Crypto World

Ripple is becoming a bank. What it means for XRP

A conditional national trust bank charter, a pending Federal Reserve master account, and a string of acquisitions in brokerage, payments, and treasury. Ripple is assembling a full regulated-finance stack. The benefits flow first to its stablecoin and the company itself. What is left for XRP is the question.

Summary

- Ripple has assembled a full regulated-finance stack: a conditional national trust bank charter, a pending Federal Reserve master account bid, and acquisitions in prime brokerage, payments, and treasury services.

- The charter and master account primarily benefit RLUSD, Ripple’s stablecoin, whose reserves would sit under federal and state oversight, not XRP directly.

- A national trust bank cannot take ordinary deposits or carry federal deposit insurance, so the real prize is direct access to Federal Reserve payment rails and custody of its own stablecoin reserves.

- For XRP, the benefit is indirect: a more legitimate, bank-grade Ripple strengthens the whole ecosystem and XRP’s role as a bridge asset, but it creates no direct token-demand mechanism.

- This is the same pattern that defined XRP through 2026, in which Ripple’s wins flow first to the company and RLUSD, with the token benefiting slowly, if at all.

Ripple is turning itself into a bank, or something very close to one, and it is doing it methodically.

Over the past year the company won conditional federal approval to operate a national trust bank, applied for a Federal Reserve master account that would give it direct access to the central bank’s payment systems, and bought its way into prime brokerage, payments, and corporate treasury services through a series of acquisitions.

Add the dollar stablecoin it already issues, the 70-plus regulatory licenses it holds around the world, and a fresh European license that lets it passport services across 30 countries, and the picture is unmistakable.

A company once known mainly for a cross-border payments network and a controversial token is assembling the full apparatus of a regulated financial institution.

For XRP holders, who have watched the token grind sideways near a dollar through a year of Ripple triumphs, the natural question is what all of this means for them.

The honest answer is more complicated, and more sobering, than the headlines suggest, because almost every piece of Ripple’s banking build benefits the company and its stablecoin first, and the token only indirectly.

This piece works through Ripple’s transformation into a regulated financial institution and what it actually delivers for XRP. It covers the banking stack Ripple is assembling, what a national trust bank can and cannot do, the real prize of a Federal Reserve master account, why the charter is mostly a stablecoin story, what genuinely accrues to XRP, the bull case within the bank build, and what holders should watch.

The goal is to separate the real significance of Ripple becoming a bank, which is considerable for the company, from the wishful assumption that everything good for Ripple is automatically good for the token, which 2026 has repeatedly shown to be false.

A payments company is turning into a financial institution

Take the full measure of what Ripple has built, because the strategy only becomes clear when you see the pieces together.

The foundation is a conditional charter to operate a national trust bank, granted by the Office of the Comptroller of the Currency, the federal regulator that supervises national banks. The OCC conditionally approved Ripple National Trust Bank alongside other crypto firms in a broader wave of national trust bank approvals.

That federal approval matters because it moves Ripple deeper into the regulated banking perimeter without turning it into an ordinary retail bank.

A subsequent rule expanded what such trust banks are allowed to do, turning what would have been a narrow custody license into something with real operational scope, including digital-asset custody, stablecoin reserve management, and certain payment services.

On top of the charter, a Ripple subsidiary applied for a Federal Reserve master account, the account that would connect Ripple directly to the central bank’s payment rails.

And around that regulatory core, Ripple has been buying capabilities: a prime brokerage, a payments business, and a corporate treasury-services firm, each acquisition adding a piece of the institutional-finance stack.

Layer in the rest and the ambition is obvious. Ripple issues a dollar-pegged stablecoin that has grown past $1 billion in market value.

It holds dozens of regulatory licenses across jurisdictions, and it recently secured preliminary European authorization that lets it offer regulated services across the entire European Economic Area.

That is where Ripple’s European license fits into the larger build. The company is not only chasing U.S. banking access; it is trying to make its regulated-finance stack portable across major markets.

Taken individually, any one of these is a notable corporate step. Taken together, they describe a single, coherent strategy: to become the institutional infrastructure layer for crypto-native finance.

Ripple wants to be a regulated entity that banks and corporations can trust to custody assets, manage stablecoin reserves, settle payments, and connect to both the traditional financial system and the blockchain world.

Ripple is not dabbling in banking. It is building a bank-grade financial institution deliberately, piece by piece.

The question for a token holder is where, in all of this carefully assembled machinery, XRP actually fits.

What a national trust bank is, and what it is not

Before assessing what the charter means for XRP, it is worth being precise about what a national trust bank actually is, because the word “bank” carries connotations the charter does not deliver.

A national trust bank is not a retail bank. It cannot take ordinary deposits, cannot offer checking or savings accounts, and does not carry federal deposit insurance, the protection that backs ordinary bank deposits.

What it can do is custody assets, provide fiduciary and trust services, manage reserves, and, under the expanded rule, handle digital-asset custody and certain payment-related functions.

Headlines that say “Ripple becomes a bank” are gesturing at something real, but they compress away an important distinction.

That distinction matters for understanding the charter’s purpose. Ripple’s trust bank exists primarily to serve Ripple’s stablecoin business.

Its core planned function is to custody and manage the reserve assets that back the stablecoin, which today are held through a separate trust entity, and to provide custody to institutional clients.

By bringing reserve management in-house under a federal charter, Ripple gains tighter control, removes reliance on third-party custodians, and obtains a regulatory standing that few stablecoin issuers can match: oversight at both the federal level, through the national chartering regulator, and the state level, through New York’s financial regulator.

That dual supervision is a genuine selling point to institutions weighing whether to trust Ripple’s rails.

This is also why the fight over trust charters matters. Senator Elizabeth Warren and banking groups have challenged the idea that crypto firms with OCC trust charters should be treated like bank-grade institutions, arguing that they could act like crypto banks without the same restrictions.

The crypto industry has pushed back. The Digital Chamber called on the OCC to uphold crypto trust bank charters for firms including Coinbase, Ripple, Circle, and BitGo, arguing that the charters are part of bringing digital assets into regulated finance rather than keeping them outside it.

But notice what the trust bank does not do. It does not custody XRP for the benefit of XRP holders, does not create any obligation to buy or hold the token, and does not make XRP a bank deposit or a regulated bank instrument.

It is, at its heart, infrastructure for the stablecoin, which is the recurring theme of Ripple’s entire banking build.

The real prize: a Federal Reserve master account

The most consequential piece of Ripple’s banking strategy is the one furthest from being secured: a Federal Reserve master account.

A master account is the account a financial institution holds directly with the central bank, and it is the gateway to the core of the financial system.

It allows direct settlement through the central bank’s payment networks, the same rails the largest banks use, and direct access to base money rather than balances held at a commercial bank.

For a stablecoin issuer, the prize is enormous. With a master account, Ripple could hold the reserves backing its stablecoin directly at the central bank, the safest possible place, eliminating the counterparty risk of relying on private banks and giving institutions far greater confidence in the stablecoin’s solvency and redemption safety.

That is why custody and reserve safety matters so much in this story. Stablecoins are only as trusted as the assets backing them, the institutions holding those assets, and the transparency around redemption.

The catch is that no crypto-native firm has ever received full access of this kind on ordinary terms, and the bar is extraordinarily high.

The central bank has historically been reluctant to extend master accounts to non-traditional institutions. Uninsured trust banks face the most stringent levels of review, and previous attempts by crypto-adjacent firms to win access have often failed or taken years.

Ripple’s subsidiary has applied, and the application remains pending, with no public timeline and no clear signal of when or whether the central bank will act.

Approval would be genuinely transformative. It would mark a deeper integration between a crypto-native company and the core U.S. financial system, and it would dramatically strengthen the institutional credibility of RLUSD.

But it is far from assured. Even in the optimistic case, the direct beneficiary is again the stablecoin and the company’s settlement capabilities, not the token.

A master account would let Ripple hold stablecoin reserves at the central bank and settle through its rails. It would not, by itself, create demand for XRP.

The prize is real, and the prize is mostly about everything except the token.

Why this is mostly a stablecoin story

Step back and a clear pattern emerges from every piece of Ripple’s banking build: it is, overwhelmingly, a stablecoin story.

The trust charter exists primarily to custody and manage stablecoin reserves. The master account, if granted, would primarily benefit the stablecoin by letting its reserves sit at the central bank.

The European license primarily expands where Ripple can offer regulated payment and stablecoin services. The acquisitions in brokerage, payments, and treasury primarily build out an institutional settlement and services business in which the stablecoin is the natural cash leg.

Ripple’s dollar stablecoin has grown past $1 billion, expanded across multiple blockchains, and won approvals in multiple jurisdictions. The banking apparatus is being constructed largely to support and legitimize it.

That is why the RLUSD the bank serves is the center of the story. A stablecoin is useful to institutions precisely because it is designed to hold a steady dollar value while moving across crypto rails.

Ripple’s own reserve-transparency page also shows why this matters. The company is trying to make RLUSD look less like an experimental crypto product and more like a regulated dollar instrument with transparent backing, regular attestations, and bank-grade custody.

This is the same dynamic that defined XRP through 2026, when Ripple’s marquee bank deals and settlement milestones ran through its stablecoin and ledger while the token captured little beyond a negligible network fee.

As previously reported, this is why Ripple wins bypass the token. Ripple can deepen its institutional footprint while XRP still waits for direct, measurable token demand.

The banking build is that dynamic taken to its logical conclusion. Ripple is constructing a regulated financial institution whose central purpose is to make its stablecoin the most trusted, most institutionally credible dollar token in the market, and to build a settlement and custody business around it.

XRP is part of the broader ecosystem, but it is not the thing the bank is for.

A holder hoping that the charter, the master account bid, and the acquisitions would translate into direct demand for the token is, once again, watching the wrong variable.

The value of all this machinery flows first to Ripple the company and to the stablecoin it is built to serve, exactly as Ripple’s own communications have acknowledged in noting that the banking progress is unlikely to move the token’s price directly or immediately.

So what do XRP holders actually get?

If the bank build is mostly about the stablecoin, the fair question is whether XRP holders get anything at all.

The honest answer is yes, but indirectly and slowly. The benefit to XRP runs through legitimacy and ecosystem strength rather than any direct mechanism.

As Ripple becomes a regulated, bank-grade financial institution, the entire ecosystem it anchors gains credibility in the eyes of the banks and corporations Ripple wants as customers.

A more trusted Ripple makes every part of its stack, including the ledger on which XRP lives and the role XRP can play, more palatable to institutional users.

The argument, which Ripple and many holders make, is that demand for one asset in an ecosystem can lift others in the same stack, and that a Ripple wired into the core of the financial system is a Ripple better positioned to drive real-world use of XRP as a bridge asset over time.

This indirect benefit is not nothing, and it would be a mistake to dismiss it. XRP’s most plausible long-term role is as a bridge asset that moves value between currencies in settlement.

A Ripple with a federal charter, a master account, and a credible institutional settlement business is a Ripple with more opportunities to route that kind of settlement in ways that touch the token.

But the benefit is conditional, gradual, and unguaranteed, three qualities that make it very different from the direct, immediate boost holders often hope for.

XRP does not become a bank deposit, a stablecoin, or a regulated instrument through any of this. It remains a separate, volatile asset whose demand depends on whether Ripple’s growing institutional infrastructure eventually channels real settlement volume through it.

The competing path is obvious: the same settlement volume could instead keep flowing through RLUSD, which is better suited to settlement precisely because it does not move in price.

The banking build improves the odds that Ripple can win regulated institutional business someday. It does not make that business flow through XRP now, and it does not create token demand on its own.

The bull case within the bank build

In fairness to the optimistic view, there is a coherent bull case for XRP buried inside Ripple’s banking transformation, and it deserves a clear statement.

The strongest version goes like this: Ripple is methodically removing every reason an institution might hesitate to build on its rails.

The charter answers the custody and reserve-management question. The master account, if granted, answers the reserve-safety question at the highest possible level.

The acquisitions answer the brokerage, payments, and treasury questions. The licenses answer the regulatory question across jurisdictions.

As those barriers fall one by one, Ripple becomes a place where serious institutions can conduct serious volume. In a world where Ripple is running large-scale regulated settlement, the case for using XRP as the neutral bridge asset between currencies strengthens, because the infrastructure to do it at scale finally exists and is trusted.

Pair that with the token’s other tailwinds, including the regulatory clarity from its resolved legal status, the spot exchange-traded funds gathering assets, and the prospect of federal legislation codifying its commodity classification, and the bull case becomes clearer.

That is where the legislation that could codify XRP fits in. If the CLARITY Act turns XRP’s commodity treatment into durable federal law, it could make institutions more comfortable using the token where it has a genuine settlement role.

In that version of the future, XRP sits inside a maturing, increasingly bank-grade ecosystem at exactly the moment that ecosystem becomes capable of institutional-scale activity.

If even a fraction of the settlement flowing through a fully built-out Ripple touches XRP as a bridge, the demand could be meaningful, and it would arrive on top of a token that has already cleared its regulatory hurdles.

This is a real argument, and it is why the banking build is truly good news for the long-term XRP thesis even though it is not a direct catalyst.

The caveat, as always, is the word “if.” The bull case depends on Ripple choosing and managing to route settlement through the token rather than through the stablecoin, and the entire pattern of 2026 suggests the stablecoin keeps winning that role.

The infrastructure being built is real. Whether XRP is wired into it is the open question.

What XRP holders should watch

For a holder trying to judge whether Ripple’s banking transformation will ever translate into token demand, the analysis points to a few specific signals worth tracking, none of which is another charter or acquisition headline.

The first is the Federal Reserve master account decision.

If granted, it would be a landmark for Ripple and the stablecoin, and it would mark the company’s deepest integration into the financial system. Over time, that expands the surface area where XRP could be used.

If denied, a key piece of the institutional thesis stalls.

Either way, it is the most consequential pending item, and its outcome shapes everything downstream.

The second and more important signal is whether XRP actually appears in the settlement flows of Ripple’s bank-grade business, as opposed to the stablecoin doing all the work.

This is the variable that decides the entire question. If Ripple’s institutional settlement increasingly routes through XRP as a bridge asset, generating real, recurring token demand, then the banking build will finally have reached the token.

If, as has been the pattern, the stablecoin carries the settlement while XRP captures only a fee, then the bank is a Ripple and stablecoin story with XRP riding the halo of legitimacy but not the flows.

The third signal is the broader regulatory picture, particularly whether federal legislation codifies XRP’s status, which would compound the legitimacy the banking build provides.

The honest synthesis is that Ripple becoming a bank is a major, genuine achievement that strengthens the company, the stablecoin, and the long-term credibility of the whole ecosystem.

For XRP specifically, it improves the odds without delivering the goods.

The token’s payoff depends on a future choice, to run regulated settlement through XRP, that Ripple has not yet shown it will make.

Until it does, the bank is being built for everything except the token, and the token, as it has all year, waits.

Frequently asked questions

Is Ripple actually becoming a bank?

Sort of, but with important caveats. Ripple won conditional federal approval to operate a national trust bank and applied for a Federal Reserve master account, and it has acquired prime brokerage, payments, and treasury businesses. But a national trust bank is not a retail bank: it cannot take ordinary deposits, offer checking or savings accounts, or carry federal deposit insurance. It is a specialized institution for custody, fiduciary services, and reserve management. So Ripple is building a bank-grade regulated financial institution, but one focused on custody and stablecoin reserves instead of traditional deposit-taking banking.

What is the Federal Reserve master account and why does it matter?

A master account is an account held directly with the central bank, giving direct access to its payment rails and to base money, the same access the largest banks have. For Ripple, it would let the company hold its stablecoin’s reserves directly at the central bank, the safest possible location, eliminating reliance on private banks and boosting institutional confidence in the stablecoin. No crypto-native firm has ever been granted full access of this kind on ordinary terms, the review is stringent, and Ripple’s application is pending with no timeline. Approval would be transformative for the company and stablecoin, though not a direct catalyst for XRP.

Does Ripple’s banking push help XRP?

Indirectly and gradually, not directly. The charter and master account primarily benefit Ripple’s stablecoin, whose reserves they would custody and secure. XRP does not become a deposit, a stablecoin, or a regulated instrument. The benefit to XRP runs through legitimacy: a bank-grade Ripple strengthens the whole ecosystem and improves the odds that XRP is eventually used as a bridge asset in regulated settlement. But that is conditional and slow, not the direct demand boost holders often hope for, and Ripple itself has acknowledged the banking progress is unlikely to move the token’s price immediately.

Why does the stablecoin benefit more than XRP?

Because the entire banking build is designed around the stablecoin. The trust charter exists mainly to custody and manage stablecoin reserves. The master account, if granted, would let those reserves sit at the central bank. The acquisitions build a settlement business in which the stablecoin is the natural cash leg. A stablecoin is suited to settlement precisely because it holds a steady value, while XRP’s volatility makes it less suitable for that role. So Ripple’s regulated infrastructure naturally channels value to the stablecoin, with XRP benefiting only as part of the broader, more credible ecosystem.

What is the bull case for XRP in all this?

The bull case is that Ripple is methodically removing every reason an institution might hesitate to use its rails, through the charter, the master account bid, the acquisitions, and the licenses. As those barriers fall, Ripple becomes capable of large-scale regulated settlement, and the case for using XRP as a neutral bridge asset between currencies strengthens because the trusted infrastructure to do it finally exists. Combined with XRP’s regulatory clarity, its ETFs, and possible federal legislation, the bull case is that XRP sits inside a maturing, bank-grade ecosystem just as that ecosystem becomes capable of institutional-scale activity. The caveat is whether settlement actually routes through XRP instead of the stablecoin.

What should XRP holders watch next?

Three things. First, the Federal Reserve master account decision, which would mark Ripple’s deepest integration into the financial system and expand where XRP could be used, or stall a key part of the thesis if denied. Second, and most important, whether XRP actually appears in the settlement flows of Ripple’s institutional business, generating real token demand, as opposed to the stablecoin doing all the work. Third, the broader regulatory picture, especially whether federal legislation codifies XRP’s commodity status. The token’s payoff depends on Ripple choosing to route regulated settlement through XRP, a choice it has not yet shown it will make.

This article is information, not investment advice. Cryptocurrency is volatile, and regulatory approvals, corporate plans, and figures reflect reporting available as of June 26, 2026, which can change quickly. Verify current data from primary sources before making any decision.

Arcus, a decentralized exchange backed by Robinhood Crypto, has expanded its onchain trading offering on Robinhood Chain by launching tokenized stocks alongside perpetual futures. The development signals how quickly DEX infrastructure is evolving to cover traditional market exposure, not just crypto-native assets.

According to an announcement shared with Cointelegraph, Arcus began trading tokenized equities and perpetual contracts on Tuesday. The platform also previously launched spot markets when Robinhood Chain went live on July 1, including stock token access across a self-custodial trading model.

Key takeaways

- Arcus launched tokenized stocks and perpetual futures on Robinhood Chain on Tuesday, building on earlier spot markets.

- The exchange supports more than 95 stock tokens and offers perpetual markets linked to equities, ETFs, commodities, indexes, and crypto assets.

- Arcus uses a self-custodial approach where users keep control of their wallets, with wallet integration via Privy and connectors such as MetaMask and Ledger.

- Paxos-issued USDG is positioned as Arcus’s primary collateral and settlement asset.

- Arcus restricts stock tokens in multiple regions, including the US, Canada, and the UK, underscoring ongoing regulatory fragmentation for tokenized securities.

Arcus adds tokenized equities and perpetual futures

Arcus is positioning itself as a bridge between onchain trading and traditional capital markets. The new offering includes tokenized versions of well-known US company stocks—such as Nvidia, Tesla, Apple, Microsoft, Meta, Google, and Amazon—alongside perpetual markets tied to equities and other offchain reference categories.

In addition to stock-linked perpetuals, Arcus’s product slate reportedly extends to perpetual markets associated with exchange-traded funds, commodities, indexes, and crypto assets. The company frames the expansion as part of a broader push to “onboard” real-world assets into decentralized trading workflows.

Arcus previously rolled out spot markets shortly after Robinhood Chain launched. Cointelegraph previously reported that Robinhood Chain saw more than 70 million in ETH bridged during its first week, and Arcus’s early spot rollout used that foundation to bring tokenized exposure to the chain.

A self-custody model built around Privy and existing wallets

A defining feature of Arcus is its self-custodial structure. Rather than depositing assets into a centralized exchange custody system, Arcus describes a trading setup where users keep control of their crypto wallets. That matters for traders because self-custody shifts responsibility for key management and reduces reliance on an intermediary to hold funds.

To support onboarding and wallet management, Arcus uses Privy, a wallet infrastructure provider. The platform enables sign-ups via email or social logins, then routes trading activity through wallet-based authorization.

For users who already hold crypto, Arcus supports connecting existing self-custodial wallets, including MetaMask, Ledger, and WalletConnect. The company also indicates support for additional Ethereum-compatible wallets.

Arcus’s trading system is also designed around stablecoin settlement. Paxos-issued USDG is described as the primary collateral and settlement asset for the platform, tying equity-linked trading to a familiar stablecoin infrastructure rather than requiring users to rely solely on native crypto volatility.

Restrictions highlight uneven regulation for tokenized stocks

While tokenized stocks are a core part of Arcus’s expansion, the company is explicit about where those instruments can’t be offered. Arcus states that its stock tokens are unavailable in the US, Canada, the UK, and other restricted jurisdictions.

Cointelegraph contacted Arcus for clarification on the restrictions, but did not receive a response by publication time. Even without additional detail, the regional exclusions reinforce a central theme in tokenized real-world assets: regulatory standards for securities representations vary widely, and product access often becomes the first battleground.

In markets including the US and UK, regulators have been scrutinizing how blockchain-based representations of traditional assets fit within existing financial rules. Key questions typically include who effectively holds or controls the asset, how ownership is defined, and what market structure is created when trading happens through token contracts.

Arcus’s approach suggests it is attempting to scale onchain trading while limiting exposure to jurisdictions where compliance requirements may be more complex or where the classification of tokenized securities remains unsettled.

Competition accelerates for onchain RWA infrastructure

Arcus’s move lands in the middle of a broader sector race: crypto firms and financial platforms are competing to build infrastructure for tokenized real-world assets (RWAs). The push isn’t limited to token issuances—DEX-style trading venues, perpetual markets, and settlement mechanisms are becoming just as important as the onchain representation of the underlying assets.

As Robinhood Chain-based products expand, the DEX landscape is also seeing other efforts to bring traditional financial instruments onchain. Cointelegraph previously reported that platforms including Coinbase-backed Base have been exploring ways to deliver tokenized equities and related products onchain, showing that the “tokenized markets” strategy is no longer confined to a single ecosystem.

There is also a thematic tension in this transition. Tokenized markets depend on regulatory permissions to determine where products can be offered, yet onchain infrastructure is often built to be globally accessible. Arcus’s launch, with explicit geographic exclusions, illustrates how companies may prioritize compliance routing while still using public blockchain networks as the underlying execution layer.

The launch adds to the growing list of platforms trying to translate traditional market participation into decentralized trading patterns—particularly for users seeking exposure to equity-linked references without using legacy brokerage interfaces.

For investors and traders, the immediate watch-items are straightforward: how Arcus evolves its regional availability, whether it expands beyond stock tokens into additional derivatives liquidity over time, and how settlement and custody design choices—centered on self-custody and USDG—hold up as regulatory scrutiny intensifies across major markets.

A single Robinhood transaction just moved 200 million DOGE, and the market wants to know who’s behind it. Dogecoin trades above $0.073, holding modest daily gains. However, the real story sits beneath the surface. Open interest has climbed above $1.08 billion, while derivatives activity continues to heat up. That combination usually means volatility is at the door.

Meanwhile, traders are watching a thick liquidation cluster around $0.074. If bulls push through, short sellers could fuel a sharp squeeze. If momentum fades instead, late buyers may find themselves trapped. Either way, the next move looks unlikely to be a quiet one.

Naturally, Elon Musk’s name has returned to the conversation. There is no evidence linking him to the transaction, and no wallet data confirms his involvement. Still, every large Dogecoin buy raises the same question. Given Musk’s history of moving DOGE with little more than a post, the rumor mill rarely needs much encouragement.

For now, the market has more questions than answers. Bitcoin’s next move could easily determine Dogecoin’s direction, while any surprise social media post could add fuel to the fire. Until the mystery buyer steps into the spotlight, traders will keep guessing. And if history has taught Dogecoin anything, sometimes the biggest rallies start with a single unexplained transfer.

Discover: The Best Token Presales

Can Dogecoin Price Reclaim $0.075 and Force a Short Squeeze This Week?

DOGE is hovering near $0.074, sitting around the 50% Fibonacci retracement level. The memecoin recently reclaimed this area but still needs to confirm it as support. That makes the level worth watching.

The latest liquidation heatmap outlines the battlefield clearly. Support sits between $0.0710 and $0.0726, while resistance stretches from $0.0754 to $0.0796. The Supertrend indicator also caps the near-term upside around $0.0796. However, spot demand and on-balance volume remain soft. That mismatch often leaves leveraged longs and shorts walking on thin ice.

The bullish path starts with DOGE holding above $0.074. If buyers keep control, short liquidations could fuel a quick move toward $0.0755 and $0.076. Nothing goes up forever, but meme coins rarely send a calendar invite before they sprint.

The base case remains a familiar grind. DOGE could continue ranging between $0.071 and $0.074 until a fresh catalyst arrives. On the other hand, losing $0.071 would weaken the setup. That could send the price back toward $0.070 as leveraged positions unwind.

Longer term, analyst Trader Tardigrade still points to cycle targets of $0.653, $0.70, and even above $1.25. Those projections depend on another full crypto bull cycle instead of the current market structure. For now, they work better as long-range markers than actionable trading levels.

Trade Memecoins like DOGE on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

Maxi Doge Eyes Early-Stage Upside as DOGE Tests Critical Resistance

DOGE at $0.074 with a $1 billion OI overhang is a trade, not a position. The asymmetry that existed at lower prices has compressed. Even a successful squeeze to $0.076 represents roughly 4% upside from here, meaningful on leverage, limited in spot. Traders looking for a larger risk-reward multiple are scanning earlier on the curve.

Maxi Doge ($MAXI) is an ERC-20 meme token built around a trading community thesis: the 240-lb canine juggernaut persona embodies 1000x leverage culture, and the project channels that into structured community mechanics.

The presale has raised closer to $5 million at a current price of just $0.000283, with a dynamic staking APY live for holders. Differentiating features include holder-only trading competitions with leaderboard rewards, a Maxi Fund treasury allocated to liquidity and partnerships, and meme-first marketing that leans into gym-bro culture without apology.

Research Maxi Doge before the next stage reprices.

Discover: The Best Crypto to Diversify Your Portfolio

The post Is Elon Musk Behind the 200 Million DOGE Buy as Open Interest Tops $1 Billion? appeared first on Cryptonews.

Crypto World

Bitcoin, ether rally on Clarity progress report, Asian chip stock rebound: Crypto Markets Today

The crypto market rallied on reports suggesting the final hurdle for the long-awaited U.S. Clarity Act may have cleared.

Eleanor Terrett, host of Crypto in America, posted on X that President Donald Trump had agreed to a crucial ethics provision for the crypto market structure bill. The specific language has been shared with a group of Senate Republicans, marking a significant step forward for the legislation.

The ethics provision is a major sticking point in holding back the bill’s passage through Senate. The legislation aims to provide a definitive regulatory framework, clearly distinguishing between digital commodities and securities to end years of enforcement-led oversight.

Bitcoin rallied above $66,000, gaining 3.5% in 24 hours to its highest in just over a month. Othe cryptocurrencies, including ether (ETH), BNB and XRP (XRP) posted even larger gains. Among industry, the standout is the CoinDesk DeFi Select Index, which surged 9%.

Additional tailwinds came from Asia, where the selloff in semiconductor stocks that dragged crypto lower last week reversed, fueling to a broad risk rally.

Gate Europe’s CEO Giovanni Cunti says the Markets in Crypto-Assets Regulation (MiCA) has raised the long-term operating burden for firms already authorized to serve EU customers, warning that some licensed providers may eventually decide they cannot afford the compliance costs.

Speaking to Cointelegraph’s Chain Reaction on Monday, Cunti argued that MiCA’s stricter requirements have tightened competition—particularly for newcomers—and that the market may now be too small for some businesses to sustain the resources required to operate under the EU framework.

Key takeaways

- MiCA compliance costs are increasingly viewed as a barrier for some licensed crypto-asset service providers (CASPs), according to Gate Europe’s CEO.

- The July 1 end of MiCA’s 18-month transition period forced a retrenchment in some services across Europe, while licensed firms continued under the new regime.

- Regulatory burden may push certain startups and projects to launch outside the EU to preserve room for product iteration and growth.

- Despite the pressure, ESMA’s CASP authorizations continue to expand, though at a slower pace since the transition deadline.

- As the market contracts from “thousands” of operators to “hundreds,” remaining providers may benefit from customer migration rather than losing users.

MiCA’s transition deadline changed who can serve EU users

MiCA is the EU’s comprehensive regulatory framework for crypto assets. The bloc’s 18-month transition period ended on July 1, meaning crypto firms serving EU customers needed authorization under MiCA or otherwise had to stop offering regulated services.

Cointelegraph previously reported that the deadline triggered service changes from several exchanges in parts of Europe while firms sought MiCA approvals. A notable example is Binance, which Cointelegraph said was unable to secure a MiCA license before the deadline. The result was a patchwork of restrictions depending on jurisdiction—an early sign that the authorization process would determine who could continue operating as usual.

Gate Europe warns some licensed firms may not endure

Cunti’s central concern is not simply that compliance is costly, but that the costs and staffing requirements needed to operate continuously under MiCA could outweigh the revenue potential for some firms—especially those that acquired a license expecting the broader market to remain large.

He told Cointelegraph that “quite a few” firms that obtain MiCA licenses may ultimately lack the capacity to sustain the “cost and the resources” required “in the long term.”

For investors and operators, the implication is straightforward: in a regulated environment with ongoing obligations, survival increasingly depends on business scale and risk management—not only on obtaining a license once. That can favor larger, better-capitalized platforms and reduce room for smaller providers that cannot spread compliance overhead across higher volumes.

Regulation may drive projects to other jurisdictions

Beyond business continuity, Cunti also suggested that MiCA’s stricter approach could affect where new crypto products and projects choose to launch. He said MiCA strengthens investor protections, but also leaves less space for innovation compared with jurisdictions that apply lighter regulatory requirements.

That, he argued, may lead some teams to choose non-EU markets as a first stop. “We may need to be prepared that some projects, possibly some important projects, may be looking at other jurisdictions with different guidelines,” Cunti said.

At the same time, the EU framework still appears to be gaining institutional traction. ESMA continues to add CASPs to its public register, indicating that the compliance pathway exists—though Cunti’s comments point to a tougher economic reality for firms after authorization.

ESMA licensing continues, but momentum is slower

According to ESMA updates cited by Cointelegraph, the number of companies authorized under MiCA has kept rising. On Friday, ESMA added 14 crypto-asset service providers to its register, bringing the total to 294. Cointelegraph noted that this followed the addition of 37 firms in ESMA’s first update after the July 1 transition deadline.

While the steady increase shows that regulatory onboarding is continuing, Cunti framed the broader effect as a reshaping of competition rather than a simple expansion of the market. He pointed to the difference between the pre-MiCA landscape—when, in his view, there were “thousands of operators”—and the post-deadline environment, which is now closer to “hundreds.”

From a market-structure perspective, this distinction matters. A shrinking number of compliant providers can reduce choice and increase regulatory concentration, but it can also redirect demand. Cunti suggested that customers still want access to EU-regulated services and therefore may migrate toward the remaining compliant platforms rather than leaving the ecosystem entirely.

“So definitely there is a big opportunity for all of us,” he said, adding that “there is an ongoing migration because customers do not want to lose access to this market.”

ESMA’s role also remains active as regulators oversee how major venues adapt. Earlier coverage from Cointelegraph referenced an ESMA warning that brought Binance’s EU service changes into scrutiny—another signal that MiCA implementation is ongoing, not a one-time switch.

What to watch next

The key question after MiCA’s transition is whether authorization translates into sustainable operations. Readers should watch for evidence that some licensed firms scale down, exit, or consolidate—alongside continued ESMA licensing updates and any further regulatory scrutiny over how exchanges restrict services in different EU regions.

In attempting to modernize and better meet its customers’ needs, MoneyGram has partnered with the Stellar network, which has underpinned many of the company’s blockchain initiatives over the past five years. But the company has also started exploring other ecosystems: while Stellar remains a core partner, MoneyGram has also become a validator on Solana and Tempo. For MoneyGram, the immediate payoff isn’t speculative crypto activity, it’s replacing legacy financial rails.

Today’s cross-border settlement still largely depends on banking hours and weekday processing. Blockchain-based infrastructure, Soohoo argued, enables real-time settlement around the clock, reducing operational costs while improving the customer experience.

“We believe if we do it right, we can achieve all three,” he said, referring to helping customers save time, effort and money. Instant settlement also allows MoneyGram to lower back-office costs, savings the company hopes to eventually pass on through lower prices. Currently, MoneyGram’s fees start at $1.89 and vary depending on what country you send them to.

Soohoo doesn’t believe consumers need to understand the technology powering those improvements. He compared blockchain to the processors inside Apple’s iPhone.

“I can’t tell you what processor is inside my iPhone,” he said. “I just know it’s faster.” In the same way, he argued, remittance customers care about whether money arrives quickly and reliably, not whether it traveled over a blockchain.

July has been historically a positive month for bitcoin and this edition hasn’t disappointed so far. The cryptocurrency began the month on the wrong foot, dipping below $58,000 for the first time in nearly two years, but it rebounded swiftly in the following weeks.

Earlier today, it rocketed past $66,000 for the first time in over a month, gaining over $8,000 since that July 1 low. Here are some of the possible reasons behind it.

Whale and ETF Accumulation

As June was coming to an end and it became known that it would be a highly painful month for the asset with a nosedive of over 20%, we outlined several factors that had to change in July for a price resurgence. One of them was the ETF inflows. The financial vehicles went on a violent eight-week withdrawal-only streak, which was finally snapped a couple of weeks ago.

Moreover, investors continued to pour funds into the ETFs, which ended two weeks in the green in a row for the first time in months. July 20 extended the streak as the funds attracted almost $227 million.

The second major reason for the price revival is whale behavior. Data shared by CryptoQuant indicated that large market participants holding between 1,000 and 10,000 BTC increased their 60-day net accumulation to roughly 66,700 units, which is close to the recent record seen a month ago.

“This is the cohort’s strongest accumulation reading since February 17, when net accumulation briefly exceeded 106,000 BTC.”

News From the US

The third reason has a more macro scent. It came a week ago when the US CPI numbers for June were announced, showing softer-than-expected inflation rates. BTC rallied immediately after the news went live as lower inflation reduced the pressure on the Fed to hike interest rates. Similar market conditions are regarded as beneficial for risk-on assets like bitcoin.

Last but perhaps most importantly at the moment comes a development on the CLARITY Act. After the odds of approval dropped toward 30% just days ago, reports emerged that the White House had agreed on an ethics package for the key legislation and sent the language to certain Senate republicans for further validation.

Although the details are still scarce, industry experts believe this is a major step in the right direction for the bill, and it increases the chances for a 2026 approval.

The post 4 Key Reasons Behind Bitcoin’s (BTC) Rally Above $66K appeared first on CryptoPotato.

Prism, a token that pays a share of trading fees to everyone who holds it, is relaunching on a new Ethereum contract after disclosing that an attacker spent most of July siphoning off nearly 40% of those fees. The original PRISM token, which the project is now abandoning, plunged about 91% in the… Read the full story at The Defiant

Citigroup has reaffirmed its KOSPI price target of 10,000, projecting that the recent sell-off in South Korean stocks could soon reverse.

The index has shown notable volatility in 2026, forcing the Korea Exchange to trigger sidecars and circuit breakers across repeated sessions.

Why Citi Sees a Buying Opportunity For KOSPI

The KOSPI has slid into a broader decline since setting a record closing high of 9,114.55 on June 22. Citi remains bullish on a revival.

The bank’s analysts told clients in a Monday note that the market’s headwinds have peaked. Citi argues that strong economic fundamentals and a market-friendly policy mix can drive the recovery.

“We think the recent share price pullback of KOSPI equities, led by KR memory suppliers, is more of a technical correction driven by market-wide profit-taking and therefore could represent a potential buying opportunity,” the analysts stated.

Meanwhile, the index posted another red session on Monday, dropping more than 4%. It reversed sharply on Tuesday. The surge tripped a buy-side sidecar at 12:41 p.m., a curb that briefly suspends program buy orders when KOSPI 200 futures rise 5% or more for at least a minute.

The KOSPI closed Tuesday up 3.56% at 6,747.95. From that level, Citi’s 10,000 target implies a 48% gain, and it sits nearly 10% above the previous closing record.

Follow us on X to get the latest news as it happens

Notably, volatility remains the KOSPI’s defining feature. Volatility on the index has topped 60% this year, almost double Japan’s Nikkei 225 and higher than Bitcoin (BTC).

The turbulence forced the Korea Exchange to trigger circuit breakers seven times through mid-July, up from none in 2025.

Tuesday’s rebound closed part of the distance Citi flagged. Whether it holds remains to be seen.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Citi Keeps 10,000 KOSPI Target Despite Market Selloff appeared first on BeInCrypto.

Crypto World

Pi Network (PI) Rises 25% in a Week But Warning Signs Point to Another Possible Pullback

Pi Network’s PI has emerged as one of the strongest performers in the top-100 crypto ranking over the past week, outpacing countless major digital assets.

However, this rally may prove short-lived and could be followed by another sharp pullback in the near future.

PI Flashes Green

In mid-July, the native token of the controversial crypto project tumbled to a new all-time low of around $0.07, while its market capitalization slipped well below the $1 billion psychological level.

Since then, though, the bulls have stepped in, and now PI trades at around $0.093 (per CoinGecko), representing a roughly 25% increase on a weekly basis.

The exact catalyst of the resurgence remains unclear since Pi Network’s team has been rather silent over the past few days and has not unveiled any new ecosystem updates. Of course, one potential factor could be the overall revival of the crypto market, where Bitcoin (BTC) crossed $66,000, while Ethereum (ETH) aims to reach $2,000.

Many analysts are now optimistic that PI can post further gains. X user Crypto With Gopal claimed that the asset is printing a “Falling Wedge” after a prolonged downtrend where selling pressure is fading, and the price is “squeezing toward the wedge apex.” They believe this formation often signals that momentum is shifting back to the bulls.

“Buyers are quietly defending support while lower highs continue to compress. A strong breakout above the wedge resistance could spark a sharp relief rally as sidelined buyers step in. If bulls reclaim the trendline with volume, PI could be setting up for a major expansion move. Market sentiment is cautiously turning bullish,” they added.

Prior to that, OxNeena argued that after months of selling pressure, PI has finally shown signs of accumulation. They believe that if buyers step in, this could mark the beginning of a strong trend reversal, with $0.20 and $0.32 set as potential upside targets.

Brace for Potential Drop

PI investors should remain cautious, as previous pumps like this have often been abruptly ended by another major move downward. The prolonged bear market and the concerning condition of the entire crypto sector reinforce those fears.

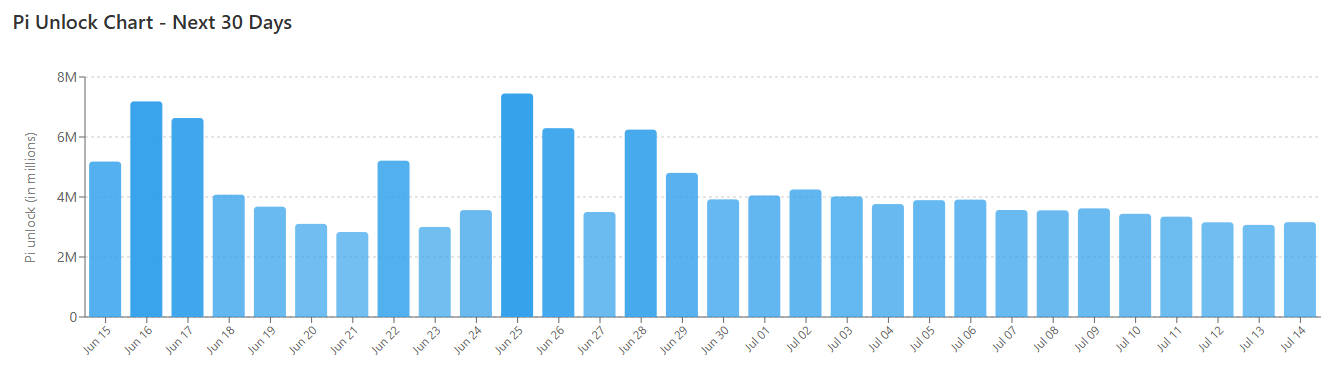

Meanwhile, the PI community must take other factors into account, including the upcoming token unlocks. Around 127.5 million coins are set for release in the next 30 days: a development that doesn’t guarantee a price drop but increases selling pressure.

- PI Token Unlocks, Source: piscan.io

X user Travladd told their nearly 500,000 followers on X that PI is “looking cooked,” noting that there is too much supply. “Won’t catch me buying into any relief rally,” they added.

The post Pi Network (PI) Rises 25% in a Week But Warning Signs Point to Another Possible Pullback appeared first on CryptoPotato.

US spot Bitcoin ETFs recorded their fifth consecutive day of inflows, their longest streak since May, as the flagship cryptocurrency crossed $66,000. Strong inflows suggest price action and investor sentiment could be stabilizing after a period of sustained outflows.

Bitcoin (BTC) has regained momentum over the past seven days, reclaiming $65,000 on Monday and extending its gains on Tuesday to surpass $66,000. BTC registered an increase of over 3% in the past 24 hours and is currently trading around $66,158.

Spot Bitcoin ETFs Extend Inflows

Spot Bitcoin ETFs registered their fifth consecutive day of inflows, recording $226.80 million on Monday, the highest single-day inflow since July 6, as institutional demand returned. The ETFs have recorded a total net inflow of $727.3 million over the five-day streak and posted back-to-back positive weeks for the first time since May.

BlackRock’s IBIT recorded the highest inflows on Monday with $116.5 million, followed by ARK Invest’s ARKB with $72.7 million. Fidelity’s FBTC recorded $24.1 million in net inflows, while Bitwise’s BITB added $8.8 million and VanEck’s HODL registered $1.8 million in net inflows. Morgan Stanley’s MSBT recorded inflows of $6.9 million. However, Grayscale’s Bitcoin Trust recorded $45.4 million in outflows. Those outflows were offset by Grayscale’s Mini Bitcoin Trust, which recorded $41.4 million in net inflows.

Institutional Interest Returning?

Consistent inflows have returned after a period of sustained outflows as institutional investors pulled capital from Bitcoin ETFs. Analysts believe the inflows suggest returning institutional interest in Bitcoin and their preference for ETFs for crypto exposure. However, Simon-Peter Massabni, the head of business development at XS, believes the inflows indicate easing sell-side pressure rather than returning institutional interest and demand. According to Massabni, BTC must break and hold above $65,000 to strengthen the bullish argument.

Richard Galvin, executive chairman of DACM, believes the inflows suggest Bitcoin was beginning to find a bottom. BTC is trading above $66,000, a level it must sustain to convince the market of a sustained uptrend. The flagship cryptocurrency has largely traded between $60,000 and $65,000 in recent weeks amid geopolitical and macroeconomic headwinds.

Damien Loh, CIO at Ericsenz Capital, warned of rising inflation and interest rate hikes if the conflict between the US and Iran continues dragging on. Loh believes this could make institutional investors reluctant to put capital in BTC and other risk assets. However, he added that if the CLARITY Act passes before the August recess, it could provide the catalyst needed to push prices higher.

Strategy Building $3.23 Billion Warchest

Rising ETF inflows come amid Strategy’s efforts to improve its liquidity. The Bitcoin treasury company sold some of its Bitcoin holdings for the first time since June 2022, as it attempts to mitigate the impact of BTC’s recent decline and meet its dividend obligations. BTC is down nearly 50% from its October 2025 high of $126,000, and recently sold $263.5 million in common stock. However, it did not use the proceeds from that sale to purchase additional BTC. Instead, the company used the funds to bolster its dollar reserve.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Walk First, Then Snack, Matty Benedetto’s Step-Counting Lockbox Makes You Earn Every Bite

NEW BEST GTA 5 Money Glitch! $4,000,000 Every 6 Minutes (2026 UPDATED)

Transfer news LIVE: Arsenal FC open Guimaraes talks, medical booked; Rogers to Chelsea; Man Utd, Liverpool latest

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

NEW BEST GTA 5 Money Glitch! $4,000,000 Every 6 Minutes (2026 UPDATED)

#abhaypatil #trading #dothingsyoudontwanttodo #cryptotrading #stockmarket #crypto

MONEY WILL FLOW LIKE CRAZY! (How To Manifest Success & Riches) | Dr Joe Dispenza

-

NewsBeat5 days ago

NewsBeat5 days agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread – Corporette.com

-

Politics3 days ago

Politics3 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Politics6 days ago

Politics6 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Crypto World6 days ago

Crypto World6 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Crypto World4 days ago

Crypto World4 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Crypto World3 days ago

Crypto World3 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Business5 days ago

Business5 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics2 days ago

Politics2 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Entertainment6 days ago

Entertainment6 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Crypto World4 days ago

Crypto World4 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World5 days ago

Crypto World5 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Crypto World6 hours ago

Crypto World6 hours agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Business5 days ago

Business5 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Tech14 hours ago

Tech14 hours agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech11 hours ago

Tech11 hours agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

Tech7 days ago

Tech7 days agoDark Secrets Emerge When Jailbreaking LLMs

-

NewsBeat4 days ago

NewsBeat4 days agoRegistration is now open for March for Men with Kev 2026

-

News Videos7 days ago

News Videos7 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

NewsBeat1 day ago

NewsBeat1 day agoUnregistered fitter used Gas Safe logo on business flyers

You must be logged in to post a comment Login