Crypto World

Memecoin crash leads to death threats

Hailey Welch, known as the “Hawk Tuah girl,” recently spoke about the fallout from the failed launch of the “HAWK” memecoin in 2024, which she promoted.

Summary

- Hailey Welch was cleared of wrongdoing after promoting HAWK memecoin despite facing backlash and death threats.

- The HAWK memecoin, valued at $490M, collapsed to $41M in hours, triggering legal action.

- Despite FBI clearance, Welch faced emotional struggles and continued public criticism after the memecoin’s failure.

Despite cooperating fully with an FBI investigation that cleared her of wrongdoing, Welch faced immense social backlash and personal distress following the memecoin’s collapse.

In December 2024, the HAWK memecoin launched with great fanfare, quickly surging to a market capitalization of over $490 million. However, within hours, the coin’s value dropped sharply, losing over 90% of its value. By the following day, the market cap had fallen to about $41 million. The event was widely described as a rug pull, where investors were left with significant losses.

Welch, who had publicly promoted the token, said that she was unaware of the technical details behind the launch and had no control over the funds. She added that the financial losses for investors were relatively small, estimating the total at around $200,000. However, the social and emotional toll was much greater.

Following the HAWK memecoin’s collapse, Welch received death threats and experienced heightened public scrutiny.

“I was starting to get death threats and everything else. People telling me I owe them all this money, and I’m like, ‘I didn’t do this,’” Welch explained.

She admitted that the backlash took a significant toll on her mental health, causing her to retreat from social media and try to maintain a low profile for months.

Welch’s lawyer emphasized that she had fully cooperated with the FBI investigation, which ultimately found no evidence of fraud or intentional wrongdoing on her part. Despite this, the public backlash continued, with many in the crypto community blaming her for promoting the memecoin.

Legal action and public reactions

After the HAWK memecoin’s collapse, an investor lawsuit was filed against the team behind the launch. The lawsuit accused the entities of selling unregistered securities, but Welch was not named as a defendant. The legal action pointed to the alleged mismanagement and fraudulent nature of the memecoin’s promotion.

Despite Welch’s claims of being a victim of the situation, not all observers were sympathetic. Onchain investigator ZachXBT criticized her involvement in the project, stating,

“She starts posting about meme coins. The entirety of [crypto Twitter] tells her ‘do not launch a token.’ She launches a memecoin anyway, and after, she blames partners and disappears off social media, with followers losing funds.”

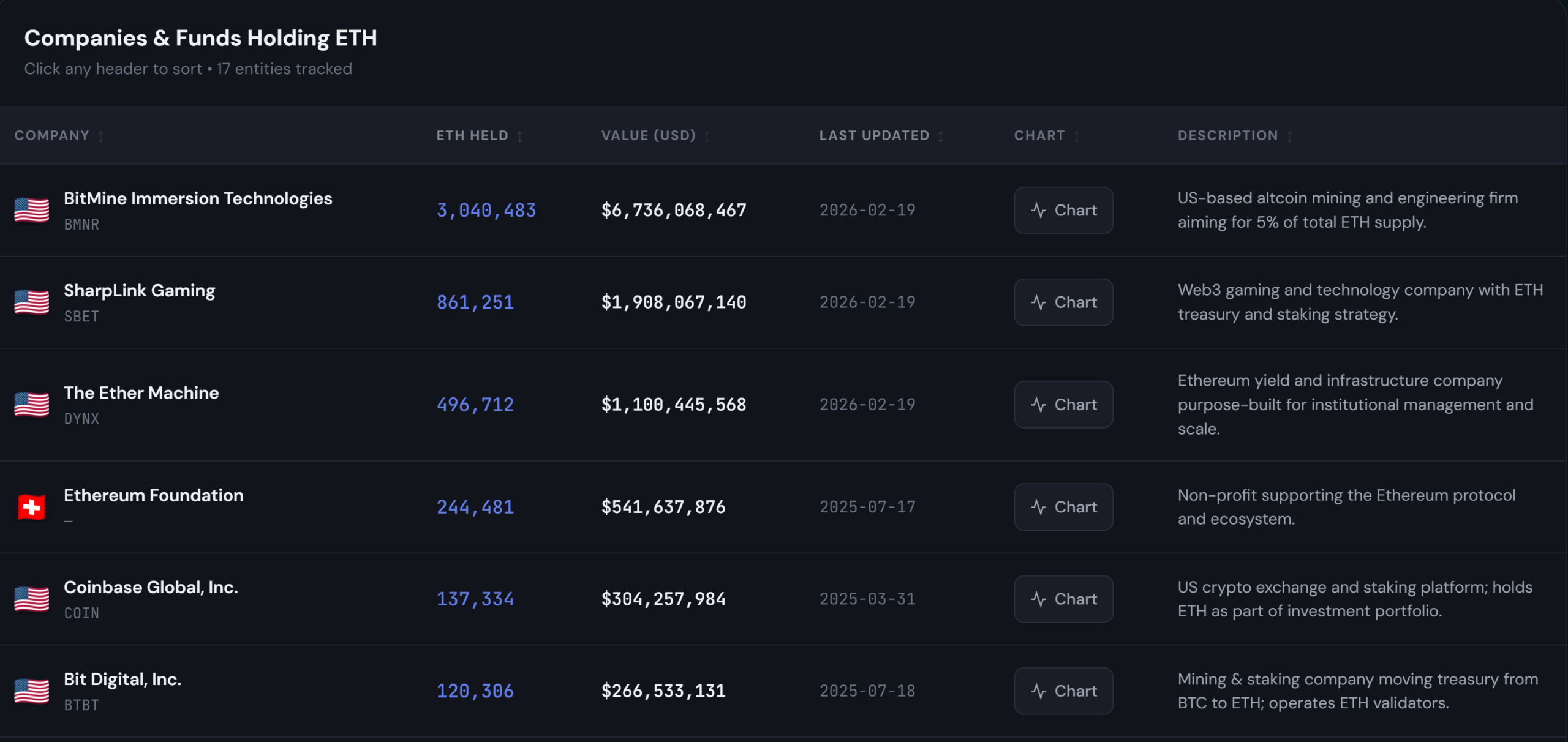

Ether Machine has called off its planned public debut after the Ethereum treasury-focused firm and Dynamix Corporation agreed to terminate their merger, citing deteriorating market conditions.

In a Saturday post on X, Ether Machine said the decision to end the deal was mutual and effective immediately. The transaction had aimed to take the firm public through a merger with the Nasdaq-listed special purpose acquisition company (SPAC), alongside involvement from The Ether Reserve LLC.

“The Ether Reserve LLC, together with certain other parties thereto, announced today that they have mutually agreed to terminate their previously announced Business Combination Agreement, effective immediately, as a result of unfavorable market conditions,” the firm wrote.

According to a filing with the US Securities and Exchange Commission, an unnamed “Payor,” identified in Annex A of the agreement but not disclosed publicly, must pay $50 million to Dynamix within 15 days of the termination taking effect.

Related: Bitmine uplists to NYSE as share buyback is increased to $4B

Ether Machine’s $1.5 billion Ethereum treasury plan collapses

Ether Machine first announced plans to launch what it described as the largest yield-bearing Ether (ETH) fund aimed at institutional investors in July last year. At the time, the company, co-founded by former Consensys executives Andrew Keys and David Merin, said it would list on Nasdaq under the ticker “ETHM,” launching with more than 400,000 ETH, worth over $1.5 billion at the time, under management.

In September, Ether Machine secured $654 million in a private financing round, including 150,000 ETH from Ethereum advocate Jeffrey Berns, who also joined the company’s board. The raise was part of its broader plan to build a large Ether treasury ahead of the planned Nasdaq debut, which has now been canceled.

Meanwhile, Dynamix retains a limited window to secure a new deal. The company has until November 22, 2026, to complete another business combination. If it fails to do so, it will be required to liquidate and return funds held in trust to shareholders, in line with its corporate charter.

Related: Peter Thiel’s Founders Fund dumps ETHZilla stake as ETH treasuries face pressure

Ethereum treasury exits deepen

Ether funds exit amid mounting pressure on Ethereum treasury strategies. Trend Research has fully unwound its Ethereum position, selling 651,757 ETH worth about $1.34 billion while locking in an estimated $747 million loss.

Separately, ETHZilla, formerly a biotech firm that pivoted into an Ethereum treasury strategy during the 2025 hype, has also moved away from Ether accumulation, updating its corporate name and brand to Forum Markets.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation — Santiment founder

Bitcoin and Ether are hovering near levels that could signal a trend shift for the year, even as a broad bear-case narrative persists across markets. Macro strategist Jordi Visser argued on the Anthony Pompliano podcast that a durable move would hinge on price anchors: BTC above $76,000 and ETH above $2,400. “If we trade above $76,000 and at the same time we see Ethereum above $2,400, I believe that is the beginning of a move that will be sustainable this year because I don’t think we’re going to have a recession,” Visser said on Friday’s episode.

From a price perspective, crossing $76,000 would imply roughly a 6% gain from Bitcoin’s around $71,646 level at the time of publication, according to CoinMarketCap data. An ETH revival to $2,400 would imply roughly an 8% lift, depending on the prevailing price trajectory. The thresholds are less about a single day move and more about signaling a potential shift in momentum if macro conditions remain supportive.

Key takeaways

- A durable rally would hinge on Bitcoin clearing the $76,000 level and Ethereum reaching $2,400, potentially marking the start of a more sustained move in 2026 if the economy avoids a recession.

- Inflation remains a central factor for market sentiment. Visser and other observers argue that elevated price pressures could push investors to seek non-equity hedges as traditional markets stagnate.

- Market-implied recession risk for 2026 sits around 24%, according to Kalshi’s pricing, down about 10 percentage points over the past month, illustrating shifting macro bets as traders reassess downside scenarios.

- Not all voices are aligned with an imminent upswing: veteran trader Peter Brandt has warned that BTC could retest or dip below recent lows later in 2026, underscoring ongoing uncertainty in timing and magnitude.

Inflation, the recession bet and crypto flows

The macro backdrop remains a central question for crypto traders. The U.S. Bureau of Labor Statistics reported that the April Consumer Price Index rose 3.3% year over year, a figure that signals the persistence of inflationary pressures even as headline prints moderate. In this environment, a segment of market participants argues that the crypto market could benefit from a rotation away from equities if the macro landscape fails to deliver broad-based growth. Kalshi’s market pricing, which points to a 24% chance of a recession in 2026, has moderated in recent weeks but continues to color risk assessments across digital assets and traditional markets.

Visser’s framing suggests that, in his view, a symmetrical rebound would depend on both BTC and ETH breaking key thresholds, paired with the absence of a macro shock. The implication for traders is clear: price action around major psychological and technical levels could catalyze a broader re-pricing of risk assets, including altcoins that have lagged during a protracted bear cycle.

Contrasting voices and potential paths for 2026

In late March, Peter Brandt—a well-known veteran trader—signaled that Bitcoin could move to new territory beyond the February low near $60,000. He described the possibility of a test of the downside later in the year, calling it a potential bear-cycle low rather than a forecast set in stone. Brandt’s stance underscores a fundamental tension in the market: even if some analysts outline scenarios for a structural bottom, timing remains highly uncertain and dependent on a convergence of macro data, policy expectations, and on-chain dynamics.

Visser has long maintained a more nuanced stance on market regimes, cautioning against rigid bull/bear labeling. He noted that even during periods of price ascent, the buildup of speculative appetite can wane, suggesting that a clean, textbook breakout may not be instantaneous. “At some point in there, it just seems like okay, they go up and then the normal course is at some point people don’t invest as much as they have,” he remarked, highlighting how sentiment can shift before traditional trend signals fully align.

What this could mean for traders and builders

For traders, the narrative hinges on whether BTC can sustain momentum through the next leg of price discovery and whether ETH can regain relevance as a macro-divergence asset in a high-inflation regime. A confirmed breakout above the $76,000/$2,400 threshold would not only mark a milestone for this cycle but could also influence funding rates, liquidity flows, and risk-off/reward dynamics across decentralized finance and broader crypto markets.

From a broader market perspective, the combination of sticky inflation and evolving recession expectations keeps macro risk at the forefront. If inflation trends were to cool more decisively or if the economy demonstrates resilience despite soft indicators, the case for a renewed crypto-upleg strengthens. Conversely, a renewed macro shock or a longer-than-expected slowdown could keep upside constrained, even if price testing around key levels continues.

For developers and infrastructure builders, the potential shift in momentum could affect funding appetites, user onboarding, and the pace of Layer-2 and cross-chain proliferation. In a scenario where risk assets regain traction, attention may move toward scaling, security, and user experience as the sector seeks to convert renewed interest into sustainable network activity.

Key references: Visser’s remarks on the Pompliano podcast, the 24% recession probability priced into Kalshi markets (down about 10 points in a month), and the latest CPI release from the U.S. Bureau of Labor Statistics. For context on price levels, Bitcoin hovered around the $71,646 mark, with Bitcoin price data corroborated by CoinMarketCap, while the ETH threshold cited sits at $2,400.

Looking ahead, market participants will be watching how inflation evolves, how central banks signal policy pivots, and whether crypto markets can translate macro resilience into durable price action. The next few weeks could help clarify whether the 2026 path favors a renewed crypto rally or a renewed test of downside support.

Watch next: as inflation data and policy cues unfold, traders will scrutinize whether the BTC-ETH cross-threshold thesis holds and which macro scenario—soft landing or renewed slowdown—ultimately shapes the year’s trajectory.

Crypto World

New Crypto Pepeto Final Exchange Testing Update While Markets Ask If Dogecoin Price Prediction Can Reach $1

The new crypto Pepeto moved into final exchange testing, and the presale pushed past $8,920,321 at the fastest pace this project has ever seen. On-chain activity inside this presale makes traders remember what showed up around Dogecoin in its earliest days, before small bags turned into serious wealth and the rest of the market wished they had moved faster.

This article breaks down the Dogecoin price prediction numbers and why the new crypto Pepeto keeps showing up as the biggest opportunity of 2026.

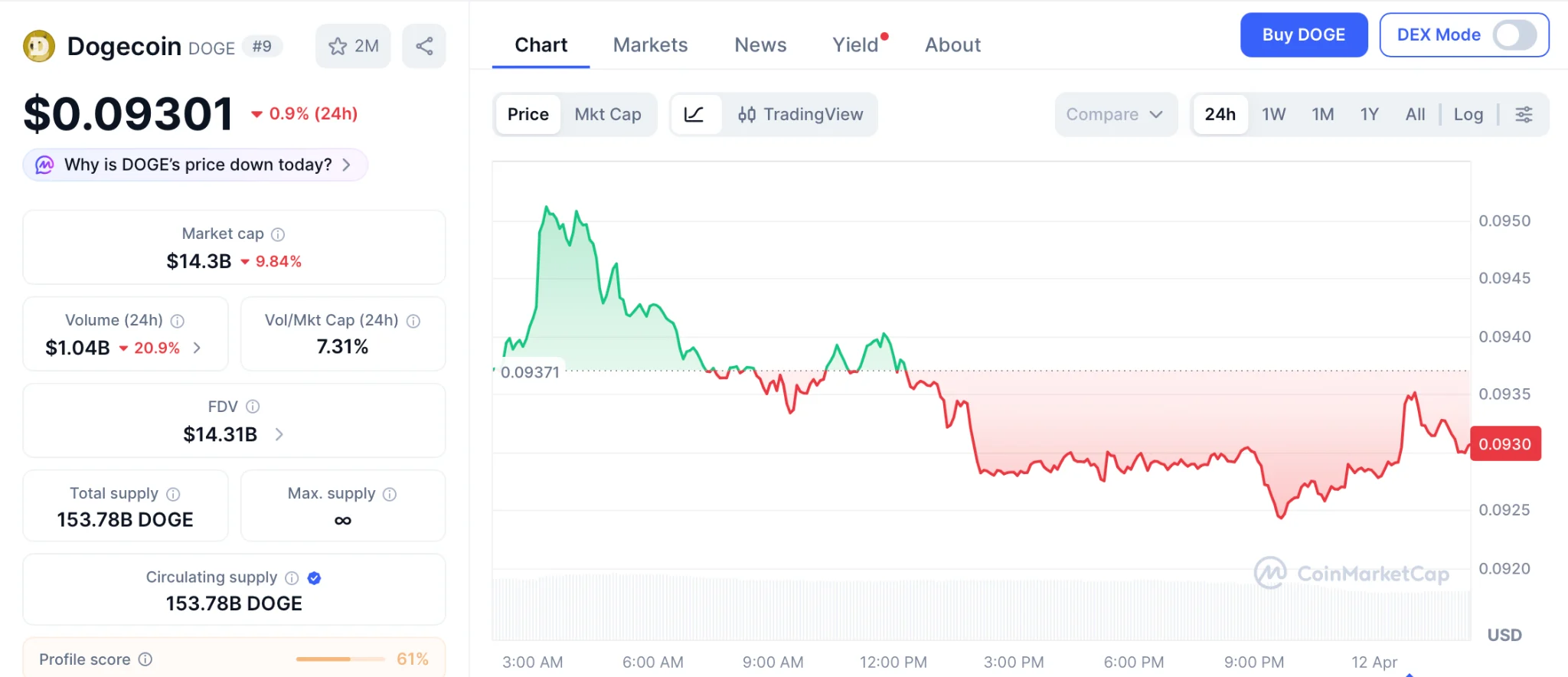

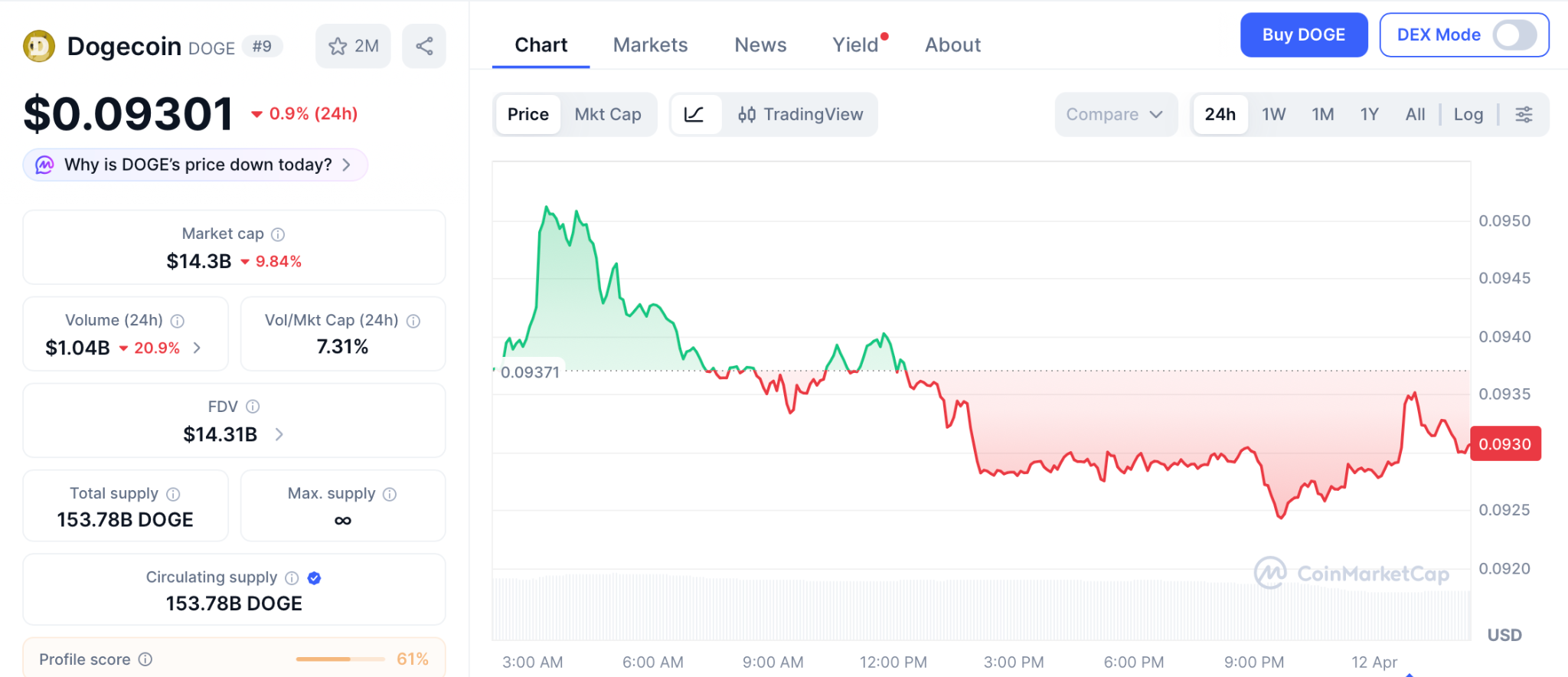

Before getting into the Pepeto project in detail, a quick look at DOGE outlook. The Dogecoin price prediction for $1 faces a long road from $0.093 but the catalysts stacking underneath make it harder to dismiss. DOGE needs to clear $0.095 first, a level that sellers have capped for six straight weeks, then break $0.10 where the Fibonacci ceiling sits according to CoinMarketCap.

After that, the 200-day EMA waits at $0.126, and the real fight starts at $0.25 where the 2026 high failed. A $1 Dogecoin price needs $148 billion in market cap, roughly ten times where it trades today.

Three spot ETFs are already live, the SEC classified DOGE as a digital commodity in March, developer activity jumped 300% year over year, and a GitHub proposal to cut annual issuance by 90% could flip the supply math entirely according to Benzinga. X Money is live with 600 million users but launched fiat-only with no DOGE integration confirmed, and every bull case above $0.25 depends on Musk making that call according to Changelly. The pieces are there. The trigger is not.

The main reason behind the Dogecoin price prediction is clear. A meme coin with no real tools behind it loses value the moment attention moves somewhere else. So where do you make real money on meme coins in 2026? Not on tokens sitting at $14 billion with nothing underneath. You find the early one, the new crypto with DOGE level energy in its first days, real Musk ties spreading across every platform, and a community growing the way DOGE grew before it blew up. That new crypto is Pepeto.

Pepeto Project In Focus

The data points anyone looking for real returns straight to Pepeto, and the case gets even stronger once you see what the team actually built behind those presale numbers.

“What would Dogecoin look like today if it launched with a real exchange behind the name instead of nothing? That question is the whole reason Pepeto was built. The exchange handles every swap at zero fees across Ethereum, BNB Chain, and Solana, the bridge sends tokens between all three chains instantly, and the AI scanner catches scam contracts before they touch any wallet. Every one of those actions runs on Pepeto, so the community pushing viral growth is the same user base generating real volume every day,” said the senior developer on the Pepeto team.

Picture being inside Dogecoin before Musk ever tweeted about it. That is where Pepeto sits right now. The wallets that rode a few thousand into millions on DOGE got one thing right: they entered before the world knew the name, and by the time Musk tweeted those positions were already worth fortunes.

Pepeto is moving on that same path. Musk’s ties to Pepeto keep growing across X and Telegram, and the only question left is when he posts about it, because the same signals that came before his Dogecoin run are showing up around Pepeto now. The whale wallets filling this presale are moving the same way early DOGE whales moved. Maybe they know something nobody else does. They always do.

Conclusion

The Dogecoin price data makes one thing clear: a $14 billion meme token cannot turn a small position into the kind of money that changes how someone lives. But early DOGE buyers know exactly what that feels like. A few hundred dollars at $0.004 became a house, a paid off car, a life with no alarm clock.

Those people did not do anything complicated. They made one right decision at the right time, and that single choice separated them from everyone who spent the next five years saying they almost bought.

Pepeto is sitting at that same moment right now, priced at presale, weeks from a Binance listing, with the same energy DOGE had before the world knew the name, and for anyone looking for the one decision that could deliver the same outcome, Pepeto is it.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the dogecoin price prediction for 2026?

Benzinga targets the Dogecoin price between $0.145 and $0.249 for 2026. DOGE sits at $0.093 with three spot ETFs live.

Why is Pepeto considered a leader in the presales space?

Pepeto leads the presales race because it pairs meme coin virality with a working zero fee exchange at presale pricing. The Pepe cofounder leads the project with $8.9 million raised and a confirmed Binance listing ahead.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Pavel Durov said push notifications can create a privacy risk even after users delete messages and apps.

Summary

- Pavel Durov said push notifications may preserve data even after users delete chats and apps.

- Reports said FBI retrieved deleted Signal messages from iPhone notification logs in a criminal investigation.

- Interest in decentralized messaging apps rose as bans, unrest and internet restrictions disrupted communication access.

His remarks followed reports that investigators retrieved deleted Signal messages from iPhone notification logs, renewing debate about metadata, device storage and private messaging tools.

Durov said push notifications can leave message data on a device outside the encrypted chat itself. He said that risk remains even when users turn off preview text, because people they contact may still use default settings.

“Turning off notification previews won’t make you safe if you use those applications, because you never know whether the people you message have done the same,” he wrote.

He linked that point to privacy settings that depend on choices made by both sides of a conversation.

Durov referred to a report first published by 404 Media. The report said the FBI accessed deleted Signal messages from notification logs stored on an Apple iPhone used in a criminal case.

The case drew attention to how investigators can access data created around messages, even when message content remains protected by end-to-end encryption.

Moreover, the reports renewed focus on metadata, notification storage and other records created by messaging apps and operating systems. Encrypted content may stay protected, but surrounding device data can still reveal communication details.

That debate also increased interest in messaging tools that try to reduce centralized data collection. Developers of decentralized platforms say local storage, routing methods and network design affect how much information remains after users send or delete messages.

Decentralized apps gain users during bans

Interest in decentralized messaging and social platforms has risen since 2025 during blackouts, unrest and internet restrictions. Exploding Topics data cited in the report showed online search interest in decentralized social media platforms rose 145% over five years.

The report also pointed to Bitchat, a Bluetooth mesh messaging app that works without the internet. It said more than 48,000 users in Nepal downloaded the app during a social media ban in September 2025, while Durov said Telegram bans in Iran drove users toward VPNs instead of state-backed services.

Bitcoin and Ether aren’t far from levels that could signal a trend reversal this year, despite a growing consensus across the industry calling for a bear market, according to macro analyst Jordi Visser.

“If we trade above $76,000 and at the same time we see Ethereum above $2,400, I believe that is the beginning of a move that will be sustainable this year because I don’t think we’re going to have a recession,” Visser said on the Anthony Pompliano podcast published on YouTube on Friday.

A move to $76,000 would represent an increase of 6.1% from Bitcoin’s (BTC) price of $71,646 at the time of publication, according to CoinMarketCap data. Ether’s (ETH) move to $2,400 would represent an increase of around 8%.

Inflation is going to remain high, says Visser

Traders on the prediction market Kalshi are leaning toward a similar macro outlook to Visser, pricing a 24% chance of a recession in 2026, down 10% over the past 30 days.

“I think inflation is going to stay elevated, and I think people are going to need to find something that is making money in a world where the S&P is not moving anywhere,” Visser said.

The United States Bureau of Labor Statistics (BLS) revealed in a report published on Friday that the Consumer Price Index (CPI) in April rose 3.3% year-over-year.

Visser’s recent comments challenge the growing view across the crypto industry that 2026 still has more downside ahead, with some even calling for a move below the Feb. 6 yearly low of $60,000.

Bitcoin may fall below $60,000 yearly low

On March 31, veteran trader Peter Brandt said that this may not be the lowest level for 2026, forecasting that Bitcoin could retest or even move “slightly lower” than the price level in September or October this year.

“That would then be the bear cycle low,” Brandt said.

Related: Bitcoin charts point to $80K in April: Here’s how it may happen

Visser explained that he has never been a “big fan” of labeling Bitcoin price trends as bull or bear markets.

“Especially when we’re at all-time highs. Like, at some point in there, it just seems like okay, they go up and then the normal course is at some point people don’t invest as much as they have,” he said.

Magazine: Should users be allowed to bet on war and death in prediction markets

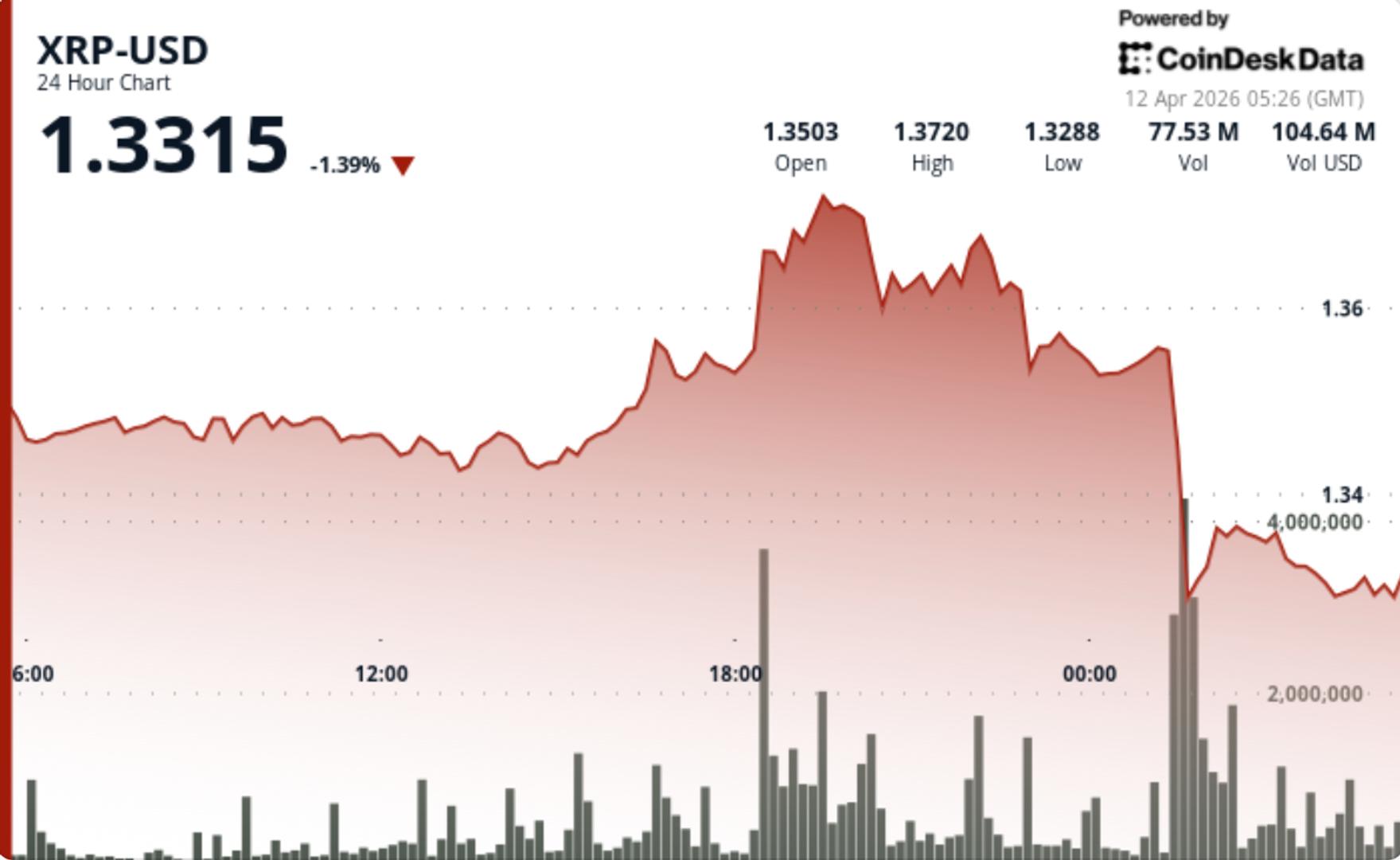

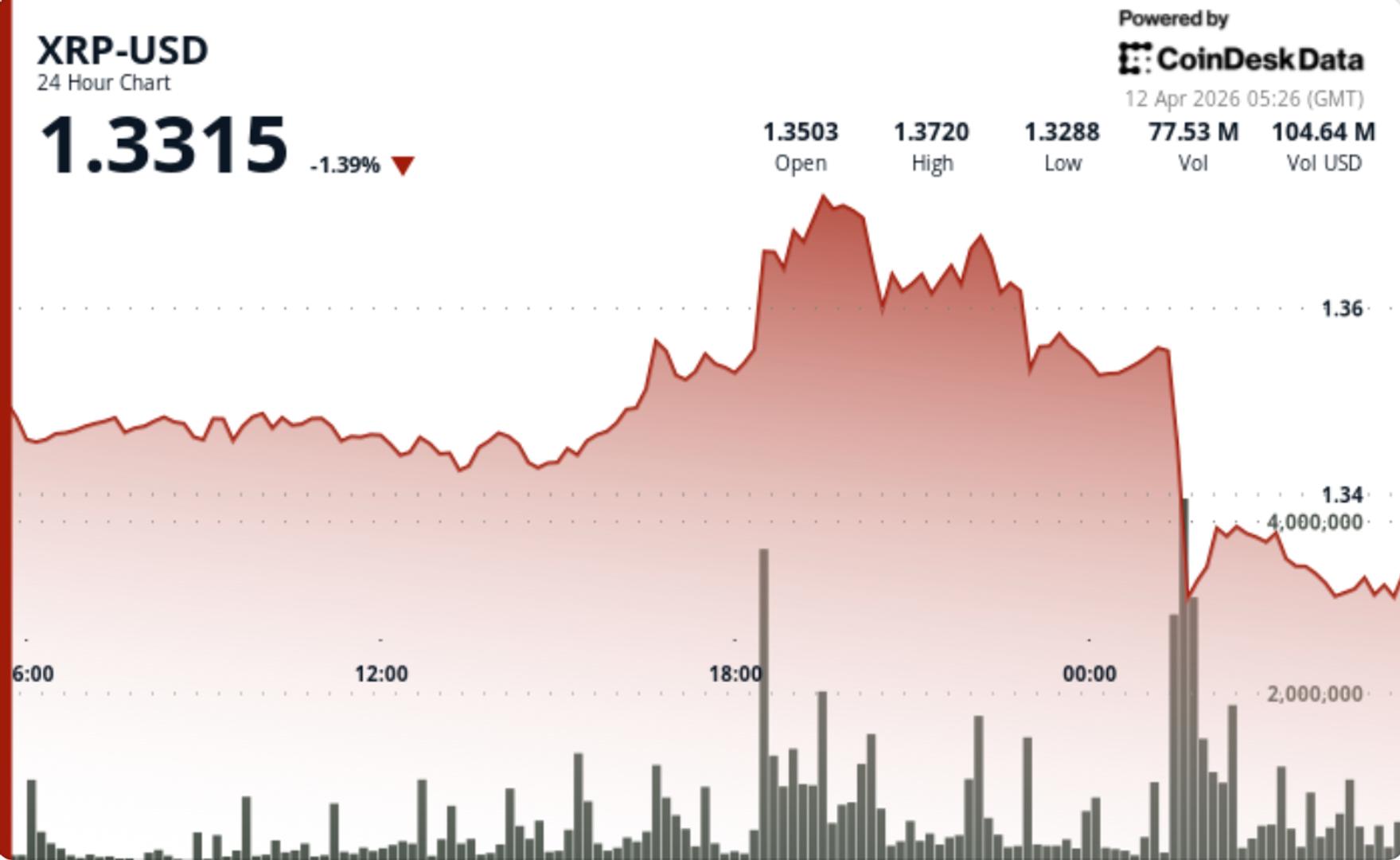

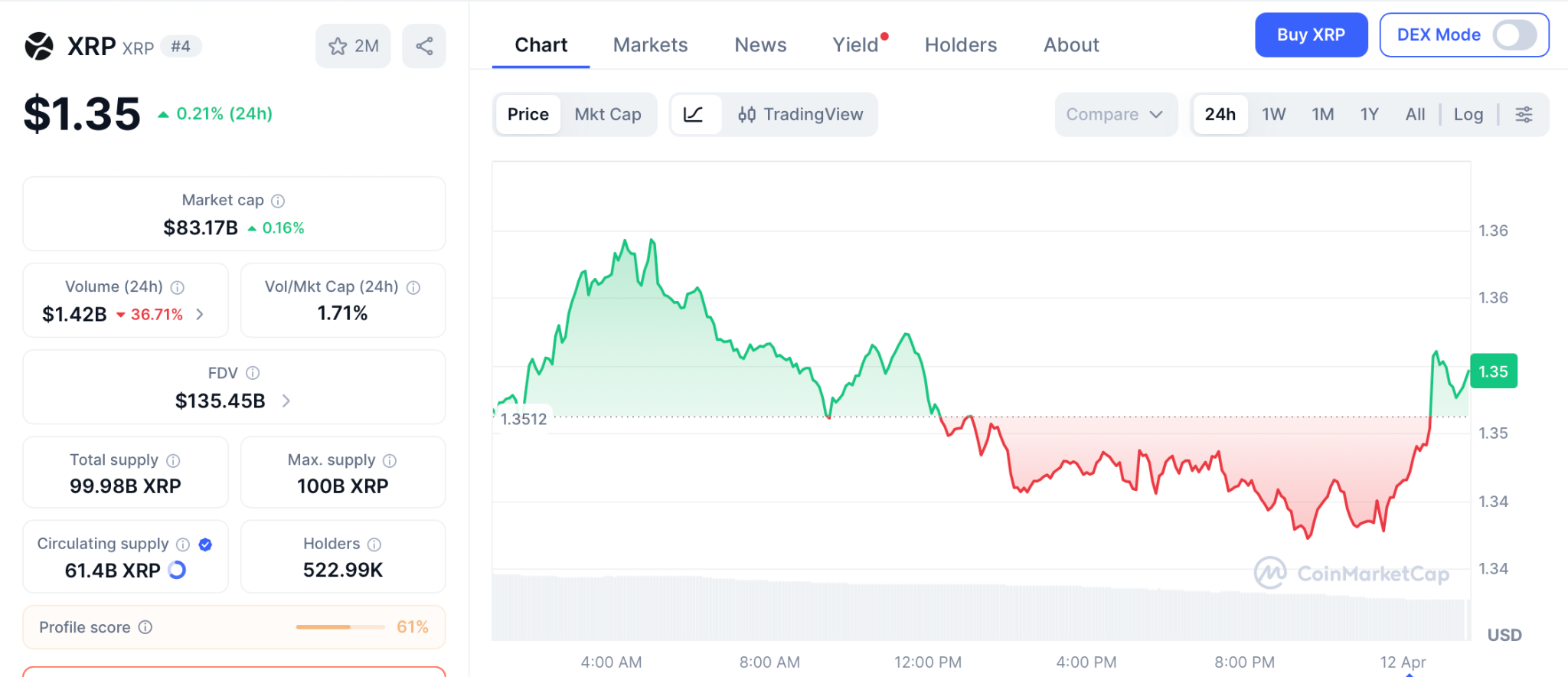

XRP saw a sharp breakdown in late trading, with a sudden wave of selling pushing price below key support. The speed of the move and lack of strong recovery suggest sellers are still in control, even as volatility compression points to a larger move ahead.

News Summary

• XRP fell from $1.36 to $1.33 in minutes, with a rapid spike in volume triggering a cascade of selling.

• The breakdown pushed price below $1.35, flipping it into resistance while upside remains capped near $1.41.

• Analysts remain split, with some calling for deeper downside while others still see a larger cycle recovery.

Market Overview

XRP declined 1.7% over the 24-hour period, but the headline move hides the real story, which is the intraday breakdown. Price was relatively stable before a sudden burst of selling hit, driving a quick drop through $1.35 and down toward $1.33.

The move came on extremely elevated volume, confirming it was not a thin liquidity move but a real flush. Once support gave way, price moved quickly, which is typical in current conditions where order books remain relatively shallow.

The bounce that followed was weak. XRP recovered slightly but failed to reclaim lost levels, forming a lower high and reinforcing the idea that the move was not just a temporary spike but a structural rejection.

Technical Analysis

The key signal is how quickly support failed and how weak the recovery has been. High volume on the way down, followed by fading volume on the bounce, typically points to distribution rather than accumulation.

XRP remains below key resistance levels and continues to trade within a broader downtrend. Indicators are mixed, with volatility compressing even as momentum weakens, creating the conditions for a larger move but without a clear direction yet.

This leaves the market in a familiar position where price is stuck between breakdown risk and the potential for a sharp reversal if resistance is reclaimed.

What traders should watch

• $1.35 is now the immediate pivot after breaking down, and price needs to reclaim it to stabilize.

• $1.40-$1.41 remains the key resistance zone that has capped multiple recovery attempts.

• On the downside, failure to hold $1.33 opens a move toward $1.32-$1.31, where the next demand zone sits.

Bitcoin (BTC) reversed its Saturday rally and fell below $72,000 after the United States and Iran failed to reach an agreement following peace talks in Islamabad, Pakistan.

The largest cryptocurrency had climbed near $74,000 on Saturday before dropping to an intraday low of $71,168 during early Asian trading hours.

Bitcoin Drops as US-Iran Talks Fail After 21-Hour Islamabad Session

At press time, BTC traded at $71,716, down 1.84% over the past 24 hours.

BeInCrypto Markets data showed that the broader crypto market cap also declined by 1.7%, with most major large-cap assets in the red. Ethereum (ETH) slipped to roughly $2,220, while XRP fell to $1.33, each shedding close to 2%.

BTC had gained ground earlier in the week after a two-week ceasefire was announced. However, the ceasefire remained fragile.

Israel continued airstrikes in Lebanon, and Iran announced crypto tolls on ships passing through the Strait of Hormuz. BeInCrypto also reported that, according to US officials, Tehran was unable to locate all the mines across the strait.

Two US Navy destroyers reportedly transited the Strait of Hormuz to begin mine-clearing operations, according to US Central Command. However, Iran rejected that claim outright.

Follow us on X to get the latest news as it happens

What Happened Between the US and Iran in Islamabad

The high-level negotiations between Washington and Tehran ended without producing a peace deal. Both sides offered competing explanations for the breakdown.

According to Fars news agency, any path to an agreement depends on Washington scaling back what Iran considers “unreasonable demands”. The control of the Strait of Hormuz and the nuclear program remain among several unresolved points of contention between the two sides.

“Despite various initiatives from the Iranian delegation, the unreasonable demands of the American side prevented the progress of the negotiations. Thus, the negotiations ended,” Iranian state broadcaster IRIB said in a post.

A source close to Iran’s negotiating team told Fars news agency that Washington sought concessions through diplomacy that it had been unable to secure from the war.

“The Americans needed the negotiation for their lost face in the international arena and were unwilling to lower their expectations despite the defeat and stalemate in the war with Iran,” the source said. “Iran has no plans for the next round of talks,” they mentioned.

On the US side, VP JD Vance held a brief press conference. He maintained that the American delegation was “quite accommodating and flexible.”

“The president told us, ‘You need to come here in good faith and make your best effort to get a deal.’ We did that, and unfortunately, we weren’t able to make any headway,” he said.

Vance emphasized that preventing Iran from developing nuclear weapons, both now and in the future, remains President Trump’s “core goal.” He left Pakistan after the briefing.

“So, look, we were constantly in communication with the team, because we were negotiating in good faith. And we leave here with a very simple proposal, a method of understanding that is our final and best offer. We’ll see if the Iranians accept it.”

The deadlock raises concerns about the fragile two-week ceasefire. However, Pakistan’s foreign minister has released a statement, urging both sides that it is “imperative that the parties continue to uphold their commitment to ceasefire”.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US-Iran Talks Breakdown, Bitcoin looses Weekend Gains appeared first on BeInCrypto.

TLDR:

- US intelligence confirms China is preparing MANPAD air defense shipments to Iran within weeks.

- Beijing is routing weapons through third countries to conceal origin and maintain plausible deniability.

- The transfer escalates beyond dual-use tech sales to direct government-to-government weapons delivery.

- Trump is set to meet Xi in Beijing next month as US-China tensions quietly build behind ceasefire talks.

Beijing has publicly taken credit for brokering the fragile US-Iran ceasefire, according to three sources familiar with US intelligence assessments.

The systems in question are MANPADS—shoulder-fired air defense missiles that threatened US aircraft throughout the five-week war. Shipments are reportedly being routed through third countries to conceal their Chinese origin.

China Prepares MANPAD Transfer To Iran While Ceasefire Holds

Three U.S intelligence sources familiar with recent assessments have confirmed to CNN that Beijing is preparing to deliver man-portable air defense systems, known as MANPADs, within the next few weeks.

The timing raises immediate questions. China claimed credit for helping broker the ceasefire that paused fighting between Iran and the US earlier this week.

Moving weapons to one side of that conflict during an active pause directly contradicts that public position. MANPADs presented a real threat to low-flying US military aircraft throughout the five-week war.

President Trump confirmed at a Monday press conference that an F-15 downed over Iran last week was struck by a shoulder-fired heat-seeking missile. Iran credited a new air defense system for that strike without identifying it further.

Two sources told CNN that Beijing is routing the shipments through third countries to conceal their origin. That approach preserves China’s ability to deny direct involvement and has been used in previous sanctions evasion cases.

A Chinese embassy spokesperson flatly denied the reporting, stating Beijing has never provided weapons to any party in the conflict.

Beijing’s Calculated Support For Iran Behind A Neutral Facade

Chinese companies have already been supplying Iran with sanctioned dual-use technology. That technology has helped Iran continue building weapons and improving navigation systems.

A direct government-to-government weapons transfer, however, would mark a clear escalation beyond those commercial arrangements.

One source described Beijing’s strategy as deliberate. China sees no value in openly entering the conflict against the US and Israel.

That path would be unwinnable and damaging to China’s broader standing. Instead, Beijing is quietly supporting Iran while maintaining the appearance of neutrality.

Iran supplies China with the bulk of its sanctioned oil, giving Beijing a firm economic reason to keep Tehran stable. Sources noted China could argue that air defense systems are defensive rather than offensive, distancing its support from Russia’s intelligence sharing that helped Iran target US forces.

Trump is set to meet President Xi in Beijing next month. High-level US-China talks took place during ceasefire negotiations this week.

Whether the reported shipment affects those diplomatic plans remains an open question as both governments continue engaging publicly.

Crypto World

Crypto News Proves the Market Is Alive as Coinbase Drops CLARITY Act Opposition and Pepeto Outpaces BNB and XRP in One Key Metric

Crypto news just delivered the clearest bullish signal of 2026 after Coinbase CEO Brian Armstrong publicly endorsed the CLARITY Act on April 9, removing the last major industry holdout standing between crypto and federal law according to 24/7 Wall St.

That means the regulatory path is open, institutional money is lining up, and Pepeto with $8.9 million in presale wallets, a running exchange, and a Binance listing is how to capture 150x before that wave hits.

Coinbase CEO Brian Armstrong reversed months of opposition and backed the CLARITY Act on April 9, the same day Treasury Secretary Scott Bessent called the bill a national security priority in the Wall Street Journal according to 24/7 Wall St.

SEC Chair Paul Atkins confirmed the SEC and CFTC are ready to implement the bill the moment Congress sends it forward.

The crypto news declaring death while Coinbase, the Treasury, and the SEC line up behind the same bill tells you everything about where this market is headed.

Regulatory Green Light, Institutional Flows, and the Presale Loading During Fear

Why Pepeto Is the Crypto News Answer Every Wallet Was Searching For

The Pepeto presale runs on a completely different model than standard launches. Each closed round lifts the cost and cuts the tokens still available. Wallets that entered early locked lower pricing because they committed before exchange tools were proven, and wallets entering today get a working platform but pay more.

This structure removes the guesswork of timing bottoms and replaces it with fixed entry windows where the terms are clear. Instead of fighting for allocation after the Binance listing opens, wallets race to lock position before it opens. That shift is why $8.9 million entered while most crypto news headlines read like obituaries.

PepetoSwap handles every trade without touching your balance, and the multi chain bridge transfers capital between Ethereum, BNB, and Solana at no cost so wallets never shrink from transfer charges. A SolidProof review confirmed every smart contract is clean, and a developer who ran Binance listing launches built the exchange debut path.

Staking at 185% APY grows holdings for wallets already committed while the crypto news audience reads doom headlines. At a presale price of $0.0000001863, the entry cost is visible and the Binance listing return is clear, and the working exchange behind this presale means the 150x math rests on real tools, not hype.

Binance Coin (BNB) Price at $606 as BNB Chain Extends Zero Fee Stablecoin Program

Binance Coin (BNB) holds $606 according to CoinMarketCap, up 0.4% on the day as BNB Chain extended its zero fee stablecoin program through April 30 covering over $4.5 million in gas costs.

BNB dropped 22% from its January high of $780 but outperformed Bitcoin’s 47% drawdown over the same stretch. From $606 with a previous peak above $1,370, the return measures in single digit percentages while the Pepeto presale gives 150x from one listing event, something BNB at an $83 billion cap cannot deliver.

Ripple (XRP) Price at $1.35 as CLARITY Act Nears Senate Vote

Ripple (XRP) trades at $1.35 according to CoinMarketCap after Armstrong’s endorsement cleared the last obstacle for the CLARITY Act, which would permanently classify XRP as a digital commodity.

XRP sits 64% below its $3.65 high with support at $1.28 and resistance at $1.40. From $1.35 at an $83 billion cap, targets range from $2.00 to $2.80, solid for percentage gains but not 150x, and the presale delivers 150x from one listing event.

Conclusion

The way serious wallets choose entries has shifted completely this cycle. Cheap prices alone no longer determine which projects earn capital. Token distribution mechanics and operational transparency now drive where money goes.

Looking for crypto news brought you here, and Pepeto is what that search was pointing to, because the working exchange means the 150x math is built on real products and BNB at $606 or XRP at $1.35 cannot deliver in a full year what one listing event delivers to presale holders.

The investors who enter the presale right now hold the same position early BNB buyers had before the exchange opened, the position that turned small entries into wealth that made every financial choice after it easy, and the presale is still accepting entries at a price the Binance listing erases the moment it goes live.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What does crypto news say about institutional adoption after the CLARITY Act breakthrough?

Coinbase, the Treasury, and the SEC all endorsed the CLARITY Act in the same week, proving crypto is entering regulated infrastructure status. Pepeto at presale pricing with a Binance listing carries the 150x that regulated products cannot access.

Is Binance Coin a better buy than presale entries at BNB’s current price of $606?

Binance Coin (BNB) trades at $606 with an $83 billion cap and single digit upside to resistance at $650. Pepeto through the Pepeto official website offers presale entry and listing event returns that BNB at this size cannot produce.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

TLDR:

- Microsoft trades near $370 after a prolonged downtrend, with weak consolidation signaling limited buyer strength.

- Meta rebounds from $540 lows as RSI improves, though price still faces resistance near the $640–660 range.

- Microsoft remains below key resistance levels, keeping the broader bearish structure intact for now.

- Meta shows early recovery signs, but failure to break higher could lead to another support retest.

U.S. technology stocks are trading below prior peaks as volatility persists across major indices. Recent market commentary points to valuation compression among leading firms, with Microsoft and Meta Platforms drawing attention for relative pricing and shifting price structures.

Microsoft Extends Downtrend as Key Support Faces Pressure

Market analyst Ali Charts recently noted that Microsoft trades about 30% below its all-time high. The stock currently holds a price-to-earnings ratio near 23x, placing it among the lower valuations within the “Magnificent 7” group.

The daily chart structure reflects a clear transition from bullish momentum into a sustained downtrend. Between May and July 2025, Microsoft advanced strongly, forming consistently higher highs and higher lows.

However, that structure weakened between August and November as repeated rejections appeared near the $540–$560 range.

Selling pressure intensified after a breakdown below the $500 level in November 2025. The move confirmed a broader trend reversal, followed by continued declines into the $400 region. Subsequent rebounds failed to hold, with price action forming lower highs throughout early 2026.

As of April 2026, the stock trades near $370, where consolidation remains weak. Candlestick bodies have narrowed, showing reduced momentum. At the same time, recovery attempts lack follow-through, indicating limited buyer strength at current levels.

Key resistance stands between $400 and $420, where previous attempts have stalled. A higher resistance band exists around $480–$500, now acting as a supply zone.

On the downside, the $360–$370 area serves as immediate support. A break below this range may expose the $340 level.

Meta Tests Recovery as Momentum Gradually Improves

Ali Charts also pointed out that Meta trades about 22% below its peak, while revenue has increased 22% year-over-year. The stock shows a different structure compared to Microsoft, with more range-bound movement and early signs of stabilization.

Price action throughout 2025 shows a strong rally between May and August, where Meta climbed toward the $780–$800 zone. That move was followed by a prolonged distribution phase, where multiple breakout attempts failed near the highs.

From November 2025 to March 2026, the stock entered a controlled decline. Prices moved within a defined range between roughly $720 and $560. Lower highs remained intact during this phase, though selling pressure appeared less aggressive compared to Microsoft.

In April 2026, Meta trades around $630 after rebounding from the $540 level. The move reflects a recovery attempt, supported by improving momentum indicators. The Relative Strength Index has risen from oversold levels near 25–30 to around 57, signaling a shift in short-term strength.

Even so, resistance remains firm between $640 and $660. A broader supply zone sits between $700 and $720, where previous rallies stalled. On the downside, support is seen between $580 and $600, with stronger demand near $540.

The current structure places Meta at a decision point. A move above $660 could open the path toward higher levels, while rejection may lead to another test of lower support zones.

The #1 Financial Account Nobody is Talking About #finance #wealth #money #tyler #realwealth

Scott Mills removed from DJ set in Harrogate after sacking

10 Must-Know Facts on America’s $2 Billion ‘Ghost’ Striking Iran in 2026

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

The #1 Financial Account Nobody is Talking About #finance #wealth #money #tyler #realwealth

Les 7 sites que les pros crypto ne veulent pas que tu connaisses.

Dopamine Hits Vs Financial Freedom (Choose One) #moneytips #psychology #shorts

-

Business6 days ago

Business6 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Politics2 days ago

Politics2 days agoUS brings back mandatory military draft registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Veronica Beard

-

Tech4 days ago

Tech4 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business7 days ago

Business7 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion6 days ago

Fashion6 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports2 days ago

Sports2 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Crypto World3 days ago

Crypto World3 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Fashion5 days ago

Fashion5 days agoLet’s Discuss: DEI in 2026

-

Business1 day ago

Business1 day agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World4 days ago

Crypto World4 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics2 days ago

Politics2 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Business2 days ago

Business2 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business15 hours ago

Business15 hours agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Tech6 days ago

Tech6 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech6 days ago

Tech6 days agoItalian court says Netflix must refund customers up to $576 over price hikes

-

Tech6 days ago

Tech6 days agoSamsung just gave up on its own Messages app

-

Tech6 days ago

Tech6 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech6 days ago

Tech6 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Politics2 days ago

Politics2 days agoLBC Presenter Mocks Trump Over Iran War Failures

You must be logged in to post a comment Login