Crypto World

Micron (MU) Stock: Analysts Hold Strong Despite Post-Earnings Dip

Key Takeaways

- Micron’s fiscal Q2 2026 delivered $23.86 billion in revenue with adjusted EPS of $12.20, surpassing analyst expectations

- The company projected fiscal Q3 2026 revenue of approximately $33.5 billion, significantly exceeding Street estimates

- Capital expenditure guidance for fiscal 2026 increased to more than $25 billion, roughly $5 billion higher than previous projections

- Shares declined following the earnings announcement despite impressive financial performance, primarily due to elevated spending concerns

- Analyst sentiment remains overwhelmingly positive with 29 Buy ratings, 5 Strong Buys, and no Sell recommendations according to MarketBeat data

Micron Technology unveiled exceptional quarterly results on March 19, yet the market’s response told a more complex story. Despite impressive revenue figures and unprecedented free cash flow generation, shares retreated as Wall Street digested the company’s ambitious capital investment strategy.

The memory chip giant reported fiscal second-quarter 2026 revenue reaching $23.86 billion alongside adjusted earnings of $12.20 per share. Micron also highlighted that it closed the period with $16.7 billion in cash and investments, marking a company record for free cash flow generation.

While these figures impressed, it was the forward-looking commentary that captured the most attention—both positive and negative.

For fiscal Q3 2026, Micron projected revenue of approximately $33.5 billion, substantially exceeding Wall Street’s expectations. The company attributed this robust outlook to explosive demand for high-bandwidth memory (HBM) products, which are essential components in AI data centers and acceleration hardware.

HBM represents today’s most sought-after memory technology. Micron operates within an oligopoly of just three major global producers, joined by Samsung and SK hynix. This concentrated supply structure has bolstered pricing power and supported healthy profit margins.

Understanding the Post-Earnings Decline

Notwithstanding the impressive financial performance, Micron’s stock price declined following the announcement. The catalyst? A significantly revised capital spending forecast.

The company disclosed that fiscal 2026 capital expenditures would surpass $25 billion, representing an approximate $5 billion increase from earlier guidance. Management explained the investment is necessary to expand clean-room infrastructure and accelerate DRAM manufacturing capacity to satisfy AI-driven demand.

This scenario represents a classic semiconductor industry dilemma—deploying massive capital to capture growth opportunities while risking oversupply if market conditions deteriorate. Memory manufacturers have historically encountered this challenge, and investors maintain vivid memories of past overcapacity cycles.

Additionally, the stock’s valuation had already reflected substantial optimism. Prior to Thursday’s retreat, Micron had surged more than 61% during 2026, building on strong momentum from 2025. At such elevated levels, any hint of risk can trigger profit-taking behavior.

Wall Street Maintains Conviction

The analyst community showed no signs of wavering. According to MarketBeat data released on March 19, Micron holds five Strong Buy ratings, 29 Buy ratings, and four Hold ratings. Notably, zero analysts recommend selling the stock.

This represents nearly unanimous bullish positioning. The four Hold ratings suggest some analysts advocate patience at current valuations, but bearish recommendations remain completely absent.

Price targets underwent revisions as analysts updated their financial models following the report. MarketBeat’s consensus tracking indicated a range settling between approximately $425.62 and $446.66.

Several firms subsequently raised their targets. Needham elevated its price objective to $500. UBS similarly increased its target while reaffirming its Buy rating. Both institutions cited the sustained strength of AI-related memory demand as their primary rationale.

These $500 price targets represent more than optimistic projections—they embody a conviction that Micron’s AI-driven growth trajectory extends further than current market pricing acknowledges.

The investment debate surrounding Micron has evolved. Questions no longer center on whether the company is emerging from a downturn. Instead, the focus has shifted to whether Micron can sustain expansion without excessive capital deployment.

Presently, analysts are answering affirmatively. With 34 Buy or Strong Buy ratings and zero Sell recommendations in current MarketBeat data, Micron stands as one of the most broadly supported equities in the AI semiconductor sector.

The stock declined on March 19. The analyst community’s conviction remained intact.

Gemini has been hit with a proposed class action in New York for allegedly misleading investors during and after the crypto exchange’s September initial public offering.

The class action lawsuit filed by shareholders on Thursday in a Manhattan federal court against Gemini, its co-founders Tyler and Cameron Winklevoss, and company executives, claims they made misleading statements in the company’s IPO documents.

Plaintiff Marc Methvin claimed that the documents portrayed Gemini as a growing crypto exchange focused on expanding its user base and international footprint, but made an “abrupt corporate pivot to a prediction-market-centric business model.”

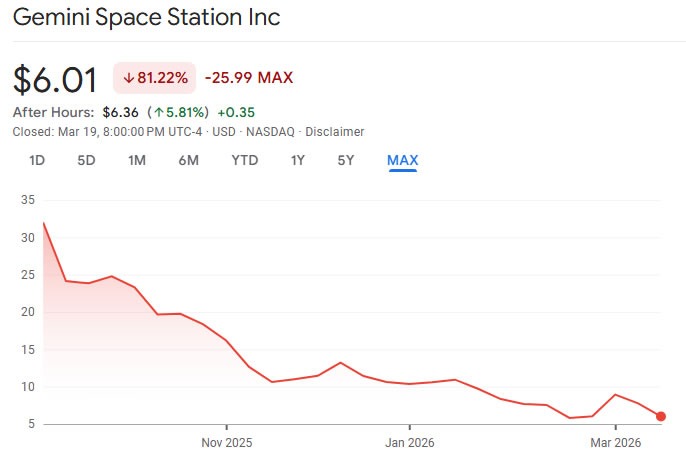

Gemini held its IPO in September, floating its shares at $28 on the Nasdaq. The stock briefly tapped $40 but has since fallen by more than 80% to trade at around $6 on Thursday.

The plaintiffs are seeking a jury trial and damages as compensation for investors who bought shares at what the complaint claimed were “artificially inflated prices” shortly after the IPO.

Prediction market pivot caused stock drop, say shareholders

According to the complaint, in November, Gemini executives publicly touted its international expansion progress, stating the company was committed to extending into “key global markets.”

The lawsuit said Gemini IPO documents described the exchange as its “core product.” However, in early February, the Winklevoss brothers announced a pivot to prediction markets called “Gemini 2.0.”

The firm also announced that it would cut 25% of its workforce and exit the EU, UK, and Australian markets.

Related: Gemini post-IPO shakeup sees exit of three top executives

Later that month, the company’s chief financial officer, chief operations officer, and chief legal officer all departed as the firm reported increased operating expenses of around 40%, according to the lawsuit.

The complaint claimed that as a result of these changes, the class group had seen “significant losses and damages” as Gemini’s stock price dropped to an all-time low of $5.82 by February 20.

Gemini reported on Thursday that its Q4 revenues rose 39% year-on-year to $60.3 million, beating analyst expectations of $51.7 million.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

US authorities say the co-founder of Super Micro Computer, Inc. has been charged and arrested over an alleged multi-billion dollar scheme to smuggle advanced artificial intelligence chips from the US to China.

The Justice Department said in a statement on Thursday that it had unsealed an indictment charging Yih-Shyan “Wally” Liaw, as well as Super Micro sales executives Ruei-Tsang “Steven” Chang, and Ting-Wei “Willy” Sun over the alleged conspiracy.

Prosecutors said the trio violated US export control laws by conspiring “to sell billions of dollars’ worth of servers integrating sensitive, controlled graphic processing units to buyers in China.”

Super Micro, which was not charged, is a $18.5 billion California-based tech company specializing in high-performance server and data center hardware for large-scale companies such as IBM. Its infrastructure partners include firms like Nvidia and Google.

The Justice Department said the alleged scheme involved the trio using a range of concealment techniques to hide the sale of around $2.5 billion worth of servers to a company in China across 2024 and 2025, with $510 million worth of sales occurring between April and May 2025 alone.

“These defendants allegedly fabricated documents, staged bogus equipment to pass audit inventories, and used a pass-through company to conceal their misconduct and true clientele list,” said James Barnacle, Jr., FBI assistant director in charge of the New York Field Office.

Liaw and Sun have been arrested and will stand before a judge in the Northern District of California. Meanwhile, the Justice Department said that Chang, a Taiwanese citizen based outside the US, “remains a fugitive.”

Super Micro stock dives, company says it’s cooperating

In a statement shared with Cointelegraph, Super Micro distanced itself from the trio and labeled the alleged actions as a “contravention of the Company’s policies and compliance controls.”

Related: DOJ and Europol take down SocksEscort network tied to crypto fraud

“The company has been cooperating fully with the government’s investigation and will continue to do so. Supermicro has not been named as a defendant in the indictment,” a company spokesperson said.

Super Micro’s stock had initially gained during regular trading hours on Thursday. Following the Justice Department’s announcement, the stock has since dropped 13.25% to $26.71 in after-hours trading.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

Bitcoin and the wider crypto market saw a notable price bounce on Friday after major economies announced joint efforts to boost oil supplies through the now-disrupted Strait of Hormuz.

BTC, the largest cryptocurrency, jumped to $70,800, up more than 1% on the day, extending its recovery from overnight lows under $68,900, according to CoinDesk data. Other major coins, including ether (ETH), XRP (XRP), and solana (SOL), saw smaller gains of less than 1%, lagging behind bitcoin.

West Texas Intermediate (WTI) crude fell nearly 2% to $93.80, alongside similar losses in Brent, after Britain, France, Germany, Italy, the Netherlands, and Japan said they would take steps to stabilize energy markets and join collaborative efforts to ensure safe passage through the Strait of Hormuz. In a joint statement issued by the U.K. Prime Minister Keir Starmer’s office, leaders of these nations condemned the attacks by Iran and urged it to halt its actions immediately.

On Thursday, U.S. Treasury Secretary Scott Bessent said the U.S. may soon remove sanctions from Iranian oil tankers and could release crude from its Strategic Petroleum Reserve.

With the Federal Reserve expressing heightened uncertainty on growth and inflation outlooks earlier this week, traders have scaled back expectations for Fed rate cuts. That has left crypto and traditional risk assets largely at the mercy of oil price swings.

The latest drop in oil, though positive, doesn’t end the uncertainty, as military conflict in the Middle East continues. WTI remains near recent support at $92.00, still significantly above pre-war valuations.

“For now, WTI crude continues to hold what appears to be an increasingly important area of support. That level aligns well with prior highs and the short-term trend. As long as oil holds that support and the trend continues higher, it will likely maintain an upward bias,” Mott Capital Management said in an email to its subscribers.

The firm added that positioning in the oil options market suggests higher levels are possible.

Another market that bitcoin traders might want to watch is the S&P 500, Wall Street’s benchmark equity index.

The index closed below its pivotal 200-day simple moving average (SMA) on Thursday – the first such instance since May last year – signaling a bearish shift in momentum. A potential strengthening of risk aversion in stocks could spill over into crypto and the wider financial markets.

TLDR:

- The Fed now projects only one rate cut for 2026, leaving Bitcoin and risk assets with limited near-term relief.

- Inflation forecasts have been revised upward to 2.7% for 2026, driven partly by rising oil and natural gas prices.

- The U.S. 30-year treasury yield is approaching 5%, raising the cost of capital and tightening global liquidity.

- Bitcoin remains caught between its identity as a store of value and a speculative asset in uncertain macro conditions.

Bitcoin continues to face mounting pressure as macroeconomic conditions grow increasingly unfavorable. The Federal Reserve’s hawkish stance, sticky inflation, and rising treasury yields are tightening global liquidity conditions.

With only one rate cut now projected for 2026, risk assets are finding it harder to attract fresh capital. Meanwhile, geopolitical tensions between the U.S. and Iran are adding upward pressure on energy prices.

This mix of factors is reshaping investor sentiment and pushing capital toward safer, higher-yielding assets.

Fed’s Hawkish Tone Puts Bitcoin Under Pressure

Federal Reserve Chair Jerome Powell recently delivered a hawkish tone on the broader economic outlook. The central bank now projects only one rate cut for 2026.

The dot plot remains unchanged for now, offering little immediate relief for risk-sensitive markets. Powell did not explicitly raise the possibility of rate hikes, but that scenario has not been fully ruled out.

Inflation remains the central issue driving the Fed’s restrained approach to monetary policy. Projections have been revised upward to 2.7% for 2026, reflecting persistent price pressures across the economy.

The Fed expects further inflationary stress, partly tied to rising oil and natural gas prices. Ongoing tensions between the U.S. and Iran are fueling much of that energy-related surge.

Crypto analyst Darkfost_Coc noted that the Fed cannot act decisively while inflation remains sticky. This restraint leaves Bitcoin and other risk assets in a difficult position.

Without rate relief, borrowing costs stay elevated and investor appetite for risk remains constrained across markets.

At the same time, early signs of weakness are beginning to surface in the labor market. Economic growth is also slowing at a measured but noticeable pace.

Together, these trends are bringing stagflation risks back into broader financial discussions. Such an environment has rarely favored speculative assets, and Bitcoin is no exception.

Rising Yields and a Stronger Dollar Limit Bitcoin’s Recovery

As yields rise, the dollar is strengthening once again, creating a challenging backdrop for Bitcoin. This dynamic tends to tighten global liquidity and reduce capital flows toward higher-risk markets.

According to Darkfost_Coc, periods when the dollar and treasury yields become too strong consistently weigh on Bitcoin.

The U.S. 30-year yield is now approaching 5%, a key benchmark closely tied to mortgage lending. The 10-year yield is hovering near 4.30%, raising the overall cost of capital across markets. Higher borrowing costs make it more difficult to invest, finance operations, or take on leveraged positions.

If geopolitical tensions persist, elevated yields could attract large pools of capital seeking safer returns. Investors may shift funds into treasuries, which offer relatively attractive yields with minimal risk. This further drains the liquidity that would otherwise flow into risk assets like Bitcoin.

Bitcoin still struggles to clearly define its role within the broader global financial system. It continues to occupy an uncertain space between a store of value and a speculative asset.

Until that identity solidifies, the current macro environment will keep limiting its ability to draw sustained capital.

The FBI has issued a warning about a fake token on the Tron blockchain that is impersonating the agency to trick users in a crypto phishing scam.

Summary

- FBI warns of fake Tron tokens impersonating the agency and claiming wallets are under investigation.

- Users are directed to fraudulent websites demanding AML verification to avoid asset freezes.

- Token has reached at least 728 wallets, with some holding over $1 million in USDT.

FBI’s New York Field Office issued a message on Thursday warning that scammers were sending tokens to users to siphon personal information under the pretence that the recipient’s wallet was “under investigation.”

Recipients of the token are redirected to a website where they are asked to complete an anti money laundering verification online “to avoid a total block on your assets.”

“FBI New York encourages users of the Tron blockchain network to exercise caution if they encounter a token purported to be from the FBI,” the agency said, advising users not to provide “any identifying information to any website associated with such [a] token.”

The token also comes with warnings that a user could face “a total block” on their assets if they fail to clear the verification process.

Once on the malicious website, victims are told that “current sanctions” can be avoided if users immediately comply with the request.

Similar tactics are common across other phishing scams where bad actors prey on urgency to extract sensitive information.

Scammers may be targeting users who are concerned about potential regulatory scrutiny and fear enforcement action.

According to data from Tronscan, the token was sent to at least 728 digital wallets, and many of these wallets held more than $1 million in USDT.

Those who have already shared information have been urged to file a report with the FBI’s Internet Crime Complaint Center.

FBI developed their own crypto to bust scammers

While the FBI has confirmed that it has no involvement with the fake token, in the past, the agency developed a token to take down a market manipulation network.

As previously reported by crypto.news, the FBI launched NexFundAI during a sting called “Operation Token Mirrors.” The token was used to expose a wash trading ring involved in artificially inflating prices.

Meanwhile, phishing remains a consistent threat and has become one of the leading attack vectors in recent years, resulting in multi-million dollar losses across incidents.

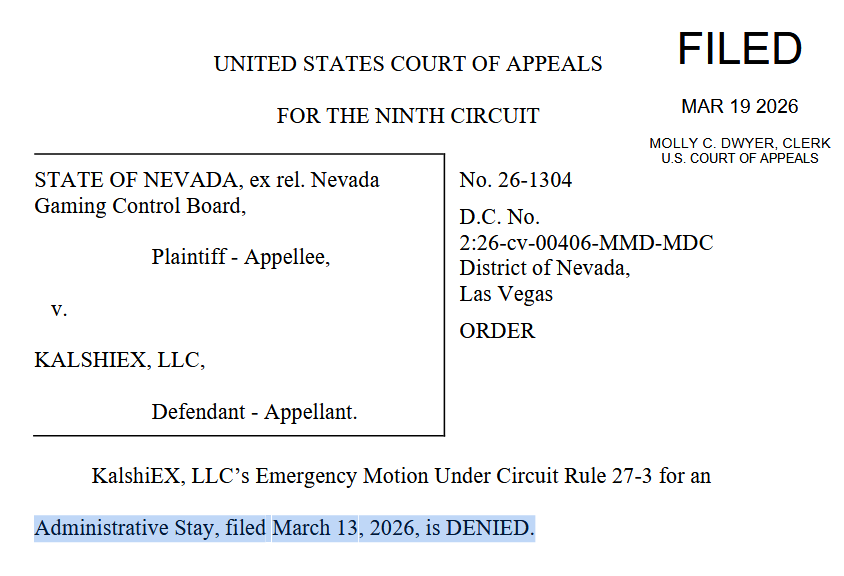

US gaming lawyer Daniel Wallach says a Nevada state court-issued restraining order against Kalshi appears imminent, preventing it from offering sports-related contracts.

A federal appeals court has cleared Nevada state authorities to enforce a temporary restraining order on Kalshi to block its sports event contracts.

The Ninth Circuit Appeals Court on Thursday denied Kalshi’s emergency request to stay a lower court proceeding, meaning the case will be sent back to federal court and will allow Nevada’s regulators to take action.

Gaming lawyer Daniel Wallach said a temporary restraining order (TRO) against Kalshi now appears imminent, and added that it wouldn’t be able to operate in Nevada for at least 14 days until a preliminary injunction hearing is held:

“Since a TRO is not appealable under Nevada law, Kalshi would be required to exit the state in the interim.”

The Nevada Gaming Control Board sent Kalshi a cease-and-desist in March over its offering of sports event contracts, arguing they are unlicensed sports betting under Nevada law.

Kalshi has argued in court that its event contracts are under the sole federal jurisdiction of the Commodity Futures Trading Commission and any block on its event contracts would cause it “imminent harm.”

Prediction markets such as Kalshi and Polymarket have recently surged with weekly trading volumes now consistently exceeding $2 billion, according to Dune Analytics, which has also attracted increased scrutiny from lawmakers with concerns over insider trading and market manipulation.

Related: SEC interpretation on crypto laws ‘a beginning, not an end,‘ says Atkins

State regulators in Connecticut, New York, New Jersey and other states have also sought to take action over sports event contracts, with Kalshi and rival prediction market platforms Crypto.com, Polymarket and Coinbase in legal battles with multiple states.

Kalshi foresees conflict between courts

In a motion on March 13, Kalshi argued that letting Nevada proceed with its temporary restraining order while federal litigation is still pending creates a serious risk of conflicting rulings.

Kalshi said the courts could arrive at “exactly the opposite conclusion” as to whether federal commodities law preempts state gambling laws, adding that it could “create jurisdictional chaos.”

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

Gemini pushed through a better-than-expected fourth quarter even as the broader crypto market remained under pressure. The exchange reported revenue of $60.3 million for Q4, up 39% from a year earlier and ahead of consensus estimates of about $51.7 million. However, the company also posted a net loss of $140.8 million for the quarter, widening from a $27 million loss in the same period a year ago. For the full year, Gemini’s loss totaled $585 million in 2025, compared with $156.6 million in 2024. The results come after the platform went public in September and amid a late-2025 crypto drawdown that saw Bitcoin slide from its peak above $126,000 in October.

Shares of Gemini initially moved higher in after-hours trading, climbing as much as 14% to a high of $6.83 before settling around $6.36, for a gain of roughly 6% on the session. The day’s action mirrored the market’s mixed reception to a growth-focused quarter that delivered a revenue win but did not escape the ongoing profitability challenge for many crypto incumbents.

Key takeaways

- Gemini’s Q4 revenue of $60.3 million rose 39% year over year and beat estimates of about $51.7 million, signaling business momentum even as trading volumes cooled.

- The quarter produced a net loss of $140.8 million, deepening from a $27 million loss a year earlier; the company’s 2025 loss reached $585 million, higher than 2024’s $156.6 million.

- Management cited deliberate fee-structure optimization and other efficiency measures as drivers of revenue growth, even with a softer trading environment.

- Gemini is accelerating a strategic shift toward a markets-focused organization, highlighted by the launch of Gemini Predictions across all 50 states and a plan to leverage that infrastructure for perpetual futures once approved in the U.S.

Strategic ambitions sharpen as cost discipline takes center stage

In a February update, Gemini said it was trimming its workforce by roughly 30% since the start of 2026, citing challenging market conditions. The leadership framing this downsizing as part of a broader pivot toward a more AI-driven, efficiency-first operating model. Co-founders Cameron and Tyler Winklevoss highlighted a rapid integration of artificial intelligence into the development process, noting that AI is now used in more than 40% of production code changes and is expected to rise significantly in the near term. “Not using AI at Gemini will soon be the equivalent of showing up to work with a typewriter instead of a laptop,” they wrote in a shareholder letter.

The Winklevoss duo signaled a clear pivot toward a U.S.-centric growth strategy, underscoring optimism about a pro-crypto regulatory environment in the United States. They stressed that 2026 would be about focusing and expanding in America, aligning with a broader investor interest in platforms that can scale within clearer regulatory boundaries.

From trading floors to markets infrastructure: Predictions and futures ambitions

Gemini has been building out its markets-oriented toolkit, most notably with Gemini Predictions. The platform rolled out its in-house prediction market across all 50 states in December, shortly after obtaining a license from the Commodity Futures Trading Commission. The company described its longer-term plan as turning Gemini into a “markets company” anchored by predictions, with the potential to extend that framework to perpetual futures contracts once U.S. approval is secured.

The December launch followed a prior line of coverage noting Gemini’s broader ambition to expand beyond traditional exchange functions into more complex financial primitives. As part of the 2026 roadmap, the company intends to refine and grow Predictions while simultaneously scaling its credit card program and exchange services, tapping into a more diversified revenue mix that could help weather ongoing volatility in crypto trading volumes. In evaluating the strategic path, investors will also be watching how regulatory feedback in the U.S. shapes the pace of approvals for new product categories, including perpetual futures.

These plans come against the backdrop of a February update that confirmed Gemini’s withdrawal from the U.K., the EU and Australia, a move the company attributed to tougher market conditions. The leadership’s stated aim is to “focus and double down on America,” a stance that aligns with the firm’s renewed investment in U.S.-based market infrastructure and its growing bets on a more favorable regulatory climate for crypto innovation.

The company’s quarterly results reflect a broader pattern among newer, publicly traded crypto platforms: revenue growth can outpace trading volumes due to fee-structure optimization, product diversification and active expansion into non-trading monetization streams. Gemini’s fourth-quarter performance—driven by its credit card program and pricing strategy—offers a data point suggesting that meaningful upside can still emerge even amid a subdued price cycle. The question for investors now is whether the path to profitability can be accelerated through AI-enabled efficiency gains and a clearer, U.S.-centered growth engine, supported by product bets in prediction markets and, potentially, regulated futures.

According to the company’s investor materials, the Q4 results marked the highest quarterly revenue in three years, reflecting the impact of the revised fee structure through the back half of 2025 and a push into more monetizable products. The combination of revenue resilience and continued investment in AI-driven scale positions Gemini as a case study in how crypto platforms seek to balance growth with cost discipline during a protracted market downturn.

For investors and builders watching the sector, the key takeaway is that 2026 could hinge on how quickly Gemini translates its market infrastructure into sustainable profitability, the pace at which U.S. regulators greenlight broader product suites, and how effectively the firm scales non-trading revenue streams, like predictions markets and card programs, in a regulated environment.

Readers should keep an eye on next-quarter earnings and regulatory developments that could determine the speed at which Gemini completes its shift toward a broader markets-facing business model while continuing to nurture its consumer-facing products.

Morgan Stanley wants its planned spot bitcoin ETF to trade under the ticker MSBT when it debuts.

The investment bank disclosed the ticker in its latest filing with the U.S. Securities and Exchange Commission (SEC), amending its January application for the fund.

The filing also revealed key fund details, which include a 10,000-share creation unit required to build the ETF, and a planned $1 million seed investment, or the initial money used to start the fund. The investment bank bought two shares early this month for audit purposes, it added.

According to an earlier filing, BNY Mellon has been designated to handle the fund’s cash and administrative functions, while Coinbase will serve as prime broker and custodian of its Bitcoin holdings.

Morgan Stanley’s move underscores Wall Street’s growing push into crypto, as established banks and custodians work to make bitcoin more accessible to mainstream investors.

If approved, the Morgan Stanley ETF would let investors get exposure to bitcoin without owning it, joining 11 other spot ETFs, including BlackRock’s IBIT, that have been active since January 2024. Those funds have already attracted over $56 billion in investor inflows.

The investment bank also filed an application for a Solana ETF alongside bitcoin earlier this year, but it has yet to submit any updates for that fund.

The major gold trade association, World Gold Council, and the Boston Consulting Group have proposed a new platform to modernize how the precious metal operates in digital financial systems.

The World Gold Council said on Thursday that it published a white paper on “Gold as a Service,” a new platform to “support the issuance and operation of scalable, interoperable digital gold products.”

The open platform would connect the physical custody of gold with the digital systems used to issue and manage tokenized gold products.

“By standardizing essential market processes such as custody coordination, reconciliation, compliance, and redemption, the model aims to reduce operational complexity, improve access, and enable greater consistency across digital gold products,” the World Gold Council said.

Crypto-native tokenized gold products include Tether Gold (XAUT) or Pax Gold (PAXG), which have formed their own custody, compliance and redemption models, but the World Gold Council’s standard could have more sway with institutions due to the trade group’s prominence.

Features include audits, fungibility, and liquidity

Key features of the Gold as a Service would include standardizing tokenized gold issuance and management, increasing digital gold’s fungibility, embedding audits and assurance, enabling interoperability with existing finance rails, and improving liquidity in lending and borrowing markets.

World Gold Council CEO, David Tait, said that financial services are undergoing a “rapid and pervasive digital transformation” and gold must also evolve to maintain its role in the global financial system.

“Shared infrastructure can help gold become more accessible, more easily traded and fully integrated into modern financial systems — ensuring it remains as relevant tomorrow as it has been for millennia,” he added.

Related: Retail tripled gold buying in last 6 months as Wall Street sells

Matthias Tauber, a managing director and senior partner at Boston Consulting Group, said, “The question is no longer whether gold will be digital; it’s how it can participate in modern financial systems without compromising physical integrity.”

Commodities are 20% of tokenized asset market

According to RWA.xyz, tokenized commodities such as gold account for around $5.5 billion, or 20% of the total on-chain value of tokenized real-world assets, a segment that has grown by 340% over the past 12 months, as demand for gold has skyrocketed.

Tether’s tokenized gold product has a market capitalization of $2.6 billion, up 17% over the past 12 months, while Pax Gold has a market cap of $2.3 billion, according to CoinGecko.

On Thursday, crypto exchange Bybit launched a yield-bearing tokenized gold product that lets users earn interest on Tether Gold.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

Shares in crypto exchange Gemini surged after hours as stronger-than-expected fourth-quarter results showed revenue growth driven by credit card adoption and a reworked fee structure.

Gemini reported on Thursday that its Q4 revenues rose 39% from the year-ago quarter to $60.3 million, reportedly beating analyst expectations of $51.7 million.

It reported a net loss of $140.8 million for Q4, deepening from its $27 million loss from a year ago. Gemini posted a total 2025 loss of $585 million, ahead of its total 2024 losses of $156.6 million.

Gemini co-founders Cameron and Tyler Winklevoss said in a shareholder letter that Q4 was the company’s highest quarterly revenue in three years, even with trading volumes declining, the revenue gain was reflective of “deliberate fee structure work through the back half of the year.”

Shares in Gemini (GEMI) initially jumped 14% after hours on Thursday to a high of $6.83, but settled at $6.36 for a gain of 5.8% after ending the trading day flat at around $6.

The results are Gemini’s second after going public in September and came amid a broad crypto market decline in late 2025, which saw Bitcoin (BTC) rapidly decline from its all-time peak above $126,000 in October.

Gemini lays off 30% of staff so far this year

In February, Gemini said it was withdrawing from the UK, the EU and Australia, citing challenging market conditions. The company also planned to lay off 25% of its workforce, in part due to artificial intelligence.

In their letter, Cameron and Tyler Winklevoss said Gemini had reduced its workforce by “roughly 30% since the start of 2026,” citing an increased use of AI.

“Today, AI is used in more than 40% of our production code changes and we expect that number to climb to close to 100% in the not-too-distant future,” they said. “Not using AI at Gemini will soon be the equivalent of showing up to work with a typewriter instead of a laptop.”

The Winklevoss brothers said the company’s plan this year was to “focus and double down on America,” adding they were encouraged by the pro-crypto stance of US market regulators.

Prediction markets and credit card key 2026 priorities

Gemini launched its in-house prediction market, Gemini Predictions, across all 50 US states in December, shortly after it obtained a license from the Commodity Futures Trading Commission.

Related: Gemini bets on ‘super app’ as stock sinks to record low on Q3 results

The company said it would refine and expand its prediction market offering and also scale its credit card and exchange.

The Winklevoss brothers said Gemini would “shift into becoming a markets company with Gemini Predictions” and use that infrastructure for its perpetual futures contracts once they’re approved in the US.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

UK tourists Tenerife emergency amid Storm Therese warning

Three Flight Attendants Hospitalised After LA-Sydney Flight Hits Severe Turbulence

Gemini Sued Over Alleged Deception for Post-IPO Pivot

-

Crypto World6 days ago

HYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech4 days ago

Tech4 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Addict Lip Glow

-

Tech3 days ago

Tech3 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Sports6 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business4 days ago

Business4 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business6 days ago

Business6 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World6 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business4 days ago

Business4 days agoAustralian shares drop as Iran war enters third week

-

Business6 days ago

Business6 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World4 days ago

Crypto World4 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports6 days ago

Sports6 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics2 days ago

Politics2 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion4 days ago

Fashion4 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos2 days ago

News Videos2 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Tech59 minutes ago

Tech59 minutes agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Crypto World2 days ago

Crypto World2 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Crypto World5 days ago

Crypto World5 days agoCrypto Losses Drop 87% in February, But Hackers Are Now Targeting People, Not Code

-

Politics3 days ago

Politics3 days agoReal-time pollution monitoring calls after boy nearly dies

-

NewsBeat1 day ago

NewsBeat1 day agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

You must be logged in to post a comment Login