Crypto World

HYPE Hits New All-Time High as BTC, ETH, and XRP Rebound: Weekend Watch

After losing roughly $8,000 in just over a week, bitcoin’s price finally rebounded in the past day after more promising developments on the US-Iran peace front.

Most altcoins have followed suit, helping the total crypto market cap regain over $80 billion since yesterday’s low.

BTC Jumps Toward $77K

As mentioned above, the primary cryptocurrency dumped hard in the past 10 days or so, driven by different factors, such as the bleeding ETFs, investor exodus, and rising geopolitical tension. It dumped below $78,000 last weekend and fell to $76,000 a few days later.

After an unsuccessful rebound attempt on Wednesday and Thursday that was stopped at $78,000, the bears took complete control on Friday and especially Saturday morning, driving bitcoin south to just over $74,000. This became its lowest price position in May, and it arrived after a new set of threats from Trump against Iran.

However, the two sides actually made significant progress on a potential permanent peace deal, as announced by the POTUS himself. This resulted in an immediate price uptick for BTC that drove it to just over $77,200 earlier today before it was stopped. Nevertheless, it still trades inches below $77,000, and its market cap has recovered to $1.540 trillion on CG.

Its dominance over the alts has also remained above 58% after a brief dip yesterday.

HYPE New ATH

Aside from yesterday’s brief crash to $55, HYPE has been the undisputed leader in market performance over the past few weeks. Its gains only intensified today as it posted a fresh all-time high of over $63.

Ethereum defended the $2,000 level and has risen past $2,100 after a 4.5% daily surge. BNB is back to $660, while XRP has reclaimed the $1.35 resistance. SOL is up to $87, ZEC is back to $645, and more gains are evident from CC, XLM, SUI, AVAX, TAO, and others.

Even more substantial double-digit increases come from WLD, NEAR, MORPHO, ONDO, and QNT.

The total crypto market cap has added over $80 billion since yesterday’s low and is up to $2.650 trillion on CG.

The post HYPE Hits New All-Time High as BTC, ETH, and XRP Rebound: Weekend Watch appeared first on CryptoPotato.

Key Highlights

- Shares of Take-Two Interactive climbed more than 6% following Rockstar Games’ announcement that GTA VI preorders begin June 25.

- Rockstar confirmed a November 19, 2025 release date, bringing clarity after multiple delays.

- Piper Sandler maintains an Overweight rating with a $280 target, forecasting over 45 million units sold initially.

- CEO Strauss Zelnick projects FY2027 net bookings between $8 billion and $8.2 billion.

- Official box art revealed by Rockstar generated significant buzz across social platforms.

Shares of Take-Two Interactive (TTWO) rallied over 6% Thursday following Rockstar Games’ confirmation that Grand Theft Auto VI will be available for preorder starting June 25, ahead of its November 19 launch. The stock traded near $241.74 during afternoon hours.

Take-Two Interactive Software, Inc., TTWO

Rockstar made the announcement through its verified X account, simultaneously unveiling the game’s retail box artwork. The reveal quickly gained traction online.

For market watchers, this preorder timeline represents more than just a marketing milestone. It provides concrete evidence that the November launch window remains on track — a crucial signal following years of uncertainty and postponements.

The road to GTA VI’s release has been turbulent. Originally targeted for 2025, the launch was subsequently delayed to mid-2026, then pushed again to November 2026. When that final postponement was revealed, TTWO shares tumbled nearly 18% in a single trading day.

By announcing preorders five months before launch, institutional investors are interpreting this as strong indication that additional delays are unlikely.

The franchise’s previous installment debuted in 2013. That represents thirteen years of accumulated anticipation, and market data supports the magnitude of this buildup.

Wall Street’s Expectations

Piper Sandler maintained its Overweight stance on TTWO with a $280 price objective. Their analysis suggests GTA VI could move more than 45 million copies in its initial release period.

To put this in perspective, GTA V generated over $1 billion in sales during its first three days in 2013 and has delivered more than 200 million units lifetime — establishing it as the most successful entertainment launch ever.

FactSet consensus estimates point to Take-Two generating $8.6 billion in revenue for the fiscal year concluding next March, representing a 27% increase from fiscal 2026.

CEO Strauss Zelnick has provided guidance for FY2027 net bookings in the $8 billion to $8.2 billion range.

Preorder Window Opens Late June

The June 25 preorder availability will span PlayStation 5 and Xbox Series X|S digital platforms, alongside physical reservation options at leading retailers globally.

The game’s cultural impact is already extending beyond the gaming sector. Burger Motorsports, an automotive parts retailer, announced it will shut down operations on November 19 — the GTA VI release day — describing it as “an unprecedented cultural event.”

TTWO remains down approximately 6.9% for the year and roughly unchanged over the trailing twelve months. Preorder metrics in the weeks ahead will provide investors with better visibility into whether consumer demand aligns with market expectations.

Strategy's STRC preferred stock extended its slide to a fresh record low on Thursday, deepening the discount on one of the main channels the largest corporate bitcoin holder uses to fund its purchases. The Variable Rate Series A Perpetual Stretch Preferred Stock, known as STRC, traded near $85 on… Read the full story at The Defiant

- Hyperliquid (HYPE) holds a strong uptrend with all major EMAs stacked bullish.

- HYPE price is testing $75.62 resistance after the recent all-time high move.

- RSI neutral at 62, leaving room for a continued momentum move.

HYPE has remained one of the strongest-performing digital assets in recent weeks as growing activity on the Hyperliquid ecosystem continues to attract attention across the crypto market.

The token recently climbed to a new all-time high of $76.70 before pulling back slightly to around $72.50 at the time of writing.

Despite the retracements, HYPE is still up more than 30% over the past seven days and more than 52% over the last month.

The rally comes at a time when Hyperliquid is reporting record levels of trading activity, revenue generation, and derivatives market participation.

Hyperliquid revenue growth continues to accelerate

Hyperliquid’s revenue growth has emerged as one of the biggest talking points surrounding Hyperliquid in 2026.

The platform has generated more than $1.16 billion in cumulative revenue, placing it among the highest-earning crypto protocols in the market.

The growth has been driven by rising trading volumes across its perpetual futures markets, which have attracted both retail traders and large institutional participants.

Notably, trading activity has remained strong throughout the year, with the DEX recording approximately $1.38 billion in 24-hour trading volume, while total value locked on the platform has climbed to roughly $6.38 billion.

The strong revenue figures are particularly notable because they come as Hyperliquid continues expanding beyond its original crypto-native derivatives business, with new markets tied to equities, commodities, indices, and pre-IPO assets broadening the platform’s reach and creating additional sources of trading activity.

Hyperliquid’s open interest surpasses $6 billion

Another major milestone arrived when Hyperliquid’s total open interest crossed $6 billion on June 14.

This places Hyperliquid among the largest perpetual futures venues globally and highlights the platform’s growing influence within the derivatives market.

Earlier in the year, Hyperliquid controlled around 8.3% of global perpetual futures open interest, demonstrating how quickly it has gained market share against established competitors.

HYPE price outlook

While the Hyperliquid price action has cooled slightly from its recently reached all-time high, the broader structure still points to a market that is holding a strong upward trend rather than reversing it.

On the technical side, the short-term setup remains firmly positive.

A majority of the technical indicators are bullish.

Oscillators are showing a buy bias, while moving averages are fully aligned on the upside.

The token is trading above all major daily exponential moving averages (EMAs), including the 10-day, 20-day, 50-day, 100-day, and 200-day EMAs.

This type of full EMA stack typically reflects sustained trend control by buyers rather than short-lived momentum.

The RSI (14) sits at 62, which places it in neutral territory with a slight upward tilt.

The RSI is not in overbought conditions, meaning there is still technical room for continuation if momentum returns.

However, price is now approaching a key decision area, and a daily close above the first major resistance at $75.62 would be required for HYPE to enter the next phase of price discovery.

But if the market becomes overbought and pulls back, the key structural support is positioned at $56.50.

A break below $56.50 would represent a meaningful shift in the current bullish structure.

BNB has fallen nearly 5% as uncertainty surrounding Binance’s European regulatory status collides with a risk-off move across crypto markets ahead of the EU’s MiCA enforcement deadline.

Summary

- BNB fell nearly 5% as uncertainty around Binance’s MiCA approval weighed on sentiment.

- Spot Bitcoin and Ethereum ETFs recorded fresh outflows as traders adjusted to a hawkish Fed outlook.

- Technical indicators place key support at $582-$585, with a breakdown risking a move toward $556.

According to data from crypto.news, Binance Coin (BNB) dropped to around $576 on June 18 after reports suggested Binance’s path toward a Markets in Crypto-Assets license (MICA) remains unresolved, less than two weeks before the European Union’s July 1 compliance deadline.

The decline unfolded alongside a broader crypto selloff that pushed total market capitalization down nearly 3% to $2.18 trillion, while Bitcoin slipped below $63,000 following a hawkish Federal Reserve outlook.

The regulatory backdrop has become a new source of concern for BNB holders. According to a report from The Big Whale, European Central Bank President Christine Lagarde has opposed Binance’s entry into the EU market, raising questions about whether the exchange can secure authorization before the transition period expires.

Without MiCA approval, exchanges may be forced to halt services for EU clients or withdraw from certain jurisdictions.

Meanwhile, institutional demand across the crypto market has weakened. Data from SoSoValue showed U.S. spot Bitcoin ETFs recorded net outflows of $82.16 million, while spot Ethereum ETFs lost another $29.37 million. The withdrawals arrived as traders reassessed expectations for interest rates after Federal Reserve officials projected fewer rate cuts and left the door open to tighter policy if inflation remains elevated.

Oil markets have provided little relief. Although crude prices have retreated from recent highs following developments in U.S.-Iran negotiations, investors continue to weigh the risk that geopolitical tensions could reemerge and complicate the inflation outlook.

Higher-for-longer rates have historically weighed on speculative assets, including exchange-linked tokens such as BNB.

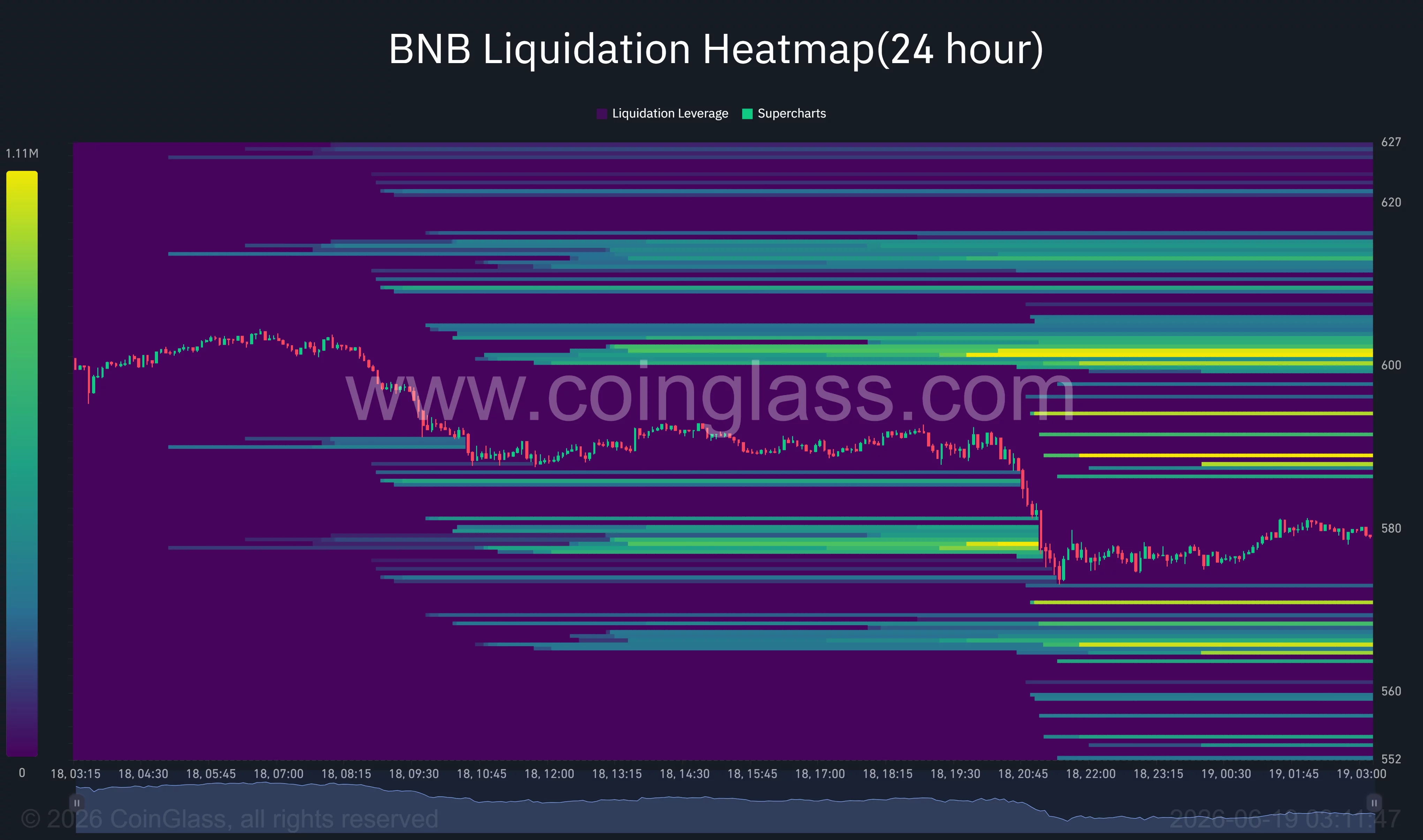

BNB technical structure keeps focus on key $585 support zone

The daily chart shows BNB trading below its Supertrend resistance near $661 after failing to reclaim momentum during several recovery attempts since February. BNB price remains trapped near the lower end of its multi-month range, while the daily RSI has fallen to around 38, its weakest reading since early April, highlighting persistent selling pressure.

On the four-hour chart, BNB recently broke below a descending trendline that had connected lower highs since late May. The selloff pushed the token toward the 100% Fibonacci retracement level near $556, calculated from the late-May rally that peaked around $745. Immediate resistance now sits near the 0.786 retracement at $597, followed by stronger supply zones around $629 and $651.

According to analyst Umair Orazkay, the $585-$600 region remains the most important area for bulls to defend.

“The number is psychological as well as is around the same area where the low of the range sits, so defending the $585-$600 area for BNB is very important as couple of closings below this can trigger a panic sell off.”

Liquidity data suggests traders are closely watching the same levels. CoinGlass liquidation heatmaps show one of the largest nearby leverage clusters concentrated around the $600 mark, with additional short liquidations stacked between $620 and $627. A recovery into those zones could trigger a squeeze, while continued weakness may attract fresh downside volatility.

A break below demand support could expose lower liquidity pockets

Another group of traders remains focused on a demand zone slightly below current prices. Commenting on the recent structure, crypto analyst Mr Bullish argued that BNB has begun forming higher highs and higher lows following June’s rebound and identified the $582-$585 region as a critical support area for buyers.

The bullish thesis weakens considerably if that demand zone fails. A decisive move below $582 would place the June low and the Fibonacci support near $556 back into focus.

Below that level, liquidation heatmaps show relatively thinner liquidity until the mid-$550 region, increasing the risk of a sharper move lower if sellers regain control.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

ADA – the native token of Cardano – has been hit hard by the ongoing bear market, while recent concerning statements from co-founder Charles Hoskinson have only worsened its condition.

And as holders cling to hopes of a much-needed rebound, some factors indicate that a deeper drop may be approaching.

Fasten Your Belts

The asset has been in a major decline over the past several months, and the widespread crypto crash at the start of June further accelerated its downturn. ADA slipped well below $0.15 (its lowest level since late 2020) and currently trades around $0.16 (per CoinGecko’s data).

Its market capitalization has dwindled to just north of $6 billion, putting the token at real risk of losing its prestigious position among the top 20 cryptocurrencies.

Market conditions remain unfavorable, and Hoskinson’s recent comments, paired with growing weakness across the ecosystem, are only adding to the pressure. Just several days ago, Cardano’s co-founder sparked panic in the community when he said he’s “taking a break” and warned of an upcoming “wave of failures in the ecosystem.”

Meanwhile, the X account BSCN revealed that ADA’s daily trading volume, which climbed to $6.3 billion in August 2025, has recently tumbled to a mere $500 million. This trend suggests fading interest in the asset, which could hamper any chance of a meaningful recovery.

Popular analyst Ali Martinez presented another concerning development. He claimed that ADA has been forming a bearish flag since the beginning of the month and is now breaking from the structure.

“Now that Cardano has reached the $0.17 support level, the odds have significantly increased for a bigger price correction towards $0.13,” he added.

The Bullish Case

Still, not everyone is pessimistic about ADA’s short-term future. X user Sssebi recently noted that the asset reached its most oversold level (on the weekly chart) in its entire history. That said, they expect a resurgence to above $0.20 within the coming weeks. Crypto with Haris ₿ also chipped in, opining that ADA’s downfall shouldn’t be seen as the end but as an opportunity.

“Back in 2023, ADA went from around $0.22 to $1.30 in just a few months. Maybe history repeats itself. Maybe it doesn’t. But if the next bull run comes, I wouldn’t be surprised to see Cardano make another crazy move,” the X user reminded.

The post Cardano’s Meltdown: Is ADA at Risk of Further Decline? appeared first on CryptoPotato.

Malta’s financial regulator has taken a step toward defining how decentralized finance (DeFi) and decentralized autonomous organizations (DAOs) could fit into Europe’s existing crypto rulebook. In a public discussion paper opened on June 12, the Malta Financial Services Authority (MFSA) proposes a potential legal framework for “software-based organizations,” a category intended to cover DAOs and other DeFi entities governed through software.

The consultation runs until July 10 and is explicitly tied to the European Union’s Markets in Crypto-Assets (MiCA) regime. While the MFSA acknowledges that truly decentralized services may fall outside MiCA, its paper argues that many DeFi projects still have elements that complicate any claim of full decentralization—creating uncertainty about who would be accountable under financial regulation.

Key takeaways

- The MFSA opened a DeFi consultation on June 12 under the EU’s MiCA framework, inviting industry feedback until July 10.

- The regulator suggests treating DAOs as a type of “software-based organization,” separating legal rules for the entity from rules for the underlying protocol.

- MFSA emphasizes MiCA’s exclusion for fully decentralized models, but says many DeFi systems retain centralized features that raise regulatory accountability questions.

- The push for clearer DeFi treatment aligns with broader EU work—including a European Central Bank paper and a European Commission MiCA review launched in May.

Why Malta is proposing a “software-based organization”

In its discussion paper, the MFSA frames a central regulatory challenge: MiCA does not neatly describe how governance and responsibility should work when a financial activity is coordinated through code rather than a traditional corporate structure. Rather than attempting to create a completely standalone legal concept for DAOs, the MFSA’s approach is more structural—defining DAOs and similar arrangements as “software-based organizations.”

According to the paper, this would allow regulators to focus on the legal characteristics of the organization using software governance, while keeping the rules for the underlying protocol and software distinct. The goal is to address a practical question for compliance and supervision: if governance is executed through decentralized mechanisms, who—if anyone—should be considered responsible for regulated activities and outcomes?

MFSA also underlines that MiCA’s scope is not meant to capture every kind of decentralized arrangement. The paper states that “MiCA excludes fully decentralised models from its regulatory scope,” adding that projects without intermediaries or central control may not need to comply with MiCA. The issue, in the MFSA’s view, is that many real-world DeFi projects do not convincingly meet that standard.

DeFi governance remains a scrutiny flashpoint in the EU

Malta’s consultation is arriving during a period of intensified EU attention to whether and how decentralized systems should be regulated under MiCA. Earlier in the year, a European Central Bank working paper examined governance and control across four major DeFi protocols and found that control remained highly concentrated. While the ECB analysis does not automatically determine MiCA applicability for every protocol, it added evidence to the argument that “fully decentralized” may be the exception rather than the rule in large DeFi markets.

That emphasis on governance structure continued in May, when the European Commission launched a targeted review of MiCA. The review sought feedback on several issues, including stablecoin interest payments and the treatment of DeFi—along with whether gaps in the framework justify further regulation.

Against this backdrop, Malta’s MFSA paper can be read as an attempt to convert a persistent policy debate into a workable legal taxonomy. If regulators cannot reliably distinguish fully decentralized services from arrangements with meaningful centralized influence, the burden falls on the market to anticipate which compliance obligations might apply.

Not everyone wants a second DeFi-focused rulebook

Even as Malta works on a DeFi-specific discussion framework, broader EU commentary suggests there is disagreement about whether DeFi requires its own separate regulatory track. In remarks reported earlier to Cointelegraph, European Commission adviser Peter Kerstens argued that policymakers should prioritize integrating tokenization into a broader digital asset framework rather than pursuing a “second version” of MiCA aimed specifically at DeFi.

That perspective highlights a tension within the EU approach: one camp believes decentralized finance needs clearer, DeFi-tailored treatment to address accountability and governance realities; another argues that tokenization and other digital asset developments are already broad enough for one coherent framework, reducing the need for a dedicated DeFi layer.

Malta’s “software-based organization” concept sits somewhere between these positions. It does not create a completely separate system from MiCA, but it does attempt to refine how key actors—especially DAOs—could be legally recognized so that MiCA’s responsibilities can be applied consistently when decentralized projects are not truly decentralized in practice.

What the MFSA’s proposal could mean for DeFi projects

For DeFi teams and governance stewards, the MFSA consultation raises a question that goes beyond legal vocabulary: how will regulators evaluate decentralization in ways that determine oversight and accountability?

By separating the legal framework governing the organization from the rules governing the protocol and software, the MFSA is implicitly pointing to a compliance model built around governance participation, decision-making authority, and the existence (or absence) of intermediaries. That approach could affect how projects document governance processes, define roles for contributors or administrators, and structure decision rights—especially where token holders, developers, or other groups retain meaningful influence.

At the same time, the MFSA’s emphasis on MiCA’s exclusion for fully decentralized models signals that the distinction will still matter. If a project can credibly demonstrate the absence of central control and intermediaries, it may argue it falls outside MiCA’s scope. If it cannot, the proposed legal categorization could make compliance planning more concrete—though it also suggests regulators may be looking closely at control concentration, not just the presence of governance tokens.

Whatever the final outcome, the consultation process itself is likely to be influential. By requesting input from the industry until July 10, the MFSA is effectively setting up a negotiation over definitions and boundaries: what exactly constitutes a “software-based organization,” and when does a DAO cross from a decentralized arrangement into something that demands traditional regulatory accountability?

For now, market participants should watch the submissions coming into Malta’s consultation and pay attention to how EU institutions continue to treat governance concentration and decentralization tests under MiCA—because the direction Malta is taking suggests regulators may increasingly rely on organizational accountability, not just code, when deciding whether DeFi fits within existing financial rules.

For the first time in seven years, the Irish government released an assessment related to digital assets, noting risks from money laundering, terrorism financing, sanctions violations and bribery.

The government of Ireland is taking aim at digital assets used in money laundering and terrorism financing as it moves to implement industry standards “relating to the acceptance of crypto-related activities as a source of funds” by the second half of 2027 as part of its policy priorities.

In part of its implementation plan following a national risk assessment released on Thursday, the Irish department of finance said crypto assets presented “very significant” risks related to money laundering and terrorism financing. The government’s 2026 report was the first time in seven years that Ireland released a risk assessment related to digital assets, noting an increase in prosecutions related to money laundering and incidents of fraud in which using crypto was “particularly attractive” to criminal groups.

Source: Government of Ireland

In the time since its last report, Ireland noted that crypto “presents vulnerabilities that may facilitate sanctions evasion,” presented challenges to the country’s tax compliance and enforcement and was used to bribe corrupt officials responsible for decisions overseeing the industry. The government highlighted vulnerabilities in the sector, including “inconsistent international regulation” posing risks to Irish service providers and largely unregulated areas of the industry such as decentralized finance.

Ireland lacks many of the laws and regulations covering the crypto industry that are common in other jurisdictions like the European Union and United States. That’s despite its relatively high crypto ownership rates compared to other areas, with the Central Bank of Ireland reporting in December that about 10% of the population invested in crypto.

Related: BitGo courts crypto firms awaiting MiCA approval amid Binance licensing concerns

In November 2025, the central bank fined Coinbase Europe Limited about $24 million for Anti-Money Laundering and Countering the Financing of Terrorism violations, noting that the company delayed reporting failures in its transaction monitoring system.

Ireland banned crypto political donations

The risk assessment noted concerns about crypto being “increasingly used to make payments to corrupt officials,” but even official donations to political groups has been banned in Ireland for more than four years. In April 2022, officials proposed that no Irish political parties be allowed to accept cryptocurrencies like Bitcoin, Ether, privacy coins and others.

Magazine: OpenAI files for IPO, SEC scraps 611 rule and Hungary overhauls crypto: Hodlers Digest June 7-13

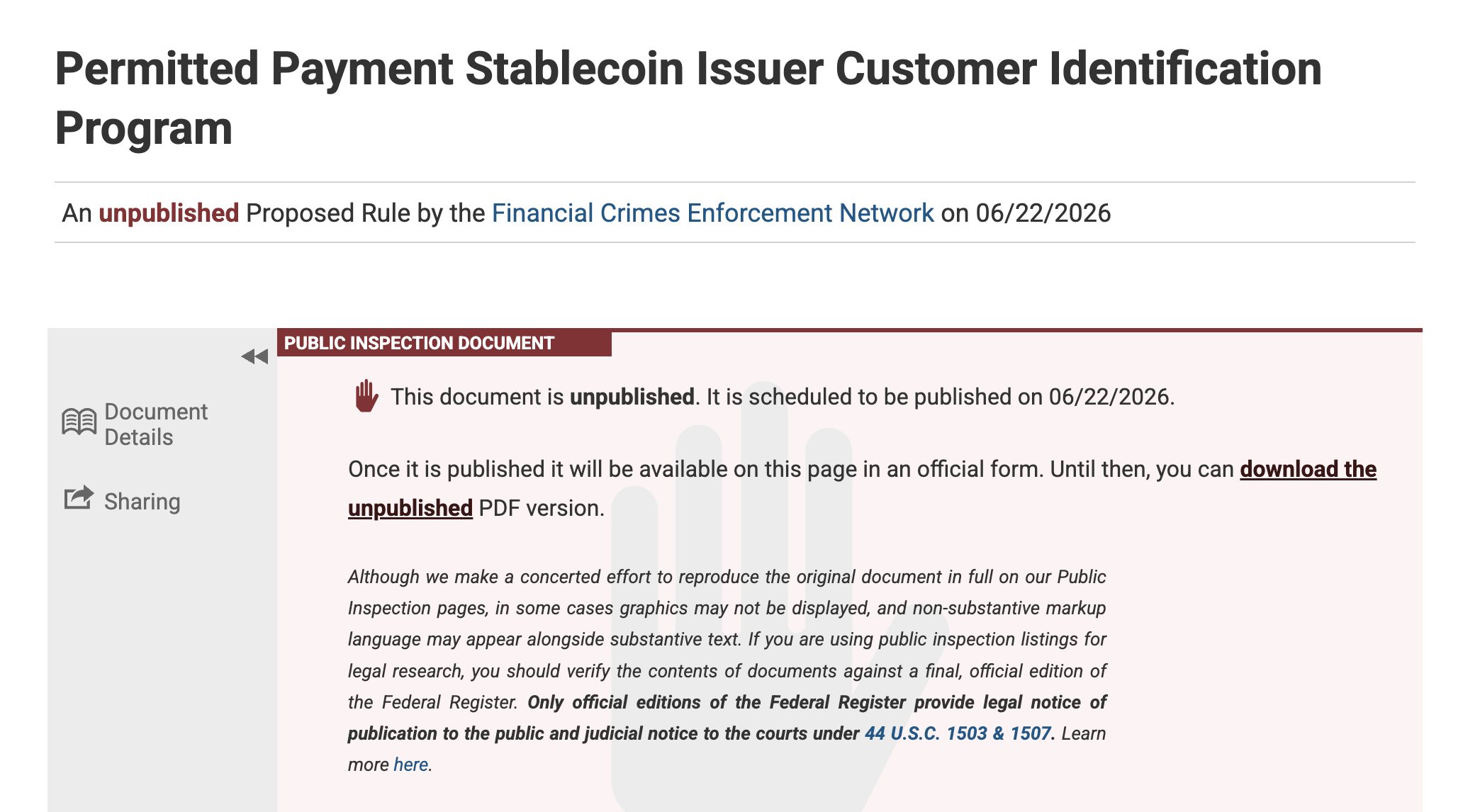

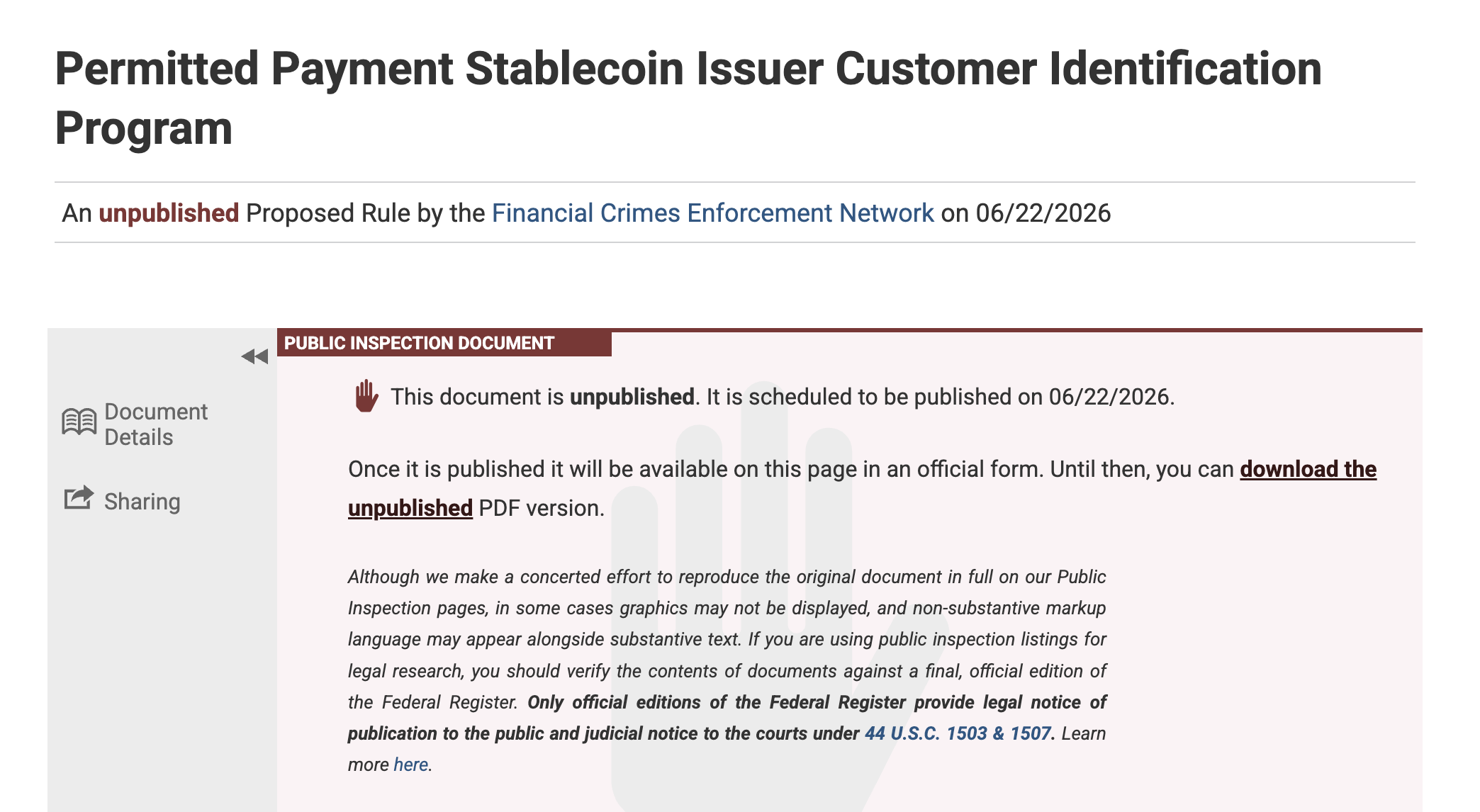

Several US government agencies responsible for financial regulation have issued a proposed rule as part of the implementation of stablecoin-focused legislation, pushing for similar identification guidelines for issuers as banks under federal law.

The Federal Deposit Insurance Corporation (FDIC), Federal Reserve, Office of the Comptroller of the Currency (OCC), National Credit Union Administration and the US Treasury’s Financial Crimes Enforcement Network (FinCEN) on Thursday proposed that stablecoin issuers be treated as regulated financial institutions in regard to verifying users’ identities. The proposed rule comes as part of the implementation of the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, signed into law in July 2025.

Source: Federal Register

The proposed rule, which will be open to public comment for 60 days after it is officially filed in the US Federal Register on Monday, is intended to address Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) requirements for stablecoin providers through the GENIUS Act.

The minimum standards under the Bank Secrecy Act for financial institutions — potentially applied to stablecoin issuers under GENIUS — include “verifying the identity of any person seeking to open an account,” maintaining records of that information, and determining if the individual is a suspected terrorist or part of any terrorist organization.

The agencies’ actions were the latest implementation related to GENIUS, largely championed by US stablecoin issuers. The law is expected to go into effect 18 months after it was signed or 120 days after federal authorities finalize regulations for implementation.

Related: Banking group asks for more time to comment on US stablecoin bill

Treasury has already proposed AML and CFT requirements targeting illicit finance under GENIUS. In April, the FDIC suggested that rules providing insurance for corporate deposits of stablecoin issuers not extend to holders.

GENIUS passed, CLARITY still being weighed

After the passage of the GENIUS Act last year, the US Congress still has no defined timeline on addressing the Digital Asset Market Clarity (CLARITY) Act, a bill intended to redefine financial agencies’ roles in regulating and enforcing crypto rules.

While many in the White House and Congress expect the bill to pass by the August recess, concerns voiced by Democrats over potential conflicts of interest from lawmakers and elected officials could slow progress.

Magazine: The end of anon? AI could unmask crypto’s hidden identities

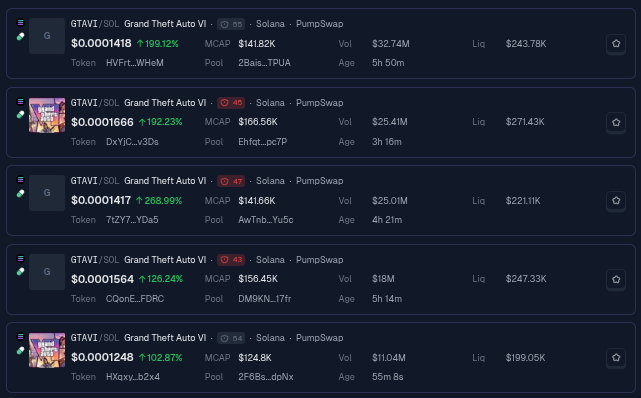

Rockstar Games officially confirmed that Grand Theft Auto VI pre-orders will begin on June 25. The announcement sent GTA 6 and Rockstar-themed meme coins skyrocketing across crypto markets within hours.

Here is what Rockstar Games confirmed, why the meme coins exploded, and what investors should track before any potential pullback.

Why the GTA 6 Pre-Orders News Sparked a Frenzy

Pre-orders are early purchases that gamers can place before a video game title’s official release date. Rockstar Games confirmed that Grand Theft Auto VI pre-orders will officially open on June 25 across all major platforms and global digital storefronts.

The announcement reignited massive hype around what is already considered one of the most anticipated game launches in history.

GTA 6 has dominated gaming conversations for years. Moreover, the long wait between the original announcement and the release has intensified retail attention.

Crypto markets reacted within minutes. GTA 6 and Rockstar-themed meme coins surged sharply across multiple decentralized exchanges, especially on Solana, Ethereum, and BNB Chain.

The speculative rally reflects how gaming narratives consistently fuel meme coin volatility cycles.

Traders quickly piled into tokens with names referencing the game, its characters, and the fictional Vice City setting.

Several previously dead tokens reached multi-week highs as social media amplified a buying frenzy across crypto communities worldwide.

The reaction follows a familiar pattern. Whenever major entertainment events approach, themed meme coins typically experience parabolic moves driven by retail FOMO. As a result, traders chase quick gains tied to the cultural relevance of the underlying brand.

What Investors Must Know About These Meme Coins

Despite the explosive moves, Rockstar Games has not released any official tokens. Every meme coin riding the GTA 6 hype is a community-driven project with no formal connection to Rockstar, Take-Two Interactive, or the franchise itself.

That distinction matters enormously. Unofficial meme coins typically carry severe risks, including supply concentration, unaudited contracts, and the possibility of sudden rug pulls.

Also, regulatory uncertainty around unauthorized branding can trigger sudden token removals from major exchanges.

The lack of official endorsement does not stop the rally. Crypto markets historically reward narrative-driven speculation, especially around culturally significant brands.

However, traders chasing late entries face the highest risk of sharp reversals once the initial hype wave fully fades.

History offers clear warnings. Similar-themed meme coin rallies tied to movies, sports events, and other gaming launches have ended with steep declines after the underlying catalyst has passed. Volume often collapses within days, leaving late buyers deeply underwater for months.

For now, the GTA 6 pre-orders announcement on June 25 stands as the next major catalyst.

Until then, meme coin volatility tied to the franchise will likely remain elevated. Investors should remember that the only confirmed news comes directly from Rockstar Games.

The post Rockstar Games Confirms GTA 6 Pre-Orders Date and Themed Meme Coins Explode appeared first on BeInCrypto.

Crypto investors and builders say the censorship of Anthropic's Fable 5 proves their long-running argument: that AI should run on decentralized networks no company or government can switch off. The model shipped with guardrails so broad that many users complained, by Anthropic's own account, and… Read the full story at The Defiant

3 Years Later, the BBC’s Perfect ‘Broadchurch’ Replacement Is Finally Back

How to Achieve FINANCIAL FREEDOM at YOUNG AGE from ZERO Rupees: A Step-by-Step BLUEPRINT for Indians

Shark chillpill handheld fan review: It’ll help you survive a heatwave

Blockchain.com files with SEC for U.S. IPO

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Israel says it has killed new Hamas military leader in Gaza City airstrikes

How to Achieve FINANCIAL FREEDOM at YOUNG AGE from ZERO Rupees: A Step-by-Step BLUEPRINT for Indians

How Did the Nazis Secretly Finance Rearmament Before WWII? (MEFO Bills Explained) #OOTF #shorts

XRP ANNOUNCED 100% SAVE THIS DATE !!!! FEDS CONFIRM (XRP) !!!! BG123 AGREEMENT SIGNED !!!!

-

Business4 days ago

Business4 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World4 days ago

Crypto World4 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World6 days ago

Crypto World6 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech6 days ago

Tech6 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech6 days ago

Tech6 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

NewsBeat7 days ago

NewsBeat7 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

NewsBeat6 days ago

NewsBeat6 days agoFBI searches office of Ohio voter registration group

-

Tech7 days ago

Tech7 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-

Entertainment7 days ago

Entertainment7 days ago‘The Pitt’s Fan-Favorite Doctor Confirms Noah Wyle Gave His Blessing to Return [Exclusive]

-

Crypto World7 days ago

Crypto World7 days agoRipple and Bitso Bring MXNB Stablecoin to XRP Ledger

-

Tech7 days ago

Tech7 days agoFormer AWS CEO Adam Selipsky to lead new $10B AI data center venture

-

Entertainment4 days ago

Entertainment4 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Business7 days ago

Business7 days agoJustin Bieber Prepares for 2026 Tour Return with New Music and Promoter Talks

-

Business4 days ago

Business4 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Tech4 days ago

Tech4 days agoAs AI companies race to go public, who else is along for the ride?

-

Crypto World4 days ago

Crypto World4 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

Tech7 days ago

Tech7 days agoEuro-Office 1.0 Arrives To Open-Source Infighting: ‘Compatibility Is Not Sovereignty’

-

Politics4 days ago

Politics4 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

Entertainment7 days ago

Ana Navarro unleashes explosive tirade on ex-Trump aide, Disney Channel star in epic on-air fight: 'Have you no shame?'

You must be logged in to post a comment Login