Crypto World

Solving Bitcoin’s gas issue (without a fork)

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Every smart contract platform has a fee asset baked in. For example, Ethereum (ETH) has ETH, Solana (SOL) has SOL, but with Bitcoin (BTC), however, things get messy. If you want expressive apps, you usually end up adopting a second network’s economics.

Summary

- Bitcoin doesn’t price computation, only block space. Unlike Ethereum or Solana, BTC’s fee market is built around sat/vB for transaction inclusion, not metering smart contract execution.

- Execution can move off-chain while settlement stays on Bitcoin. Systems like OpNet run contract logic in a Wasm VM while anchoring payments and final state changes through normal BTC transactions.

- BTC can function as the gas asset without a new token. By pricing execution costs in satoshis and settling interactions through Bitcoin transactions, apps avoid creating a second fee economy.

On Stacks, for example, you pay fees in STX. On EVM-style Bitcoin layers, you might be told that BTC is the gas token, but it’s typically an L2-native representation with EVM-like conventions (including 18 decimals), and you’re still operating inside that L2 environment. Bitcoin itself, meanwhile, already has a clean fee market, where users bid for block space in sat/vB, and miners prioritize higher fee rates.

With this in mind, what if a smart contract interaction could be initiated and paid for as a normal Bitcoin transaction, with fees in BTC terms (no extra gas token or fork) while the smart part runs elsewhere and stays provably tied back to Bitcoin? OpNet is setting out to provide an answer.

Bitcoin doesn’t meter compute (that’s a problem)

Bitcoin’s fee market is excellent at one thing: pricing block space. You compete in sat/vB, miners pick the highest fee rates, and the network stays simple and adversarially robust. What Bitcoin does not do is run a general-purpose execution environment where the chain can measure and charge for arbitrary computation. Bitcoin Script is deliberately stateless and not Turing-complete, specifically lacking loops or gotos, so every node can validate scripts predictably without opening the door to unbounded computation.

That’s why most Bitcoin smart contract approaches end up placing execution on a separate system that can meter compute and run a fee market of its own. Once you have that separate execution layer, it usually comes with a separate fee asset (Stacks, for instance, charges fees in STX).

This isn’t ideal, and a system where you could keep payment within Bitcoin’s native fee market while moving execution elsewhere would be preferable.

Execution isn’t what Bitcoin needs to do

Once you accept that Bitcoin Script is intentionally limited (stateless and not designed for unbounded computation), you start thinking about how to make Bitcoin settle the results and the payments.

Indeed, execution can happen in a dedicated virtual machine that’s built to run smart contract logic deterministically, while Bitcoin remains the base layer that timestamps, orders, and prices the interactions through its existing fee market. In OpNet’s design, contract logic is evaluated by a Wasm-oriented VM (OP-VM), while the broader node stack is explicitly built to manage and execute smart contracts using Bitcoin’s existing transaction and UTXO mechanics.

Crucially, this isn’t paired with a new fee asset. Bitcoin doesn’t need to meter computation to be the gas currency. It needs to be the final settlement layer that everything ultimately pays into and anchors to.

What a BTC-paid contract call looks like

Our interaction model follows a simulate-then-spend flow rather than a conventional smart contract execution pattern, with the final execution step taking place as an actual Bitcoin transaction. First, your app calls a contract method in simulation mode. That request goes through a provider to an OPNet node, which executes the contract in its VM and returns a CallResult (including gas/fee estimates) without broadcasting anything to Bitcoin.

If the call is state-changing, you take that CallResult and send it as an execution. At this point, the library builds a Bitcoin transaction, signs it, and broadcasts it to the Bitcoin network. Two points are worth remembering:

- Miner fees are Bitcoin-native. You choose a feeRate in sat/vB, optionally add a priorityFee in sats, and set a hard cap on fee spending via maximumAllowedSatToSpend (the parameter is literally named maximumAllowedSatToSpend).

- The contract target is expressed as a P2OP-style contract address. The contract instance exposes its p2op address format, and transactions reference a “p2op contract address” as the contract destination.

Meanwhile, OpNet’s own compute metering still exists. But it’s priced in satoshis (estimated SATS Gas, refunds in SATS, etc.), so the unit never drifts into a separate token economy.

Less friction, cleaner incentives

Users no longer have to adopt a second fee economy just to interact with apps. On Bitcoin, fees are already an auction for block space, priced per byte and paid to miners. When contract calls are just Bitcoin transactions, you’re back on familiar ground (with sat/vB fees, mempool churn, and miner incentives), without having to learn a separate gas token market.

Also, the tooling leans into standard Bitcoin workflows such as UTXO handling, provider connections, and even offline/cold signing. Contracts live in a Wasm runtime and are written in AssemblyScript, aiming for Solidity-like expressiveness without pretending Bitcoin Script suddenly became a VM.

Bitcoin as gas, without a second token

The claim that BTC cannot function as gas usually rests on the assumption that the base layer must meter computation to price it. Bitcoin does not meter computation; it meters block space and settles value.

The solution is to let a virtual machine handle execution deterministically, and then route every state-changing interaction through a standard Bitcoin transaction, where fees are expressed in familiar terms such as sat/vB and capped in satoshis. In our case, this is implemented at the client level through parameters like feeRate and maximumAllowedSatToSpend.

So maybe BTC-as-gas is truly plausible. Fees stay BTC-native from end to end, while the contract runtime stays WebAssembly-based (AssemblyScript → Wasm), which keeps the logic expressive without changing the fee currency.

The Bank of England’s (BOE) position on stablecoins is evolving to a more friendly stance, but according to the bank’s deputy governor, constructive dialogue with the industry is still lacking.

The UK’s central bank launched a consultation on stablecoins in November last year. Some of the proposed requirements drew the ire of crypto industry representatives, who claimed they could stifle innovation.

Over the past few months, the bank has been working with industry groups to develop its stance on stablecoins. These include revising backing requirements and rethinking account limits.

Some industry observers believe that the bank is coming around on stablecoins, but there is still work to be done.

Bank of England open to feedback on stablecoin risk

On Nov. 10, 2025, the BOE released a document outlining its vision for a stablecoin regulatory regime. This came two years after an initial discussion paper which, according to the bank, included the perspectives of “banks, non-bank payment service providers, payment system operators, trade associations, academia, and individuals.”

At the time, industry observers told Cointelegraph that BOE was overstating the perceived risks that stablecoins pose to the UK economy. Tom Rhodes, chief legal officer at UK-based stablecoin issuer Agant, said at the time that the bank was “disproportionately cautious and restrictive.”

One of the more controversial measures was stablecoin holdings limits, namely 20,000 pounds for individuals and 10 million pounds for businesses that accept it as a form of payment.

Now, it appears that the bank is coming around. Speaking before the House of Lords Financial Services Regulation Committee on Wednesday, BOE Deputy Governor Sarah Breeden told MPs that it is open to reconsidering those limits.

Breeden said that the proposed limits were to mitigate the risk of a large migration of deposits to stablecoins, which has the potential to destabilize banks.

“We proposed holding limits as a way of managing that risk. We are open to feedback on other ways of achieving it,” she said.

However, feedback itself also seems to be an issue, at least according to Breeden. She said, “The pressure from the industry to do it in a different way is very real. What we’ve been a bit disappointed with, is nobody said, ‘Why not do it this way?’”

“I don’t think we’ve yet had constructive engagement on a different way to solve the problem that I might have hoped for. Instead, what we’ve had is ‘don’t do this,’ and ‘I understand why you want to do something’ as opposed to filling the gap.”

Rhodes told Cointelegraph on Thursday that this isn’t necessarily the case. “Over the past two years we have reviewed thousands of pages of consultations from the FCA and the Bank, attended numerous roundtable meetings, and submitted hundreds of pages of input both ourselves and as part of trade associations.”

He said that the main challenge for the industry and regulators is that they are making a “comprehensive regulatory regime for a market that has yet to develop.”

Rhodes explained:

“It’s not possible to provide concrete data in the circumstances, which is why lighter touch principles-based regimes are appropriate at this nascent stage.”

Nick Jones, the founder and CEO of UK-based digital assets platform Zumo, said, “Industry groups have been working hard, and to tight deadlines, to make tangible recommendations.”

He said the feedback could be more constructive if the bank followed the Financial Conduct Authority’s (FCA) Spring model. These time-boxed workshops focus on practical applications of the technology to answer regulators’ questions.

The ‘multi-moneyverse’ and what’s next for stablecoins in the UK

Breeden opened her remarks with assurances that at the bank, “we do want to see tokenized money issued by non-banks.”

“We can have what I call a ‘multi-moneyverse’ with greater choice and competition today.”

Such a system, she said in a September speech, is “characterised by choice across different forms of money and payment; with technology driving faster, cheaper, and more innovative payments for the benefit of business, households, and users of financial markets; and — critically — with the whole system underpinned by trust in money itself.”

Inter-monetary competition and its purported benefits have been a core argument from the crypto industry. Rhodes said, “Stablecoins being part of a competitive multi-moneyverse represents a substantial and positive evolution in the Bank’s thinking.”

Related: UK dodges ‘US malaise’ as regulator finalizes crypto rules

However, Rhodes noted that this was in “sharp contrast” to BOE Governor Andrew Bailey’s statements, where “he doesn’t see stablecoins as a substitute for commercial bank money.”

Jones said, “Over time, we’ve seen the Bank of England’s scepticism towards digital assets start to dissipate.” It’s “encouraging” that the central bank is more receptive to competing forms of money and that pound sterling-backed stablecoins can co-exist with fiat money.

“It’s clear that different emerging types will fit different use cases — for example, large institutional capital is more comfortable with tokenised deposits while smaller retail payments companies can tap into the network effect of stablecoins,” he said.

The next step, per Rhodes, is a final policy position from the BOE, but revisions are still possible.

The industry is still pushing to remove the holding caps and scrap bank-like capital rules for issuers. Jones said that the latter “are inappropriate for fully-backed issuers, and should be replaced with oversight focused on reserve quality and transparency.”

They also want a reconsideration of reserves. So far, BOE requires issuers to hold 40% of reserve assets in unremunerated Bank of England deposits and up to 60% in high-quality, short-term UK government debt.

This is based on past runs like the Silicon Valley Bank collapse in 2023 which resulted in the USDC stablecoin losing its peg. Breeden told Reuters, “Those numbers are broadly in line with that. That’s why we’re proposing 40% rather than a smaller number.”

“Regulators should perhaps consider remunerating a portion of the 40% held at the Bank of England to help maintain commercial viability,” said Jones.

“The UK can be one of the leaders in stablecoins, but only if regulation is proportionate and competitive.”

Magazine: All 21 million Bitcoin is at risk from quantum computers

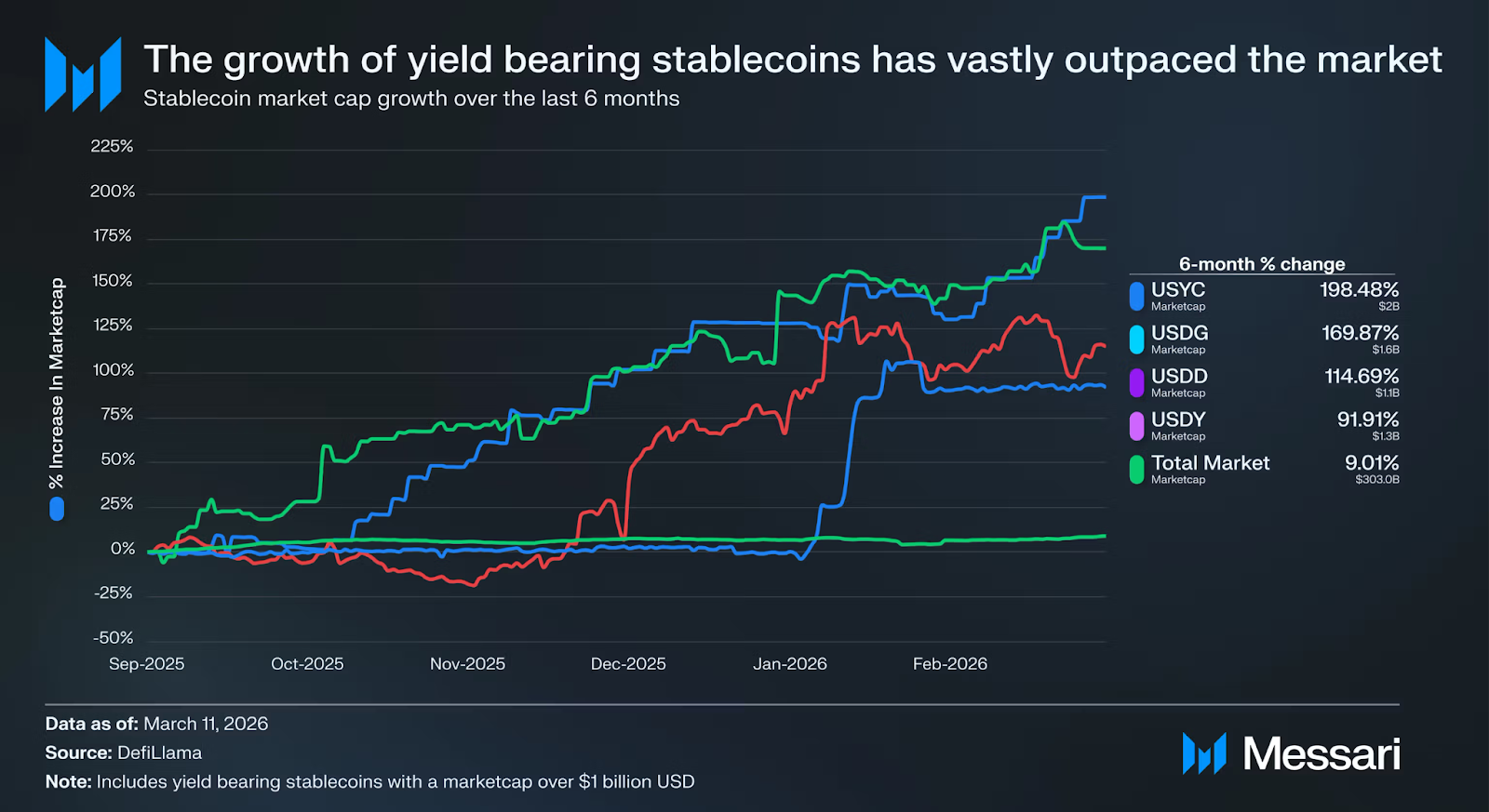

Yield-bearing stablecoins are growing faster than the broader stablecoin market, according to Messari, as Washington remains divided over how crypto-linked yield should be treated under US law.

Yield-bearing stablecoins have outpaced the growth of the broader stablecoin market 15-fold over the past six months, according to a Messari research report published on Thursday.

The increase was driven by a 198% rise in the market cap of Circle’s USYC (USYC), a 169% increase in Paxos’ Global Dollar (USDG), a 114% rise in the value of the Tron DAO-linked Decentralized USD (USDD), and a 91% rise in Ondo Finance’s Ondo US Dollar Yield (USDY). The overall stablecoin market capitalization rose 9%.

Messari said the largest yield-bearing stablecoins are starting to function more akin to money market funds or bank deposits. “The winners don’t do payments,” Messari said, adding that the largest issuers focus their offer on a single asset, rather than payment-related use cases.

Yield-bearing stablecoins started outpacing the growth of the stablecoin supply in mid October 2025, Messari said. The trend suggests rising demand for blockchain-based US dollar products that offer yield without direct exposure to broader crypto volatility.

Yield stablecoins are currently worth a cumulative $22.7 billion, after their market capitalization rose 11% over the past 30 days, according to Stablewatch data.

While this marks a two-fold increase overthe $11 billion market capitalization reached in May 2025, the $22.7 billion value of yield-bearing stablecoins only accounts for about 7.4% of the total $303 billion stablecoin market capitalization, up from 4.5% in May last year.

Among the largest yield-bearing stablecoins by value are Sky’s (sUSDS), Ethena’s (sUSDe) and Maple’s Syrup USDC, according to DefiLlama.

In terms of yield, Maple’s Syrup USDC led this week with a 4.54% annual percentage yield, followed by Maple USDT with a 4.17% APY, Sky Lending’s SUSDS with a $3.75% APY in third place and Ethena’s USDe with 3.49% APY, according to Messari.

Related: Stablecoin payments startup Kast raises $80M at $600M valuation: Report

Lawmakers at odds over stablecoin yield regulations

Despite the growing demand, US lawmakers remain at odds over the market structure bill’s provisions related to yield-bearing stablecoins.

On Thursday, US Senator Majority Leader John Thune reportedly said he doesn’t expect the chamber to move forward with the crypto market structure bill before April.

Yield-bearing stablecoins have become a key sticking point in the debate, with banking groups warning they could create a loophole that pulls deposits away from traditional banks.

The Senate Banking Committee postponed its markup in mid-January as bipartisan negotiations continued, drawing criticism from US President Donald Trump for delaying the bill.

Related: Stablecoin inflows rebound to $1.7B as Washington battles over yield rules

The Digital Asset Market Structure Clarity Act, known as the CLARITY Act, is designed to provide a clear regulatory framework for digital assets. The House of Representatives passed the measure on July 17, 2025, and it has been under debate in the Senate since.

The US’s federal stablecoin framework, the GENIUS Act, prohibits issuers from paying interest or yield for holding a payment stablecoin, but still allows third-party platforms to offer reward programs tied to stablecoin holdings. The act was signed into law on July 18, 2025.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

Some of the involved cryptocurrencies nosedived by over 80% after the disclosure.

The world’s largest cryptocurrency exchange announced a major delisting, following which most affected cryptocurrencies collapsed by double digits.

Prior to that, the firm temporarily suspended certain withdrawals and deposits and implemented additional amendments to its platform.

The Binance Effect

Binance Alpha (a dedicated platform inside the exchange’s ecosystem that showcases early-stage crypto projects) removed 21 altcoins, including WorldShards (SHARD), FreeStyle Classic (FST), Alliance Games (COA), BNB Card (BNB Card), MilkyWay (MILK), Hyperbot (BOT), and many more.

The company clarified that the sale of the impacted tokens will still be allowed after the removal. At the same time, it warned users to conduct proper research before trading the aforementioned coins to avoid any scams and protect their funds.

As is typically the case, many of the delisted digital assets headed south shortly after the disclosure. After all, Binance is the largest crypto exchange, and withdrawing support usually results in reduced liquidity, diminished availability, and a damaged reputation. MILK and SHARD fell by 6-7% daily, whereas FST and BNB Card nosedived by 70-80%.

A similar reaction was observed in late 2025 when Binance disallowed all services with Kadena (KDA), Flamingo (FLM), and Perpetual Protocol (PERP). Similar to FST and BNB Card, the involved altcoins crashed by double-digit percentages immediately after the news broke.

Other Recent Efforts

Earlier this week, the exchange supported an upgrade and temporarily paused withdrawals and deposits on the Ethereum network. The process was expected to take about an hour, after which operations were supposed to resume smoothly.

You may also like:

This is a routine procedure that Binance has executed flawlessly many times before. Over the years, it has taken similar measures to support upgrades across various ecosystems, including Cardano, BNB Smart Chain, and others.

Prior to that, Binance issued numerous listing announcements focused on U (United Stables) – a stablecoin launched last year and pegged to the American dollar. In January, it expanded the list of trading choices offered on its Spot section with the BNB/U, ETH/U, KGST/U, and SOL/U pairs.

In February, it added XRP/U, SUI/U, ASTER/U, and PAXG/U, while earlier this month it opened trading for AVAX/U, LINK/U, LTC/U, PAXG/U, and ZEC/U.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Key Takeaways

- Year-over-year core PCE inflation registered 3.1% in January, exceeding the Federal Reserve’s 2% objective

- On a monthly basis, core PCE increased 0.4%, matching analyst forecasts

- Overall PCE recorded 2.8% annual growth, marginally lower than the anticipated 2.9%

- Financial markets broadly anticipate the Federal Reserve will maintain interest rates between 3.5%–3.75% during the upcoming policy meeting

- These figures predate the Iran military engagement, which has elevated crude oil costs and introduces uncertainty to future inflation trends

On March 13, 2026, the Bureau of Economic Analysis published its personal consumption expenditures (PCE) report for January. This metric serves as the Federal Reserve’s primary gauge for measuring inflationary pressures.

The core PCE measure, which excludes volatile food and energy components, climbed 3.1% on an annual basis in January. This figure aligned with expert predictions but represented an acceleration from December’s 3.0% reading. Monthly core PCE advanced 0.4%, consistent with projections.

The overall PCE measurement — encompassing all consumer goods and services — expanded 2.8% annually. This result fell marginally short of the 2.9% consensus estimate and represented a deceleration from the previous month’s velocity.

On a month-to-month basis, overall PCE increased 0.3%, in line with market expectations.

The Federal Reserve maintains an inflation target of 2%. With core PCE currently positioned at 3.1%, consumer prices continue running significantly above the central bank’s desired threshold.

Markets are pricing in that the Fed will maintain its current rate range of 3.5% to 3.75% during next week’s policy deliberations. Given the stubborn inflation readings, interest rate reductions appear unlikely in the near term.

The PCE measure has been registering higher readings compared to the Labor Department’s Consumer Price Index. This divergence primarily stems from varying methodologies for weighing housing and healthcare expenditures. PCE assigns reduced importance to shelter expenses, which have been moderating, while giving greater emphasis to medical costs, which have been climbing.

February’s CPI registered 2.4% year-over-year — a considerably more subdued figure.

What These Numbers Miss

The January data captures economic circumstances from over a month in the past. It fails to incorporate consequences from the Iran military conflict, which commenced following U.S. and Israeli aerial operations in late February.

Oil prices have surged substantially since hostilities began. Elevated crude costs typically translate to higher inflation in subsequent months.

The economic landscape faces additional complexity from broad-based tariff implementations and substantial corporate capital allocation toward artificial intelligence initiatives. Both factors are already influencing economic conditions but remain challenging to measure accurately in real time.

Paul Ashworth, Chief North America Economist at Capital Economics, observed that America’s status as a net petroleum exporter may cushion the impact of rising oil valuations. He acknowledged that while increased energy expenses could initially diminish consumer purchasing capacity, any corresponding investment gains would require time to materialize throughout the economy.

Personal consumption expenditures rose 0.4% in January compared to the previous month, surpassing forecasts. Personal income expansion, conversely, experienced modest deceleration.

Looking Forward

Fourth-quarter 2025 GDP expansion underwent substantial downward revision to merely 0.7%.

Ashworth anticipates economic recovery during the first quarter of 2026, attributable in part to diminishing headwinds from a government shutdown that occurred in late 2025.

The Federal Reserve’s upcoming interest rate determination will follow a two-day policy meeting next week. Current market indicators suggest rates will remain unchanged.

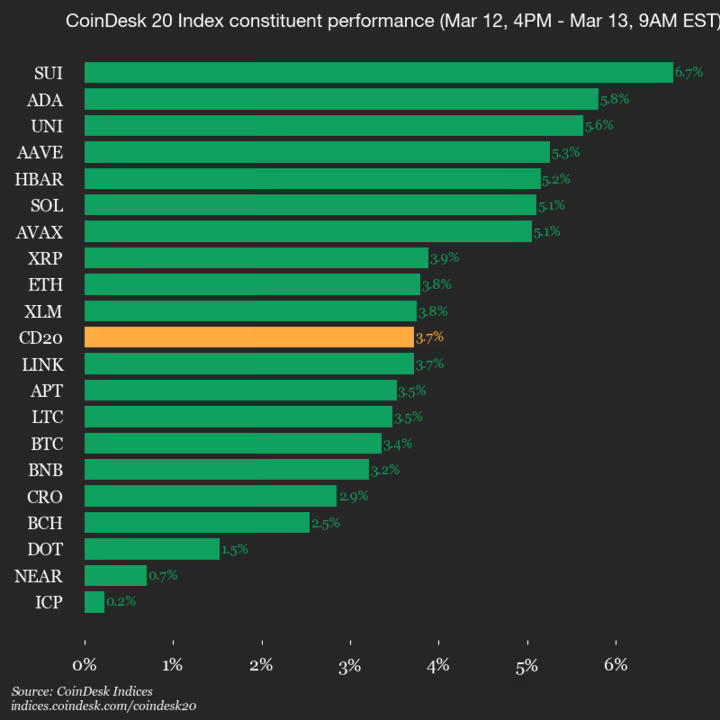

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 2077.68, up 3.7% (+74.61) since 4 p.m. ET on Thursday.

All 20 assets are trading higher.

Leaders: SUI (+6.7%) and ADA (+5.8%).

Laggards: ICP (+0.2%) and NEAR (+0.7%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

The price of oil has more than doubled in just two weeks, driving crypto platforms into a speculative frenzy that saw them list leveraged oil derivatives for overnight commodities futures experts willing to risk it all on-chain.

The results were predictable.

Tokenized crude oil perpetuals on Hyperliquid, a platform that earned initial fame from hedge fund-like copytrading and a leaderboard of leveraged degeneracy, have generated multiple, billion-dollar trading days this week.

Oil has suddenly become Hyperliquid’s second-most popular market behind only bitcoin (BTC) itself.

Open interest on Hyperliquid’s CL-USDC, a West Texas Intermediate crude futures-linked contract, exceeded $169 million. Trailing 24-hour volume still exceeded $1.2 billion at time of writing.

When crude spiked more than 30% to nearly $120 a barrel on March 9, oil short-sellers on Hyperliquid, across a 12-hour period, experienced $36.9 million in liquidations relative to just $2.1 million in long liquidations.

The largest single victim held 72,178 CL shorts worth around $7.7 million. The platform liquidated every one of them.

Not that anyone should feel particularly sorry about the loss, given the choice of venue and size in the first place. Indeed, the obviously well-capitalized trader re-opened short positions almost immediately.

Two other million-figure shorts were liquidated near the very top for oil at $120 per barrel. Another trader, rather embarrassingly, started shorting when barrels were in the $70s.

When oil hit $108 on the morning of March 9, they wiped out.

Another trader decided to label their wallet “Oil Bear” on the Hyperliquid leaderboard, turning the dangerous trade into something of an identity. The account has used multiple tens of millions of dollars worth of leverage to gamble on the commodity.

Of course, in highly volatile commodities markets, it can be just as dangerous to bet on the upside as the downside, depending on the moment. On March 11, a $6 million liquidation occurred when oil fell below $87.

Read more: Bitcoin up, Dubai real estate down since Iran war began

Hyperliquid isn’t the only venue offering crypto oil. Aster, a perpetual futures exchange on BNB Chain, launched its own CL-USDT crude oil perpetuals on March 2.

The exchange, which has earned praise from Binance founder Changpeng Zhao, ran a $10,000 oil trading competition. Binance Wallet also launched its own crude oil perpetual contract, CL-USDT, on March 7 with 0% maker fees and 1.2x Aster airdrop points.

As individual traders make and lose millions, leveraged positions can suffer liquidations within minutes. Oil perpetuals didn’t exist on these platforms a few weeks ago. Yet when the Iran war created the demand, Hyperliquid, Aster, and Binance Wallet rushed to supply it.

At $95.57 per barrel, crude oil has rallied 66% year-to-date. It was at $120 per barrel as recently as Monday.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Prediction markets have shed their experimental veneer and matured into a durable layer of crypto finance. New research shows a dramatic uptick in activity, with monthly notional volumes surpassing $13 billion by late 2025, up from under $100 million in early 2024. The growth isn’t just about more traders; it reflects broader participation across verticals and a shift in product design toward trustworthy settlement and deterministic outcomes. Even as regulators scrutinize the space, trading volume continues to rise, underscoring a persistent demand for markets that reveal information about future events. This piece examines how the industry’s next leap hinges on resolution infrastructure—how outcomes are determined, verified, and settled—as much as on liquidity or incentives. The analysis draws on a joint research effort from Dune and Keyrock that maps the trajectory of prediction markets and their evolving architecture.

Key takeaways

- Prediction-market activity has moved beyond the initial breakout phase, reaching more than $13 billion in monthly notional volume by late 2025, with diversification across sports, politics, macro indicators, and other domains.

- Trust in resolution—how an outcome is determined and settled—emerges as the central bottleneck as the market footprint expands and disputes become more common.

- Resolution architecture, including bond-based dispute mechanisms, challenge windows, and arbitration paths, is increasingly treated as infrastructure rather than a product feature.

- Industry players point to explicit, auditable resolution rules as a prerequisite for institutional participation and scalable growth.

- Despite regulatory pressure, the sector’s growth persists, indicating a mature demand for on-chain information markets backed by robust settlement guarantees.

Sentiment: Neutral

Market context: The momentum in prediction markets aligns with a broader shift toward information-centric crypto infrastructure, where reliability of resolution and governance increasingly shapes user trust and capital allocation.

Why it matters

As prediction markets scale, the quality of their resolution mechanisms becomes a practical measure of reliability. Traders buy conditional claims on future events, and the system must convert those claims into redeemable value once an outcome is determined. When resolution is slow, ambiguous, or discretionary, traders price in risk, which dampens liquidity and narrows participation to a few trusted markets. The industry is learning that resolution is not a cosmetic feature but a core component of financial infrastructure—analogous to how custody, execution, and liquidation became baseline expectations in centralized finance years ago.

The push toward explicit, auditable resolution rules has practical implications for builders and users. Platforms are redesigning governance and protocol logic to preempt disputes rather than resolve them retroactively. Bond sizes, dispute windows, and arbitration pathways are being calibrated to scale with open interest, ensuring that the cost of manipulation grows alongside demand. In this sense, resolution architecture is not just about ending a disagreement; it is about creating a predictable settlement environment that institutions can rely on and integrate into broader risk management frameworks.

These shifts echo a broader trend in crypto: moving from product features that attract early adopters to system properties that institutions expect as standard. Just as custody and execution transitioned from optional features to fundamental expectations, resolution is trending toward becoming a durable layer of the prediction-market stack. That transformation—where resolution becomes infrastructure—could unlock a wider spectrum of use cases, from hedging macro surprises to funding governance experiments with verifiable outcomes.

In this evolving landscape, the industry’s focus on resolution is underscored by concrete design choices. Optimistic oracle designs—where an answer is presumed correct unless challenged—are paired with financial incentives to deter false reporting. A fixed challenge window opens after an event, inviting disputes through post-event bonding. The more significant disputes become, the larger the bond requirement, raising the economic cost of manipulation. When disputes are unresolved, arbitration by decentralized jurors can determine the outcome and enforce it back into the oracle state. This framework, and the mechanisms that support it, are increasingly viewed as essential public goods for a robust, scalable prediction market ecosystem.

Some projects are already codifying these ideas into formal infrastructure. For example, Seer Resolution Infrastructure represents a blueprint for how resolution paths and arbitrage channels can be standardized across prediction markets. See the evolving documentation and diagrams that illustrate how resolution interacts with market creation, oracle questions, and final settlement. Such references help align market design with practical execution, reducing ambiguity at the moment of settlement and enabling more reliable capital formation around information events.

Beyond the technical specifics, the market’s appetite for reliable resolution is evident in historic patterns. The industry has observed sustained post-event activity even as high-profile regulatory actions target the space. The growth of prediction-market volumes has persisted, suggesting that traders are not simply chasing novelty but seeking durable informational endpoints and transactable risk. In parallel, classic industry players and new entrants alike are exploring standalone platforms and interoperability approaches that place resolution at the center of product strategy, rather than as an afterthought when a dispute arises.

In practical terms, the industry’s trajectory signals a shift from “product feature” to “infrastructure as a standard.” This reorientation implies a higher bar for market design: markets must be live with explicit resolution definitions, markets must scale their bonds and arbitrage paths to accommodate growing open interest, and arbitration processes should be predictable and enforceable across jurisdictions and platforms. When these properties are embedded in the protocol from day one, prediction markets begin to function more like traditional financial systems—reliable venues for price discovery and risk transfer in the realm of future events.

The broader takeaway is clear: resolution is becoming the backbone of prediction-market growth. Platforms that bake clear, verifiable rules into their core architecture are more likely to attract participants, liquidity providers, and institutional capital. The industry’s push toward resolution-focused design—from explicit outcome criteria to auditable settlement workflows—frames the next phase of growth as a maturation of financial infrastructure, rather than a series of isolated product launches.

As one senior analyst noted in the industry discourse, “Resolution is undergoing the same transition as custody and execution did years ago—no longer a differentiator but a baseline expectation.” This shift matters for anyone who uses prediction markets for information signals, hedging, or governance experiments. The promise is not merely more bets; it is more trustworthy outcomes, settled with speed and clarity that participants can rely on for financial planning and decision-making.

Analysts and builders continue to monitor the ongoing development of the resolution layer, including the interplay between optimistic finalization, bond economics, and dispute arbitrage. The goal is an ecosystem where outcomes can be deterministically converted into value in a timely, auditable manner—an essential criterion for widespread adoption and durable liquidity.

Opinion by: David Azubike, lead analyst at Blocksquare

Further reading and contextual links to ongoing research and architecture diagrams can be found in related documentation and coverage cited in the references.

What to watch next

- Publishments and updates detailing explicit resolution rules for ongoing prediction markets, including changes to bonding and challenge windows.

- Arbitration pathway enhancements and standardization across platforms to ensure enforceability of settlements.

- Governance votes or protocol upgrades that affect how final outcomes are proposed and validated by oracles.

- New platform launches and interoperability efforts that emphasize resolution as a core infrastructure layer.

- Regulatory developments and compliance guidance affecting the legality and structure of prediction-market platforms.

Sources & verification

- Data dashboards and metrics on prediction markets via Dune.

- Joint research context from Keyrock detailing market growth and architecture.

- Historical volumes and coverage related to prediction-market activity, including articles such as Prediction market trading volumes hit new high.

- Industry reference: Crypto.com’s standalone prediction market platform launch, discussed in coverage linked within the source material.

- Seer Resolution Infrastructure documentation outlining architecture and interaction with the prediction market stack.

What the article topic changes

Resolution-centric design is redefining how prediction markets communicate risk, resolve disputes, and settle funds. The shift toward auditable, enforceable outcomes promises more stable liquidity and broader inclusion of market participants, including institutions that require transparent settlement processes. The industry’s evolution suggests that prediction markets will increasingly function as information infrastructure—supporting decision-making and risk management in a way that mirrors traditional financial markets, but tailored to the unique demands of forecasting future events.

Key Takeaways

- Shares of Robinhood declined approximately 2% during after-hours trading following the March 12 release of February performance data.

- February equity trading volumes reached $194.4 billion, representing a 14% sequential decline but a 36% improvement versus the prior year.

- Options contract volume totaled 180.3 million for the month, reflecting a 10% decrease compared to January.

- Cryptocurrency trading emerged as a standout performer — $25 billion in monthly volume, climbing 9% sequentially and surging 74% annually.

- Platform assets under management reached $314 billion at February’s close, slipping 3% from the prior month while jumping 68% year-over-year.

The popular trading platform released its February performance metrics on March 12, triggering a roughly 2% decline in shares during extended trading hours. The data painted a nuanced picture of activity across the company’s various trading segments.

Equity volumes totaled $194.4 billion throughout February. This represented a sequential decline of 14% compared to January’s figures, although the number still exceeded last February’s volume by 36%. On an average daily basis, equity trading volumes measured $10.2 billion, declining 11% month-over-month while maintaining a 36% year-over-year increase.

The Robinhood mobile application experienced more pronounced weakness. App-specific average daily volumes plummeted 35% annually to $336 million, creating a notable contrast with the overall platform’s healthier year-over-year comparison.

Options activity similarly disappointed. February saw 180.3 million options contracts change hands across the platform, representing a 10% monthly decrease. Daily average options volume registered at 9.5 million contracts, falling 5% sequentially despite posting a 9% annual gain.

Event contracts suffered the steepest decline. Monthly volume contracted 29% from January to 2.4 billion contracts, while average daily volume retreated 22% month-over-month to 86 million contracts.

Cryptocurrency Trading Shines

Digital asset trading provided the month’s positive highlight. Robinhood recorded $25 billion in cryptocurrency trading volume during February — advancing 9% sequentially and soaring 74% compared to the year-ago period. Bitcoin’s resilience, despite experiencing a significant mid-month correction, contributed to sustained elevated activity levels.

The mobile app platform generated $9.4 billion of the total crypto volume, representing an 8% monthly increase. However, app-level cryptocurrency average daily volumes remain 35% below their year-ago benchmark.

Cash and customer deposits concluded February at $16.5 billion, surging 67% year-over-year. During the month, the company modified its brokerage High-Yield Cash offering to facilitate margin lending expansion. This strategic adjustment moved more than $6 billion from Cash Sweep balances into free credit balances.

Account Growth Maintains Momentum

The platform’s customer base continued expanding. Robinhood closed February with 27.4 million funded customer accounts, extending its consistent growth trajectory.

Total assets held on the platform measured $314 billion at month-end, declining 3% from January 2026 levels but climbing 68% versus February 2025. The sequential monthly decrease mirrors both reduced trading activity and prevailing market dynamics during the period.

Analyst sentiment toward the stock remains predominantly positive. Current consensus ratings show Strong Buy, derived from 14 Buy recommendations, two Hold ratings, and zero Sell ratings issued during the last three months. The mean analyst price target stands at $125.77.

CryptoBreaking is excited to announce a brand-new giveaway for our community in partnership with The Bitcoin Conference.

We are giving away 3 free General Admission passes to Bitcoin 2026, taking place at The Venetian in Las Vegas from April 27 to April 29, 2026.

This is your chance to be part of the world’s largest and most influential Bitcoin event, completely free.

Bitcoin 2026 will bring together builders, investors, entrepreneurs, developers, and Bitcoin believers from around the world for three days of networking, innovation, and the future of sound money.

According to the organizers, this year’s event will once again continue the momentum of what has already become the biggest Bitcoin gathering in the world, following the success of previous editions that attracted tens of thousands of attendees.

If you want a chance to attend, all you need to do is register through the form embedded on this page.

How to Enter the Giveaway

Entering is simple.

Just fill out the registration form below with your:

-

First name

-

Last name

-

Email address

Once you complete the form, you will be officially entered into the draw for one of the 3 General Admission passes.

Important: registration through this page is the only valid way to enter the giveaway.

What the Winners Will Receive

The three selected winners will each receive one Bitcoin 2026 General Admission pass.

The GA Pass is designed for newcomers and the Bitcoin-curious, and includes:

-

Access on Days 2 and 3 only: April 28 and April 29, 2026

-

Entry to the Main Stage

-

Entry to the Genesis Stage

-

Access to the Expo Hall

Please note that the giveaway covers the General Admission ticket only. Travel, accommodation, and any upgrades are not included.

Upgrade Option and Hotel Benefit

The giveaway tickets are GA passes, which also give winners the option to upgrade separately if they wish.

According to the organizers, GA ticket holders who upgrade may be eligible for a significant hotel discount package, with savings of up to $800.

This makes the GA option especially attractive for attendees who may want flexibility while still keeping costs lower.

Special Discount for CryptoBreaking Readers

Prefer to secure your spot right away instead of waiting for the giveaway results?

CryptoBreaking readers can use the promo code CryptoBreaking10 at checkout to receive an exclusive 10% discount on tickets for Bitcoin 2026.

If you already know you want to attend, this is a great way to lock in your place early and save on your purchase.

For full event details and tickets, visit the official website:

https://2026.b.tc/

Why Attend Bitcoin 2026

Bitcoin 2026 is being presented as more than just a conference. It is a global meeting point for the Bitcoin ecosystem, where ideas, innovation, and opportunity come together.

As described by the organizers:

Bitcoin 2026 is where the global Bitcoin community comes alive, uniting builders, thinkers, and believers to push the boundaries of sound money and financial freedom.

The event will take place at The Venetian, Las Vegas, one of the city’s most iconic venues, and is expected to attract major names, companies, media, and Bitcoin leaders from across the industry.

Giveaway Rules

-

The giveaway is open to anyone

-

Entry is valid only through the form embedded on this page

-

Only one entry per person is allowed

-

Three winners will be selected at random

-

Each winner will receive one Bitcoin 2026 General Admission pass

-

Winners will be contacted by email

-

If a selected winner does not respond in time, another winner may be chosen

-

By entering, participants agree to subscribe to the CryptoBreaking newsletter

-

Travel, hotel, visa, and personal expenses are not included

Privacy and Email Registration

By entering this giveaway, you agree to subscribe to the CryptoBreaking newsletter, which is required in order to participate.

Your information will be used only for giveaway-related communications, winner notification, and future CryptoBreaking updates. Winner details may be shared with the event organizers only for the purpose of ticket registration and delivery.

You can unsubscribe from the newsletter at any time.

Register Now

If you want a chance to attend Bitcoin 2026 in Las Vegas for free, make sure to register as soon as possible.

The earlier you enter, the better, so winners can be selected in time and begin planning their trip.

Complete the form below now and secure your chance to win one of the 3 free GA passes.

TLDR

- Stock futures for the Dow, S&P 500, and Nasdaq posted gains Friday morning following a sharp decline the previous day, supported by a modest retreat in oil prices.

- Brent crude momentarily breached the $100 per barrel mark for the first time since August 2022, subsequently falling back to approximately $99.

- Analysts describe the current oil supply disruption, linked to the Iran conflict entering its second week with the Strait of Hormuz remaining blocked, as historically unprecedented.

- Bitcoin climbed above $70,000, with market observers pointing to a social media message from Trump as a potential catalyst for the cryptocurrency’s advance.

- Market expectations for Federal Reserve policy have shifted dramatically, with traders now pricing in a 47% probability of no rate cuts in 2026, compared to merely 3% four weeks earlier, amid mounting inflation concerns.

Friday morning brought relief to US equity markets as stock futures posted modest gains after Thursday’s bruising session pushed all three primary indices to their 2026 lows. Futures contracts for the Dow Jones Industrial Average, S&P 500, and Nasdaq 100 each advanced between 0.3% and 0.4% during early trading hours.

The upward movement came after an Axios report suggested a potential breakthrough in the Middle East crisis. According to the report, President Donald Trump informed fellow world leaders during a Wednesday virtual summit that Iran was on the verge of capitulation. However, official White House confirmation of these statements has not been forthcoming.

Contradicting any notion of imminent surrender, Iran’s newly appointed supreme leader, Mojtaba Khamenei, doubled down on Thursday with pledges to continue hostilities. He explicitly stated Iran’s intention to maintain the closure of the Strait of Hormuz, a vital waterway for global petroleum shipments.

As the confrontation between Iran and Israel stretches into its second week, military operations continue to intensify. Fresh Israeli strikes targeted Tehran, while evidence suggests Iranian involvement in missile attacks affecting Dubai and Turkey. The United States military also reported the tragic loss of four service members in a refueling aircraft accident.

Oil Pulls Back But Stays Elevated

Oil prices experienced a modest decline Friday following days of turbulent trading. West Texas Intermediate crude futures dropped approximately 2% to trade beneath $94 per barrel. Brent crude, the global pricing benchmark, retreated from the psychologically significant $100 threshold after closing above that level Thursday for the first time in over two years.

Energy market experts characterize the current supply disruption as unparalleled in scope and severity. Washington responded by issuing its second exemption permitting purchases of previously sanctioned Russian petroleum, attempting to alleviate supply constraints.

According to The Wall Street Journal, Indian government representatives are engaged in intensive negotiations with Tehran to secure passage for no fewer than 23 oil tankers currently stranded due to the Strait of Hormuz blockade. Indian officials suggest initial transit approvals could materialize within days.

Fed Rate Cut Bets Fall Sharply

The petroleum-fueled inflation anxiety is fundamentally altering market projections for Federal Reserve monetary policy. CME FedWatch data reveals traders now assign a 47% likelihood to the scenario where the central bank implements zero interest rate reductions throughout 2026. This represents a dramatic shift from the 3% probability assigned to this outcome just one month prior.

Friday morning saw the 10-year Treasury yield holding at 4.28%. Meanwhile, the US dollar index gained 0.3%, reaching its strongest position in three and a half months.

Market participants eagerly awaited Friday’s release of the Personal Consumption Expenditures price index, the Federal Reserve’s favored inflation measurement tool. Additional economic data including fourth quarter GDP figures and the January JOLTS employment openings report were also on the calendar.

Bitcoin broke through the $70,000 barrier in early Friday trading. Market commentators suggested a social media message from former President Trump may have contributed to the cryptocurrency’s upward momentum. Gold was tracking toward a weekly decline, pressured by dollar strength.

Thursday witnessed Brent crude’s most substantial single-session percentage increase since May 2020, highlighting the extraordinary volatility characterizing this week’s energy market trading.

Factbox-How many people have been killed in the US-Israeli war on Iran?

Bank of England Comes Around on Stablecoins

“Outlander” recap: A surprise death shocks the Ridge

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Bitcoin Just Flashed a Signal Nobody Is Ready For – Arthur Hayes

Nick Cannon and Mariah Carey: Love tested by financial pressures #nickcannon #mariahcarey

URGENT ANOTHER 2008 BANKING COLLAPSE HAPPENING NOW?! #crypto #cryptocurrency #xrp #bitcoin #finance

-

Business7 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

News Videos4 days ago

News Videos4 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Ann Taylor

-

Tech2 days ago

Tech2 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Crypto World4 days ago

Crypto World4 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech3 days ago

Tech3 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Business3 days ago

Business3 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Sports6 days ago

Sports6 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports5 days ago

Sports5 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

NewsBeat2 days ago

NewsBeat2 days agoResidents reaction as Shildon murder probe enters second day

-

Entertainment6 days ago

Entertainment6 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

Business5 days ago

Business5 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business2 days ago

Business2 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat4 days ago

NewsBeat4 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech4 days ago

Tech4 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

NewsBeat2 days ago

NewsBeat2 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Business4 days ago

Business4 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

Business6 days ago

Business6 days agoIran war enters second week as Trump demands ’unconditional surrender’

-

Sports4 days ago

Sports4 days agoSkateboarding World Championships: Britain’s Sky Brown wins park gold

-

Crypto World3 days ago

Crypto World3 days agoWill Chainlink price reclaim $10 amid volatility squeeze?