Crypto World

SBI to Buy Bitbank in $289M Deal, Forming Japan’s Largest Crypto Exchange

Japan’s SBI Holdings has moved to fully take control of the Bitbank cryptocurrency exchange in a deal valued at 46.7 billion yen (about $289 million), building a larger, more consolidated crypto trading platform under one regulated umbrella. The agreement follows an initial announcement made in May, which positioned the combination as a potential scale-up into the country’s largest crypto exchange.

On Thursday, SBI said its wholly owned subsidiary, SBICAH, will acquire Bitbank shares from Bitbank CEO Noriyuki Hirosue and other shareholders, then participate in a third-party share allotment. After that, Bitbank will buy back shares currently held by MIXI and Ceres, leaving SBI with 100% indirect ownership. SBI expects the transaction to close around October, subject to regulatory approval.

Key takeaways

- SBI will pay 46.7 billion yen to gain full indirect control of Bitbank, aiming to accelerate its position in Japan’s regulated exchange market.

- The restructuring plan includes a third-party share allotment and a Bitbank share buyback from MIXI and Ceres, with SBI ending at 100% indirect ownership.

- SBI forecasts the combined group will manage about 1.1 trillion yen in assets under custody and reach roughly 2.92 million crypto accounts, based on end-April figures.

- Bitbank’s trading has been relatively muted for months, with CoinGecko data showing daily volume typically below $50 million over much of the past four months.

- SBI says the enlarged exchange footprint could add another distribution channel for stablecoins, tokenized assets, and onchain financial products.

Why SBI’s Bitbank control matters to Japan’s crypto market

For investors and market participants, the main significance of the Bitbank deal is not only consolidation, but also capacity—SBI is trying to connect an exchange-led customer base with a broader digital-asset product lineup. SBI’s stated goal is to expand its regulated crypto exchange operations and customer reach, which it argues could support distribution of stablecoins, tokenized assets, and other onchain financial services.

In effect, the acquisition is designed to strengthen SBI’s role across multiple layers of Japan’s crypto ecosystem: trading infrastructure, custody and account management, and settlement or product distribution. That matters in a market where regulatory clarity and institutional participation are key constraints—and where distribution channels can be as important as underlying technology.

How the transaction will be structured

SBI’s announcement outlines a multi-step process. First, SBICAH will acquire Bitbank shares from Hirosue and other existing shareholders. It will then subscribe to shares issued through a third-party share allotment. After those steps, Bitbank is expected to repurchase the shares held by MIXI and Ceres.

The result, SBI says, is that the group will hold 100% indirect ownership once the buyback completes. SBI expects the overall deal to close around October, but only after it receives regulatory clearance—an important reminder that Japan’s exchange and stablecoin frameworks rely on approvals and compliance review.

Scale effects: custody and accounts, plus the trading backdrop

Alongside the ownership changes, SBI provided combined operating figures for the enlarged group. According to SBI, combining Bitbank with SBI VC Trade would bring the group to about 1.1 trillion yen in assets under custody and roughly 2.92 million crypto accounts, using data from the end of April.

SBI also claims that this combined business would rank first among Japanese crypto exchanges by assets under custody and among the largest by account numbers. While the exact competitive landscape can shift with market activity and reporting periods, the direction of travel is clear: SBI is targeting scale metrics that are closely watched by institutions, compliance teams, and potential partners.

Trading liquidity is another piece of the picture. CoinGecko data cited by SBI indicates Bitbank’s daily trading volume has generally stayed below $50 million for most of the last four months. The exchange’s activity is heavily concentrated in key fiat pairs—BTC/JPY accounts for 39.5% of volume, with XRP/JPY and ETH/JPY each at 19.7%.

That concentration underscores why integration could matter: combining Bitbank with SBI VC Trade may help SBI manage customer routing, product access, and onchain distribution more efficiently—especially if volumes are expected to respond to broader cross-platform adoption.

SBI’s broader push: stablecoins and tokenized financial markets

The Bitbank acquisition fits into a wider strategy by SBI to extend from trading into digital-asset settlement and tokenized finance. SBI frames the move as additional infrastructure for its evolving product suite.

Earlier this year, SBI and Startale Group unveiled Strium, a layer-1 blockchain intended to support around-the-clock trading and settlement for tokenized equities and real-world assets. In parallel, SBI has been expanding stablecoin-related capabilities in Japan.

Most recently, SBI said that on Wednesday, SBI and Startale launched JPYSC, a yen-pegged stablecoin. SBI stated that the token is issued by SBI Shinsei Trust Bank and distributed by SBI VC Trade. Initially, JPYSC circulation is limited to transfers within SBI VC Trade accounts, with public blockchain circulation planned after resolving outstanding legal and tax conditions.

On the same day, Ripple and SBI Group also launched Ripple USD (RLUSD) in Japan via SBI VC Trade. SBI said RLUSD became available to both institutional and retail customers after receiving approval under Japan’s regulatory framework for foreign-issued stablecoins.

Taken together, these developments highlight why exchange ownership is strategically valuable. If distribution for stablecoins and tokenized instruments depends on access points that regulated exchanges can provide, acquiring a bigger platform and integrating accounts can directly influence adoption timelines—at least from the perspective of product rollout and customer onboarding.

Investors should watch two things next: whether SBI clears the remaining regulatory steps to complete the Bitbank acquisition around October, and how the combined operations evolve in practice—particularly whether SBI can translate scale in accounts and custody into stronger liquidity and smoother distribution for JPYSC, RLUSD, and future tokenized offerings.

Balaji Srinivasan’s Network School is looking to plant a new campus in Kazakhstan after regulatory pressure in Malaysia forced its Johor operation to halt. The move comes via a memorandum of understanding (MoU) between Kazakhstan’s Ministry of Digital Development, Innovation and Aerospace Industry and Srinivasan, signaling a rapid attempt to preserve the project’s cross-border footprint.

The Kazakhstan agreement positions Network School for a fresh base following actions that disrupted its local operations in Johor. Kazakhstan has been actively courting technology and digital-industry activity, including plans for a Central Asia “crypto city” in Alatau—an environment that Network School appears eager to tap.

Key takeaways

- Network School signed an MoU in Kazakhstan, potentially creating its first local campus there.

- Malaysia’s Johor authorities revoked the business license of NSO Malaysia Sdn Bhd, the operator behind Network School’s Forest City-linked presence.

- Malaysia Digital status is under immediate review, since the operator’s Malaysia Digital recognition is tied to compliance with local and federal laws.

- Srinivasan says the Kazakhstan campus will focus on talent attraction, including expedited visas and streamlined redomiciliation.

Kazakhstan MoU offers a fallback for Network School’s expansion

According to a ministry statement, Kazakhstan’s Ministry of Digital Development, Innovation and Aerospace Industry signed an MoU with Balaji Srinivasan to establish the first Network School campus in the country. The memorandum was signed by Zhaslan Madiyev on behalf of the ministry and Srinivasan on the Network School side.

For the project, the timing matters. Network School’s Kazakhstan plan appears framed as continuity after setbacks in Malaysia. The article also notes that Kazakhstan has been positioning itself as an emerging technology hub, and references ambitions such as a Central Asia “crypto city” in Alatau—suggesting regulators and policymakers there may be more receptive to experiments that sit near the boundary between technology policy and digital-asset culture.

Srinivasan described the new campus as a place designed to accelerate onboarding for participants. In a post dated Tuesday on X, he said the campus would offer a “haven for global techno-optimism,” including expedited visas, streamlined redomiciliation, and active recruitment of talent.

Malaysia regulatory action escalates: license revocation and Malaysia Digital review

Network School’s Kazakhstan pivot follows multiple regulatory developments in Malaysia. On Tuesday, the Iskandar Puteri City Council (MBIP) revoked the business license of NSO Malaysia Sdn Bhd, which operates Network School. The revocation was linked to alleged breaches of licensing conditions and premises-use requirements.

The Malaysia Digital Economy Corporation (MDEC), which oversees the “Malaysia Digital” program, then announced immediate steps to revoke the operator’s Malaysia Digital status. Malaysia Digital recognition is granted to eligible technology and digital companies and, as described in the source coverage, can come with incentives such as tax benefits, flexibility around ownership, and the ability to employ local and foreign workers.

Crucially, the program also requires licensees to comply with local and federal laws. With NSO Malaysia’s license revoked, MDEC’s move indicates the regulator is treating the Malaysia Digital designation as contingent on continued lawful operations.

Johor politics and immigration scrutiny widen the dispute

Beyond the licensing issue, the dispute has also pulled in higher-level political attention. The source reports that Onn Hafiz Ghazi, Chief Minister of Johor, urged Malaysia’s federal authorities to continue investigating whether Network School violated immigration laws. He framed Johor as a “strategic entry point” due to the state’s proximity to Singapore, arguing that any weaknesses or misuse of the immigration system should be addressed promptly and firmly.

This matters for Network School because its model—bringing in global “digital nomads” and hosting a dense community of talent—depends on predictable pathways for visas, residency changes, and compliance. When immigration questions enter the picture, the risk is not only reputational; it can directly affect members’ ability to travel, work, or remain in the country.

The source also indicates that Srinivasan pushed back on reports that Network School was shutting down. On Friday, he denied the closures, saying the project had received two notices: one requiring a sign’s wording to be changed, and another related to a coworking setup created by joining two adjacent units. He said one side of that arrangement had a valid license while the other did not, and claimed the group had a remedial period to address both issues.

According to Srinivasan, members were otherwise unaffected during that remedial window. Cointelegraph reported that it reached out to Srinivasan and Network School for comment, but the article’s account focuses primarily on the regulatory steps already taken by the local council and MDEC.

What changes—and what remains uncertain—if Network School relocates

The Kazakhstan MoU suggests Network School wants to avoid a prolonged pause by securing an alternative operating base quickly. But an agreement is not the same as full operational clearance. Readers should view the MoU as a framework for collaboration and campus establishment, while awaiting more detailed information on licensing, immigration logistics, and the practical timeline for opening.

Still, the contrast between Malaysia and Kazakhstan is instructive. In Malaysia, the dispute moved from licensing conditions to a broader discussion involving Malaysia Digital compliance and immigration law scrutiny. In Kazakhstan, the present reporting centers on cooperation and talent-attraction features—expedited visas and streamlined redomiciliation—language that typically signals a focus on easing administrative friction.

For investors, builders, and community operators watching the “network state” concept, the underlying takeaway may be how regulatory pressure in one jurisdiction can accelerate relocation tactics. A community anchored in one place can gain momentum, but it is also exposed: local licensing, premises rules, and immigration enforcement can rapidly reshape operating reality. Network School’s next steps in Kazakhstan will therefore function as a real-world test of whether the administrative environment for techno-nomad hubs can be replicated across borders.

As the Kazakhstan campus planning progresses, the most important thing to watch is how the MoU translates into concrete permits and member onboarding on the ground—particularly on visas and local compliance. Until then, Network School’s situation remains a moving target shaped by how regulators interpret licensing, premises usage, and immigration obligations in each country.

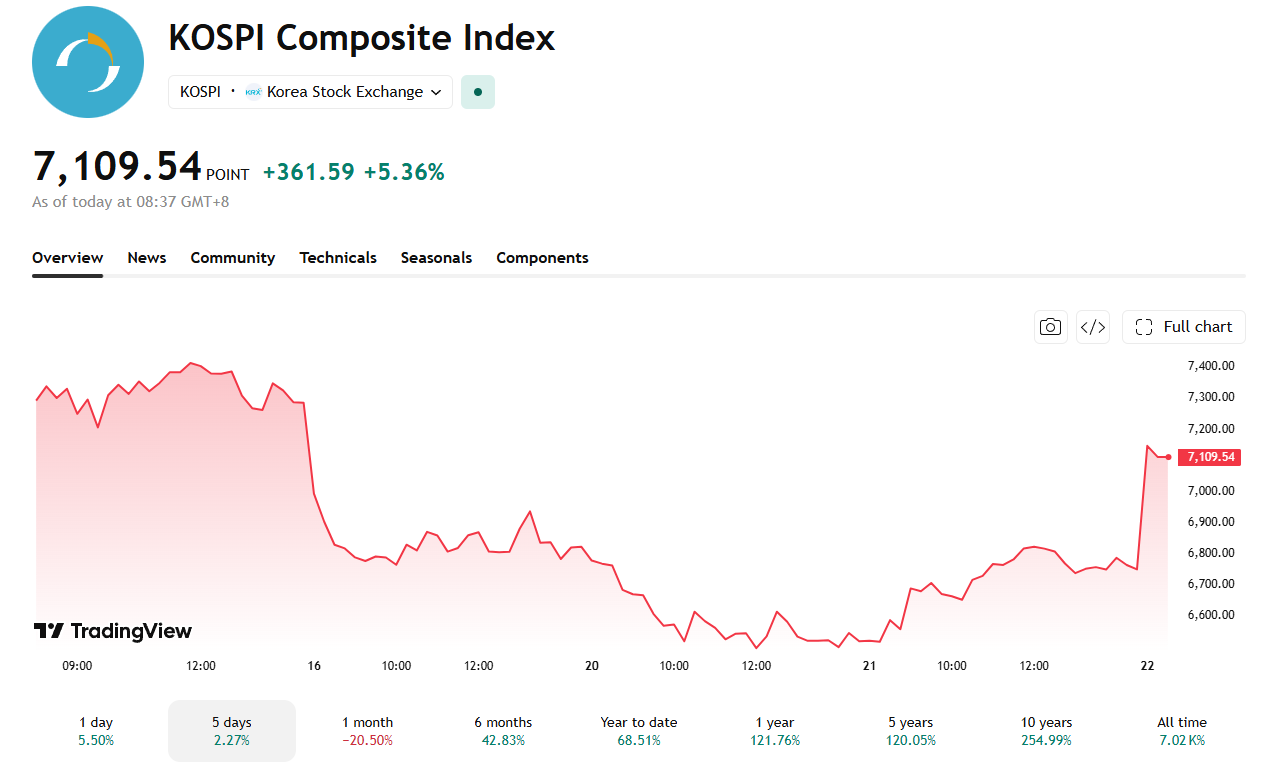

South Korea’s Kospi surged over 5% to a high of 7,164 on Wednesday’s early trading, extending its rebound from an artificial intelligence stock selloff. Asian chipmakers led the gains for a second straight session.

Japan’s Nikkei 225 added near 2% to 67,524.22, also in early trading. The rally builds on Tuesday’s rebound across Asian markets.

Samsung, SK Hynix Lead the Recovery

The gains extend July 21’s rebound, when the Kospi jumped 3.6% and the Nikkei rose 3% after a number of days trending downwards. Chipmakers are looking to pull the Kospi back from a bear market slide that AI valuation fears caused earlier this month.

Samsung Electronics surged reversed its downward trend on Tuesday while SK Hynix, the memory chipmaker, gained also started gaining, recovering from its sharp sidecar plunge earlier this month.

The Kospi is still down more than 20% over the past month, even after gaining over 50% year-to-date. Investors had locked in profits on AI bubble concerns.

Wall Street Also Jumps at Semiconductors

Wall Street added its own momentum on Tuesday. The Nasdaq 100 posted its best session in three weeks, and a key semiconductor gauge jumped 5.2%, according to Bloomberg.

Analysts remain split on whether the bounce will last.

“The recent correction appears more consistent with a healthy reset following a parabolic advance than a fundamental breakdown in the AI investment theme.”

Adam Turnquist, LPL Financial

Nearly 20% of S&P 500 companies by market value report earnings this week. Alphabet and Tesla release results Wednesday. Those results will test whether the chip rally can hold.

The post Kospi Jumps 5% as Asian Chipmakers Rebound From AI Selloff appeared first on BeInCrypto.

S&P Dow Jones Indices and Pantera Capital have launched the S&P Pantera Digital Asset Index, a new crypto benchmark that excludes Bitcoin (BTC) entirely.

CEO Cathy Clay said Bitcoin fails the index’s core test, generating real protocol revenue instead of trading purely on speculation.

How the Index Weighs Its Tokens

The index holds 18 constituents. Its five largest holdings are Ether (ETH), Binance Coin (BNB), Solana (SOL), Tron (TRX), and Hyperliquid (HYPE), a decentralized derivatives exchange.

The benchmark weights holdings by market capitalization and rebalances quarterly. No single token can exceed 35% of the total, and no other holding can top 20%. These caps mirror rules S&P applies to its own equity benchmarks.

Clay wants to bring stock-index discipline into digital assets. She favors protocols with verifiable economic activity over ones that trade on name recognition alone.

Pantera co-developed the methodology with founder Dan Morehead. The firm has managed over $3 billion across three investment strategies since launching its first crypto fund in 2013.

“S&P Dow Jones Indices helps investors cut through market noise with benchmarks you can trust.”

Clay, CEO of S&P Dow Jones Indices

Wall Street Warms to Altcoin Season

The exclusion highlights a widening split in how institutions define crypto value. By this measure, revenue beats Bitcoin’s dominant narrative as the market’s largest asset. Pantera’s history with institutional crypto access suggests more revenue-screened benchmarks could follow.

The launch lands as retail altcoin season signals stay unconfirmed but improving. CoinGlass’s Altcoin Season Index climbed to 58 in mid-July, building on a June 4 spike to 64. That reading sits above the neutral midpoint, but it remains short of the 75 threshold that confirms genuine rotation.

Institutional flows tell a parallel story. A March BeInCrypto Expert Council discussion found major allocators narrowing institutional crypto bets to Bitcoin, Ethereum, and a short list of DeFi names.

A revenue-screened benchmark like the S&P Pantera Digital Asset Index offers portfolio managers a compliant route into that same thesis. It provides exposure to large-cap altcoins with real usage, skipping meme coins and speculative networks entirely.

If other index providers copy the approach, institutional capital could rotate into select altcoins early. That could happen well before retail-driven altcoin season data confirms a broader move.

The post S&P Dow Jones New Crypto Index Snubs Bitcoin, Not a Revenue-Generating Protocol appeared first on BeInCrypto.

Bitcoin (BTC) passed one-month highs on Tuesday as price action defied the odds to top $66,000.

Key points:

- Bitcoin broke through resistance to hit $66,000 for the first time in more than a month.

- Traders see as much as 6% BTC price gains if further nearby upside targets are reached.

- Month-end derivatives positioning underscores crypto risk confidence slowly returning.

BTC price 6% upside could come “very quickly”: Trader

BTC/USD hit highs of $66,306 on Bitstamp, according to TradingView data. That’s a level last seen on June 17.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

A series of rejections around the $65,000 mark had failed to quash traders’ enthusiasm, with calls for $67,000 or higher gaining momentum. Those short-term predictions continued on the day, with key psychological levels around $70,000 now on the horizon.

“$BTC reclaimed the range lows, and is now pushing higher – as expected,” trader Jelle wrote in his latest analysis on X.

“The area between 65 and 67k is resistance from the Q1 range, but given how we sliced through it on the way down – it might not put much of a fight up here either. Eyes on those 70k range highs if so.”

BTC/USD one-day chart. Source: Jelle/X

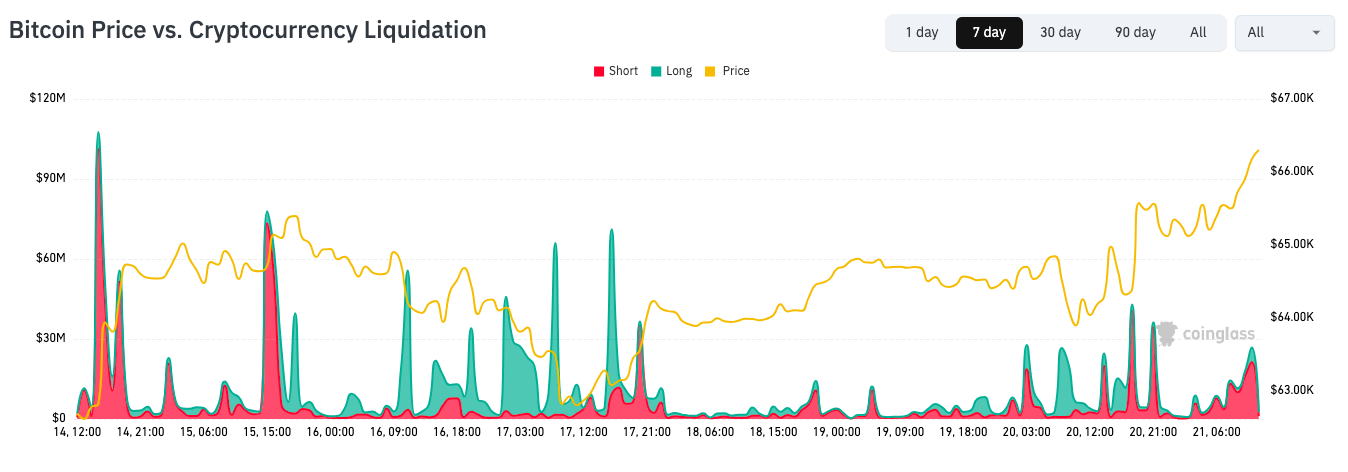

Short liquidations began to mount as the BTC price broke through range highs, with data from CoinGlass putting 24-hour cross-crypto liquidations at around $200 million.

BTC/USD vs. crypto liquidations (screenshot). Source: CoinGlass

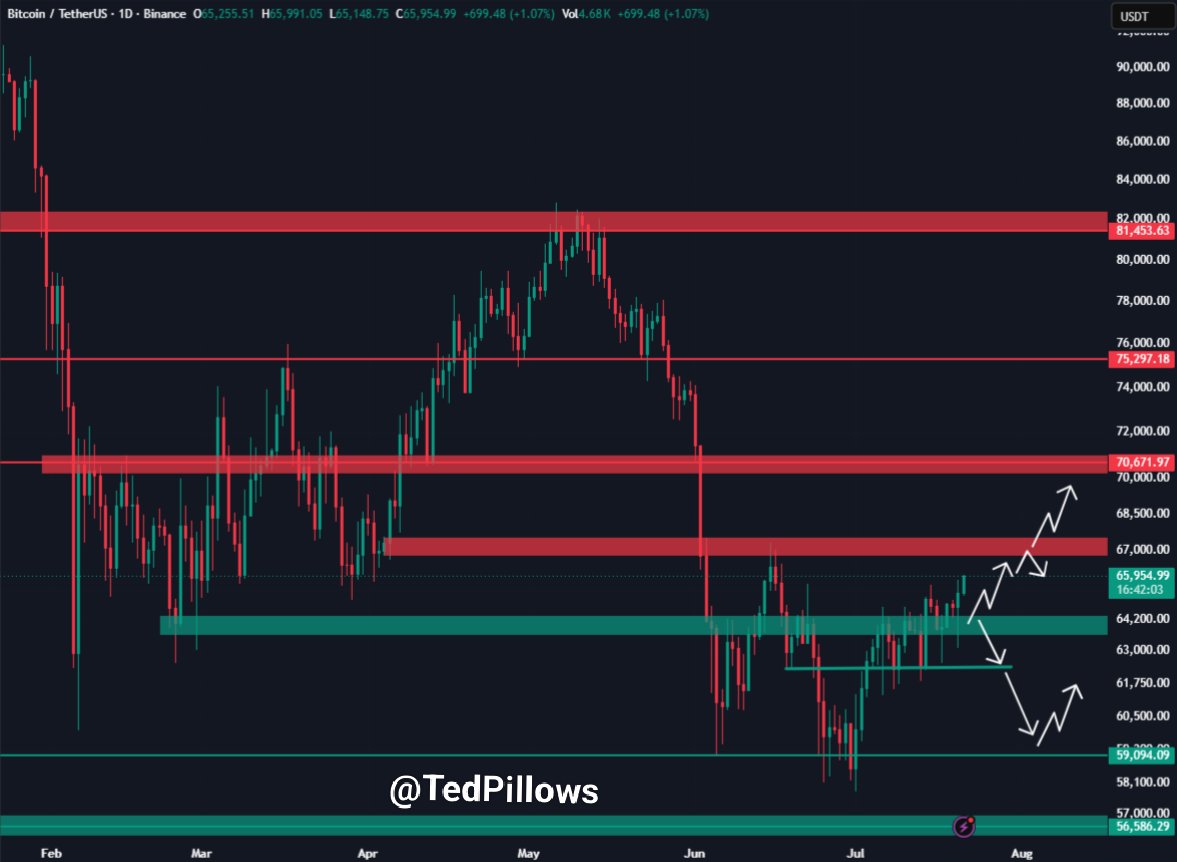

“$BTC has reclaimed the $65,000 level. The next key resistance is $67,500-$68,000, which means Bitcoin has some room to pump,” trader Ted Pillows said.

“If BTC manages to reclaim the $68,000 resistance too, it could rally another 5%-6% very quickly.”

BTC/USDT one-day chart. Source: Ted Pillows/X

Concerns had accompanied the start of the latest move, with commentator Exitpump seeing closing short positions fueling the upside.

“There’s very little real buying interest here,” they warned X followers while analyzing derivatives markets.

BTC derivatives hint at risk-on return

Observing options trends, trading company and market maker QCP Capital flagged “some demand” for higher Bitcoin bets into the end of July.

Related: Trader maintains $67K BTC price target: Five things to know in Bitcoin this week

Here, it noted the US Federal Reserve would hold its next meeting on interest-rate changes, with chair Kevin Warsh potentially offering fresh insight into future policy.

As Cointelegraph reported, market expectations remain that the Fed will leave rates unaltered before September. CME Group’s FedWatch Tool shows 83.4% probability that policy makers will stick with the current target range of 3.50-3.75% at their July 29 meeting. For the Sept. 16 FOMC meeting, there’s a 53.8% probability of a hike to 3.75-4.00%.

“There has been some demand for month-end BTC upside,” Monday’s QCP Market Colour analysis said.

“This positioning leaves dealers short upside gamma into the 28 to 29 July FOMC meeting, increasing the potential for an accelerated move higher should tensions around the Strait of Hormuz ease.”

QCP referred to the US-Iran war once again closing a key global oil route.

Russia’s State Duma has completed the final readings that bring the country’s long-awaited crypto regulatory bill one step closer to becoming law, approving draft legislation that would create a comprehensive framework for digital assets and define how regulated intermediaries can operate.

According to official parliamentary records, lawmakers approved bill No. 1194918-8, titled “On Digital Currency and Digital Rights,” in its second and third readings on Tuesday. The measure is now set to move to Russia’s upper house, the Federation Council, and then to President Vladimir Putin for signature before it can take effect.

Key takeaways

- The bill would establish rules for a regulated crypto market, including exchanges, brokers, asset managers, and custodians.

- The Bank of Russia would be given wide authority to supervise the framework and decide which crypto assets can be offered via licensed intermediaries.

- Crypto use for payments inside Russia would remain prohibited, while the bill allows digital assets to be used in foreign trade operations.

- Non-qualified investors would face purchase and cross-border transfer limits, with higher thresholds for qualified investors.

- If enacted, most provisions would begin on Sept. 1, 2026, with a compliance transition period lasting until July 1, 2027.

Bank of Russia oversight takes center stage

A central feature of the proposed framework is the role assigned to the Bank of Russia. Under the bill, the central bank would oversee the regulated market, including the power to determine which crypto assets are eligible to be offered through licensed intermediaries and to publish implementing regulations.

The bill also lays out five categories of participants that would operate within the new rules: crypto exchanges, brokers, asset managers, custodians, and exchange service providers. By defining who can buy, sell, hold, and exchange crypto assets, lawmakers aim to formalize the market structure and reduce reliance on informal or unlicensed activity.

For investors, the bill differentiates between “qualified” and “non-qualified” participants. Non-qualified investors would be subject to an annual ceiling of 300,000 rubles (about $3,800) on purchases made through a single intermediary, and a 100,000-ruble annual limit on transfers abroad. Qualified investors would have annual purchase limits of 3 million rubles and annual cross-border transfer limits of 1 million rubles.

Payments at home remain blocked, cross-border use allowed

While the bill expands the legal perimeter around crypto markets, it also preserves a key restriction: it would continue to ban the use of crypto assets to pay for goods and services within Russia.

At the same time, lawmakers chose to make room for digital assets in international commerce. The legislation would allow crypto assets to be used in foreign trade operations, aligning with Russia’s broader push to facilitate cross-border settlement alternatives outside conventional payment rails.

Timeline: broad provisions from September 2026, transition through 2027

Most of the bill’s provisions are scheduled to take effect on Sept. 1, 2026, contingent on presidential approval. A transition period runs through July 1, 2027, designed to give market participants time to adapt to the new compliance requirements.

After the transition window closes, the bill indicates that crypto transactions would need to be executed through regulated organizations. It also states that banks would have to reject transactions that do not comply with the framework laid out in the law.

Russia’s legislative push does not stop at market rules. Lawmakers are also drafting related measures, including proposals on taxation and penalties for violations. A separate tax bill has already passed its first reading, while expectations are that penalty provisions would be considered before the transition period ends.

Industry activity appears to be moving alongside the policy work. Earlier coverage from Cointelegraph noted developments involving Russia’s banking sector, including Alfa-Bank testing crypto trading.

Legal framework is not the finish line

Even if the bill becomes law, implementation would still depend heavily on the regulatory follow-through and supporting infrastructure. Olga Goncharova, head of the Digital Financial Assets and Digital Currencies Expert Center at the Association of Russian Banks, told Cointelegraph that the measure creates a legal foundation but requires “extensive follow-up regulation” before the market can function smoothly.

“The law itself is only the beginning,” Goncharova said, adding that practical effectiveness depends on mechanisms that are still being developed by the banking community together with the Bank of Russia.

According to Goncharova, the central bank plans to issue around 80 additional regulatory acts by the end of the year. These would be intended to specify how the framework operates in practice, particularly around compliance expectations for institutions and market participants.

She also pointed to work on operational infrastructure needed for a regulated environment, including development of a domestic Travel Rule system, blockchain node infrastructure, and crypto analytics tools. These elements would be important for monitoring transactions, reporting, and ensuring that regulated intermediaries can meet the requirements that come with licensing and oversight.

The broader regulatory trajectory will also need to align with licensing and supervisory expectations for custody services. Earlier Cointelegraph reporting referenced that custodians face scrutiny even under the EU’s MiCA regime, underscoring that custody regulation is typically a key test case for any emerging framework.

With the State Duma’s approval now secured, the next critical moment is whether the Federation Council and President Vladimir Putin sign the bill. Investors and market participants should watch closely for the Bank of Russia’s forthcoming regulatory acts—especially details on asset eligibility, licensing requirements, and how banks will operationalize the transaction rejection rules once the transition period ends.

Ionic Digital has secured SEC approval for its registration statement, clearing the final regulatory hurdle before its planned Nasdaq direct listing on July 28.

Summary

- Ionic Digital has cleared its final SEC regulatory hurdle ahead of its planned Nasdaq direct listing on July 28.

- Existing shareholders, including former Celsius creditors, will be able to sell their shares as Ionic lists under the ticker IOND.

- The company continues building its AI and high performance computing business alongside its Bitcoin mining operations.

According to a company statement issued Monday, the digital infrastructure operator expects its Class A common stock to begin trading on the Nasdaq Global Select Market under the ticker IOND, subject to Nasdaq’s final listing requirements.

The company is entering public markets through a direct listing instead of a traditional initial public offering. Under that structure, Ionic will not issue new shares or raise fresh capital from the transaction. Existing registered shareholders will instead be able to sell their holdings on the public market once trading begins.

For many investors, the listing represents the first opportunity to trade shares received through the bankruptcy restructuring of crypto lender Celsius Network. Ionic Digital was created in January 2024 to hold Bitcoin mining assets transferred from the Celsius estate after a U.S. bankruptcy court approved the lender’s restructuring plan.

Former Celsius creditors became shareholders after receiving about 37 million Class A shares under the bankruptcy plan. As previously reported by crypto.news, Celsius later continued distributing funds through additional payout rounds, while some creditors also became eligible to receive equity in Ionic Digital.

Unlike a conventional IPO, a direct listing does not involve underwriters setting an offering price. Instead, Nasdaq determines the opening price using buy and sell orders collected before trading begins. Ionic also stated in earlier SEC filings that direct listings can experience higher price volatility because existing shareholders gain a public venue to sell shares without the price stabilization mechanisms commonly associated with underwritten offerings.

Ionic expands beyond Bitcoin mining

Although Ionic began as a Bitcoin mining company, it has increasingly repositioned itself around digital infrastructure supporting artificial intelligence and high-performance computing workloads.

Earlier this month, the company filed its Form S-1 registration statement with the SEC. Before pursuing the listing, Ionic completed a roughly $400 million private equity financing that the company said would fund general corporate purposes, including continued investment in digital infrastructure and data center development.

According to earlier SEC filings, the financing implied a pre-money equity valuation of approximately $2 billion. CEO Andy Stewart previously said the funding strengthened the company’s capital base as it continued building its digital infrastructure platform.

The company’s strategy now extends well beyond cryptocurrency mining. Its Cedarvale campus in Ward County, Texas, has become the centerpiece of that transition after portions of the site were repurposed to support AI and high-performance computing infrastructure.

Earlier company disclosures said the Ward County property includes approximately 234 megawatts of installed capacity. Mining equipment at the site was decommissioned during late 2025 as Ionic prepared the facility for AI infrastructure under a long-term agreement with AI cloud provider Nscale.

According to previous company filings, the lease spans 126 months and is expected to generate about $1.95 billion in contracted revenue, with additional expansion possible if further capacity receives regulatory approval.

During the first quarter of 2026, Ionic reported $44 million in digital infrastructure leasing revenue, while Bitcoin mining revenue declined 82% year over year to $7.4 million from $41.1 million.

The company has also stated that revenue from AI and other high-performance computing services is eventually expected to exceed revenue generated through Bitcoin mining.

Mining companies are transitioning to AI

Ionic’s repositioning comes as several publicly traded Bitcoin miners invest more heavily in AI-focused data centers while mining profitability remains under pressure.

As previously reported by crypto.news, Bitcoin miners generated about $1.086 billion in revenue during May, the strongest monthly performance since January. However, lower Bitcoin prices later reduced mining profitability as hashprice declined and network hashrate eased, prompting some operators to scale back less efficient mining equipment.

Industry participants have increasingly turned toward AI infrastructure because many mining companies already control large power supplies, cooling systems and data center facilities that can be adapted for high-performance computing workloads.

IREN has followed a similar strategy. Earlier this year, the company completed its acquisition of Spain-based Nostrum Group, adding roughly 490 megawatts of secured grid-connected power to support European AI cloud expansion. IREN also reported that AI cloud revenue increased during its latest quarter even as Bitcoin mining revenue declined.

HIVE Digital and Bitdeer have also announced projects converting existing mining facilities into AI computing infrastructure, further illustrating how miners are seeking additional revenue streams beyond cryptocurrency production.

For Ionic, however, the upcoming Nasdaq debut represents more than another mining company entering public markets.

It also provides former Celsius creditors with a long-awaited opportunity to trade shares received through one of the cryptocurrency industry’s largest bankruptcy restructurings while giving investors a chance to evaluate a business increasingly focused on AI infrastructure rather than Bitcoin mining alone.

Sen. Cynthia Lummis said Tuesday she will introduce CLARITY Act bill text "in the next few days," marking the latest step in the Senate's push to pass a crypto market structure law before its August recess. "We've been working on the Clarity Act every day for 10 months, and we'll introduce bill… Read the full story at The Defiant

US lawmakers used a House Agriculture Subcommittee hearing this week to press the Commodity Futures Trading Commission (CFTC) on oversight of sports event prediction market platforms—while also pointing to a pending Senate effort, the Digital Asset Market Clarity (CLARITY) Act, as a potential source of clearer authority and funding.

At the hearing titled “Examining Customer Protections and Market Integrity in Sports Event Prediction Markets,” Carl Kennedy, a partner at law firm Katten Muchin Rosenman, argued that the CFTC may be unable to fully regulate and enforce rules for rapidly expanding prediction markets, citing staffing constraints. Kennedy said the CLARITY Act could expand the agency’s jurisdiction beyond digital assets and help it address the “explosive growth” of prediction markets.

Key takeaways

- Carl Kennedy told the House Agriculture Subcommittee that the CFTC is likely “short-staffed” to effectively oversee prediction market platforms.

- Kennedy said the CLARITY Act could grant the CFTC additional authority covering not only digital assets but also the fast-growing prediction market sector.

- CFTC Chair Michael Selig has argued the agency has “exclusive jurisdiction” over event contracts on major prediction platforms, treating them as “swaps.”

- State regulators have increasingly challenged that federal position, including through lawsuits and court disputes involving platforms such as Kalshi and Polymarket.

- Senate supporters of the CLARITY Act expect the bill text to be released soon, but details on prediction market provisions were not publicly available as of Tuesday.

Why lawmakers are focusing on prediction market oversight

The hearing, chaired around customer protections and market integrity in sports event prediction markets, highlighted how the legal and regulatory question has shifted from whether prediction platforms can operate to who is responsible for regulating them.

Kennedy’s core point was that even if the CFTC has jurisdiction, it may not have the resources to supervise new and complex markets at the pace they are growing. He suggested that an expanded mandate under the CLARITY Act would need to be paired with additional capacity so the agency can handle oversight and enforcement across cash markets and crypto as well as prediction markets.

“With additional resources… to address these new asset classes in the cash markets and crypto… as well as to deal with the explosive growth of prediction markets, I think that the CFTC certainly should receive additional resources,” Kennedy said during the Tuesday hearing.

The subcommittee discussion also reflected that prediction markets—often built on event contracts linked to real-world outcomes—have become a regulatory stress test for existing derivatives rules, especially as platforms attract broader participation.

The CFTC’s “exclusive jurisdiction” position under scrutiny

Legal and regulatory experts at the hearing referenced the CFTC’s approach under Chair Michael Selig, who was confirmed by the Senate in December and is the only Senate-confirmed member heading the commission in a leadership panel that would normally include five commissioners.

Since taking the role, Selig has taken the position that the CFTC has “exclusive jurisdiction” over prediction market companies. The argument is that the event contracts on these platforms fall under the CFTC’s authority because they can be classified as “swaps.”

This stance has drawn criticism—particularly from Democratic senators—who have described it as an “assault” on state authority to regulate prediction markets.

That federal-versus-state tension has produced a growing body of litigation. Some states have pursued lawsuits against platforms including Kalshi and Polymarket over what they see as state-level sports betting concerns.

State court clashes and the path toward the Supreme Court

One recent flashpoint involved a dispute where the CFTC chair’s position came into direct conflict with a state court ruling. Last week, Selig ordered Kalshi to ignore a Michigan court decision, according to prior coverage, with Kalshi arguing that the directive placed it in an “impossible position” between federal and state authorities.

More broadly, experts have suggested that the legal conflict between state regulators and the CFTC could eventually end up before the US Supreme Court. That possibility centers on the same foundational question raised by lawmakers: whether the CFTC’s reading of its jurisdiction leaves room for states to regulate event contracting tied to sports and related forms of wagering.

For market participants, this matters because jurisdiction affects compliance obligations, product design decisions, and the legal risk profile of operating in different states. For consumers, it affects who sets the rules for customer protections and how those rules are enforced—particularly when the platforms operate nationwide.

What the CLARITY Act could change—and what remains unclear

Much of Tuesday’s discussion pointed toward the CLARITY Act as the most significant potential legislative change on the horizon. Republican senators pushing for a vote before August recess have indicated they expect to release the bill’s text soon.

As of Tuesday, details of how the CLARITY Act would address prediction markets, ethics provisions, and other concerns raised by lawyers were not yet public.

However, earlier reporting indicates there is active political pressure to shape the bill’s scope. In June, gambling industry groups petitioned the Senate to add language to CLARITY that would explicitly prohibit event contracts tied to sports and casino-style gaming. Separately, reports cited by earlier coverage said the White House had confirmed that the Trump administration agreed to ethics provisions described as comprehensive, while also accommodating Democrats’ concerns.

That mix—requests for tighter boundaries around wagering-linked event contracts alongside broader ethics requirements—underscores that CLARITY is not only about regulatory authority for digital assets. Kennedy’s remarks at the hearing framed the bill as potentially relevant to prediction markets as a category, particularly in relation to customer protections and market integrity.

For traders, platform operators, and state regulators, the immediate watch item is the CLARITY Act’s released text and how it addresses the core jurisdiction conflict: whether it expands and clarifies federal oversight for event contracts, and whether it limits or displaces state enforcement where prediction markets intersect with sports wagering. Until the bill language is published, the questions raised in court and in Congress—about who regulates, who enforces, and how resources match the scale of these markets—are likely to keep escalating.

Balaji Srinivasan’s Network School, a community of “digital nomads,” is eyeing a new campus in Kazakhstan after its Forest City campus had its business license revoked over alleged premises-use violations.

A memorandum of understanding was signed between Kazakhstan’s Minister of Digital Development, Innovation and Aerospace Industry, Zhaslan Madiyev and Srinivasan to establish the first Network School campus in Kazakhstan, according to a statement from the ministry.

The Kazakhstan agreement gives the Network School a potential new base after its Johor operation was ordered to cease operations effective Wednesday. Kazakhstan has been positioning itself as an emerging technology hub, including plans for Central Asia’s first “crypto city” in Alatau.

“Ironically, this whole drama with Balaji literally validated the network state thesis,” said Dragonfly Capital managing partner Haseeb Qureshi. “The whole idea of a network state is taking a dense group of talent and capital, and collectively negotiating with states. The Malaysia drama set up Balaji to negotiate better terms with another state to copy and paste the network there. “

“Our new campus will become a haven for global techno-optimism, with expedited visas, streamlined redomiciliation, and active recruitment of talent,” Srinivasan said Tuesday.

Network School faces loss of Malaysia Digital status

The new memorandum of understanding with Kazakhstan comes as the Forest City campus faces regulatory action on several fronts.

On Tuesday, the Iskandar Puteri City Council (MBIP) revoked the business license of NSO Malaysia Sdn Bhd, which operates the Network School, alleging the company breached licensing conditions and premises usage requirements.

This led to the Malaysia Digital Economy Corporation (MDEC) announcing it is taking immediate steps to revoke the Malaysia Digital status of NSO Malaysia, which requires companies under the program to follow all local and federal laws.

Malaysia Digital is a recognition awarded to qualified technology and digital companies, providing them with tax incentives, freedom of ownership and allowing the employment of local and foreign workers, among other incentives.

Meanwhile, Onn Hafiz Ghazi, Chief Minister of Johor State, has urged Malaysia’s federal authorities to continue investigating whether the Network School violated immigration laws.

Related: Balaji seeks Malaysia deal, threatens exit after Network School probe

“This matter cannot be taken lightly, especially since Johor is a strategic entry point for the country bordering Singapore. Any weaknesses or abuse of the immigration system must be addressed promptly, firmly, and without compromise,” said Onn.

On Friday, Srinivasan denied reports that the Network School was shutting down, claiming that it had received two notices, with one notice requiring it to “change the text of a sign” and the other regarding a coworking site, created by joining two adjacent units, that had a valid license on one side, not on the other.

“We have a remedial period for both issues, and will remediate them shortly. But our members are otherwise unaffected,” he said.

Cointelegraph reached out to Srinivasan and Network School for comment.

Magazine: Binance & OKX users face $1,900 fines in Vietnam, Coinbase in China? Asia Express

Coinbase began offering a High Yield tier on its USDC lending product paying about 7.02% APY, roughly double the 3.63% APY on its standard Core tier, days after Robinhood Earn launched a competing 7% campaign. Both products route deposits through Morpho, a decentralized lending protocol with $7.11… Read the full story at The Defiant

Balaji Network School Expands to Kazakhstan After Malaysia Setback

Forced Daughter To Have Stepdad Baby

Americans dub Donald Trump ‘dangerous’ and ‘corrupt’ in scathing new survey

-

NewsBeat5 days ago

NewsBeat5 days agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Politics7 days ago

Politics7 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Crypto World5 days ago

Crypto World5 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Crypto World6 days ago

Crypto World6 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Crypto World4 days ago

Crypto World4 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Business6 days ago

Business6 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics3 days ago

Politics3 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Entertainment6 days ago

Entertainment6 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Crypto World4 days ago

Crypto World4 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World18 hours ago

Crypto World18 hours agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Crypto World5 days ago

Crypto World5 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Business6 days ago

Business6 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Tech1 day ago

Tech1 day agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech23 hours ago

Tech23 hours agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat5 days ago

NewsBeat5 days agoRegistration is now open for March for Men with Kev 2026

-

NewsBeat2 days ago

NewsBeat2 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Sports6 days ago

Sports6 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos5 days ago

News Videos5 days agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

You must be logged in to post a comment Login