Crypto World

Influence360 Launches as the First AI & Data-Driven Web3 KOL Platform with Global KOL Coverage and Real Attribution

Influence360 introduces a campaign engine that enables Web3 projects to discover KOLs globally, execute structured campaigns, and track real performance across regions, languages, and channels.

A benchmark study of 143 Web3 KOLs highlights major gaps in payments, access, and campaign infrastructure, providing context for the platform’s launch.

Influence360 today announced the launch of its platform, introducing a new infrastructure layer for Web3 influencer marketing built around trust, data, and global execution.

Projects can discover web3 KOLs across 10+ languages and key platforms, including X, YouTube, TikTok, and Telegram; launch structured campaigns; and manage execution in one place with AI-powered optimization, smart contract escrow, and real-time performance tracking, enabling transparent payments and clear attribution at a global scale.

“Web3 influencer marketing already moves serious budgets, but the infrastructure around it still feels too basic for the level the market has reached,” said Dejan Horvat, founder & CEO of Influence360. “The biggest issue in the industry is that campaigns don’t compound, as teams aren’t learning what actually drives performance. Influence360 turns every campaign into data, showing which creators deliver value, what content works, and how to optimize spend over time. That’s how we bring trust, structure, and measurable performance to Web3 marketing.”

Influence360 is built by a team with extensive experience in Web3 influencer marketing and campaign execution. Through their previous work at Innovion, the co-founders, Dejan Horvat and Laura Toma, have collaborated with leading blockchain projects and KOL networks across multiple regions over the last 9 years, managing campaigns and partnerships that directly informed the platform’s design and its focus on real-world execution challenges.

Influence360 also extends this infrastructure to Web3 agencies and talent managers. Through a permission-based system, influencers can grant agencies custom access levels covering everything from campaign applications to payment handling, while agencies manage their full roster from a single account. Agencies can apply to campaigns on behalf of creators, set their own pricing on top of influencer rates, and earn a share of platform fees from influencers they bring on, for life. This structure is part of Influence360’s broader referral program, which will expand to include a dedicated affiliate marketing feature focused on performance-based campaigns.

Influence360 is now open to Web3 projects looking to run structured campaigns, KOLs seeking reliable partnerships, agencies managing creator rosters, and affiliate marketing partners focused on performance-driven growth. Learn more and join at influence360.io.

For its launch, Influence360 is releasing The State of Web3 Influencer Marketing 2026, based on survey responses from 143 Web3 KOLs across seven global regions.

The research shows a financially active ecosystem, where more than half of KOLs earn between $1,000 and $5,000 per campaign, with experienced KOLs exceeding that range. The report highlights a persistent trust gap in the market, with only 35% of KOLs reporting that they have been paid by every project they have worked with.

The findings also confirm that Web3 influencer marketing is already a repeat-driven and increasingly professionalized channel. 97% of the KOLs surveyed have worked with the same projects multiple times, while most evaluate factors such as team transparency, investor backing, and project credibility before accepting collaborations. However, the lack of structured tooling, reliable payments, and performance attribution continues to limit efficiency and scale.

Influence360 is built to close this gap by combining campaign execution, real attribution, and a growing data layer that will power AI-driven campaign benchmarking and optimization. With a roadmap that expands into advanced analytics, UGC campaign infrastructure, and automation, the platform is positioning itself as a long-term growth engine for Web3 marketing, where campaigns are continuously measured and improved.

About Influence360

Influence360 is a Web3 creator marketing platform designed to make influencer campaigns transparent, fairly compensated, and measurable at scale. The platform enables global creator discovery across regions, languages, and niches; structured campaign execution; smart-contract escrow payments; performance tracking linked to real outcomes; and AI-powered campaign strategy and optimization. Visit influence360.io.

The post Influence360 Launches as the First AI & Data-Driven Web3 KOL Platform with Global KOL Coverage and Real Attribution appeared first on BeInCrypto.

XRP price is down by 4% over the past 24 hours, after an on-chain data confirmed a coordinated wave of whale distribution that erased a multi-day rally in under 72 hours. The token briefly touched $1.29 before sellers stepped in hard, and large-wallet behavior is now the dominant price driver.

According to data, wallets holding at least 1 million XRP offloaded more than 30 million tokens over five days, with Santiment data showing combined large-address holdings dropping from 3.82 billion to 3.77 billion XRP.

This supply hit spot exchanges directly, absorbing the buying pressure that had built from a $1.14 base on June 14. A cascade of leveraged long liquidations in derivatives markets accelerated the drop, with new Fed Chair Kevin Warsh delivering hawkish signals that killed rate-cut expectations and hit risk assets globally.

The macro overhang is not going away fast. Can XRP’s spot ETF inflows of $5.30 million on June 16 and $2.55 million on June 18 be enough to absorb continued whale selling?

Discover: The Best Crypto to Diversify Your Portfolio

XRP Price Prediction: $1.20 or Is a Test of $1.05 Next?

XRP is currently consolidating near $1.12, having lost every support level it built during the June rally. The move from $1.14 to $1.29 and back down was a full round-trip with nothing to show for it.

Resistance is now stacked between $1.20 and $1.25, the range where profit-taking overwhelmed buying. Below the current price, the next meaningful support zone sits near $1.05, flagged by analysts as the next critical battleground.

A daily close beneath $1.10 would make that test highly likely. Momentum indicators remain bearish, with price trading below short-term moving averages and volume on down days outpacing recovery sessions.

If whale selling exhausts, and ETF inflows accelerate, XRP could reclaim $1.20 within the week and sets up a retest of highs. The ETF inflow data offers a genuine counterpoint for bear

Discover: The Best Token Presales

Maxi Doge Presale Draws Rotation Capital as XRP Stalls at Key Levels

When a mid-cap like XRP gives back a full rally in three days with no structural damage repaired, active traders start scanning for asymmetric setups elsewhere. That rotation is real, and it tends to favor early-stage projects where the entry price hasn’t already been through a 4% haircut before the week ends.

Maxi Doge ($MAXI) is pulling that attention in the meme token segment. Built on Ethereum, the project frames itself around high-conviction trading culture, 1000x leverage mentality, holder-only trading competitions with leaderboard rewards, and a Maxi Fund treasury designed for liquidity management and partnerships.

The presale has raised $4.8 million at a current token price of $0.0002824, with dynamic staking APY available to participants. The community competition structure differentiates it from pure meme plays with no retention mechanism.

Traders considering a position should research Maxi Doge.

The post XRP Price Under Pressure: 30M XRP Whale Sale Pushes Token Down 4% appeared first on Cryptonews.

This Friday, we examine Ethereum, Ripple, Cardano, Binance Coin, and Hyperliquid in greater detail.

Ethereum (ETH)

This week, Ethereum is up 2%, but that is hardly relevant given that the price has failed to reclaim the $1,800 resistance. Sellers returned there to keep the price locked in under this key level.

With the uptrend halted, this cryptocurrency is forced to range between support at $1,500 and resistance at $1,800.

Looking ahead, because sellers appear to control price action, they’re likely to make another attempt to break the key support. If ETH shows weakness and loses $1,500, then new yearly lows will materialize with key targets at $1,400 and $1,100.

Ripple (XRP)

XRP closed the week in red with a modest 1% loss. While that is not much, the more concerning aspect is that the price was rejected at the $1.3 resistance, and since then it’s only been down.

If nothing changes, then this cryptocurrency is on a clear path to revisit the support at $1 where buyers showed up a few weeks ago. The question is if they will return there again or shy away.

Looking ahead, the XRP chart shows weakness with buyers absent. This has encouraged sellers to step up, and they are dominating right now. This could change once the price hits $1, but this is still uncertain now.

Cardano (ADA)

Cardano fell by 4% this week, and after losing support at $0.24, its market cap dropped significantly. This caused it to lose several places on the list of the biggest coins by market cap, where it now ranks 16th, behind the likes of Stellar and Monero.

The price found short-term relief at the $0.15 support, but this appears to have ended as of this post. Now, sellers are back, and they may soon test this key support again with the aim of breaking it and pushing ADA even lower.

Looking ahead, if bears are successful in the coming days, the price could quickly fall again to hit new lows around $0.10, where the next major support level is located. This would be quite unfortunate and prolong the existing downtrend that started in 2025.

Binance Coin (BNB)

After a long battle and consolidation, it appears BNB is finally falling below its support at $580. Because of this, it also closes the week 5% lower. If nothing changes and buyers don’t return, then $580 will turn into resistance, with lower lows likely.

The next key support is found at $500, and this level is likely to be tested if this bearish momentum persists. Since sellers appear to be dominating across the market, a reversal here appears unlikely.

Looking ahead, Binance Coin’s pause between $580 and $690 is about to end. This flat consolidation lasted for six months and a breakdown is a significant bearish signal. Expect new lows this year if bulls cannot regain control.

Hype (HYPE)

Surprisingly, HYPE closed the week 16% higher after a strong performance by buyers, briefly pushing it to $76. However, since then, the price entered a pullback which could see it return to the support at $63.

While the overall momentum remains bullish, the current price pattern may indicate a double top around $76. To confirm this, the price will need to make a lower low under $52 later on.

Looking ahead, buyers and sellers are actively competing to control the price. Right now, the ball is changing hands every few days. While buyers still appear to have the advantage, this remains fragile at the time of this post.

The post Crypto Price Analysis June 19: ETH, XRP, ADA, BNB, and HYPE appeared first on CryptoPotato.

The XRP community’s reaction to the Ripple Swell 2026 announcement was immediate and hostile. Retail holders flooded the @RippleSwell reply thread within hours of the announcement. The consistent theme was not excitement about 1,500 attendees or a merged XRPL Apex agenda; it was anger that Ripple’s flagship institutional event appears to be building a case for RLUSD while XRP falls.

The frustration has a specific target as Ripple’s USD-pegged stablecoin is taking up conference oxygen that long-term holders believe should belong to XRP. Community members used language that ranged from sharp to outright furious. The community is even calling Ripple’s leadership out by name, including CEO Brad Garlinghouse.

The underlying accusation is not subtle. Ripple is constructing a regulated institutional business around RLUSD while XRP’s price stagnates and holders are disappointed.

Discover: The Best Token Presales

Swell 2026 Scope: What’s Ripple Actually Doing

Swell 2026 is scheduled for October 27–29 at The Shed in Hudson Yards, New York City, and represents the first time Ripple is folding its developer-focused XRPL Apex summit into the main Swell conference. The combined event is targeting 1,500-plus attendees, 75-plus speakers, and 50-plus sessions across three programmatic stages covering finance, blockchain infrastructure, and digital assets.

Ripple’s stated agenda themes include payments, tokenization, decentralized finance, AI applications, interoperability, and stablecoins. RLUSD’s role in enterprise treasury management and cross-border settlement is a prominent feature of the institutional track.

The XRP Ledger’s milestone of surpassing 4 billion completed transactions is being cited by Garlinghouse as evidence that the network has matured enough for the institutional audience Ripple is targeting.

Garlinghouse framed the moment with deliberate confidence:

“I’ve been in crypto long enough to know when a moment is real”

The statement positions Swell 2026 as a threshold event for institutional crypto adoption, which is accurate as a description of Ripple’s ambition, but says nothing specific about what that adoption means for XRP price or holder value.

Discover: The Best Crypto to Diversify Your Portfolio

XRP Holders Are Not Hiding Their Frustration

The community sentiment is not a fringe reaction. Retail XRP holders expressed a clear and recurring grievance. Ripple is allocating conference prominence to RLUSD and institutional partnerships while XRP’s price continues to underperform relative to the company’s corporate milestones.

The tone in several replies was openly hostile toward Garlinghouse and the Ripple leadership team, with holders describing themselves as investors who have been systematically sidelined.

The token burn argument has re-emerged as a focal point. A portion of the XRP community is pushing for supply reduction as a mechanism to create direct price pressure, a demand that Ripple has consistently declined to act on.

That refusal, combined with a conference agenda that leads with stablecoins and tokenization rather than XRP utility, is being read by holders as a signal about where Ripple’s actual priorities sit.

Community sentiment of this intensity is a legitimate market signal. When the XRP community, historically one of the most vocal and coordinated retail bases in crypto, publicly turns on a Ripple event, it registers in social volume metrics that can suppress short-term buying pressure and amplify sell-side momentum.

Discover: The Best Token Presales

The post Ripple Swell 2026 Sparks Holder Backlash Over RLUSD Priority appeared first on Cryptonews.

Bitcoin (BTC) rose above $63,000 on Friday as markets adjusted to geopolitical and macro changes.

Key points:

- Bitcoin takes a time-out near week-to-date lows after a broadly hawkish Fed interest-rate meeting.

- US-Iran tensions slowly resurface with the Strait of Hormuz oil route in the firing line.

- A trader suggests that a “black swan” event could still come in this Bitcoin bear market.

BTC price lack upside momentum after hawkish Fed cues

Data from TradingView showed BTC/USD locked in a tight trading range on low time frames after dropping to eight-day lows.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

Weakness had entered after the US Federal Reserve’s latest interest-rate decision, which sparked a broader risk-asset comedown.

Wednesday’s meeting on the Federal Open Market Committee (FOMC) was the first for new Fed chair, Kevin Warsh, who avoided giving traders dovish signals on future policy.

“Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy,” he said in a statement after a unanimous board decision to keep rates at current levels.

“The Committee will deliver price stability.”

Warsh’s tone was unusual, as expectations had seen him being accommodating to US President Donald Trump’s insistence on rate cuts. He also cut the FOMC statement length considerably, using drier language than former chair, Jerome Powell.

“We will have far less information going forward,” trading resource The Kobeissi Letter reacted in a post on X, noting that Warsh had also “dropped” its forward guidance.

“He even hinted that the ‘dot plot’ could be changed or eliminated along with all forms of Fed communication, such as the policy statement and press conferences. In other words, the market will now have less Fed outlook which means more uncertainty.”

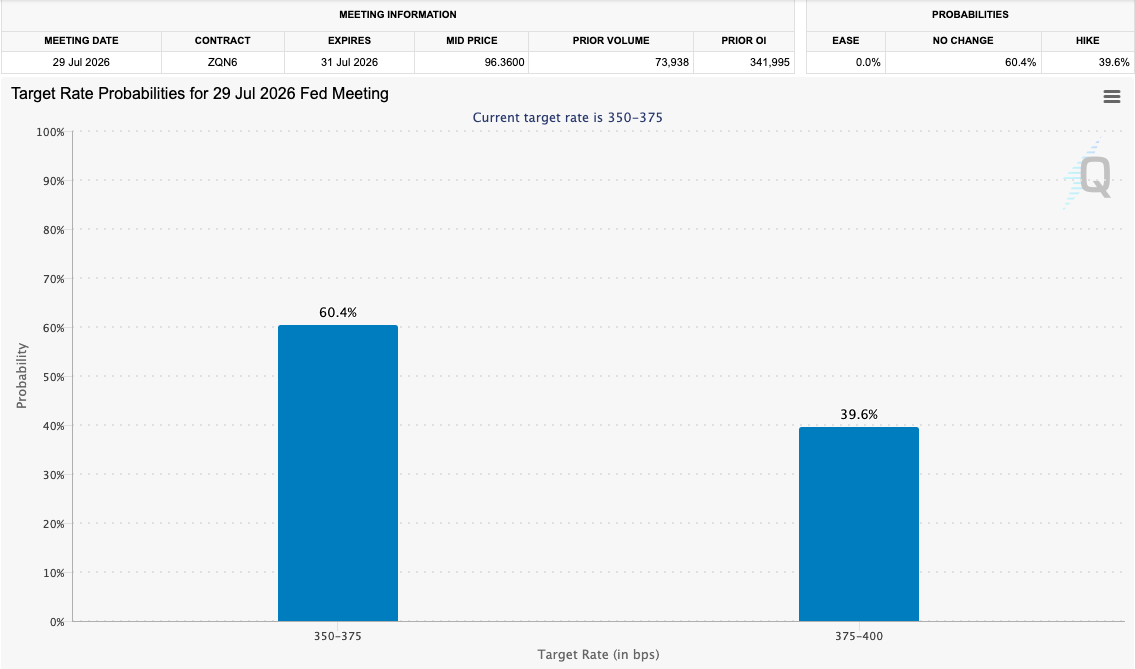

Fed target rate probabilities for July 29 FOMC meeting (screenshot). Source: CME Group

The latest data from CME Group’s FedWatch Tool showed markets pricing in a near 40% chance of a rate hike at the next FOMC meeting in late July.

Bitcoin “black swan” back on the radar

With US markets closed for the Juneteenth holiday, meanwhile, Bitcoin and crypto were alone in digesting the latest developments in the US-Iran war.

Related: Bitcoin tipped for Q3 ‘macro bottom’ near $50K as major liquidity grab looms

Despite signing a memorandum of understanding (MoU), the two sides appeared far from aligned on the future road map, with Iran once more eyeing the newly reopened Strait of Hormuz oil route.

Citing Bloomberg, Kobeissi reported that traffic “cannot cross the Strait of Hormuz without its permission.”

“The MoU signed with the US only says that transit through the Strait of Hormuz would be free for the duration of its 60 day term,” it explained on Friday.

“It appears Iran is preparing for long-term control of Hormuz.”

CFDs on WTI crude oil one-day chart. Source: Cointelegraph/TradingView

WTI crude oil continued to circle $75 per barrel on the day after hitting its lowest levels since early March.

Amid the lull in risk-asset volatility, trader and analyst Rekt Capital hinted that Bitcoin bulls’ true test is yet to come.

“There tends to be a Black Swan event in the second half of Bitcoin Bear Markets. Lesson there,” he told X followers.

Chris Larsen, the Ripple co-founder and apparent privacy champion who wired San Francisco with thousands of police cameras, has appeared on a leaked guest list for Dialog, surveillance mogul Peter Thiel’s invitation-only network.

Investigative journalist Dave Troy published previously unreported names yesterday.

He tagged Larsen as both a participant and a founding fellow of the organization, which has been described as “Bilderberg (an off-the-record gathering of political and business elite) meets Silicon Valley salon.”

Dialog, meanwhile, positions itself as a hush-hush place where leaders from various fields and ideological backgrounds can come together and build relationships.

As part of this, it runs annual in-person retreats featuring highly secretive sessions, which have included “Money (Does?) Buy Happiness,” “Bring Back Nuclear,” “Navigating WWIII,” and “How’s Your Sex Life?”

Larsen, who branded himself a privacy champion, co-founded the coalition Californians for Privacy Now, served on the board of the Electronic Privacy Information Center, and made his fortune from the cryptographically secure XRP Ledger, now appears on a roster at the highest echelons of the surveillance state.

His name wasn’t generally associated with surveillance until his police camera initiative, the Real-Time Investigation Center that operated out of the same building as Ripple’s former headquarters in San Francisco.

In stark contrast, Thiel is one of the most recognizable leaders in the surveillance state.

He co-founded the citizen monitoring giant Palantir and invested in face-scanner Clearview AI, license plate reader Flock Safety, and movement monitor SafeGraph.

Chris Larsen, the privacy advocate who surveilled a city

Larsen tried to make a name for himself as a consumer advocate. In addition to the two privacy-focused organizations listed above, he co-founded E-Loan, the first company to advocate for consumer access to FICO credit scores.

He then built the democratized lending marketplace Prosper, before co-founding Ripple.

Bloomberg estimates his net worth above $12 billion, most of it tied to Ripple stock and XRP tokens.

His privacy branding has aged somewhat poorly, however. He now appears on a list of Dialog participants, founded in 2006 by Thiel and data broker Auren Hoffman whose movement monitoring company SafeGraph tracks phone location data.

The Dialog roster only became public this week. Swiss hacktivist Maia Arson Crimew found an internal directory inside the group’s website code. Wired verified the leak.

The new records have exposed an upcoming 222-person retreat near Dublin, originally scheduled for August. Internal documents describe over 1,000 paying members to Dialog overall, and Wired reported that leaders might grade attendees on a hidden scale by wealth and fame.

Of course, if anyone were curious about Larsen’s ties to the surveillance state, Thiel’s relationship with Ripple actually predates Larsen’s participation in Dialog.

Indeed, Thiel’s Founders Fund was an early investor in OpenCoin, the startup that became Larsen’s Ripple. Therefore, it was public knowledge that surveillance leader Thiel and Larsen were on the same cap table long before this week’s Dialog leak.

Peter Thiel’s secret society or just a ‘convening’?

There’s disagreement about whether Dialog is a particularly secret society.

Troy, who revealed the names, cautioned that Dialog is “more of a convening than secret society,” and noted that many participants claimed to have never met Thiel.

Moreover, the leaked file “looks like a list of attendees for the upcoming [meeting] and not ‘members’ per se,” he clarified.

As an additional indication that Dialog isn’t particularly secretive, another member of Ripple’s leadership has publicly acknowledged it.

Specifically, Brad Garlinghouse said in 2021, “You know, I attended a conference hosted by a gentleman named Auren Hoffman and Peter Thiel called Dialog.”

Elsewhere in that interview, Garlinghouse admitted that Dialog was his first exposure to the Bitcoin network.

Read more: Ripple’s Chris Larsen to fund police surveillance, drones in San Francisco

Larsen once personally bankrolled the largest private surveillance buildout in San Francisco’s history.

New York Magazine counted roughly 2,700 cameras, 93 police drones, and a $9.4 million Real-Time Investigation Center that shared a location with Ripple’s former headquarters.

At the time, Larsen insisted that the system was tightly restricted. “The police can’t monitor it live,” he told ABC7 in 2020. “That’s actually against the law in San Francisco.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Binance’s faltering European Union Markets in Crypto-Assets Regulation (MiCA) license application in Greece has raised questions about whether the bloc’s central bank may have played an informal role in the process, despite not having formal authority over licensing decisions.

Even though MiCA assigns approval of crypto-asset service provider (CASP) licenses to national competent authorities (NCAs), lawyers told Cointelegraph that its wording does not prevent other EU institutions, including the European Central Bank (ECB), from communicating with those regulators during the review process.

“Nothing in the MiCA framework would prevent a third party like the ECB from offering its opinion to that national authority on Binance’s application,” David Lesperance, founder at Lesperance & Associates, told Cointelegraph.

The Big Whale reported on Wednesday, citing unnamed sources, that ECB President Christine Lagarde had signaled to Greek Prime Minister Kyriakos Mitsotakis that Binance was not welcome in Europe. The report followed a Reuters story on Tuesday that Greece’s market regulator was set to reject Binance’s MiCA application.

The reports surfaced less than two weeks before the end of MiCA’s transitional period on July 1, a deadline that will determine which crypto firms can continue operating across the EU under its licensing regime.

Who actually decides under MiCA?

Under MiCA, CASP licenses are granted by national regulators, not by EU-level institutions like the ECB. In Binance’s case in Greece, that authority sits with the Hellenic Capital Market Commission (HCMC). The exchange said in January that it had applied for a MiCA license in Greece.

“Our understanding is that the HCMC completed its review of the application and considered it compliant with MiCA requirements. Our understanding is also that the application was subject to review at the European Securities and Markets Authority (ESMA) level,” Binance wrote in a blog post following the Reuters report.

A Binance spokesperson told Cointelegraph that the company believed ESMA intended to advance the application and authorize it at an upcoming board meeting. The company did not respond to an additional request for clarification. The ESMA does not itself authorize CASP licenses under MiCA.

Yuriy Brisov, a lawyer at Digital & Analogue Partners, said the HCMC hasn’t published a decision on Binance’s application.

Related: BitGo courts crypto firms awaiting MiCA approval amid Binance licensing concerns

Brisov said MiCA “contains nothing that stops the ECB from talking to, advising, or sharing concerns” with a national regulator. However, he noted that ECB involvement is explicitly defined only in certain parts of MiCA, particularly rules governing stablecoin issuers, not CASP licenses such as exchanges like Binance.

Source: EUR-Lex

“That’s a concern that MiCA parks in the stablecoin chapter, not in the exchange-license one,” Brisov added.

Stablecoins raise the political stakes

The ECB has consistently voiced concerns about privately issued stablecoins, favoring tokenized financial infrastructure anchored by central bank money instead. According to The Big Whale, Lagarde’s reported intervention was tied to stablecoins.

Lagarde has argued that Europe should prioritize regulated settlement systems rather than rely on private stablecoins, while ECB Executive Board member Isabel Schnabel has warned that stablecoins could even reinforce US dollar dominance.

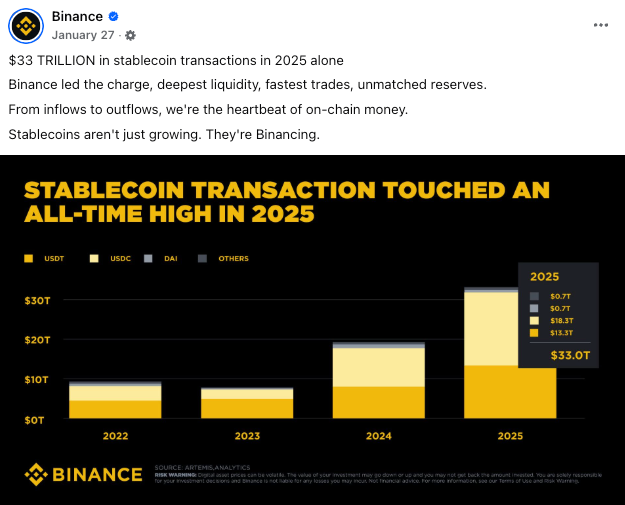

At the same time, market data underscores Binance’s position as the world’s largest stablecoin exchange and the dominant hub for stablecoin liquidity.

Source: Binance

According to CryptoQuant data reported in February, Binance held approximately $47.5 billion in USDT and USDC combined, representing about 65% of total stablecoin reserves across centralized exchanges. That figure was up from roughly $35.9 billion a year earlier.

Related: AllUnity debuts SEKAU, a fully reserved Swedish krona stablecoin

The Big Whale also reported that France could be Binance’s remaining route, though no formal French application had been filed.

ESMA and HCMC did not immediately respond to Cointelegraph’s requests for comment. The ECB and French regulator Autorité des marchés financiers (AMF) declined to comment.

Magazine: Crypto wanted to overthrow banks, now it’s becoming them in stablecoin fight

Crypto World

Where Could BTC Bottom After Breaking Below Key Ascending Channel? (Bitcoin Price Analysis)

Bitcoin is still under heavy selling pressure after breaking below a significant rising channel that had been guiding the price action since February, and there seems to be little stopping the asset from dropping lower.

The latest rejection from a short-term resistance has accelerated downside momentum once again and is pushing BTC back toward the key demand zone around $60K. Meanwhile, on-chain data suggest that long-term holders are realizing losses, reflecting a notable shift in market dynamics.

Bitcoin Price Analysis: The Daily Chart

On the daily timeframe, Bitcoin has decisively broken below the large ascending channel that contained the price action for nearly four months. The breakdown occurred after BTC failed to reclaim the confluence of the 200-day moving average and the $80k zone and was rejected decisively to the downside.

The 100-day moving average located near the $72k area has now formed a key resistance zone. The market attempted to retest it following the initial breakdown, but sellers quickly regained control and triggered another leg lower before the market even reached the area, as the price failed to break back above the $67k short-term supply zone. The rejection confirms that bears remain in control of the broader trend for now.

The asset is currently trading around $63k and is hovering just above a major support area at $60k. This key demand zone marks the most important level on the chart, as it previously acted as a launchpad for the February recovery following the sharp capitulation move.

As long as BTC remains below the broken channel and beneath the moving averages, rallies are likely to be viewed as corrective. Moreover, should the $60k support region fail to hold, the next significant downside target appears to be the large demand area around $50k-$52k. Conversely, reclaiming the $72k resistance zone would be required to invalidate the current bearish outlook and potentially reopen the path toward the $80k region.

BTC/USDT 4-Hour Chart

The 4-hour timeframe provides a clearer view of the recent breakdown. Following the breakdown from the $72k-$74k block, BTC experienced an aggressive sell-off that drove the price into the $60k support zone. The subsequent rebound formed a short-term rising channel, which is often considered a bearish continuation pattern when it develops after a strong decline.

The price has recently broken below the lower boundary of the channel, confirming the bearish pattern and increasing the probability of another test of the $60k-$61k support area. The failed breakout attempt at $67k highlights the lack of bullish conviction. In addition, the RSI has rolled over from near-overbought conditions and is now trending lower near the oversold region, suggesting weakening short-term momentum.

If sellers maintain control, the immediate focus remains on the $60k support zone. A decisive breakdown could trigger another wave of liquidations and accelerate the move toward higher time-frame liquidity pockets beneath the recent lows.

On the upside, BTC would need to recover the $67k resistance region before any meaningful bullish scenario can be considered. Above that, the next major barrier remains the $72k zone, which aligns with the broken daily support and moving-average cluster.

On-Chain Analysis

The Long-Term Holder SOPR (Spent Output Profit Ratio) continues to trend sharply lower and is now below the critical 1.0 threshold. This metric measures whether long-term holders are spending coins at a profit or a loss. Values above 1 indicate profitable spending, while readings near or below 1 suggest holders are either realizing minimal profits or refusing to distribute their coins.

The persistent decline in the 30-day EMA of the Long-Term Holder SOPR reflects a substantial reduction in profit-taking activity among experienced market participants. Historically, such conditions often emerge during prolonged corrections, as investors become less willing to sell after a significant drawdown.

The metric has recently reached capitulation territory, and its continued deterioration confirms the weakening market environment visible on the price charts. If SOPR remains below 1, it would signal that long-term holders are consistently realizing losses, which is a condition that has historically coincided with late-stage correction phases and important market inflection points.

For now, the combination of bearish market structure, resistance rejection, and weakening long-term holder profitability suggests that Bitcoin remains vulnerable to further downside pressure unless buyers can reclaim the $72k region and re-establish control of the broader trend.

The post Where Could BTC Bottom After Breaking Below Key Ascending Channel? (Bitcoin Price Analysis) appeared first on CryptoPotato.

Key Takeaways

- The European Commission may reveal next week that Microsoft Azure and Amazon Web Services meet the threshold for Digital Markets Act regulation.

- A conclusive determination is anticipated by the close of 2025, although the schedule remains flexible.

- Upon formal classification, both platforms must comply with requirements regarding interoperability, preventing vendor lock-in, and eliminating preferential treatment of proprietary services.

- This investigation stems from a November 2024 EU declaration recognizing both corporations maintain “exceptionally dominant market positions” in cloud infrastructure.

- Multiple significant service disruptions affecting AWS and Azure have intensified regulatory focus on the sector.

The European Union is advancing toward subjecting Microsoft’s Azure and Amazon Web Services to regulatory oversight through its Digital Markets Act legislation. Bloomberg reports the European Commission may unveil its initial assessment within the coming week.

The DMA framework specifically addresses major digital platforms that possess what European authorities characterize as “gatekeeper” market influence. Should Azure and AWS receive official gatekeeper status, they’ll be obligated to adhere to regulations crafted to ensure competitive fairness.

Implications of Gatekeeper Classification

Once designated under the DMA, both cloud platforms must satisfy interoperability standards. Additionally, they’ll encounter limitations designed to eliminate practices that trap customers within their ecosystems and prohibit giving preferential treatment to their own offerings over competitor alternatives.

Regulators expect to finalize their determination before 2025 concludes. Nevertheless, individuals with knowledge of the proceedings indicate the timeline remains subject to adjustment.

The examination began in November 2024 following the European Commission’s acknowledgment that Microsoft and Amazon maintain exceptionally strong market positions within cloud computing. This declaration initiated the official investigation process.

European lawmakers established the DMA to combat monopolistic practices among dominant technology companies operating across the continent. The legislation has previously been enforced against corporations including Apple and Google in different technology sectors.

Service Disruptions Intensify Regulatory Pressure

Regulatory attention on these cloud infrastructure leaders has intensified following several prominent service failures. AWS experienced an extended outage lasting approximately 15 hours that affected major clients including Apple, McDonald’s, and Epic Games. A distinct Azure disruption in October disabled Alaska Airlines’ passenger check-in infrastructure and interrupted legislative operations at the Scottish Parliament.

These technical failures highlighted the extent to which modern digital commerce relies upon a concentrated group of cloud service providers.

Both Microsoft and Amazon declined to provide statements when contacted for this report.

The Commission has yet to release its official assessment publicly. Should the initial conclusions remain unchanged, both organizations will receive an opportunity to submit responses prior to any binding determination.

Cloud computing infrastructure has emerged as a priority surveillance area for EU regulatory bodies, reflecting the sector’s rapid expansion and the extensive number of enterprises dependent upon these platforms.

This probe represents one component of the EU’s comprehensive effort to enforce competition standards across the largest operators in digital infrastructure services.

Prediction market Kalshi is reportedly in early, informal talks with investment banks about an initial public offering (IPO), despite increasing regulatory scrutiny over sports betting contracts on these platforms.

Kalshi is in early-stage talks to go public via an IPO after the platform surpassed $2 billion in annualized revenue, unidentified sources familiar with the matter told news outlet The Informant, according to a Friday report.

A spokesperson for Kalshi declined to comment on the matter.

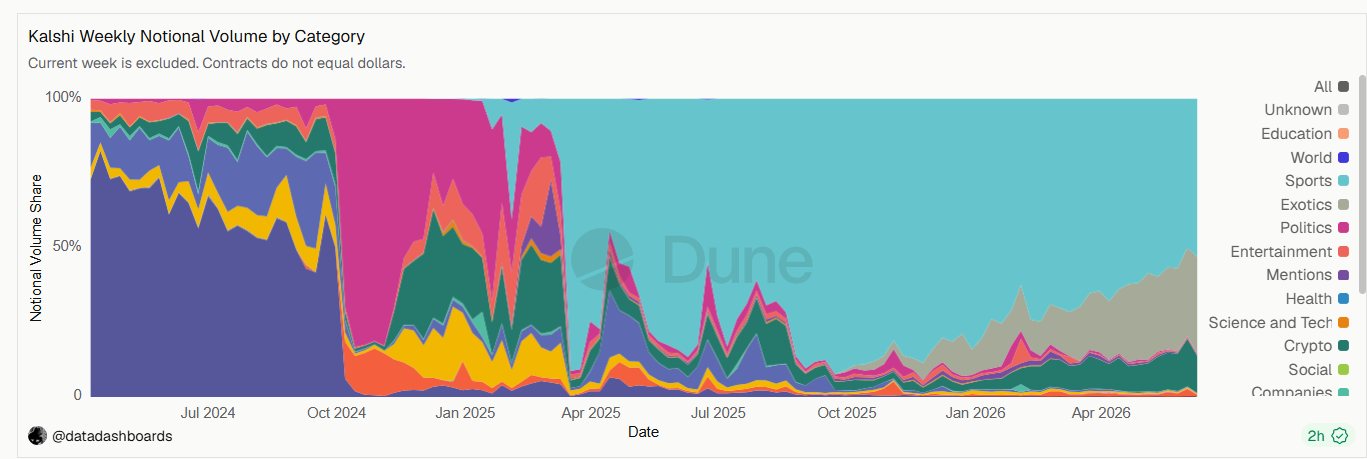

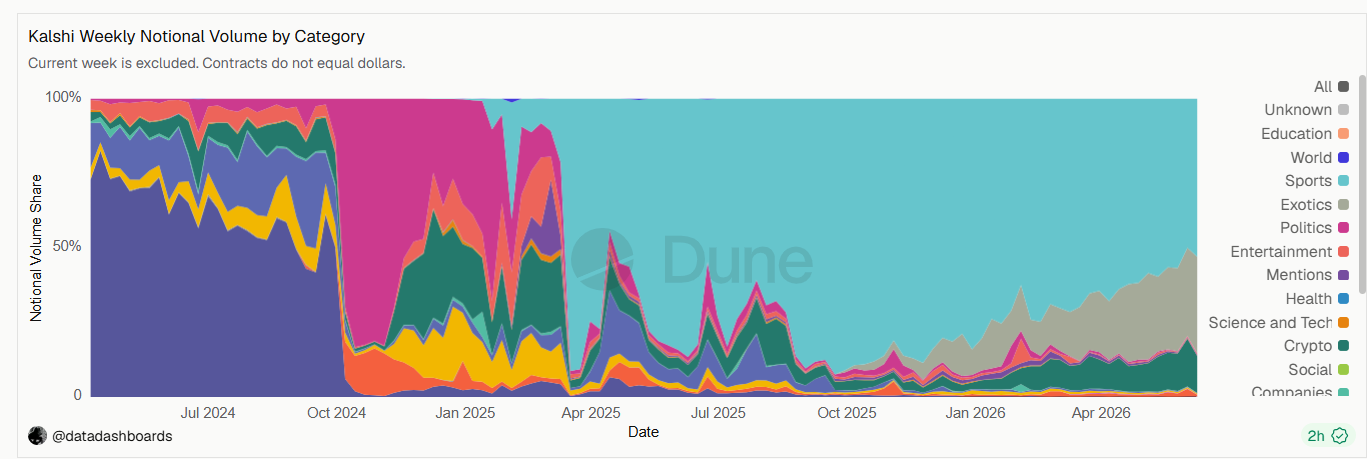

The reported IPO discussions come as sports betting contracts account for more than half of Kalshi’s weekly notional trading volume, even as those markets face mounting legal challenges from US states.

Sports betting contracts were the leading category on Kalshi, representing about 53% of its weekly notional trading volume, according to Dune data. Sport-related betting was also the leading category on Polymarket, accounting for about 69% of its weekly trading volume.

Kalshi doubled its valuation to reach $22 billion after closing a $1 billion Series F funding round led by Coatue Management, Cointelegraph reported on May 7.

Kalshi weekly notional volume by category. Source: Dune

US regulators are cracking down on sports-related prediction market contracts

Kentucky became the latest state to sue five prediction markets, including Kalshi and Polymarket, accusing them of “operating unlicensed and illegal sports betting and gambling platforms,” Cointelegraph reported on Thursday.

Related: Polymarket users cry foul after Strategy sale market resolves to ‘no’

At least 17 other states have taken prediction market operators to court, attracting the involvement of the US Commodity Futures Trading Commission (CFTC).

State authorities argue that sports event contracts require state-level licenses, while prediction markets claim their event contracts are swaps regulated under federal commodities law.

The CFTC also argued that event contracts qualify as “swaps” as they are based on binary events. On May 14, the CFTC issued a no-action letter seeking to ease event contract reporting rules.

CFTC no-action letter on prediction markets. Source: CFTC.gov

The CFTC has sued at least five states in a bid to cement its authority over prediction markets, including Wisconsin, New York, Arizona, Connecticut and Illinois.

Magazine: The legal battle over who can claim DeFi’s stolen millions

Japan’s Financial Services Agency has suspended part of moomoo Securities’ operations for three months and ordered the brokerage to strengthen its internal controls after regulators found compliance, customer protection, anti-money laundering, and cybersecurity failures.

Summary

- Japan’s Financial Services Agency has barred moomoo Securities from acquiring new customers for three months after finding compliance, AML, and cybersecurity failures.

- Regulators said the brokerage incorrectly labeled 78 non NISA eligible U.S. investment products as tax exempt assets and failed to adequately address the issue for affected clients.

- Authorities also cited shortcomings in suspicious transaction monitoring, stock transfer handling, and internal governance, prompting a business improvement order and management overhaul.

The Financial Services Agency said on June 19 that moomoo Securities must stop soliciting and accepting applications for new accounts from June 19 through Sept. 18. The regulator also issued a business improvement order that requires the company to clarify management responsibility and submit a plan to prevent similar issues from recurring.

The action follows an investigation by Japan’s Securities and Exchange Surveillance Commission, which concluded that the brokerage expanded its business and introduced new services without establishing adequate compliance and risk management systems.

FSA cites NISA misrepresentations and compliance failures

Regulators said moomoo Securities incorrectly presented investment products as eligible for Japan’s Nippon Individual Savings Account program even though the products did not qualify under the tax-advantaged scheme.

The Securities and Exchange Surveillance Commission found that between early 2025 and early 2026, the brokerage displayed 78 U.S. exchange-traded funds and exchange-traded notes as NISA-eligible assets on its smartphone trading platform. The commission said retail investors subsequently purchased products that did not qualify for tax-free treatment.

Japanese authorities stated that the firm did not adequately address the issue after discovering the mistake. Regulators said the company failed to proactively contact affected customers or restore annual investment allowances impacted by the transactions.

The watchdog also cited restrictions on domestic stock transfers. The commission said moomoo Securities had declined customer requests to move Japanese stocks to other brokerages since early 2024, limiting clients’ ability to transfer assets outside the platform.

Financial authorities said the company also failed to properly comply with anti-money laundering obligations. The commission found that more than 1,500 rejected or flagged account applicants had not undergone sufficient reviews for suspicious activity because the firm incorrectly believed screening requirements applied only to approved accounts.

Japanese regulators said the brokerage had not conducted required examinations or reporting related to suspicious transactions for an extended period.

Cybersecurity and governance concerns

The Financial Services Agency said cybersecurity controls were also inadequate. Regulators found that management failed to maintain a complete inventory of important transaction systems and did not properly assess vulnerabilities affecting critical infrastructure.

The agency ordered the company to establish clearer accountability among executives and strengthen its internal management framework. Moomoo Securities must submit a detailed business improvement plan to regulators by July 21.

Moomoo Securities is the Japanese subsidiary of Hong Kong-based Futu Holdings, an online brokerage group listed on the Nasdaq. The company has expanded rapidly through its mobile investment platform and has surpassed 2 million app downloads in Japan while promoting low-cost trading in U.S. stocks.

The enforcement action comes as other parts of the Futu group continue expanding overseas. Moomoo Crypto, a separate subsidiary under the Futu umbrella, recently extended its cryptocurrency trading services into Texas, adding to operations in California, New Jersey, and Pennsylvania. The U.S. platform offers trading in 52 digital assets and supports direct transfers between external crypto wallets and customer accounts.

The case adds to a period of heightened oversight of digital finance activities in Japan. Earlier this year, the Financial Services Agency proposed stricter standards for stablecoin reserve assets and introduced additional supervisory requirements for financial institutions involved in cryptocurrency-related services as part of broader reforms under the country’s updated digital asset framework.

XRP Price Under Pressure: 30M XRP Whale Sale Pushes Token Down 4%

Fabrizio Romano reveals the truth behind Liverpool’s reported interest in Micky van de Ven

Why People Might Ditch Their Smartwatches For Something Simpler

-

Business5 days ago

Business5 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World6 days ago

Crypto World6 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech7 days ago

Tech7 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

NewsBeat7 days ago

NewsBeat7 days agoFBI searches office of Ohio voter registration group

-

Entertainment5 days ago

Entertainment5 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Business5 days ago

Business5 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Tech5 days ago

Tech5 days agoAs AI companies race to go public, who else is along for the ride?

-

Crypto World5 days ago

Crypto World5 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

Politics5 days ago

Politics5 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

NewsBeat5 days ago

NewsBeat5 days agoWarning of disruption as Cardiff Crossrail works to start

-

News Videos5 days ago

News Videos5 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

NewsBeat5 days ago

NewsBeat5 days agowhat doctors are seeing in ebike crashes

-

Entertainment6 days ago

Entertainment6 days agoDeion Sanders Shares Powerful Post After Viral Advice To Deiondra

-

Crypto World5 days ago

Crypto World5 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Crypto World5 days ago

Crypto World5 days agoMarket Preview: SpaceX (SPCX) IPO Record, Federal Reserve Meeting, and Iran Nuclear Agreement

-

Entertainment5 days ago

Entertainment5 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Business5 days ago

Business5 days agoInvesco Quality Income Fund Q1 2026 Commentary

You must be logged in to post a comment Login