Crypto World

Reform UK isn’t sharing crypto wallets with UK regulators, report

Reform UK hasn’t shared its crypto donation addresses with the UK’s Electoral Commission despite the official body’s apparent requests.

The Nigel Farage-led party announced it was accepting crypto donations last year, a situation that’s caused concern about the potential for foreign political interference and dubious funding.

A representative for the electoral commission told Byline Times, “Reform has not shared any crypto wallet address with us.”

They said, “We routinely request a variety of information from parties to ensure they are fulfilling their legal responsibilities,” adding that they “cannot comment any further on the nature of these requests as it may impact our enquiries.”

The commission is also seeking new powers to regulate political crypto donations and told Byline Times that existing laws need to be “strengthened to prevent impermissible foreign funds entering the UK system.”

Read more: Nigel Farage aide George Cottrell bets US war will last four more months

It warned that crypto donations “present particular challenges and risks in meeting electoral law requirements in identifying donors and ensuring they are permissible.”

Byline Times says no crypto donations have been reported to the commission as of yet. However, it said that donations below £500 aren’t subject to reporting rules, and warned that this loophole could allow large donations to be split up into numerous smaller ones.

Reform UK’s crypto processor exempt from UK scrutiny

Reform UK’s crypto donations are processed by a firm called Radom, which gets its virtual asset service provider license through its Poland-based arm.

Crypto donations handled by the Polish entity avoid scrutiny from the UK’s Financial Conduct Authority.

It’s not entirely covered by Europe’s Markets in Crypto-Assets Regulation (MiCA) either, as Polish President Karol Nawrocki has reportedly vetoed implementing MiCA regulations twice.

As of 2026, Poland reportedly has 1,800 virtual asset service providers listed in the country. If it doesn’t implement the MiCA regulation by July 1, 2026, Radom and these firms will have to find regulatory approval from another country within the European Union.

Read more: Huione Group head ‘Boss Xi’ reportedly arrested then released

Byline Times reports that Poland’s current regulatory regime is far from perfect, and claims that obtaining a Polish license only requires a small fee and little to no scrutiny.

Top Polish lawyer Robert Nogacki told Byline Times that the country’s crypto regulations are just “an automated registration roll — low-friction by design, high-risk by consequence — that turned a $150 formality into an exportable badge of EU credibility.”

Byline Times notes that the Huine Group, which allegedly helped launder billions of dollars worth of funds linked to South Asian scam empires, and North Korea’s hacking collective, was also licensed under Poland’s system.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Justin Sun-owned Poloniex has announced fee-free trading for any user who enrols in its “Poloniex Super” membership, which currently offers 30 days’ worth of fee-free “spot, margin, and futures trading.”

Poloniex has yet to announce what this membership will cost once the 30-day period has elapsed, though it does mention that “[a]fter the trial period ends, you will be automatically enrolled in the basic Super plan by default.”

This product announcement has led users to ask how Poloniex will make money without fees. Sun quickly explained that Poloniex has no need to make more money because “we already made enough from the bitcoin (BTC) we bought in 2012.”

Poloniex was founded in 2014 and therefore couldn’t possibly purchase any BTC in 2012, so presumably Sun is referring to BTC he purchased.

This statement that Poloniex can continue to operate based only on these profits brings to the forefront concerns about how Poloniex has managed the BTC in its reserves.

In 2020 Poloniex offered a new product, which it described at different times as “BTC on TRON” and “BTCTRON.”

This initial announcement described BTCTRON as “a type of wrapped BTC token that exists on the TRON blockchain.”

Poloniex’s Help Center provides us the contract address for this token, TN3W4H6rK2ce4vX9YnFQHwKENnHjoxb3m9.

Reviewing this contract address reveals that this token currently has a circulating supply of 17,545 BTC, worth approximately $1.3 billion.

Disturbingly, Poloniex’s so-called “proof of reserves” claims that Poloniex has a balance of only 11,090 BTC in its entire reserves and 11,082 of those are “User Balance.”

This is insufficient to reserve this tokenized BTC product.

Protos has previously repeatedly reached out to Poloniex during our past reporting on this product, and it has never been willing to provide the addresses that hold the BTC for this tokenized product.

We attempted to reach out to Poloniex again; however, it didn’t provide these addresses before publication.

Read more: FTX estate says Justin Sun still owes it millions

Increasing the concern about this product is how deeply it has been integrated into another Sun-owned exchange, HTX.

At HTX, typically there is more of this mysterious BTCTRON product, which provides no transparency, than real BTC.

As of the most recent HTX snapshot, dated March 1, there were a total of 21,362 BTC on HTX. BTCTRON accounted for 10,291 of those.

There are also an additional 1,212 BTC that are in the form of Sun-advised Wrapped Bitcoin.

What this means, taken as a whole, is that Poloniex will not disclose where the $1.3 billion in BTC that is supposed to collateralize this product is located.

Yet despite that fact, HTX is willing to make it a massive portion of its reserves, all while Sun claims that Poloniex can afford to offer “fee-free” trading because of the appreciation in the price of bitcoin.

Perhaps instead of making grandiose claims about the value of his BTC, Sun should instead work on solving the apparent BTC shortfall at the exchanges he owns.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

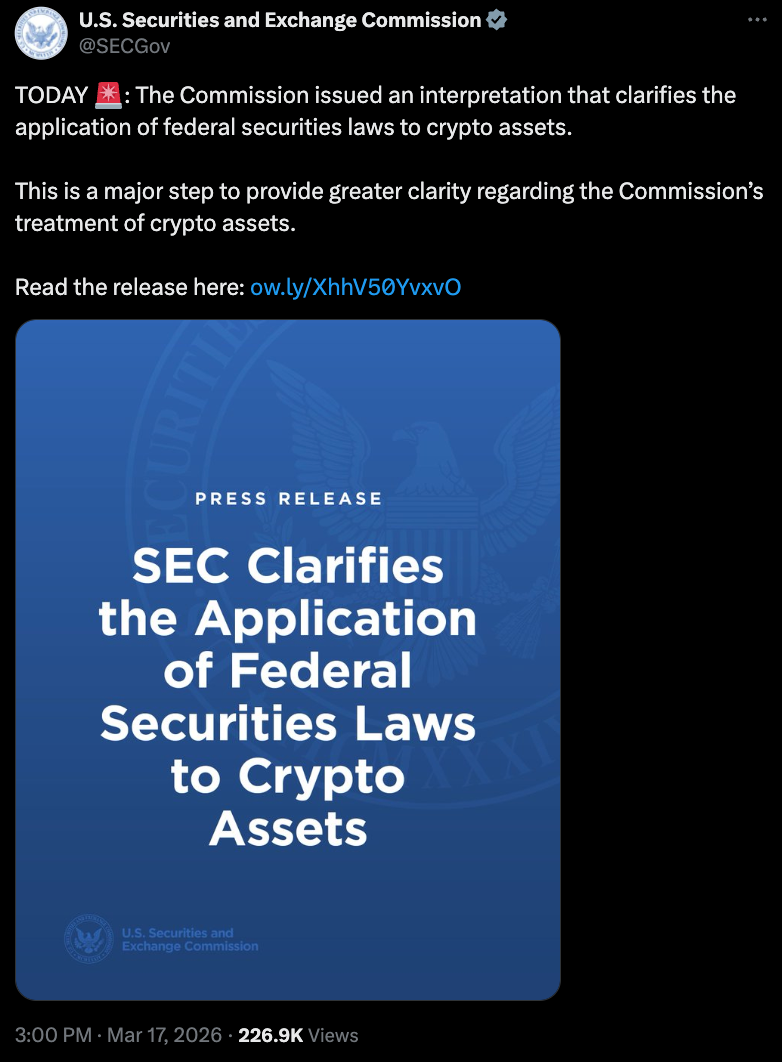

In one of its first actions since signing a memorandum of understanding with the Commodity Futures Trading Commission (CFTC), the US Securities and Exchange Commission (SEC) said it would interpret how “non-security crypto assets” fall under federal securities laws.

In a Tuesday notice, the SEC said its interpretation of how to address crypto assets would serve as an “important bridge” as lawmakers in the US Congress consider market structure legislation which will codify how financial regulators oversee digital assets.

The commission said the interpretation would provide a “coherent token taxonomy for digital commodities, digital collectibles, digital tools, stablecoins, and digital securities,” address how a “non-security crypto asset” may or may not be considered an investment contract under the SEC’s purview, and clarify federal securities laws on “airdrops, protocol mining, protocol staking, and the wrapping of a non-security crypto asset.”

“This is what regulatory agencies are supposed to do: draw clear lines in clear terms,” said SEC Chair Paul Atkins. “It also acknowledges what the former administration refused to recognize -– that most crypto assets are not themselves securities. And it reflects the reality that investment contracts can come to an end.”

According to Atkins’ prepared remarks for the DC Blockchain Summit on Tuesday, “only one crypto asset class remains subject to the securities laws” under the interpretation, and those were “traditional securities that are tokenized.” The commission called on market participants to review the interpretation to “better understand the regulatory jurisdiction between the SEC and CFTC” on cryptocurrencies.

Related: SEC, CFTC sign memo to regulate crypto, other markets in harmony

The SEC notice came as lawmakers in the US Senate continue to negotiate terms under which they may reach an agreement on a digital asset market structure bill. The legislation is expected to give the CFTC more authority in overseeing cryptocurrencies.

Shakeup in SEC enforcement leadership draws criticism

On Monday, the SEC announced that its enforcement division director, Margaret Ryan, resigned from the agency. Its principal deputy director, Sam Waldon, was named as acting enforcement director.

In response to Ryan’s departure, former SEC official John Reed Stark said “not a single person on this planet” believed the commission’s claims that the enforcement director prioritized investor protection and “renewed focus on holding individual wrongdoers accountable” at the agency.

“The SEC has abandoned its identity,” said Stark on Monday. “It has transformed from the cop on Wall Street’s beat into something far more troubling, a regulatory body that functions less like a law enforcement agency and more like a concierge service for the largest financial players in the country.”

A 19-year veteran of the regulator, Stark was founder and chief of the SEC’s Office of Internet Enforcement, according to his LinkedIn profile.

Atkins, along with SEC Commissioners Mark Uyeda and Hester Peirce — all Republicans — remain the only three leaders at the agency on a panel intended to consist of a bipartisan group of five members. As of Tuesday, US President Donald Trump had not announced any plans to nominate other commissioners to the SEC or CFTC, which had only one Senate-confirmed member.

Magazine: Clarity Act risks repeat of Europe’s mistakes, crypto lawyer warns

Institutional holders quietly added roughly 26,600 BTC to ETF positions during the recent recovery, a 2% increase in total holdings.

Bitcoin (BTC) touched $76,000 on March 17 to register its highest price level since early February, as institutional investors continued to put money into U.S. spot ETFs, extending a multi-day recovery streak coming after heavy outflows in February.

However, the rebound in demand is running into a key constraint, according to analyst Axel Adler Jr., with ETF investors still sitting on an average unrealized loss of $5,174, which he says could affect price action around the $80,000 mark.

ETF Flows Recover, But the $79,962 Realized Price Looms

In his latest market update, Adler said that spot Bitcoin ETF flows have gone through what he called a “full cycle” over the past month, going from capitulation in mid-February to a steady recovery in the last few weeks. According to him, from February 15 to 24, the seven-day average of ETF net flows stayed negative, hitting a low of about -1,883 BTC per day on February 18.

However, around February 25, the trend changed, with flows turning positive and peaking at about +3,387 BTC per day on March 2. Adler currently puts the seven-day average at around +1,472 BTC per day, with liquidity conditions also getting better. During the same period, the total number of ETF holdings rose by about 26,600 BTC, which is a little over 2%.

The analyst sees this change as a return of institutional demand after the earlier outflows. He does, however, point out that this demand is below a clearly defined level of resistance.

That level is the realized price for the ETF cohort, which Adler mapped at $79,962, an amount showing the average cost of buying an ETF for all investors. And with BTC trading just above $74,000 after earlier hitting a six-week high, it means the group still has an overall paper loss of over $5,000.

Adler described the gap as one of the most important structural features of the current market. This is because, as Bitcoin gets closer to the realized price, more investors will get closer to breaking even, which can make it more likely for them to sell. For that reason, the market technician says that the $80,000 region is a place where upward movement may slow down unless demand is strong enough to take in the potential extra supply.

You may also like:

Market to Test Resistance Condition

At the time of writing, data from CoinGecko showed BTC up over 5% in the last 7 days and the same across 30 days. However, the uptick was almost 9% over two weeks, although performance still lagged year-on-year, with the asset shedding nearly 11% from its value in that time, keeping it over 41% below its all-time high.

For now, Adler is watching the $80,000 level as the key battleground.

“A spot close above $79,962 combined with sustained ETF net inflow above +2,000 BTC per day would signal a regime change,” he wrote in his analysis.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

South Korea’s National Police Agency has introduced new guidelines for handling seized cryptocurrencies after multiple security lapses.

Summary

- South Korea’s National Police Agency has drafted new guidelines to standardize how seized cryptocurrencies are stored and managed, including provisions for privacy-focused assets.

- The move follows a series of security lapses, including lost Bitcoin linked to custody failures.

The KNPA has drafted a directive outlining compliance requirements across multiple stages of crypto seizure, storage, and management, local media outlet Asiae reported on Tuesday.

As part of the measures, law enforcement would have to follow standardized procedures for managing wallet addresses, private keys, and software wallets, including specific provisions for handling privacy-focused assets that cannot be easily stored in hardware wallets.

“In the past, seized assets were stored in warehouses. Now we must manage wallet addresses and private keys,” a police spokesperson said in an accompanying statement.

Last month, South Korea’s finance minister Koo said the government, alongside the Financial Services Commission and the Financial Supervisory Service, would conduct a full inspection of digital assets held by public institutions and review how they are managed under enforcement processes.

Comments from the minister followed back-to-back security incidents that exposed weaknesses in custody practices across agencies.

In one case, Bitcoin seized in 2021 was lost after authorities relied on a third-party custodian without maintaining control over private keys, with the issue only coming to light following an internal probe.

Police arrested two suspects related to the theft of Bitcoin from wallets linked to seized assets, further underscoring gaps in internal controls.

A separate incident led to the Gwangju District Prosecutors’ Office losing roughly 70 billion won, about $48 million, in seized Bitcoin due to a phishing attack that exposed login credentials and enabled unauthorized transfers from a state-controlled wallet.

Two Democratic lawmakers in the United States have formally introduced a bill aimed at curbing what they describe as government-insider trading risk tied to prediction markets. The BETS OFF Act, unveiled in a joint effort by Representative Greg Casar of Texas and Senator Chris Murphy of Connecticut, targets platforms whose markets place bets on sensitive government actions. The move follows a spate of high-profile bets linked to potential U.S. action in the Middle East, prompting questions about the role of real-time markets in shaping or amplifying political decisions.

Key takeaways

- The BETS OFF Act was introduced by Rep. Greg Casar and Sen. Chris Murphy in response to suspicious bets on international conflict scenarios, including a possible war involving the U.S., Israel, and Iran.

- The bill seeks to prohibit event contracts tied to sensitive government decisions and federal functions, effectively narrowing the scope of markets like Polymarket and Kalshi.

- The push comes amid continued regulatory scrutiny of prediction markets, following earlier proposals such as Sen. Adam Schiff’s DEATH BETS Act targeting war, terrorism, assassination, and deaths.

- Public discourse around insider information is central: lawmakers argue decisions in the Situation Room should not be swayed by financial positions on open markets.

- Industry声音 remains mixed—Polymarket defends the value of crowd wisdom, while Kalshi limits certain military action forecasts, reflecting divergent approaches to risk and governance in prediction markets.

Market context: The debate over prediction markets sits at the intersection of financial innovation, governance, and national security. As lawmakers push for tighter controls, market operators face clarifications on what kinds of forecasts can be legally listed, while observers watch whether broader crypto-asset and derivatives markets will influence or respond to policy changes.

Why it matters

At the heart of the BETS OFF Act is a concern that insider information—or access to non-public policy deliberations—could be translated into lucrative bets on the outcomes of military or other sensitive actions. Rep. Casar framed the issue around the possibility that “someone sitting in the situation room” could be empowered by market positions in decisions of life and death. The proposed legislation would restrict event contracts tied to government operations and major federal actions, which would notably limit the kinds of bets that platforms like Polymarket and Kalshi can offer on foreign policy and national security events.

The controversy is not purely theoretical. Earlier in the year, Sen. Schiff introduced the DEATH BETS Act, which emphasizes prohibition of markets listing events connected to war, terrorism, assassination, and deaths. The parallel push from multiple offices signals a growing concern among U.S. lawmakers about how prediction markets intersect with public policy and accountability. As markets, regulators, and political actors continue to navigate these questions, the debate intensifies around whether such platforms should be allowed to operate with the same latitude as other forms of speculative markets—and what safeguards are necessary to prevent misuse.

On the platforms themselves, Polymarket has positioned its operations as a way to harness collective intelligence for better forecasting, emphasizing the value of crowd-sourced signals during volatile periods. Kalshi, by contrast, has taken a more constrained stance for certain high-stakes scenarios, choosing not to list contracts on specific military actions or other sensitive geopolitical outcomes. The tension underscores a broader governance question: can prediction markets deliver genuine societal value without creating incentives that could distort policy or provoke manipulation?

Concerns about safety and legitimacy have also resonated beyond the markets’ floors. A Times of Israel military correspondent reported receiving death threats related to coverage of the Iranian missile strike date, underscoring the real-world stakes involved when financial markets entwine with geopolitics. Such incidents amplify the call for clearer boundaries around which events can be bet on and under what conditions, particularly when coverage intersects with ongoing conflict and public safety considerations.

Why it matters

Prediction markets have long claimed to distill “wisdom of the crowd” into probabilistic forecasts on a range of topics, from elections to sporting events. The current controversy places a sharp spotlight on how such frameworks function when sensitive geopolitical actions are on the line. If lawmakers succeed in restricting certain classes of contracts, the markets’ ability to reflect near-term probabilities on foreign policy may be curtailed. That could alter how information flows in high-stakes environments and potentially shift shifts in risk pricing across related derivative markets.

For policymakers, the BETS OFF Act represents a legislative attempt to recalibrate the balance between innovation and guardrails. The bill’s proponents argue that ensuring decisions about war and peace are not influenced by betting markets is essential to preserving the integrity of national security processes. Critics, however, may contend that market-based signals can illuminate risk and improve transparency—if properly designed with safeguards. The unfolding policy discussion will likely test the resilience and adaptability of prediction-market platforms, as well as the broader ecosystem of crypto- and mainstream financial markets intertwined with these services.

What to watch next

- Prospective committee hearings and floor votes on the BETS OFF Act, including potential amendments clarifying the scope of prohibited contracts.

- Regulatory clarifications from U.S. agencies overseeing prediction markets and related financial instruments, potentially addressing enforcement mechanisms and permissible product design.

- Updates on Kalshi’s and Polymarket’s product offerings in response to any new regulatory guidance or legislative actions.

- Ongoing reporting on insider-information concerns connected to policy decisions and how such concerns may influence market design and investor protection measures.

Sources & verification

- Official statements from Representative Greg Casar and Senator Chris Murphy announcing the BETS OFF Act, and the legislative text when released.

- Public statements and policy positions from Polymarket on the role and limits of prediction markets in current events.

- Kalshi’s publicly stated market scope and its approach to sensitive geopolitical contracts, including any restrictions on military action forecasts.

- Past congressional actions and debates around prediction markets, such as the DEATH BETS Act introduced by Senator Adam Schiff.

Key figures and next steps

Market participants and policy observers will be watching how lawmakers articulate the balance between innovation and safeguards in prediction markets. The BETS OFF Act joins a broader set of questions about the accountability of platforms that monetize forecasts on sensitive events. If enacted, the legislation could reorient product design, risk controls, and the permissible scope of bets offered to the public. Until then, Polymarket and Kalshi—along with other platforms—continue to operate within the existing regulatory framework while navigating the evolving political discourse surrounding insider information, elections, and foreign policy risk.

What to watch next (summary)

- Legislative votes or committee actions on the BETS OFF Act and its potential amendments.

- Regulatory clarifications issued by relevant U.S. agencies about prediction-market operations.

- Platform policy adjustments by Polymarket and Kalshi in response to new rules or enforcement actions.

- Ongoing media reporting on insider-information concerns and related safety incidents tied to market-driven forecasts.

The popular Solana wallet can now partner with registered exchanges to offer in-app access to derivatives and event contracts without registering as a broker.

Phantom, a popular self-custodial crypto wallet, has obtained no-action relief from the Commodity Futures Trading Commission (CFTC), allowing it to connect users to derivatives trading through registered market participants without registering as an introducing broker.

The relief allows Phantom to act as a technology service vendor (TSV) to Designated Contract Markets (DCMs), registered futures commission merchants (FCMs), or introducing brokers (collectively, “Collaborators”), enabling users to access event contracts, perpetual contracts, and other CFTC-regulated derivatives through Phantom’s interface.

Phantom described the relief as “first-of-its-kind,” signaling a potential regulatory template for other crypto wallet providers looking to bridge crypto-native users into traditional financial markets. Phantom also said it proactively engaged with the CFTC to clarify how a non-custodial interface could provide access to regulated markets.

The letter imposes 10 conditions, including: providing users with risk disclosures consistent with CFTC regulations; complying with National Futures Association rules on public communications; executing joint-and-several-liability undertakings with each Collaborator; and maintaining records in line with CFTC standards. The relief remains in effect until the Commission issues formal rulemaking addressing broker registration requirements for software providers.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Crypto World

Best Crypto Presale: DeepSnitch AI Surges 200% as Web3 Companies Go All-In on AI Technology

Messari just replaced its CEO and laid off staff to become an AI company. The crypto data firm that built its reputation on human-driven research is now opening its data layer to autonomous AI agents and repositioning entirely around artificial intelligence.

Messari spent years building the human research model before concluding AI had to replace it. DeepSnitch AI started there. Five live AI agents running today, and a TGE confirmed for March 31st on Uniswap.

While Messari restructures its entire company to catch up to where AI-native crypto intelligence is heading, DSNT is already operating inside that future, and the best crypto presale opportunity closes in weeks.

Messari pivots to an AI-first strategy

Messari has announced layoffs alongside a leadership transition, with founder-era CEO Eric Turner stepping down in favor of longtime CTO Diran Li, who is repositioning the crypto data firm as an “AI-first company serving institutions through research and AI products.”

The restructuring follows previous workforce reductions in 2023 and 2025, suggesting ongoing pressure on crypto-native data businesses to find sustainable revenue models.

Messari’s transformation reflects a broader industry pattern: crypto-native companies are increasingly reorienting around AI as the primary growth vector. As institutional demand shifts toward AI-powered research and autonomous agent infrastructure, the line between crypto data providers and AI companies is rapidly dissolving.

Top 3 best crypto presales to buy in 2026

DeepSnitch AI

Messari just concluded that human-driven crypto research can’t compete with AI-native intelligence, and restructured its entire company around that conclusion. DeepSnitch AI reached the same conclusion before writing a single line of fundraising copy and built the product first.

That sequencing matters. Messari is now racing to open its data layer to autonomous agents. DeepSnitch AI’s five AI agents have been running continuously since before this presale launched.

The same institutional demand that forced Messari’s restructuring is the demand DeepSnitch AI was designed to serve at the retail level: real-time, AI-driven market intelligence that doesn’t require a research team or a Bloomberg terminal to access.

The market has already started pricing that in, naming DeepSnitch AI the best crypto presale of 2026.

$2.2M raised during a bear market, the same conditions Messari called difficult enough to justify layoffs. That capital arrived because investors looked at a working platform and made a deliberate call about where AI-native crypto intelligence is heading.

The March 31st TGE is the fixed point that everything converges on. After the presale closes, a 7-day claim period opens for tokens, presale bonuses, and staking rewards.

Messari took years to conclude that AI had to replace its old model. The market won’t wait that long to reprice a live AI-native trading platform hitting public markets for the first time. At $0.04487, that repricing hasn’t happened yet for DeepSnitch AI.

Based Eggman

Based Eggman (GGs) sold out two presale stages and raised over $311,000. Built on Base, the project accesses low fees and institutional ecosystem credibility that meme coins on congested networks can’t match.

The token combines play-to-earn gaming and community events in one ecosystem. Multiple demand drivers give holders real reasons to hold beyond listing day. That’s more ambitious than the single-feature offerings crowding this space.

The ambition is also the risk. Building gaming, streaming, and social infrastructure simultaneously at the presale stage is complex. Projects that spread across too many verticals early tend to underdeliver across all of them.

Pepeto

Pepeto raised over $8M, building dedicated infrastructure for the meme coin ecosystem. Dual audits from SolidProof and Coinsult add security credibility that most projects at this stage skip.

The differentiation challenge is real. DEX functionality, bridging, and staking have become baseline expectations, not advantages. The crowded field moved while Pepeto was building.

The broader headwind compounds it. Investors rotate toward utility-focused and TradFi-adjacent projects. Building infrastructure for a contracting market segment creates structural demand risk that community enthusiasm alone doesn’t solve.

Closing thoughts

Messari fired staff to become an AI company. The writing is on the wall: manual crypto research is ending, and AI-native intelligence is taking over. DeepSnitch AI was already there, which is why it is considered the best crypto presale of this year. Live tools, $2.2M raised, 200% presale gains, and a March 31st Uniswap launch confirmed.

DSNT delivers a working AI intelligence layer at the exact moment Messari’s restructuring confirms that’s where the industry is heading. A $10,000 position with the DSNTVIP150 code adds a 150% token bonus before the first listing candle prints.

Visit the official website for more information, and join X and Telegram for community updates.

FAQs

Which crypto presale coins offer the strongest early investor opportunities as AI reshapes the market?

The best crypto presales right now are DeepSnitch AI, Ozak AI, and Pepeto. DSNT leads with $2.2M raised, five live AI agents, and a confirmed March 31st Uniswap launch with 1,000x return potential backed by a working product.

What makes DeepSnitch AI one of the best early investor crypto deals heading into Q2 2026?

DeepSnitch AI stands out among early investor crypto deals because the product is already live. The protocol has five AI agents running daily, 200% presale gains, and a hard March 31st deadline before Uniswap listing and major CEX additions could follow shortly after.

How do token presale opportunities like Ozak AI and Pepeto compare to DeepSnitch AI right now?

Among current token presale opportunities, Ozak AI raised $6.4M with promising analytics tools, and Pepeto raised $7.8M with meme infrastructure, but DeepSnitch AI’s confirmed launch date and AI-first positioning make it the strongest complete opportunity available before Q2.

The post Best Crypto Presale: DeepSnitch AI Surges 200% as Web3 Companies Go All-In on AI Technology appeared first on Blockonomi.

Summary

- Ripple plans to apply for a Virtual Asset Service Provider license from the Central Bank of Brazil, pulling its operations under Brazil’s new crypto framework instead of operating as a grey “technology vendor.”

- Banks and fintechs including Banco Genial, Braza Bank and Nomad already use Ripple infrastructure for same‑day dollar transfers, real‑backed stablecoins and cross‑border fund flows, while partners like CRX and Justoken issue tokenized commodities and other RWAs via Ripple custody tools.

- For Ripple and XRP watchers, Brazil combines deep remittance corridors, a sophisticated banking sector and pragmatic tokenization rules, making it a key test case for whether XRP‑ledger rails can matter beyond litigation headlines and secondary‑market hype.

Ripple (XRP) is stepping up its Latin American strategy, moving to formalize its presence in Brazil’s regulated crypto market while quietly deepening real-world payment and tokenization rails in the country. The company said it plans to apply for a Virtual Asset Service Provider (VASP) license from the Central Bank of Brazil, a move that would pull its local operations directly under the country’s evolving crypto framework.

The push comes as several Brazilian financial institutions are already plugged into Ripple’s infrastructure for cross‑border flows and on‑chain settlement. Investment bank Banco Genial uses Ripple’s network to process same‑day dollar transfers, effectively turning the ledger into back‑end plumbing for faster FX and remittance rails. Braza Bank has gone a step further, issuing a real‑backed stablecoin on the XRP Ledger, using Ripple’s tech stack to tokenize local fiat and streamline domestic and cross‑border settlements.

Fintech firm Nomad is also using Ripple’s network for stablecoin‑based fund flows between Brazil and the U.S., positioning XRP‑ledger rails as an alternative to traditional correspondent banking in a corridor notorious for fees and friction. At the same time, partners including CRX and Justoken are issuing tokenized assets through Ripple’s custody products, covering commodities and other real‑world assets that local investors already understand and regulators can more easily slot into existing frameworks.

If granted, a VASP license would effectively turn Ripple from a quasi‑grey “technology vendor” into a supervised participant in Brazil’s digital asset regime. That matters for institutions that want crypto‑adjacent yield, remittance efficiency, or tokenization upside but remain unwilling to touch unlicensed infrastructure. For Ripple, Brazil offers the right mix: large remittance corridors, a sophisticated banking sector, and regulators that are tough but pragmatic on stablecoins and tokenized assets.

For XRP and broader market watchers, the Brazil pivot is another sign that Ripple’s post‑U.S.‑litigation strategy leans heavily on jurisdictions where payment use cases, not speculative trading, are the headline. If Ripple can secure a VASP license and scale real‑world flows through banks like Genial and Braza, Brazil could become one of the key test beds for whether XRP‑ledger infrastructure can matter beyond courtrooms and secondary‑market narratives.

NFT marketplace shelves March 30 TGE target with no new date, ends rewards campaign, and offers fee refunds.

OpenSea has pushed back the launch of its long-awaited SEA token for the second time, with co-founder and CEO Devin Finzer announcing Monday that the previously planned March 30 token generation event will not go ahead as scheduled.

“A delay is a delay. I’m not going to dress it up, and I know how it lands,” Finzer wrote on X, adding that the OpenSea Foundation opted to hold off rather than force a debut in challenging market conditions. No new date has been set.

The SEA token was first announced in February 2025 as part of OpenSea’s broader strategy to transform the platform beyond NFTs into a multi-chain trading hub.

Alongside the delay, OpenSea is making several changes to its incentive program. The current Treasure rewards wave will be the last, though accumulated rewards will be “meaningfully considered.”

Users who participated in Seasons 3 through 6 will have the option to claim refunds for platform fees paid during those periods, though doing so will require forfeiting any Treasure accumulated from those waves.

Starting March 31, OpenSea will also cut token swap trading fees to 0% for 60 days, a move aimed at driving adoption of its expanded OS2 platform, which now includes cross-chain trading, mobile features, and perpetual futures.

Finzer framed the delay as a strategic decision rather than a setback. “The thing that’s carried us through every cycle was a willingness to make hard calls when it mattered,” he wrote, adding that the foundation would announce a new timeline only once launch conditions are deemed appropriate.

Community Apathy

The response from the community has been predictably sour, though muted; likely a reflection of eroding expectations rather than surprise.

The refund mechanism itself has drawn criticism, with users questioning why participants in earlier waves who traded significantly higher volumes weren’t given the option.

“Like many of you, I’ve been personally looking forward to SEA since before I joined. I’m with you. But I also want to see it set up for long-term success and sustainability,” OpenSea CMO Adam Hollander wrote on X.

The reassurances may not land easily, given the platform’s track record on this front. As The Defiant reported last October, most users’ trust in the legacy NFT platform had already fallen as the company sought to convince users to trade tokens on OpenSea, with data showing that much of the activity at the time was driven solely by SEA farming incentives.

For many participants who have spent months farming Treasure across multiple reward waves, the indefinite delay amounts to the latest in a long series of deferred promises from a platform once synonymous with the NFT boom.

A Long Time Coming

The SEA token has been dangled in front of OpenSea users for the better part of two years.

Speculation began in earnest in late 2024, when the OpenSea Foundation surfaced on X and was found to have been registered in the Cayman Islands.

The formal announcement arrived in February 2025 alongside the public launch of OS2, OpenSea’s revamped trading platform, which integrated token swaps, a pivot driven by a significant decline in NFT trading volume, which had fallen from a peak of $5 billion per month in January 2022 to just $195 million in January 2025.

In September 2025, OpenSea quietly doubled its NFT trading fees from 0.5% to 1%, funneling half of all fees into a pre-token launch rewards pool distributed through a gamified system.

Much of the trading activity that followed was driven by SEA farming incentives rather than genuine product-market fit, with critics pointing to surprise KYC requirements and vague promises regarding how 2021-era traders would be rewarded.

After OpenSea concluded its first chest farming season in October 2025, the platform’s DEX aggregator volumes plummeted from an all-time high of $462 million on October 15 to roughly $5 million per day in the weeks that followed. DeFiLlama data shows that daily volumes have plunged further to just $2 million.

Crypto World

Orlando Bravo pushes back on private markets criticism: ‘Everybody’s extremely comfortable’

Orlando Bravo, managing partner of Thoma Bravo, speaks during “Squawk on the Street” at the World Economic Forum in Davos, Switzerland, on Jan. 21, 2026.

Oscar Molina | CNBC

Orlando Bravo, founder and managing partner of Thoma Bravo, pushed back on mounting criticism of private markets, saying deep sector expertise is separating winners from losers as artificial intelligence creates disruption across the software industry.

“We have been living in the details of the space for a very, very long time, not on a high level, not investing in stocks, [but] investing in companies, customer contracts, knowing the details. So, yes, as a sector specialist in private equity, our companies are very, very different,” Bravo said Tuesday in an interview with CNBC’s Leslie Picker. “We are so comfortable with our private credit book, given the choices we’ve made as a specialist.”

His comments come as investors step up scrutiny of private-market valuations and liquidity after a wave of markdowns and redemption pressure across private credit and equity funds.

Morgan Stanley recently said it expects direct-lending default rates to reach about 8%, nearing Covid-era peaks. Meanwhile, John Zito of Apollo Global Management told UBS clients last month that private equity firms are broadly misstating the value of their software holdings, saying “all the marks are wrong.”

Bravo said Thoma Bravo’s investor base, which includes major U.S. pension funds and global sovereign wealth funds, has remained confident due to the firm’s long track record and transparency.

“They’ve seen our marks, they’ve seen our exits, they’ve seen our progression,” he said. “Everybody’s extremely comfortable.”

Addressing one of the firm’s more visible missteps, Bravo acknowledged overpaying for customer experience software company Medallia. Apollo’s Zito pointed to this $6.4 billion take-private deal in 2021 specifically, saying it will be “worse than people expect,” according to the Wall Street Journal.

“When we bought it, we way overestimated or extrapolated the very high rate of growth of that company into the future. We made a mistake. And that cost us to pay too much. Now, the equity from our standpoint has been impaired for a long time,” Bravo said. “Our investors, this group that holds the capital in the world, has known that for years. So there is no new news.”

Still, he said the broader portfolio is performing strongly.

“The other 77 companies that we have, for the most part — and it’s so relevant for AI — they’re absolutely crushing it,” Bravo said.

Bravo drew a sharp distinction between private equity-owned companies and many publicly traded software firms, saying the latter face accelerating disruption. He noted that recent valuation declines in some names are “very warranted.”

“In the public markets, if you look at it, there are many, many software companies in the public markets that will be disrupted from AI. Those companies were going to be disrupted anyway. AI will create a disruption a lot faster,” Bravo said.

No Neymar for Brazil’s last friendlies before Ancelotti names his WC squad | Football News

Arizona Charges Kalshi With Illegal Gambling Operation

U-Shaped Yield Curve Warning: Rare Signal of Financial Crises? | US Treasury Yield Curve

-

Tech7 days ago

Tech7 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Crypto World4 days ago

Crypto World4 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Sports3 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

NewsBeat6 days ago

NewsBeat6 days agoResidents reaction as Shildon murder probe enters second day

-

Business2 days ago

Business2 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business7 days ago

Business7 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

Sports6 days ago

Sports6 days agoPWHL, Senators discussing plan to keep Charge in Ottawa

-

Business3 days ago

Business3 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Tech6 hours ago

Tech6 hours agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World3 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

NewsBeat6 days ago

NewsBeat6 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Business3 days ago

Business3 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Business2 days ago

Business2 days agoAustralian shares drop as Iran war enters third week

-

Sports4 days ago

Sports4 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Crypto World2 days ago

Crypto World2 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Politics7 days ago

Politics7 days agoTrump Says Middle East Is ‘Very Lucky’ That He’s President

-

Crypto World6 days ago

Crypto World6 days agoThree Binance Charts May Be Hinting at Bitcoin’s Next Move

-

Business5 days ago

Business5 days agoTrump demands Powell cut rates as Iran conflict raises energy prices

You must be logged in to post a comment Login