Crypto World

Opt-in privacy is failing crypto

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Privacy has been a recurring narrative in crypto for years. Just weeks after Bitcoin (BTC) launched, Hal Finney pointed out the problem in only his second tweet about it, but the concept didn’t gain wider traction until Monero (XMR) arrived in 2014. Since then, privacy has repeatedly re-emerged as a core promise of decentralised money, especially during moments of regulatory pressure or heightened concerns around financial surveillance.

Summary

- Opt-in privacy fractures networks: When users must “turn on” privacy, anonymity sets shrink and private transactions become more conspicuous — not less.

- Design, not demand, is the problem: Zcash’s advanced cryptography exists, yet most transactions remain transparent. Narrative momentum hasn’t translated into usage.

- Privacy must be the default to work: Like security, financial privacy only strengthens when everyone shares it — automatic, universal, and baked into the protocol.

Analysts are positive that crypto’s future will continue to be defined by the privacy narrative. Investor Balaji Srinivasan argued privacy will define the industry’s following eight years; meanwhile, a16z crypto said privacy will be the industry’s most important “moat” in 2026. Indeed, privacy coins have rallied at the end of 2025 and continue to fluctuate into the start of the new year. At their peak, the sector reached a combined market capitalisation surpassing $40 billion, before falling back to roughly $17 billion.

Zcash (ZEC) was a key driver of that resurgence, rising by more than 1,300% from late September 2025 to its all-time high and remaining up over 600% at current prices, briefly overtaking Monero by total market volume. Yet despite renewed interest and price momentum, actual privacy usage remains strikingly low. Zcash’s shielded pool continues to hold just above 30% of the circulating supply, while roughly two-thirds of transactions remain fully visible on-chain.

This disconnect exposes a deeper issue. If interest in privacy is rising, why are users not migrating into the very privacy layers designed for that purpose? The answer could just be structural: opt-in privacy is failing crypto.

Opt-in privacy was a design compromise

In 2013, the pseudonym Nicolas van Saberhagen published the CryptoNote v2 paper, which explicitly framed transaction privacy not as a “nice to have,” but as a core requirement of electronic cash. This paper argued that Bitcoin’s transparency made it pseudo-anonymous at best, and outlined two properties a truly private payment system should satisfy: untraceability and unlinkability. Andrey Sabelnikov, now co-founder of Zano, worked alongside Nicolas to bring this vision to life, implementing the protocol he had designed. From the start, CryptoNote made privacy the default, baked into every transaction rather than offered as an afterthought.

But as the industry evolved, many projects lost sight of this principle. Rather than pushing the boundaries of privacy-preserving technology, they took the path of least resistance, prioritizing compatibility, performance, and mainstream appeal over user protection. Privacy-preserving cryptography was still expensive and unfamiliar, so newer designs retreated to opt-in models.

This compromise had serious consequences. Privacy became a feature to be toggled on rather than a baseline guarantee. Users who chose the private option effectively marked themselves as having something to hide, while the default transparent experience left the majority exposed. This trade-off may have seemed pragmatic at the time, but it fundamentally betrayed the original vision that CryptoNote had established: that true electronic cash must protect user privacy by design and wasn’t something to bolt on later; it had to be designed into the core transaction model itself.

The biggest network carrying the original default-privacy philosophy is Monero. Launched in 2014, it adopted the CryptoNote protocol, preserving the principles that Nicolas and Andrey had already established. Instead of asking users to choose between public and private modes, the design assumes that financial transactions should be private by default, and that privacy improves when everyone shares the same protections.

Through this philosophy, privacy does not just become a feature, but a network effect. A privacy system is only as strong as the crowd it can hide in. When privacy is optional, the network fractures into transparent and private activity. The private pool becomes smaller, the anonymity set shrinks, and the privacy model weakens in practice, regardless of how sophisticated the cryptography may be.

The Zcash paradox

Zcash illustrates the central contradiction facing much of today’s privacy ecosystem. On paper, it offers some of the most advanced privacy technology in crypto, including zero-knowledge proofs that can fully shield transaction details. In practice, however, the majority of network activity remains transparent.

Despite renewed market interest and strong price performance, Zcash’s shielded pool continues to hold just above 30% of the circulating supply, while roughly two-thirds of transactions remain fully visible on-chain. The technology exists. The privacy guarantees are real. Yet most users do not use them.

This gap is not a failure of cryptography, nor a lack of demand for privacy. It is the predictable outcome of opt-in design. When privacy is presented as a separate mode, something users must consciously enable, it introduces friction, uncertainty, and behavioural drop-off. Many users default to transparent transactions simply because they are easier, faster, or more familiar. Others may be unaware of the distinction altogether.

The consequence is a fragmented network. Public and private transactions coexist, but they do not reinforce one another. Instead, the private pool remains small, limiting the size of the anonymity set and weakening privacy guarantees for those who do opt in. Ironically, using privacy in an opt-in system can make a user more conspicuous rather than less.

Privacy can only work when it is the default

Privacy is not a behaviour users reliably opt into. It functions as a collective property. The more participants who share the same privacy guarantees, the stronger those guarantees become. When privacy is optional, networks fracture into public and private activity, shrinking anonymity sets and weakening protection for those who do opt in. In practice, optional privacy often makes users more conspicuous, not less.

The repeated cycles of privacy coin interest show that demand is not the problem; design is. Systems that rely on users to actively choose privacy struggle to translate narrative momentum into real adoption. If privacy is to become crypto’s defining moat, it must be treated as foundational infrastructure, not a feature toggle. Financial privacy works best when it is automatic, universal, and secure by default.

Key takeaways:

-

Private credit risks and weak US jobs market data drive Bitcoin lower, but is there a silver lining?

-

Institutional Bitcoin ETF outflows and miner sales test BTC’s strength, but the Federal Reserve’s options for addressing the federal deficit may also favor scarce assets.

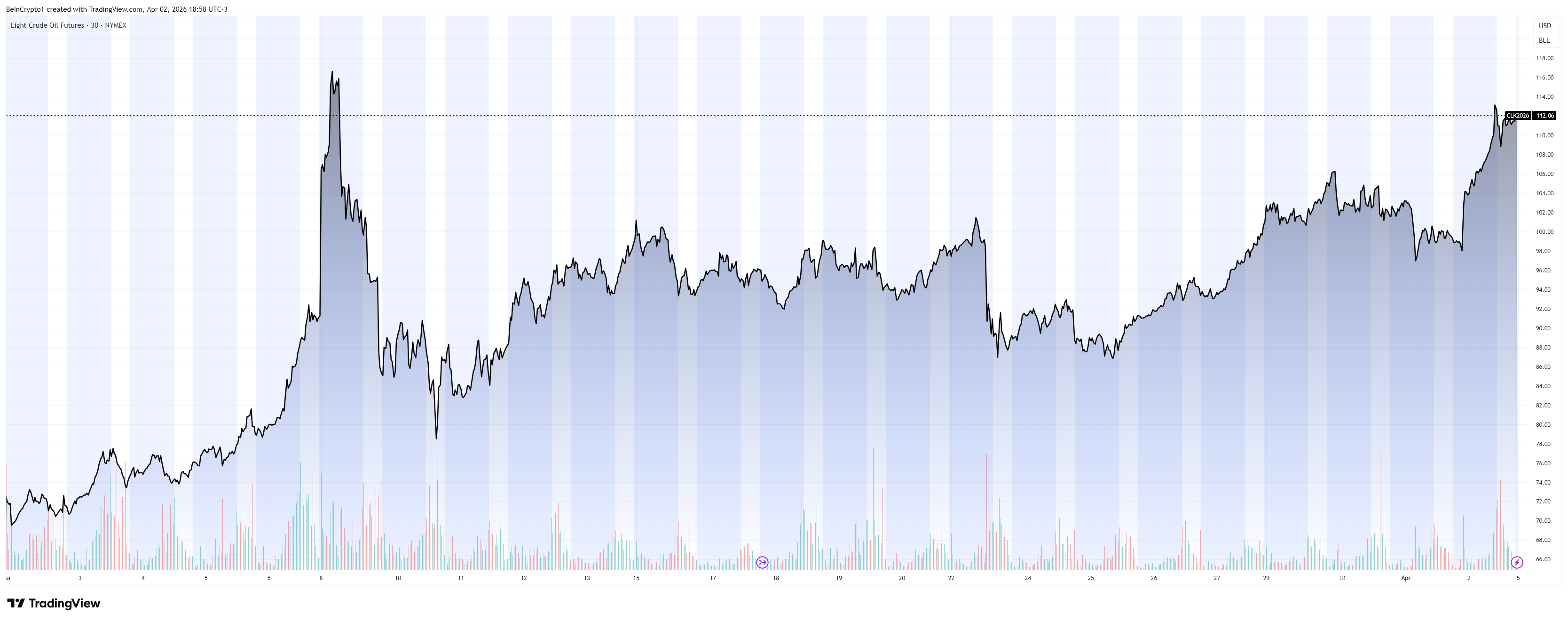

Bitcoin (BTC) faced rejection at $69,000 on Wednesday after President Donald Trump’s speech failed to guarantee an end to the war in Iran. Oil prices soared following the speech and beyond traders’ war-related worries, tumult in the private credit markets is also taking a toll on investor confidence across multiple markets.

While Bitcoin has successfully defended the $66,000 level throughout the week, traders remain concerned about downside risk over the upcoming weekend, as US and European markets will be closed on Friday for Easter.

The threat of additional US-led military action in Iran caused WTI crude oil prices to rally above $110, triggering a move away from risky assets. Traders chose to cut their exposure to Bitcoin and stocks as the US Treasury Department expressed concerns regarding the $2 trillion private credit markets on Wednesday. Domestic and international insurance regulators will be surveyed through early May.

Private credit markets sound the alarm: Will BTC respond?

Blue Owl, a $307 billion alternative asset manager, announced “extraordinary redemption requests” for two of its private credit funds in shareholder letters issued Thursday. Over 70% of the companies Blue Owl lends to are in the software industry, as reported during a quarterly earnings call. The fund manager capped withdrawal requests at 5%, adding fresh concerns to the credit market.

Adding to the short-term bearish sentiment among traders was a surge in US continuing jobless claims, which rose to 1.84 million for the week ending March 21, up from 1.82 million the week prior. This data is not inherently negative for equities; however, as the global outplacement firm Challenger, Gray & Christmas noted, most layoffs originated from companies “shifting budgets toward AI investments at the expense of jobs.”

The odds of economic stimulus initiatives amid weakening economic activity could ultimately support Bitcoin’s price in the medium term. The US federal deficit is expected to reach a massive $1.9 trillion in 2026, leaving little room to maneuver other than injecting liquidity, which tends to benefit scarce assets.

An improvement in the risk perception of Bitcoin will be decisive for a potential rally above $75,000. There has been a considerable negative impact from net outflows from US-listed spot exchange-traded funds (ETFs), the liquidation of positions held by companies that previously focused on building corporate reserves, and the unwinding by publicly listed miners.

US-listed Bitcoin ETFs have seen $450 million in net outflows since March 24, which serves as a proxy for weak institutional demand. Traders fear further selling pressure because the industry holds $88 billion in Bitcoin under management, with BlackRock’s iShares Bitcoin Trust (IBIT US) leading at $53.9 billion. However, these outflows should slow if Bitcoin continues to show strength near $66,000.

Related: Bitcoin hits weekly low on oil fears as analyst teases $10K BTC price target

MARA Holdings (MARA US) announced the sale of 15,133 BTC in March at a price far below the company’s estimated cost basis. Meanwhile, Riot Platforms (RIOT US) reportedly transferred 500 BTC for sale on Wednesday. Additionally, Nakamoto Holdings (NAKA US) disclosed a sale of 284 BTC, despite having previously announced its intention to continue accumulating the asset.

As long as companies such as Strategy (MSTR US) and Metaplanet (MTPLF US) continue to absorb some of this selling pressure, investors will likely recognize that Bitcoin serves as a safeguard against increasing money supply. Governments will do everything possible to avoid a recession, raising the odds that Bitcoin’s path to $75,000 stays firmly in play despite worsening macroeconomic conditions.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

The ongoing Iran conflict is now costing Americans real money—and the numbers are starting to add up. New estimates show the war has cost roughly $30–45 billion in just over a month.

When broken down, that equals about $2.5 to $3.8 per person per day, with a central estimate near $3 daily.

The biggest driver is US military spending. Early data suggests tens of billions have already been spent on operations, making it the largest direct cost.

However, Americans are feeling it most at the pump. Oil prices surged from around $79 a month ago to over $110 per barrel, driven by supply fears and disruptions around the Strait of Hormuz.

That pushed gasoline prices sharply higher, adding billions in extra household fuel costs.

Meanwhile, inflation is starting to creep up. Rising oil feeds into transport, food, and goods pricing. Mortgage rates have also moved higher, increasing borrowing costs.

There is also a much higher “hidden” cost. US stocks have lost trillions in value during the conflict. That hits retirement accounts and savings, though it is not a direct daily expense.

Simple Cost Breakdown (34 Days)

| Category | Estimated Cost |

| Military spending | $23B – $34B |

| Higher fuel costs | $4B – $6B |

| Inflation spillover | $2B – $4B |

| Total | $30B – $45B |

Implications are Higher

In simple terms, the average American is quietly paying a few dollars a day through higher prices and government spending.

But the real risk is escalation. If oil keeps rising—or the war expands—these costs could increase sharply, hitting both inflation and financial markets at the same time.

The post How Much Has the Iran War Cost the Average American Per Day? appeared first on BeInCrypto.

Soluna Holdings, a publicly traded Bitcoin mining and AI infrastructure firm focused on renewable energy, disclosed a $53 million deal to acquire the Briscoe Wind Farm in Briscoe County, Texas. The purchase is aimed at powering its upcoming Project Dorothy 3 AI data center campus. The Briscoe facility carries a potential capacity of up to 300 megawatts (MW), and Soluna expects the site to generate annualized revenue in a range of $20 million to $24.4 million. On the news, Soluna’s shares rose about 7.6%, trading near $0.76 per share.

Soluna has been diversifying beyond crypto mining since February 2024, expanding into AI data center infrastructure in the midst of a broader industry pivot toward AI and high-performance computing to shore up revenues as mining profits faced pressure.

Related coverage on the strategic shift and its implications for the crypto mining sector provides additional context for readers following this transition.

Key takeaways

- Soluna commits to a wind-powered expansion with the Briscoe Wind Farm, potentially adding up to 300 MW of capacity to feed its Dorothy 3 AI campus.

- The project is expected to generate $20–$24.4 million in annual revenue, illustrating a shift toward diversified infrastructure revenue streams for crypto-focused operators.

- Industry profitability remains under pressure: CoinShares reports show up to 20% of mining companies aren’t profitable as of early 2026, with miners facing higher energy costs and flattening block rewards.

- Mining economics have deteriorated: the average cost to mine one BTC rose to nearly $80,000 in Q4 2025, while Bitcoin traded well below that level amid a volatile price environment.

- Hashrate growth and balance-sheet strain have driven renewed emphasis on renewables, with several operators adopting wind and solar solutions to reduce exposure to traditional energy markets.

Wind power as a hedge for an evolving sector

The Briscoe Wind Farm purchase aligns with Soluna’s broader strategy of integrating renewable energy with cutting-edge compute capacity. The company’s plan to power Dorothy 3 with wind capacity reflects a longer-term thesis: align infrastructure assets with revenue streams less tied to the cyclical swings of crypto mining. Soluna previously highlighted its foray into AI hosting and co-location services as part of a February 2024 expansion into AI data center infrastructure, signaling a deliberate pivot away from relying solely on volatile mining rewards.

In September, Soluna also announced a collaboration with Canaan, a major mining hardware manufacturer, to deploy a wind-powered BTC mining facility at the Briscoe site. That partnership underscores a dual objective: leveraging renewable energy to improve mining cost structures while integrating AI-focused data center capabilities to diversify cash flows.

The move comes amid a broader industry environment where operators are rethinking energy strategies. The growing emphasis on renewables is partly driven by the need to reduce exposure to asymmetric power costs and by the search for predictable, long-term capacity utilization that AI and HPC workloads can provide.

Industry profitability in the crosshairs

The mining sector continues to grapple with a convergence of challenges. A March 2026 report from asset manager CoinShares notes that a sizable portion of miners are operating at or near breakeven, with as many as 20% of surveyed firms not profitable in that period. The report attributes slipping margins to several factors, including the halving cycle’s aftermath, elevated energy costs, and a tougher price environment for BTC.

The trajectory of Bitcoin prices has also weighed on miners. CoinShares notes that the October 2025 market crash pulled BTC from a peak near $125,000 to around $60,000, a move that compressed margins further as network hashrate continued to climb. The rising hashrate implies more competition for block rewards, intensifying the push for cost-efficient energy and hardware strategies.

In response, several miners have been retreating to renewable energy and smarter energy arrangements. The industry’s energy-cost sensitivity is evident in the fact that miners sold more than 15,000 BTC between October and early March to cover operating expenses, with selling continuing into recent weeks. The pivot to renewables, including partnerships and wind/solar-powered facilities, has become a cornerstone of efforts to sustain operations in a tighter profitability environment.

Renewable deployments are not limited to Soluna’s circle. Other operators—such as The Phoenix Group and Sangha Renewables—have begun integrating renewables to power mining operations, highlighting a broader market trend: energy resilience is increasingly a competitive differentiator for miners facing margin compression.

The momentum around AI-oriented data centers and renewable energy co-location has also fed into broader industry discussions about how Bitcoin mining can coexist with high-demand compute workloads. A related piece of coverage has explored whether AI buildouts could crowd out or compete with mining for energy resources, a dynamic that investors are watching closely as the sector evolves.

What changes, and what remains uncertain

Soluna’s strategic bet on a wind-powered, high-capacity data center campus signals an ongoing effort to diversify revenue beyond commodity mining rewards. The Briscoe deal illustrates how renewable energy assets can bolster a capital-intensive plan to scale AI infrastructure while mitigating the sensitivity of traditional mining to price swings.

Yet the path forward is not without risk. The profitability gap for miners, volatile BTC pricing, and ongoing energy price dynamics remain central uncertainties. The success of Dorothy 3 will hinge on the pace of AI compute adoption, the cost of wind-energy integration, and the ability to sustain utilization at scale. Investors will also be watching how revenue from AI-focused data center operations compares to, and complements, traditional mining earnings over time.

As the sector navigates a period of transition, market participants will likely scrutinize the economics of similar renewable-energy collaborations, the pace of AI demand growth, and the regulatory environment shaping both mining and data-center development.

Readers should monitor Soluna’s project updates, energy grid considerations in Texas, and how the company’s revenue projections progress against actual performance once the facility becomes operational. The evolving balance between AI infrastructure and mining economics will help determine whether renewables can reliably stabilize cash flows for crypto-native operators moving forward.

For context, Soluna’s objectives and the broader industry dynamics continue to be discussed in tandem with coverage on AI-hosting momentum and its potential impact on Bitcoin mining, underscoring a pivotal moment for the sector’s energy strategies and growth trajectories.

Source context: Soluna’s deal details and the Briscoe Wind Farm capacity were reported by Cointelegraph, while CoinShares provided analysis on mining profitability, energy costs, and hashrate dynamics. Market price references for Soluna shares come from Yahoo Finance, reflecting intraday movement around the announcement.

Crypto World

Coinbase’s x402 Payment Protocol Moves to Linux Foundation With Backing From Google, Stripe, and Visa

The open standard for embedding payments into HTTP interactions aims to become the settlement layer for AI agent commerce, with over 20 founding members spanning tech, payments and crypto.

The x402 protocol, Coinbase’s open standard for embedding stablecoin payments directly into web interactions, has officially moved to the Linux Foundation as the newly launched x402 Foundation opens its doors with a broad coalition of industry heavyweights.

The announcement, made Thursday at the MCP Dev Summit North America, marks the protocol’s transition from a Coinbase-led project to a vendor-neutral, community-governed standard designed to accelerate adoption as AI agents increasingly need to pay for services autonomously.

The foundation’s initial governing body includes Cloudflare and Stripe, and founding members include Adyen, Amazon Web Services, American Express, Ampersend.ai, Ant International, Base, Circle, Fiserv Merchant Solutions, Google, KakaoPay, Mastercard, Merit Systems, Microsoft, Polygon Labs, PPRO, Sierra, Shopify, Solana Foundation, Thirdweb and Visa.

From HTTP Error Code to Payment Layer

The x402 protocol revives HTTP’s long-dormant “402 Payment Required” status code, turning it into a functional payment handshake. When an AI agent requests a paid resource, the server responds with a 402 status containing machine-readable price and settlement details. The client signs a payment payload and retries the request, and a facilitator verifies and settles the transaction on-chain.

The design supports both fiat and crypto payment methods across multiple blockchains.

The launch comes as the race to build the internet’s AI payment layer intensifies. x402 faces competition from the Machine Payments Protocol, developed by Stripe and Paradigm’s Tempo blockchain, which uses session-based authentication rather than x402’s per-request model.

Google has already integrated x402 into its Agentic Payments Protocol as the default stablecoin rail. The surrounding infrastructure is also expanding: MoonPay last week released the Open Wallet Standard for AI agent wallet interactions, Visa launched its CLI payment tool targeting agent commerce, and Circle built its Nanopayments directly on x402 for sub-cent USDC transactions.

Coinbase and Cloudflare first announced their intent to create the foundation in September 2025. By placing the protocol under the Linux Foundation’s governance, x402 aims to function as an AI commerce equivalent to SSL, the encryption standard that has become foundational to secure web browsing.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Bitcoin’s (BTC) range-bound trading within the $60,000 to $73,000 range is impressive, especially when considering the macroeconomic backdrop of Brent crude oil rising to levels not seen since 2008, a hot war between the US, Israel and Iran, and a volatile stock market where the S&P 500 index trades at a 3.95% year-to-date loss.

Despite these intensifying headwinds, Bitcoin buyers have shown a steady appetite for buying the price drops to $60,000, and while the level currently holds as support, the risk of lower prices is not zero.

Bitcoin’s 1-day chart shows a bearish continuation pattern, with one pattern confirmed on Jan. 20 as BTC price entered a correction to $60,014, and a second bear flag currently in play. Every price rally to the flag’s overhead trendline has been rebuffed since Feb. 8, and technical analysis stresses the importance of a rally and multi-day candle close above $76,000 to negate the pattern.

Ideally, a rally to $76,000 would hold through a 2- to 3-day consecutive-candle close, followed by a retest of the trendline at $75,000 to confirm a support-resistance flip, where a former resistance level is now confirmed as support.

Analysis by chartered market technician Aksel Kibar predicts a potential price drop to $52,500. Referencing analysis from March 18, Kibar said that a,

“Breakdown of the lower boundary will be the signal for a possible move toward $52,500.”

Related: Bitcoin traders forecast short-term downside even as BTC price chases $68K

Data from Velo highlights the relatively flat market demand across Bitcoin’s spot and futures markets. Although traders appear to view instances where BTC’s funding rate turns negative as a buying opportunity, their confidence is largely absent during rallies into the bear flag’s trendline resistance.

Evidence of this is seen in Bitcoin’s aggregated open interest remaining pinned below $20 billion, a level not seen since Feb. 2 when BTC traded near $79,000.

Regarding Kibar’s $52,500 price prediction and its alignment with Bitcoin’s futures markets, Hyblock liquidation heatmap data shows a large number of leveraged long positions at risk of liquidation if BTC falls into the $63,000 to $65,000 range.

Below this is a liquidity gap, and the next block of open margin long positions starts in the $57,500 to $56,000 range.

The current price action essentially reflects a market that trades sideways and consolidates as traders search for capital flow or narrative-related factors that would push them into larger directional bets.

Until such a catalyst emerges, it’s likely that Bitcoin will continue to trade within its $10,000 range, with $60,000 as the lowest key support and $70,000 as the most challenging level of resistance.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Summary

- The Central Bank of Nigeria has launched a supervisory pilot for virtual asset providers, selecting KuCoin alongside five local fintech and crypto firms.

- The program focuses on AML, CFT and CPF compliance in line with FATF standards, requiring detailed reporting and upgrades to governance, monitoring and Travel Rule controls.

- KuCoin’s inclusion underscores its push to align with national regulatory frameworks in major emerging markets, rather than operating purely offshore.news.

The Central Bank of Nigeria has launched a pilot supervisory program for Virtual Asset Service Providers and selected a first cohort of six entities, with KuCoin standing out as the only global crypto exchange on the list. According to local press coverage, the initial phase includes Nigerian payment and crypto players cNGN, Flutterwave, Juicyway, KoinKoin and Paystack, alongside KuCoin, which serves a global user base but has significant volumes in Africa’s largest crypto market.

The pilot is designed to test how selected VASPs perform under direct central bank oversight on issues such as anti-money laundering, counter-terrorism financing and counter-proliferation financing, all framed against the Financial Action Task Force’s Recommendations 15 and 16. CBN statements cited by outlets including Leadership and AInvest describe the program as a structured effort to understand VASP business models, risk controls and data flows, and to push participants toward full FATF-aligned compliance.

Under the arrangements, participating firms must engage in regular, structured regulatory communications with the central bank and other agencies. They are required to submit periodic data on AML/CFT/CPF performance, undergo audits of customer onboarding and KYC, sanctions screening, transaction monitoring, and demonstrate credible plans to track cross-border flows under the Travel Rule for crypto transfers.

The pilot, which is expected to run for six to nine months, does not itself confer licenses or formal approval, but it does bring KuCoin and the local platforms into what the CBN calls a “controlled and structured environment” for supervision. Authorities say the goal is to move from fragmented restrictions to a risk-based regime that can both weed out bad actors and keep Nigeria’s $92.1 billion annual crypto flows inside a more stable, transparent framework.

For KuCoin, being named in the first batch alongside domestic fintech leaders is a signal that Nigerian regulators see the exchange as a core liquidity node worth pulling into the official perimeter. Analysis from regional outlets notes that the pilot engages “Nigeria’s most visible VASPs,” suggesting KuCoin’s role in local crypto activity made it unavoidable for the CBN’s initial supervisory experiment.

The selection also fits KuCoin’s broader narrative of improving its compliance posture across emerging markets, as regulators from Africa to Asia tighten rules for offshore exchanges after years of largely unregulated growth. If KuCoin can meet Nigeria’s demands on governance, monitoring and Travel Rule adherence, it will strengthen the case that large global platforms can operate under domestic oversight rather than being pushed out of key markets.

Crypto World

Crypto market structure bill release pushed back as industries view revised stablecoin yield compromise this week

Representatives of the crypto and banking industries are meeting with legislative staffers on Thursday and Friday to review revised compromise language on stablecoin yield provisions in the market structure bill, three people familiar with the plans told CoinDesk.

Industry representatives first viewed the compromise language, spearheaded by Senators Angela Alsobrooks (D-Md.) and Thom Tillis (R-N.C.), last week. At the time, the proposed compromise banned yield based solely on stablecoin balances, but did allow companies to pay out yield based on activities. The crypto industry had some issues with the language.

Politico first reported that the meetings were taking place earlier Thursday.

The text was originally expected to be released this week, but that is now unlikely. Crypto in America first reported that the text release would be delayed on Wednesday.

An individual familiar told CoinDesk earlier this week that portions of the language were still being negotiated. Another person told CoinDesk late last week that some of the crypto industry’s desired changes were largely technical tweaks to clarify details, rather than substantive changes around the treatment of yield.

It was not clear as of press time what actual changes were made, or when the text may be released to the general public.

Senator Cynthia Lummis (R-Wyo.) said last month that she expected a markup hearing — where lawmakers will debate the bill, possible amendments and vote on whether to advance the legislation to the full Senate — later in April. Under the Senate Banking Committee’s rules, the bill must be published at least 48 hours before the hearing.

While stablecoin yield and rewards are the most prominent issues holding up passage of the market structure bill, other concerns remain outstanding. These include how exactly decentralized finance (DeFi) might be defined and regulated in the bill and whether it will address U.S. President Donald Trump’s family’s involvement with various crypto projects.

Li Xiong, 41, the former chairman of Huione Group and a core member of what Chinese authorities call the Chen Zhi criminal syndicate, was escorted off a China Southern Airlines flight in Beijing on April 1 – shaven-headed, handcuffed, flanked by officers from China’s Ministry of Public Security.

The real story is what his extradition confirms: Beijing is systematically dismantling the leadership layer of what the US Treasury identified as the world’s largest illicit crypto marketplace, and Cambodia is cooperating.

Huione Group processed over $89 billion in cryptoassets through what Elliptic researchers described as the largest illicit online marketplace ever identified – a number that dwarfs most legitimate crypto exchanges by transaction volume.

- Who Was Extradited: Li Xiong, 41, former chairman of Huione Group, extradited from Phnom Penh to Beijing on April 1, 2026, at China’s request following a joint Sino-Cambodian investigation.

- Alleged Role: Li is accused of multiple crimes as a core figure in the Chen Zhi syndicate, which allegedly ran cross-border gambling, fraud, and crypto laundering operations across Southeast Asia.

- Network Scale: Huione Group’s marketplace processed over $89 billion in cryptoassets, serving pig-butchering scam centers and facilitating laundering linked to North Korean state-sponsored cyber heists.

- Enforcement Context: Li’s extradition follows Chen Zhi’s arrest in January 2026 and the US Treasury’s May 2025 designation of Huione as a primary money-laundering concern – part of a coordinated multi-jurisdiction squeeze.

- Compliance Signal: FinCEN directed US banks to sever all accounts and payments tied to Huione Group in October 2025; the extradition reinforces active enforcement risk for any institution with residual Huione exposure.

- What to Watch: Chinese authorities have indicated ongoing investigations and additional syndicate arrests – further asset seizures and indictments targeting Prince Group subsidiaries are the next likely enforcement move.

Discover: Top Crypto Presales to Watch Before They Launch

What the Huione Extradition Actually Covers – and Why the Sequencing Matters

China’s Ministry of Public Security confirmed the operation via WeChat, describing Li as a “core key member” of the Chen Zhi syndicate suspected of “multiple crimes” tied to a “major cross-border gambling and fraud syndicate.”

Cambodian authorities arrested Li separately at Beijing’s formal request before transferring custody – a distinction that matters, because it signals Cambodia is now acting on specific Chinese extradition requests rather than conducting broad regional sweeps.

Huione Group operated as a subsidiary of Prince Group, the holding entity controlled by Chen Zhi. The structure was deliberate: Prince Group provided corporate legitimacy while Huione ran the payment infrastructure that funneled proceeds from pig-butchering scams – elaborate long-con investment frauds targeting victims globally – into the broader financial system via crypto.

The US Treasury’s Financial Crimes Enforcement Network designated Huione a “primary money-laundering concern” in May 2025, citing its role processing over $4 billion in traceable illicit transactions between August 2021 and January 2025 – including proceeds from North Korean cyber heists.

That North Korea connection is not incidental. It elevated Huione from a regional enforcement problem to a sanctions-tier national security concern, which accelerated US pressure on Cambodia to act. Li’s extradition, three months after Chen Zhi’s, follows the pattern: leadership arrests are running top-down through the syndicate hierarchy.

Explore: Best Crypto Projects With High Growth Potential in 2026

The post Alleged Huione Group Money Laundering Boss Extradited to China appeared first on Cryptonews.

Crypto World

Hyperliquid Price Surge as Futures Volume Blows Out, Golden Cross Standard Breakout to $44

Hyperliquid prices soar as the futures trade activity expands. Open interest has risen to about 1.61 billion in the past 24 hours, signaling increased participation in the futures market.

Daily trading volumes have surged to record levels of over 2.4 billion, indicating strong demand for perpetual contracts and growing trader confidence in further upside.

The rise in open interest and volume suggests market participants are not leaving the market but are actively pursuing gains, supporting the current bullish trend.

Key Insights

- The derivatives participation and greater market conviction were shown by open interest exceeding 1.6 billion.

- Daily trading volumes exceeded 2.4 billion, boosting token burn mechanisms and increasing demand.

- Bullish technicals, such as a flag formation and a possible golden cross, point to a rise to 44 if momentum continues.

Futures Trading Pushes the Price

The recent price run-up is closely linked to rising derivatives trading activity. Market data show open interest around 1.61 billion in the past 24 hours, indicating more traders engaging in the futures.

Daily volumes have soared beyond 2.4 billion, signaling strong demand for perpetual contracts and growing trader confidence in further upside movement.

The increase in open interest and volume indicates market participants remain active, supporting the bullish trend.

Diversification to Real-World Assets

The platform’s move into physical assets trading has increased activity. With HIP-3, perpetual contracts based on commodities like gold, silver, and crude oil are now tradable.

This enables traders to gain exposure to conventional assets in a crypto-native setup. In March, daily volumes in crude oil contracts reached over $1 billion at the peak amid geopolitical tensions.

Moreover, the 24/7 trading feature provides a competitive edge, especially as event contracts enhance engagement.

Hyperliquid has added event-based contracts, adding another layer of participation for traders. These tools let users speculate on real-life results while managing futures exposure.

Consequently, trading activity has risen, contributing to higher fee generation. This supports token buybacks and burn facilities, which gradually reduce supply and promote price stability.

The mix of new products and increased user interaction continues to strengthen the platform’s ecosystem.

Bullish Technical Set Up Develops

Technically, Hyperliquid’s price action shows signs of a bullish continuation pattern. A flag formation formed after a sharp rise, suggesting consolidation before a potential breakout.

Additionally, the token is approaching a milestone: a potential golden cross as the 50-day moving average crosses above the 200-day moving average. This is typically viewed as a bullish signal upon confirmation.

If a breakout occurs, the next major resistance zone is around the 44 level, which analysts in traditional markets are watching in response to global events in real time.

Risks and Key Support Levels

Despite the optimistic forecast, there are downside risks. The 200-day moving average sits near 34.8 and serves as a critical support zone.

A break below this level could undermine the current setup and shift the mood to the downside. Traders will monitor price action around this region to confirm continuation or reversal.

Prognosis: Derivatives Activity Is Still Important

Derivatives trading is likely to remain a major driver of Hyperliquid’s short-term trajectory. Open interest and volumes are expected to grow, reflecting trader confidence.

Additionally, token burns tied to platform charges and product diversification contribute to liquidity and demand.

If these trends persist, Hyperliquid may continue its upward trajectory, with technical confirmations and the possibility of an upward price target near the $44 level.

Bitcoin fell below $67,000, and Ether dropped over 4% as oil surged on renewed geopolitical tensions.

Crypto markets slumped on Thursday as a fresh wave of risk-off sentiment swept across global markets following President Donald Trump’s pledge to continue military strikes against Iran.

Bitcoin (BTC) is trading at around $66,900, down 1.7% over the past 24 hours. ETH slipped 4% to $2,050, and SOL plunged 6% to $79 in the wake of the Drift exploit. Meanwhile, Ripple (XRP) dropped 3.3%.

Total crypto market capitalization decreased by 1.7% to $2.38 trillion, according to Coingecko.

The rout was triggered after Trump said Wednesday evening that the U.S. would continue strikes on Iran, reversing hopes for a diplomatic resolution that had buoyed markets earlier in the week.

The risk-off mood extended to institutional products. U.S. spot Bitcoin ETFs recorded a net outflow of $173.7 million on April 1, while spot Ethereum ETFs posted a $7.1 million withdrawal, according to SoSoValue.

Big Movers

Almost all of the Top 100 digital assets posted losses over the last 24 hours.

Algorand (ALGO) and MemeCore (M) outperformed, rallying 5%. Lighter (LIT) surged 10% after unveiling a collaboration with Wallet in Telegram.

Uniswap (UNI) and Solana (SOL) are today’s biggest losers, down 13% and 6%, respectively.

Around 185,000 leveraged traders were liquidated for $441 million in the past 24 hours, according to CoinGlass. Bitcoin accounted for $103 million, while ETH made up $93 million.

Bitcoin Rally To $75K Still Possible Despite Huge Macro Challenges

Will Their Unique Financial Structure Hold Up?

Police investigating group assault in Osgodby, Scarborough

![Bitcoin Will Drop Below $50K Unless... [Watch Today]](https://wordupnews.com/wp-content/uploads/2026/04/1775172669_maxresdefault-80x80.jpg)

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

NewsBeat5 hours ago

NewsBeat5 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Entertainment3 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World1 day ago

Crypto World1 day agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports2 days ago

Sports2 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoApple will hide your email address from apps and websites, but not cops

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech4 days ago

Tech4 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Business7 days ago

Business7 days agoChinese universities with military links bought Super Micro servers with restricted AI chips

-

Fashion6 days ago

Fashion6 days agoWeekly News Update, 3.27.26 – Corporette.com

You must be logged in to post a comment Login