Crypto World

Revolut Secures UK Bank License, Teases Upcoming Services

Revolut has received regulatory clearance to operate a fully licensed bank in the United Kingdom, launching Revolut Bank UK after approval from the Prudential Regulation Authority (PRA). The bank will offer deposit accounts to individuals and businesses, with insured deposits capped at 120,000 pounds by the Financial Services Compensation Scheme (FSCS). The transition for existing Revolut UK customers will be rolled out gradually over several months to integrate the new banking framework, while the fintech outlines a roadmap that includes lending and other services beyond basic accounts. In a broader push, Revolut also disclosed that it had filed for a full banking license in Peru and a federal US banking charter in January, signaling a multi-jurisdictional strategy to blend digital finance with traditional banking regulation.

Details of the PRA approval were echoed by Revolut in a post on X, linking to the announcement from the company. The step marks a notable milestone for a fintech that has built a reputation around rapid, user-friendly digital services and now seeks to operate within the safety nets and supervisory standards that govern traditional banks.

Revolut’s UK rollout is positioned as a foundational move that could unlock a broader range of services in due course. The bank will begin by offering deposit accounts to eligible customers, with the FSCS providing a safety net similar to the way insured deposits work in other jurisdictions. The gradual migration means customers can expect a phased onboarding process as Revolut builds the operational capacity to handle regulatory compliance, risk management, and capital requirements that accompany a licensed bank. While the immediate focus is deposit taking, the company has signaled that lending, payments, and other regulated activities could follow as the business scales within the safety framework of UK banking supervision.

The announcement aligns with a wider trend in which fintechs and crypto-adjacent firms are pursuing formal banking relationships or licenses to access regulated payment rails and traditional funding channels. Revolut’s move mirrors a broader strategic arc in the sector, where digital-first financial platforms are increasingly comfortable trading in a regulated environment that offers consumer protections and a defined line of accountability for capital and operations. In that context, Revolut’s UK license acts as both a proof of concept and a potential template for regional expansion, should regulatory approvals in other jurisdictions align with its product roadmap.

Beyond the UK, Revolut’s filings point to a multi-regional ambition. In January, the company disclosed it had applied for a full banking license in Peru and a federal banking charter in the United States. Peruvian licensing could open doors to cross-border remittances and local consumer banking, while a U.S. banking charter would place Revolut on a sharply regulated stage with potential access to broader U.S. payments infrastructure. Taken together, these moves illustrate how fintechs are recalibrating their growth strategies—seeking regulatory legitimacy not as a mere compliance checkbox, but as a platform for diversified financial services that can compete with incumbents on a more level playing field.

The sector’s momentum toward formal banking has also intensified discussions about the role of crypto and digital assets within regulated systems. A subset of crypto-focused firms has long argued that national bank charters could unlock direct access to the payments rails and reduce friction for on-ramps and off-ramps between crypto ecosystems and traditional finance. Notable examples cited in industry conversations include Ripple, Paxos, and Circle, all of which have pursued or explored regulatory designations that would position crypto-related activities within the broader banking ecosystem. In March, Kraken—one of the largest crypto exchanges—was granted a limited-purpose master account with the Federal Reserve Bank of Kansas City, marking a historic step toward direct Fed access for crypto entities, albeit with clear constraints designed to preserve safety and supervision of the payments system.

The broader regulatory environment remains dynamic. A banking trade association in the United States has reportedly considered legal action against the Office of the Comptroller of the Currency (OCC) to block crypto firms from acquiring bank charters, highlighting the friction between innovation and traditional banking controls. At the same time, bankers and lobbyists have pushed back against yield-bearing stablecoins and other crypto-enabled services that could shift market share away from established lenders. The tension between encouraging financial innovation and maintaining systemic safeguards continues to shape policy, litigation, and strategic partnerships across the fintech and crypto sectors.

From a market perspective, these developments come amid ongoing debates about how to balance consumer protection, financial stability, and competitive innovation. While Revolut’s UK launch demonstrates growing appetite for regulated, tech-enabled banking, the path forward will likely hinge on how regulators interpret cross-border licensing, consumer protections, and the interplay between digital assets and traditional financial rails. The next 12 to 24 months could see a flurry of licensing activity, updated supervisory frameworks, and more structured collaborations between fintechs, crypto firms, and conventional banks as the financial system absorbs rapidly evolving digital capabilities.

In parallel, the industry’s push toward deeper integration with the formal banking system underscores a broader shift in which digital-first firms are increasingly treated as participants in traditional finance rather than isolated disruptors. That shift is fueling a dual dynamic: a demand for robust regulatory compliance to gain legitimacy and, at the same time, a push to innovate on product design and customer experience within those regulatory boundaries. Revolut’s UK bank launch is a concrete manifestation of this trend, signaling that the boundary between fintech and conventional banking is continuing to blur in a carefully managed, policy-driven manner.

Key takeaways

- Revolut Bank UK begins operations after PRA approval, offering deposit accounts with FSCS protection up to 120,000 pounds per depositor.

- Existing Revolut UK customers will be transitioned gradually to the new bank accounts over several months, with lending among the future service expansions.

- Revolut has pursued cross-border licensing, filing for a full Peruvian banking license and a US federal banking charter in January.

- The crypto industry continues to seek bank charters to access traditional payment rails, while regulators and bankers push back on risk and market disruption.

- Kraken secured a limited-purpose master account with the Federal Reserve Bank of Kansas City in March, marking a milestone for crypto access to the Fed system, albeit within defined limits.

- Regulatory debates around stablecoins and crypto banking remain a central battleground for incumbents and fintechs alike.

- Timeline for Revolut Bank UK’s onboarding of existing customers and the rollout of new lending products.

- Progress and outcomes of Revolut’s Peru banking license application and the US federal charter filing made in January.

- Regulatory responses to crypto firms pursuing bank charters, including any developments from the OCC or related lawsuits.

- Further updates on crypto firms’ access to Fed-like payment rails, including any new master accounts or adjusted eligibility criteria.

- Revolut’s official announcement confirming Revolut Bank UK and FSCS-deposits coverage of up to 120,000 pounds.

- PRA regulatory approval documentation for Revolut Bank UK.

- Revolut’s disclosures about Peru and the US banking charter filing in January.

- Kraken’s master account with the Federal Reserve Bank of Kansas City and related coverage of Fed access for crypto firms.

- Public industry discussions regarding crypto banking, OCC actions, and debates on stablecoins and traditional banking disruption.

Sentiment: Neutral

Market context: The move illustrates a broader trend of fintechs seeking regulated banking status to access payments rails and expand product offerings, while regulators balance innovation with consumer protection and systemic resilience.

Why it matters

For consumers and businesses, Revolut Bank UK unlocks insured banking through a familiar digital platform, potentially simplifying tasks such as savings, payments, and lending within a single ecosystem. The FSCS protection up to 120,000 pounds provides a safety net that investors and everyday users expect from a licensed bank, enhancing trust as customers migrate from non-bank services to regulated accounts.

From a broader industry perspective, the move signals a continued convergence between fintechs, crypto-adjacent firms, and traditional banking. By pursuing regulated status, fintechs aim to secure greater access to payments infrastructure, risk controls, and capital markets channels—without surrendering the speed and user-centric design that define their brands. Yet the path is not without risk: industry advocates must navigate a complicated regulatory landscape and potential pushback from lenders wary of new entrants encroaching on the core of conventional banking. The Kraken development and the OCC-related discussions underscore how policy, liquidity access, and the stability of the payments system remain central to any expansion of crypto and fintech activities into licensed banking territory.

What to watch next

Sources & verification

US-based prime brokers, financial institutions that provide services to hedge funds, are reportedly working to give their clients access to Kalshi’s event bets, with prediction markets booming over the past year.

According to a report from Bloomberg on Wednesday, executives from both Clear Street and Marex Group Plc confirmed that their firms expect to open up access to Kalshi’s prediction markets in the near future.

Clear Street, which is valued at over $12 billion, is expected to be the first of the two to make the jump, with CEO Ed Tilly stating that the firm expects its first Kalshi trade to clear in late March. Marex, valued at around $2.6 billion, plans to follow suit in the next few months.

Thomas Texier, Marex’s global clearing head, said they are seeing strong demand from large financial institutions that are looking for ways to tap into prediction markets.

“Over the last few weeks, we’ve seen very large hedge funds coming to us and saying, ‘Can you give us access to these markets?’” Texier said, adding that the firm is also interested in using prediction markets to hedge its own positions.

Kalshi CEO sees accelerating institutional adoption

In a post on LinkedIn on Wednesday, Kalshi CEO Tarek Mansour said institutional adoption will greatly accelerate in 2026 due to prediction markets’ utility in providing data on future events and investment hedging.

“This is no longer an early-adopter space – it is becoming a core pillar of the financial ecosystem, with billions flowing through weekly,” he said, adding:

“Institutions are increasingly using these markets to generate returns, hedge real-world risk, and understand what’s most likely to happen next. CNBC, CNN, Bloomberg, and Fox now regularly cite Kalshi markets alongside traditional market tickers.”

Clear Street’s CEO emphasized, however, that the firm is treading with caution amid a regulatory gray area for the prediction market space, alongside a host of lawsuits filed by state regulators across the US.

Related: Kalshi, Polymarket eye $20B valuations in potential fundraising: WSJ

The primary issues currently hanging over the industry are related to sports markets and whether or not they fall under the legal category of sports betting, and the potential for insider trading given the wide-reaching nature of markets offered on prediction market platforms.

Earlier this week, executives from major exchanges such as Nasdaq and CME called for regulatory clarity on prediction markets to support adoption in the US.

“Markets thrive when we have consistent regulation, and it allows investors, first of all, to be protected,” Nasdaq CEO Adena Friedman said at the FIA Global Cleared Markets Conference on Tuesday.

“We are going to the SEC, because the options markets are governed by the SEC, and we want to make sure that within the confines of the rule base that we operate in, we can create a construct that will work for investors,” she added.

The Commodities Futures Trading Commission is claiming to have primary oversight on the sector, while the Securities and Exchange Commission said it will also have a role to play.

Magazine: All 21 million Bitcoin is at risk from quantum computers

TLDR:

- Volkswagen to cut 50,000 jobs in Germany by 2030 following sharp profit decline.

- Chinese EV makers reduce Volkswagen’s market share in its most profitable region.

- Rising German energy and labor costs intensify pressure on Volkswagen operations.

- U.S. import tariffs add nearly €3bn in costs, impacting high-value German exports.

Volkswagen’s job cuts plan targets 50,000 positions in Germany by 2030 following a 44% drop in profits. The company faces intense competition from Chinese EV makers, rising energy costs, and U.S. import tariffs while transitioning toward electric vehicles.

Profit Decline and Cost Pressures

Volkswagen reported a net profit fall from €12.4 billion to €6.9 billion last year, representing a 44% decline. This marks the lowest post-tax profit since 2016, reflecting ongoing global market pressures.

The cuts will span the entire group, including Audi and Porsche, as the company focuses on efficiency. Chief executive Oliver Blume emphasized that operating conditions are now fundamentally different from previous years.

Finance chief Arno Antlitz stressed that the current profit margin is insufficient in the long term. Volkswagen aims to reduce costs rigorously while investing in software and electric vehicle technologies.

The company has already agreed with unions to cut over 35,000 jobs in a socially responsible manner. Executives estimate the restructuring will save €15 billion by 2030.

The remaining reductions are part of a broader strategy to maintain competitiveness amid declining profit margins and changing production dynamics.

Competition from China and EV Transition

China has historically been Volkswagen’s most profitable market. Domestic EV manufacturers like BYD now dominate with faster product cycles, competitive pricing, and strong technological integration.

Sales volumes for Volkswagen in China have declined as a result. Chinese EV makers are also entering European markets, increasing pressure on Volkswagen’s traditional base.

Electric vehicles require fewer components than combustion engine models, which reduces assembly complexity and the workforce needed.

Volkswagen’s focus on electrification has increased restructuring costs. Investments in battery production, software, and new EV models are substantial, making cost control essential.

These factors, combined with global market shifts, make workforce reductions unavoidable. Rising energy prices in Germany and high labor costs add further challenges.

Tariffs on U.S. imports also reduce competitiveness for German-produced vehicles. Volkswagen now faces the dual task of cutting costs while accelerating its transition to electric mobility to remain viable.

TLDR:

- Apparent demand remains negative, showing new supply exceeds market absorption for Bitcoin.

- CryptoQuant cycle indicators fall into deep bear territory despite price holding $65K–$75K.

- Long-Term Holder SOPR below 1 signals stress among historically strong investors.

- Sideways price action with fading rallies reflects a prolonged patience phase in the cycle.

Bitcoin mid-cycle consolidation is evident as on-chain metrics show weakening demand and investor fatigue. Apparent demand is negative, cycle indicators remain bearish, and long-term holder SOPR has slipped below 1, reflecting stress among historically resilient holders and sideways market behavior.

Apparent Demand Reflects Market Stagnation

Bitcoin mid-cycle consolidation is apparent through the behavior of apparent demand, an on-chain metric measuring how new supply is absorbed. It compares newly mined coins to changes in long-inactive supply entering circulation.

Positive readings indicate absorption, while negative readings suggest supply exceeds demand. Recent data shows mostly negative demand, with brief green spikes in late February failing to sustain.

This indicates that buyers are not consistently strong enough to maintain upward momentum. Such behavior is typical of mid-cycle consolidation, where early investors distribute holdings while new participants hesitate to buy at elevated prices.

Price action remains choppy, fluctuating between short rallies and pullbacks. Traders experience psychological strain as optimism during brief rallies is often followed by disappointment.

Markets show resilience despite negative demand, maintaining the $65K–$75K range, yet lacking sufficient capital inflow to trigger sustained upward trends.

Historical cycles indicate that these periods often precede renewed accumulation. The negative demand environment slowly tests investor patience, producing sideways movement rather than sharp corrections.

False breakouts and fading rallies become common during this stage, emphasizing the patience required to navigate consolidation.

Long-Term Holder SOPR Signals Growing Stress

Long-Term Holder SOPR measures whether holders sell at a profit or a loss, providing insight into market psychology. Recent readings show the 30-day EMA slipping below 1.0, signaling that even resilient holders are realizing losses.

This occurs during a mid-cycle compression phase where price stagnates and short-lived rallies fail to attract aggressive accumulation. The combination of negative apparent demand and SOPR below 1 reinforces market stagnation.

Price oscillates around the mid-$60K range, producing repeated false breakouts. Traders face uncertainty while long-term holders’ conviction is tested.

Coins gradually move from weaker hands to stronger holders, quietly setting the foundation for eventual accumulation once demand and confidence return.

This convergence of on-chain signals confirms Bitcoin is navigating a psychologically challenging mid-cycle consolidation, with patience as the primary tool for market participants.

Osmosis has proposed converting OSMO to ATOM and tightening Cosmos Hub integration, testing whether chain mergers can boost liquidity, governance, and valuations.

Summary

- Osmosis plan offers OSMO–ATOM conversion at a fixed rate over six months, with unclaimed ATOM returning to the Hub community pool.

- Proposal would bind Osmosis liquidity, security, and governance more tightly to Cosmos Hub, positioning ATOM as the primary base asset.

- The move sharpens Cosmos’ consolidation vs app‑chain sovereignty debate, putting OSMO and ATOM holders in control via governance votes.

Interoperable DEX Osmosis has put forward a sweeping proposal to convert OSMO into ATOM and migrate its core protocol more tightly into the Cosmos Hub, in one of the most aggressive consolidation moves yet seen in the Cosmos ecosystem. The plan would effectively bind Osmosis’s liquidity, security, and governance more directly to the Hub, while offering OSMO holders a time‑limited path into ATOM exposure.

Under the proposal, all circulating OSMO – excluding undeployed community pool tokens – could be converted to ATOM over a six‑month window at a fixed rate of 1.998 OSMO for 0.0355 ATOM. Holders who do not claim within that period would see the corresponding ATOM returned to the Cosmos Hub community pool, concentrating unclaimed value under Hub governance. The structure is explicitly designed to avoid permanent dangling liabilities, while forcing a clear decision from tokenholders on whether they want to align with the Hub or exit.

Strategically, the proposal aims to turn Osmosis from a largely independent app‑chain into a native liquidity engine for Cosmos Hub, potentially simplifying the stack for users and institutional players who view Cosmos as fragmented. By consolidating liquidity and security at the Hub layer, proponents argue that Cosmos can present a cleaner narrative to external capital: one core base asset (ATOM), one primary liquidity venue (Osmosis on Hub), and unified governance. For Osmosis, the move could widen its addressable user base if ATOM’s brand and distribution outweigh the loss of a standalone token.

The trade‑offs are significant. OSMO holders face dilution of protocol‑specific upside in exchange for broader ATOM exposure and tighter alignment with the Hub’s long‑term roadmap. Cosmos Hub, on the other hand, would be implicitly underwriting Osmosis’s future, importing not only its liquidity and fees but also its technical and governance risk. Success would push Cosmos further toward a “hub and spokes” model with ATOM at the center; failure would strengthen the case for app‑chain sovereignty over consolidation.

If passed, the proposal would mark a clear escalation in the ongoing debate over how Cosmos should compete with more monolithic ecosystems like Ethereum and Solana. It would also provide a live test of whether token conversions and protocol mergers can unlock higher valuations and deeper liquidity, or whether they simply shuffle risk and governance complexity from one balance sheet to another. For now, all eyes will be on how both OSMO and ATOM holders respond at the ballot box.

US-based prime brokers are quietly positioning themselves to give hedge funds and large institutions direct access to Kalshi’s prediction markets, a move that signals growing institutional interest in event-based betting markets. A Bloomberg report from March 11, 2026, indicates that Clear Street and Marex Group Plc are both lining up access for their clients in the near term. Clear Street, valued at over $12 billion, is expected to clear Kalshi trades as early as late March, while Marex, with a current valuation around $2.6 billion, plans a staged rollout over the coming months. The development underscores a broader shift as predictively driven markets gain traction among mainstream financial players, even amid regulatory ambiguity surrounding their legality and oversight.

Key takeaways

- Prime brokers plan to enable client access to Kalshi’s prediction markets within weeks, signaling rapid institutional onboarding.

- Kalshi’s leadership frames 2026 as a tipping point for institutional adoption, highlighting the market’s utility as data on future events and hedging tools.

- Hedge funds and other large institutions have begun approaching Kalshi contractors for direct market access, indicating a demand-driven expansion.

- Regulatory uncertainty remains a central hurdle, with debates over whether prediction markets fall under sports-betting rules and concerns about insider trading.

- Industry leaders, including Nasdaq and CME, are calling for clearer rules to support broader US adoption of prediction markets, signaling potential regulatory alignment or pathways forward.

Sentiment: Neutral

Market context: The push by prime brokers sits at the intersection of expanding interest in reputation-based forecasting markets and ongoing regulatory scrutiny. As major exchanges press for clarity, policymakers in the U.S. are weighing how prediction markets should be treated in relation to traditional securities and gaming rules, shaping the pace at which institutions can experiment with these platforms.

Why it matters

The entry of prime brokers into Kalshi’s ecosystem represents more than a new distribution channel. It signals a potential inflection point for prediction markets, where institutions view event outcomes as a tool for hedging risk, benchmarking forecasts, and generating returns. Kalshi’s CEO, in a LinkedIn post, has argued that institutional adoption will accelerate in 2026 as the market’s utility becomes clearer—citing the ability of these markets to provide data on future events and a framework for hedging real-world positions. This perspective aligns with broader industry narratives that such markets can function as a complementary data layer for traditional asset classes and macro strategies.

The practical appeal for institutions is twofold: first, the ability to hedge corporate or portfolio risk using event-based contracts; second, an opportunity to participate in markets that CNBC, CNN, Bloomberg, and Fox increasingly reference alongside conventional tickers. Yet, this enthusiasm exists within a regulatory gray zone, particularly around whether certain prediction market offerings resemble sports betting and how insider information may flow through these platforms. The tension between potential financial utility and compliance risk is a central theme shaping how quickly banks and brokers move from exploration to formalized access.

Industry participants have underscored that regulatory clarity is prerequisites for scalable adoption. Executives from Nasdaq and CME recently urged regulators to establish a clearer framework for prediction markets in the United States, arguing that consistent rules protect investors and foster market integrity. The CFTC has signaled its role in overseeing such markets, while the SEC has indicated it will also be involved in defining the boundaries for these instruments. The convergence of these regulatory positions will heavily influence whether institutional traction continues or stalls as cases and compliance questions proliferate across state and federal levels.

What to watch next

- Kalshi trade launches at Clear Street are expected in late March, with additional brokers like Marex rolling out in the ensuing months.

- Regulatory clarity on the classification of prediction markets—whether they fall under sports-betting or another regulatory category—will shape product design and participant eligibility.

- Key lawsuits and ongoing regulatory actions in the U.S. will test the resilience of prediction markets amid a landscape of diversified enforcement.

- Public statements from major exchanges and regulatory bodies, including updates from the CFTC and SEC, will indicate the pace of broader adoption and potential compliance requirements.

- Institutional hedging strategies using Kalshi and similar platforms may become more visible as fund managers assess risk-off and risk-on environments amid macro volatility.

Sources & verification

- Bloomberg report dated March 11, 2026, detailing prime brokers’ race to give Wall Street access to Kalshi’s prediction markets.

- LinkedIn post by Kalshi CEO Tarek Mansour discussing expected acceleration of institutional adoption in 2026 and the market’s broader utility.

- Reuters coverage of Nasdaq and CME executives calling for clearer rules to support prediction-market adoption in the U.S.

- Statements from the Nasdaq and CME discussions about regulatory alignment, and the CFTC/SEC roles in overseeing the sector.

- Related reporting mentioning Kalshi and Polymarket valuations and potential fundraising coverage in mainstream outlets.

Institutional access to Kalshi’s prediction markets gains momentum

Institutional appetite for prediction markets is expanding as prime brokers gear up to broaden access to Kalshi’s event-led contracts. The Bloomberg report paints a picture of late-March milestones for Clear Street, which is expected to clear the first Kalshi trade soon, and Marex, poised to follow in the coming months. The strategic move signals that major financial intermediaries view prediction markets not as speculative oddities but as components of a diversified risk management toolkit. In this view, there is a push to translate the insights from prediction markets into tradable risk-management signals for complex, multi-asset portfolios.

Kalshi’s leadership has framed 2026 as a turning point, arguing that the utility of prediction markets extends beyond speculation into practical data sources for forecasting and hedging. The company’s CEO, in a LinkedIn post, emphasized that institutional adoption will accelerate as more large players recognize the markets’ potential to quantify futures scenarios and hedge exposures. As he noted, the space is no longer an early-adopter niche but a core pillar of the financial ecosystem, with billions flowing weekly through these markets. This perspective is echoed by mainstream media outlets—CNBC, CNN, Bloomberg, and Fox—who regularly cite Kalshi alongside traditional market indicators, underscoring a shift in perception from novelty to necessity.

Nevertheless, the path forward is not without friction. Clear Street and Marex acknowledge a regulatory gray area surrounding prediction markets, alongside active litigation across the United States related to sports betting and other matters. Industry participants stress the importance of robust governance and clear rules to ensure investor protection and market integrity as adoption scales. The broader regulatory dialogue—pursued by exchanges and oversight bodies alike—aims to delineate permissible activities, address insider-trading concerns, and establish a stable framework within which institutions can transact with confidence.

In parallel, major exchanges have publicly called for regulatory clarity to facilitate US adoption. Nasdaq’s chief executive executive highlighted the need to bring options markets under a familiar rule framework, suggesting that a well-defined construct could enable investors to participate in a predictable regulatory environment. The SEC and CFTC have signaled their respective roles in overseeing emerging prediction-market activity, a development that could unlock more comprehensive product design while ensuring critical guardrails remain intact. The dynamic underscores a broader industry trend: practical finance increasingly sits at the intersection of regulatory alignment and innovative market structures, where data-driven decision-making and risk mitigation converge.

What it means for the market

For traders and investors, the potential mainstreaming of Kalshi and prediction markets offers an additional source of informational signals—complementing traditional data feeds with market-based expectations about future events. It may also prompt portfolio managers to incorporate event-based hedges into strategic plans, especially for scenarios with high impact on sectors or individual holdings. The regulatory dialogue surrounding these markets will be pivotal; a clear, harmonized framework could spur broader participation, elevate liquidity, and reduce friction for institutions seeking to deploy these instruments as part of diversified risk management strategies.

Stephen Gregory, a former compliance executive at CEX.IO and Gemini, has taken over as CEO of Binance.US, a crypto exchange that was once a target of a long-running SEC lawsuit.

Binance.US, the US affiliate of crypto exchange Binance, has named compliance lawyer Stephen Gregory as CEO as the company looks to re-expand in the country.

The company said on Wednesday that Gregory took over from former CEO Norman Reed on March 9, who will now serve in an advisory role.

Gregory is the former CEO of crypto exchange Currency.com and previously served as compliance chief and counsel at CEX.IO and as a compliance officer for Gemini.

“I am honored to lead the Binance.US team as we write the next chapter for the best platform for U.S. crypto investors,” Gregory said. “The Binance.US brand is extremely powerful, with a founder, Changpeng Zhao (CZ), who has continuously advocated to make the US the crypto capital of the world.”

Binance.US once sat in legal hot water for years after it was sued by the Securities and Exchange Commission in 2023, alleging it failed to register as an exchange, among other charges.

However, the SEC dismissed its case against the company with prejudice in May, adding to one of many crypto enforcement actions the agency has recanted under US President Donald Trump’s administration.

Binance.US hints at expanded offerings

It was also just over a year ago that Binance.US reinstated US dollar deposits and withdrawals after operating as a crypto-only exchange following the SEC lawsuit.

Related: Binance sues Wall Street Journal amid report of DOJ Iran probe

The past year has also seen the company launch products to expand its rewards and staking offering, as well as a referral program.

Binance.US said in its latest announcement that it plans to continue expanding its crypto staking product and will introduce services around decentralized finance and tokenized assets.

It follows other crypto exchanges that have begun to offer products outside of solely trading, offering digital assets tied to stocks and enticing customers with various ways to earn yield.

Magazine: When privacy and AML laws conflict — Crypto projects’ impossible choice

Ghana’s securities regulator has given the nod to 11 crypto trading platforms to participate in its new regulatory sandbox program, its first major step in support of crypto after passing a law to provide the local market with regulatory clarity in December.

Ghana’s Securities and Exchange Commission said on Tuesday that the 11 crypto platforms will operate under the country’s Virtual Asset Service Providers Act, adopted in December, which provides a regulatory sandbox framework for those companies to pilot their products and services in a controlled environment under the SEC’s oversight.

The companies admitted into the SEC’s regulatory sandbox are Africoin, Blu Penguin, Goldbod, Hanypay, Hyro Exchange, HSB Global, KoinKoin, Whitebits, Vaulta, XChain and Bsystem.

The sandbox program aims to spur crypto innovation while ensuring adequate consumer protection safeguards are in place. The participants will also need to comply with anti-money laundering and counter-terrorism financing standards.

The sandbox will last for 12 months, though companies that show market readiness and comply with all regulatory requirements can transition to a full license after six months.

Ghana said lessons from the pilot will shape the country’s future policies for the crypto market.

The VASP law stated that digital asset activities would fall under the SEC’s oversight and that industry players need to obtain a license or register with the Bank of Ghana or the SEC to operate in the country.

Foreign crypto companies are expanding into Ghana too

The new pilot comes after Blockchain.com said on Monday that it has expanded into Ghana as part of a push to broaden its presence in Africa.

A Blockchain.com spokesperson told Cointelegraph at the time that it would focus on expanding Ghana’s crypto payments infrastructure.

“Given how widely used mobile money is in Ghana, integration with the mobile money ecosystem is a key focus,” they said.

Related: Africa records highest stablecoin conversion spreads, data shows

Ghana is one of the larger economies on the African continent, which sees a high rate of crypto transactions under $1,000.

Crypto value received across the Sub-Saharan African region rose 52% year-on-year to over $205 billion between July 2024 and June 2025, blockchain analytics platform Chainalysis reported in September.

Nigeria dominates crypto activity, receiving over $92 billion over that period, while South Africa, Ethiopia, Kenya, and Ghana are the next-largest markets in the region.

Magazine: A ‘tsunami’ of wealth is headed for crypto: Nansen’s Alex Svanevik

Strive Asset Management (ASST) said Wednesday it has allocated $50 million of its corporate treasury to STRC, the variable-rate perpetual preferred stock issued by Strategy.

The investment represents more than one-third of Strive’s treasury reserves and reflects growing institutional interest in yield-generating securities linked to Bitcoin-focused treasury strategies, according to a company announcement.

The allocation makes Strive the latest company to add STRC to its balance sheet, following similar moves by companies including Prevalon Energy, Anchorage Digital and Oranjebtc, according to Strategy.

The development comes as Wall Street analysts begin covering companies built around Bitcoin treasury strategies. On Monday, investment bank B. Riley Securities initiated coverage of Strategy (MSTR) with a Buy rating, signaling expectations that the stock could outperform the broader market.

Strategy’s Nasdaq-traded STRC pays a floating dividend and trades publicly, allowing companies to hold it as a liquid treasury asset rather than cash or money market funds.

Data from Strategy’s dashboard shows STRC trading around $100, with a market capitalization of about $3.85 billion and around $90.6 million in daily trading volume. The variable dividend is currently at 11.5%.

“Many institutions maintain USD reserves as a buffer for dividend obligations and operational liquidity,” said Matt Cole, chairman and CEO of Strive, adding that allocating a portion of those reserves to instruments such as STRC may provide stronger yield dynamics than traditional money market funds while maintaining liquidity.

Strive is a structured finance company and asset manager that holds about 13,311 Bitcoin, ranking it as the 11th-largest corporate Bitcoin treasury, according to BitcoinTreasuries.NET data. The company’s Nasdaq-listed shares were up about 3.5% at last look on Wednesday.

Related: Strategy buys $1.3B in Bitcoin as holdings top 738,000 BTC

Inside Strategy’s ‘digital credit’ model and the STRC preferred stock

STRC is part of a category Strategy calls “digital credit,” securities designed to generate yield while allowing the company to raise capital linked to its Bitcoin treasury strategy.

Strategy raised about $2.5 billion in a July 2025 initial public offering of the preferred shares.

Strive’s $50 million purchase comes a day after Strategy recorded its largest issuance of STRC following changes to its at-the-market share sales program. The update allows a second sales agent to execute share sales outside regular US trading hours, easing a previous restriction that limited the program to one agent per trading day.

Data from STRC.live shows the company sold roughly 2.4 million STRC shares in a single day, with proceeds estimated to have funded the purchase of about 1,420 Bitcoin.

Strive has also issued its own digital credit instrument, SATA, a variable-rate perpetual preferred stock designed to generate floating yields tied to the company’s Bitcoin-per-share growth.

The shares, which launched in November 2025, currently offer yields of about 13% and have a market capitalization of roughly $319 million.

Magazine: All 21 million Bitcoin is at risk from quantum computers

The crypto market showed a muted reaction after US CPI data held at 2.4%, leaving investors watching Federal Reserve policy and Bitcoin price levels.

Summary

- US CPI held at 2.4% in February, matching forecasts and indicating easing inflation.

- The crypto market reaction remained muted, with Bitcoin stabilizing near $69K.

- Rate expectations remain steady as prediction platforms like Polymarket and Kalshi show low odds of near-term cuts.

The latest inflation data from the United States landed almost exactly where economists expected. February’s Consumer Price Index showed 2.4% annual inflation The report suggests price pressures are cooling, though not disappearing entirely.

The data was released by the U.S. Bureau of Labor Statistics on March 11. On a monthly basis, CPI rose 0.3%, slightly higher than January’s 0.2% increase. Core CPI, which excludes food and energy, increased 0.2% for the month and 2.5% year-over-year.

This is the lowest headline CPI reading since May 2025. Despite recent oil price swings linked to geopolitical tensions in the Middle East, inflation appears to be easing gradually.

Crypto market reaction remains muted

The crypto market reacted calmly after the report. Bitcoin (BTC) briefly dipped below $69,000 before recovering to around $69,500. The move was short-lived, and prices stabilized quickly.

Other major assets followed a similar pattern. Ethereum (ETH) and several large altcoins posted small gains or losses, while overall crypto market capitalization stayed relatively steady.

Inflation data often affects crypto indirectly. When inflation slows, markets tend to expect easier monetary policy from the Federal Reserve. Lower interest rates usually support risk assets such as cryptocurrencies because borrowing becomes cheaper and liquidity improves.

However, the latest CPI reading did not strongly shift expectations. Investors already expected a similar result, which limited the market reaction.

Interest rate outlook and market direction

The Federal Reserve is now widely expected to keep interest rates unchanged at its upcoming March meeting. Current projections place the federal funds rate in a 3.5% to 3.75% range, with markets assigning very low odds to an immediate rate cut.

Because of that, the crypto market may remain in consolidation mode in the short term. Analysts expect Bitcoin to trade between $65,000 and $72,000 while investors wait for clearer signals from macroeconomic data.

A break above the $72,000 resistance zone could re-open the path toward higher levels if liquidity improves and investor sentiment turns more positive. On the downside, renewed geopolitical stress or stronger inflation data could push prices back toward the $60,000 range.

Looking ahead, the next CPI report will be closely watched. Some forecasts suggest inflation could edge higher in March, potentially reaching 2.6% to 2.9%, partly due to energy price pressures.

For now, the crypto market appears to be in a holding pattern. Inflation is easing slowly, interest rates remain high, and traders are waiting for a stronger signal before placing bigger bets on the next move.

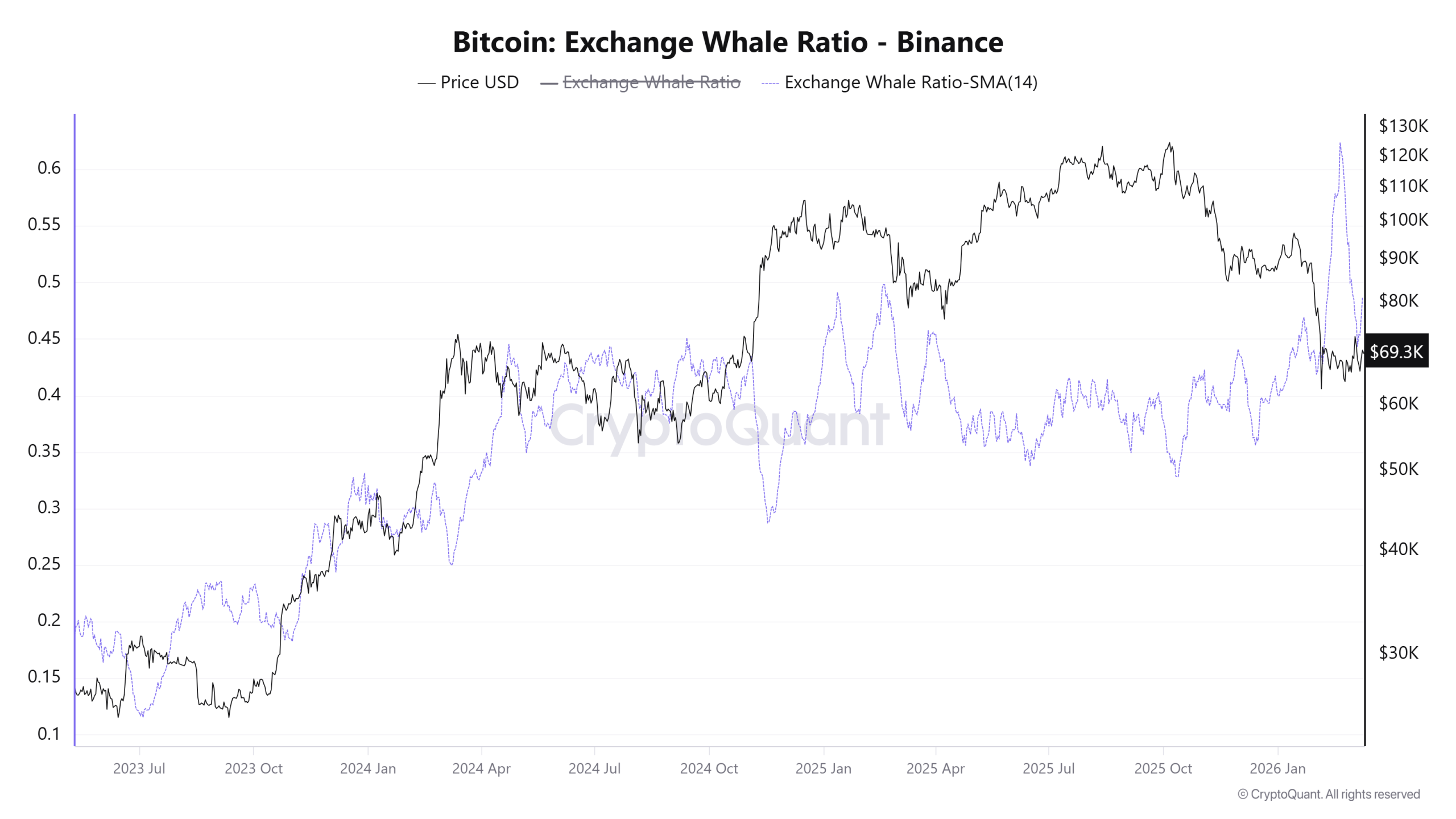

The next big breakout for Bitcoin (BTC) may hinge on changes unfolding across Binance’s exchange flows and derivatives activity.

Onchain data from the largest cryptocurrency exchange currently show a cooling of whale deposits, rising BTC withdrawals, and growing futures dominance, which may influence the next direction for Bitcoin’s price.

Bitcoin whale activity cools after February spike

The Bitcoin exchange whale ratio on Binance, which measures the ten largest inflows relative to total exchange deposits, surged above 0.60 during early February, indicating strong selling by whales.

Since then, the 14-day moving average has settled closer to 0.45, levels seen throughout 2024 and 2025. The drop in large inflow spikes indicates that fewer dominant sell-side transfers are entering Binance during the current range phase.

The price action during this period is also important to note. Bitcoin stabilized in the $65,000-$72,0000 region after its February decline rather than extending the drop.

Related: Bitcoin will need 17% of ‘store of value’ market to hit $1M: Bitwise

Meanwhile, Crypto analyst CW noted that some whales may still be accumulating. Bitcoin’s cumulative volume delta (CVD) indicator shows persistent whale buying during the recent consolidation.

At the same time, whales are showing signs of accumulation. Crypto analyst CW said Bitcoin’s Cumulative Volume Delta (CVD) shows buying from large traders as BTC price consolidates.

The CVD tracks the net difference between aggressive market buys and sells. Higher readings while the price moves sideways may indicate larger participants absorbing supply without allowing the price to accelerate quickly.

BTC outflows on Binance rise as futures dominate spot trading

The exchange netflow on Binance has also changed since mid-February. The total netflow tracks the difference between coins entering and leaving exchanges.

The 14-day moving average moved deeper into negative territory at -1,151 BTC on March 11, showing a sustained wave of Bitcoin withdrawals from the platform. This indicates that more BTC is leaving the exchange, reducing the supply immediately available for selling.

Derivatives activity has expanded alongside these flows. Crypto analyst Maartunn said that the futures-to-spot trading volume ratio on Binance has climbed to roughly 5.3, its highest level since October 2023, meaning futures markets have more than five times the spot volume.

Higher futures activity may signal that traders are using leverage and bracing for BTC price volatility.

Meanwhile, Coinbase research points to improving spot demand. The exchange noted that the spent output profit ratio (SOPR) for short-term holders has turned higher since late February.

Related: Bitcoin faces ‘highly volatile’ setup as bulls eye return to $80K by month-end

According to the exchange, the recovery in short-term holder SOPR above 0 across both Bitcoin and Ether (ETH) indicates that recent demand has been strong enough to absorb selling pressure from newer traders. This has helped stabilize the BTC price in the current range.

These factors highlight the reason behind Bitcoin’s current consolidation phase, which should result in sharper repricing if BTC solidifies the $70,000 level as support.

However, failure to break the $72,000 resistance over the next few days or weeks may confirm a bull trap and trigger the next leg down if history repeats.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Adam Sandler’s Most Gripping Performance Is A High-Anxiety Thriller On Hulu

Games Inbox: Is buying physical video games becoming more popular?

US stock market remains calm, even as oil prices rise

-

Business6 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

Tech7 days ago

Tech7 days agoBitwarden adds support for passkey login on Windows 11

-

News Videos3 days ago

News Videos3 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Ann Taylor

-

Crypto World2 days ago

Crypto World2 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech20 hours ago

Tech20 hours agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Sports6 days ago

Sports6 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Politics6 days ago

Politics6 days agoTop Mamdani aide takes progressive project to the UK

-

Business1 day ago

Business1 day agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Sports4 days ago

Sports4 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports4 days ago

Sports4 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

NewsBeat9 hours ago

NewsBeat9 hours agoResidents reaction as Shildon murder probe enters second day

-

NewsBeat6 days ago

NewsBeat6 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Entertainment5 days ago

Entertainment5 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

Business3 days ago

Business3 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business20 hours ago

Business20 hours agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat2 days ago

NewsBeat2 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech3 days ago

Tech3 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Tech7 days ago

Tech7 days agoACIP To Discuss COVID ‘Vaccine Injuries’ Next Month, Despite That Not Being In Its Purview

-

Business2 days ago

Business2 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs