Crypto World

Stablecoin Salary Payout Platform Development: UK & EU Guide

Stablecoin-based payroll infrastructure is entering a regulated growth phase across the United Kingdom and the European Union. The UK and EU represent one of the largest fintech and cross-border employment markets globally. As regulatory clarity around digital assets improves under the Financial Conduct Authority (FCA) and the Markets in Crypto-Assets (MiCA) regulation, enterprises are accelerating efforts to modernize payroll infrastructure using stablecoins.

For fintech startups, payroll SaaS providers, cross-border payment companies, and embedded finance platforms, this presents a strategic opportunity. Launching a compliant and scalable stablecoin payment platform built specifically for regulated workforce payouts is a major competitive advantage. This guide explains the requirements to design, build, and deploy a stablecoin salary payout infrastructure that meets UK and EU regulatory expectations while remaining commercially viable and technically scalable.

Why Stablecoin Salary Payouts Are Growing in the UK and EU

A stablecoin salary payout platform allows employers to distribute wages using regulated digital currencies such as USD Coin (USDC) or Tether (USDT). These digital assets maintain price stability relative to fiat currencies while enabling programmable and near real-time settlement.

Unlike simple crypto transfers, enterprise payroll systems must include:

- Employer onboarding and identity verification

- Employee wallet provisioning

- Automated recurring payment execution

- Fiat conversion capabilities in GBP and EUR

- Audit logs and compliance reporting

- Risk monitoring and transaction analytics

From the Trenches Insight: Industry experience shows that reconciling fast stablecoin settlement with strict GDPR data privacy standards is often the primary hurdle for modern payout gateways. When structured properly, the system functions as a fully compliant payment gateway seamlessly integrated with traditional HR software and financial institutions.

Core Architecture of a Stablecoin Salary Payout Platform

Building a stablecoin payroll system requires a multi-layered infrastructure designed for resilience and scale.

- Blockchain Settlement Layer: Select a blockchain network that balances scalability, cost efficiency, and ecosystem maturity. Smart contracts must support scheduled payments, multi-recipient distribution, and programmable treasury logic.

- Wallet and Custody Layer: Institutional clients often prefer custodial or hybrid custody models with hardware-backed key management and multi-signature controls.

- Fiat On and Off Ramp Layer: Integration with regulated banks or Electronic Money Institutions (EMIs) ensures smooth conversion between stablecoins and GBP or EUR.

- Compliance and Risk Engine: Embed identity verification APIs, AML monitoring tools, transaction analytics, and automated reporting modules.

- Integration Layer: API-first architecture ensures seamless connectivity with HRMS, ERP systems, and payroll software providers.

Talk to a specialist at Antier today to scope the technical requirements.

Once deployed, the infrastructure can evolve into a comprehensive stablecoin remittance platform supporting vendor payouts, contractor settlements, and treasury transfers beyond salary use cases.

Regulatory Considerations in the UK and EU

Compliance is the foundation of any stablecoin payroll solution in these regions. Regulatory readiness is often the deciding factor for enterprise adoption. Failure to design compliance into the architecture from day one can delay licensing approvals and restrict institutional partnerships.

UK vs. EU Regulatory Landscape for Stablecoins:

| Feature | UK (FCA) | EU (MiCA) |

|---|---|---|

| Regulatory Body | Financial Conduct Authority (FCA) | European Securities and Markets Authority (ESMA) |

| Primary Framework | E-Money Regulations & Cryptoasset Registration | Markets in Crypto-Assets (MiCA) |

| Stablecoin Rules | Strict focus on fiat-backed stablecoins | Authorization required for E-Money Tokens (EMTs) and Asset-Referenced Tokens (ARTs) |

| AML & KYC | Money Laundering Regulations (MLRs) | AMLD6 and strict Travel Rule compliance |

Businesses must align with anti-money laundering standards, Know Your Customer (KYC) requirements, Travel Rule data-sharing obligations, and GDPR data privacy regulations. A compliant gateway should include automated onboarding workflows, sanctions screening, risk classification systems, and real-time monitoring dashboards.

Essential Features for Enterprise Adoption

Enterprise clients expect more than just basic blockchain settlement. To compete effectively, a solution should include:

- Multi-stablecoin compatibility: Support for major fiat-pegged assets like USDC, EURC, and USDT.

- Automated payroll scheduling: Smart contract triggers for bi-weekly or monthly disbursements.

- Bulk payout execution: Batch processing to minimize gas fees and streamline employer operations.

- Treasury management dashboard: Real-time visibility into asset reserves and liquidity.

- FX visibility tools: Transparent conversion rates between crypto and fiat.

- Compliance export modules: One-click report generation for internal audits and tax authorities.

- Role-based administrative controls: Multi-tier access for HR, finance, and executive teams.

- Scalable API endpoints: Easy integration for white-label partners.

Providing full-stack stablecoin remittance platform development enables fintech startups and payroll companies to deploy branded solutions without building the infrastructure internally.

Access the 2026 MiCA & FCA Enterprise Checklist

Monetization Model for Stablecoin Payroll Platforms

A profitable stablecoin payroll solution in the UK and EU should combine recurring revenue with transaction-based income and enterprise services.

- Transaction Fees: Charge per salary payout, bulk disbursement, or contractor transfer. A well-structured system automates fee calculation and provides transparent reporting.

- Subscription Plans: Offer tiered SaaS pricing based on active employees, transaction volume, API access, and compliance features.

- White Label Licensing: Allow payroll SaaS providers and fintech firms to deploy under their own brand. Licensing and setup fees create long-term recurring contracts.

- FX and Conversion Margins: Earn revenue from GBP and EUR conversions. Efficient settlement through secure payment rails ensures competitive spreads.

- API and Compliance Modules: Premium features such as advanced AML tools and reporting dashboards can expand the platform into a scalable cross-border remittance tool, even revenue and recurring platform income in a rapidly growing digital payroll market.

Frequently Asked Questions

- Is paying salaries in stablecoins legal in the UK and EU?

Yes, paying salaries in stablecoins is legal in both regions, provided the employer and the payment platform comply with local tax laws, employment contracts, and financial regulations (such as FCA guidelines in the UK and MiCA in the EU). Both parties must mutually agree to the payment method in writing.

- What are the tax implications of a stablecoin salary?

In the UK and EU, stablecoin salaries are subject to standard income tax and social security contributions. The fiat value of the stablecoin at the exact time of the payout is used to calculate the tax liability. Employees may also be subject to capital gains tax if the stablecoin fluctuates in value before it is sold or converted to fiat.

- How do stablecoin payroll platforms handle fiat off-ramping?

Enterprise payroll platforms partner with regulated Electronic Money Institutions (EMIs) or crypto-friendly banks. This integration allows employees to receive stablecoins into a designated wallet and immediately convert them into GBP or EUR, which is then routed directly to a traditional bank account via SEPA or Faster Payments.

Moving Forward

If evaluating blockchain salary infrastructure as a fintech founder, payroll technology provider, or enterprise, this is a strategic inflection point. The UK and EU are moving toward regulated digital asset integration. Companies that establish compliant and scalable payroll infrastructure today will lead tomorrow’s cross-border workforce economy.

Antier helps businesses design and deploy enterprise-ready solutions tailored for these markets. Whether launching a stablecoin payment platform, integrating a compliant payment system, or optimizing settlement through secure stablecoin payment rails, the development delivered is strictly aligned with regulatory and enterprise standards. Ready to build a regulation-ready stablecoin payroll platform? Connect with Antier’s experts today and start the deployment journey.

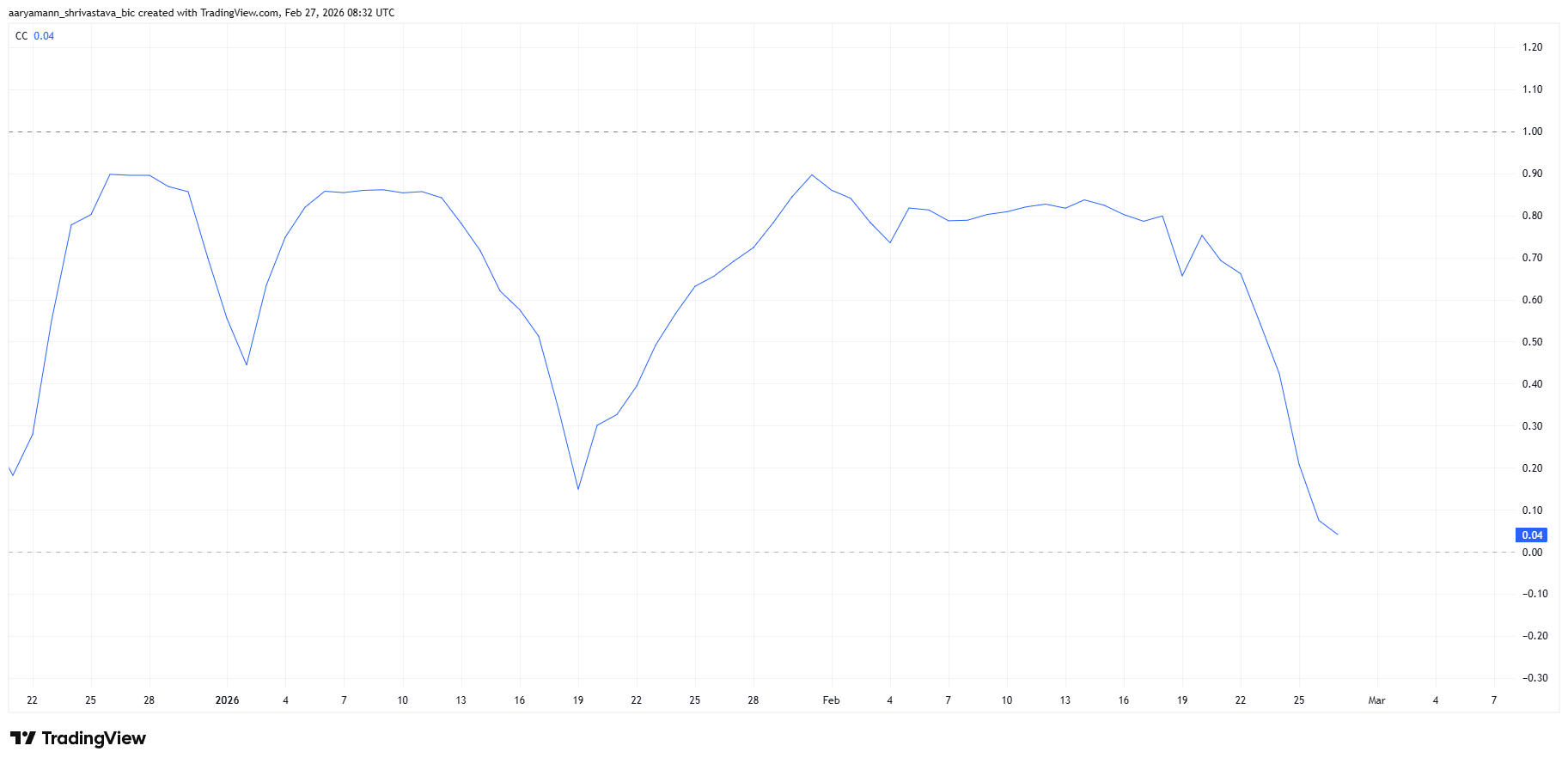

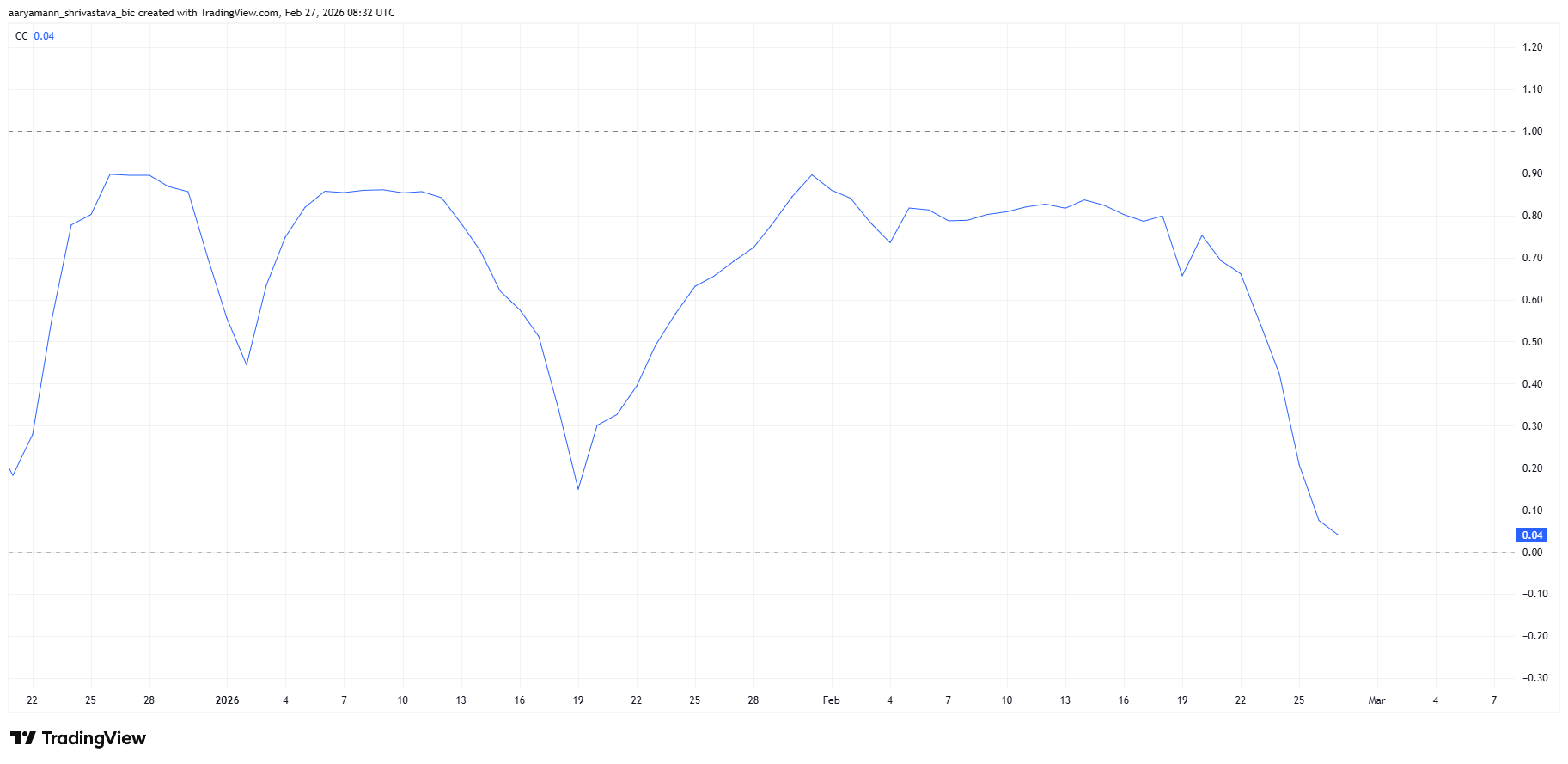

Terra Luna Classic (LUNC) price lacked clear direction for weeks before staging a sharp three-day rally. The sudden surge pushed the token up nearly 30% at its intraday peak. However, technical and on-chain signals suggest the breakout may struggle to sustain momentum.

The broader crypto market has experienced periodic bursts of volatility. LUNC’s recent move stands out due to its speed rather than structural strength. While price action turned briefly bullish, underlying metrics indicate caution is warranted.

Bitcoin – The Cause Of LUNC’s Rise

The primary catalyst behind LUNC’s rally was a surge in trading volume. Increased speculative activity drove short-term price acceleration. At the same time, LUNC’s correlation with Bitcoin dropped to 0.04, signaling near-complete decoupling.

Such low correlation suggests the token temporarily moved independently of BTC. Decoupling phases can attract traders seeking isolated momentum plays. However, similar patterns have appeared across several altcoins recently. These shifts often reflect short-lived speculative rotations rather than lasting structural change.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

LUNC Is Trapped Under Bearish Pressure

The Chaikin Money Flow indicator reveals a concerning divergence. Despite rising prices over the past three days, CMF did not confirm sustained inflows. Capital entering the market remained subdued relative to price movement.

A bearish divergence formed as price climbed while CMF weakened. This pattern indicates that buying pressure failed to match the rally’s strength. Outflows continued quietly beneath the surface.

Weak inflow confirmation raises questions about durability. Without consistent capital accumulation, rallies risk reversal. Price movements unsupported by strong liquidity often correct once speculative interest fades.

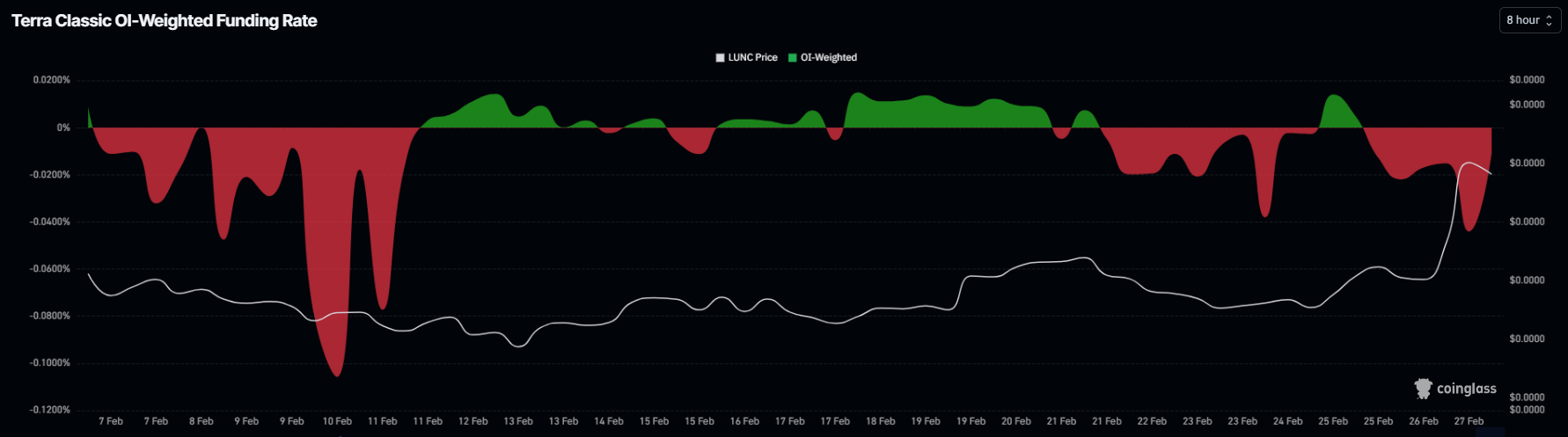

Derivatives data adds to the cautious outlook. LUNC’s funding rate currently sits in negative territory. Negative funding signals dominance of short positions over longs.

Aggregate funding metrics show traders are positioning for downside risk. Elevated short interest can cap upward momentum. If short bias persists, LUNC may continue consolidating unless forced liquidations trigger a squeeze.

LUNC Price May Not See Much Growth

LUNC rose roughly 20% over the past three days and surged 30% at its recent intraday high before retreating to $0.00004136. The long upper wick on the chart signals rapid profit-taking. Quick distribution at higher levels limited further upside continuation.

Current technical conditions present a bearish bias. If selling pressure resumes, LUNC could decline toward $0.00003459. This level aligns with the 23.6% Fibonacci retracement. A breakdown below $0.00003459 may expose the next support near $0.00003236, invalidating the bullish recovery narrative.

On the upside, LUNC remains capped beneath the $0.00004203 resistance, marked by the 61.8% Fibonacci level. A decisive breakout above this barrier would shift short-term momentum. Flipping $0.00004203 into support could push the token toward $0.00004530 and potentially higher, invalidating the immediate bearish thesis.

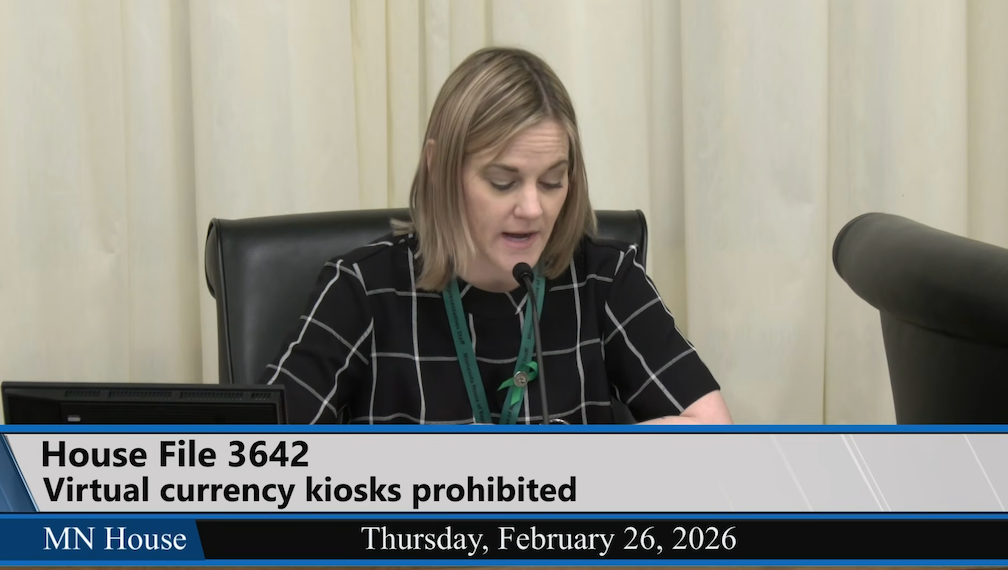

A Minnesota lawmaker has introduced a bill that could ban virtual currency kiosks statewide after reports of scams tied to crypto ATMs. Bitcoin ATMs (CRYPTO: BTC) have emerged as a focal point in law-enforcement briefings, where operators have been accused of enabling irreversible transactions that are hard to trace. Rep. Erin Koegel unveiled House File 3642 during a Thursday session of the Commerce Finance and Policy Committee, arguing the technology behind crypto kiosks remains novel and minimally regulated. Minnesota voters have already seen a 2024 law intended to curb kiosk abuse by capping new-user deposits at $2,000 and requiring refunds to fraud victims, but Koegel’s measure would push toward a full ban if enacted. Supporters say it would shield residents from irreversible financial crimes, while opponents caution it could restrict access to legitimate crypto services and push activity underground. Koegel cited committee remarks and testimony during the session.

Key takeaways

- House File 3642 would ban crypto kiosks across Minnesota if enacted, expanding beyond the state’s 2024 safeguards.

- The 2024 law introduced a $2,000 deposit limit for new kiosk users and required refunds for fraud, signaling a trend toward consumer protections.

- Law enforcement officials described cryptocurrency kiosks as a common scam vector, with aging populations identified as particularly vulnerable groups.

- There are about 350 licensed crypto kiosks in Minnesota, operated by firms including Bitcoin Depot and Coinflip, according to the state’s findings.

- Industry responses emphasize a broader regulatory debate about crypto ATMs, privacy, and access versus fraud risk, with related moves like ID-verification policies signaling a shifting risk profile.

Tickers mentioned: $BTC

Sentiment: Neutral

Market context: The Minnesota proposal sits within a broader regulatory moment as lawmakers and regulators reassess crypto kiosks amid ongoing fraud concerns. Across the U.S., states are weighing standardized protections for crypto ATM users, while operators consider compliance measures to balance customer access with risk controls. The trend toward enhanced identity checks and clearer fraud warnings reflects a shift in how the market perceives the balance between innovation and consumer protection.

Why it matters

The bill’s momentum highlights a policy question at the intersection of financial technology and consumer protection. Crypto kiosks offer convenient access points for the public to buy and sell digital assets, but their relative lack of traditional safeguards has made them attractive targets for scammers. Minnesota’s current framework—enacted in 2024—was designed to curb abuse by imposing a deposit cap and mandating refunds for fraud victims. Yet the proposed HF 3642 would push the state toward a more restrictive approach, potentially banning the devices altogether. The stakes are not merely about kiosks; they reflect a broader debate about how to regulate rapidly evolving crypto infrastructure without stifling legitimate use cases or hindering access to digital assets for ordinary residents.

Industry responses point to a practical tension: operators argue that well-defined rules can reduce abuse while preserving access. Bitcoin Depot, one of the largest operators in the U.S., has already begun a phased rollout of ID verification for all transactions at its machines, a policy aimed at curbing misuse while maintaining user convenience. The move signals a willingness among some players to embrace stronger controls in the name of compliance and consumer protection; it also foreshadows a regulatory environment in which basic access could be contingent on identity verification and heightened disclosures. The pressurized policy backdrop is further amplified by consumer advocacy groups that emphasize protections, such as fraud warnings and transaction-limits, as essential to preserving trust in mainstream crypto usage.

For the market, these developments touch on liquidity, risk sentiment, and the perceived legitimacy of on-ramp infrastructure. When a state with tens (and potentially hundreds) of kiosks contemplates a ban, it underscores the fragility and scrutiny surrounding crypto-on-ramp channels. While the debates unfold, observers watch for how other states respond to similar concerns and whether broader federal or regulatory moves could harmonize or clash with state-level approaches. The tension between enabling convenient access to digital assets and preventing harms linked to fraudulent activity remains a defining feature of the current regulatory landscape.

In parallel, consumer protection narratives continue to gain traction. The American Association of Retired Persons (AARP) has highlighted ongoing fraud protections in several states, urging operators to implement practical safeguards such as transaction limits and clear fraud warnings. As lawmakers weigh HF 3642 against the potential benefits of accessible crypto tools for everyday users, the interplay between policy, technology, and consumer trust will likely shape the contours of Minnesota’s crypto kiosk ecosystem in the months ahead. The discussion also echoes broader policy conversations about how to regulate novel financial technologies while preserving opportunities for legitimate innovation.

“Because of the nature of cryptocurrency, these fraudulent transactions are often irreversible and incredibly hard to track,” Koegel said, emphasizing the need for a coordinated, cross-partisan response to protect citizens from irreversible financial crimes.

The current environment therefore blends caution with pragmatism: protect vulnerable users and deter fraud, while acknowledging that kiosks can provide a straightforward entry point to digital assets for some residents. The outcome of HF 3642 remains uncertain, but the policy debate is unlikely to fade anytime soon as Minnesota and other states evaluate how to balance accessibility and security in an evolving crypto economy.

What to watch next

- Progress of House File 3642 in the Minnesota House of Representatives, including committee votes and potential floor action.

- Any Senate companion or changes in the legislative process that could influence the bill’s trajectory.

- Updates to kiosk regulations and enforcement actions stemming from the 2024 deposit-limit law, and any new operator compliance measures.

- Industry responses from crypto ATM operators regarding verification policies and fraud-prevention efforts, and how these may influence state debates.

Sources & verification

- House File 3642 and committee materials from the Minnesota House of Representatives (HF 3642 – Commerce Finance and Policy Committee materials).

- Committee hearing coverage and remarks, including Rep. Koegel’s statements and the discussion on the 2024 law, captured in the committee video (YouTube: https://www.youtube.com/watch?v=w6hc8OkvaZE).

- State data on licensed crypto kiosks in Minnesota (approximately 350 kiosks operated by Bitcoin Depot, Coinflip, and others).

- Bitcoin Depot policy update requiring ID verification for all crypto ATM transactions (Cointelegraph: https://cointelegraph.com/news/bitcoin-depot-mandatory-id-verification-crypto-atms).

- AARP’s guidance on crypto ATM fraud protections and related protections in multiple states (https://www.aarp.org/advocacy/crypto-atm-fraud-protections/).

A Minnesota lawmaker has introduced a bill that could ban virtual currency kiosks across the state after reports of incidents involving crypto-related scams.

In a Thursday session of the Minnesota House of Representatives Commerce Finance and Policy Committee, Representative Erin Koegel said the bill, House File 3642, would address the “novel” and “minimally regulated” technology of crypto kiosks.

Koegel said she had heard from state law enforcement agencies that many scammers used the kiosks to trick residents into sending crypto, while legitimate traders tended to use centralized exchanges.

“Because of the nature of cryptocurrency, these fraudulent transactions are often irreversible and incredibly hard to track,” said Koegel, adding:

“This bill gives us an opportunity to work across party lines to protect the people of Minnesota from irreversible financial crimes.”

Minnesota’s government already passed a law in 2024 attempting to fight scammers using the state’s virtual currency kiosks. The law set a $2,000 deposit limit for new kiosk users and required companies to issue full refunds for fraud victims. However, Koegel’s bill, if passed, could fully ban the technology in Minnesota.

“Within the past couple of years, we’ve definitely identified an issue with these Bitcoin ATMs, specifically in our jurisdiction,” said Sergeant Jake Lanz of the St. Cloud Police Department at the Thursday committee meeting. “[…] it also is notable for us that it is definitely a target of our aging population.”

Related: US senators to weigh CFTC, other amendments to crypto market structure bill

According to the House, Minnesota has about 350 licensed crypto kiosks operated by several companies, including Bitcoin Depot and Coinflip. The American Association of Retired Persons reported in February that 17 states had laws on the books requiring crypto ATM operators to implement protections against fraudsters, such as setting daily transaction limits and requiring fraud warning signs.

Bitcoin ATM operator to require IDs for all transactions

On Tuesday, Bitcoin Depot, one of the largest crypto ATM operators in the US, announced that it would implement a policy requiring ID verification for users with every transaction at one of its machines. The phased rollout, which began in February, was in response to “potential misuse,” though the company did not specifically mention state-level crackdowns on scammers.

Magazine: Would Bitcoin really be at $200K if not for Jane Street? Trade Secrets

Multinational bank Barclays (BARC) is exploring the creation of a blockchain platform for payments and other processes, Bloomberg reported on Friday.

The London-based financial services giant is consulting with prospective technology providers on the development of such a platform that would see it rival JPMorgan (JPM) and others in using decentralized technology for banking services.

Barclays’ blockchain-based plans could include stablecoins and tokenization, according to the report, citing people familiar with the matter.

JPMorgan first allowed tokenized deposits — deposits represented as digital tokens on a decentralized ledger — through its dollar-denominated JPM Coin all the way back in 2019.

More recently, HSBC has also enabled tokenized deposits to expand its own push into blockchain-based payments.

Such institutions are exploring how blockchain technology can make existing financial processes more transparent and more efficient by carrying them out on decentralized networks that lack some of the input of intermediaries and allow faster settlement.

Barclays did not respond to CoinDesk’s request for comment.

Read More: JPMorgan expands blockchain goals, plans to build ‘interoperable digital money’

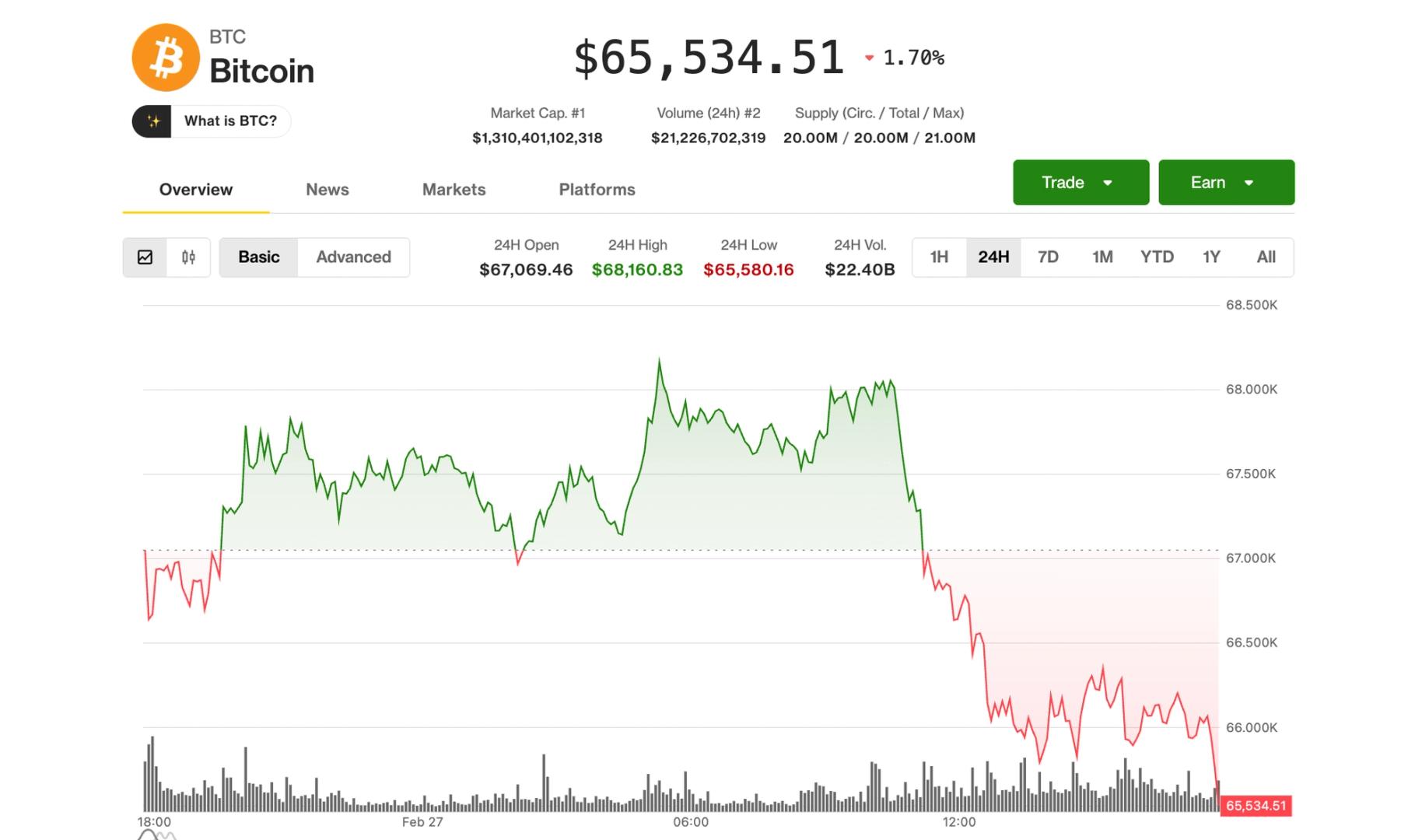

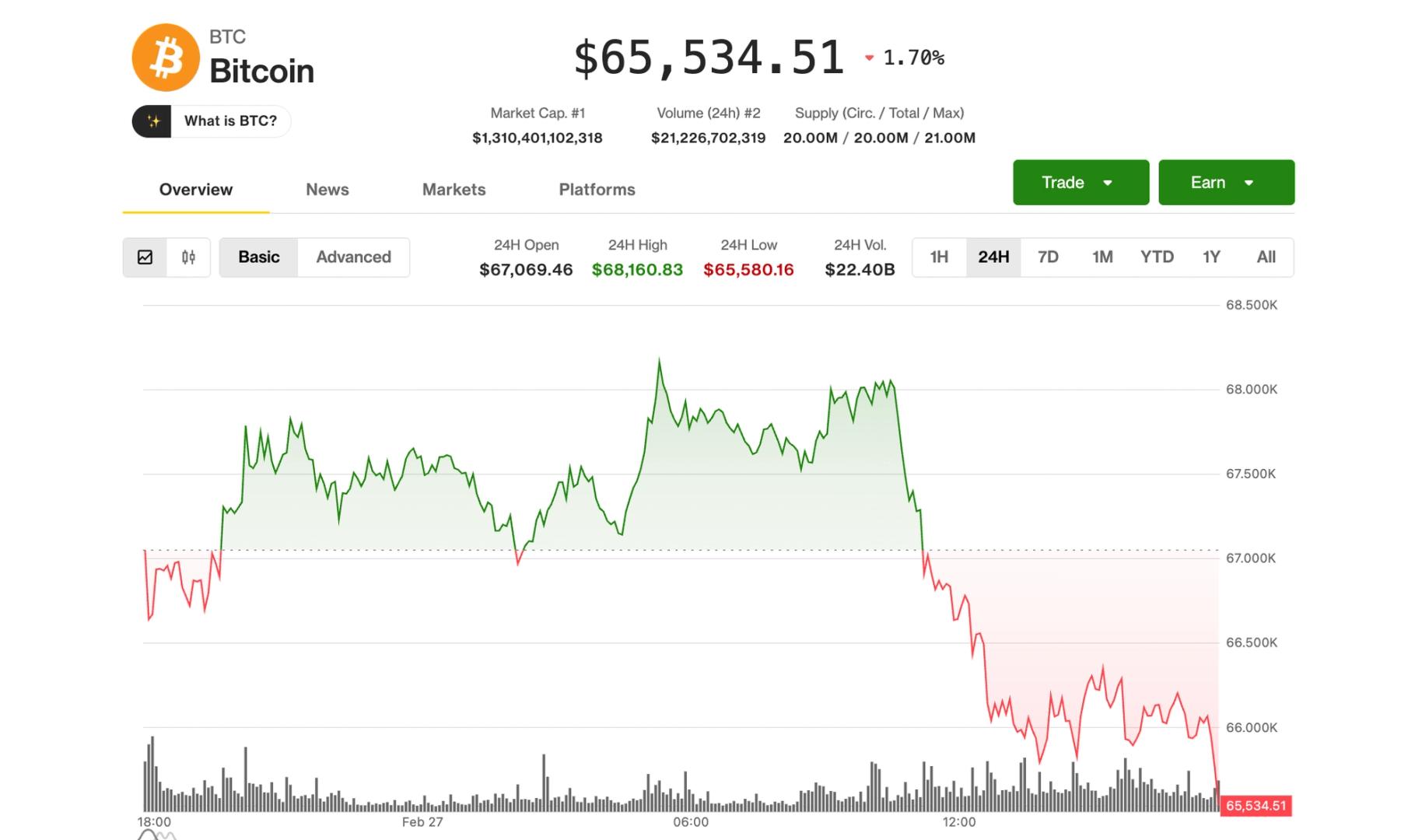

Bitcoin fell back below $66,000 Friday in the early U.S. session as mounting macro risks are spooking investors away from risky assets.

The largest crypto now has erased most of Wednesday’s surge, plunging 3% from around $68,000 in the past few hours to $65,600 in the morning hours. The braod-market CoinDesk 20 Index was 2.3% lower in the past 24 hours, with ether (ETH), XRP (XRP) and solana (SOL) down similar amounts.

Crypto-related stocks also followed the move, giving up part of the gains earlier this week. Strategy (MSTR), the largest corporate bitcoin holder, slipped 3%, while Coinbase (COIN) was more than 2% lower. Stablecoin issuer Circle (CRCL), declined almost 5%%, snapping its rebound that saw the stock gaining nearly 50% in a couple of sessions.

Miners, increasingly linked to AI infrastructure buildout, performed even worse, with IREN (IREN), Cipher Mining (CIFR), Core Scientific (CORZ) and TeraWulf (WULF) losing 6%-8%.

The action occurred as U.S. equity indexes fell, with the Nasdaq down 0.8% and the S&P 500 lower by 0.6%.

In the backdrop, there was a mix of risks for investors to get concerned about.

A hotter-than-expected Producer Price Index (PPI) inflation reading for last month spooked those who hoped for a continuation in the cooling inflation trend. In January, core PPI rose 3.6% year over year, above the 3.0% estimate, and up from 3.3% previously. Markets are now pricing in a 96% chance of no rate cut for the March 18 Federal Reserve meeting.

Concerns about stress in the credit markets also linger, with credit spreads at their widest in four months. Private equity firms KKR (KKR), Ares (ARES) and Apollo Global Management (APO) plunged 6%-7% to fresh lows during the session.

On top of that, prediction market odds of U.S. strikes against Iran rose this morning after the U.S. has begun evacuating embassy staff from Israel.

Money flows to safe-havens

In fixed income, the U.S. 10-year Treasury yield has slipped below 4% for the first time since November 2024. Precious metals continue to rally, with gold up 1% to above $5,230 an ounce, while silver has surged 4% to trade back above $92. Meanwhile, crude oil jumped 2.3% to above $67 a barrel.

Read more: The worst may lie ahead. Bitcoin chart revisits historic pattern

OpenAI on Thursday confirmed a $110 billion valuation, fueling expectations that it could stage the largest IPO in US tech history if it moves forward with a public listing.

The company has not yet filed for an IPO. However, the valuation announced on February 27 positions OpenAI above several landmark Silicon Valley debuts and signals strong backing from major technology investors.

Who are the Big Tech Going All-In on OpenAI?

OpenAI has raised billions in private funding over the past few years. Its most significant backer remains Microsoft, which committed multi-year investments reportedly totaling around $13 billion through structured equity and cloud partnerships.

The new funding includes $30 billion from SoftBank, $30 billion from NVIDIA, and $50 billion from Amazon. Additional financial investors are expected to join as the round progresses.

Other major investors include Thrive Capital, Khosla Ventures, Sequoia Capital, and Andreessen Horowitz. These firms participated in earlier funding rounds as OpenAI scaled ChatGPT and enterprise AI infrastructure.

OpenAI Could be the Biggest IPO in US History

If OpenAI proceeds at this valuation, it would rank among the largest US tech IPOs ever. The scale of this funding dwarfs most historic IPO valuations.

For comparison, Meta Platforms (Facebook) went public in 2012 at about $104 billion. Snowflake debuted in 2020 at roughly $70 billion. Alibaba Group was listed at around $168 billion in 2014.

Globally, Saudi Aramco still holds the overall IPO record at $1.7 trillion.

At a $730 billion valuation, OpenAI now stands in a different category.

If it proceeds to a public offering, it would likely rank as the largest US tech IPO ever, reflecting the scale of investor conviction behind frontier AI.

The company has not disclosed a potential listing date or share price range. Those details would emerge in a formal IPO filing.

- Kaspa price currently mirrors the broader market, with Bitcoin struggling.

- The KAS token recently bounced off $0.028 and is holding $0.03.

- If a decisive breakout materializes amid likely catalysts, bulls could target $0.10 in the coming months.

Kaspa (KAS) price has declined by 22% over the past month and by over 64% since its peak above $0.13 in May 2025.

The token trades near $0.03, but remains in an extended downtrend amid prevailing weakness across the crypto market. Friday’s session saw Bitcoin retest lows of $65,600, and Ethereum dip to near $1,900, a move that pinned most altcoins lower, including Kaspa.

Why Kaspa bulls may hold the upper hand

Despite the potential for a retest of recent lows, bullish catalysts are on the horizon. Combined with current strength, these possible upside triggers suggest the advantage in the coming months lies with the buyers. What KAS needs is for bulls to navigate the broader crypto market headwinds while holding $0.03 as support.

Among key milestones is Kaspa’s network notching over 600 million total transactions.

Details on the Kaspa Explorer show that total transactions have surpassed 604 million. According to market observers, this proves that the BlockDAG protocol delivers real-world throughput with sub-second confirmations.

Also notable is Kaspa’s pivotal hard fork expected in May. Implementation will introduce programmable covenants, native assets like KRC20 tokens, and SilverScript for easier Layer 1 development.

Meanwhile, nearly 95% of its 28.7 billion max supply is already mined, and a move to the limit can only slash new coin emissions further. If broader catalysts align, the KAS price will benefit.

Kaspa price analysis

While bulls have the upper hand in terms of what’s upcoming, current price action hints at a potential battle for dominance by both buyers and sellers.

KAS has remained in a downtrend since late 2025, with lows of $0.028 in February. The daily chart highlights a key supply zone at the falling 50-day and 100-day simple moving averages, with bulls hitting a supply wall around these levels multiple times.

If the price fails to break out decisively, a combination of negative market conditions could deepen the downtrend. Support could be at $0.025

On the upside, immediate hurdles are at the 50-day and 100-day SMAs near $0.036 and $0.041.

The key level for bulls will be $0.050-$0.055, a zone that marks a previous supply wall and above which KAS could run to $0.10 or higher.

It’s notable that the Kaspa price jumped to near $0.05 in mid-December 2025 amid excitement around KAS listing on HTX.

Ethereum price trades near $1,950 as the Binance buy/sell ratio hints at a potential shift in derivatives positioning.

Summary

- Ethereum price sits near the lower end of its weekly range after a sharp monthly decline.

- Binance Taker Buy/Sell Ratio has climbed toward neutral after weeks of sell-side pressure.

- A move above $2,200 is needed to challenge the current downtrend structure.

Ethereum (ETH) trades at $1,947 at press time, down 4% in the past 24 hours. Price is sitting near the bottom of its seven-day range of $1,815.54 to $2,099.16. Over the last month, ETH has fallen 35%, and it is still roughly 60% below its August all-time high of $4,946.

Daily trading volume came in at $22.5 billion, down 25% from the previous session. Participation has thinned as the market drifts sideways near recent lows, with traders appearing cautious rather than aggressive.

Binance taker buy/sell ratio shows early improvement

A Feb. 27 report from CryptoQuant contributor Darkfost focused on Ethereum’s Taker Buy/Sell Ratio on Binance. This metric tracks whether aggressive futures orders are dominated by buyers or sellers.

When the ratio pushes above 1, market buys outweigh market sells. When it stays below 1, sellers are pressing harder.

During Ethereum’s push toward prior highs, the ratio stayed under that equilibrium level. The monthly reading slipped to 0.95, while the weekly average dropped further to 0.92. At the same time, price began to roll over. Persistent futures selling added weight to the move lower.

With derivatives volume hovering around $65 billion, futures flows carry significant influence over price discovery. Heavy sell-side pressure in that market often feeds into spot weakness.

Over the past two weeks, the picture has started to shift. The weekly ratio has hovered near 1.0, and there have been several daily spikes above 1.12, reflecting bursts of aggressive buying. The monthly figure has edged up to around 0.99.

ETH has not staged a decisive rebound yet, but the imbalance seen earlier is less extreme. If the ratio can hold above 1 for a sustained stretch, it would show that buyers are taking control of short-term futures positioning. That kind of shift can lay the groundwork for price stabilization.

Ethereum price technical analysis

On the chart, the trend still favors the downside. Ethereum has printed a series of lower highs and lower lows since breaking down from the $3,000–$3,200 area.

Price is now compressing between roughly $1,950 and $2,000. A higher high has not formed, and until ETH climbs through the $2,200–$2,300 region, the larger structure tilts bearish.

Bollinger Bands widened sharply during the drop as price pierced the lower band near $1,850. That expansion reflected a spike in volatility.

The bands have begun to narrow, pointing to a cooling phase. ETH trades below the middle band, currently around $1,980–$2,000, which is acting as near-term resistance.

The relative strength index fell into the 25–30 zone during the selloff, deep in oversold territory. It has recovered to around 40. Momentum has improved slightly, yet buyers have not regained full control. A push above 50 would strengthen the case for a more durable bounce.

Support lies between $1,850 and $1,880. If that floor gives way, the next area to watch sits near $1,700–$1,750. On the upside, $2,000 is the first barrier, followed by stronger resistance between $2,120 and $2,200.

Ethereum co-founder Vitalik Buterin has published a new blog post on X outlining his latest vision for scaling the blockchain, arguing the network can boost capacity in the near term while laying the groundwork for a longer-term shift to advanced cryptography and data-heavy “blobs” that would change how Ethereum is validated.

The post reflects Buterin’s renewed focus on scaling Ethereum’s base layer, after several years in which much of the ecosystem’s scaling strategy centered on layer-2 rollups. The plan comes on the heels of the Ethereum Foundation publishing a ‘strawmap’ aimed at making the network more efficient in the long term.

In the short term, Buterin says Ethereum can safely increase throughput by making blocks easier and faster to check. Upcoming upgrades will allow the computers that run Ethereum to review different parts of a block simultaneously, rather than processing everything step by step. At the same time, changes to how blocks are built will let the network use more of each 12-second processing window, rather than finishing early out of caution (known as ePBS, and will be implemented in the upcoming Glamsterdam upgrade).

The result: Ethereum should be able to fit more transactions into each block without increasing the risk of errors or instability.

Another major piece of the plan involves rethinking how transaction fees — known as “gas” — are calculated. Buterin argues that not all activity on Ethereum puts the same strain on the network. There’s a big difference between using computing power temporarily and permanently adding new data that every Ethereum computer, or node, must store forever.

Right now, those costs are largely bundled together. But creating new permanent data — such as deploying a new contract — increases the blockchain’s long-term size, making it more expensive to run a node over time. That, in turn, risks pushing out smaller operators. Buterin’s proposal would make long-term storage more expensive while allowing more room for everyday transaction processing. In effect, Ethereum could handle more activity without dramatically increasing how fast the blockchain grows.

The goal, he argues, is to avoid a future in which Ethereum processes more transactions but becomes so data-intensive that only large, well-funded players can afford to participate.

Longer term, Buterin sees Ethereum leaning more heavily on zero-knowledge proofs (a private verification method) and expanded data capacity through so-called blobs. Originally introduced to help layer-2 networks post transaction data more cheaply, blobs could eventually carry Ethereum’s own transaction data — a shift that would allow validators to confirm activity without re-running every transaction themselves.

Read more: Ethereum’s ‘Glamsterdam’ upgrade aims to fix MEV fairness

Key Takeaways

- Shares of Sunrun plummeted 28% to $14.74 following the release of conservative 2026 guidance

- Fourth quarter earnings delivered 38 cents per share, significantly surpassing analyst expectations of 3 cents; revenue jumped 124% to reach $1.16 billion

- Company forecasts 2026 cash generation between $250M and $450M, representing a potential decrease from 2025’s $377M

- Investment firm Jefferies cut its rating on RUN to Hold from Buy while maintaining a $22 price target

- Management’s silence on potential dividends or share repurchases left investors disappointed

The solar company delivered impressive fourth quarter results, posting earnings of 38 cents per share—substantially exceeding the analyst consensus of just 3 cents. Revenue reached $1.16 billion, representing a remarkable 124% increase compared to the previous year. Much of this revenue surge stemmed from a strategic decision to sell newly created lease agreements to external parties—marking a fresh approach for the organization.

However, it was the forward-looking guidance that spooked market participants.

Management provided 2026 cash generation estimates ranging from $250 million to $450 million. The midpoint of this forecast—$350 million—falls short of the $377 million achieved in 2025. This apparent regression caught Wall Street’s attention immediately.

Shares declined 28% to close at $14.74 on Friday. The drop is particularly painful considering the stock had rallied 182% over the preceding twelve months and gained 11% year-to-date before the earnings announcement.

Investment bank Jefferies revised its stance, downgrading the stock from Buy to Hold while keeping its $22 price objective intact. Research analyst Julien Dumoulin-Smith characterized the company’s approach as adopting a “defensive posture” heading into fiscal 2026.

Analyst Highlights Conservative Stance

Dumoulin-Smith observed a notable contrast: while competing residential solar firms have expressed increasing optimism about market recovery, Sunrun’s management painted a more sobering picture during its earnings conference call—emphasizing extended market weakness and heightened focus on balance sheet discipline.

The company also revealed plans to reduce its affiliate partner network by approximately 40%. Jefferies interprets this restructuring as an indicator that total installations and new customer acquisitions will decelerate.

Market participants had anticipated announcements regarding dividends or stock buyback programs, particularly given the robust cash generation in 2025 and meaningful progress toward the company’s 2x leverage ratio objective. Management declined to commit to either option. Executives clarified that returning capital to shareholders remains under consideration, but current priorities center on safe-harbor investments and reducing outstanding debt.

Jefferies identified challenging conditions in tax equity markets and quality issues among Sunrun’s partner ecosystem as further obstacles ahead.

The firm maintained its constructive long-term view on Sunrun but anticipates limited share price appreciation through 2026 until capital market conditions normalize.

Contrarian Voice Emerges

Not all analysts share this pessimistic outlook. Clear Street analyst Tim Moore reaffirmed his Buy recommendation and increased his price objective to $24 from $23.

Moore expressed confidence despite anticipated volume reductions, highlighting Sunrun’s strategic pivot toward channels with superior profit margins. He believes the monetization strategy for newly created subscription agreements will drive improved profitability even if installation volumes decline.

Jefferies also acknowledged that third-party originators such as Sunrun stand to benefit from approximately 25% growth this year following the conclusion of the 25D tax credit—though this potential upside hasn’t yet materialized in official guidance.

Sunrun’s measured outlook contrasts sharply with industry peers like Enphase Energy, which has aggressively pursued prepaid lease and loan products as the sector undergoes transformation.

The stock concluded Friday’s trading session at $14.74, down 28% for the day.

Why LUNC Price Soared 30%

Judge Orders Rehab After New Orleans Arrest

Foreign Office advises against all but essential travel to Israel and Palestine | World News

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Financial Planning in Your 40s | #ytshorts #shorts #financialplanning #personalfinance #moneygoals

Love over hip hop, money over love (feat. Basick)

Jio Financial Services Latest News | Jio Financial Services Share News | Jio Finance Breaking News

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics17 hours ago

Politics17 hours agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business5 days ago

Business5 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat2 days ago

NewsBeat2 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics5 days ago

Politics5 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Business2 days ago

Business2 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Sports4 days ago

Sports4 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week

-

Crypto World3 days ago

Crypto World3 days agoEntering new markets without increasing payment costs