Crypto World

Senators Press CFTC for Investigation Into Polymarket Ad Claims

A bipartisan group of US lawmakers has asked the Commodity Futures Trading Commission (CFTC) to examine Polymarket after reports that the prediction market operator paid social media influencers to publish videos depicting fake bets. The request highlights intensifying scrutiny over how prediction platforms market products to US audiences—and whether existing CFTC oversight is sufficient to address deceptive advertising and gambling-style promotion.

In a letter to CFTC Chair Rostin Behnam, Senators John Curtis (Republican) and Adam Schiff (Democrat) said the allegations, if accurate, would point to “deceptive marketing tactics” used to promote gambling-like products. The correspondence follows investigative reporting by The Wall Street Journal and comes as the CFTC’s broader approach to prediction markets remains a subject of legal and policy dispute.

Key takeaways

- US Senators John Curtis and Adam Schiff have asked the CFTC to investigate Polymarket following allegations of deceptive influencer promotion.

- Reports cited by lawmakers describe videos showing fake trades on content styled like Polymarket, with limited or no disclosure that creators were paid.

- The lawmakers questioned whether the CFTC is enforcing existing rules effectively and whether it has the resources to regulate prediction market advertising and conduct.

- The request underscores ongoing tension between federal commodity regulation and state-level efforts to treat prediction markets as gambling or sports betting.

- Institutional compliance teams may face heightened scrutiny of marketing practices, influencer disclosures, and the product characterization used by prediction market platforms.

Senators request CFTC scrutiny over reported influencer promotions

The senators’ letter—sent to the CFTC—centers on concerns that Polymarket allegedly used influencer campaigns to promote its platform using content that did not reflect real trading activity. According to reporting by The Wall Street Journal, Polymarket paid influencers to record videos of “fake bets” on websites resembling the platform, and many creators reportedly did not disclose that they were being compensated by Polymarket.

The Journal said it reviewed more than 1,100 videos and found that roughly 70% depicted fake bets totaling nearly $2 million. The senators framed the conduct, if verified, as both a consumer protection and regulatory enforcement issue—arguing that marketing practices can distort how US audiences perceive the risks and nature of prediction market products.

In response to the earlier reporting, a Polymarket spokesperson told Cointelegraph that the company was “conducting a comprehensive audit” of active promotional content to ensure compliance with its standards and applicable regulatory and legal disclosure requirements.

Regulatory authority and the “gambling-style” framing debate

Beyond the specific allegations, Curtis and Schiff raised broader questions about how prediction markets should be regulated in the US. In their letter, they argued that the CFTC has repeatedly claimed authority over prediction markets and event contracts, yet they described a marketing environment in which content creators often depict prediction products as “free money.”

The senators contended that these representations provide little basis for treating prediction markets differently from gambling-style offerings. They also warned that the contracts are not in the public interest and should not be treated as derivative products with hedging characteristics.

While the senators’ argument is policy-oriented, it is also operational from a compliance perspective: product characterization affects which regulatory frameworks apply, how marketing claims are reviewed, and whether conduct could be evaluated under commodity laws, anti-fraud standards, or state gambling statutes.

The dispute is occurring against a backdrop of increased prediction market use and regulatory attention. US lawmakers have highlighted concerns about the CFTC’s ability to police content and advertising, including how promotional campaigns influence consumer perceptions—particularly when promotions resemble or mimic real trading.

What the CFTC investigation could examine

The letter asks the CFTC to provide written answers by July 10 to several questions, including whether it is investigating Polymarket, whether the reported advertising practices were legal, and whether the commission has sufficient resources to police prediction markets. The senators’ requests reflect an enforcement focus that goes beyond marketplace mechanics—targeting marketing disclosures, promotional content integrity, and the adequacy of regulatory capacity.

Multiple reports have indicated that the CFTC is considering enforcement steps. CNBC, citing a person familiar with the inquiry, reported that the CFTC has an ongoing and extensive investigation into Polymarket, though the timeline for when it began was not disclosed. Polymarket declined to comment on the senators’ letter and on the reported investigation.

In practice, an inquiry of this kind could also involve scrutiny of influencer marketing controls—such as disclosure requirements, the use of simulations or staged content, and whether promotional material could be viewed as misleading. For regulated firms and institutional counterparties, such issues matter because marketing representations can be linked to compliance risk, reputational risk, and potential legal exposure under consumer protection and anti-fraud principles.

Federal vs. state oversight: the broader legal context

The Curtis-Schiff letter arrives amid persistent federal-state regulatory friction over prediction market platforms. The CFTC has argued that it holds authority over prediction markets because platforms are registered with the agency and operate under federal commodities law.

At the same time, the CFTC has pursued litigation tied to state efforts to regulate prediction markets. The regulator has sued nine US states that filed legal action to accuse prediction market platforms of offering unlicensed sports betting through event contracts.

This federal posture remains politically and legally contested. For compliance teams, the key uncertainty is that even when platforms argue they fall within commodity regulation, marketing practices can become a flashpoint—particularly if promotional content is perceived by regulators or litigants as indistinguishable from gambling or sports betting activity.

MiCA is not directly implicated in these US disputes, but the situation offers a broader institutional lesson: cross-border crypto businesses must manage divergent regulatory interpretations across jurisdictions. In the US, characterization battles can flow from product design and contract structure into advertising and promotion, creating compliance obligations that extend well beyond technical listings or trading interfaces.

Closing perspective

As lawmakers press for answers from the CFTC, the immediate focus will likely be on whether promotional campaigns and influencer arrangements complied with disclosure expectations and anti-misleading standards, and what enforcement resources the agency can deploy across a fast-growing prediction market ecosystem. The outcome could shape how regulated platforms structure marketing approvals, manage influencer relationships, and document compliance—while leaving unresolved questions about the line between commodity-regulated contracts and gambling-style promotion.

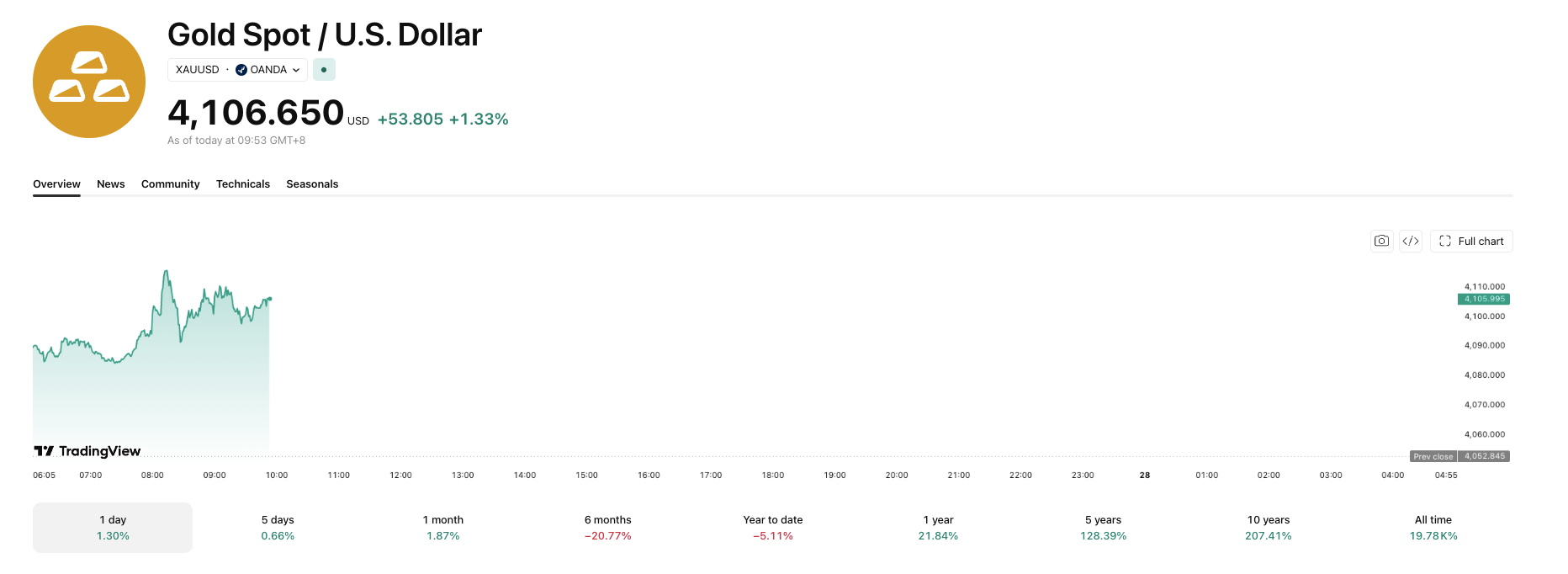

Gold climbed more than one percent in Asian trading Monday. A weekend pause in US-Iran hostilities pushed oil prices lower and eased fears of prolonged high interest rates.

Spot gold traded at $4,106.65 per ounce Monday, up 1.33% on the day, according to TradingView data.

Oil Retreat Lifts Precious Metals

The pause came as advisers reportedly warned Trump that the military was nearing the limit of viable targets in Iran. They also flagged concerns about draining U.S. munitions stockpiles, prompting the pause in strikes. Iran will halt its own attacks as long as Washington does the same, a senior Iranian official told Reuters.

Oil prices tumbled as much as 7% on hopes for a diplomatic resolution. That reverses recent forecasts that Brent crude could revisit its war-era peak near $120 after going above $100 at the weekend. Lower energy costs typically ease inflation, reducing the odds the Fed holds rates high for longer. Gold’s appeal fades when rates stay high since the metal pays no yield.

Traders are still pricing an 80% chance of a rate hike in September, according to the CME Group’s FedWatch Tool, which tracks futures-implied rate expectations.

Gold also Boosts Silver

Other precious metals rallied in tandem. Spot silver climbed 2.7% to $59.74 an ounce, building on a recent breakout above key resistance. Platinum gained 2% to $1,619.75, and palladium rose 2.3% to $1,271.93.

COMEX gold speculators added 4,438 contracts to their net long position in the week to July 21. That brought the total to 123,586 contracts, according to CFTC data.

The Fed’s rate decision this week will test whether the truce holds long enough to sustain the rally. A split among 104 economists over the central bank’s next move shows how uncertain the path remains. That uncertainty deepens if fighting resumes and oil prices reverse.

The post Gold Gains as US-Iran Pause Also Sends Oil Prices Lower appeared first on BeInCrypto.

Decentralized cloud storage provider Storj Labs has filed for voluntary Chapter 11 bankruptcy protection in the United States, opening a restructuring process that could test how—if at all—utility-token holders might participate in the equity of a company that emerges from bankruptcy. The filing was made in the US Bankruptcy Court for the Northern District of West Virginia, according to a statement published by Storj.

Storj says the restructuring is aimed at addressing legacy liabilities that it argues can’t be resolved through growth alone, while keeping its network running and preserving the token’s core utility. At the time of writing, STORJ appeared to have reacted mutedly to the news, trading around $0.072 based on CoinGecko data.

Key takeaways

- Storj Labs entered voluntary Chapter 11 in the Northern District of West Virginia while stating that ordinary operations and customer services will continue under court oversight.

- The company says its liabilities largely predate its current strategy and are too large to clear solely through business expansion.

- Storj management plans to propose a pathway for STORJ token holders to participate in the equity of a reorganized company, subject to bankruptcy priorities and court approval.

- Storj has not yet detailed how tokenholder eligibility would work, including whether a token snapshot, lockup, or other criteria would be used.

- STORJ’s market reaction to the filing was limited in the immediate term, with CoinGecko showing trading near $0.072 at publication time.

Chapter 11 filing framed as a legacy-liability fix

On Sunday, Storj announced that it filed for voluntary Chapter 11 “to resolve legacy liabilities and position the business for growth,” according to a post on its own website. The company indicated that day-to-day operations would not stop, and that customer services would continue during the process, but under supervision by the bankruptcy court.

Storj also said its parent company, Inveniam, would continue to support the business throughout the restructuring. That support, along with Storj’s insistence that the underlying network remains functional, is central to the company’s message to token holders: the technology and the token’s intended role should not be treated as collateral to be sidelined while legal obligations are worked through.

A proposal for tokenholder equity—without the mechanics yet

Storj’s open letter to its community argues that the restructuring need is driven by obligations from earlier stages of the company, rather than issues stemming from the present network model. The letter also states that the network is operating normally and that the token’s utility is unchanged.

Crucially, Storj said management intends to submit a plan that would create a mechanism for token holders to participate in the reorganized company’s equity. However, the company has not disclosed essential details, including how eligibility would be determined (for example, whether participation would depend on token ownership at a particular time), whether any tokens would be locked up, or what portion of equity might be offered.

Storj acknowledged that any proposal must align with bankruptcy requirements—meaning the reorganization plan has to follow established priority rules and receive court approval. That constraint matters because Chapter 11 restructurings typically involve complex treatment of different classes of creditors, equity holders, and other stakeholders. In this case, token holders are not automatically treated as equity holders, so Storj’s approach will likely hinge on how the court-approved plan defines who receives value and under what conditions.

Cointelegraph contacted Storj for additional comment but did not receive a response before publication.

Why the Storj case is a test for utility-token ownership

Storj’s bankruptcy filing is likely to draw attention beyond its community because it sits at the intersection of two unresolved questions in crypto: how regulators and courts may interpret token-related claims in insolvency, and whether “utility” token holders can convert their economic exposure into equity-like rights during a restructuring.

The company described the restructuring as a potential “ownership pathway” for STORJ token holders, which—if it moves from proposal to approved plan—could become a reference point for other projects with token distributions and decentralized networks. At the same time, uncertainties remain. Storj has not provided a framework for how a tokenholder-to-equity mechanism would be structured, and bankruptcy priorities could limit what any token holder pathway ultimately looks like.

For market participants and builders, this is also a reminder that decentralized infrastructure tokens can still carry company-level legal and financial risk. Even when networks continue operating, restructuring plans can reshape governance expectations, economic arrangements, and the distribution of future upside.

Part of a broader Chapter 11 wave in crypto

Storj’s filing comes amid a month in which multiple crypto-related businesses sought Chapter 11 protection. Earlier coverage highlighted Movement Labs filing under Subchapter V on July 15 after turmoil connected to its MOVE token, and a separate filing by Bitcoin mining pool Poolin on July 22 as it pursued a court-supervised sale of two Texas mining sites.

Meanwhile, other exchanges faced operational endpoints without filing for bankruptcy. BitMEX announced in July that it would shut down after 11 years, following announcements connected to legal action, while BitMart said it would end trading on Aug. 26 before fully ceasing operations on Jan. 31, 2027. Storj’s case differs in that it is explicitly pursuing a court-supervised reorganization with potential equity-related outcomes for token holders.

Storj itself traces its origins to 2014, when it began as an open-source peer-to-peer cloud storage concept designed to let users rent storage from network participants rather than rely on centralized providers, according to earlier reporting. That longer history may help explain why the company emphasizes continuity: the network has market credibility and operational history, and Storj is positioning Chapter 11 as a legal course-correction rather than a shutdown.

As the bankruptcy process develops, investors and token holders will be watching for what Storj’s eventual reorganization plan actually proposes—particularly the eligibility criteria for tokenholder participation and how (or whether) any proposed equity allocation can comply with Chapter 11 priorities and court approval. The next phase will also reveal whether the network’s stated “normal operation” stance can be maintained through the litigation and settlement decisions that typically follow a major restructuring filing.

Strategy has skipped four straight weekly Bitcoin (BTC) purchases, its longest buying pause in two years. The company reports second-quarter earnings Thursday, July 30, after the US market closes.

SEC filings confirm Strategy’s last purchase covered the week ending June 21. Since then, the company has sold Bitcoin instead of adding to its stack.

A Pause Built on Falling mNAV

Strategy’s stock traded at a premium to its Bitcoin holdings for years, a ratio called mNAV. That premium let the company sell shares above BTC value and grow Bitcoin per share for holders.

The model breaks once mNAV drops toward 1. New share sales then destroy value instead of creating it. mNAV touched roughly 0.99 in late June, its first sub-parity reading ever, before recovering to about 1.03. Strategy’s holdings now trade underwater against their purchase price, and management puts the real breakeven closer to 1.22.

Strategy sold 3,588 BTC in two tranches between June 29 and July 5 for about $216 million. The sales funded preferred stock dividends and topped up its cash reserve. Strategy adopted this capital framework in late June, and the reserve reached $3.225 billion by July 20.

What Thursday Could Show

Strategy posted a $14.5 billion operating loss in the first quarter on Bitcoin’s mark-to-market decline. LSEG’s consensus estimate points to a swing back to $3.86 billion in Q2 operating income, but two of the seven analysts behind that number submitted forecasts before June’s bitcoin slide.

Thursday’s results will show whether Strategy sticks with this trade-off, raising fresh capital while leaving its Bitcoin holdings untouched.

The post Strategy Earnings Loom as Bitcoin Buying Freeze Hits a Month appeared first on BeInCrypto.

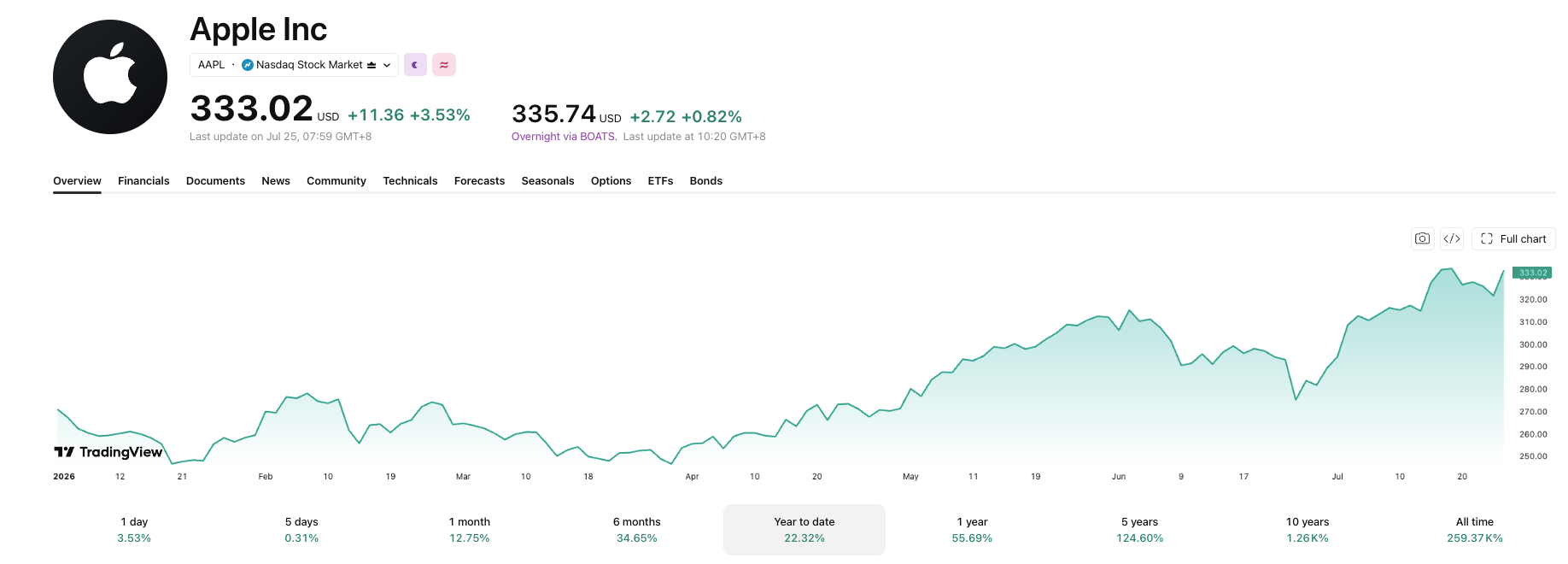

Four Big Tech giants report second-quarter earnings this week, testing whether massive AI spending is translating into real returns. SK Hynix also delivers its first results since a record Nasdaq debut, and Tim Cook holds his final call as Apple’s chief executive.

The reports arrive a day before the Federal Reserve’s Wednesday rate decision, with markets already pricing a possible hike. Oil going above $100 a barrel, and subsequently dropping on a pause in hostilities, adds another layer of pressure to the week.

Microsoft and Meta report Wednesday

Microsoft and Meta open the busiest stretch on Wednesday. Analysts expect Microsoft to raise its 2026 capex forecast toward $238 billion. That would test whether spending discipline can offset rising memory chip costs.

Meta faces separate scrutiny. Investors have grown skeptical of Meta’s AI spending, rotating capital toward Google instead. Alphabet’s cloud unit grew 82% last quarter, the number Wall Street now wants Meta to match.

Apple closes an era Thursday

Apple reports Thursday alongside Amazon, in Tim Cook’s final earnings call as chief executive. Analysts expect revenue near $108.9 billion, per MarketBeat estimates. The company has leaned on a capital-light AI approach, avoiding the outsized spending pressuring rivals.

Apple stock hit a record high earlier this month as rising memory prices squeezed cheaper phone rivals.

SK Hynix reports first, on Tuesday

SK Hynix reports Tuesday, its first earnings since a record Nasdaq debut. Consensus points to 84.1 trillion won in sales, per Yonhap Infomax, which would set a new operating profit record. The report follows a volatile month, including a post-listing selloff and a KOSPI rebound past 7,000.

Brent’s climb past $100 adds another variable to the week. Investors are already juggling four earnings reports and a Fed decision in three days. Not to mention the price of oil has slid over 7% as hostilities eased in the Middle East

The post 5 Earnings Reports to Watch as Big Tech’s AI Spending Faces a Test appeared first on BeInCrypto.

Blockaid said an attacker drained about $450,000 in USDT from Garden Finance’s HTLC contracts across Ethereum, Base, Arbitrum and BNB Smart Chain.

Storj Labs, the decentralized cloud storage provider behind the STORJ token, has filed for voluntary Chapter 11 bankruptcy protection in the United States. The company says it will continue operating its network and providing customer services while it restructures legacy liabilities and seeks a court-approved pathway that could allow tokenholders to participate in the ownership of a post-bankruptcy entity.

In a statement released Sunday, Storj said the case was filed in the US Bankruptcy Court for the Northern District of West Virginia. Storj also stated that its parent company, Inveniam, will continue supporting the business during the restructuring process, subject to court oversight.

Key takeaways

- Storj Labs has entered voluntary Chapter 11, with the network and customer services expected to keep running during restructuring.

- The company is exploring a mechanism that could give STORJ tokenholders a route to equity in the reorganized business, but details remain undisclosed.

- Storj says its core network utility is unchanged and that its liabilities largely predate its current strategy.

- STORJ saw no immediate major price move at announcement time, trading around $0.072, according to CoinGecko.

Bankruptcy filing with continuity for the network

According to Storj’s filing announcement and accompanying community communication, the bankruptcy is primarily aimed at addressing legacy obligations that the company says are too significant to resolve through growth alone. Storj emphasized in an open letter to tokenholders that the platform’s operations were continuing normally and that the token’s utility would remain unchanged.

The company’s approach matters because decentralized infrastructure businesses rely on ongoing participation and service continuity. While Chapter 11 typically involves constraints around certain contracts and expenditures, Storj is positioning its restructuring as compatible with maintaining the storage network’s day-to-day functioning through the period of court supervision.

Tokenholders and the challenge of an equity pathway

Storj’s most notable claim is that management intends to propose a mechanism for STORJ tokenholders to participate in the equity of the reorganized company. The company, however, did not provide specifics on how eligibility would be determined—whether through a token snapshot, a lockup requirement, or other criteria. It also did not disclose what portion of equity, if any, might be reserved for tokenholders.

Storj acknowledged that any plan must comply with bankruptcy priority rules and receive court approval. That point is central: equity participation for token holders in bankruptcy typically depends on how the token’s legal and economic status is treated in the restructuring process, and on how the reorganization plan is structured relative to creditor claims.

The situation effectively becomes a live test of whether utility-token holders can secure a meaningful ownership role in a company emerging from Chapter 11, especially when the token’s utility is positioned as separate from the company’s preexisting liabilities.

Market reaction and what investors should watch

STORJ did not show an immediate sharp reaction following the news. CoinGecko data, as cited in the announcement coverage, indicated STORJ was trading around $0.072 at the time of writing.

For investors and network participants, the more consequential variable is unlikely to be the short-term token price—rather, it is the eventual shape of the Chapter 11 plan. The missing details from Storj’s statements include the criteria for tokenholder eligibility, the form participation might take (equity allocation versus other compensation structures), and whether there will be any valuation framework tied to token holdings.

As the process moves forward, readers should focus on court filings and confirmed reorganization terms: how Storj categorizes its liabilities, how claims are prioritized, and whether the proposed “shared ownership” pathway survives the restructuring review with creditor and court buy-in.

A broader pattern of crypto Chapter 11 filings

Storj’s bankruptcy comes amid a period in which at least two other crypto-related firms sought Chapter 11 protection. Movement Labs filed under Subchapter V on July 15 following months of turmoil connected to its MOVE token, while Bitcoin mining pool Poolin filed on July 22 as it pursued a court-supervised sale of two Texas mining sites. Separately, BitMEX announced in July that it would shut down after 11 years, choosing an orderly wind-down rather than filing for bankruptcy.

This clustering of Chapter 11 actions highlights a sector-wide reality: decentralized and blockchain-adjacent businesses still depend on traditional legal and financial structures when legacy obligations become unmanageable. For utility-token networks, that can create a difficult tension between keeping infrastructure running and negotiating outcomes that may reshape the relationship between token economics and corporate ownership.

What happens next for Storj

Storj’s next steps—especially the specifics of any tokenholder equity mechanism and the court-approved reorganization plan—will determine whether the company’s “shared ownership” vision is feasible within bankruptcy priorities. Until then, tokenholders will be watching for concrete filing details rather than assurances, and for confirmation that network continuity remains intact under court oversight.

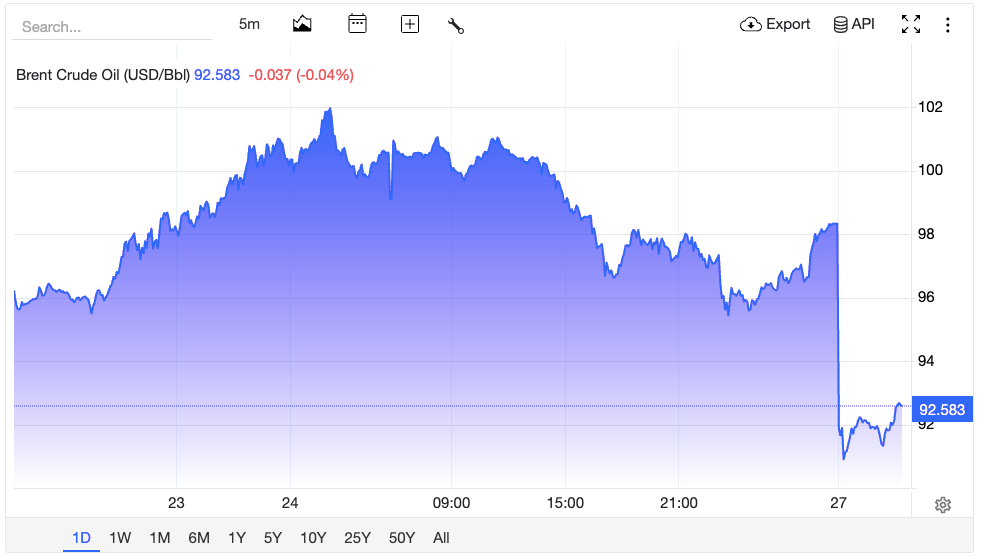

Oil prices tumbled Sunday after a senior Iranian official told Reuters that Tehran will halt its own attacks as long as the United States keeps its bombing pause in place. The move eased nearly two weeks of escalating conflict.

The price of Brent crude oil fell over 7% to touch a low of $90.9 a barrel. West Texas Intermediate crude oil also dropped as much as 7% to touch $84.

Tehran Sets Conditions for Oil

The Iranian source described Tehran’s stance as “attack for attack.” Iran will stop its operations once the US stops, and Tehran has already passed that message to Washington, according to the official’s account.

“There is more scepticism than optimism about the halt in attacks. The prevailing view is that the pause is tactical rather than genuine.”

The pause follows Washington’s decision to suspend its bombing campaign after 13 nights of US strikes. Advisers reportedly warned President Donald Trump that the military was running low on viable targets. They also raised concerns about depleting weapons stockpiles.

US Ambassador to the United Nations Mike Waltz said Trump chose the pause to give diplomacy room. Iranian officials voiced more doubt than hope that the calm will last.

Fed Watching Inflation Risk

HSBC US rates strategist Dhiraj Narula said pricier oil has revived bets that the Federal Reserve may hold rates higher for longer. He noted inflation expectations have stayed contained so far. Narula credited firm Fed messaging on price stability for that resilience, which has kept the energy rally from feeding into longer-term forecasts.

Brent held near $92 a barrel into Monday, confirming Sunday’s drop stuck rather than snapping back. Whether the halt lasts through the week will test if Tehran’s skepticism proves right, or if the pause turns into lasting de-escalation.

The post Oil Slides 7% as Iran Signals It Will Halt Attacks If US Pause Holds appeared first on BeInCrypto.

Decentralized cloud storage provider Storj Labs has filed for Chapter 11 bankruptcy protection. The company said it plans to keep its network running while restructuring legacy liabilities and exploring an ownership pathway for STORJ tokenholders.

On Sunday, Storj said it filed the voluntary case in the US Bankruptcy Court for the Northern District of West Virginia. The company said ordinary operations and customer services would continue during the process, subject to court oversight, while its parent company, Inveniam, would continue to support the business.

The restructuring could become an unusual test of whether utility-token holders can participate in the ownership of a company emerging from bankruptcy.

In an open letter to its community, Storj said its liabilities largely predate its current strategy and are too substantial to resolve through business growth alone. It said the network continues to operate normally and its token’s utility is unchanged.

STORJ showed no significant immediate price reaction following the announcement, trading around $0.072 at the time of writing, according to CoinGecko.

Storj explores equity pathway for tokenholders

Storj said management intends to propose a mechanism allowing tokenholders to participate in the reorganized company’s equity.

However, Storj has not disclosed how tokenholder eligibility would be determined, whether participation would involve a token snapshot or lockup, or how much equity might be allocated. The company acknowledged that any plan must follow bankruptcy priorities and receive court approval.

Cointelegraph reached out to Storj for comment but did not receive a response before publication.

Storj is among the crypto industry’s longest-running decentralized infrastructure projects. Storj began in 2014 as an open-source peer-to-peer cloud storage project that sought to let users rent storage from other network participants rather than rely on centralized providers.

Related: BitMEX hit with 623 BTC lawsuit on day it announces shutdown

Storj’s bankruptcy filing comes in the same month as at least two other crypto companies sought Chapter 11 protection.

Movement Labs filed under Subchapter V on July 15 after months of turmoil linked to its MOVE token, while Bitcoin mining pool Poolin filed on July 22 as it pursued a court-supervised sale of two Texas mining sites.

BitMEX also announced in July that it would shut down after 11 years. Still, the derivatives exchange did not file for bankruptcy, instead opting for an orderly wind-down following a strategic review.

Magazine: CLARITY hopes fade, BitMEX shuts as lawsuit looms: Hodler’s Digest

With the August recess deadline closing in, U.S. lawmakers are still negotiating the Clarity Act—an ethics-focused proposal tied to digital asset activity that would also restrict officials from issuing or sponsoring crypto. Senate Majority Leader John Thune has signaled skepticism that there are enough votes for passage, but said a floor vote could still be pursued to “get Clarity started” and test support.

The bill is also at the center of a deeper political struggle over enforcement. Democrats want ethics rules to be enforced by state attorneys general, while the White House and Republicans have advanced an approach that hinges on the federal Attorney General—an official appointed by President Trump. The dispute, along with provisions that Democrats criticize as giving the President special leeway, is leaving the legislation in limbo even as industry and law enforcement groups begin to line up behind the latest version.

Key takeaways

- Clarity Act momentum depends less on technical drafting and more on whether lawmakers can reconcile a major enforcement disagreement and the scope of presidential exceptions.

- Senate Majority Leader John Thune doubts the bill has the votes for passage, but may still move toward a vote to gauge support.

- Institutional backers—including Fidelity and Charles Schwab, and a statement of support from Goldman Sachs CEO David Solomon—suggest the bill remains attractive to parts of traditional finance despite imperfections.

- Outside politics, crypto infrastructure news continues with BitMEX announcing it will shut down operations in September after 11 years, while S&P Dow Jones and Pantera launch an institutional digital asset benchmark index that excludes Bitcoin and XRP.

Clarity Act: ethics rules collide with enforcement politics

At the heart of the Clarity Act negotiations is a proposed ethics deal that would bar U.S. officials from issuing or sponsoring digital assets. However, the plan also includes exceptions Democrats say amount to a “get out of jail free” arrangement for the President. One sticking point raised in reporting is that certain rules would expire on the day President Trump is scheduled to leave office in 2029—an element that has been criticized as undermining the durability of the restrictions.

The enforcement mechanism is another major fault line. The ethics provisions would be administered by the Attorney General appointed by Trump, but Democrats have pushed for state attorneys general to enforce the rules instead. That expansion would create a broader enforcement footprint across jurisdictions—something Republicans and the White House appear unlikely to support, especially given the likelihood that the President would resist changes that empower many independent state-level prosecutors.

According to Cointelegraph, Senate Majority Leader John Thune does not believe the bill has enough votes to pass yet. Still, he indicated he may bring it to the floor to “get Clarity started” and determine where the remaining votes stand as the August recess deadline nears.

Support from institutions and law enforcement—while trust remains strained

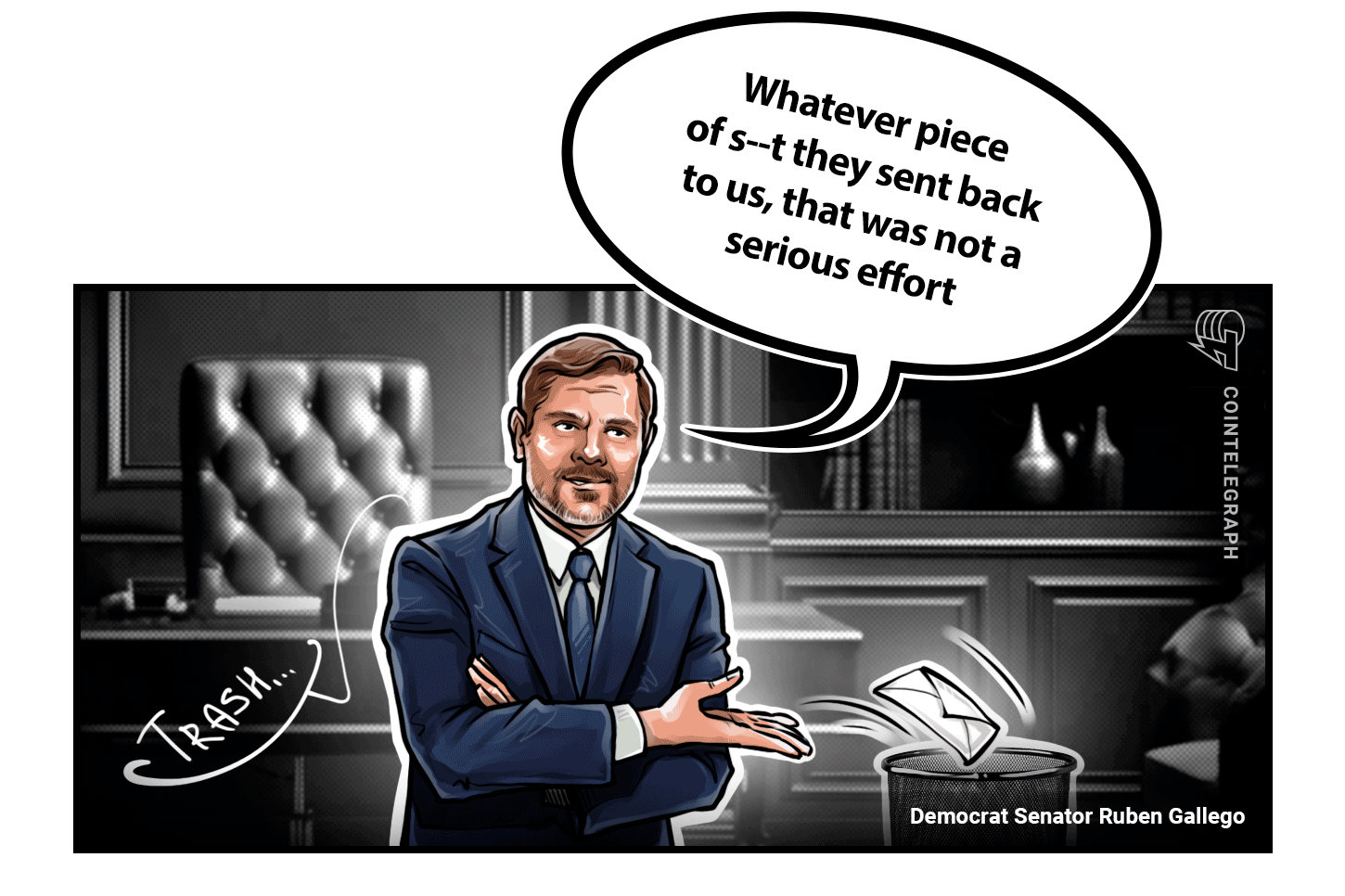

While political factions remain divided, signals of support from outside government have started to build. The White House described the bill as the “most comprehensive and wide-ranging ethics provision in history,” while Democratic Senator Ruben Gallego characterized it with unusually blunt language, calling it neither serious nor acceptable. Negotiations are reportedly continuing in an effort to find wording that both sides can accept.

Financial institutions have also weighed in. Goldman Sachs CEO David Solomon acknowledged the proposal is “not perfect,” but still supported it. Cointelegraph also reported that Fidelity and Charles Schwab have backed the initiative. Taken together, these endorsements suggest the bill’s advocates see it as a workable baseline for reducing perceived conflicts—particularly for firms that want clearer conduct expectations involving digital assets.

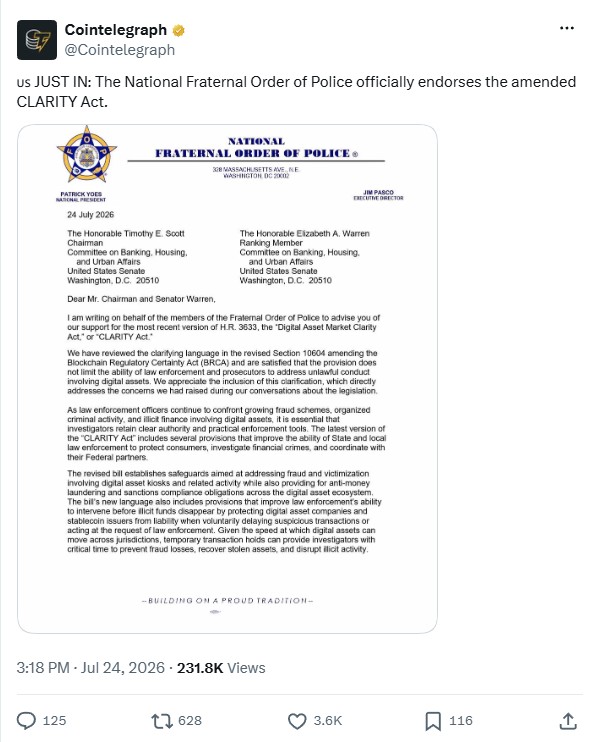

Law enforcement signals have been another ingredient. The National Fraternal Order of Police said the latest version of the BRCA—described as protecting developers of decentralized protocols—would not impede investigations into money laundering and fraud. That point matters for the bill’s political sell: proponents want ethics restrictions to target conflicts of interest without unintentionally constraining legitimate enforcement activity.

Still, the level of distrust between parties appears to be the dominant constraint. Negotiators may be able to close gaps on implementation details, but the bill’s most consequential disagreements—presidential exceptions and who can enforce the rules—go to the core of each side’s incentives.

What the odds say—and what to watch next

Market odds also reflect uncertainty. According to Polymarket, the odds of the Clarity Act passing this year are currently 38%. Even if a floor vote is scheduled, that number implies the bill could still face serious headwinds, particularly if negotiations fail to produce a package that enough senators can defend publicly.

Investors and market participants should watch for two developments in the near term: whether the enforcement framework shifts meaningfully toward a multi-enforcer model, and whether the presidential exception provisions remain intact or are narrowed. Those items likely determine whether additional lawmakers feel comfortable turning a political compromise into a concrete vote.

BitMEX to shut down, highlighting consolidation in derivatives trading

Elsewhere in crypto policy and markets, BitMEX—one of the early pioneers of crypto derivatives trading—announced it will shut down operations in September after 11 years. BitMEX launched in 2014 and gained notoriety for introducing 100x leverage perpetual swaps.

But in recent years, volumes fell as competition intensified, with major centralized exchanges such as Binance and fast-growing decentralized venues like Hyperliquid taking share. CryptoQuant CEO Ki Young Ju said BitMEX’s share of the Bitcoin futures market has dropped to 0.08%, with about $84 million in daily trading volume.

Ju described the closure as an industry “torch” moment—an exchange that helped shape the market now stepping aside for the next wave it inspired. Cointelegraph also reported that BitMEX’s utility token, BMEX, fell sharply after the shutdown announcement. The same day, a class action lawsuit surfaced alleging that BitMEX fraudulently engineered liquidations to seize trader collateral. BitMEX denied the accusations and said it previously defended itself successfully against similar claims.

Analysts tied the shutdown to broader structural changes. Cointelegraph reported restructuring adviser Roshan Dharia saying BitMEX’s demise reflects accelerated consolidation. A quoted passage highlighted that the top five platforms control an estimated 80% of global spot volume, squeezing mid-tier operators as structural headwinds—rather than temporary cycles—reduce margins and limit scaling pathways.

That consolidation narrative continued quickly: Cointelegraph also reported that BitMart later announced it would close in the coming months, underscoring how pressure is spreading across crypto venues rather than concentrating on a single platform.

Institutional benchmarks expand: S&P and Pantera launch a crypto index

Index providers are also moving deeper into digital assets. S&P Dow Jones Indices and Pantera Capital launched the S&P Pantera Digital Asset Index, positioned as an institutional benchmark that tracks major crypto assets but excludes Bitcoin and XRP.

According to Cointelegraph, the index is designed to serve institutions by filtering blockchains based on minimum thresholds for protocol revenue, market capitalization, and liquidity. The index launched with 18 constituents. Ether (ETH), BNB (BNB), Solana (SOL), TRON (TRX), and Hyperliquid (HYPE) make up the five largest holdings, while Bitcoin (BTC) and XRP remain the largest non-constituents.

The effort fits a broader industry push for institutional-grade benchmarks. Cointelegraph cited related products such as the Nasdaq Crypto Index US ETF, a Franklin Crypto Index ETF, and a Coinbase Store of Value Index—signaling that tradfi-style benchmarking continues to shift from concept to increasingly concrete infrastructure.

Robinhood prediction markets grow as regulators focus on event contract specificity

On the U.S. consumer-facing side, Robinhood is reportedly discussing an expansion of its prediction markets business by integrating yes-or-no event contracts supplied by Crypto.com. Cointelegraph noted that Robinhood began prediction markets in March 2025, initially facilitated by Kalshi to satisfy compliance requirements from the U.S. Commodity Futures Trading Commission (CFTC).

At the same time, regulatory scrutiny is intensifying around how event contracts are certified. Cointelegraph reported that the CFTC issued another warning that platforms must be more specific rather than relying on broad template-style certifications covering multiple potential variations of events. The regulatory push matters because it can constrain how quickly providers scale new contract templates or broaden the range of covered scenarios.

Cointelegraph also referenced legal commentary linking potential clarity on market structure oversight to the Clarity Act, framing the ethics legislation as possibly supportive of the CFTC’s ability to monitor prediction market growth.

Across governance, exchanges, and benchmarks, the throughline is clear: crypto is entering a phase where regulation, institutional infrastructure, and market structure pressures are reshaping outcomes. For the Clarity Act specifically, the next signals to monitor are whether negotiations produce a durable enforcement compromise and whether senators are willing to translate that compromise into votes before the August recess deadline.

Clarity may get a vote, but don’t get your hopes up yet

Despite wealthy memecoin entrepreneur Donald Trump agreeing to an ethics deal, the Clarity Act is floundering as the August recess deadline looms.

Senate Majority Leader John Thune doesn’t believe the Act has the votes to pass just yet, but may bring it to a vote anyway to “get Clarity started. We’ll see where the votes are.”

The ethics deal would prohibit all US officials from issuing or sponsoring digital assets, but contains some “get out of jail free” provisions for the President that the Democrats are unhappy with, including the fact the rules expire the day he is scheduled to leave office in 2029.

The ethics provisions will also be enforced by the Attorney General that Trump appointed. The Democrats instead want state Attorney Generals to enforce it — but Trump seems unlikely to agree to empower dozens of state AGs to attempt to prosecute him.

The White House described the bill as the “most comprehensive and wide-ranging ethics provision in history,” while Democratic Senator Ruben Gallego described it as a “piece of shit” and “not a serious effort.”

Negotiations are continuing to find a deal both sides can live with, but given the lack of trust, it’s not going to be easy to find a compromise.

Goldman Sachs CEO David Solomon conceded the bill is “not perfect” but has supported it anyway, along with Fidelity and Charles Schwab who represent many trillions in assets under management each.

Law enforcement organizations have also begun to signal support, with The National Fraternal Order of Police representing hundreds of thousands of members, stating the latest version of the BRCA (which protects developers of decentralized protocols) would not impede investigations into money laundering and fraud.

The odds of the bill passing this year are at 38% on Polymarket.

BitMEX to shut down after 11 years as class action launched against it

BitMEX, one of the pioneers of cryptocurrency derivatives trading, announced it will shut down operations in September after 11 years.

BitMEX launched in 2014 and became known for introducing the 100x leverage perpetual swaps.

In recent years volumes have tanked increased competition from major exchanges like Binance and decentralized protocols like Hyperliquid.

CryptoQuant CEO Ki Young Ju said BitMEX’s share of the Bitcoin futures market has fallen to just 0.08%, with roughly $84 million in daily trading volume.

“It was a great exchange that helped shape the industry, and now it is passing the torch to the next generation of exchanges it inspired,” Ju said.

BitMEX’s utility token BMEX collapsed in value after the announcement. That same day, news emerged of a class action lawsuit accusing the crypto derivatives platform of fraudulently engineering customer liquidations to seize traders’ collateral. BitMEX denied the allegations and said it had successfully defended itself against similar claims in the past.

Restructuring adviser Roshan Dharia told Cointelegraph the exchange’s demise shows the industry is consolidating.

The top five platforms now control an estimated 80% of global spot volume, leaving mid-tier and regional exchanges with shrinking margins and no viable path to scale… The headwinds are structural, not cyclical.

As if to undescore the point, BitMart subsequently announced it would also close in the coming months.

S&P launches blockchain fundamentals index for digital assets

S&P Dow Jones Indices and Pantera Capital have launched a digital asset index that tracks the major crypto assets — but doesn’t include Bitcoin or XRP.

The S&P Pantera Digital Asset Index is designed to be the benchmark crypto index for institutions, but it screens out blockchains based on minimum thresholds for protocol revenue, market capitalization and liquidity.

The index launched with 18 constituents, with Ether (ETH), BNB (BNB), Solana (SOL), TRON (TRX) and Hyperliquid (HYPE) as its five largest holdings, while Bitcoin (BTC) and XRP (XRP) are the largest non-constituents.

The latest index follows a broader industry push to develop institutional-grade benchmarks for digital assets, with similar products including the Nasdaq Crypto Index US ETF, the Franklin Crypto Index ETF and the the Coinbase Store of Value Index among others.

Robinhood to expand prediction markets as CFTC issues new warning

Robinhood is reportedly discussing plans to expand its existing prediction markets offerings with crypto exchange Crypto.com.

According the Wall Street Journal the talks involve integrating yes-or-no event contracts supplied by Crypto.com. Robinhood launched its prediction markets in March 2025, initially facilitated by Kalshi in order to comply with regulatory requirements from the US Commodity Futures Trading Commission (CFTC).

Bernstein analysts last week raised its price target on Robinhood (HOOD) stock to $160 from $130 per share, based on the company’s outlook for prediction markets and tokenized equities.

Meanwhile the CFTC, which aims to become the primary regulator of prediction markets, issued a shot across the bow of providers last week, telling platforms they need to get a lot more specific about event contracts certifications.

The advisory addresses concerns about the practice of submitting broad, template-style certifications that combine many potential event contract variations into a single certification.

Carl Kennedy, a partner at New York law firm Katten Muchin, also told a House Agriculture Committee hearing last week, that the CLARITY Act could help the CFTC’s efforts to oversee the “explosive growth of prediction markets.”

Balaji’s Network School turns to Kazakhstan amid Malaysia setback

Balaji Srinivasan’s Network School, a community of “digital nomads,” is eyeing a new campus in Kazakhstan after its Forest City campus had its business license in Malaysia revoked over alleged premises-use violations.

A memorandum of understanding was signed between Kazakhstan’s relevant Minister Zhaslan Madiyev and Srinivasan to establish the first Network School campus in the country, which aims to become a digital hub.

The School was forced out of Johor in Malaysia, following a controversy in Malaysia over allowing Israeli dual citizens to attend. The Muslim majority country has no diplomatic relations with Israel. Despite an investigation finding no visa violations, the Network School was ordered to shut down on another pretext.

Dragonfly Capital managing partner Haseeb Qureshi said the drama has validated Balaji’s Network State thesis.

“The whole idea of a network state is taking a dense group of talent and capital, and collectively negotiating with states. The Malaysia drama set up Balaji to negotiate better terms with another state to copy and paste the network there.“

Winners and losers

At the end of the week, Bitcoin (BTC) is at $65,395, Ether (ETH) is at $1,958, and XRP (XRP) is at $1.11. The total market cap is at $2.24 trillion according to CoinMarketCap.

Among the biggest 100 cryptocurrencies, the top three altcoin winners of the week are Audiera (BEAT), which gained 53%, Shinba Inu (SHIB) with a 29% gain, and Venice Token (VVV), which increased 19%.

The top three altcoin losers of the week are DeXe (DEXE), which lost 89%, Midnight (NIGHT), which fell 26%, and Pyth Network (PYTH), which dropped 10%.

Prediction of the Week

Bitcoin will get ‘lift’ from Hyperliquid, Robinhood in next crypto bull market

Bitcoin (BTC) is “finally showing signs of a bottom,” according to Matt Hougan, chief investment officer at Bitwise.

Houghan predicts that TradFi integrations, particularly Hyperliquid and Robinhood, will drive the next crypto bull market, and the resulting tide should “lift” the largest cryptocurrencies including Bitcoin and Ether.

Houghan believes crypto is bringing major benefits like 24/7 trading to traditional markets, and noted that today “nearly half the volume on Hyperliquid is in conventional assets like oil, silver, and the S&P 500 [and] it’s expanding into spot commodities, prediction markets, and options,”

Bitwise data also suggests apparent demand for BTC is showing signs of reversal. The metric measures the difference between newly-mined BTC and the supply inactive for at least one year.

Top FUD of the Week

Home invasions became most common crypto wrench attack in H1 2026: CertiK

Home invasions became the most common form of crypto wrench attacks during the first half of 2026, rising to 20 publicly reported incidents from just one a year earlier, according to blockchain security firm CertiK.

On Thursday, CertiK said it verified 52 wrench attacks worldwide in the first half of 2026, up 33.3% from 39 incidents during the same period in 2025. Kidnappings rose to 16 from 12, while robberies declined from five incidents to one.

CertiK said the recorded financial exposure linked to the attacks reached about $124.1 million, up from $10.5 million a year earlier.

The increase in home invasions suggests criminals are increasingly bypassing digital safeguards by physically coercing crypto holders and their families.

Hackers steal $31.6M in 2 crypto bridge attacks within 7 hours

Hackers stole more than $31.6 million across two unrelated crypto bridge exploits spaced just hours apart, targeting bridges operated by decentralized perpetual exchange AFX and Verus Protocol.

According to Blockaid, AFX, a decentralized perpetual exchange operating on Arbitrum, reportedly lost $24.15 million on Wednesday through a hack targeting one of its cross-chain bridges. Hours later, Blockaid said it detected an exploit targeting the Verus Ethereum Bridge that resulted in about $7.5 million in crypto being stolen.

“Another bridge, another exploit. Bridges will always be a weak link, until security is upgraded,” onchain investigator TheCrypticWolf said in a post on X.

Ethereum ETFs close week in red, end 5-day inflow streak

US-listed spot Ethereum exchange-traded funds (ETFs) logged $70.62 million in net outflows on Friday, ending a five-day inflow streak.

Ethereum funds saw $211.25 million in net inflows over the previous five sessions from July 17, according to SoSoValue data. They still posted $103.9 million in net inflows for the week ended Friday.

Despite the outflows, Ethereum ETFs extended their weekly inflow streak to three straight and have attracted $337.74 million in net inflows so far in July.

The Bitcoin ETFs reversed gains made earlier in the week to end up with $33.9 million of inflows.

Top Magazine Stories of the Week

Both parties say they want US crypto market structure legislation, but a dispute over ethics rules and who enforces them is becoming the bill’s biggest obstacle.

A Bitcoin development roadmap that addresses quantum computing risks could see the price surge by “double digits” very quickly, according to Charles Edwards.

Are the fears of an AI driven hacking epidemic totally overblown, or is this just the lull before the storm?

Cointelegraph publishes long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Content published in here does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence.

Anytime 13u vs the money flock 13u

Oil Price Today (July 27): Crude oil dips 5%, below $95 as US pauses strikes on Iran. What are experts saying?

Doubt Time lands plunge on Caulfield debut in 2026

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat5 days ago

NewsBeat5 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech6 days ago

Tech6 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat7 days ago

NewsBeat7 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Business5 days ago

Business5 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment5 days ago

Entertainment5 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Tech7 days ago

Tech7 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

NewsBeat6 days ago

NewsBeat6 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World7 days ago

Crypto World7 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Tech7 days ago

Tech7 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

-

Tech3 hours ago

Tech3 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Sports6 hours ago

Sports6 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos3 days ago

News Videos3 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Sports3 days ago

Sports3 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion3 days ago

Fashion3 days ago16 Dresses for the High Summer Event

-

Entertainment7 days ago

Entertainment7 days agoStephen Colbert Returns to Social Media After Late Show End

-

Politics14 hours ago

Politics14 hours agoSpain sweeps the board at 2026 World Cup with individual awards

You must be logged in to post a comment Login