Crypto World

Micron (MU) Stock: Analysts Hold Strong Despite Post-Earnings Dip

Key Takeaways

- Micron’s fiscal Q2 2026 delivered $23.86 billion in revenue with adjusted EPS of $12.20, surpassing analyst expectations

- The company projected fiscal Q3 2026 revenue of approximately $33.5 billion, significantly exceeding Street estimates

- Capital expenditure guidance for fiscal 2026 increased to more than $25 billion, roughly $5 billion higher than previous projections

- Shares declined following the earnings announcement despite impressive financial performance, primarily due to elevated spending concerns

- Analyst sentiment remains overwhelmingly positive with 29 Buy ratings, 5 Strong Buys, and no Sell recommendations according to MarketBeat data

Micron Technology unveiled exceptional quarterly results on March 19, yet the market’s response told a more complex story. Despite impressive revenue figures and unprecedented free cash flow generation, shares retreated as Wall Street digested the company’s ambitious capital investment strategy.

The memory chip giant reported fiscal second-quarter 2026 revenue reaching $23.86 billion alongside adjusted earnings of $12.20 per share. Micron also highlighted that it closed the period with $16.7 billion in cash and investments, marking a company record for free cash flow generation.

While these figures impressed, it was the forward-looking commentary that captured the most attention—both positive and negative.

For fiscal Q3 2026, Micron projected revenue of approximately $33.5 billion, substantially exceeding Wall Street’s expectations. The company attributed this robust outlook to explosive demand for high-bandwidth memory (HBM) products, which are essential components in AI data centers and acceleration hardware.

HBM represents today’s most sought-after memory technology. Micron operates within an oligopoly of just three major global producers, joined by Samsung and SK hynix. This concentrated supply structure has bolstered pricing power and supported healthy profit margins.

Understanding the Post-Earnings Decline

Notwithstanding the impressive financial performance, Micron’s stock price declined following the announcement. The catalyst? A significantly revised capital spending forecast.

The company disclosed that fiscal 2026 capital expenditures would surpass $25 billion, representing an approximate $5 billion increase from earlier guidance. Management explained the investment is necessary to expand clean-room infrastructure and accelerate DRAM manufacturing capacity to satisfy AI-driven demand.

This scenario represents a classic semiconductor industry dilemma—deploying massive capital to capture growth opportunities while risking oversupply if market conditions deteriorate. Memory manufacturers have historically encountered this challenge, and investors maintain vivid memories of past overcapacity cycles.

Additionally, the stock’s valuation had already reflected substantial optimism. Prior to Thursday’s retreat, Micron had surged more than 61% during 2026, building on strong momentum from 2025. At such elevated levels, any hint of risk can trigger profit-taking behavior.

Wall Street Maintains Conviction

The analyst community showed no signs of wavering. According to MarketBeat data released on March 19, Micron holds five Strong Buy ratings, 29 Buy ratings, and four Hold ratings. Notably, zero analysts recommend selling the stock.

This represents nearly unanimous bullish positioning. The four Hold ratings suggest some analysts advocate patience at current valuations, but bearish recommendations remain completely absent.

Price targets underwent revisions as analysts updated their financial models following the report. MarketBeat’s consensus tracking indicated a range settling between approximately $425.62 and $446.66.

Several firms subsequently raised their targets. Needham elevated its price objective to $500. UBS similarly increased its target while reaffirming its Buy rating. Both institutions cited the sustained strength of AI-related memory demand as their primary rationale.

These $500 price targets represent more than optimistic projections—they embody a conviction that Micron’s AI-driven growth trajectory extends further than current market pricing acknowledges.

The investment debate surrounding Micron has evolved. Questions no longer center on whether the company is emerging from a downturn. Instead, the focus has shifted to whether Micron can sustain expansion without excessive capital deployment.

Presently, analysts are answering affirmatively. With 34 Buy or Strong Buy ratings and zero Sell recommendations in current MarketBeat data, Micron stands as one of the most broadly supported equities in the AI semiconductor sector.

The stock declined on March 19. The analyst community’s conviction remained intact.

CME Bitcoin futures open interest has fallen to a 14‑month low as the once‑crowded basis trade collapses, compressing yields and pushing leveraged institutions out.

Summary

- CME Bitcoin futures average daily open interest fell below $8B in March and to about $7.2B in early April, the lowest since February 2024.

- March volume slid to $163B, nearly half January 2025’s peak, as the spot‑ETF plus short‑futures basis trade unwound and leveraged funds exited.

- With annualized basis near 5% versus ~4.5% risk‑free rates, funding costs and counterparty risk have erased arbitrage appeal at CME.

CME Bitcoin futures activity has fallen to its weakest level in more than a year as the once‑crowded basis trade unwinds and leveraged institutions pull back. Average daily open interest dropped below $8 billion in March 2026 and slid to about $7.2 billion in early April, marking a new low since February 2024 and extending a five‑month decline. Monthly trading volume on CME fell to $163 billion in March, almost half the peak seen in January 2025, underscoring how quickly institutional demand has cooled.

At the center of the shift is the cash‑and‑carry structure that dominated Wall Street’s crypto exposure after U.S. spot Bitcoin ETFs launched. For much of 2024 and 2025, funds bought spot ETFs while shorting CME futures to capture a relatively low‑risk yield from the spread between futures and spot. “The CME Bitcoin futures basis is primarily driven by price momentum and market sentiment,” CF Benchmarks wrote in a 2025 analysis, noting that aggressive rallies tended to push futures into rich contango and make basis trades highly attractive.

That regime has broken down as Bitcoin has retreated from highs near $120,000 to below $70,000, compressing the annualized basis to around 5% — barely above a roughly 4.5% U.S. risk‑free rate. With funding costs and counterparty risk taken into account, “a near‑flat basis reduces the incentive for basis trades that rely on futures premia to generate low‑risk carry,” derivatives commentary from MEXC noted in February, describing CME’s structure as close to neutral. In some stress episodes, the CME‑to‑spot basis has even turned negative, a sign of “aggressive hedging or the unwind of cash‑and‑carry structures when risk appetite fades,” according to Padalan Capital’s observations cited in the same report.

The result is a sharp drop in the very type of activity CME was built to attract. Total Bitcoin futures open interest across venues remains sizable — over $43 billion as of early March, according to derivatives trackers — but liquidity is increasingly concentrated offshore or in perpetual swaps, while regulated CME contracts lose share. A Binance research note in January captured the turning point bluntly: “The era of arbitrage is over; Wall Street withdraws from Bitcoin basis,” after CME open interest fell below major offshore exchanges for the first time.

For Bitcoin (BTC), the implications are mixed. A lower, flatter CME basis suggests less leveraged carry and more spot‑driven price action, which can make the market structurally healthier but also more sensitive to directional flows. For CME, the open question is whether new use cases — such as more nuanced hedging by spot ETF issuers — can replace the vanished basis trade, or whether regulated futures will remain a shrinking island in a derivatives complex increasingly dominated by 24/7 offshore products.

Bitcoin pulled back to $71,843 on Friday after a third attempt to breach $73,000 was met with selling on Thursday, a level that has now rejected the price on every rally since the Iran conflict began in late February.

The retreat is modest. Bitcoin is up 7.9% on the week, its strongest weekly performance of the war so far, holding above the 50-day moving average which has turned upward for the first time since the conflict started. Ether held at $2,189, up 6.6% on the week. Solana’s SOL gained 5.1% to $83.09. XRP added 2.8% to $1.34. Dogecoin climbed 2.4% to $0.092. The entire top 10 is green on the weekly chart for the first time in over a month.

But $73,000 is seemingly a wall. The level has capped bitcoin three times since the ceasefire was announced on Tuesday — each attempt producing a rally that faded within hours. The pattern is identical to the pre-ceasefire range, just shifted higher. Instead of grinding between $65,000 and $73,000, bitcoin is now grinding between $70,000 and $73,000.

“We will need to wait for the price to rise above $75,000 before we can speak of the market entering an active bullish phase,” said Alex Kuptsikevich, FxPro’s chief market analyst, in a note to CoinDesk. He added that bitcoin remains above the 50-day moving average, reinforcing short-term bullish sentiment, but flagged the repeated rejection at $73,000 as the barrier that needs to break.

Galaxy Digital CEO Mike Novogratz set the bar higher, saying the key conditions for bitcoin to resume its uptrend are consolidation above $74,000 followed by a break above $80,000. “Breaking through these levels could trigger a new wave of optimism and restore the uptrend,” he said.

The ceasefire that triggered Tuesday’s rally is already fraying. Iran accused the U.S. of breaching three clauses of the agreement.

The Strait of Hormuz remains only partially reopened with “technical limitations.” Oil rebounded from its 15% single-day crash to trade back above $97.

Ether’s setup is similarly range-bound. The token pulled back 4% from its Wednesday peak to $2,189, which Kuptsikevich described as market noise within a $2,000 to $2,400 consolidation zone.

“A breakout beyond this calm consolidation zone would signal the start of a directional move,” he said.

Outside of majors, Algorand dropped 11.4%, Aptos fell 6.1%, and Polkadot lost 6.1%, marking an altcoin divergence that typically appears when traders are rotating rather than entering fresh capital.

The Fear and Greed Index climbed out of single digits for the first time in over a month, meanwhile.

If the ceasefire survives through the weekend and the Strait opens further, $73,000 gets its fourth test with momentum behind it. However, Tehran’s grievances escalate or Trump’s rhetoric shifts, the pullback toward $68,000 to $70,000 is the path of least resistance.

XRP is trying to stabilize after a sharp move higher, but the bigger question is whether this is real strength or just a short-term bounce. The breakout came on solid volume, yet the lack of follow-through and weak broader structure suggest buyers are still cautious.

News Background

- XRP ETFs saw $3.32M in inflows, but the scale remains too small to meaningfully shift price direction given the token’s size.

- The move continues to be driven more by technical positioning than fundamentals, with no clear catalyst behind the recovery.

Price Action Summary

- XRP moved from $1.33 to $1.35, breaking above the $1.34 level on strong volume.

- The initial push was sharp, but price quickly settled into a tight range just below $1.36 without extending higher.

- Short-term volatility remains elevated, with quick dips being bought but rallies still struggling to hold.

Technical Analysis

- The key signal is the quality of the breakout. Volume confirms participation, but the lack of continuation suggests this is not yet a strong trend shift.

- XRP remains within a broader downtrend, and rallies are still capped below the $1.40 level.

- Some indicators point to exhaustion rather than strength, with analysts flagging potential downside if momentum fades.

- At the same time, tight consolidation near current levels shows buyers are at least attempting to build a base.

What traders should watch

- $1.34 is now the immediate pivot. Holding above it keeps the short-term recovery intact.

- $1.36-$1.40 remains the key resistance zone. A clean break is needed to shift momentum meaningfully.

- On the downside, a move back below $1.32-$1.31 would signal the breakout has failed and reopen pressure toward $1.28.

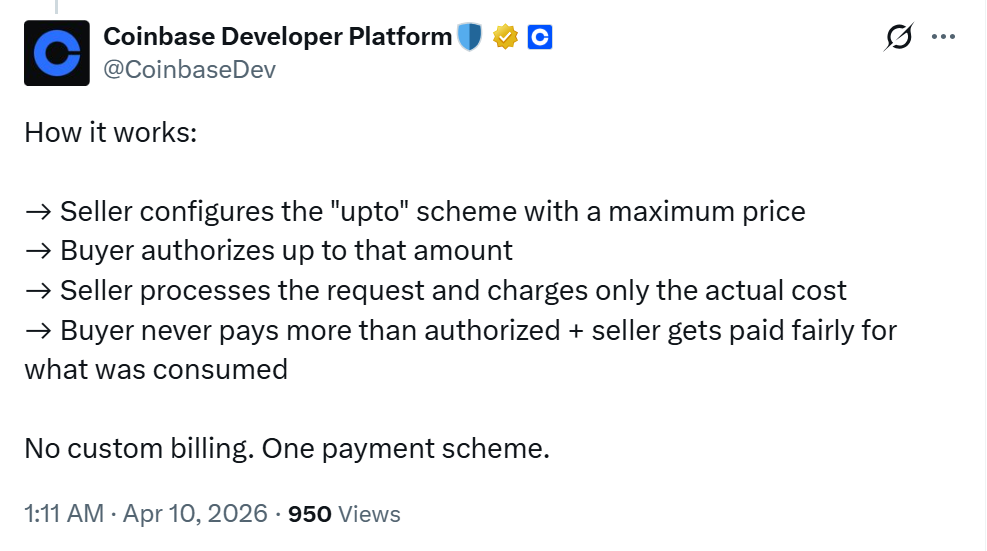

Coinbase has announced an upgrade for the x402 protocol, enabling usage-based pricing for agentic AI compute requests, which replaces the former flat fee model.

In a post on X on Thursday, Coinbase Developer Platform announced the “Upto” scheme has gone live, adding it will help open up “variable-cost services” for agentic AI such as large language model inference, compute and data queries.

“Until now, x402 only supported exact, fixed-price payments. That works great for deterministic APIs. But it blocked an entire category of services where the cost depends on usage, such as token count, compute time, or query complexity,” Coinbase Developer Platform said.

“Upto is an EVM implementation, supporting all ERC20s, and CDP Facilitator supports fully gasless payments,” it added.

The move comes amid growing support for the x402 protocol as a wide range of firms prepare for future agentic commerce adoption, which is expected to bring extreme levels of network demand and require frictionless payments and near-instant transactions to support agentic AI.

Flat-fee problem gets a fix

The Upto scheme allows sellers to configure maximum prices, while buyers will be able to authorize prices up to a specific amount.

On the server end, where costs fluctuate, the server will charge only for how much it actually takes to complete the task, meaning users won’t be overcharged and may even pay less than the specified maximum price.

Previously, simple and complex requests cost the same amount, resulting in some users either overpaying or underpaying for tasks done by AI agents. This upgrade will help users set prices they are willing to pay before a task instead of guessing how much they think the task will cost for an agent to complete.

Related: CIA to integrate AI ‘co-workers’ to process intelligence, catch spies

Developed by Coinbase, the protocol’s ownership was handed over to the nonprofit Linux Foundation earlier this month, with big tech firms such as Google, Microsoft and Amazon Web Services having a stake in the protocol via the x402 Foundation.

Despite the hype surrounding x402, the network has seen declining adoption rates in 2026 after hitting peak levels in November, according to Dune Analytics data. Between Nov. 4 and Nov. 10, the protocol saw 13.7 million transactions, its biggest week on record.

However, it has been on a steep decline since then, with weekly transaction volume dropping below 1 million in early January and continuing to plunge further over the first quarter. As of the last week in March, x402 saw just 112,708 transactions.

Magazine: AI agents will kill the web as we know it: Animoca’s Yat Siu

BeInCrypto, the world’s leading multilingual crypto news platform, and Proof of Talk, the “Davos of Web3,” are joining forces to co-host the Institutional 100 Awards. An awards program with a simple rule: if you made the list, you deserved to be there. Winners will be announced during Proof of Talk, June 2-3, 2026, at the Musée des Arts Décoratifs within the Louvre Palace in Paris.

The BeInCrypto x Proof of Talk Institutional 100 is an independent media awards program across six segments and 25 categories, from capital markets and tokenization to regulation, enterprise blockchain, and retail access to digital assets. It identifies and benchmarks the companies and individuals driving the convergence of TradFi and digital assets. Proof of Talk brings the right room: 2,500 CEOs, founders, and policymakers representing more than $18 trillion in AUM, 85% of whom hold decision-making authority. Getting into that room and getting onto this list work the same way.

Alena Afanaseva, CEO & Founder of BeInCrypto, comments:

“The Institutional 100 was built on a simple principle: no one buys their way onto this list, and no single opinion puts them there. Our two-stage evaluation combines hard data with independent expert judgment, so whoever makes the final list got there on merit. Proof of Talk is built the same way. You get in because of your track record, full stop. Having them come on as co-host is the most natural partnership we could have made.”

DEHNADI Zohair, Co-Founder & CEO, Proof of Talk, comments:

“Davos defined global finance for a generation. Proof of Talk is where Web3 defines the next one. We chose the Louvre deliberately, because history doesn’t happen in convention centres. It happens in rooms that convene CEOs who already know what it means to change the world. That’s the intention we bring to every conversation here.”

The Institutional 100 Methodology

The ranking evaluates over 500 candidates using a proprietary scoring system. Data is sourced from verifiable outlets including DefiLlama, Dune Analytics, SEC EDGAR, and Kaiko. Every nominee goes through two sequential assessment stages conducted by separate teams: Stage 1 applies quantitative screening using publicly verifiable data, followed by Stage 2, where a senior Expert Council of 10 to 13 practitioners spanning traditional finance, digital asset management, and regulatory advisory score the shortlisted candidates.

Council members include Rayhaneh Sharif-Askary, Managing Director and Head of Product and Research at Grayscale Investments; Sunday Domingo, Global Head of Digital Channel Solutions at Standard Chartered; Fabian Dori, Chief Investment Officer at Sygnum Bank; and Gregory Johnson, Board Member of the Bretton Woods Committee, among others.

Learn more about the awards: https://awards.beincrypto.com/

For PR and media requests, contact Iva Belamaric at iva.belamaric@beincrypto.com

About BeInCrypto

Founded in 2018, BeInCrypto is one of the world’s top three crypto news media platforms, known for accurate, unbiased, and multilingual reporting on blockchain, Web3, and market trends in 26

different languages; recognised by the Trust Project, a global standard for journalism

transparency.

For more information, visit: beincrypto.com | awards.beincrypto.com

About Proof of Talk

Proof of Talk unites Web3’s 2,500 most influential decision-makers under one roof to deliver the world’s highest value-per-square-meter experience in the Louvre Palace. Attendance is highly curated: 85% of participants hold C-level or equivalent roles, collectively responsible for $18+ trillion in assets under management.

For more information, visit: proofoftalk.io

The post BeInCrypto Teams Up with Proof of Talk to Launch the Institutional 100 Awards appeared first on BeInCrypto.

Bitcoin has climbed back above $72,000, keeping the short‑term uptrend intact while setting up a test between bullish targets near $78,000 and critical support around $70,000.

Summary

- BTC/USDT is trading just above $72,000 with a modest 24‑hour gain, keeping the short‑term uptrend intact as long as $70,000 support holds.

- A sustained push could open room toward the $78,000–$80,000 zone, but failure to defend $70,000 risks a move back toward $63,000–$65,000.

- Macro drivers such as rates, liquidity and U.S. regulation will likely matter more for the next big move than any single intraday breakout.

Bitcoin has pushed back above $72,000, but the structure behind the move matters more than the headline level. According to Gate, BTC/USDT is trading around $72,036, up 1.28% over the past 24 hours, while the Bitcoin price on crypto.news shows spot hovering near $71,375 with a 7‑day gain of more than 7% and a 24‑hour range between roughly $70,500 and $72,700. That places the market just below the upper end of its recent band and well off the October 2025 all‑time high near $126,000.

Bitcoin reclaims $72k as traders brace for upward momentum

Short term, the breakout above $72,000 keeps the bulls in control as long as Bitcoin holds the $70,000–$71,000 zone on closing bases. Several recent updates note that BTC has been forming a bullish continuation pattern, with some technical analyses flagging upside targets in the $78,000 area if momentum persists. On-chain and exchange‑flow data also show continued net outflows from centralized venues, a pattern often associated with spot accumulation rather than distribution. As long as those outflows persist and funding rates stay contained, a grind toward the mid‑$70,000s and a potential test of $78,000 looks plausible over the coming weeks.

Medium term, most model‑driven forecasts see room for further upside but not a straight line. One aggregated prediction set has Bitcoin trading in a rough $72,000–$93,000 band over the next 6–12 months, implying 10–30% potential upside from current levels if macro conditions cooperate. Separate scenario work suggests a base case around $98,000 by late 2026, with bull targets in the low $130,000s and bear cases closer to the low $50,000s, underscoring that volatility and policy risk remain central to the thesis. In practice, the path will be driven less by chart patterns than by the Federal Reserve’s rate path, U.S. regulatory clarity around bills like the CLARITY Act, and the durability of ETF inflows.

For now, the key levels are clear: holding $70,000 keeps the current structure intact and leaves room for a push toward $78,000–$80,000; losing that floor would reopen a slide back toward $63,000–$65,000, where ETF demand and institutional bids last showed up in size. Traders betting on a clean breakout need to remember the obvious: at these valuations, Bitcoin trades as a high‑beta macro asset, and any shock to rates, liquidity, or regulatory confidence can turn a 1.28% daily gain into a double‑digit drawdown fast.

Tether has released QVAC SDK, an open-source toolkit that lets developers run llama-based AI apps fully on-device across major platforms, without relying on cloud servers.

Summary

- Stablecoin issuer Tether has launched QVAC SDK, an open-source kit for running AI applications locally on devices instead of in the cloud.

- Built on a llama.cpp branch called QVAC Fabric, it supports text, speech, vision and translation, using Holepunch for peer-to-peer model distribution and delegated inference.

- Tether plans to add decentralized training and fine-tuning, plus specialized toolkits for robotics and brain-computer interface use cases.

Tether is extending its ambitions beyond stablecoins, launching an open-source software development kit called QVAC SDK that lets developers run AI applications directly on user devices without relying on cloud servers. According to the company, the toolkit is designed to make “local-first” AI accessible across consumer hardware, with support for iOS, Android, Windows, macOS, and Linux.

Built on a customized branch of llama.cpp dubbed QVAC Fabric, the SDK supports core AI capabilities including text generation, speech processing, visual recognition, and translation. Rather than pulling models from central servers, QVAC uses the Holepunch protocol stack for peer-to-peer model distribution and delegated inference, allowing devices in a network to share workloads and updates. In practical terms, that means a developer can ship an AI assistant, translator, or vision tool that runs primarily on the device, with models and computations distributed across a swarm of peers instead of a single data center.

For Tether, the move pushes its brand deeper into decentralized infrastructure at a time when concerns over data privacy, cloud dependence, and AI centralization are growing. Local inference reduces exposure to centralized outages and limits the need to send sensitive data to remote servers, but it also shifts more responsibility for optimization, security, and user experience to the edge. The company says QVAC SDK is intended to make that trade-off easier by abstracting away much of the platform-specific integration across phones, desktops, and servers.

Looking ahead, Tether plans to add decentralized training and fine‑tuning capabilities on top of QVAC, alongside specialized toolkits for robotics and brain–computer interface applications. If delivered, that would move the project from inference-only tooling into a full-stack environment where models can be trained, adapted, and deployed in a distributed way. The roadmap underlines a broader bet: that the next wave of AI will not only live in hyperscale clouds, but also in local, peer‑to‑peer networks where ownership of both data and compute sits closer to the user. Whether QVAC can attract a critical mass of developers—and demonstrate that local, open-source AI can compete with tightly integrated cloud offerings—will determine if this toolkit becomes core infrastructure or just another experiment on the edge of the AI-crypto frontier.

Bitcoin’s (BTC) relief rally to $72,000 appears to be cooling off, but analysts said that the BTC price may “continue rising” in the short term.

Key takeaways:

-

Bitcoin must flip the short-term holder realized price at $80,000 into support to confirm the trend change.

-

Spot volume and trading activity must recover to ensure a sustained breakout in BTC price.

Bitcoin must reclaim $80,000 as support

Bitcoin’s 8% climb over the last three days to $72,000 saw it reclaim key levels, including the 200-day exponential moving average (EMA) at $68,000, and the 50-day EMA at $70,000, where it has found support.

“$BTC is currently in a buy wall zone. The current zone is a support zone,” said analyst CW8900 in a Thursday post on X, referring to the area between $67,700 and $70,000.

Related: Bitcoin eyes $90K as Binance data shows surge in aggressive buying

The bullish case for BTC now hinges on cracking a sell wall between $72,000 and $73,000, where investors acquired 386,100 BTC over the last three months.

“There is a sell wall up to $73K,” CW8900 said, adding:

“It must break through this sell wall to continue rising to $75K.”

Glassnode’s risk indicator reveals another major resistance higher up between the true market mean at $78,000 and the short-term holder cost basis level around $80,000.

“This is a particularly meaningful threshold,” Glassnode said in its latest Week Onchain newsletter, adding:

“Until price reclaims this level, the mid to long-term bias remains tilted to the downside, as any rally into this zone is likely to encounter meaningful distribution pressure from recent buyers seeking to exit at or near breakeven.”

As Cointelegraph reported, the bulls must decisively break above the $76,000-$80,000 range to confirm a trend change.

Bitcoin’s transfer volume cools by 50%

The market remains in a cool-down phase, with Bitcoin onchain transfer volume and spot trading volume still down.

The seven-day moving average of onchain transfer volume has dropped by about 50.5% to 660,000 BTC on Thursday, from 1.36 million BTC less than 30 days ago.

Additionally, spot activity remains subdued, with the 30-day spot relative volume across all exchanges muted below 1.0, significantly lower than the cyclical peaks seen in the latest bull market.

This divergence further underscores the lack of speculative intensity required to drive prices higher.

The chart below shows only a mild uptick in the spot volume, but nothing that suggests a meaningful return of participation.

“Until spot demand picks up, rallies are likely to feel fragile, with limited follow-through,” Glassnode said, adding:

“A clear expansion in volume would signal stronger conviction and a healthier foundation for continuation.”

As Cointelegraph reported, spot and derivatives markets are entering recovery mode, with Bitcoin’s spot net volume delta and taker cumulative volume delta edging back into the positive territory.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

TLDR

- Pavel Durov said TON is now 10× faster after its latest blockchain upgrade.

- TON said the mainnet will begin sub-second finality on April 10 through Catchain 2.0.

- Durov said block production increased by 6× and transactions are now instant.

- TON said the faster network will support payments, trades, and Mini Apps inside Telegram.

- Durov said the next planned step will reduce TON transaction fees by

Pavel Durov said on Thursday that TON now processes transactions in about one second. He said the latest network upgrade raised block production and improved transaction speed. TON said the mainnet will gain sub-second finality on April 10 through Catchain 2.0.

TON Upgrade Raises Speed and Cuts Confirmation Time

Durov posted the update on Telegram and called the blockchain “10× faster.” He added, “Block rate increased 6× … Transactions are now instant, subsecond.”

TON said the upgrade already runs, yet the release is also named April 10 for mainnet sub-second finality. That wording placed the rollout details at the center of Thursday’s announcement.

The company said Catchain 2.0 powers the change and cuts confirmation times from about ten seconds. It said faster finality supports instant payments, quicker trades, and responsive Mini Apps.

Telegram uses TON for transactions and for Mini Apps inside its messaging platform. The blockchain operates separately, yet it remains closely linked to Telegram’s ecosystem.

TON said the upgrade targets scale inside Telegram’s user base of more than 1 billion people. It said lower delay makes in-app payments feel like sending a message.

The statement said earlier that confirmation times limited some app behavior inside Telegram. It said some trades and app responses could not feel instant at ten seconds.

Durov described the release as step one of seven in a plan he called MTONGA. He said the next step will cut TON transaction fees by 6×.

Telegram Link and TON Roadmap Remain in Focus

Telegram began work on blockchain tools in 2018 before U.S. regulators challenged the original project. Open-source developers revived the work in 2022 and renamed it The Open Network.

That effort produced TON, which now serves as infrastructure for payments and app activity around Telegram. Thursday’s upgrade marked the network’s latest technical change under that revived project.

TON said more blocks should raise validator rewards and increase staking incentives. It linked those economics to the higher block rate after the upgrade.

The release did not list new fee levels or a date for the planned fee cut. Durov only said the network would target fees that are already low.

The company framed the speed gain as a base for apps that need immediate user responses. It said those uses include payments, trading, and Mini App actions.

Durov repeated that TON had become faster and said the release started a seven-step roadmap. He gave no added technical details in his Thursday post. TON said sub-second finality on mainnet begins April 10 under Catchain 2.0.

TLDR

- BlackRock appointed Galaxy Digital as an approved validator for its iShares Staked Ethereum Trust ETF, ETHB.

- ETHB held more than $435 million in assets under management as of April 8.

- The fund had staked $339 million in Ether through institutional validators, including Figment, Attestant, and Galaxy.

- Galaxy ended 2025 with $5 billion in staked assets across Ethereum, Solana, and other proof-of-stake networks.

- BlackRock said ETHB will distribute staking rewards to investors on a monthly basis.

BlackRock has appointed Galaxy Digital as a validator for its iShares Staked Ethereum Trust ETF, ETHB. The move adds Galaxy to the fund’s validator roster after ETHB launched last month. BlackRock will distribute monthly staking rewards directly to investors through the ETF structure.

BlackRock Expands ETHB Validator Lineup

As of April 8, ETHB held more than $435 million in assets under management. The fund had also staked $339 million in Ether across approved institutional validators.

BlackRock selected Figment, Attestant, and Galaxy to stake most of the fund’s Ether. The company said those providers support the operational standards required for the product for BlackRock.

Steve Kurz said BlackRock chose Galaxy because it proved “systems, scale, and accountability.” He added, “That trust is something we’ve earned over years of building.”

Kurz serves as Galaxy’s global co-head of digital assets. His statement appeared in Thursday’s press release announcing Galaxy’s validator role for ETHB for the BlackRock fund.

BlackRock’s Bitcoin ETF remains one of the largest digital asset funds launched globally since 2024. ETHB now follows that expansion with a product built to generate staking income for shareholders.

Galaxy Builds out Institutional Staking Services

Galaxy ended 2025 with $5 billion in staked assets across Ethereum, Solana, and other networks. Its digital infrastructure unit manages validation services for several proof-of-stake blockchains and related infrastructure.

During 2025, Galaxy completed custodial integrations with BitGo, Zodia Custody, Fireblocks, and Coinbase Prime. Those links expanded access for institutions using Galaxy’s staking and digital asset services across major custody channels.

Galaxy also became the development company behind Liquid Collective, an institutional liquid staking protocol. The protocol targets clients seeking yield and liquidity at the same time for institutions.

Robert Mitchnick said staking is “a core component” of Ethereum and ETHB investor access. He leads BlackRock’s digital assets division.

Mitchnick added that experienced providers help BlackRock meet the structure and standards clients expect. BlackRock included that comment in the announcement.

Galaxy recently launched staking on GalaxyOne, its platform for institutional clients and counterparties. The company said clients can earn yield there without platform commissions.

Galaxy has also advanced proxy voting on blockchain through a partnership with Broadridge. That work uses the Avalanche network for on-chain corporate governance functions and shareholder voting.

The partnership extends Galaxy’s institutional blockchain services beyond validation and staking. Broadridge and Galaxy announced the effort separately earlier this year.

ETHB launched last month as BlackRock’s first crypto exchange-traded product with staking rewards. Galaxy now joins its approved staking validators.

SI.com Proposes Very Weird Vikings QB Trade

York’s Shambles was worse in the old potty-emptying days!

Morning Bid: ’That is not the agreement we have!’

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

Business5 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion4 days ago

Fashion4 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion3 days ago

Fashion3 days agoLet’s Discuss: DEI in 2026

-

Politics7 days ago

Wings Over Scotland | The quality of mercy

-

Crypto World2 days ago

Crypto World2 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Crypto World17 hours ago

Crypto World17 hours agoCanary Capital Files SEC Registration for PEPE ETF

-

Fashion7 days ago

Fashion7 days agoFrugal Friday’s Workwear Report: Hammered Metallic Button Sweater Vest

-

Politics6 days ago

Politics6 days agoThe UK should not pay a penny in slavery reparations

-

Tech4 days ago

Tech4 days agoHaier is betting big that your next TV purchase will be one of these

-

Business7 days ago

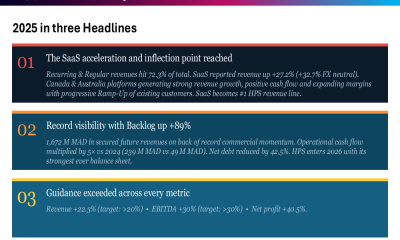

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion7 days ago

Fashion7 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

-

Fashion7 days ago

Fashion7 days agoWeekly News Update, 4.3.26 – Corporette.com

-

Tech4 days ago

Tech4 days agoSamsung just gave up on its own Messages app

-

NewsBeat7 days ago

NewsBeat7 days agoRory McIlroy hopes to emulate greats as he aims to make more history

You must be logged in to post a comment Login