Crypto World

Is South Korean Capital Fleeing Stocks for Crypto? Upbit Volume Says Maybe

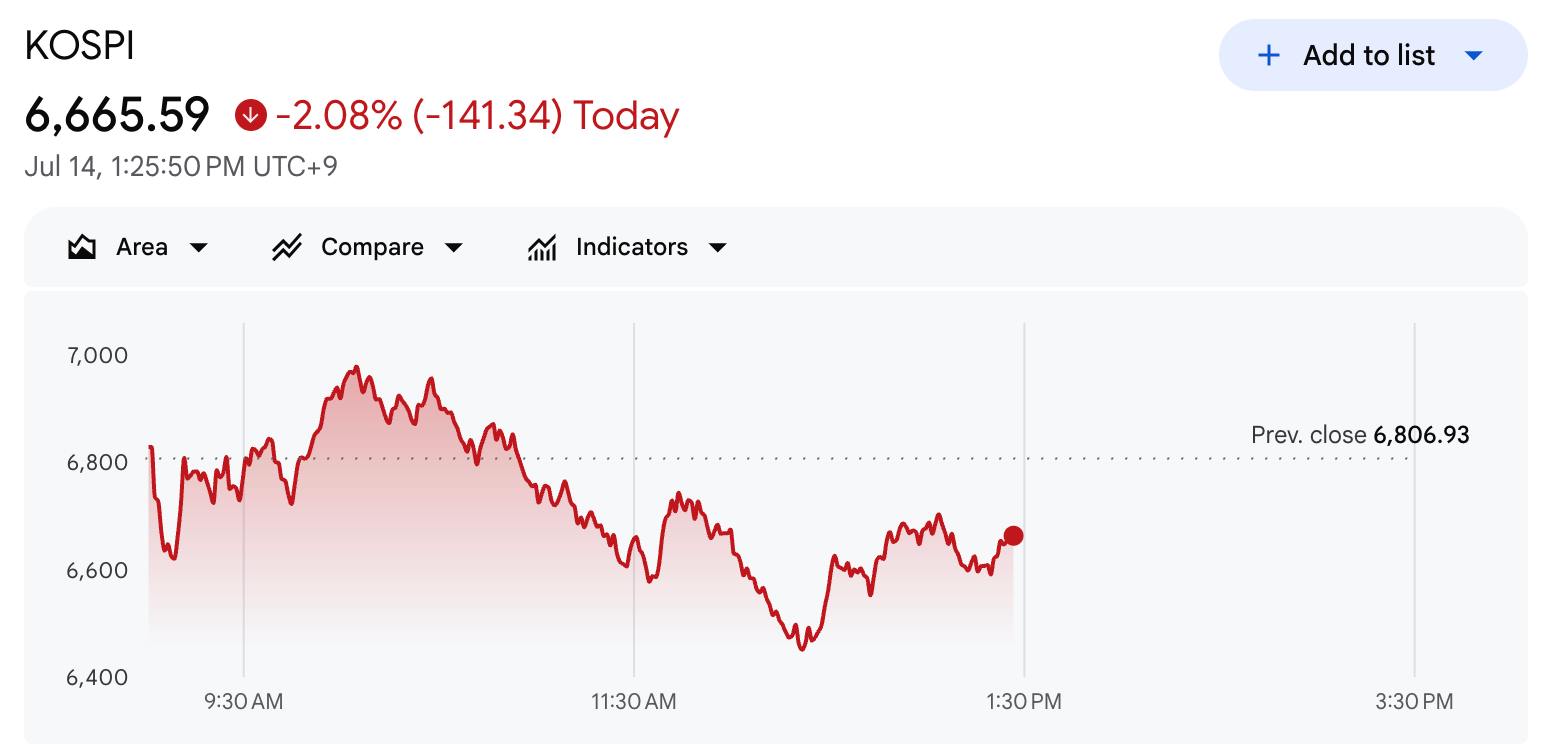

Upbit’s reported 24-hour trading volume surged 1,437% today, as South Korea’s KOSPI index tumbled and equity markets across Asia weakened.

The activity spike coincided with a broad regional selloff. Trading turnover jumped even as major benchmark indices in Seoul, Hong Kong, Tokyo, and Taipei all trended lower.

Trading on Upbit Rockets 1,437% as KOSPI Sinks 4%

The turnover reflects heightened trading activity rather than a confirmed shift of capital out of equities. The dollar total reached $4.24 billion as of press time, according to CoinGecko data.

Upbit ranks as South Korea’s largest cryptocurrency exchange by volume. A surge of this size signals a jump in participation across the platform’s markets.

The jump coincided with the KOSPI’s sharp decline on July 14. According to Wu Blockchain, the index fell 4% intraday to 6,534.34 before recovering some ground. It traded down about 2% as of press time.

Follow us on X to get the latest news as it happens

South Korea’s secondary market fared worse. The tech-heavy KOSDAQ Composite dropped 3.97% to 767.66 on the day.

SK Hynix, a major chip supplier, dropped 3.52% after sliding 15% in the previous session. The stock has led losses among Korean technology names.

Nonetheless, Samsung bucked the trend, gaining 2.36% on the day. The split performance points to uneven pressure across the region’s largest technology stocks.

Technology shares carry heavy weight in both Korean indices. Sharp moves in names like SK Hynix and Samsung, therefore, drive much of the daily swing.

Broader Asian markets also weakened. The Hang Seng Index slipped 0.47% to 24,099.89, and Japan’s Nikkei 225 edged down 0.086%. Taiwan’s TAIEX fell 1.93% to 44,503.61.

The coming sessions will show whether the surge marks a lasting increase in Korean crypto trading.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Is South Korean Capital Fleeing Stocks for Crypto? Upbit Volume Says Maybe appeared first on BeInCrypto.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Institutional crypto OTC markets are evolving beyond block trades as firms demand liquidity, settlement, and cross-border infrastructure services.

Summary

- Institutional crypto OTC desks are evolving beyond block trades into full-service execution and settlement infrastructure.

- Growing institutional demand is reshaping crypto OTC desks into providers of execution, settlement, and treasury infrastructure.

- Crypto OTC markets are expanding beyond large trades as institutions seek integrated execution and liquidity solutions.

For most of its early history, the institutional crypto OTC market was defined by a single problem: how to move large blocks of Bitcoin or Ethereum without those orders moving the market against themselves. OTC desks existed to solve that problem, and the mechanics were straightforward. A desk aggregated liquidity across venues, quoted a price, and settled the transaction off-exchange. That was the value proposition, and for the institutions active in the market at the time, it was sufficient.

The market that exists today is considerably more complex. The institutions using OTC infrastructure now range from payment companies running millions of stablecoin conversions per month to sovereign wealth funds building digital asset exposure to regional exchanges managing fiat liquidity across multiple jurisdictions simultaneously. Their requirements go well beyond block execution, and the desks serving them have had to evolve accordingly. Understanding how that evolution unfolded and what it means for institutions evaluating OTC partners today is increasingly important as off-exchange activity accounts for a larger share of total institutional crypto volume.

From block trading to execution infrastructure

The original institutional OTC use case was straightforward: an investor wanted to acquire or liquidate a significant position in Bitcoin or Ethereum, and the depth available on public exchange order books at any given moment was insufficient to absorb the order without meaningful price impact. OTC desks solved this by aggregating liquidity from multiple venues simultaneously, executing the full position off-exchange at a single blended rate. The client received a cleaner outcome than exchange execution could deliver at a comparable size, and the desk managed the inventory risk.

As institutional participation broadened, the use cases multiplied faster than most desks anticipated. Payment companies discovered that stablecoin-to-fiat conversion at scale required the same off-exchange execution logic as block trades, but at far higher frequency and with much tighter settlement timing requirements. Mining operations needed to convert consistent production volumes without compressing spot prices on public markets. Funds allocating across a broader digital asset universe needed OTC access to assets with limited exchange liquidity. Each of these use cases placed different demands on OTC infrastructure, and the desks that grew with their clients were the ones that treated execution as a starting point rather than an end product.

The shift from block trading to execution infrastructure represents the most significant structural change in the institutional OTC market over the past several years. A desk operating as execution infrastructure is not just quoting prices on large orders. It involves managing settlement rails, maintaining credit relationships, operating compliance frameworks across multiple jurisdictions, and providing the reporting and operational integration that institutional treasury functions require. The technical and operational gap between a desk capable of this and one that handles only straightforward block trades is substantial.

Settlement as the real differentiator

Among the structural changes in institutional OTC, none has been more consequential than the shift in how clients evaluate settlement capability. For the first generation of institutional OTC clients, settlement was binary: did the transaction complete, and did it complete accurately? Speed was a secondary consideration because the use cases did not require it.

For the current generation of institutional users, settlement infrastructure is often the primary criterion for evaluation. Payment companies and fintechs running real-time stablecoin conversion flows cannot absorb settlement delays lasting hours. Treasury operations managing liquidity across multiple jurisdictions in different time zones need finality that is reliable rather than probabilistic. Regional exchanges facilitating local fiat pairs need settlement rails that are actually present in their markets rather than routing through correspondent banking chains that add latency and introduce clearing risk.

The desks that have responded to this have built onshore banking infrastructure across the regions where their clients operate, rather than relying on cross-border correspondent relationships to approximate regional settlement. The operational investment required to do this genuinely, with actual banking licenses, compliance infrastructure, and local operational presence, is one of the more significant barriers to entry in the institutional OTC market today. Recent developments reinforce why this matters: central banks moving to blockchain-based settlement rails is raising the baseline of what institutional settlement infrastructure is expected to deliver, making the gap between desks with genuine regional presence and those with nominal coverage more consequential. It is also one of the reasons that headline spread comparisons between desks are increasingly insufficient as an evaluation framework. A desk offering tight spreads with slow or uncertain settlement is, in practice, more expensive than one offering slightly wider spreads with second-level finality across all relevant markets.

The role of multi-venue aggregation in modern OTC execution

Multi-venue aggregation has always been part of the OTC value proposition, but how it is executed and the depth at which it operates have changed considerably as the crypto market structure has matured. In the early institutional OTC market, aggregation across a handful of major exchanges was sufficient to source competitive pricing on the assets clients needed. As the asset universe expanded and trading activity was distributed across more venues globally, connectivity requirements grew accordingly.

The practical implication is that the quality and quantity of multi-venue aggregation have become a primary differentiator among OTC desks, rather than just a baseline capability. A desk with deep connectivity across a broad network of exchanges can source liquidity and lock pricing for a wide range of digital assets simultaneously, giving clients certainty on the rate before execution begins, regardless of where the underlying liquidity happens to be distributed at that moment. The infrastructure required to deliver this, low-latency connections to a large number of venues, real-time pricing engines operating across all of them, and price-locking mechanisms that hold the rate through execution, represents a meaningful operational investment that separates the leading desks from the rest of the market.

Counterparties offering crypto OTC trading at this level of infrastructure depth provide a fundamentally different execution environment than lighter-touch alternatives. The difference is not primarily visible in a standard spread comparison. It shows up in execution consistency across a wide range of assets, in settlement reliability during volatile market conditions, and in the operational continuity that high-frequency clients depend on when their own business processes are built around it.

Emerging market demand and what it requires

One of the more underappreciated developments in institutional crypto OTC over the past few years has been the expansion in demand from emerging-market participants. Exchanges operating in Southeast Asia, Latin America, and MENA now represent a significant and growing share of institutional OTC activity, and their requirements are specific enough to constitute a distinct market segment rather than a geographic variation of the same use case.

The core challenge for emerging market participants is not execution pricing. Spreads on major pairs are competitive across most institutional desks. The challenge is regional settlement: reliably getting fiat in and out of local markets at speed, without the correspondent banking dependencies that introduce unpredictable latency. An exchange in Southeast Asia managing local fiat pairs needs a counterparty that can settle in the local market in seconds, not one that routes through a chain of correspondent banks and delivers settlement on the following business day.

This requirement has pushed institutional OTC desks toward genuine regional operational presence as a competitive necessity rather than a growth aspiration. The desks with onshore banking infrastructure and compliance frameworks in the markets where their emerging-market clients operate can serve this segment in ways those without it simply cannot replicate at the service levels these clients require. As emerging market institutional participation continues to grow, this regional operational depth is likely to become one of the most important factors in OTC counterparty selection.

How institutional clients are evaluating OTC desks today

The evaluation framework that institutional clients apply to OTC desks has become considerably more sophisticated as their use of OTC infrastructure has deepened. The clients who are now moving the most volume through OTC desks, payment companies, active trading operations, exchanges, and large fund managers have developed detailed views of what genuinely capable infrastructure looks like, and they apply those views when selecting or reviewing counterparties.

Settlement speed and regional coverage have already been discussed, but two additional dimensions are worth examining. Capital structure, specifically whether the desk operates on its own balance sheet or relies on borrowed inventory, shapes how risk is distributed within the arrangement and has direct implications for same-day settlement capability and credit availability. Desks operating on their own institutional capital can hold inventory, extend credit facilities to eligible counterparties, and absorb the timing differences between client execution and position management. These capabilities underpin the kind of operational reliability that high-frequency clients require.

Reporting and integration capability have also emerged as significant evaluation criteria for institutional treasury operations. Clients running high transaction volumes need real-time, granular visibility into execution quality, API integration that removes manual steps from the execution workflow, and operational transparency that enables their finance teams to accurately account for every transaction. Desks that treat reporting as an afterthought are increasingly unsuitable for the more sophisticated segment of the institutional OTC market, regardless of how competitive their pricing appears.

Where the institutional OTC market is heading

Several structural trends are likely to shape institutional crypto OTC over the coming years. Stablecoin adoption by major financial institutions is already changing the settlement economics of cross-border institutional flows, and OTC desks positioned within that infrastructure are likely to see volume growth that differs structurally from traditional block-trading demand. Visa’s CFO recently outlined how stablecoin settlement is reshaping institutional payment infrastructure, a signal that stablecoin-denominated settlement is moving from an emerging capability to an operational expectation across a significant segment of institutional payment flows, with direct implications for the OTC desks serving those clients.

Regulatory development across key markets is creating both clarity and new compliance requirements for institutional OTC operations. Desks with the compliance infrastructure to operate across multiple regulated jurisdictions are better positioned to serve the institutional segment as regulatory frameworks mature, while those without it face increasing friction in markets where institutional participation is growing fastest.

The consolidation dynamic evident in the institutional OTC market over the past few years is likely to continue. The operational investment required to maintain competitive execution infrastructure across a broad asset universe, genuine regional settlement capability, and the compliance frameworks that institutional clients now require is substantial. The desks that have built this infrastructure are pulling further away from those that have not, and the evaluation gap between them is becoming more visible to institutional clients with each passing cycle.

What this means for institutions evaluating OTC partners

The evolution of institutional crypto OTC from a block-trading service to a genuine financial infrastructure has significant implications for how institutions should approach counterparty evaluation. A framework built around spread comparison was adequate when OTC desks were doing a simpler job. It is insufficient for evaluating the kind of operational relationships that institutional crypto participation now requires.

The institutions best positioned in this market have treated their OTC counterparty decision as a strategic infrastructure choice rather than a transactional one, selecting partners with the settlement depth, regional presence, capital structure, and operational integration capability to support their business as it scales. The quality of that decision tends to compound over time. The desks with the right infrastructure today are the ones whose clients transact the most volume, and the gap between them and lighter alternatives is becoming harder to close from the outside.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Peter Schiff renewed his long-running criticism of Bitcoin (BTC) on the July 15 episode of “The Peter Schiff Show,” arguing that investors who hold the asset near its current price will eventually regret not selling, as he expects another major decline.

He also questioned Strategy’s decision to sell $450 million in common stock rather than touch its BTC holdings, saying it shows how boxed Michael Saylor’s company has become.

Schiff Lays Out His Bitcoin Case, and Takes Another Shot At Saylor

In the podcast, Schiff admitted that Bitcoin has been surprisingly resilient despite what he believes are growing risks beneath the surface. The economist said that he regretted not buying BTC when he first heard of it 15 years ago, but watching the asset in the last few years had tempered that regret.

“I don’t regret not buying it three, four, five years ago,” he told listeners. “But yeah, 15 years ago, sure, I should have bought it.”

However, he claimed that those who currently hold the OG crypto and still refuse to sell will soon rue their choice. Referring to the cryptocurrency’s current trading range, he argued that there is resistance around $65,000 while support is near $58,000. According to him, if that level fails, Bitcoin could fall below $50,000 before eventually hitting rock bottom at $30,000 or even $20,000.

‘The people who don’t sell it now, they’re going to be the ones that are going to have a lot of regrets,” he warned.

At the time of writing, CoinGecko data showed that BTC was trading a couple hundred bucks under $65,000, having gone up nearly 4% following the release of lower-than-expected US CPI numbers.

The economist then turned to another of his pet subjects, Strategy, which he noted had gone three straight weeks without buying Bitcoin and hadn’t sold any either since disposing of 3,588 BTC last week. Instead, Saylor’s firm raised $450 million through a common stock sale, pushing up its cash reserves to $3 billion, all while the stock traded at a huge discount to the value of its Bitcoin.

Schiff called it a needless dilution and argued that Strategy had avoided selling BTC only because doing so would tank the cryptocurrency’s price.

“Saylor knows if he starts really selling Bitcoin, the price is going to crash,” he claimed. “Now, the problem is it’s going to crash anyway because the market realizes the bind he’s in, and even if he doesn’t sell the market is going to crash out from under him.”

Corporate Treasury Debate In Focus

Schiff’s criticism has come at a time when analysts are reassessing the corporate Bitcoin accumulation story, of which Strategy is the biggest player. According to a recent report from QCP Capital, when Saylor’s firm sold some of its Bitcoin for the first time in late May, the amount, though small (32 BTC out of an over 847,000 BTC stash), still changed the way investors looked at such companies.

Many of them are now paying more attention to their cash reserves, equity issuances and the funding conditions of such operations to determine whether future purchases remain sustainable instead of just being swept away by the latest headline-grabbing buys.

The post Peter Schiff: Bitcoin Holders Will Soon Regret Not Selling at Current Levels appeared first on CryptoPotato.

Securitize and Cantor Fitzgerald have announced a partnership aimed at enabling blockchain-based primary issuances and follow-on equity offerings for listed companies using tokenized securities. The initiative is designed to fit within existing regulatory pathways for public offerings, positioning tokenization as a potential upgrade to traditional IPO and secondary capital-raising workflows.

According to the companies, they are developing a framework that would allow issuers to raise capital through tokenized securities while maintaining compliance with the rules applicable to public offerings. The plan covers both initial public offerings and subsequent, or secondary, share sales by companies that are already publicly listed.

Key takeaways

- Securitize and Cantor Fitzgerald plan to build a regulated issuance and settlement framework for tokenized securities covering both IPOs and follow-on equity offerings.

- Securitize will provide the tokenization infrastructure, while its SEC-registered broker-dealer affiliate, Securitize Markets, is set to participate in offering and settlement.

- Cantor will contribute its equity capital markets experience and trading capabilities associated with public offerings.

- The move aligns with a broader shift toward tokenized stocks and real-world assets as institutional infrastructure efforts accelerate.

A framework designed for public-offering compliance

The partnership is structured around the mechanics required to issue and distribute digital securities in a way that can be administered under the current public-offering regulatory environment. The companies said the framework is intended to support both IPOs and follow-on offerings—where an already listed company issues additional shares to raise capital.

Under the agreement, Securitize is expected to handle the tokenization infrastructure that underpins issuance, distribution, and ongoing servicing of the digital securities. Its SEC-registered broker-dealer affiliate, Securitize Markets, will take part in the offering and settlement process, bridging the digital issuance layer with the traditional market structure.

Cantor Fitzgerald, for its part, will bring its equity capital markets and trading capabilities—capabilities that are typically central to underwriting, market execution, and the infrastructure surrounding public equity transactions.

Why this matters as tokenized equities gain momentum

The announcement arrives as tokenized securities continue to attract increasing attention from established finance. While tokenization has historically found early traction in areas such as private credit and tokenized U.S. Treasurys, the latest wave of interest is increasingly directed at public equity markets.

RWA.xyz data cited in the announcement indicates that tokenized stocks onchain have grown notably: the value of tokenized stocks is reported to have increased 16% over the last 30 days to nearly $1.9 billion. That rate of growth, according to the piece, outpaces much of the broader digital asset market—an important sign for investors watching where tokenization is scaling beyond niche use cases.

More significantly for traditional market participants, the narrative is shifting from isolated pilots to recurring questions about issuance, trading, custody, and settlement at institutional scale. Even when tokenized products are still being explored, the industry attention itself is a signal that infrastructure and compliance teams are beginning to treat tokenization as a serious operational track rather than an experimental technology.

Institutional infrastructure: DTCC’s plans and Wall Street pilots

Tokenized equities are also being pursued through mainstream market infrastructure efforts. Earlier coverage cited in the announcement points to moves by the Depository Trust & Clearing Corp. (DTCC). In a report published Wednesday by The Wall Street Journal, DTCC said it plans to pilot tokenization of stocks and U.S. Treasurys with nearly 40 financial companies, including JPMorgan and Goldman Sachs.

The DTCC trial is described as following its May announcement that it aims to roll out tokenized trading services by October. If the timeline holds, it would represent another step toward standardizing how tokenized assets could be cleared and settled in ways that mirror current institutional workflows.

The WSJ report also notes that the assets targeted for tokenization include shares of Microsoft and Circle, as well as exchange-traded funds tracking major indexes such as the S&P 500 and the Nasdaq 100, alongside short-term U.S. Treasury bonds. The selection is notable because it spans both equity and high-liquidity fixed-income benchmarks—assets that tend to draw heavy institutional participation and could therefore stress-test infrastructure at scale.

For investors and market operators, the practical question is not whether tokenization can “work,” but whether it can interoperate with existing systems for corporate actions, settlement finality, and operational risk controls. Partnerships like Securitize and Cantor’s can be interpreted as one answer on the issuance side, while efforts like DTCC’s pilot focus on the post-trade and market structure layers.

Building on an existing relationship

The partnership is also not starting from zero. Securitize previously moved into public markets via a merger with a special purpose acquisition company (SPAC) backed by Cantor Fitzgerald, according to the announcement. That prior connection helps explain why the two firms are positioning themselves to collaborate on a more ambitious use case: applying tokenization infrastructure to new public-offering activity rather than limiting it to private markets or narrow asset classes.

Even so, key details about implementation and scope remain to be seen. The announcement emphasizes the intent to remain within existing regulatory frameworks, but readers should watch for additional specifics on how the framework will be executed in practice—such as which markets or jurisdictions it initially targets, what types of issuers it prioritizes, and how the settlement and servicing process will be operationalized for tokenized IPOs and follow-on sales.

As tokenized equities continue to attract both infrastructure investment and growing onchain activity, the next phase will likely hinge on regulatory clarity, market-structure integration, and whether pilot projects can graduate into repeatable issuance pipelines for mainstream public companies.

Crypto World

DTCC moves tokenized securities into live trading, marking a milestone for Wall Street’s blockchain push

DTCC safeguards more than $114 trillion in securities, making it one of the most important pieces of financial market infrastructure. Every day, it records ownership and settles transactions involving stocks, bonds and other securities. Rather than creating new digital assets, DTCC’s system converts existing securities into blockchain-based “digital twins” that retain the same legal ownership, dividend and governance rights as the underlying assets.

That distinction separates DTCC’s approach from many tokenized stock offerings available today.

Some crypto platforms issue tokenized “wrappers” that mirror a stock’s price but do not necessarily provide investors with the legal rights associated with owning the underlying shares.

DTCC’s model instead allows institutions to convert existing securities between traditional electronic records and blockchain-based tokens without changing ownership.

“They’re the ones who are flipping from one settlement regime to the next,” Mark Wendland, CEO of Canton Strategic Holdings, said in an interview. “I cannot understate the importance of a firm like DTC piloting and doing these real transactions given the role they play in U.S. financial markets.”

Throughout the day, participants demonstrated several use cases. JPMorgan converted holdings of the Invesco QQQ Trust ETF into tokenized assets before using tokenized collateral to satisfy central counterparty margin requirements with CME Group. DTCC also processed tokenized Treasury transactions, equity trades and collateral pledges, while the SPDR S&P 500 ETF Trust, one of the world’s largest ETFs, was also tokenized during the event.

BlackRock has joined a Depository Trust & Clearing Corporation pilot that has begun tokenizing stocks and U.S. Treasuries within a market infrastructure that safeguards about $114 trillion in assets.

Summary

- DTCC has launched a tokenization pilot with BlackRock, JPMorgan, Goldman Sachs, and nearly 40 financial firms.

- Microsoft, Circle, QQQ, SPY, and BlackRock Treasury ETF are among the first assets being tokenized.

- The pilot uses Hyperledger Besu and Canton, while Stellar-based custody tokenization is planned for 2027.

According to a Wall Street Journal report, BlackRock, JPMorgan, Goldman Sachs, Vanguard, the New York Stock Exchange, and nearly 40 financial firms are participating in DTCC’s latest tokenization initiative.

The pilot focuses on securities already held at the clearinghouse, allowing participating firms to test blockchain-based versions of traditional financial assets while keeping them within DTCC’s existing custody framework.

Live tokenization begins with major public market assets

The first phase of the pilot has started with DTCC tokenizing shares of Microsoft and Circle alongside the Invesco QQQ Trust, the State Street SPDR S&P 500 ETF, and BlackRock’s iShares 0–3 Month Treasury Bond ETF. DTCC has stated that these tokenized assets will be stored at the clearinghouse using blockchain infrastructure.

Participating firms will use the assets in live blockchain transactions covering collateral transfers, repo agreements, and equity trades during the trial. The program is expected to move into its formal operational phase in October after the current testing period.

Separately, DTCC confirmed through a live update that JPMorgan completed the first conversion in the pilot by turning shares of the Invesco QQQ Trust ETF into a tokenized real-world asset.

According to DTCC, the conversion demonstrates that tokenized versions of traditional securities can function inside existing market infrastructure while preserving the same liquidity, investor protections, transparency, and ownership rights as the underlying assets.

Private blockchain leads current rollout while public network plans continue

Rather than using public layer-1 blockchains such as Ethereum or Solana, DTCC has chosen to settle transactions on either its private Hyperledger Besu blockchain or the Canton Network, depending on the infrastructure selected by participating institutions. The approach keeps settlement within permissioned blockchain environments designed for regulated financial markets.

Meanwhile, the project arrives as tokenization continues to gain traction across major financial institutions. The United Kingdom’s Treasury is also advancing a £33 billion tokenization initiative through its Wholesale Digital Markets Taskforce, with BlackRock, Morgan Stanley, and Goldman Sachs among the firms participating in that effort.

Additional plans extend beyond the current pilot. As previously reported by crypto.news, DTCC and the Stellar Development Foundation are preparing DTC custody asset tokenization services on the Stellar public blockchain.

The partners have targeted the first half of 2027 for the launch of live tokenized assets, introducing Stellar as one of the public blockchain networks in DTCC’s developing multi-chain tokenization strategy.

For now, however, the active pilot remains centered on permissioned blockchain infrastructure, giving participating firms an opportunity to test tokenized securities within DTCC’s existing clearing and custody system before the program expands further.

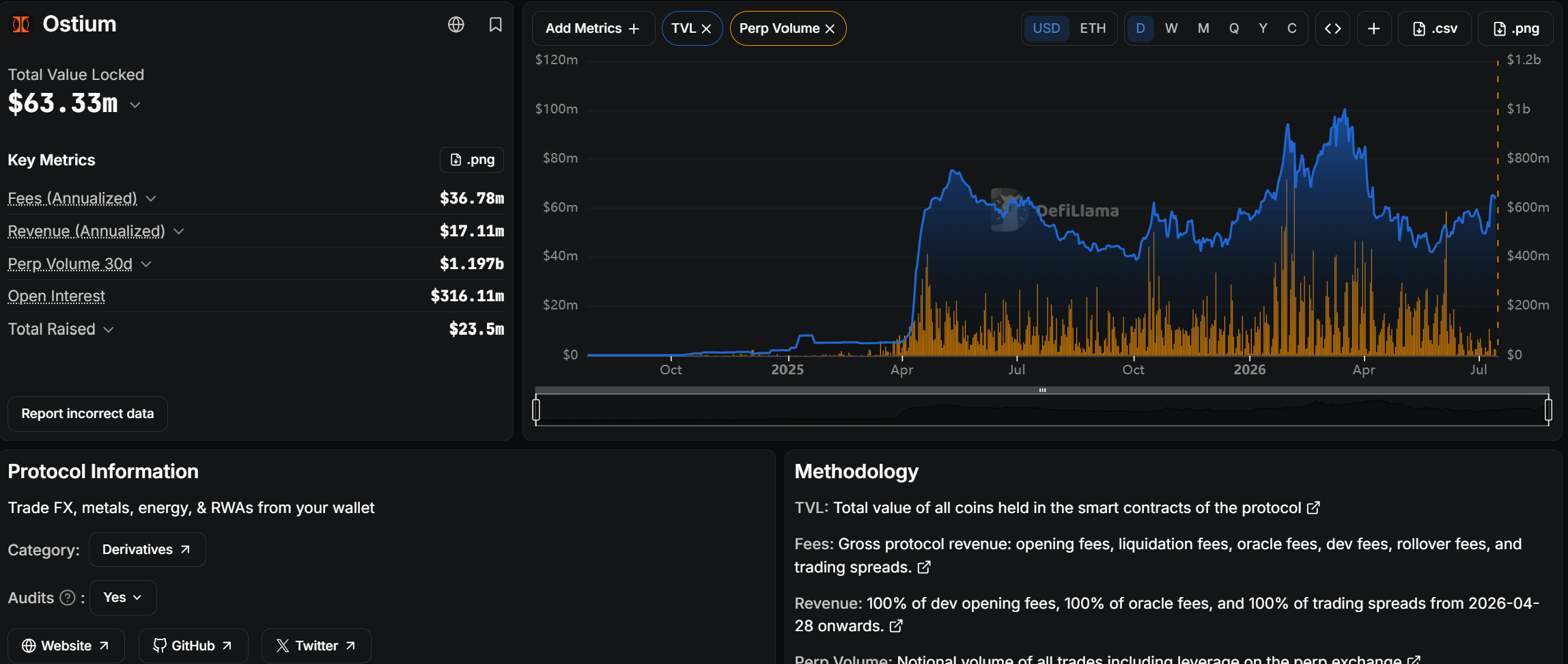

Arbitrum’s RWA perpetual platform Ostium lost nearly $18 million USDC today after attackers compromised an oracle signer key and manipulated prices.

The root cause was a compromised oracle signer private key. This allowed the attacker to bypass verification checks and submit favorable future prices. They executed around 20 looped trades through delegated actions, instantly profiting at the protocol’s expense without genuine market exposure.

Exploit Drains One-Third of Vault in Hours

Security firm Blockaid first flagged the incident, indicating that the attacker used a registered PriceUpKeep forwarder and future-dated authorized oracle reports to generate artificial trading profits. This triggered repeated open-and-close loops that drained funds from Ostium’s main liquidity vault.

Follow us on X to get the latest news as it happens

On-chain data shows roughly $11.86M–$18M USDC extracted from the vault, representing about 28% of its $63 million TVL at the time of the attack. The primary exploit transaction is publicly verifiable on Arbiscan.

Ostium is a leading decentralized perpetuals exchange focused on real-world assets, including equities, commodities, forex, and indices, built on Arbitrum.

Major Backing Meets Major Setback

The protocol had raised approximately $27.8 million from top-tier investors including General Catalyst, Jump Crypto, Coinbase Ventures, Wintermute, and GSR.

Despite strong institutional support and multiple audits, the incident exposes persistent risks in oracle-dependent RWA infrastructure.

The exploit is under active investigation. Users should monitor official channels for withdrawal guidance and security updates. The event highlights the need for hardened oracle key management and real-time monitoring in hybrid DeFi protocols.

As the RWA perpetuals sector grows rapidly, this breach serves as a timely reminder: even well-funded projects remain vulnerable to private-key and oracle attacks.

The post Ostium Perp DEX Hit for $18 Million in Brutal Oracle Exploit appeared first on BeInCrypto.

Decentralized lending protocol Aave has launched V4 on Avalanche, marking the first expansion of its latest lending infrastructure beyond Ethereum and setting the stage for future lending markets backed by tokenized real-world assets.

The deployment introduces Aave V4’s Hub & Spoke architecture, which allows specialized lending markets to operate with their own collateral requirements and risk parameters while drawing on shared liquidity across the protocol.

According to Aave, one of the first planned markets on Avalanche will support borrowing against tokenized assets.

The architecture is designed to support a broader range of collateral than previous versions of the protocol, Aave’s statement said. As well, future specialized markets on Avalanche could support tokenized assets including US Treasurys, money market funds, private credit and corporate bonds, each with customized collateral requirements and risk parameters.

Aave is the largest decentralized lending protocol by total value locked, with nearly $14 billion in assets across 23 blockchains, according to DeFiLlama data.

Source: DefiLlama

Related: Aave brings V3 lending and GHO stablecoin to Monad

Tokenized assets move beyond issuance

The launch comes as financial institutions and blockchain firms are fast building infrastructure and partnerships that allow tokenized assets to be used as collateral across traditional and decentralized finance.

In February, Franklin Templeton partnered with Binance to let institutions use tokenized money market fund shares as off-exchange collateral while keeping the underlying assets in regulated custody.

The following month, Nasdaq announced plans to integrate its collateral management platform with Talos’ digital asset infrastructure to streamline institutional workflows for managing tokenized collateral. The integration is intended to combine collateral management, risk monitoring and trade surveillance within a single platform for institutional digital asset trading.

Market infrastructure providers have also entered the space. In May, DTCC said it would integrate Chainlink technology into its tokenized collateral platform to support near real-time movement, valuation and settlement of tokenized collateral ahead of a planned fourth-quarter launch.

More recently, the push has expanded into institutional lending. On Wednesday, Grove announced a $500 million warehouse lending facility with Galaxy Digital to finance institutional crypto-backed loans using blockchain-based infrastructure.

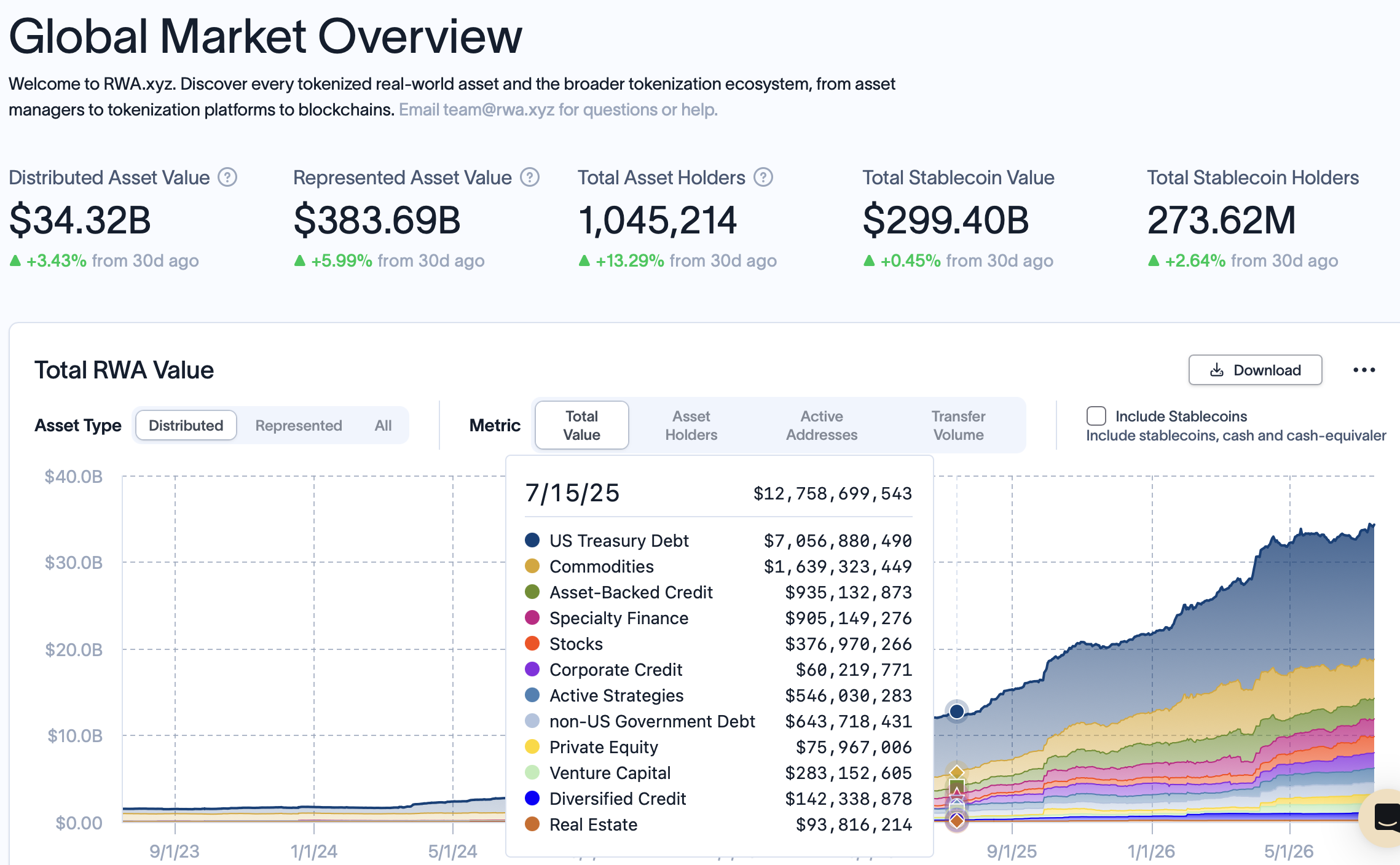

Tokenized real-world assets have become one of the fastest-growing sectors of the digital asset industry. According to RWA.xyz, more than $34 billion worth of real-world assets are currently tokenized on public blockchains, up from about $12.8 billion a year ago.

Magazine: Is Robinhood Chain’s success bullish or bearish for ETH the asset?

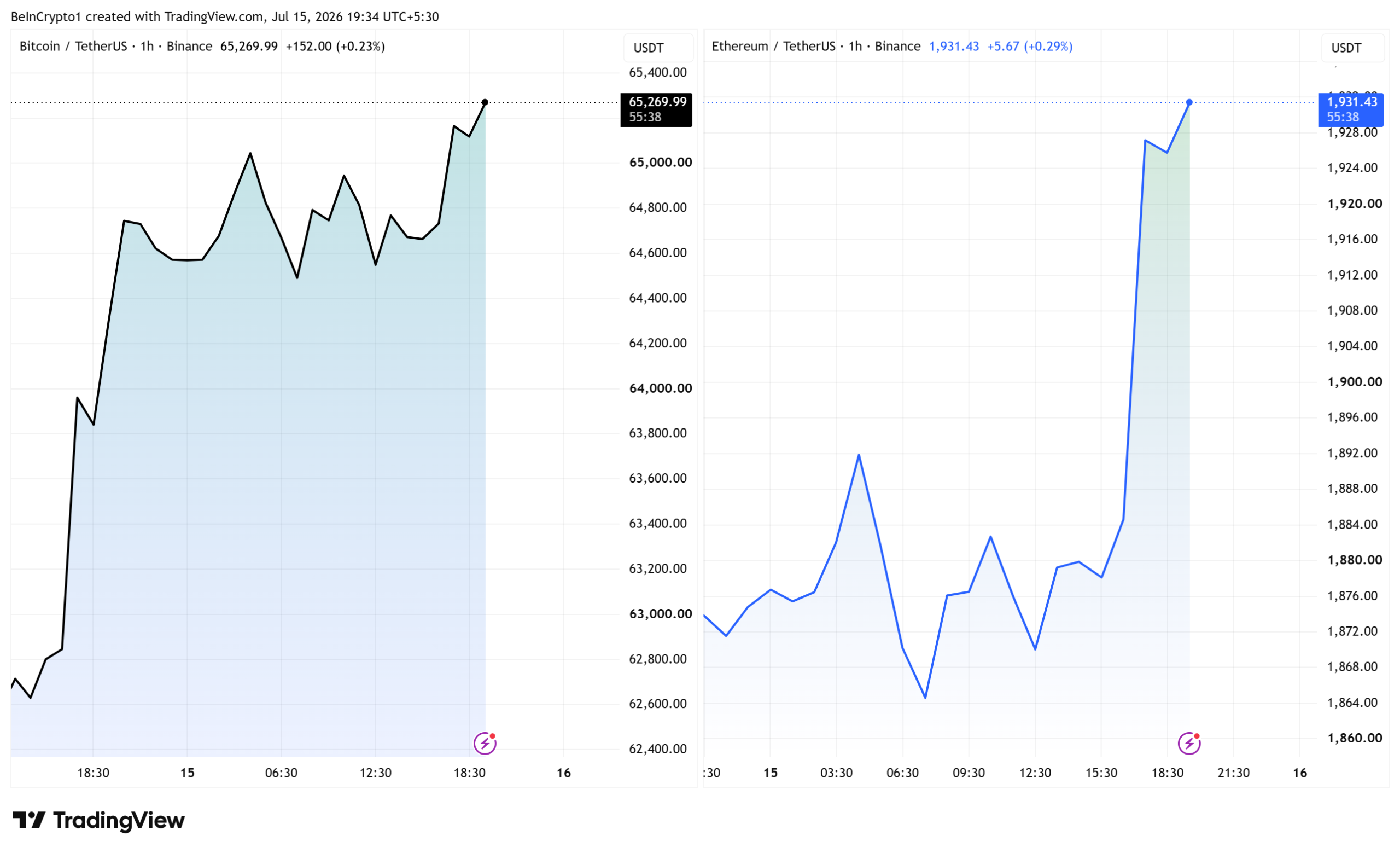

US PPI inflation fell 0.3% in June, the first monthly decline since August 2025. Bitcoin (BTC) reclaimed $65,000 and Ethereum (ETH) topped $1,900 as traders cut bets on a July Fed rate hike.

The producer data landed one day after consumer inflation also missed forecasts. Together, the two reports have shifted market expectations decisively against further Federal Reserve tightening this month.

PPI Inflation Reinforces the Disinflation Trend

Bureau of Labor Statistics data showed headline PPI at 5.5% year-over-year, below the 6.2% consensus. Core PPI eased to 4.7% against a 5.2% forecast. May’s monthly rise was also revised down from 1.1% to 0.6%.

The 0.3% monthly drop was the sharpest since April 2025. Only a month ago, annual PPI stood at 6.5%, its highest level since December 2022.

Energy drove most of the relief. Gasoline prices fell 12%, accounting for nearly two-thirds of the 1.4% slide in final demand goods.

Even after that drop, gasoline remains nearly 43% higher than a year earlier. Services held firmer, with trade margins up 0.4%.

The print builds on the CPI surprise a day earlier, when consumer inflation cooled faster than economists anticipated. Both reports strengthen the case for lower Treasury yields, supporting equities and digital assets alike.

Fed Hike Odds Collapse as Crypto Rallies

CME FedWatch data now shows an 87.7% probability that the Fed holds rates at 3.50% to 3.75% on July 29. Hike odds dropped to 12.3%.

The repricing came fast. Markets saw a 31% chance of a hike just one week ago, before consecutive soft inflation reports flipped the positioning.

The central bank held rates steady at Chair Kevin Warsh’s first meeting in June, flagging inflation risks from artificial intelligence spending.

Warsh struck a harder tone in congressional testimony a day before the release, saying the central bank has

“No tolerance for persistently elevated inflation,” Kevin Warsh, Federal Reserve Chair said in his testimony.

Bitcoin traded near $65,256 after the release, up 2.5% in 24 hours. Ethereum gained 3.6% to $1,930, its first move above $1,900 since early June.

The rebound liquidated nearly $100 million in crypto shorts within 30 minutes. A similar short squeeze fueled Bitcoin’s recovery in early July, when weak jobs data drove BTC to the $62,000 area.

Still, the relief may prove fragile. Gasoline drove much of June’s decline, and oil has pushed above $85 after President Donald Trump announced a Strait of Hormuz blockade on Monday.

The waterway carries about one-fifth of the world’s oil. A hotter energy print could stall the disinflation story as soon as next month.

The next test for BTC sits at the $66,000 resistance zone that has capped gains since mid-June.

The post US PPI Lands Soft, Fed Rate Hike Odds Lower as Bitcoin Price Reclaims $65,000 appeared first on BeInCrypto.

Democratic Senator Chris Murphy has accused the CLARITY Act of protecting President Donald Trump’s crypto business interests, intensifying a Senate fight over the digital asset bill just as lawmakers prepare for a floor vote.

Summary

- Chris Murphy has accused the CLARITY Act of shielding Trump’s crypto business interests.

- Senate Democrats are demanding stricter conflict-of-interest rules before backing the bill.

- The Senate is expected to begin considering the CLARITY Act between July 15 and July 20.

According to statements made during a July 14 Capitol Hill press conference, Murphy argued that the legislation, in its current form, would fail to prevent the president from profiting from an industry that Congress is attempting to regulate.

His remarks came shortly after Trump’s latest financial disclosure reported roughly $1.4 billion in crypto-related income, largely tied to his family’s involvement with World Liberty Financial.

Democratic opposition centers on conflict-of-interest provisions

Speaking at the press conference, Murphy described the CLARITY Act as legislation that would “essentially legalize Donald Trump’s crypto corruption scheme.”

A video of his remarks was later shared on X. Murphy argued there is little justification for creating a new crypto regulatory framework if it does not stop elected officials from benefiting financially from the sector they oversee.

Standing alongside Murphy, Senators Jeff Merkley and Chris Van Hollen repeated calls for stronger ethics rules before the bill advances. The lawmakers said they want explicit provisions preventing the president, vice president, members of Congress, and their immediate families from profiting from crypto businesses that could be affected by future regulation.

The latest criticism follows an earlier push by Senate Democrats. Five days before the press conference, ranking Democrats across five Senate committees, including Senator Elizabeth Warren, requested hearings into Trump’s crypto interests after reviewing his financial disclosures.

According to those lawmakers, the filings indicated that crypto ventures operated by Trump’s family generated most of his reported income.

Those ethics concerns have become a central issue as the Senate debates legislation that would divide oversight of digital assets between the Commodity Futures Trading Commission and the Securities and Exchange Commission while also establishing consumer protection rules and restricting a U.S. central bank digital currency.

Senate vote approaches as negotiations continue

Attention has now shifted to the Senate calendar after Senator Cynthia Lummis confirmed on July 15 that the joint Banking and Agriculture Committee draft has been completed and is ready for introduction on the Senate floor.

Trump has separately urged lawmakers to move quickly on the CLARITY Act, although his financial disclosures have added fresh political pressure to that request. The Senate version has been under negotiation for more than ten months, with discussions over stablecoin yield provisions joining the debate alongside ethics concerns.

Industry groups continue to support the legislation despite the political dispute. Coinbase executives have argued that clear crypto rules are necessary to keep U.S. digital asset markets competitive with jurisdictions such as China and the European Union, describing regulatory certainty as a national security issue.

For crypto investors, the legislative timeline remains important because many analysts continue to link institutional participation in digital assets with regulatory certainty in the United States. XRP, in particular, has frequently been viewed by market participants as one of the assets most sensitive to progress on the CLARITY Act because of its long-running regulatory history.

The next phase is expected between July 15 and July 20, when Lummis has indicated the Senate floor process could begin. Whether Senate Majority Leader John Thune schedules the bill quickly, or negotiations over conflict-of-interest provisions delay its consideration, will determine how the legislation moves through its final stage and whether Democratic ethics demands become part of the final package.

Early in Donald Trump’s second term, his special advisor, Elon Musk, began to promote a conspiracy theory that suggested that Fort Knox didn’t contain the gold it was supposed to.

This was always nonsensical; documents released in Trump’s first term confirm that the Treasury Office of Inspector General conducts “audits of United States Mint Custodial Gold Schedules” on an annual basis.

This audit “includes an inspection of all gold compartments and joint seals to verify the compartments are locked, and the seals are in-tact and have not been tampered with.”

Furthermore, despite Musk promoting the claim that the gold hadn’t been seen since 1974, during Trump’s first term it was actually visited by then Treasury Secretary Steven Mnuchin and then Senate Majority Leader Mitch McConnell, and photos of them inside the vault were released.

Read more: Zero Hedge invited to White House press pool despite lies about Fort Knox gold

Recently, Scott Bessent, the current treasury secretary, went on Jesse Watters’ show on Fox News and confirmed that all the gold is present and accounted for — over $1 trillion worth in total.

Musk, for his part, hasn’t posted about this most recent confirmation, with his last X post about Fort Knox coming in February of last year.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

F*** Messi

Hubble Captures LH 59, Showcasing Crimson Clouds Where Stars Take Shape

Does FIFA have a financial incentive to keep Lionel Messi in the World Cup?

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Does FIFA have a financial incentive to keep Lionel Messi in the World Cup?

Bitcoin: From $1 to $2 Trillion Industry – Masterclass on Blockchain & Finance | Jayasim Jayakumar

The Crypto Market Just Flipped (Michael Saylor & Gary Vee)

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics5 hours ago

Politics5 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos22 hours ago

News Videos22 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech21 hours ago

Tech21 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos7 days ago

News Videos7 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech7 days ago

Tech7 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World7 days ago

Crypto World7 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World1 day ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Crypto World7 days ago

Crypto World7 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login