Crypto World

Solving Bitcoin’s gas issue (without a fork)

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Every smart contract platform has a fee asset baked in. For example, Ethereum (ETH) has ETH, Solana (SOL) has SOL, but with Bitcoin (BTC), however, things get messy. If you want expressive apps, you usually end up adopting a second network’s economics.

Summary

- Bitcoin doesn’t price computation, only block space. Unlike Ethereum or Solana, BTC’s fee market is built around sat/vB for transaction inclusion, not metering smart contract execution.

- Execution can move off-chain while settlement stays on Bitcoin. Systems like OpNet run contract logic in a Wasm VM while anchoring payments and final state changes through normal BTC transactions.

- BTC can function as the gas asset without a new token. By pricing execution costs in satoshis and settling interactions through Bitcoin transactions, apps avoid creating a second fee economy.

On Stacks, for example, you pay fees in STX. On EVM-style Bitcoin layers, you might be told that BTC is the gas token, but it’s typically an L2-native representation with EVM-like conventions (including 18 decimals), and you’re still operating inside that L2 environment. Bitcoin itself, meanwhile, already has a clean fee market, where users bid for block space in sat/vB, and miners prioritize higher fee rates.

With this in mind, what if a smart contract interaction could be initiated and paid for as a normal Bitcoin transaction, with fees in BTC terms (no extra gas token or fork) while the smart part runs elsewhere and stays provably tied back to Bitcoin? OpNet is setting out to provide an answer.

Bitcoin doesn’t meter compute (that’s a problem)

Bitcoin’s fee market is excellent at one thing: pricing block space. You compete in sat/vB, miners pick the highest fee rates, and the network stays simple and adversarially robust. What Bitcoin does not do is run a general-purpose execution environment where the chain can measure and charge for arbitrary computation. Bitcoin Script is deliberately stateless and not Turing-complete, specifically lacking loops or gotos, so every node can validate scripts predictably without opening the door to unbounded computation.

That’s why most Bitcoin smart contract approaches end up placing execution on a separate system that can meter compute and run a fee market of its own. Once you have that separate execution layer, it usually comes with a separate fee asset (Stacks, for instance, charges fees in STX).

This isn’t ideal, and a system where you could keep payment within Bitcoin’s native fee market while moving execution elsewhere would be preferable.

Execution isn’t what Bitcoin needs to do

Once you accept that Bitcoin Script is intentionally limited (stateless and not designed for unbounded computation), you start thinking about how to make Bitcoin settle the results and the payments.

Indeed, execution can happen in a dedicated virtual machine that’s built to run smart contract logic deterministically, while Bitcoin remains the base layer that timestamps, orders, and prices the interactions through its existing fee market. In OpNet’s design, contract logic is evaluated by a Wasm-oriented VM (OP-VM), while the broader node stack is explicitly built to manage and execute smart contracts using Bitcoin’s existing transaction and UTXO mechanics.

Crucially, this isn’t paired with a new fee asset. Bitcoin doesn’t need to meter computation to be the gas currency. It needs to be the final settlement layer that everything ultimately pays into and anchors to.

What a BTC-paid contract call looks like

Our interaction model follows a simulate-then-spend flow rather than a conventional smart contract execution pattern, with the final execution step taking place as an actual Bitcoin transaction. First, your app calls a contract method in simulation mode. That request goes through a provider to an OPNet node, which executes the contract in its VM and returns a CallResult (including gas/fee estimates) without broadcasting anything to Bitcoin.

If the call is state-changing, you take that CallResult and send it as an execution. At this point, the library builds a Bitcoin transaction, signs it, and broadcasts it to the Bitcoin network. Two points are worth remembering:

- Miner fees are Bitcoin-native. You choose a feeRate in sat/vB, optionally add a priorityFee in sats, and set a hard cap on fee spending via maximumAllowedSatToSpend (the parameter is literally named maximumAllowedSatToSpend).

- The contract target is expressed as a P2OP-style contract address. The contract instance exposes its p2op address format, and transactions reference a “p2op contract address” as the contract destination.

Meanwhile, OpNet’s own compute metering still exists. But it’s priced in satoshis (estimated SATS Gas, refunds in SATS, etc.), so the unit never drifts into a separate token economy.

Less friction, cleaner incentives

Users no longer have to adopt a second fee economy just to interact with apps. On Bitcoin, fees are already an auction for block space, priced per byte and paid to miners. When contract calls are just Bitcoin transactions, you’re back on familiar ground (with sat/vB fees, mempool churn, and miner incentives), without having to learn a separate gas token market.

Also, the tooling leans into standard Bitcoin workflows such as UTXO handling, provider connections, and even offline/cold signing. Contracts live in a Wasm runtime and are written in AssemblyScript, aiming for Solidity-like expressiveness without pretending Bitcoin Script suddenly became a VM.

Bitcoin as gas, without a second token

The claim that BTC cannot function as gas usually rests on the assumption that the base layer must meter computation to price it. Bitcoin does not meter computation; it meters block space and settles value.

The solution is to let a virtual machine handle execution deterministically, and then route every state-changing interaction through a standard Bitcoin transaction, where fees are expressed in familiar terms such as sat/vB and capped in satoshis. In our case, this is implemented at the client level through parameters like feeRate and maximumAllowedSatToSpend.

So maybe BTC-as-gas is truly plausible. Fees stay BTC-native from end to end, while the contract runtime stays WebAssembly-based (AssemblyScript → Wasm), which keeps the logic expressive without changing the fee currency.

The price that underpins real-world oil cargo transactions surged to its highest level since 2008. Dated Brent hit $141.37 per barrel, reaching an 18-year high.

Meanwhile, Brent crude futures traded near $107, still below 2022 levels. Thus, it’s clear that the benchmark for actual crude cargoes now trades more than $34 above Brent futures.

“The last time Dated Brent touched such heights was 18 years ago, when the global financial crisis that had been brewing for months was on the cusp of puncturing a historic crude rally,” Bloomberg wrote. “The surge is a sign of the growing disconnect between futures contracts and various pockets of physical markets that are pricing increasingly scarce supplies.”

This isn’t just a price difference. It’s a stress signal. The physical oil market is under acute strain, with immediate demand far outpacing available supply.

Follow us on X to get the latest news as it happens

Recently, Chevron CEO Mike Wirth warned that futures are not reflecting the true scale of the oil supply disruption. He stated that the market is trading on “scant information” and “perception.” According to him,

“There are very real, physical manifestations of the closure of the Strait of Hormuz that are working their way around the world and through the system that I don’t think are fully priced into the futures curves on oil.”

Energy Aspects founder Amrita Sen also told CNBC that the futures market is obscuring the real stress.

“You are seeing it, but the financial market is almost masking the true tightness that everywhere else is showing up,” Sen remarked.

Trump’s Shifting Stance Deepens Uncertainty

The Strait of Hormuz, which handles roughly one-fifth of global crude flows, has been closed for over a month. Gulf producers have cut output by at least 10 million barrels per day, as tanker traffic has dropped by 95%.

President Trump has sent conflicting messages on the Strait. In a prime-time address on April 2, he declared Iran “essentially decimated” and said the waterway would reopen “naturally” once the conflict ends.

Meanwhile, he told other nations they should “grab it and cherish it.” However, his shifting timelines and statements have layered uncertainity onto an already fractured supply picture.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Paper vs. Physical: The $34 Gap Exposing the True Cost of the Iran Oil Shock appeared first on BeInCrypto.

The International Monetary Fund has highlighted both the promise and the peril of tokenization in finance. In a 23-page assessment released this week, the IMF said tokenization could reduce friction and increase transparency across issuance, trading, settlement and asset management. Yet it warned that the same technology could also introduce risks that might affect financial stability, especially as speed and automation enable rapid, automated flows that leave less room for traditional oversight.

The IMF’s analysis stresses that while atomic settlement and enhanced visibility can mitigate some longstanding dangers, the accelerated pace of tokenized markets could give rise to new systemic stress if controls aren’t aligned with legal and supervisory clarity. A central finding remains: “The net effect of tokenization on financial stability is uncertain,” the IMF wrote, underscoring the delicate balance between improved efficiency and new risk vectors.

Key takeaways

- Tokenization reduces some traditional risks through faster settlement and greater transparency, but speed and automation introduce new financial-stability challenges.

- On-chain tokenization of real-world assets has surpassed $27.6 billion, excluding stablecoins, according to RWA.xyz data, highlighting growing industry activity.

- Long-run forecasts for the tokenization market vary widely—BCG in 2022 projected up to $16 trillion by 2030, while McKinsey in 2024 offered a more conservative $2 trillion—the gap reflecting differing assumptions about liquidity, regulation and adoption.

- Legal clarity over ownership records and settlement finality remains a bottleneck; the IMF notes fragmented markets could hamper widespread use unless governance keeps pace with technology.

The economic arc of tokenized real-world assets

The IMF’s report acknowledges that tokenization expands how securities and other financial products are issued, traded, settled and managed. But it also cautions that the technology effectively shifts some systemic risk from traditional banking rails to shared ledgers and smart contract code. In a phrase that captures the urgency for policymakers, the IMF warned that “stress events in tokenized markets are likely to unfold faster than in traditional systems, leaving less time for discretionary intervention.”

On the demand side, tokenization is being seen as a means to accelerate cross-border payments, broaden financial inclusion and unlock new channels for capital flow in emerging markets. Yet, the IMF also flags potential downsides: greater volatility in capital moves, rapid currency substitution and a perceived erosion of monetary sovereignty if participants rely on programmable money without adequate supervisory guardrails.

While the IMF is cautious, market participants are moving ahead. Real-world asset (RWA) tokenization has already drawn substantial traction. As of early April, data from RWA.xyz show more than $27.6 billion of real-world assets tokenized on-chain, excluding stablecoins. The scale of this segment points to a broader appetite among institutions to digitize assets like receivables, property interests and other non-tokenized holdings.

In the broader market outlook, the debate centers on scalability and liquidity. Industry studies have delivered mixed signals about the ultimate size of the opportunity. Boston Consulting Group estimated in 2022 that the tokenization market could swell to as much as $16 trillion by 2030, while McKinsey & Co. offered a notably more cautious projection of around $2 trillion for the same horizon. The IMF’s assessment sits between these bounds, emphasizing potential but underscoring the need for robust risk management as the ecosystem grows.

Industry momentum and notable players

Interest from Wall Street has been a key driver. High-profile figures such as BlackRock CEO Larry Fink have signaled support for tokenizing a broad spectrum of assets—from equities and bonds to money market funds and real estate—marking a shift in institutional attitudes toward on-chain representations of traditional instruments.

Within the on-chain asset category, Securitize has emerged as a leading platform by total value locked (TVL) in real-world asset tokenization. Securitize powers the BlackRock USD Institutional Digital Liquidity Fund, a major RWA project with reported TVL around $3.38 billion, per CryptoDep’s April data. Closely following are Tether Gold and Ondo Finance, with roughly $3.35 billion and $3.21 billion in TVL, respectively, underscoring a crowded field of tokenized wealth vehicles aimed at institutional investors.

Beyond tokenized assets themselves, the traditional exchanges are signaling their intent to bring tokenization into mainstream trading and settlement. Intercontinental Exchange, the parent company of the New York Stock Exchange, announced in January that it would launch a tokenization platform designed for 24/7 trading and instant settlement of stocks and exchange-traded funds via a blockchain-based post-trade system. The move indicates a direction where tokenized securities could become an integrated, continuous-source of liquidity rather than a niche, off-hours exercise.

Standards, regulation and practical controls

One of the IMF’s pointed critiques centers on legal and regulatory clarity. Without well-defined ownership records and settlement finality, tokenized markets risk becoming fragmented and peripheral to the broader financial system. In response, the industry has begun embracing standards and access controls to align technology with regulatory expectations.

Among the notable technical developments is the Ethereum ecosystem’s ERC-3643 standard, which enables permissioned access to tokenized assets and imposes identity and eligibility checks for holders. In practice, this standard is already being applied by some tokenized products to ensure compliance with investor requirements. A concrete example cited in the industry press is Coinbase Asset Management’s tokenized shares for the Coinbase Bitcoin Yield Fund, issued on the Base network (an Ethereum Layer 2). The fund leverages ERC-3643 to verify holder identity and eligibility during tokenization and post-trade processes.

The IMF also points to the broader regulatory architecture around stablecoins, cross-border flows and monetary sovereignty as areas that require ongoing attention as tokenized markets scale. The balance between enabling innovation and preserving monetary policy effectiveness will be a central theme for policymakers over the coming years.

What to watch next

As tokenization marches from pilot projects to greater market participation, investors and builders will be watching several key dynamics. First, whether legal frameworks and settlement finality standards crystallize in a way that reduces fragmentation and reassures traditional market participants. Second, whether liquidity continues to grow in real‑world asset tokens to the point where they rival or surpass traditional offline channels. Third, which infrastructure—clearing, custody, identity verification, and cross-border rails—will emerge as the de facto backbone for scalable tokenized markets. And finally, whether central banks and regulators adopt a calibrated stance that supports innovation without sacrificing financial stability.

In the near term, a handful of large players and platforms—creators of RWA markets, major asset managers experimenting with tokenized funds, and exchange operators expanding tokenized trading—will likely shape the pace and direction of adoption. The IMF’s findings suggest this is not a one-off tech experiment but a continental shift in how assets are created, traded and settled—one that demands careful risk governance as the ecosystem matures.

Readers should monitor developments around legal clarifications for tokenized ownership, concrete liquidity metrics for tokenized assets, and the progression of compliant standards like ERC-3643 as the market seeks a balance between efficiency and resilience.

Polymarket has partnered with oracle provider Pyth Network to launch traditional asset markets on its platform.

Summary

- Polymarket partnered with Pyth Network to introduce equity, commodity, and stock-linked contracts.

- The new markets include daily up or down and closing price contracts that reset at the end of each trading session.

- Pyth Network is providing real-time price feeds from trading firms and market makers to serve as the resolution layer for the new contracts.

According to an Apr. 2 announcement, the latest addition brings daily up-or-down and closing price contracts for major equity indexes, alongside commodities such as gold and oil, and US-listed stocks. Outcomes on these contracts are determined using Pyth’s real-time price feeds, and the markets reset at the end of each trading session.

Pyth Network will act as the resolution layer for these markets, replacing manual or exchange-specific references with a standardized data source aggregated from trading firms and market makers.

Simultaneously, Pyth has launched a data interface called Pyth Terminal, allowing users to track live price feeds and the reference values used to settle markets on Polymarket.

Oracle networks like Pyth bring off-chain data such as prices, foreign exchange rates, and commodities onto blockchains. These feeds are widely used across decentralized finance, prediction markets, and tokenized asset platforms, and have seen growing adoption, including by US government agencies.

PYTH price rallied over 70% after the announcement, while its market capitalization moved past $1 billion.

The latest products on Polymarket were launched as the platform continues to cement its position as a leading prediction market operator.

Last month, the project secured a $600 million investment from Intercontinental Exchange, the parent company of the New York Stock Exchange, as part of a broader multibillion-dollar commitment.

Meanwhile, Polymarket made investments of its own by acquiring DeFi infrastructure startup Brahma for an undisclosed sum.

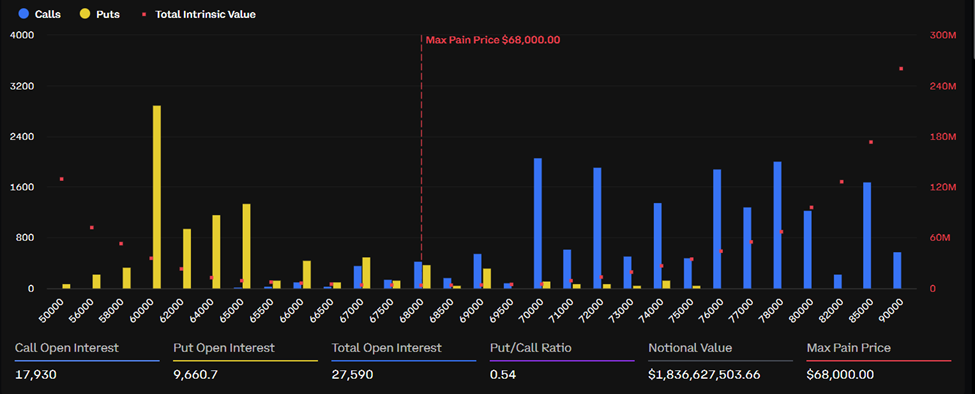

A whale accumulated more than 2,000 Bitcoin (BTC) put contracts overnight, targeting a move below $66,000, just as over $2.15 billion in Bitcoin and Ethereum (ETH) options settle on Deribit today, April 3.

The back-to-back repositioning signals that at least one large player sees downside risk in BTC’s current price range, even as call open interest still outnumbers puts across both assets.

Why the Whale Trade Matters

Options analytics platform Greeks.live flagged the position shift on April 2, noting the same whale had closed a profitable long trade hours earlier before pivoting bearish.

Per the analysts, the whale entered a long position at $66,000 and exited above $68,000, booking a confirmed profit.

Within hours, a trader of comparable size began accumulating put contracts, this time betting on a move lower.

The rapid reversal is notable. A whale exiting a winning trade and immediately loading the opposite direction suggests a view that the $66,000–$68,000 zone is a resistance ceiling, not a launchpad.

With BTC trading at $66,575 and its max pain level set at $68,000, the spot price sits $1,425 below the level where options sellers profit most. If BTC fails to close that gap before settlement at 08:00 UTC, the bearish whale’s puts gain value.

The Expiry Data

Bitcoin accounts for $1.84 billion of today’s total notional value, with 27,590 contracts outstanding. Call open interest stands at 17,930 against 9,600 puts, giving a put-to-call ratio of 0.54.

The call skew still leans bullish in aggregate, but the whale’s 2,000-contract put position adds concentrated downside weight near the $66,000 strike.

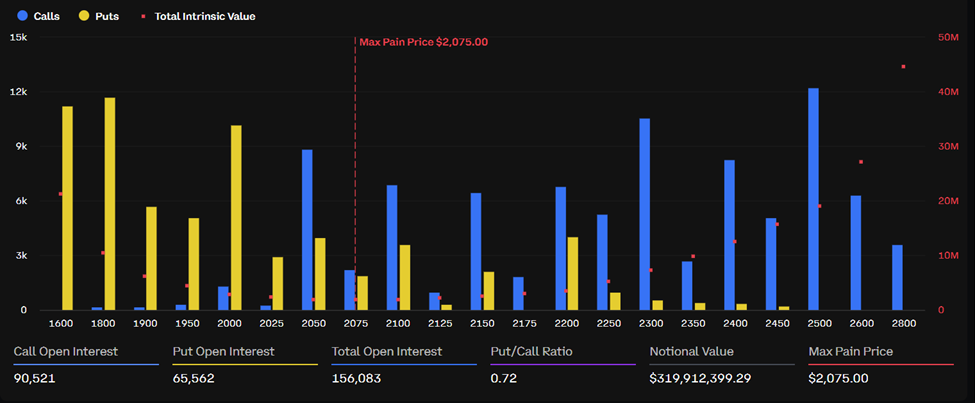

Ethereum’s expiry is smaller but similarly structured. With $319.9 million in notional value and 156,083 total contracts, ETH trades at $2,052 against a max pain level of $2,075. Its put-to-call ratio of 0.72 points to heavier downside hedging than BTC’s.

“Yesterday, the whale closed out the two positions on the right side… The whale entered the position at 66K and closed it out above 68K — this trade was a resounding success. Starting late last night, a whale of similar size began buying put options again, with over 2,000 contracts expiring today, targeting a price below 66K,” the analysts stated.

What Comes Next

Options settle at 08:00 UTC on Deribit. The hours leading up to that window typically generate the sharpest gamma hedging activity, pulling prices toward max pain.

For BTC, that means a potential drift toward $68,000 if bulls hold ground, or a break below $66,000 if the whale’s put bet plays out.

The post Whale Turns Bearish Ahead of $2 Billion Bitcoin and Ethereum Options Expiry appeared first on BeInCrypto.

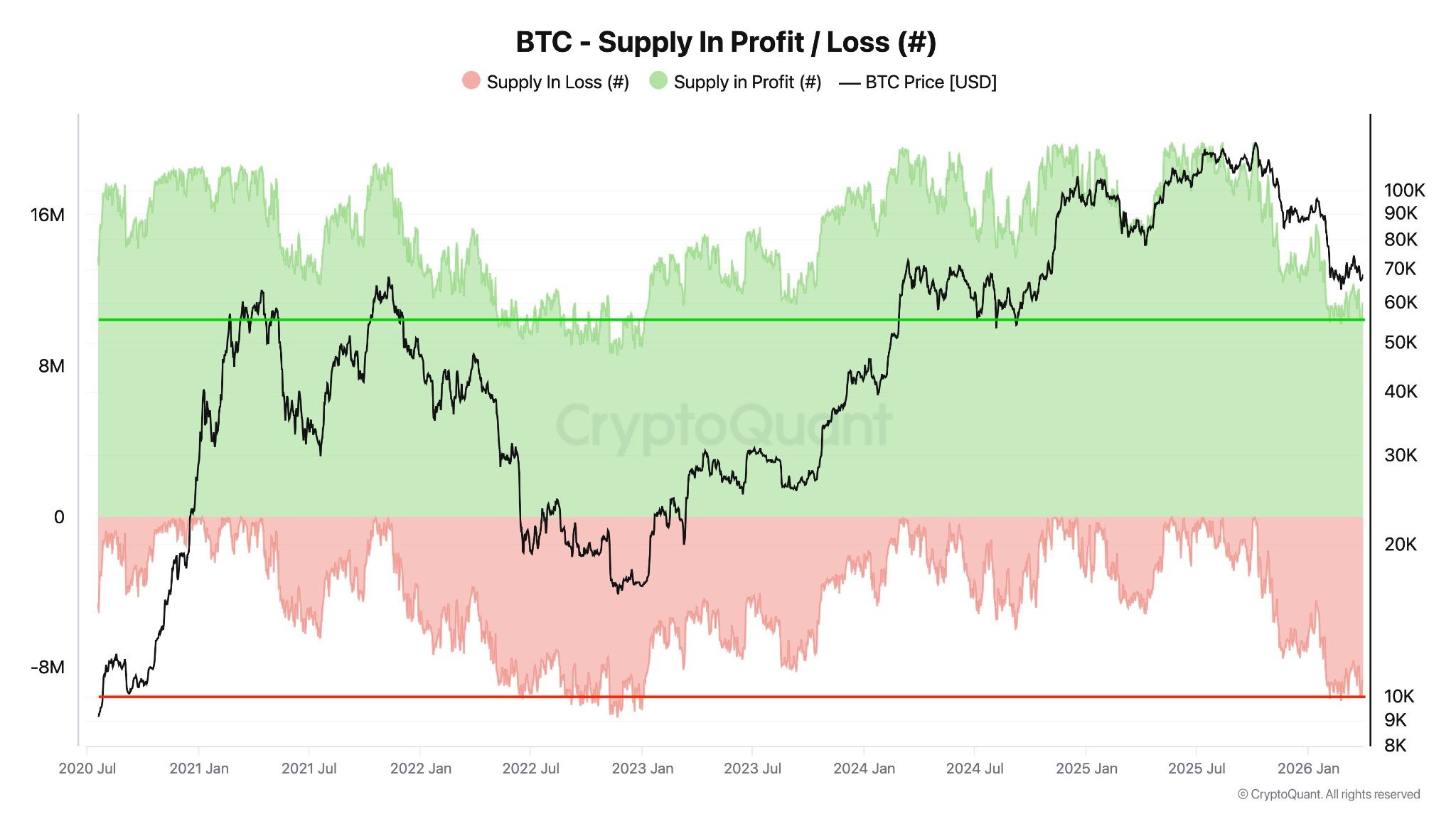

The amount of Bitcoin supply in profit and loss is now getting closer to levels typical of a bear market, according to a CryptoQuant analyst.

There are currently about 11.2 million Bitcoin (BTC) in profit. The previous bear market recorded 9 million BTC in profit at its lowest point, CryptoQuant analyst “Darkfost” said Thursday.

CryptoQuant data also shows there are about 8.2 million Bitcoin at a loss, with Glassnode data confirming it’s at levels not seen since late 2022.

“This is quite significant, considering that during the last bear market this figure reached about 10.6 million BTC,” Darkfost said.

Analysts have been debating whether Bitcoin has further to fall this year amid growing global turmoil. Bitcoin metrics that show a movement toward previous cycle lows could suggest that a market bottom is getting closer.

“This suggests that the market is reaching a notable level of undervaluation, comparable to the conditions observed during the previous bear market,” the analyst added.

Analyst sees increasing market stress, not undervaluation

However, Andri Fauzan Adziima, research lead at the Bitrue exchange, argued the data signals “increasing market stress, not immediate undervaluation.”

True capitulation bottoms saw deeper pain, he told Cointelegraph. The supply in loss in 2022 was greater than 50% and the supply in profit was around 45% or lower, while metrics such as net unrealized profit/loss (NUPL) and market value to realized value ratio (MVRV) were at “extremes.”

“Current data points to early/mid-bear transition (potential structural bottom near $55,000), with more downside or consolidation likely before a full reset.”

Related: Bitcoin’s drawdown is ‘less dramatic’ this cycle, Fidelity says

Data also shows Bitcoin has declined by about 52% from its all-time high this cycle, much less than previous bear markets, which saw 77% to 84% drawdowns from their cycle highs.

Strong dollar hampering recovery

Bitcoin author Timothy Peterson commented on X that Bitcoin “tends to struggle when the dollar is strong, and the Chinese yuan is weak.”

He added that this was due to tighter global liquidity, with higher dollar yields attracting capital into cash and bonds and cautious investor sentiment as China eases policy.

That only changes when US interest rates fall and “dollar yield loses its attractiveness,” which is not likely until the second half of 2026 or more likely 2027, he said.

The US dollar index (DXY) has gained about 5% over the past two months, according to TradingView.

For years, decentralized finance sold a simple, powerful idea: anyone, anywhere, can access financial services without gatekeepers. No banks, no approvals, no identity checks—just code and capital.

But beneath the surface, something is changing.

A growing number of protocols are quietly introducing permissioned layers—KYC-gated pools, whitelisted participants, and compliance-driven infrastructure. It’s subtle. Gradual. Easy to miss.

Yet it may redefine what DeFi actually is.

The Shift No One’s Loudly Talking About

Permissioned DeFi doesn’t arrive with headlines. It slips in through features like:

- KYC Pools – Liquidity pools restricted to verified users

- Whitelisted Access – Only approved wallets can interact with certain products

- Compliance Layers – Protocol-level rules aligning with regulatory frameworks

At first glance, these look like optional features. In reality, they signal a deeper evolution:

DeFi is adapting itself to fit inside the traditional financial system.

Why This Is Happening

Let’s be blunt—pure permissionless systems make regulators nervous.

Institutions want exposure to DeFi yields, but they need:

- Legal clarity

- Counterparty accountability

- Risk controls

Permissioned layers act as a bridge:

- They let institutions participate without violating compliance rules

- They give regulators something to work with

- They reduce the “wild west” perception of DeFi

In short, capital is forcing compromise.

What Changes (And What Breaks)

This shift isn’t just technical—it’s philosophical.

1. Participation Is No Longer Universal

The original promise of DeFi was inclusion.

Permissioned systems introduce exclusion by design.

If access requires:

- Identity verification

- Jurisdiction checks

- Approval from a governing entity

Then DeFi starts to look a lot like the system it aimed to replace.

2. “Open Finance” Becomes Conditional

DeFi assumed:

If you have a wallet, you’re in.

Permissioned DeFi changes that to:

If you meet the criteria, you’re in.

That’s a massive shift. It replaces code-based neutrality with policy-based access.

3. Liquidity Fragmentation

Instead of one unified pool of capital, we get:

- Public pools (permissionless)

- Private pools (permissioned)

This can lead to:

- Uneven yields

- Reduced efficiency

- Insider advantages for approved participants

Basically, the market starts splitting into tiers.

4. Power Starts Re-centralizing

Whitelists don’t manage themselves.

Someone decides:

- Who gets access

- Who gets removed

- What rules apply

Even if governance is “decentralized,”

Control creeps back in through decision-making layers.

The Trade-Off: Growth vs Principles

Let’s not pretend this is entirely bad.

Permissioned DeFi enables:

- Institutional capital inflows

- Regulatory survival

- Scalable adoption

Without it, DeFi risks staying niche—or getting shut out entirely.

But there’s a cost:

- Less openness

- Less censorship resistance

- Less equality

So the real question isn’t whether permissioned DeFi is good or bad.

It’s this:

How much of DeFi’s core ethos are we willing to trade for growth?

The Future: Two DeFis?

We may not end up with one unified ecosystem.

Instead, expect a split:

Permissionless DeFi

- Open to everyone

- Higher risk, higher innovation

- Resistant to control

Permissioned DeFi

- Regulated and compliant

- Institution-friendly

- Controlled access

They’ll coexist—but not as equals.

One maximizes freedom.

The other maximizes scale.

Final Thoughts

Permissioned DeFi isn’t sudden; it’s a slow drift.

No dramatic announcements.

No clear line crossed.

Just small changes… that quietly redefine everything.

And if you blink, you might miss the moment when “open finance” stops being fully open.

REQUEST AN ARTICLE

OpenAI has acquired technology talk show TBPN as it looks to refine how it communicates with audiences beyond its core products.

Summary

- OpenAI has acquired TBPN, a Silicon Valley-focused tech talk show, as it expands its role in shaping public conversations around artificial intelligence.

- TBPN will continue operating with editorial independence while also contributing to OpenAI’s communications and marketing efforts.

According to an Apr. 2 announcement, the deal brings the Los Angeles-based program under OpenAI’s umbrella. Financial terms of the deal were not disclosed.

TBPN, hosted by John Coogan and Jordi Hays, streams live for three hours each weekday and features interviews with founders, venture capitalists, and senior technology executives. Guests in recent months have included Mark Zuckerberg, Satya Nadella, and Sam Altman, underscoring the show’s growing influence within the tech ecosystem.

OpenAI’s leadership framed the acquisition as part of a push to shape how conversations around artificial intelligence unfold.

In an internal memo, Fidji Simo, OpenAI’s chief of strategy, said the company sees a need for “real, constructive conversation” as AI systems become more embedded in society. The company believes TBPN can help create that space while also expanding its reach.

Despite the ownership change, OpenAI has emphasized that TBPN will retain full editorial control.

Behind the scenes, the show is expected to contribute to OpenAI’s communications and marketing efforts beyond its daily broadcasts. Simo noted that TBPN’s track record in brand storytelling and its close view of industry trends played a role in the decision.

Founded in October 2024, TBPN began daily livestreaming in March 2025 and has since carved out a niche audience. Each episode draws roughly 70,000 viewers across platforms such as X, YouTube, and Spotify.

While modest compared to traditional financial media, the show has gained traction among technology leaders who see it as more aligned with industry perspectives than legacy outlets like Bloomberg or CNBC.

The acquisition comes shortly after OpenAI closed a $122 billion funding round led by Amazon, Nvidia, and SoftBank.

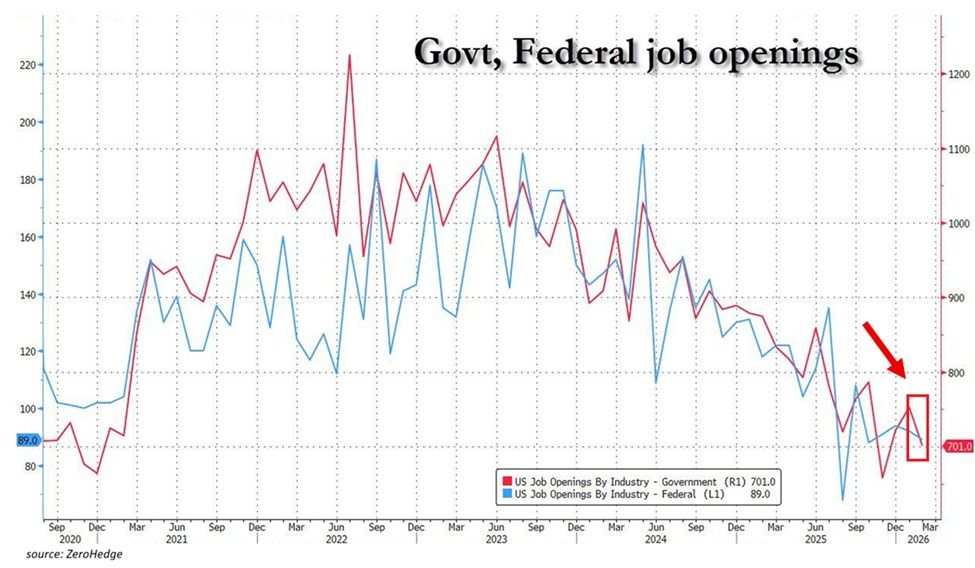

The US job market is showing alarming deterioration. According to The Kobeissi Letter, government job openings dropped 51,000 in February to 701,000.

This marked the second-lowest reading since December 2020. Available government vacancies have fallen 524,000 since their 2022 peak and now sit at pre-pandemic levels.

In addition, federal government openings fell to 89,000, the second-lowest since the pandemic low. This level is also in line with readings from 2017 and 2018.

Follow us on X to get the latest news as it happens

“Meanwhile, the government hiring rate stood at 1.4%, one of the lowest levels since mid-2020 and matching the 2016 and 2017 lows. Government hiring is frozen,” the post read.

Meanwhile, the private sector is shedding jobs at scale. Oracle reportedly laid off up to 30,000 employees on March 31. Amazon cut 16,000 corporate roles in January, and Block eliminated over 4,000 positions. These were just some of the many companies that made job cuts.

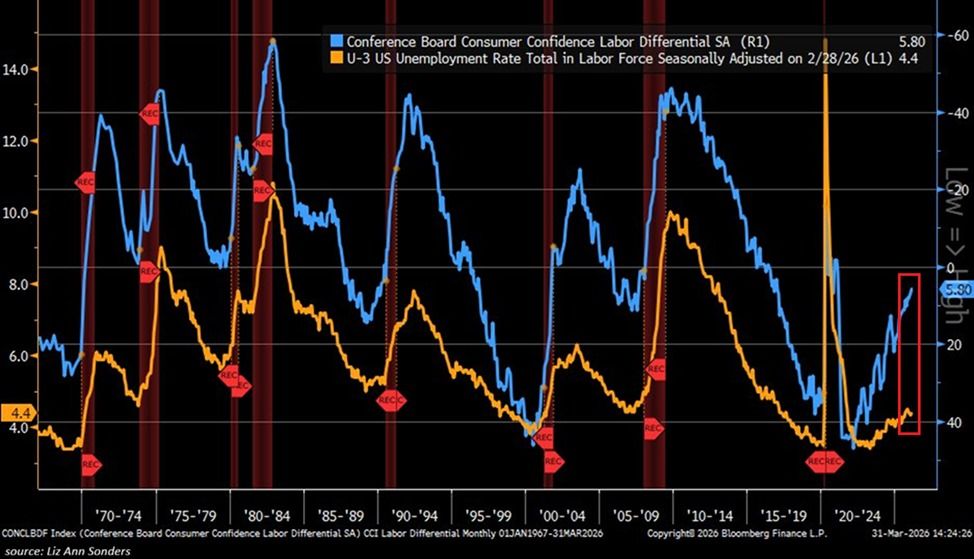

Consumer Sentiment Signals Trouble Ahead

In a separate post, The Kobeissi Letter suggested that forward-looking indicators” point to a further increase in US unemployment.” The Conference Board’s March survey showed that only 27.3% of consumers described jobs as “plentiful.”

This was a marginal uptick from 26.7% in February, but still well below the roughly 55% who felt that way in 2022. At the same time, 21.5% said jobs were “hard to find,” up from approximately 10% over the same period.

The gap between these two readings, known as the labor market differential, fell to just 5.8 points. That represents the lowest level since the 2020 pandemic.

The Kobeissi Letter noted that historically, this indicator has been one of the most reliable leading signals of rising unemployment.

“Furthermore, current levels in this indicator have only been seen prior to or during a US recession since the 1990s. The job market is set for even more weakness,” the analysts added.

With these indicators pointing in the same direction, the March jobs report will be closely watched to determine whether underlying deterioration is cyclical or marks a deeper shift.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US Job Market Flashes Warning Signs Last Seen During 2020 Pandemic appeared first on BeInCrypto.

Circle plans to launch its own version of wrapped Bitcoin on the Ethereum network to target institutional markets.

Summary

- Circle plans to launch cirBTC on Ethereum, a 1:1 bitcoin backed wrapped asset targeting institutional markets.

- Wrapped Bitcoin allows BTC to be used on networks like Ethereum, giving institutions access to decentralized finance applications.

In a Thursday announcement, stablecoin issuer Circle said it plans to introduce cirBTC, a token that is backed 1:1 by bitcoin and aimed at over-the-counter desks, market makers, lending protocols, and other institutional participants, framing the asset as a “highly secure and neutral version of wrapped BTC.”

Wrapping allows a native asset like Bitcoin to be tokenized and used across other blockchains. In this case, wrapped Bitcoin lets BTC be brought onto networks such as Ethereum, which gives users access to decentralized finance applications.

The token will also launch on Circle’s layer-1 blockchain Arc and integrate with the Circle Mint platform.

Circle joins a growing list of participants that have introduced wrapped Bitcoin as demand for decentralized finance continues to expand among institutional users.

The sector is currently led by BitGo’s Wrapped Bitcoin, which currently holds a market capitalization of about $8 billion.

Coinbase also launched its own version, Coinbase Wrapped Bitcoin (cbBTC), in September 2024, which has since grown rapidly to reach a market capitalization of $5.9 billion. Last year, Coinbase launched Wrapped ADA (cbADA) on the Base blockchain to facilitate cross-chain liquidity.

Meanwhile, several other exchanges have released their own wrapped assets, including Kraken Wrapped BTC (kBTC), Binance Wrapped BTC (BBTC), Bitget Wrapped BTC (BGBTC), and OKX Wrapped BTC (okBTC), among others. These offerings are often paired with proof-of-reserve transparency to assure institutional traders that the underlying assets are held in secure, 1:1 custody.

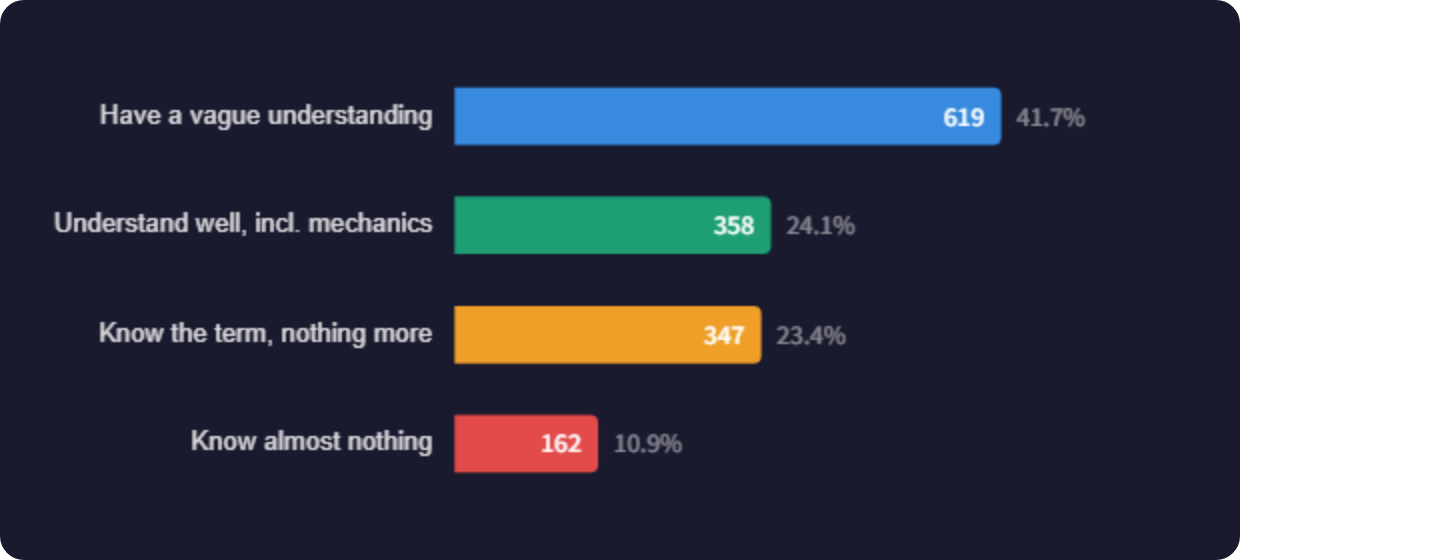

Japanese Gen Z stands out as the most scam-conscious generation when it comes to crypto. A new survey of 1,486 people across Japan found that younger users are far more alert to fraudulent pitches on social media than their older peers.

The gap between generations reveals that Japan’s crypto trust problem is not uniform — it varies by age and online habits.

Gen Z Watches for Scams, Boomers Struggle With Basics

The survey, conducted by Tokyo-based consulting firm Clabo in February 2026, asked respondents why they view crypto as suspicious. The top answer overall was “I don’t understand how it works,” chosen by 23.3% of respondents. Price swings came second at 21.1%, followed by fraud concerns at 19.2%.

But generational breakdowns tell a different story. Gen Z respondents flagged social media scams as their primary worry. They encounter fake giveaways and shady promotions on platforms they use daily. Older cohorts, including Japan’s bubble generation, pointed instead to the complexity of blockchain technology itself.

Millennials showed the highest rate of actual crypto investment among all age groups. They also reported the most active information-seeking behavior.

Across all groups, half of the respondents said they had never invested in crypto. Only 33.7% said they currently hold digital assets. Another 15.7% said they once invested but have since stopped.

YouTube Leads for Investment Decisions

When it comes to where people get crypto news, traditional news sites ranked first at 38.4%. Social media followed at 36.7%, with YouTube at 31.6%. But for actual investment decisions, YouTube jumped to first place at 27%.

The survey suggests that Japan’s crypto industry still faces a basic education gap. Clabo, which offers wallet recovery and security consulting, recommended more accessible educational content tailored to each generation’s specific concerns.

The post Japanese Gen Z Fears Crypto Scams More Than Any Other Generation appeared first on BeInCrypto.

Extreme poverty in the Asia-Pacific region has declined but inequality remains high, says OECD

Paper vs. Physical: The $34 Gap Exposing the True Cost of the Iran Oil Shock

Jessa Duggar Slams Brother Joseph Amid Molestation Charges

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

XRP ITS OVER!? I CAN PROMISE YOU AREN’T READY FOR THIS!!!

Tom Lee Just Warned That Bitcoin Will Crash Before It Does Something Nobody Has Ever Seen Before

Next Financial Crisis WORSE Than 2008 – $3T Private Credit Collapsing, $4.6B TRAPPED

-

NewsBeat6 days ago

NewsBeat6 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat12 hours ago

NewsBeat12 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Crypto World1 day ago

Crypto World1 day agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Business6 hours ago

Business6 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Business1 day ago

Business1 day agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Politics3 days ago

Politics3 days agoShould Trump Be Scared Strait?

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

You must be logged in to post a comment Login