Crypto World

JPMorgan Gives Bold Nvidia Price Prediction, But Is It Realistic?

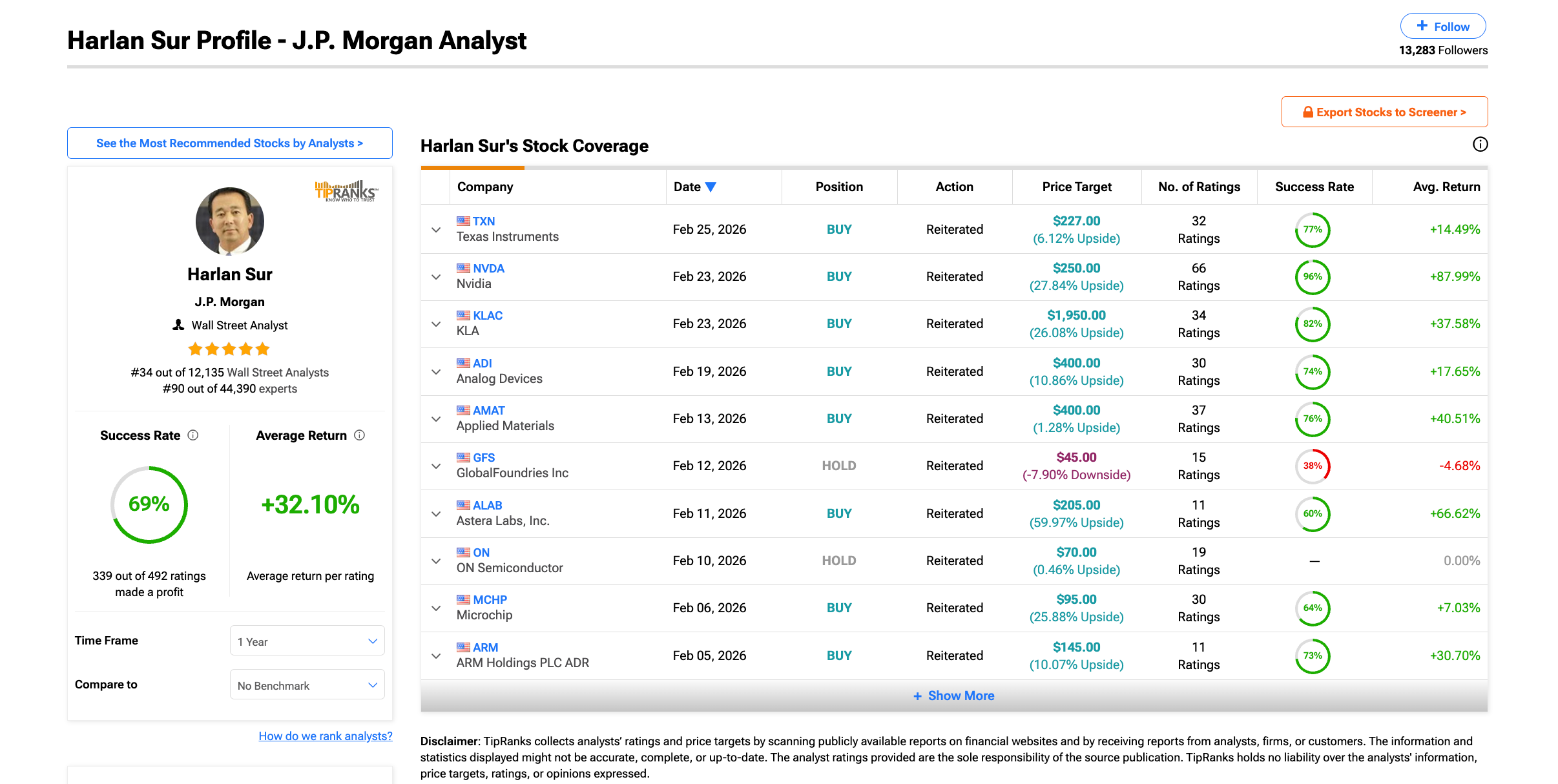

NVIDIA Stock just delivered a record-breaking Q4 with $68.1 billion in revenue, 73% year-over-year growth, and earnings per share of $1.62 that crushed estimates. JPMorgan, among others, wasted no time raising its price target from $250 to $265.

Yet on February 26, the stock fell nearly 7% from its session high of $197 to under $185. The results are undeniable. But the price action, the money flow, and the institutional behavior tell a very different story. At least, for now.

The Numbers Look Bulletproof, Until You Look Closer

NVIDIA’s Q4 numbers speak for themselves. Revenue hit $68.1 billion, up 73% year-over-year. The data center segment alone pulled in $62.3 billion, making up 91% of total revenue. EPS (Earnings Per Share) of $1.62 beat the $1.53 consensus by nearly 6%.

And the Q1 FY2027 guidance of $78 billion blew past Wall Street’s $72.8 billion estimate — a figure that notably excludes any revenue from China.

JPMorgan analyst Harlan Sur responded by lifting the Nvidia price target from $250 to $265.

But here is what most analysts are not highlighting. NVIDIA’s quarter-over-quarter growth rate is quietly decelerating. Q3 grew 22% over Q2. Q4 grew 19.5% over Q3.

The Q1 guidance implies roughly 14.5% sequential growth. Revenue keeps hitting records, but the pace of acceleration is fading. For a stock priced on growth momentum, this distinction matters. Something big money might be watching.

There is also the question of who is actually driving this revenue. Deepwater Asset Management’s Gene Munster estimates that roughly 70% of Nvidia’s revenue comes from just 8 companies.

CFO Colette Kress confirmed that the top 5 hyperscalers (cloud computing providers) account for slightly over 50% of data center revenue. That level of customer concentration means that even a modest 10-15% reduction in AI capex from a few major buyers could translate into billions in lost quarterly revenue.

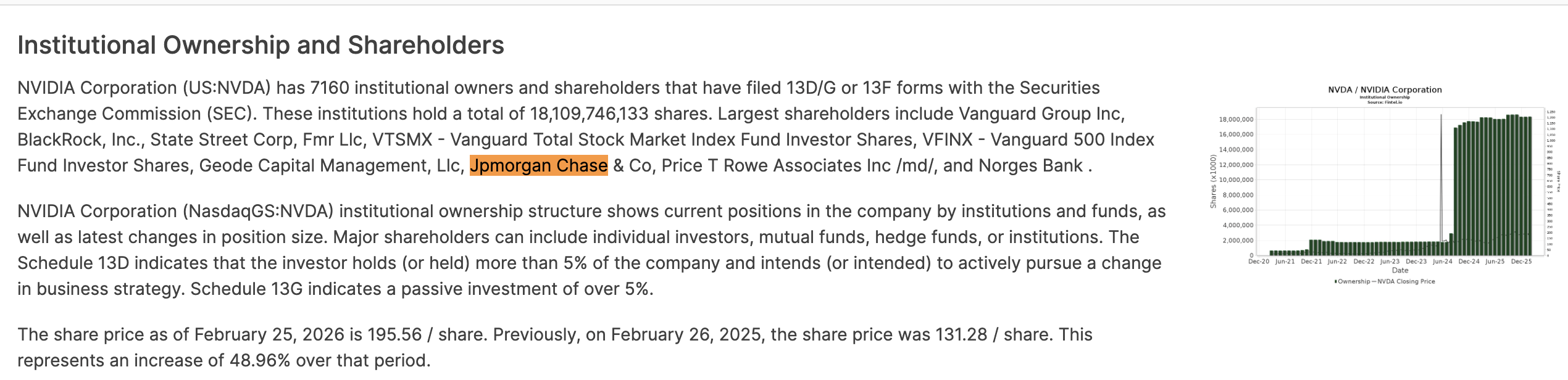

It is also worth noting that JPMorgan’s asset management division is itself a significant institutional holder of Nvidia.

This is standard on Wall Street, but it is a context that retail investors should be aware of when evaluating the bullishness behind a price target upgrade.

What Retail NVDA Investors See vs What Institutions Are Doing

On-Balance Volume (OBV), an indicator that tracks cumulative buying and selling pressure by adding volume on up days and subtracting it on down days, tells a positive story on the surface.

OBV has maintained higher highs throughout Nvidia’s 3-month consolidation, suggesting retail-driven buying pressure remains consistently positive. However, it still needs to break past its ascending trendline resistance to confirm genuine broad-based strength.

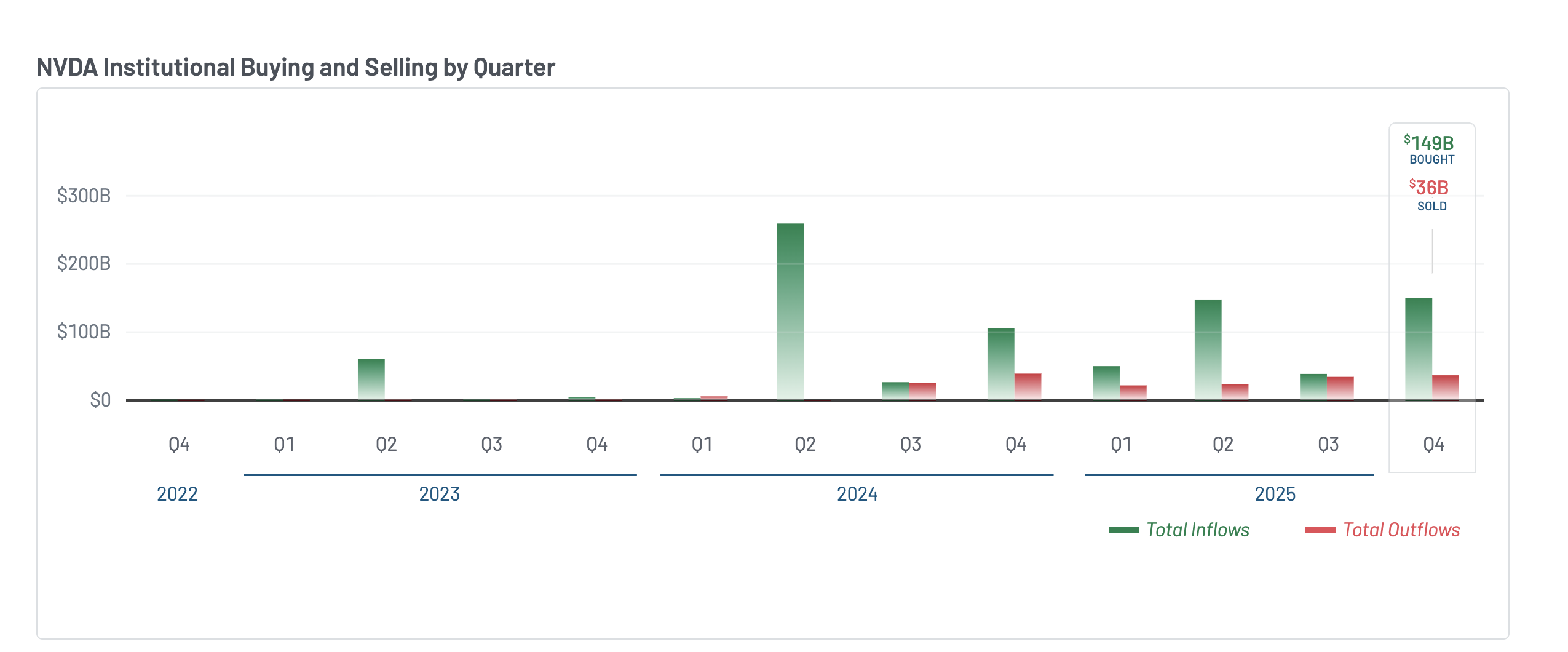

The most recent 13F filings (quarterly reports large investors must file with the SEC revealing their positions) for Q4 2025 show a dramatic shift in institutional sentiment.

Net institutional money flow surged to approximately $149 billion in purchases against $36 billion in sales — a net inflow of roughly $113 billion. That is a massive improvement from Q3, where institutions bought $38 billion and sold $34 billion, leaving a net inflow of just $4 billion.

Yet despite this wall of institutional money entering NVDA in Q4, the stock barely moved — trading sideways for most of the period. That suggests institutions were accumulating, but supply from insiders and earlier holders absorbed the demand. NVIDIA director Mark Stevens sold approximately $40 million in shares in December.

Bank of America, while slightly increasing its equity stake, closed out both its call and put options positions entirely — neutralizing its directional bets.

Institutions are clearly positioned. But the hedging and the flat price despite massive inflows suggest they are bracing for something. The next section explores what that might be.

The Risk Hiding in the Charts

The Chaikin Money Flow (CMF), an indicator that measures whether money is flowing into or out of a stock based on where the price closes within its daily range weighted by volume, reveals what the earnings headline does not.

Since February 5, as the right shoulder of Nvidia’s inverse head and shoulders pattern formed, CMF climbed steadily alongside the price. It rose all the way into the February 25 earnings breakout when Nvidia briefly touched $197.

Then on February 26, as the stock reversed sharply to $185, CMF plunged.

That sudden collapse suggests the money flowing in during the rally was speculative positioning — not committed institutional capital — and it evaporated the moment the breakout failed. And based on what we discussed earlier, revenue deceleration could be a reason.

The monthly VWAP (Volume Weighted Average Price, which approximates where institutions have built their positions) reinforces this. NVIDIA had been trading above its monthly VWAP since breaking out on February 17.

The last time Nvidia broke below the monthly VWAP was on January 30, which led to a correction of approximately 8.5% by early February.

As of February 26, the stock has once again fallen below this line. This means recent institutional buyers are now underwater, which historically triggers further selling as stop losses unwind.

The technical breakdown has context. Michael Burry flagged today that Nvidia’s supply commitments have ballooned to levels that mirror Cisco before the dot-com bust — a company that wrote down billions when demand didn’t meet expectations.

CFO Kress acknowledged Nvidia has locked in inventory “further out in time than usual.” Bulls like BofA’s Vivek Arya argue this secures Nvidia’s dominance. But CMF collapsing and VWAP breaking on the same day suggests the market isn’t waiting to find out who’s right.

The NVIDIA Stock Price Levels That Decide What Happens Next

The charts, the money flow, and the institutional positioning all point to the same conclusion — $195 is where conviction gets tested, a level highlighted later on the chart. But first, the risk.

On the daily chart, a hidden bearish divergence has formed between November 10 and February 25. During this period, the NVIDIA stock price made a lower high while the Relative Strength Index (RSI), a momentum indicator, made a higher high

It is a signal that upward momentum is quietly fading even as the stock appears to hold its range.

Since that November divergence started developing, Nvidia has been locked between $169 and $199. It couldn’t break out of this consolidation despite multiple attempts — including the inverse head-and-shoulders breakout on February 25, which failed within 24 hours.

The Fibonacci extension levels from the pattern now frame what comes next. On the downside, $183 at the 0.5 level is the immediate support. Below that, $180 at the 0.382 level becomes critical — a break there exposes $170, the right shoulder low, and $169, the head. Those levels would invalidate the pattern entirely.

On the upside, the neckline at $195 remains the key resistance and the conviction tester. A clean daily close above it, which the NVIDIA stock failed to do yesterday, is needed to reactivate the pattern.

That could push it towards the projected target at $226, the full head-to-neckline measurement.

The next extension at $235 brings it closer to JPMorgan’s $265 target. The path exists on paper.

But as the money flow, the hidden bearish divergence, and today’s 7% rejection all confirm, this is a market that’s not buying it yet.

The stablecoin company had a strong 2025 and is exploring a token launch for Arc, its new Layer 1 blockchain.

Circle’s stock, CRCL, is up 40% over the last two trading days after the company unveiled its Q4 2025 report, showcasing a 64% increase in revenue and 104% growth in earnings year over year (YoY).

The report sent CRCL rallying from $61 per share to $86.25, as the company also shared an 82% increase in total USDC minted and a 59% increase in what it calls “meaningful wallets,” defined as any onchain wallet holding more than 10 USDC.

The stock appears to be pricing in future growth, as the company still posted a net loss of $70 million in 2025, “significantly impacted by $424 million for stock-based compensation.”

The company also touched on its upcoming Layer 1 stablechain, Arc, which launched its testnet in October.

In addition to Arc’s impending mainnet launch, Circle CEO Jeremy Allaire also revealed that Circle is exploring a native token for the Arc blockchain, but did not reveal any further details.

While the earnings report and subsequent rebound offer some relief for shareholders, CRCL is still down 71% from its all-time high of $300, reached shortly after its initial public offering (IPO).

Since dropping by 35% from Jan. 14 to Feb. 5, Bitcoin (BTC) has consolidated in a range from $60,000 to $70,000 over the past 22 days. At the same time, several BTC adoption-linked metrics are moving in different directions across exchange-traded funds (ETFs), whales, miners and corporate Bitcoin treasuries.

These divergences highlight steady capital commitment beneath muted price action and how each signal fits into the bigger picture.

Bitcoin ETF flows remain negative

The 90-day rolling average of US spot Bitcoin ETF net flows has dropped to -$2.18 billion. Over the past two years, the metric has turned negative only twice: from March to May 2025, and in the current stretch that began on December 11, 2025. In both instances, Bitcoin followed with a corrective phase.

When the rolling average turns negative, it means more money is leaving ETFs than coming in over a longer period. That reduces buying pressure, weakens overall demand, and can make it harder for prices to move higher.

A move back above zero, followed by steady inflows, may mark the return of institutional participation. Sustained positive readings tend to align with stronger price action from BTC, alongside improving liquidity conditions.

BTC whale accumulation versus dominant trend

CryptoQuant data tracks the one-year change in total whale holdings and its 365-day moving average. Addresses holding 1,000 to 10,000 BTC added more than 200,000 BTC from June to November 2023, while the price ranged from $25,000 to $30,000.

When the raw one-year change crosses above its 365-day average, whales are accumulating faster than their longer-term trend. That crossover in 2023 coincided with supply absorption during sideways trade, which eventually led to BTC’s bullish rally.

Thus, a bullish trend may unfold for BTC once the one-year change sustainably moves above its moving average (365-SMA), signaling renewed large-scale absorption.

Hash rate and infrastructure signal

Bitcoin’s 30-day mean hash rate stands near 0.99 ZH/s after peaking at 1.10 ZH/s in November 2025. Both hash rate and price have moved lower in recent weeks.

Hash rate measures the computational power securing the network and reflects miner investment in hardware and energy capacity. Rising hash rate during price consolidation points to infrastructure expansion independent of short-term price gains.

If the hash rate trends higher while the price trades sideways, it points to a stronger long-term commitment from miners. A sustained divergence, where hash rate rises ahead of price, can signal growing confidence within the mining sector.

Likewise, miner economics must also improve. Stabilizing the hash price and lower miner sell pressure confirms that rising computational power is backed by healthier revenue conditions rather than tightening margins.

Related: Analysts reject Jane Street ‘10 a.m. dump’ claims, say Bitcoin isn’t easily manipulated

Corporate BTC treasury concentration cools

A recent report from bitcointreasuries.net noted that treasuries added about 43,200 BTC in January, with Strategy accounting for about 40,150 BTC.

Zooming out, the chart shows that corporate accumulation by Strategy has slowed significantly since late 2024. Monthly additions peaked near 148,000 BTC in November 2024 and 87,000 BTC in July 2025.

Recent monthly figures are materially lower, and the last 30-day increase represents only a marginal change relative to the 1.13 million BTC now held by public companies.

The latest monthly net increase equates to roughly 0.1% growth relative to total public company holdings. That pace signals stability rather than acceleration in treasury expansion.

For BTC price, broader and accelerating treasury inflows help absorb available supply more effectively. Slower increases, by contrast, signal companies are largely maintaining positions rather than driving new demand.

Related: Bitcoin bear market not ‘over already’ as price rejects at $68K trend line

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

TLDR

- Circle shares surged nearly 50% within two sessions after the company reported fourth quarter earnings.

- Analysts said a short squeeze drove the rally rather than a change in the company’s fundamentals.

- Hedge funds had built large bearish positions before the earnings release, which led to rapid short covering.

- USDC circulation rose 72% year over year to $75.3 billion during the quarter.

- Circle reported a net loss of $70 million for 2024 compared with a net profit in the prior year.

Circle shares surged nearly 50% within two sessions after the company released fourth quarter earnings on Wednesday. The rally followed an 80% decline from record highs reached last year and reversed recent losses. Analysts said short covering, rather than improved fundamentals, powered most of the advance.

Circle Earnings Trigger Short Squeeze

Circle reported strong growth in USDC circulation during the fourth quarter. The company said USDC supply reached $75.3 billion, up 72% year over year. However, analysts linked the sharp share price jump to hedge fund positioning.

Markus Thielen, founder of 10x Research, said positioning drove the move. He stated, “The magnitude of the move was not driven purely by the headline numbers.” He added, “The real catalyst was positioning,” and described the rally as a “high-probability short squeeze rather than a fundamental re-rating.” He estimated hedge funds lost about $500 million in one day on short positions.

Hedge funds had built large bearish bets before the earnings release. As the stock climbed, short sellers rushed to cover positions. Consequently, buying pressure accelerated and pushed shares sharply higher.

The surge broke a prolonged downtrend that had erased most of last year’s gains. Shares had fallen about 80% from prior record levels before the earnings report. The rapid rebound followed heavy trading volumes across sessions.

USDC Growth Contrasts with Profitability Decline

Circle’s flagship stablecoin, USDC, expanded in circulation during the quarter. The company reported $75.3 billion in USDC supply, which outpaced Tether’s USDT growth rate. Harvey Li, founder of Tokenization Insight, highlighted the supply increase in a research note.

Revenue from reserve income rose 58% to $2.64 billion. Circle earns reserve income mainly from U.S. government debt backing USDC. However, distribution costs climbed 66% to $1.66 billion during the same period.

Despite higher circulation, Circle posted a net loss of $70 million for 2024. The company had reported a $156 million net profit in 2023. Li said, “Stablecoin may be scaling; stablecoin issuance is a tough business.”

Japanese investment bank Mizuho raised its price target on Circle to $90 from $77. The bank cited stronger fourth-quarter results and growth linked to prediction markets. However, it kept a neutral rating and warned that lower rates could pressure reserve income.

Analysts Dan Dolev and Alexander Jenkins said revenue and profit exceeded expectations. Management pointed to prediction and betting platforms, including Polymarket, as drivers of USDC growth. Executives also described USDC as a potential default currency for AI agents in digital marketplaces.

Mizuho projected an average USDC circulation of about 123 million in 2027. The bank modeled reserve income near $3.7 billion and EBITDA of $916 million for that year. It applied a 24x EBITDA multiple and set a $90 price target.

Bloomberg is collaborating with Kaiko, a Paris-based digital asset market data provider, to make Bloomberg’s licensed financial data accessible directly within blockchain environments rather than through traditional offchain databases.

The companies said Thursday that the initiative is designed to address the challenge of inconsistent data across tokenized markets.

In many tokenized asset ecosystems, companies may rely on different versions of pricing data, security identifiers or reference information, increasing the risk of discrepancies and operational inefficiencies.

By enabling a common, licensed data source to be embedded onchain, the collaboration aims to ensure that market participants reference the same dataset, potentially reducing reconciliation disputes and improving data integrity.

The first use case focuses on tokenized US Treasurys and repo markets operating on the Canton Network, a permissioned blockchain network designed for institutional financial applications. Kaiko launched that data on-ramp service in August.

The integration targets banks, asset managers and other regulated financial institutions experimenting with blockchain-based versions of traditional financial instruments, rather than retail crypto traders.

Questions around data reliability and market size in tokenized real-world assets (RWAs) have surfaced before.

In May, Cointelegraph interviewed Chris Yin, co-founder of RWA platform Plume, who said that the tokenized asset market may be significantly smaller than figures cited by some industry aggregators. At the time, Yin said the sector’s actual size was likely closer to half of what major data sources were reporting.

Related: Hong Kong to link new digital bond platform with regional tokenization hubs

Why data integrity matters for tokenized markets

Kaiko CEO Ambre Soubiran said institutional-grade data is essential for well-functioning financial markets, stating that the collaboration with Bloomberg “will extend the availability of market data used in traditional markets to now support the next generation of tokenized securities infrastructure.”

Kaiko expanded its footprint in the digital asset data sector with its 2024 acquisition of European crypto index provider Vinter, strengthening its presence in regulated benchmark and index services across Europe.

Reliable data has long been a priority in the digital asset industry, where market participants have relied not only on price feeds but also on onchain analytics and sentiment indicators to improve transparency.

In tokenized markets, particularly those linked to real-world assets like Treasurys, consistent pricing data and reference information help ensure that onchain assets accurately mirror the underlying financial instruments.

Related: Aster’s quiet relisting on DefiLlama leaves ‘big gaps’ in data: Exec

Crypto World

The network is moving away from being a slow giant to become a high-speed ‘internet of value’ by 2029

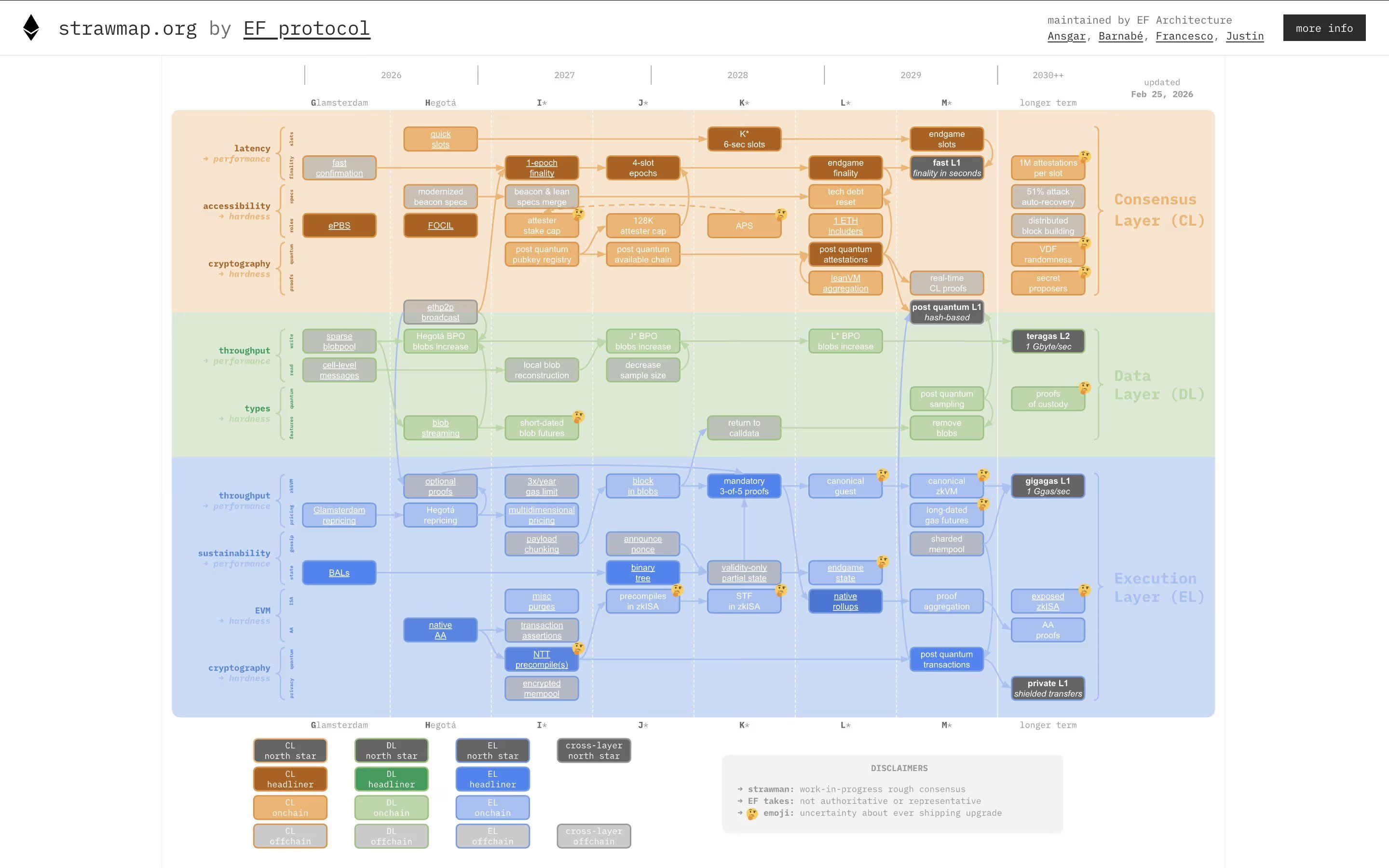

The Ethereum Foundation’s newly released “Strawmap” reads, at first glance, like something only a protocol researcher could immediately comprehend. It’s dense, diagram-heavy and packed with references to forks, zkEVMs and data availability sampling.

But beneath the technical language is a far simpler story: Ethereum — the second-largest blockchain with more than $200 billion market cap — is trying to decide what kind of infrastructure it wants to be by the end of the decade.

The ‘Strawmap’ — explicitly framed as a draft, not an official plan — sketches out Ethereum upgrades through 2029. It is not binding, but it signals where some of the network’s most influential researchers believe the base layer should head next.

“The Strawmap is largely independent from Ethereum governance… it’s a tool that helps inform R&D well ahead of Ethereum governance, potentially even years ahead,” Justin Drake, a prominent Ethereum Foundation researcher, told CoinDesk in an interview.

That direction has real consequences beyond core developers.

At the center of the document are five ambitions: near-instant transaction finality, dramatically higher throughput, built-in privacy, quantum-resistant cryptography and tighter integration between Ethereum’s base layer and its layer 2 ecosystem.

Stripped of jargon, the goal is straightforward: make Ethereum faster, more scalable, more private and durable enough to last a long time.

Today, Ethereum transactions are included in blocks quickly, but the point at which they are considered irreversible, known as finality, takes too long (roughly 16 minutes). For most casual users, that nuance is invisible. For exchanges, bridges and financial applications, it’s critical.

In a thread responding to the roadmap, Ethereum co-founder Vitalik Buterin laid out how that could change. “Today, finality takes 16 minutes,” he wrote, adding that the goal is to “decouple slots and finality” and move toward a system where “endgame finality time might be eg. 6–16 sec.”

Moving from minutes to seconds changes how comfortably large amounts of value can move across the network.

The Layer 2 debate

Earlier this month, Buterin argued that some of the assumptions behind the original layer 2 roadmap “no longer make sense” in their earlier form. Layer-2 networks were previously incorporated into Ethereum’s roadmap to scale the network by processing transactions off the main blockchain and settling them back to Ethereum, helping reduce congestion and fees.

However, as layer 1 or base layer scaling has improved and some rollups have taken longer than expected to decentralize, the idea that Ethereum would outsource most of its scaling burden entirely to L2s has become less clear-cut.

Instead, Buterin suggested a more balanced future — one where the base layer continues to strengthen while layer 2 networks evolve into more specialized roles, whether for privacy, specific applications or enhanced security models.

“Ultimately, we’re going to have finality in seconds,” Drake told CoinDesk, arguing that faster settlement will “help with bridging between the L2s” and improve user experience.

The Strawmap reflects that shift. It doesn’t necessarily say layer 2s will go extinct, but neither does it treat layer 1 as frozen. Instead, it builds on a stronger base layer, alongside improvements that enable significantly higher layer 2 capacity, which could be seen as a dual-track scaling strategy.

Privacy and quantum threat

Privacy marks another notable shift in the draft of the new roadmap.

Ethereum’s transparency has long been viewed as a positive, as every transaction is visible. But openness limits certain use cases. The Strawmap contemplates native “shielded” transfers at the base layer, which would allow ETH to move without exposing full transaction details publicly. For individuals, that’s a matter of financial discretion. For businesses, it could determine whether certain activities move onchain at all.

And then there’s the long game: post-quantum cryptography. Quantum computing remains a developing field, but if Ethereum is meant to secure trillions in value over decades, its security assumptions cannot remain static. The Ethereum Foundation recently brought together a post-quantum team, and the roadmap only shows that it continues to double down on these efforts.

For developers and businesses, the roadmap provides directional clarity. Ethereum has often been criticized for moving slowly or for perpetually delaying the timelines of upgrades. By publishing a multi-year sketch, researchers are signaling that the network’s next phase is not just about patching limitations.

Ethereum’s history, though, is full of ambitious timelines that are overstretched. Governance in a decentralized system ensures debate and revision. The Strawmap itself acknowledges it will evolve.

“For me, this is ultimately about Ethereum becoming the internet of value, and ether, the asset, becoming money for the internet,” Drake told CoinDesk.

Read more: Ethereum Foundation drops most ambitious roadmap in years, targets finality in seconds by 2029

Bitcoin has inched back toward the $70,000 mark, but traders remain wary as derivatives signals fail to echo the price recovery. On Wednesday, the benchmark cryptocurrency briefly touched the round level after a Tuesday dip to around $62,500, a move that was supported by a fresh wave of inflows into U.S.-listed Bitcoin ETFs. Yet the mood in the derivatives market stayed guarded: the annualized futures premium versus the spot price hovered near 2%, well below a neutral readings range, and options markets showed a cautious stance despite the price rebound. The combination of a tepid cycle in bullish bets and lingering macro and liquidity concerns suggests that bulls may need a more durable catalyst before revisiting higher targets, such as $75,000. For context, Bitcoin has been trading in a choppy corridor as market participants weigh the near-term risk-and-reward dynamics.

Bitcoin has retested the $70,000 level amid a broader risk-off environment that has cooled some of the enthusiasm that followed the earlier rally. Official data indicates that inflows into U.S.-listed Bitcoin exchange-traded funds helped stabilize sentiment over a two-day window, with net inflows of $764 million, partially offsetting $1.2 billion of outflows observed over the prior eight trading sessions. In practice, this signals that institutional demand can surface when prices experience sharper pullbacks, even if momentum remains fragile. The underlying caution, however, is underscored by the futures market where traders appear reluctant to extend bullish exposure through leverage, a sentiment that has persisted since late January when BTC briefly relinquished a long-standing $85,000 support level.

Analysts tracking the options surface point to a more nuanced risk posture. The 30-day delta skew on BTC options, a proxy for appetite to buy protection versus chasing gains, showed a 14% premium on put options relative to calls on the most recent session, indicating that risk-off hedging remained a priority for many market participants. Although this measure has moved away from the distress levels seen earlier in the week, it remains outside a balanced range, suggesting that professional traders prefer downside protection even as the spot price paused near $70,000. Data from Laevitas.ch, cited in the market commentary, also highlights that the two-month futures annualized premium persists well below the neutral threshold of 5%, with readings around 2% on Thursday.

Beyond pure price mechanics, a spectrum of theories has circulated about what’s keeping Bitcoin under pressure. Some observers have pointed to a potential exogenous shock—quantitative trading activity and internal market dynamics at major venues—that could have contributed to the recent volatility, including episodes linked to well-known trading desks. In particular, a highly publicized line of inquiry has centered on the activities of a prominent quantitative trading firm and its relationship to other liquidity channels in the ecosystem. While those theories have triggered debate, there is no conclusive public evidence tying any single entity to the broader price weakness. The narrative has nonetheless fueled ongoing market chatter about liquidity risk and cross-venue arbitrage.

Is a single entity behind Bitcoin’s price weakness?

Over the past several weeks, a constellation of explanations has circulated for the price pullback from multi-year highs. Some narratives trace the decline to macro headlines and risk-off sentiment, while others hinge on perceived vulnerabilities within the crypto liquidity stack. The discussion intensified when a market-catalyzing event earlier in the year coincided with a broader shift in institutional posture toward risk assets. In parallel, discussions about long-term security risks—some tied to advancements in quantum computing—reappeared in market commentary, prompting blockchain developers to explore on-chain post-quantum cryptography enhancements (for example, proposals centered on upgrading cryptographic resilience).

Within this broader debate, the possibility that several market actors are reconfiguring leverage and hedging strategies has drawn attention. Recent filings from major trading firms in the context of public equity positions have sparked speculation about delta-neutral approaches and how those strategies might intersect with crypto exposure. One notable thread has involved the public disclosures of holdings that intersect with Bitcoin-related instruments, underscoring how large players may be combining on- and off-chain positions to manage risk.

Meanwhile, price action has occasionally mirrored shifts in benchmark technology equities, with macro-driven risk-off moves weighing on speculative bets. A notable signal came from a sector that often correlates with sentiment across growth and tech equities: a sharp daily decline in a leading semiconductor stock, historically viewed as a bellwether for risk appetite. The implication is not that Bitcoin’s trajectory directly mirrors that stock, but that broader risk sentiment remains a powerful driver of crypto price behavior in the near term.

On the regulatory and governance front, the crypto community has kept a close eye on proposals aimed at strengthening on-chain security and resilience. Proponents of post-quantum readiness have advanced technical ideas, including on-chain upgrades that could reduce future exposure to quantum-related risks. While the market remains in a wait-and-see mode, these technical conversations underscore the industry’s ongoing effort to harden infrastructure in the face of evolving threats.

Another strand of the discourse centers on the role of major exchanges and liquidity providers in shaping market outcomes. In the wake of high-profile liquidations tied to oracle pricing and latency issues, industry participants have emphasized the importance of robust risk controls and transparent pricing mechanisms to prevent cascading effects during periods of stress. While it is difficult to attribute BTC’s price dynamics to a single cause, the confluence of macro headwinds, hedging demand, and structural liquidity considerations appears to be anchoring sentiment at a cautious level as traders monitor the path to the next price milestone.

The conversation around Bitcoin’s price trajectory continues to be informed by a mix of on-chain indicators, derivatives signals, and macro context. While the price flirted with the $70,000 zone, the absence of a broad-based acceleration in bullish bets, coupled with persistent hedging interest, suggests that a sustained move into higher territory will require more than a momentary price bounce. Investors and traders will be watching whether this resilience can translate into a clean breakout or whether the market remains tethered to a diplomatic, risk-aware stance as the year progresses.

Why it matters

The ongoing tension between price action and derivatives signals matters for a wide range of market participants. For retail traders, the current environment underscores the importance of risk management and positioning beyond simple directional bets. For institutions, the pattern of ETF inflows and hedging activity highlights the appetite for crypto exposure when prices pull back, while also signaling caution about leverage-driven risk during periods of volatility. Miners and token issuers watch these dynamics closely because sustained price strength could influence capital expenditure plans and liquidity provisioning.

From a broader market perspective, the narrative around Bitcoin cycles—how price recovers against a backdrop of risk-off sentiment and evolving on-chain security considerations—helps frame the trajectory for other digital assets. The confluence of derivatives mood, ETF flows, and major macro indicators can serve as a guide to the potential impulse needed to push liquid markets back into a more constructive regime. In this sense, Bitcoin’s near-term path remains a useful proxy for assessing risk appetite within the crypto sector and for calibrating expectations around liquidity and institutional engagement in the months ahead.

What to watch next

- Upcoming ETF flow data and their potential to sustain or extend recent inflows, particularly if prices test or breach key levels such as $75,000.

- Public disclosures and 13-F filings from major market participants that could signal shifts in delta-neutral strategies or crypto exposure across portfolios.

- Regulatory or technical updates aimed at post-quantum security on-chain, including any formal governance proposals or implementation milestones.

- Bitcoin volatility and option markets around major expiries, which could amplify price moves if hedging demand surges or wanes.

- Key macro developments that influence risk sentiment and liquidity conditions across traditional and digital-asset markets.

Sources & verification

- Bitcoin price and futures premium data cited from Laevitas.ch, including the annualized premium around 2% and the 5% neutral benchmark.

- Bitcoin put-call delta skew data from Deribit via Laevitas.ch, showing a 14% premium for puts on the latest session.

- Net flows into US-listed Bitcoin ETFs, with $764 million in two days of inflows and prior $1.2 billion of outflows.

- Market commentary referencing on-chain security discussions and post-quantum cryptography proposals (e.g., BIP-360 concepts).

- Industry observations on liquidity dynamics, exchange risk controls, and the impact of large-scale trading activity on price moves.

Market reaction and key details

The near-term narrative remains one of cautious optimism rather than a decisive bullish breakout. While price action has managed to flirt with the $70,000 threshold, the lingering fear in derivatives markets and the absence of broad bullish momentum point to a more nuanced transition phase for Bitcoin. Investors will be watching whether upcoming ETF inflows persist and whether major options expiries bring a clearer signal about the direction of risk appetite. In the meantime, Bitcoin (CRYPTO: BTC) continues to function within a spectrum of hedging considerations and risk-management strategies as market participants weigh the evolving balance of incentives and constraints facing the crypto sector.

Tickers mentioned: $BTC, $NVDA

Market context: The current environment reflects cautious risk sentiment across both crypto and traditional markets, with liquidity conditions and hedging activity shaping short-term moves as macro factors and regulatory considerations continue to influence pricing.

Why it matters: The interaction between ETF flows, futures hedging, and security-focused on-chain proposals determines how quickly the market can transition from a risk-off stance to a more constructive rally, with implications for traders, institutions, and developers alike.

Circle reported strong fourth-quarter results, and it widened the measurable gap in the regulated stablecoin market. The company posted sharp revenue growth, and USDC circulation reached new highs. Meanwhile, Ripple’s RLUSD operates from a far smaller base, and the contrast highlights shifting scale dynamics in dollar-backed tokens.

USDC Expands Revenue Base and On-Chain Footprint

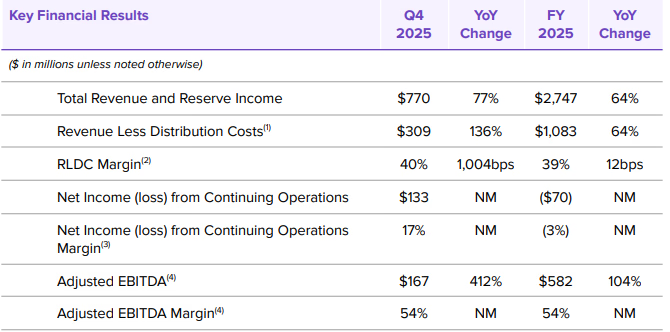

Circle Internet Group increased total revenue and reserve income by 77% year over year in the fourth quarter of 2025. The company generated $770 million, and reserve income accounted for $733 million of that figure. Moreover, reserve income rose 69% from the prior year, even as yields moderated.

USDC’s average circulation doubled during the period, and that expansion supported higher aggregate reserve balances. However, reserve yield declined to 3.8%, reflecting a 68 basis point drop. Even so, larger balances offset lower yields, and overall income continued to grow.

Distribution costs without revenue climbed 136% to $309 million, yet margins improved to 40%. Net income from continuing operations reached $133 million, and adjusted EBITDA rose 412% to $167 million. As a result, Circle strengthened its operating profile while scaling distribution.

USDC closed 2025 with $75.3 billion in circulation, marking a 72% annual increase. In addition, on-chain transaction volume hit $11.9 trillion in the fourth quarter alone. That figure represented a 247% surge, and it underscored rising usage across exchanges and payment channels.

Circle issues USDC as a regulated dollar-backed stablecoin, and it holds reserves in cash and short-duration instruments. The company positions USDC as a compliance-focused alternative within the stablecoin sector. Consequently, growth in circulation directly expands reserve income capacity and reported earnings power.

RLUSD Operates from Smaller Capital Base

Ripple introduced RLUSD to expand its stablecoin presence within global payments and exchange markets. However, RLUSD’s market capitalization stands at $1.56 billion. Daily trading volume remains around $124 million, and that scale limits reserve income potential compared with USDC.

Unlike Circle, Ripple remains privately held, and it does not publish detailed quarterly financial statements. Therefore, direct profitability comparisons remain limited by available disclosures. Even so, the difference in circulating supply creates a clear quantitative contrast.

Stablecoin economics rely on reserve balances and prevailing yields, and larger supplies generally produce higher income. Because RLUSD circulates at a fraction of USDC’s size, its reserve base remains smaller. As a result, operating leverage and reported earnings capacity trail behind USDC’s scale.

Ripple integrates RLUSD into its broader payments network, leveraging established exchange relationships. The company built its reputation on cross-border settlement infrastructure, and RLUSD extends that model into dollar liquidity. Nevertheless, current data show that adoption levels remain significantly lower than those of USDC.

Market observers previously speculated about potential consolidation within the stablecoin segment, including reports about possible acquisition discussions. However, no confirmed transaction has reshaped the competitive landscape. Instead, current standings reflect organic growth and differing starting points.

USDC’s dominance rests on circulation size, reserve economics, and transparent reporting metrics. Meanwhile, RLUSD operates within Ripple’s global framework but from a narrower capital base. The competitive gap, therefore, reflects measurable differences in supply and income rather than structural capability constraints.

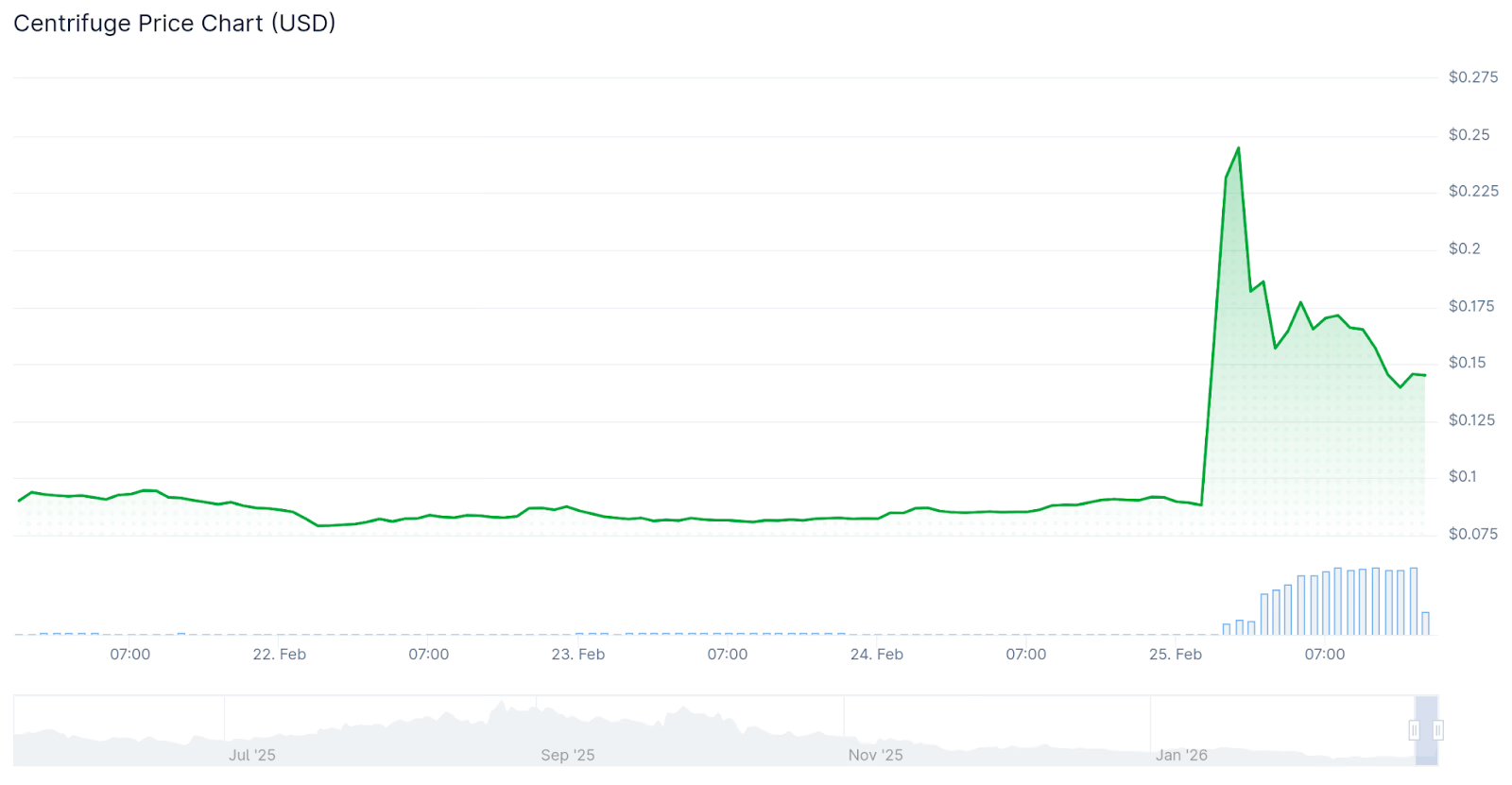

Centrifuge and Espresso experienced explosive moves after being listed on major Korean exchanges this week.

The Korean bid is becoming altcoin holders’ best friend these days, as Korean traders pile into new listings on the country’s leading centralized exchanges (CEXs).

Over the last week, South Korean CEXs Bithumb and UpBit listed two mid-sized altcoins, Centrifuge’s CFG and Espresso’s ESP, and both tokens surged. CFG rallied 177% from $0.088 to $0.24, and ESP jumped by 103% to $0.195.

The Bithumb and UpBit effects have become common at this point, and Korean CEXs have been responsible for plenty of one-time pumps in small- to mid-sized altcoins. While these CEX traders are happy to jump in and speculate on new listings, the effect usually wears off in a few days to weeks as volumes return to their pre-listing levels.

Korean CEX Bithumb also made headlines earlier this month after accidentally sending more than 200 users 2,000 BTC, worth $140 million at the time, instead of 2,000 WON.

The “airdrop” resulted in BTC dropping 18% below the actual market price on Bithumb as recipients rushed to sell the tokens and offramp the funds; however, the exchange successfully froze “most” of the accounts before funds could be withdrawn.

The long-term plan proposes a series of upgrades aimed at faster transactions, higher capacity, and new privacy features.

The Ethereum Foundation (EF) has shared a long-term plan, dubbed the “strawmap,” that outlines how Ethereum could evolve over the rest of the decade, with goals including faster transactions and higher capacity.

The roadmap lays out several possible changes across Ethereum’s core layers. If completed, it would mark the biggest evolution of the network since The Merge in 2022, which moved Ethereum from proof-of-work to proof-of-stake.

The plan underscores how Ethereum developers are preparing the network for more users and more activity by gradually improving speed, security, and reliability. Ethereum co-founder Vitalik Buterin described the roadmap as a “very important document” in a post on X.

Ethereum is currently the world’s largest smart contract blockchain, with more than $56 billion in total value locked (TVL) across decentralized finance, according to DefiLlama. Following the news, Ether (ETH) briefly moved higher. The token is currently trading at $2,030 – down about 2% on the day but still up more than 4% over the past week.

The Details

The strawmap outlines a long-term path with around seven forks through 2029. Justin Drake, a member of the EF Architecture team, explained in a post on X that the roadmap is built around five “north stars.”

These include making the main network faster through shorter block times and near-instant finality, increasing capacity to roughly 10,000 transactions per second on Layer 1, scaling Layer 2 networks to as much as 10 million transactions per second, introducing post-quantum cryptography, and adding native privacy through shielded ETH transfers.

“The strawmap is an invitation to view L1 protocol upgrades through a holistic lens,” Drake said. “By placing proposals on a single visual, it provides a unified perspective on Ethereum L1 ambitions.”

Meanwhile, Buterin described the roadmap as a gradual revamp of Ethereum’s core systems, in which slot times, consensus, and cryptography are replaced bit by bit rather than through a single large overhaul.

The new roadmap builds on Ethereum’s recent upgrades, including Fusaka, which launched in December 2025. That upgrade introduced the PeerDAS data availability system to help the network process more transactions while keeping fees low.

However, while the upgrade marked a major step in the network’s scaling strategy, cheaper transactions have also coincided with a rise in spam and address-poisoning attacks, The Defiant previously reported.

Anthropic CEO Dario Amodei publicly rejected the Pentagon’s demand on Thursday. The Defense Department wants unrestricted military use of the company’s AI technology. The deadline, just hours away, could see the $380 billion startup expelled from the US military’s supply chain.

The showdown marks the first time a major AI company has publicly defied a US government threat to seize control of its technology.

The Standoff

In a blog post published on Anthropic’s website, Amodei called the Pentagon’s threats “inherently contradictory,” noting that one designates Anthropic as a security risk while the other treats Claude as essential to national security.

“Regardless, these threats do not change our position: we cannot in good conscience accede to their request,” Amodei wrote.

The dispute centers on two conditions Anthropic placed on military use of Claude. The company bars autonomous targeting of enemy combatants and prohibits mass surveillance of US citizens. The Pentagon views these as unacceptable limitations on lawful military operations.

Anthropic said the Pentagon’s “final offer,” received overnight Wednesday, failed to address its core concerns. “New language framed as compromise was paired with legalese that would allow those safeguards to be disregarded at will,” an Anthropic spokesperson said in a statement, as reported by The Hill.

Defense Department spokesman Sean Parnell issued a public ultimatum on Thursday. He gave Anthropic until 5:01 pm ET on Friday to grant unrestricted access to Claude Gov — or face termination of the partnership and designation as a supply chain risk.

“We will not let ANY company dictate the terms regarding how we make operational decisions,” Parnell wrote on X.

Timeline of Escalation

On Tuesday, Amodei met directly with Defense Secretary Pete Hegseth, during which Pentagon officials outlined three consequences for noncompliance. First, removal from military systems. Second, supply chain risk designation that would bar other defense contractors from using Anthropic products. Third, the invocation of the 1950 Defense Production Act to legally compel the company to hand over its technology.

Amodei argued in the blog post that the refusal is also grounded in technical reality. “Frontier AI systems are simply not reliable enough to power fully autonomous weapons,” he wrote, adding that without proper oversight, such systems “cannot be relied upon to exercise the critical judgment that our highly trained, professional troops exhibit every day.”

Republican Senator Thom Tillis criticized the Pentagon’s handling of the dispute. “Why in the hell are we having this discussion in public? This is not the way you deal with a strategic vendor,” Tillis told reporters.

What’s at Stake

For Anthropic, the immediate exposure is a $200 million military contract. But the supply chain risk designation carries far broader implications. It would force every defense contractor to verify that they don’t use Anthropic products in their operations.

The competitive landscape is shifting fast. Elon Musk’s xAI signed a deal to use Grok in classified systems, according to Axios, accepting the ‘all lawful purposes’ standard for classified work. OpenAI and Google are accelerating negotiations to enter the classified space. Anthropic, once the only AI company cleared for classified material, risks losing that first-mover advantage entirely.

Why Crypto Should Pay Attention

The Pentagon’s willingness to invoke the Defense Production Act against a technology company sets a precedent that extends beyond AI. If the government can legally compel an AI firm to remove safety restrictions on national security grounds, the same framework could, in theory, be applied to compel crypto companies to modify privacy features or weaken transaction safeguards.

The standoff also strengthens the case for decentralized AI development. A centralized AI provider can be pressured — or legally compelled — to strip away guardrails at a government’s demand. That validates the thesis that decentralized alternatives offer more resilient infrastructure against state coercion.

Anthropic’s rapid growth has already raised concerns for crypto markets. The company’s $380 billion valuation and AI-driven disruption of traditional software revenue are putting pressure on private credit flows that correlate closely with Bitcoin.

Anthropic also has a historical link to crypto: FTX’s bankruptcy estate held a significant early stake in the company, which it later sold to help fund creditor repayments.

The Friday deadline will pass, but the real question begins after: whether the Pentagon follows through, and what that means for every technology company drawing a line between government contracts and product integrity.

Circle Stock Jumps 40% on Q4 Earnings

“Bridgerton” showrunner talks [SPOILER’s] tragic death: Grief 'presents in so many different ways'

BBC Ghosts fans convinced show ‘returning’ as cast share mystery post

-

Video7 days ago

Video7 days agoXRP News: XRP Just Entered a New Phase (Almost Nobody Noticed)

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports3 days ago

Sports3 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics3 days ago

Politics3 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business2 days ago

Business2 days agoTrue Citrus debuts functional drink mix collection

-

Politics1 hour ago

Politics1 hour agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business4 days ago

Business4 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Tech2 days ago

Tech2 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat1 day ago

NewsBeat1 day agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat1 day ago

NewsBeat1 day agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech4 days ago

Tech4 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat4 days ago

NewsBeat4 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics4 days ago

Politics4 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

NewsBeat2 days ago

NewsBeat2 days agoPolice latest as search for missing woman enters day nine

-

Business21 hours ago

Business21 hours agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Crypto World2 days ago

Crypto World2 days agoEntering new markets without increasing payment costs