider developer community. Buterin’s own posts have highlighted expectations that progress on “Strawmap” could yield progressive decreases in both slot time and finality time, signaling a more agile path to security without sacrificing decentralization or user experience. The architecture changes under consideration—ranging from signature schemes to data verification protocols—must harmonize with these operational expectations to minimize disruption while maximizing resilience against quantum-era threats.

What to watch next

- Updates on Lean Ethereum: Any formal milestones or testnet deployments that demonstrate practical quantum-ready components in action.

- Hash-function selection for post-quantum signatures: The criteria, security proofs, and network-wide implications of choosing a long-term standard.

- Progress toward STARK-based data storage: Engineering roadmaps, performance benchmarks, and on-chain verification strategies.

- Adoption of lattice-based or alternative signatures for user accounts: Changes to wallets, client libraries, and tooling compatibility.

- Implementation of recursive signatures and proof aggregation: Realistic timelines, gas impact assessments, and potential protocol changes needed to support such a paradigm.

Sources & verification

- Vitalik Buterin’s quantum-resistance roadmap post and related discussions: https://x.com/VitalikButerin/status/2027075026378543132

- Lean Ethereum proposal by Justin Drake: https://cointelegraph.com/news/justin-drake-proposes-lean-ethereum

- Headlines about quantum threats to Bitcoin: https://cointelegraph.com/news/saylor-says-quantum-threat-to-bitcoin-is-more-than-10-years-out-expects-coordinated-global-upgrade-if-risk-emerges

- Quantum-resistant data storage and STARKs vs KZG discussion: https://cointelegraph.com/news/vitalik-details-roadmap-for-faster-quantum-resistant-ethereum

- Ethereum Foundation quantum gas‑limit priorities and protocol considerations: https://cointelegraph.com/news/ethereum-foundation-quantum-gas-limit-priorities-protocol

- Strawmap and related timing expectations: https://cointelegraph.com/magazine/bitcoin-7-years-upgrade-post-quantum-bip-360-co-author/

- Recursive-STARK mempool concept: https://ethresear.ch/t/recursive-stark-based-bandwidth-efficient-mempool/23838

Ethereum’s quantum resilience roadmap: four frontiers and the road ahead

Ethereum’s path to quantum resistance, as articulated by Buterin, centers on four pivotal domains: validator signatures, data storage, user account signatures, and zero-knowledge proofs. The proposal calls for replacing the current Boneh-Lynn-Shacham (BLS) consensus signatures with a lean, hash-based, post-quantum alternative. The selection of the hash function is underscored as a long-term decision, potentially locking in an approach for years to come. This shift aims to preserve the integrity of validator operations while mitigating the risk that quantum computers could break current signatures used to attest to blocks and transactions.

In parallel, the data layer would transition away from KZG-based storage to STARKs, a move designed to maintain verifiability under quantum pressure. Buterin notes this is a technically manageable transition, yet it requires substantial engineering effort to integrate seamlessly with Ethereum’s existing data availability and verification mechanisms. If realized, the change would address a core vulnerability by ensuring that data proofs remain verifiable even in a quantum era, without compromising network performance.

On user accounts, the plan envisions a broader compatibility with signature schemes beyond ECDSA, including lattice-based approaches that resist quantum attacks. The practical challenge here is gas consumption: quantum-safe signatures tend to be heavier to compute, which could elevate gas costs in the near term. The longer-term payoff, though, would be a network able to function securely even when advanced quantum hardware becomes capable of breaking traditional cryptographic keys. To counterbalance the added computational load, Buterin points to a protocol-layer solution—recursive signature and proof aggregation—that could dramatically reduce on-chain gas overhead by consolidating verification work into master frames that validate thousands of signatures or proofs at once.

Quantum-resistant proofs pose another cost hurdle, motivating the same aggregation strategy. Instead of individually verifying every signature and proof on-chain, a single, compiled structure—an overarching validation frame—would authorize thousands of sub-validations in a single operation. This approach could reduce the per-transactions verification burden to near-zero costs in practice, enabling a scalable model for post-quantum proof workloads. The narrative echoes ongoing research, including discussions around a recursive-STARK-based bandwidth-efficient mempool, which envisions more efficient data flow and validation under heavy workloads.

Finally, the Strawmap discussions hint at a broader tempo for the network upgrade. Buterin and researchers anticipate incremental improvements in slot times and finality, signaling a measured cadence for upgrading cryptographic primitives without triggering disruptive forks. The convergence of these threads—signature upgrades, data storage shifts, and aggregation-based efficiency—paints a future where Ethereum (ETH) remains secure and usable as quantum capabilities advance. The dialogue around these topics reflects a mature, evidence-based approach to governance and engineering, balancing theoretical security with the practicalities of a live, billions-of-dollars ecosystem.

Happy Thursday, advisors!

In today’s newsletter, David Lawant, head of research at Anchorage Digital reviews crypto’s evolving role in 401(k)s, as regulatory clarity is poised to open up investments.

Then, in Ask an Expert, Kevin Tam answers questions about crypto adoption around the world looking at the recent 13F filings.

Happy Reading.

Modernizing the nest egg: the past, present, and future of crypto in 401(k) plans

The United States retirement system is about to reach a structural inflection point. For over a decade, the $10 trillion 401(k) market remained insulated from crypto assets due to regulatory ambiguity and litigation concerns. However, a decisive shift in federal policy is transforming 2026 into the year of integration, which in the long term will move crypto from the periphery into the institutional core of the American retirement system.

The regulatory shift from “extreme care,” to “principled neutrality,” to “democratizing access.”

The Department of Labor (DOL) is responsible for making sure that ERISA, the 1974 federal law that sets minimum standards for most voluntarily established retirement and health plans in private industry, is at the epicenter of this issue. In March 2022, it issued Compliance Assistance Release No. 2022-01. This release created a de facto ban on crypto assets in retirement plans by mandating that fiduciaries exercise “extreme care” and threatening targeted investigations for those engaging with crypto assets.

On May 28, 2025, the DOL formally abandoned the “extreme care” standard with the Compliance Assistance Release No. 2025-01. This release formally rescinded the restrictive 2022 guidance, stating that the previous stance had “deviated from the requirements of ERISA” and the department’s “historically neutral, principled-based approach”. The rescission re-established the legal standard set by the Supreme Court which holds that fiduciaries must act prudently based on a contextual evaluation of risk and return, rather than adhering to categorical bans on specific asset classes.

But the real catalyst came with President Donald Trump’s Executive Order 14330, signed on August 7, 2025. Titled “Democratizing Access to Alternative Assets for 401(k) Investors,” this directive fundamentally redefined the government’s stance, shifting from a cautionary tone to an affirmative mandate for facilitating access to “alternative assets,” which the order explicitly defined to include crypto assets among more established classes such as private equity and real estate.

Upcoming DOL guidance on alternative assets and what adoption could look like

This past January, the DOL submitted a proposed rule that would clarify its position on alternative assets and the appropriate fiduciary process. The document is not public yet and is still sitting with the Office of Management and Budget (OMB), but given that the 180-day White House deadline has already expired, there is expectation that it could be released for public comment quite soon.

For crypto specifically, attention hinges on the design of the upcoming fiduciary safe harbor. This regulatory ‘’checklist’ is intended to immunize fiduciaries from liability for investment losses, provided specific standards are met. Its critical pillars are expected to include qualified custody requirements, liquidity constraints and portfolio allocation caps.

Even after the major regulatory hurdle is cleared, however, broad adoption will likely unfold more akin to a glacial shift over several years than like a speculative spark.

The evolution from high-friction Self-Directed Brokerage Accounts (SDBAs) toward seamless inclusion in core menus and Target Date Funds relies on myriad critical factors, including fiduciary buy-in and platform compatibility. Investment consultants like Mercer, Aon and Willis Towers Watson serve as critical gatekeepers, and although they tend to move cautiously, allocation to alternatives is emerging as a top-of-mind issue. Simultaneously, the industry must bridge the gap between legacy ‘mutual fund plumbing’ and digital asset infrastructure to ensure 401(k) platforms can seamlessly handle the new asset class.

Still, the 401(k) market is critical not only due to its sheer size but also because of its unique flow profile acts as a mechanical volatility dampener. Because retirement participants are price-inelastic, their bi-weekly, non-discretionary payroll contributions provide a stabilizing bid that persists regardless of short-term market sentiment. This effect is reinforced by managed accounts and target-date funds (TDFs), which institutionalize “buying the dip” by automatically purchasing assets during market corrections to restore target weights.

Unlike the high-velocity debut of spot exchange-traded funds (ETFs), the move into retirement accounts will likely be an accumulating wave that will build over years. Yet the sheer size and unique stability of this investor base make 2026 the year crypto’s role in the American nest egg became an undeniable, permanent fixture.

– David Lawant, head of research, Anchorage Digital

Ask an Expert

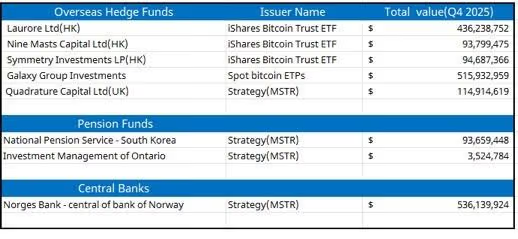

Q: What do Norges Bank and overseas hedge funds have in common?

Overseas hedge funds from Hong Kong and the UK are showing a massive appetite for regulated exposure, heavily accumulating spot bitcoin ETFs to build their portfolios. Laurore Ltd. has newly emerged with a 100% portfolio concentration IBIT.

In Pension fund growth, South Korea’s National Pension Service increased its MSTR exposure to $93.6 million, far outpacing the $3.5 million position held by Investment Management of Ontario (IMCO).

In Q4, the Central Bank of Norway opened a new position of MSTR valued at $536 million.

Q: Is Canada’s bitcoin bet starting to cool off?

National Bank of Canada cut its stake in MSTR by 51% in Q4 2025, reducing shares simultaneously with the stock’s price drop. The bank’s position dropped from $659 million to $152 million in this quarter. Notably, the bank also holds $52.4 million in put options on MSTR.

Q: What does the global regulator roadmap tell us about bitcoin’s trajectory into 2026 and beyond?

The direction is towards legalization. Regulatory timelines show a coordinated global build-out with MiCAR implemented across the EU in June 2025, the GENUIS Act signed in the US in July 2025, and HK, Singapore andthe UAE all establishing formal digital asset frameworks. Looking further, Canadian Securities Administrators are expected to propose amendments enabling broader tokenization of securities and ETFs in Q4 2026.

Driven by regulatory clarity and the continued adoption of digital asset ETFs, institutional investors view them as strategic assets for diversification and long-term growth.

– Kevin Tam, digital asset research specialist

Keep Reading

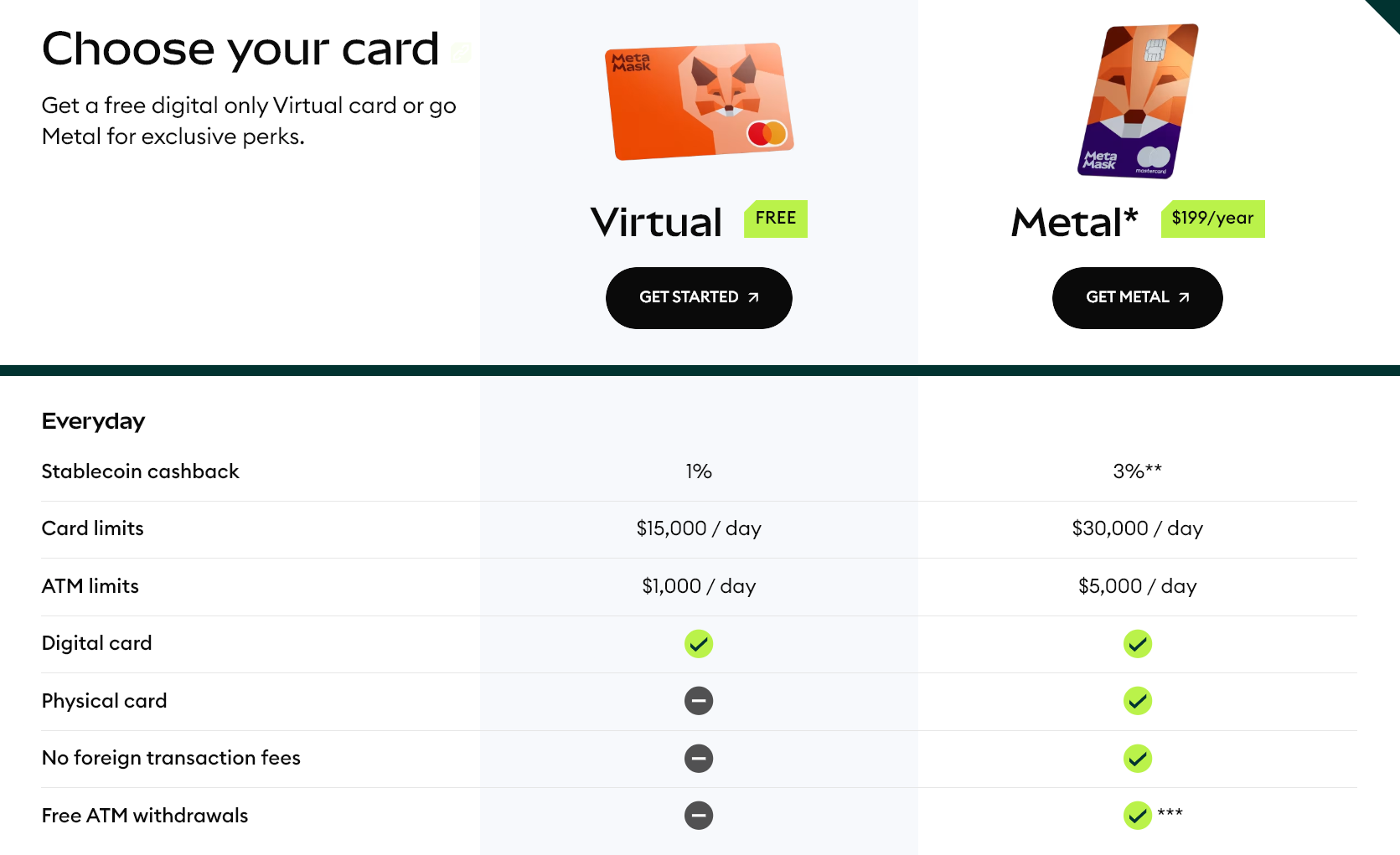

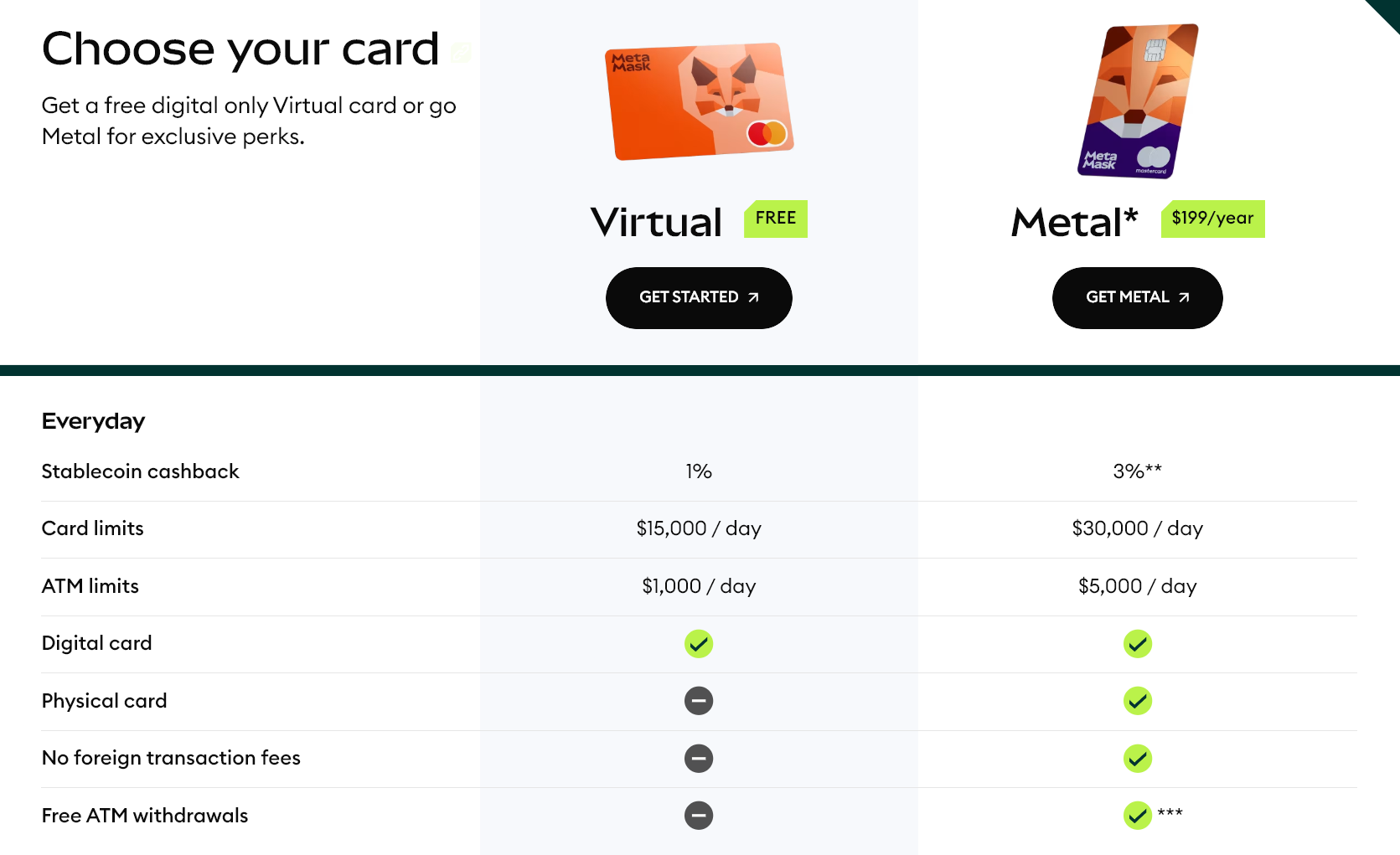

MetaMask has partnered with Mastercard to launch a new payment card program in the United States that links spending to on-chain rewards. The rollout includes a Virtual Card users can start with immediately and a MetaMask Metal Card available for pre-order.

The card is also available to New York residents, a notable inclusion given the state’s tighter posture toward crypto-linked financial products.

MetaMask says the Metal Card offers 3% cashback on the first $10,000 of spend, zero foreign transaction fees, and additional benefits tied to a new rewards program.

US Residents Can Now Earn On-Chain Points Via Mastercard

MetaMask’s new rewards layer turns everyday activity—transfers, transactions, and card spending—into points.

Users can redeem those points for ecosystem perks such as discounts, token allocations, and early access opportunities.

Unlike older crypto card models that often rely on holding funds on an exchange, MetaMask frames this card as an extension of a self-custody wallet experience. Users manage assets through MetaMask, while the card lets them pay through Mastercard’s merchant network.

The launch highlights how wallet providers now compete directly in payments. Crypto products are using rewards to keep users inside their ecosystem rather than pushing them toward centralized platforms.

At the same time, the model still depends on intermediaries. Users should also consider practical frictions: crypto-to-fiat conversion at checkout can create taxable events, and fees, limits, eligible tokens, and network support can shape the real value of “cashback” in day-to-day use.

MetaMask’s card push lands as major payment networks and fintech partners race to make stablecoins and on-chain balances spendable at mainstream merchants.

Gate Technology gains MFSA PSD2 license, expanding EU payment and stablecoin services.

Summary

- Gate Technology Ltd, Gate.com’s Malta-based entity, obtained an MFSA Payment Institution license under PSD2, making it one of few crypto-native firms with this approval in Europe.

- The firm previously secured a MiCA license for exchange and custody, and will now passport PSD2 rights to roll out compliant payment services and fiat–Web3 rails across the EU.

- Gate reports over 30–36m registered users and ranks among the top three global spot exchanges by volume and liquidity, underlining the scale of its regulated expansion push.

Gate Technology Ltd, the Malta-based entity of cryptocurrency exchange Gate, has obtained a Payment Institution license under the European Union’s Second Payment Services Directive (PSD2) from the Malta Financial Services Authority (MFSA), the company announced.

The license places Gate among crypto-native companies in Europe to secure this level of regulatory approval, according to the announcement.

Giovanni Cunti, CEO of Gate Technology Ltd, stated the license positions Gate to build infrastructure between traditional finance and Web3, delivering compliant payment solutions to clients across Europe. Cunti noted the license establishes a foundation for future financial services and provides regulatory certainty for institutional and retail clients in the European market.

The development follows Gate’s earlier regulatory achievements in Malta, where the company previously obtained a Markets in Crypto-Assets (MiCA) license to provide exchange and custody services, according to the announcement.

Gate’s compliance strategy spans multiple jurisdictions including Malta, Cyprus, the Bahamas, Japan, Australia, and Dubai, the company reported.

The PSD2 license enables Gate to expand payment services across the European Union through passporting rights, according to the announcement. The license allows Gate to integrate traditional finance mechanisms with Web3 applications.

Gate was founded in 2013. The company’s flagship platform, Gate.com, serves over 49 million users globally and ranks among the top three crypto exchanges worldwide by market share, according to company data.

The announcement included a disclaimer stating the content does not constitute an offer, solicitation, or recommendation, and that Gate may restrict or prohibit services for users from restricted regions.

U.S. demand for Bitcoin has strengthened as pricing data shows a shift in exchange dynamics. The Coinbase Premium Index has turned positive after nearly two months in negative territory. The move signals renewed domestic appetite as Bitcoin rebounds from recent weakness.

Bitcoin Premium Turns Positive on Coinbase

The Coinbase Bitcoin Premium Index has moved back into positive territory after weeks of discount pricing. The shift reflects higher Bitcoin prices on Coinbase compared with Binance. Market data shows the spread has widened to around $10 in favor of Coinbase.

This pricing difference indicates stronger demand on the U.S.-based exchange. Analysts from CryptoQuant highlighted the change and linked it to institutional flows. They noted that Coinbase Advanced remains a preferred venue for large-volume trading.

Ein leises Signal aus den USA, aber genau das ist oft entscheidend. 🤔

Das Coinbase Premium Gap ist wieder positiv. Das heißt: Bitcoin wird auf Coinbase leicht teurer gehandelt als auf Binance. Aktuell liegt der Aufschlag bei rund 10 Dollar. Das gilt als Hinweis auf… https://t.co/Gz19M9cS5Z

— MissCrypto (@MissCryptoGER) February 25, 2026

The premium had stayed negative for almost two months before this reversal. During that period, Bitcoin faced persistent selling pressure across global exchanges. However, the recent positive reading suggests improved sentiment within the U.S. market.

Bitcoin has faced a difficult start to the year despite periodic rallies. The asset has declined about 24% since January and remains far below its peak. It currently trades near $67,151 after gaining nearly 6% within 24 hours.

The all-time high of $126,198 still stands as a distant benchmark. Despite the rebound, Bitcoin remains roughly 47% below that record level. Even so, the latest premium data suggests renewed domestic accumulation.

Market participants interpret the premium as a demand gauge rather than a price guarantee. A positive reading often signals stronger buying activity in the United States. However, analysts stress that the metric alone does not confirm a sustained trend reversal.

Quantum Risk and Market Structure Influence Outlook

Research from CoinShares has addressed concerns around quantum computing risks. The firm estimates that quantum threats to Bitcoin remain at least 10 to 20 years away. It also expects developers to implement protective measures through protocol upgrades.

The report suggests that network participants would likely adopt soft fork solutions. Such changes could strengthen cryptographic security before quantum risks materialize. Therefore, long-term structural risk appears limited under current projections.

Beyond technological concerns, liquidity conditions continue to shape price action. Spot Bitcoin exchange-traded funds have influenced market flows in recent months. Large issuers have adjusted holdings in response to demand and redemption patterns.

BlackRock has periodically reduced Bitcoin exposure within its ETF products. These sales have added an intermittent supply to the market. Consequently, price momentum has faced additional resistance during recent rallies.

Futures market data also reflects elevated selling pressure. Bears have maintained dominance in derivatives positioning over recent weeks. This activity has coincided with a three-month high in aggregate selling pressure.

Despite these headwinds, the premium shift indicates improving domestic sentiment. The U.S. market often acts as a liquidity anchor during volatility. Therefore, sustained positive premiums could support price stabilization.

Binance Pricing and Global Exchange Dynamics

Binance pricing has remained slightly below Coinbase levels during the recent shift. This gap has reinforced the positive Coinbase Premium Index reading. The difference highlights regional demand imbalances across exchanges.

Global liquidity fragmentation often creates short-term arbitrage opportunities. Traders respond quickly to pricing inefficiencies between major platforms. However, persistent spreads typically reflect broader regional sentiment trends.

The current premium suggests stronger spot accumulation within the United States. At the same time, international markets show more balanced demand conditions. This divergence has shaped recent intraday price behavior.

Bitcoin’s rebound followed several sessions of downward pressure earlier in the week. Buyers entered the market after prices approached short-term support zones. As a result, momentum indicators have improved modestly.

The asset’s 24-hour gain has helped restore confidence after extended consolidation. Trading volumes have also increased alongside the price recovery. Higher turnover supports the view of renewed engagement on U.S. exchanges.

While the premium alone cannot define the next trend, it provides directional context. Sustained positive readings often align with constructive price phases. Therefore, the market now assesses whether domestic demand can offset broader structural pressures.

Bitcoin continues to trade below its historical peak despite the recent uptick. Nevertheless, exchange-based metrics now signal a potential shift in demand balance. Market participants will assess whether this dynamic can extend the ongoing recovery.

Anthropic boss rejects Pentagon demand to drop AI safeguards

Real estate tokenization’s missing layer

Team Edo Crowned Champions at 2nd Niger Delta Games

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports3 days ago

Sports3 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics3 days ago

Politics3 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business2 days ago

Business2 days agoTrue Citrus debuts functional drink mix collection

-

Politics4 hours ago

Politics4 hours agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business4 days ago

Business4 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Tech2 days ago

Tech2 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat1 day ago

NewsBeat1 day agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat1 day ago

NewsBeat1 day agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech4 days ago

Tech4 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat4 days ago

NewsBeat4 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics5 days ago

Politics5 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

NewsBeat2 days ago

NewsBeat2 days agoPolice latest as search for missing woman enters day nine

-

Crypto World2 days ago

Crypto World2 days agoEntering new markets without increasing payment costs

-

Business24 hours ago

Business24 hours agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Business7 hours ago

Business7 hours agoOnly 4% of women globally reside in countries that offer almost complete legal equality