Crypto World

Nvidia Stock Slides 5% After Strong Q4 Earnings Beat

TLDR

- Nvidia stock fell as much as 5% in early trading on February 26 despite strong fourth quarter results.

- The company reported fiscal Q4 revenue of $68.1 billion, marking a 73% increase year over year.

- Data Center revenue reached $62.3 billion, driven by continued demand for advanced chips.

- Non-GAAP earnings per share rose to $1.62, reflecting an 82% annual increase.

- Gaming and Automotive revenue came in below analyst expectations during the quarter.

Nvidia (NVDA) shares fell in early trading on February 26 despite strong quarterly results. The stock dropped as much as 5% after the company released its fiscal fourth quarter earnings. Traders shifted focus from headline growth to demand durability and capital spending trends.

Nvidia Stock Drops After Earnings Beat

Nvidia stock declined in early market activity even after the company beat revenue and profit estimates. The pullback followed a rally that had priced in strong data center demand. As a result, the earnings report failed to drive further upside momentum.

The company reported total revenue of $68.1 billion for fiscal Q4 2026, rising 73% year over year. Data Center revenue reached $62.3 billion, climbing 75% from the prior year. Non-GAAP earnings per share increased to $1.62, reflecting 82% annual growth.

However, Gaming revenue reached $3.73 billion and fell short of analyst expectations. Automotive revenue totaled $604 million and also missed consensus estimates. Consequently, investors questioned revenue concentration within the data center segment.

Management issued revenue guidance of $78.0 billion, plus or minus 2%, for fiscal Q1 2027. Wall Street had expected about $72.6 billion for the same period. Therefore, the outlook exceeded projections despite the stock decline.

CEO Jensen Huang said, “Demand for Blackwell remains strong across hyperscale customers.” He also confirmed that the company has started shipping samples of the Rubin platform. These updates reinforced continued product development and deployment.

Investors Focus on AI Spending Sustainability

Investors reacted with a sell-the-news move after recent gains in Nvidia stock. In recent weeks, Meta and Amazon signaled higher capital expenditure plans. Those updates had already supported expectations for strong chip demand.

As a result, the earnings beat did not materially alter the broader outlook. Traders shifted attention toward long-term returns on infrastructure investments. They questioned whether enterprise monetization would match hardware spending levels.

The data center division accounted for most of the company’s revenue growth. That concentration raised questions about balance across segments. Gaming and automotive performance failed to match the strength of data center sales.

Gross margin expanded to 75.2%, improving by 1.7% points year over year. The margin gain reflected pricing strength and product mix. However, supply constraints in memory components continued to affect certain segments.

- Bitcoin stalls near $67,000 after partial recovery from all-time highs.

- On-chain data shows half of BTC is held at a loss, hinting at market fatigue.

- Analyst warns deeper correction possible, with bottom around $45,000.

Bitcoin’s recent recovery attempt has stalled just below $70,000, with the cryptocurrency slipping back to around $67,250 at press time.

The drop comes as the broader crypto market struggles to maintain upward momentum following a few months of volatility.

After reaching an all-time high of $126,080 in October 2025, Bitcoin (BTC) has now retraced nearly half of its value.

All eyes are now on the cryptocurrency as it appears to consolidate around $67,000 after the steep drawdown.

Analyst Willy Woo warns of further downside

Renowned on-chain analyst Willy Woo has predicted a significant price correction following the recent bounce.

He estimates that the bear market bottom could be around $45,000, with more extreme scenarios potentially testing $30,000 or even lower.

Woo’s caution stems from declining liquidity across spot and derivatives markets, which historically reduces the strength of rallies.

He suggests that Bitcoin may briefly climb to the mid-$70,000 range before facing renewed downward pressure.

On-chain signals hint at market fatigue

On-chain metrics suggest that Bitcoin may be entering the later stages of a bear market cycle rather than the early phase.

Roughly half of all circulating BTC, nearly 9.2 million coins, are currently held at a loss, according to the latest weekly report by on-chain analytics firm Glassnode.

Historically, such levels indicate significant selling pressure and potential capitulation, yet the pace of accumulation by long-term holders hints at a market beginning to stabilise.

Some analysts view these patterns as signs that bitcoin’s price may be closer to a bottom than the start of a prolonged decline.

The balance between holders in profit and those in loss is an important measure of market sentiment, and it shows that while short-term volatility remains high, there is underlying support at current levels.

Bitcoin ETF inflows show cautious optimism

Institutional investors have recently stepped back into the market, with Bitcoin ETFs recording over $1 billion in net inflows over a few days.

This trend follows a period of withdrawals totalling nearly $3 billion, signalling that some investors see the current price as a buying opportunity.

Spot ETFs, in particular, are attracting attention from long-term investors looking for regulated exposure to Bitcoin.

The renewed interest demonstrates that, despite the pullback from all-time highs, there is confidence in the asset’s long-term prospects.

However, inflows are not a guarantee of sustained upward momentum.

Short-term technical indicators suggest that Bitcoin is trading near the top of a tight consolidation range between $67,000 and $68,000, and a breakout above this zone could spark a rally, although rejection may force the price back toward $63,000 or lower.

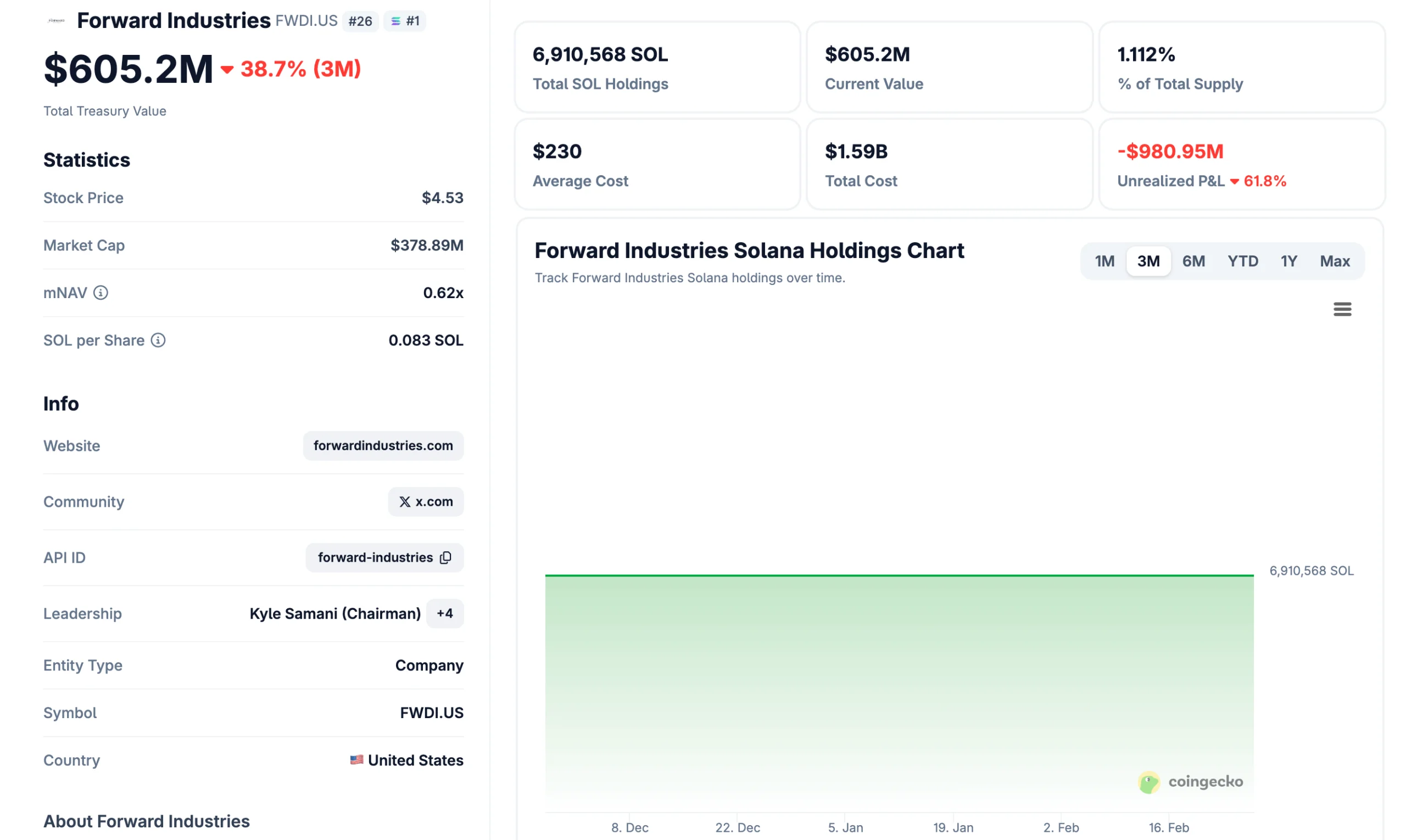

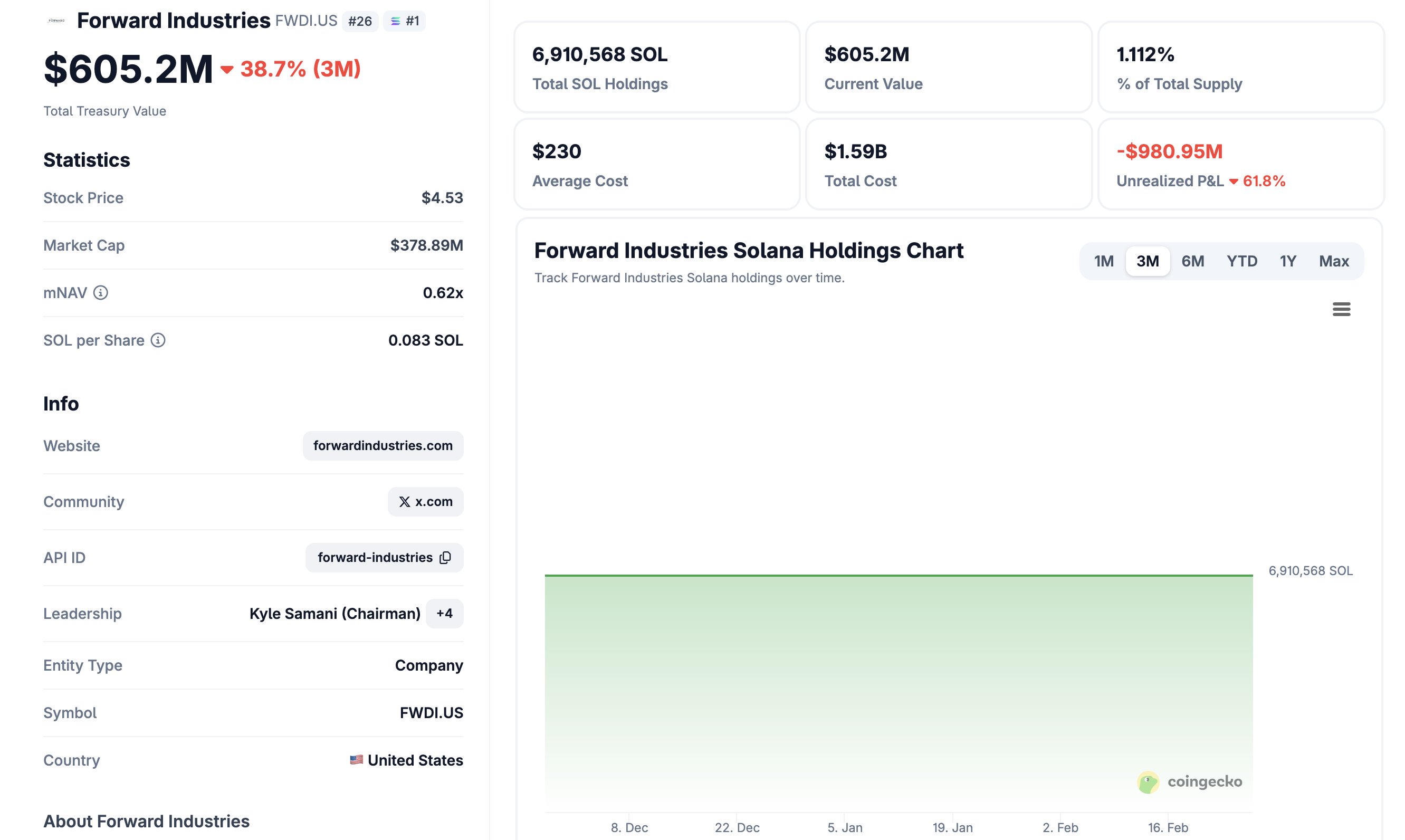

Forward Industries’ CIO says the company aims to become the “Berkshire Hathaway of the Solana ecosystem,” even as its treasury approaches $1 billion in unrealized losses.

The statement comes as SOL has declined nearly 30% year-to-date, a drop that is impacting balance sheets across major Solana-focused digital asset treasury (DAT) firms.

Solana’s Price Decline Deepens Institutional Pain

Forward Industries is the largest institutional holder of Solana. The company began accumulating SOL in September 2025 after raising approximately $1.65 billion through a private investment in public equity (PIPE), backed by Galaxy Digital, Jump Crypto, and Multicoin Capital.

According to the latest data from CoinGecko, it holds over 6.9 million SOL. The firm acquired its position at an average price of around $230 per token, implying a total cost basis of roughly $1.59 billion.

Follow us on X to get the latest news as it happens

With the altcoin trading near $87, the company’s stake is now worth approximately $605.2 million. That represents an unrealized loss of nearly $1 billion, or roughly 62% from its average entry price.

Furthermore, FWDI shares have fallen from over $39 to roughly $5 since the company started buying SOL. According to Google Finance data, the stock price declined by 31.47% in 2026 alone.

Despite the drawdown, the firm’s conviction remains strong. Company leadership has outlined an ambitious long-term vision that transcends short-term volatility.

“Our longer-term aspiration is to be the Berkshire Hathaway of the Solana ecosystem. We believe Solana is best positioned as the blockchain for the future of internet capital markets,” Forward Industries’ CIO Ryan Navi said.

According to CoinGecko treasury data, Forward Industries is not alone. Firms like DeFi Development Corp, Upexi, and Sharps Technology are also sitting on significant unrealized losses as Solana’s price continues to slide.

The losses extend well beyond Solana-focused firms. Bitmine’s Ethereum (ETH) holdings have produced unrealized losses exceeding $7 billion. Meanwhile, Strategy’s Bitcoin (BTC) position carries paper losses of roughly $5 billion, according to Saylortracker data.

The broader DAT model, in which publicly listed companies hold crypto assets as their primary balance sheet instrument, is showing its vulnerabilities as a synchronized market decline compresses asset values while equity investors reprice risk.

Solana Launches “Solana Payments” Amid Ecosystem Momentum

Despite price struggles, ecosystem developments have continued. Yesterday, the team introduced Solana Payments, a new initiative to accelerate on-chain payment adoption.

According to the network, major players, including Visa, PayPal, Stripe, Western Union, and Fiserv, are running live products on the network, not just pilots. It also stated that the network has processed over 480 billion transactions and facilitates approximately $2 trillion in stablecoin transfers per quarter.

“Payments.org has everything you need to start building: Live payment simulator. Developer docs. Case studies from the biggest names in finance,” the post read.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

Thus, while ecosystem development continues and institutional narratives remain ambitious, prolonged price weakness is testing balance sheets and investor confidence alike. Forward Industries’ bet on SOL’s long-term value may yet prove correct, but the timeline and the market’s patience for it remain open questions.

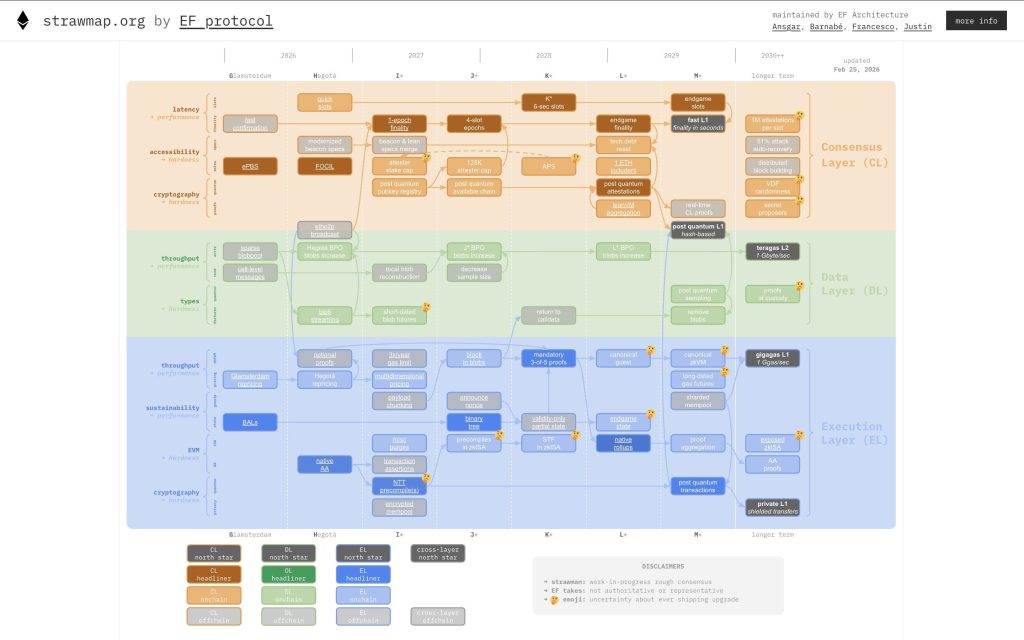

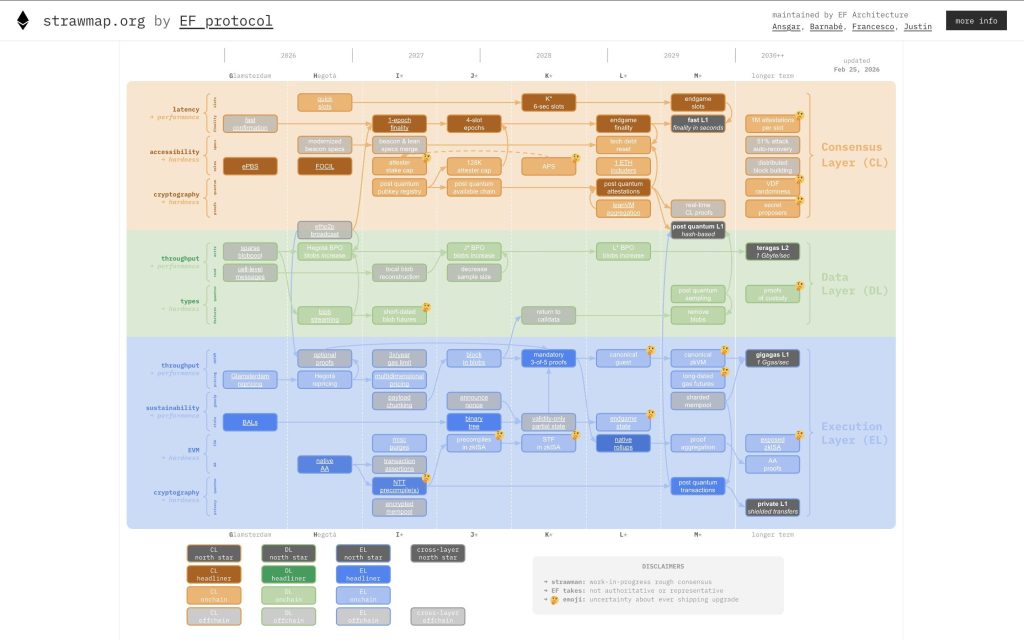

Ethereum just put a timestamp on its ambition, and the new roadmap could shape its price valuation. The Foundation’s new “Strawmap” (roadmap) targets a high-throughput settlement layer by 2029, cutting finality from around 16 minutes to seconds and aiming for 1 gigagas per second directly on Layer 1.

Instead of leaning almost entirely on Layer-2s for speed, Ethereum wants the base layer itself to become faster, tougher, and globally competitive with traditional financial rails.

Key Takeaways

- The Target: The roadmap aims for 10,000 TPS (1 gigagas/s) on Layer 1 and up to 10 million TPS on Layer 2 via data availability sampling.

- The Shift: Introduction of “Minimmit” single-slot finality intends to reduce transaction irreversible time from roughly 16 minutes to 6–16 seconds.

- The Timeline: Developers are planning seven hard forks on a six-month cycle through 2029 to implement these changes incrementally.

The Strawmap or Ethereum Roadmap: 10,000 TPS and Instant Finality

The big number is 10,000 TPS on Layer 1.

The Strawmap targets roughly 1 gigagas per second using zkEVMs and real-time proving. Today, transactions are included quickly but take around 16 minutes to reach finality. The new goal is 6 to 16 seconds, which is critical for serious financial use.

To get there, Ethereum plans up to seven hard forks through 2029. Slot times would gradually fall from 12 seconds to 8, and eventually toward near single-second blocks. That delays any push toward full “ossification” and prioritizes performance.

Vitalik has acknowledged that earlier assumptions about relying almost entirely on L2s need revision. If rollups are expected to process millions of TPS, the base layer must handle far more load itself.

For institutions, the message is clear. Ethereum wants to become a settlement infrastructure capable of supporting heavy, real-world financial flows without congestion.

Ethereum Roadmap: L1 Velocity vs. L2 Scale

For years, the message was simple: scale on Layer 2. The Strawmap adjusts that stance. Scale on L2, but make Layer 1 fast enough so it does not become the bottleneck. Ethereum is reacting to competitive pressure.

Vitalik has acknowledged that earlier assumptions about L2 reliance need updating. If rollups are expected to process millions of TPS, the base layer must comfortably handle around 10,000 TPS. Faster finality also matters for emerging AI-driven use cases, where agents require near-instant settlement to execute complex on-chain strategies.

The proposed shift toward techniques like erasure coding signals a deeper focus on data propagation and network efficiency. If successful, Ethereum strengthens its position as a high-speed settlement layer. If not, it risks ceding performance perception to faster, more centralized alternatives.

Ethereum Price Analysis: The Path to 2029 Valuation

The market reacted fast, with ETH whipping around the $2,060 area after the roadmap dropped. Long term, the plan gives investors a structural anchor. It signals Ethereum does not intend to fall behind faster monolithic chains.

Technically, Ethereum price is compressing. $2,150 is the key resistance. A clean break there opens the path toward $2,400. On the downside, $2,000 is the short-term pivot, and $1,920 to $1,800 is the structural support zone if sentiment turns.

Execution risk matters. If slot-time reductions and early upgrades slip past late 2026, the market could reprice lower. The move toward erasure coding shows the Foundation is tackling core data bottlenecks. If it works, Ethereum strengthens its case as a high-speed settlement infrastructure. If not, it risks being overshadowed by faster alternatives.

For now, holding $2,000 keeps the bullish structure alive. Losing $1,920 would weaken the setup until a new catalyst appears.

Discover: Here are the crypto likely to explode!

The post Ethereum 2029 Roadmap: ETH to Become the High-Speed Internet of Value appeared first on Cryptonews.

Earnings season is wrapping up with a mixed bag of results across crypto miners, AI infrastructure plays and fintech names, including MARA Holdings (MARA), TerraWulf (WULF), CoreWeave (CRWV) and Block (XYZ).

Bitcoin has remained relatively flat around $67,000 during Asia and European hours, with limited movement spilling over into other crypto related equities.

MARA Holdings jumped 16% to $9.80 after striking a deal with Starwood Capital to convert select bitcoin mining facilities into AI focused data centers. The partners expect to deliver about 1 gigawatt of capacity in the near term, with plans to scale beyond 2.5 gigawatts.

The pivot reflects a broader shift among miners looking to monetize power access as AI compute demand surges, following Bitfarms (BITF) and Cipher Digital (CIFR) amongst others.

TerraWulf is trading 3.5% lower at $17 after its Q4 print, with revenue down due to lower bitcoin production and transitional GAAP optics.

However, executives emphasized that the key story is the ramp in contracted high performance computing revenue. The company has expanded from one site a year ago to five today and expects about 2.9 gigawatts of gross capacity by year end, according to head of digital assets VanEck, Matthew Sigel.

CoreWeave shares are down 12% despite revenue of $1.57 billion, beating expectations of $1.53 billion. The company reported weaker than forecasted Q1 revenue guidance, in addition to an increase in capital expenditure, which raised concerns about profitability and cash burn. EPS came in at -$0.89 versus -$0.68 expected, a 31% miss.

Block is up 20% after announcing it will cut more than 40% of its workforce, reducing headcount to about 6,000. While management pointed to AI driven efficiencies, investors are also weighing longer term margin pressure from stablecoin based payment rails.

The company guided Q1 operating income to $600M versus $574M expected, forecast Q1 gross profit of $2.8B versus $2.72B consensus and raised full year gross profit, according to Sigel.

TLDR

- BofA increased Caterpillar’s price target from $735 to $825, maintaining its Buy recommendation following impressive 2025 financial results.

- The industrial giant delivered $67.6 billion in annual revenue with 4% growth, while its Power & Energy division jumped 23% to $9.4 billion.

- CNBC’s Jim Cramer expressed support for CAT’s turbine business but suggested Cummins (CMI) offers better value at current levels.

- February saw short positions increase by approximately 61%, while company insiders offloaded more than $98 million in shares during the last quarter.

- Trading at roughly 40 times earnings after a 124% annual surge, CAT faces a consensus analyst price target of $712.52 with a “Moderate Buy” average recommendation.

Caterpillar (CAT) has experienced an impressive rally. Shares have climbed 124% during the past year and gained 28% since the beginning of 2025, starting Friday’s session at $752.81.

Following the release of Caterpillar’s full-year 2025 financial results, Bank of America wasted no time adjusting its outlook. The investment bank elevated its price objective on CAT from $735 to $825 while reaffirming its Buy recommendation.

BofA’s analysis was clear-cut. Caterpillar is experiencing turbine demand from multiple sectors extending far beyond data center applications, which the firm believes undermines concerns about potential turbine oversupply in the market.

The financial performance supported this thesis. Caterpillar generated $67.6 billion in total revenue throughout 2025, representing a 4% year-over-year improvement. The Power & Energy division emerged as the star performer, expanding 23% to achieve $9.4 billion in sales.

Fourth-quarter performance was equally impressive. The company delivered earnings per share of $5.16 for the period, surpassing the analyst consensus of $4.67. Revenue reached $19.13 billion, significantly exceeding projections of $17.81 billion. This represented a 17.9% increase compared to the corresponding quarter one year prior.

Jim Cramer recently shared his thoughts on CAT, stating plainly, “We like their stuff.” He highlighted turbines and power equipment as the foundation of the optimistic investment thesis.

However, Cramer also expressed some reservation. When a club member inquired in January about entering a position, he noted the stock had already experienced a substantial appreciation and said he’d prefer to see a pullback before adding exposure. He indicated he currently finds Cummins (CMI) more attractive than CAT at present valuations.

Cramer also offered criticism regarding retail investor participation, suggesting that Caterpillar’s leadership team should be working harder to engage individual investors — and questioning why an iconic American corporation trades at $749.

Analyst Ratings Split

The overall analyst community remains divided. CAT currently has sixteen Buy ratings, seven Hold ratings, and one Sell rating. The average price target stands at $712.52, which actually falls below the stock’s current trading level.

Wells Fargo pushed its target to $870 alongside an Overweight rating. Daiwa elevated its projection to $790. Jefferies established a $750 target with a Buy recommendation. Oppenheimer moved to $729 with an Outperform rating. Morgan Stanley, however, only increased its target to $425 while maintaining an Underweight stance.

Wall Street Zen downgraded CAT from Buy to Hold on February 21st.

Insider Selling and Short Interest

Not all market participants are bullish. Executive Denise C. Johnson divested 39,138 shares on February 2nd at an average price of $681.08, totaling more than $26.6 million. This transaction represented a 47% reduction in her stake.

Insider Bob De Lange executed his own sale on February 6th, offloading 22,656 shares at $720.11 for approximately $16.3 million. Throughout the past 90 days, company insiders have collectively sold $98.2 million worth of shares.

Short interest also surged roughly 61% during February, indicating that some market participants are positioning for a decline.

Institutional investors control 70.98% of CAT’s outstanding shares. Erste Asset Management expanded its stake by 32.7% in Q3, purchasing 33,634 shares. Norges Bank established a new position valued at more than $2.1 billion in Q2.

CAT’s 52-week trading range extends from $267.30 to $789.81. The stock currently trades at a P/E ratio of 40 with a market capitalization of $350.27 billion. The upcoming quarterly dividend is $1.51 per share, translating to an annualized distribution of $6.04 and a yield of 0.8%.

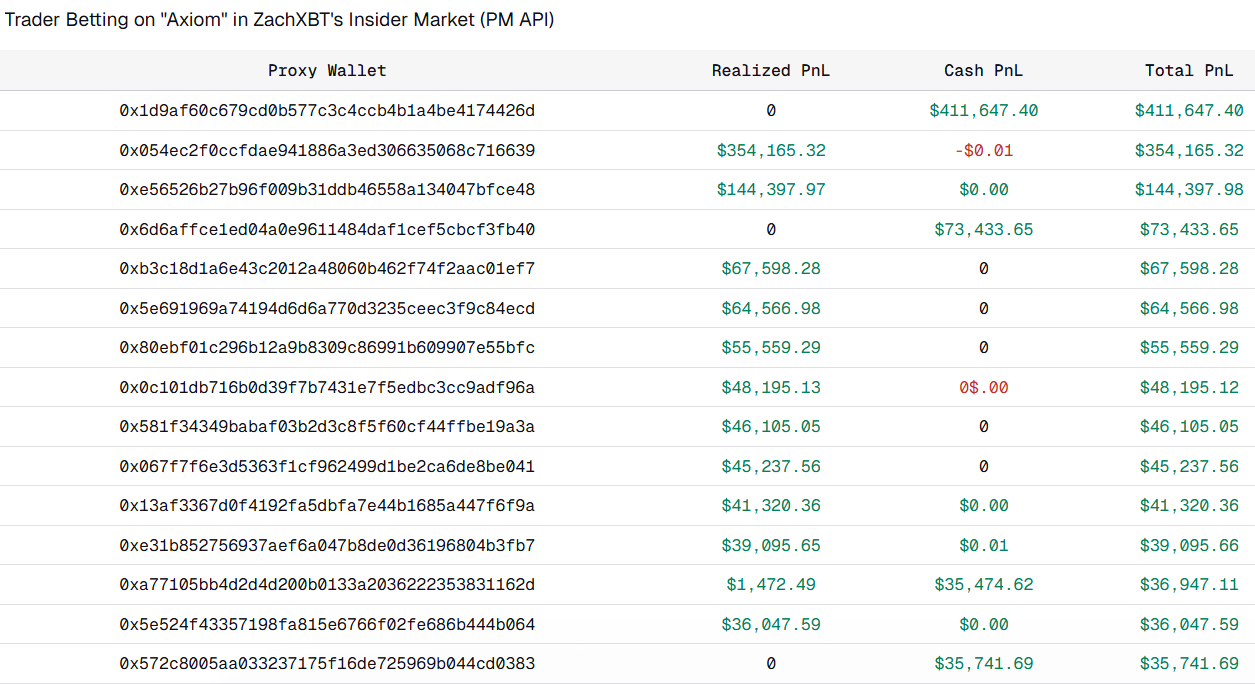

A small group of crypto wallets won more than $1.2 million betting on a Polymarket contract tied to an onchain investigation into decentralized finance (DeFi) trading platform Axiom, fueling fresh concerns that prediction markets can reward people with advance knowledge of market-moving disclosures.

The eight most profitable wallets on the market collectively made about $1.2 million, according to trading data compiled on Dune. The same dataset showed more than 50 wallets posting combined losses of roughly $1.23 million, while two wallets lost about $366,000.

Eight out of the top 10 wallets are likely insider addresses, judging by their onchain transaction patterns, according to onchain researcher Defioasis. “There are 3 addresses that achieved profits exceeding $100,000, all of which are insider addresses that traded only this single market,” said the researcher in a Friday X post.

ZachXBT released the much-anticipated investigation on Thursday, alleging that Axiom employee Broox Bauer and others had been responsible for insider trading activity since early 2025.

In an X response to the incident, Axiom said it was “shocked and disappointed” in the news and that it had removed access to the tools that were used in the alleged insider trading.

Related: Analysts reject Jane Street ‘10 a.m. dump’ claims, say Bitcoin isn’t easily manipulated

Prediction markets raise insider trading allegations

Insider trading concerns in prediction markets mounted in early January after a highly profitable bet on the removal of Venezuelan President Nicholas Maduro by the US raised eyebrows.

On Jan. 3, a Polymarket account placed a bet on a contract predicting that Maduro would be removed from office just hours before US forces captured him in a military operation, netting the user about $400,000 in profit.

US lawmakers have since proposed legislation aimed at restricting political prediction market trading by government officials, adding to the regulatory spotlight on the sector.

Related: Solo Bitcoin miner bags over $200K block reward using rented hashrate

Polymarket faces growing regulatory scrutiny on gambling concerns

Polymarket, the largest decentralized prediction market, has faced mounting regulatory pressure in several countries where authorities have argued that the platform offers unlicensed gambling.

Hungary and Portugal blocked access to the platform in January, citing concerns related to forbidden gambling activities.

A week earlier, Ukraine blocked Polymarket, classifying its activities as unlicensed gambling under national law.

Polymarket has also been restricted or blocked in several other countries over gambling concerns, including France, Belgium, Poland, Singapore and Switzerland.

Magazine: Inside a 30,000 phone bot farm stealing crypto airdrops from real users

Matt Hougan dismissed claims that Jane Street is orchestrating Bitcoin’s recent decline, calling the downturn “a classic crypto winter.”

Matt Hougan, chief investment officer at Bitwise, has pushed back on claims that trading firm Jane Street is behind Bitcoin’s recent slide, writing on X on February 26 that the downturn is “a classic crypto winter,” not a coordinated attack.

His comments come as lawsuits and viral threads revive old fears about market manipulation just as Bitcoin is trading over 46% below its all-time high.

Conspiracy Claims Collide With ETF Mechanics

Speculation intensified after reports emerged that Terraform Labs’ bankruptcy administrator had sued Jane Street in a Manhattan federal court, accusing the firm of using insider information before the May 2022 Terra-Luna collapse.

According to the complaint, Jane Street withdrew 85 million TerraUSD from Curve’s 3pool minutes after Terraform removed 150 million UST, a sequence the suit claims accelerated the $40 billion collapse. Jane Street has denied the allegations, calling the case a “desperate attempt” to recover losses and blaming Terraform’s management for the failure.

At the same time, some crypto analysts, including Bull Theory, alleged that Jane Street runs a “10 AM” sell algorithm to push Bitcoin lower and profit from derivatives.

Bull Theory also pointed to an interim order from India’s Securities and Exchange Board accusing Jane Street entities of expiry-day index manipulation between January 2023 and March 2025, alleging thousands of crores in unlawful gains. The case is ongoing, and the firm has appealed.

However, Hougan dismissed the narrative as misplaced. “The conspiracy theories are wild,” he wrote, arguing that Bitcoin is down because investors unwound long positions, reduced leverage, and rotated capital elsewhere.

You may also like:

The Bitwise CIO also amplified colleague André Dragosch’s analysis of intraday Bitcoin performance since the ETF launch in January 2024. Dragosch’s data countered the viral 10 AM slam narrative by showing pronounced weakness around midnight ET, pointing to non-U.S. trading hours as the actual vulnerability period.

Macro strategist Alex Krüger also echoed Hougan’s skepticism, calling the Jane Street theory “yet another viral and flawed conspiracy theory.” He noted that basis traders and authorized participants (APs) simply close gaps between ETFs, futures, and spot markets.

“Too many doomer narratives and conspiracy theories looking for villains circulating right now,” Krüger posted. “Historically, that’s the kind of sentiment you see at bottoms.”

Structural Questions Linger Beyond the Blame

The controversy has also revived debate about ETF plumbing. ProCap CIO Jeff Park wrote on February 25 that concerns are less about a single firm and more about how APs operate under regulatory exemptions that allow in-kind creations and redemptions.

In theory, APs can hedge ETF exposure with futures instead of buying spot Bitcoin directly, which critics argue could dull spot demand.

None of the lawsuits or regulatory filings so far establish coordinated misconduct in Bitcoin markets. Still, the overlap between large quantitative firms, derivatives strategies, and ETF mechanics has fueled suspicion during a downturn.

For Hougan, the explanation is simpler. Bitcoin’s four-year cycle, leverage resets, and shifting investor priorities are enough to explain the pullback.

“This is a classic crypto winter and there will be a classic crypto spring,” he wrote. “People want someone to blame — I get it — but the reality is far more boring than that.”

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

AllUnity, a joint venture between DWS, Galaxy, and Flow Traders, has expanded its stablecoin lineup with a new token pegged to the Swiss franc, which has emerged as a haven darling for major banks and analysts.

The BaFin-regulated e-money institute has unveiled CHFAU, which is backed 1:1 by Swiss franc reserves, in response to institutional demand for regulated digital CHF for payments, settlements, and treasury operations.

It debuts on the Ethereum blockchain as an ERC-20 token, with plans to expand to other networks later this year.

“In response to strong demand for a compliant digital Swiss Franc, we progressed from concept to launch in a matter of months, demonstrating the strength and scalability of AllUnity’s multicurrency platform,” Alexander Höptner, CEO of AllUnity, said in a press release shared with CoinDesk.

“This milestone is just the start of a broader transformation in how global liquidity moves,” said.

The debut is a sign of growing investor demand for stablecoins pegged to fiat currencies beyond the U.S. dollar. Last year, AllUnity debuted the EUR-stablecoin, while several other firms have issued tokens pegged to other fiat currencies such as JPY.

The debut signals surging demand for stablecoins pegged to fiat currencies beyond the dollar. Last year, AllUnity launched its EUR-pegged token, joining others that have issued JPY-tied alternatives. The stablecoin market has exploded since 2020, hitting $310 billion in combined value, with dollar-pegged tokens in pole position.

Safe haven CHF

Prospects for CHF-linked assets look bright as the currency is gaining notoriety as a better haven currency than the widely popular Japanese yen.

A safe haven currency is a stable, liquid currency that investors seek to hold during periods of economic uncertainty, political turmoil, or market volatility to protect their capital.

“If you’re a fiscal basket case, markets weaken your currency and push up government bond yields. Japan and Switzerland are polar opposites: Japan is a basket case, Switzerland is a massive safe haven,” Economist Robin Brooks said on X, echoing what Bannockburn Global Forex’s Chief Market Strategist Marc Chandler told CoinDesk last year.

Investment banking giant Morgan Stanley has compared the Swiss franc to gold, calling for a 17% appreciation against the U.S. dollar.

“CHF is an overlooked, under appreciated asset safe haven asset that looks set to appreciate more substantially and speedily than investors think and markets anticipate,” the bank said this week.

Goldman and Bank of America revealed a bias for franc over yen as haven currency in September last year.

Ethereum is preparing for a future where quantum computers could break much of today’s internet cryptography, as co-founder Vitalik Buterin outlined a step-by-step “quantum resistance roadmap” targeting the network’s most vulnerable components.

Summary

- Vitalik Buterin outlined a quantum resistance roadmap targeting Ethereum’s consensus signatures, data availability, wallet cryptography, and ZK proofs.

- The plan proposes replacing vulnerable BLS and ECDSA systems with hash-based or lattice-based quantum-resistant alternatives, supported by recursive STARK aggregation.

- While large-scale quantum attacks remain theoretical, Ethereum is proactively engineering long-term defenses to future-proof the network.

Ethereum braces for quantum future as Vitalik Buterin unveils sweeping resistance roadmap

In a detailed post, Buterin identified four key areas exposed to quantum attacks: consensus-layer BLS signatures, data availability mechanisms relying on KZG commitments, externally owned account (EOA) signatures using ECDSA, and application-layer zero-knowledge proofs such as Groth16.

Powerful quantum machines, if realized at scale, could theoretically crack ECDSA and similar elliptic curve systems using Shor’s algorithm, potentially allowing attackers to forge signatures and compromise wallets.

To address this, Ethereum’s roadmap proposes gradually replacing vulnerable cryptography with quantum-resistant alternatives. At the consensus layer, hash-based signatures and STARK-based aggregation could replace BLS signatures.

For EOAs, Buterin points to native account abstraction under EIP-8141, allowing wallets to adopt post-quantum signature schemes once efficient implementations are available.

The shift, however, comes with tradeoffs. Quantum-resistant signatures are significantly larger and more computationally expensive than current standards. Buterin suggests protocol-level recursive proof aggregation as a long-term fix, enabling multiple signatures or proofs to be compressed into a single STARK verification, potentially preventing massive increases in on-chain gas costs.

Ethereum’s data availability stack may also migrate from KZG commitments toward STARK-based constructions, though this would require substantial engineering work.

While large-scale quantum computers capable of breaking modern cryptography may still be years away, Ethereum’s proactive planning signals an effort to future-proof the network. The roadmap does not represent an immediate upgrade, but rather a phased transition designed to ensure Ethereum remains secure in a post-quantum world.

Where is XRP heading next? Here are some of the recent predictions and analyses.

Ripple’s cross-border token has often been the object of some wild price predictions, many of which might sound absurd at the time being. However, its infamous volatility has proved that it can produce massive gains (or drop violently) in the span of just weeks and months.

In this article, we will review some of the latest bull and bear cases, one of which was even called precision and not ‘hopium.’

XRP’s Bull Predictions

We will begin with the more ‘modest’ forecast coming from perma-XRP bull John Squire. In a recent post, he outlined some rumors that Ripple’s US national bank license is set for approval. Without providing any further details on the matter, he added that such a “major step for crypto adoption and institutional finance” can instantly send the underlying token to $5.

EGRAG CRYPTO, an analyst also known for their pro-XRP calls, relied on technical analysis to determine the asset’s next targets. They indicated that the long-term XRP chart shows a 814% surge during the first Elliott Wave, which transpired between 2015 and 2018. The subsequent corrective wave 2 took the asset south by over 70% to under $0.12 during the 2020-2022 bear market.

The analyst believes XRP is approaching the third wave, but it still needs to confirm it by reclaiming the wave 1 high of over $3.40 with a strong “weekly close and momentum expansion.” Until that happens, the asset is “still corrective.”

If it does, though, the sky would be the limit for the cross-border token, with EGRAG indicating a massive price target of somewhere between $15 and $31 during wave 3.

#XRP – Elliott Wave Reality Check (W3🟰$15-$31):

Let’s be precise. No hopium.

✔️ Wave 1⃣:

The ~814% expansion fits a textbook impulsive Wave 1. Strong momentum, clean channel respect.✔️ Wave 2⃣(Now):

The current pullback sits perfectly within normal Wave 2 retracements… pic.twitter.com/iK4eEV0zSR— EGRAG CRYPTO (@egragcrypto) February 26, 2026

You may also like:

Or, Below $1?

In the opposite corner stands Ali Martinez, who, instead of going with the hype and predicting some mind-blowing bull targets, outlined XRP’s most significant support levels in case another correction is to take place. The token has plunged by over 60% since its July 2025 all-time high, and currently struggles to remain above $1.40.

He noted that Ripple’s token could find some support “along the triangle’s hypotenuse between $0.90 and $0.60” if it loses the coveted $1.00 defense level. Recall that XRP dipped to $1.11 on February 6 when the entire market collapsed, but has remained above that line since then.

$XRP could find support along the triangle’s hypotenuse between $0.90 and $0.60. pic.twitter.com/F04KWLknux

— Ali Charts (@alicharts) February 26, 2026

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Face of ketamine-addicted driver who killed biker in horror crash

How Newly Released Documents Reveal JPMorgan Bankers’ Ongoing Ties to Jeffrey Epstein

Bitcoin price recovery falters, drops to $67k as popular analyst predicts major crash

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics11 hours ago

Politics11 hours agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business5 days ago

Business5 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

NewsBeat1 day ago

NewsBeat1 day agoCuba says its forces have killed four on US-registered speedboat | World News

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics5 days ago

Politics5 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Business1 day ago

Business1 day agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Crypto World3 days ago

Crypto World3 days agoEntering new markets without increasing payment costs

-

Business14 hours ago

Business14 hours agoOnly 4% of women globally reside in countries that offer almost complete legal equality