Crypto World

Strategy calls its new bitcoin funding tool an ‘iPhone’ moment but analysts warn of hidden risks

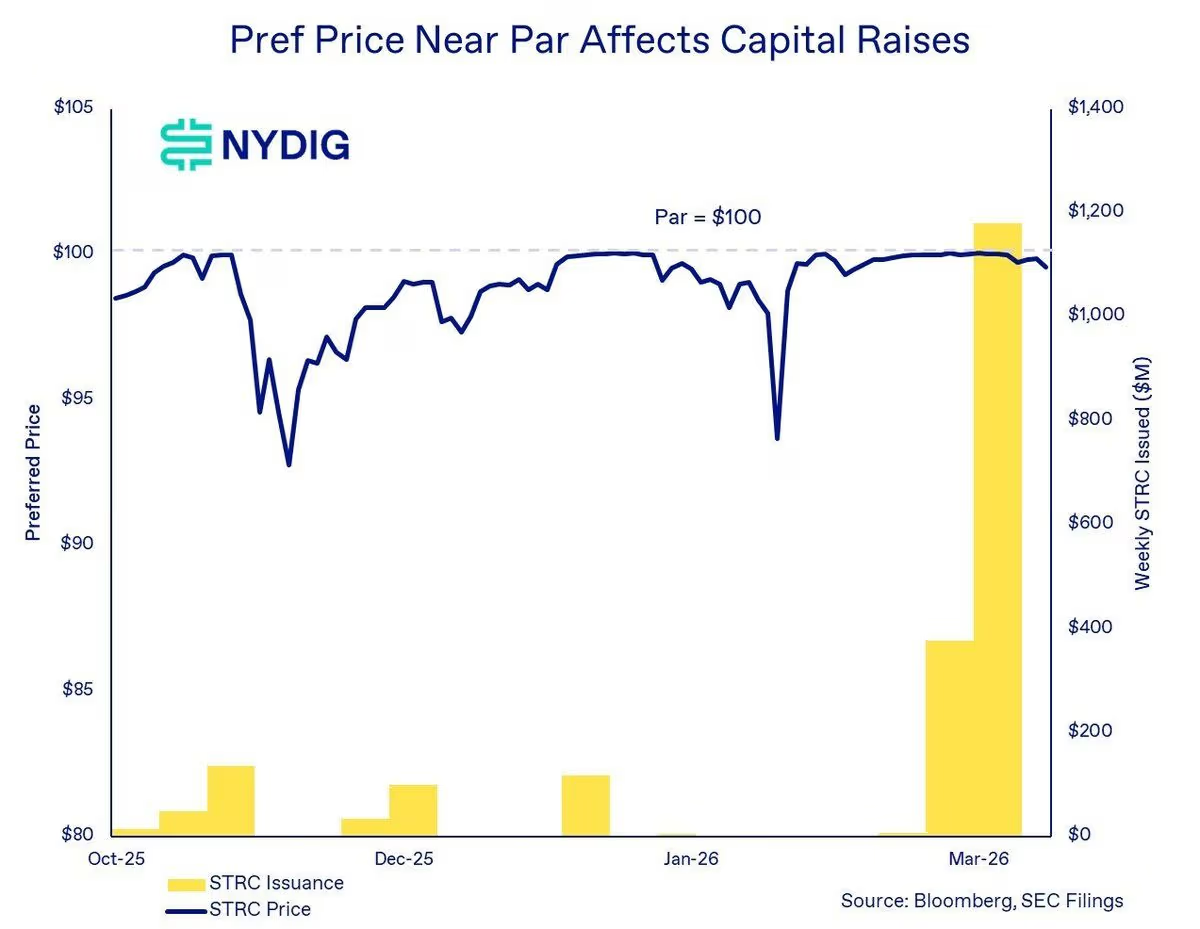

Strategy (MSTR), the leading corporate holder of bitcoin, has described the launch of its Perpetual Stretch Preferred Stock (STRC) as the firm’s “iPhone moment,” and despite its support in BTC accumulation, risks remain.

Before digging into these risks, it’s worth noting that while the focus is on STRC, specifically over its larger liquidity and adoption, they also apply to similar preferred offerings, including another bitcoin treasury company, Strive’s preferred offering, SATA.

These instruments are “not well understood through the lens of traditional credit or equity,” and instead require a different analytical framework, said NYDIG’s Global Head of Research Greg Cipolaro in a note.

By design, STRC targets a steady $100 share price, using a variable monthly dividend to keep trading near that level. The approach has already supported multi-billion dollar issuance and the acquisition of more than 50,000 bitcoin, according to STRC.live data.

At its core, STRC works by adjusting yield to steer price. If shares trade above $100, the company can trim the dividend to cool demand. If shares fall below that level, it can raise dividends to attract buyers. Keeping the price anchored lets the firm issue new shares near par, bringing in capital that is then deployed to buy bitcoin.

The novel financial instrument has been a success so far. Not only has it allowed Strategy to buy more than $3.5 billion worth of bitcoin, but it has also attracted institutions that have added STRC to their balance sheets.

In practice, the product resembles a money market fund with a floating yield of 11.5%, far above U.S. Treasuries. The appeal hinges on the steady $100 price tag coupled with high yields.

When conditions are favorable, NYDIG’s Cipolaro wrote, the mechanism creates a powerful feedback loop. The loop, in which STRC trades near par, enables the firm to raise capital, deploy proceeds to buy more bitcoin, expand the asset base, and sustain investor confidence. That confidence sustains additional issuance.

“As long as preferreds remain anchored near par, equity trades above the NAV, and capital markets stay open, the flywheel drives ongoing bitcoin demand,” Cipolaro wrote in the note.

Still, not everything’s rosy.

BitMEX Research has written in a note titled “A bit of Stretch” that it sees the risks related to the product as “substantially greater than those related to short duration U.S. treasuries.”

Where the risks actually sit

Bullish investors often point out that STRC is well-capitalized and could easily cover dividend payments, given Strategy’s massive 761,068 BTC war chest and more than $2.2 billion in cash reserves. That’s around 50 years of covered dividend payments, while the company can still lower STRC’s dividend over time to further the coverage. On top of that, there are monetization options for the company’s massive bitcoin stash, which could further dividend payments.

The risks, however, aren’t based on dividend coverage at all, according to NYDIG’s Cipolaro.

“The appropriate way to assess risk in STRC and SATA is through the lens of governance and subordination rather than focusing solely on payment risk,” he wrote.

The mechanism STRC uses also creates a stress path. If bitcoin drops and confidence in Strategy’s balance sheet weakens, STRC could slip below par.

To defend the price, the company would need to raise the dividend. Higher payouts increase cash obligations, which can, in turn, worry investors and push the price lower. That feedback loop is a familiar one in credit markets.

In a standard corporate setting, that cycle can end in forced asset sales. Companies may have to sell core holdings to meet rising obligations, locking in losses at the worst time. For Strategy, that would mean selling BTC into a falling market. However, Strategy’s Michael Saylor has repeatedly said he won’t sell the company’s bitcoin stack.

The STRC terms, however, give the company another option. The target price is not a binding promise. If conditions turn, Strategy can reduce the dividend rather than increase it.

According to BitMEX Research’s reading of the SEC filings related to STRC, Strategy can “at its absolute discretion, lower the dividend rate by up to 25 bps a month, no matter what else is happening.”

Unpaid dividends can, in addition, accrue without triggering default or forcing asset sales. As BitMEX Research put it, instruments like these were “written by the company for the company.”

Read more: Strategy’s latest massive bitcoin purchase offers insight into its evolving funding model

Built to bend, not break

That flexibility shifts what would happen to STRC in cases of a crisis.

Instead of a company caught in a squeeze, the pressure moves to the security holders. If the dividend is reduced, the yield becomes less attractive, and the market price can fall to reflect the new reality.

NYDIG’s Cipolaro made it clear in his note that the structure “can remain solvent while still delivering suboptimal outcomes for preferred holders due to the loss of confidence and funding access.” The risk isn’t a default on its dividend, but rather the loss of its attractiveness.

Strategy’s legacy software business does not cover those payments on its own. The model depends on continued issuance or balance sheet management tied to its bitcoin holdings.

The binding constraint is not income generation, but the combination of continued access to capital markets and sufficient asset coverage,” NYDIG’s Cipolaro wrote. The setup invites comparisons to structures that rely on new inflows to support payouts.

The difference here is that payouts are not fixed. If demand slows, the company can lower the dividend instead of maintaining a rate it cannot sustain. That feature helps protect the issuer but weakens the claim for investors seeking stability and income.

“When the music stops, if things become challenging for MSTR, instead of selling bitcoin, MSTR could just abandon the narrative that STRC is targeting stability,” BitMEX Research wrote. “This feels very favourable for MSTR and the dividend payments are therefore quite sustainable and affordable, in our view.”

Breaking the mechanism

Market impact will depend on how long the $100 anchor holds.

As long as demand for yield products remains strong and bitcoin sentiment is supportive, STRC can keep channeling funds into the company’s treasury strategy.

That, in turn, reinforces Strategy’s position as a major public holder of bitcoin. NYDIG has shown that bitcoin’s price stability is what enables the economic viability of at-the-market issuance of these products.

STRC and Striv’es SATA have seen their prices drop below par during periods of sharp bitcoin price declines, the firm’s research found. When that happens, “issuance becomes uneconomic, limiting the ability to raise capital and slowing the flywheel.”

The risk shows up when conditions change. A prolonged drop in BTC’s price or a shift in rates could test the price mechanism. If the dividend is cut to preserve cash, STRC could trade well below par. Losses would be borne by investors who treated the shares as a near-cash substitute.

“It resembles being short a put on bitcoin asset coverage, earning yield in exchange for bearing downside risk if bitcoin declines and erodes the asset cushion,” NYDIG offered as a frame for institutional investors. “Unlike a standard option, however, there is no fixed strike or maturity, and outcomes are path-dependent and shaped by management discretion.”

The broader significance is the template itself.

STRC blends equity features with bond-like behavior and a built-in adjustment lever. It offers a new path for companies to raise capital tied to volatile assets without locking in fixed obligations.

For now, these instruments have done their job: attract capital and support further bitcoin accumulation. The open question is how it behaves under stress and who absorbs the cost when the trade no longer looks stable.

The interpretation of that scenario isn’t great, but not for MSTR, “it’s the investors who may feel somewhat aggrieved when the music stops,” BitMEX concluded.

Read more: Strategy’s credit risk falls as preferred equity value surpasses convertible debt

The divergence between gold and Bitcoin (BTC) in 2026 can be explained by two distinct segments of buyers, according to Stephen Coltman, head of macro at crypto exchange-traded product (ETP) provider 21Shares.

Gold’s rally over the last three years has been primarily fueled by central bank buying, while Bitcoin is more widely held by individuals than financial institutions, Coltman told Cointelegraph. He said:

“Physical gold has a greater geopolitical strategic role currently, as the asset of choice for state actors who want to store wealth in a way that is protected from rival powers. This has meant that it has traded with greater sensitivity to deteriorating international relations.”

However, BTC has more utility for individuals who may use it as an alternative “lifeline” when local banking infrastructure fails during times of crisis, and accessing the traditional financial system is not possible.

“Shortly after the conflict started, both the Dubai and Abu Dhabi exchanges were shut down following missile and drone strikes from Iran,” which, he said, is a “stark reminder” of how valuable 24/7 access is in wartime situations or other emergencies.

Coltman told Cointelegraph that the inverse correlation between BTC and gold means that investors should hold both to benefit from each asset’s unique properties.

Ongoing macroeconomic and geopolitical shocks over the last several years drove gold to an all-time high of nearly $5,600 per ounce in January 2026.

However, heightened volatility dragged the precious metal back down to about $4,497 per ounce, leading to renewed debate among analysts about gold’s role as a store of value asset, and how it will perform against Bitcoin in the coming years.

Related: Bitcoin vs gold shows potential bottom signals as BTC bulls defend $70K

Financial analysts are split on gold versus BTC dominance

Bitcoin is likely to outperform gold over the next three years, according to macroeconomist Lyn Alden.

“It’s usually a pendulum between the two. If gold has gone up as much as it did, the entire diminishing return story per cycle is going to be erased in the coming one, too,” Alden said.

However, former hedge fund manager Ray Dalio expects that BTC will never replace gold as a store-of-value asset because it still trades like a risk-on asset with correlation to technology stocks, while gold is entrenched as a reserve asset in the banking system.

Magazine: Is China hoarding gold so yuan becomes global reserve instead of USD?

Crypto World

Hyperliquid Surpasses 218,000 Active Traders as Crude Oil Perpetuals Hit $300 Million Open Interest

TLDR:

- Hyperliquid’s active perpetual traders reached 218,340, marking a fresh local high with a 2.14% 24-hour gain.

- Crude oil perpetuals crossed $300M in open interest, overtaking every crypto and equity pair on Hyperliquid.

- Hyperliquid’s HIP-3 markets surpassed $1.43B in total open interest as platform activity hit an all-time high.

- Real-world assets including commodities, stocks, ETFs, and FX now account for roughly 30% of platform volume.

Hyperliquid is recording fresh activity highs across its perpetual trading platform in 2025. Active perpetual traders have reached 218,340, marking a new local high with a 24-hour gain of 2.14%.

Simultaneously, crude oil perpetuals on the platform have crossed $300 million in open interest. This figure places crude oil above every crypto and equity pair on the exchange.

Together, these numbers reflect a platform experiencing steady and measurable expansion this year.

Hyperliquid Trader Activity Recovers and Pushes Into New Territory

Hyperliquid’s active trader count has followed a notable recovery path over recent months. The platform peaked around November before pulling back sharply into January, dropping to roughly 150,000 active traders. That kind of reset typically stalls momentum on most trading platforms.

However, Hyperliquid began climbing again from late January onward. Since then, participation has moved steadily higher, reclaiming previous levels along the way. The platform has now pushed past its earlier highs into fresh territory.

According to data shared by Hyperliquid Hub on X, the platform went from around 127,000 traders in August to over 218,000 today.

That represents a broad expansion in user activity within less than a year. The growth has been gradual rather than driven by a single spike.

The post further noted a reinforcing dynamic: more traders bring more liquidity, which tightens spreads and improves execution.

Better execution, in turn, draws additional traders to the platform. This cycle has been building steadily through 2025 and continues to gain traction.

Crude Oil Perpetuals Lead Platform as Real-World Assets Drive Volume

Crude oil perpetuals have emerged as the largest market on Hyperliquid by open interest. The $300 million figure surpasses all crypto and equity pairs currently listed on the exchange. This development was reported by Delphi Digital and reflects a shift in what traders are engaging with.

Real-world assets, including commodities, stocks, ETFs, and foreign exchange pairs, now account for approximately 30% of overall platform volume.

That share represents a meaningful portion of activity. The growth of non-crypto markets on the platform has been a defining trend this year.

Hyperliquid’s HIP-3 markets have also crossed $1.43 billion in total open interest across all listed pairs. Active traders reached a new all-time high alongside this open interest figure. Both metrics moved higher together, suggesting broad participation rather than concentrated positioning.

The expansion into real-world assets marks a broader shift in how the platform is being used. Traders are no longer limited to crypto pairs when using Hyperliquid. The platform’s range of markets has grown, and so has the volume flowing through them.

Bitcoin (BTC) traded just below the $69,000 mark as traders braced for a pivotal weekly candle close, with prices hovering near the long-term line around $68,300. After a weekend slide, the setup underscores a tug-of-war between a fragile near-term outlook and the possibility of a contrarian move, even as analysts debate the significance of a fresh technical signal.

Historically, the 200-week exponential moving average has anchored multi-year cycles, but this year its reliability has been questioned. Cointelegraph has noted that the long-term EMA has failed to act as a clear support in 2026, complicating investor expectations for a durable bottom or renewed upside. As BTC approached the $68,300 region, traders watched to see whether the weekly close would restore any confidence in the metric or amplify the lingering bearish bias.

Key takeaways

-

Bitcoin remained under $69,000, testing the 200-week EMA near $68,300 as a critical reference point for the weekly close.

-

Market psychology tilted toward caution, with substantial liquidations signaling risk-off dynamics over the past 24 hours.

-

A fresh bullish tempo appeared with a golden cross developing between the 21-day and 50-day moving averages, but durability remains uncertain.

-

Analysts split on the path forward: some warn of continued macro downside even as near-term momentum offers a potential relief rally.

Weekend test of the long-term line

Trading data show BTC price action around the 200-week trend line, a level that has historically framed major cycles even as the asset wobbled through the weekend. The immediate vicinity of $68,300 serves as a focal point for whether bulls can sustain a bid above entrenched resistance or if sellers reassert control as the weekly close approaches.

Extended downside pressure in the days leading into the close produced notable liquidations across the market. CoinGlass reported that more than $300 million in long positions were liquidated, with roughly $100 million in shorts also liquidating in the same window. The liquidation profile underscores a risk-off environment in which traders are shrinking risk exposure into key technical junctures.

From a chart perspective, BTC’s motion around the 200-week EMA has reinvigorated debate about whether this line can again offer a meaningful foothold. In a broader 2026 context, some analysts have warned that the EMA’s traditional role as a durable support may be waning, complicating the interpretation of daily moves around this level.

Liquidity pressure and trader sentiment

The weekend action underscored a broader mood among market participants: risk appetite remains fragile as macro uncertainties persist. With a large portion of the futures market liquidated into the close, traders may adopt a cautious stance, awaiting a clearer directional cue from the weekly close and any subsequent macro catalysts.

In such a regime, the key question is whether the counter-move, if it occurs, can sustain momentum beyond a relief rally. The balance between safe-haven flows and renewed appetite for risk will likely define BTC’s trajectory over the coming sessions, particularly as market participants await more concrete signals from on-chain data, derivatives activity, and broader market liquidity conditions.

Momentum flicker: the Golden Cross and what it may imply

On the technical front, a visible positive signal emerged as the 21-day simple moving average crossed above the 50-day moving average, a formation often interpreted as a short-term momentum cue. Proponents of the setup cautioned that the cross could herald a temporary lift, though they emphasized that durability would hinge on subsequent price action.

Keith Alan, cofounder of trading resource Material Indicators, commented on the potential implications, saying the Golden Cross “will likely deliver some short term bullish momentum. Must watch to see if it develops into something durable.” He added a more cautious note, reflecting the prevailing sentiment: “For now…the range game continues.”

These near-term signals come after March saw two “death crosses” on BTC’s daily chart, a pattern historically associated with renewed downside pressure. The market’s interpretation of a Golden Cross in the current environment remains mixed: a possible spark for a bounce, but no guarantee of a sustained breakout without follow-through from higher timeframes.

Bearish undertones persist in higher timeframes

Several well-known traders have stressed that longer-horizon momentum remains skewed to the downside. A prominent analyst reiterated a bearish thesis for the macro cycle, highlighting ongoing fragility in higher timeframes despite any short-term bullish cues. The tension between near-term momentum signals and longer-term risk remains a defining feature of the BTC narrative as the market approaches another pivotal weekly close.

“There are still 0 signs of bear market exhaustion on HTF. No divs, no bear PA exhaustion, no momentum loss, etc.” He also noted a continued outlook for lower prices, saying, “I still have high confidence in seeing 50k and likely a bit lower.”

That sentiment sits alongside reminders from earlier periods that the market can swing on a few data points, even as long-run structural factors weigh on price discovery. The debate over whether BTC can muster a sustained recovery or slide toward new macro-driven lows remains unresolved, with bulls awaiting confirmation from price action and bears watching for any renewed downside momentum.

What readers should watch next

The immediate focus for BTC markets is the weekly candle close and how price behaves in the aftermath. If the price can hold above key support near the 200-week EMA and demonstrate follow-through above near-term moving averages, a cautious upside tilt could emerge. Conversely, failure to defend the region around $68,000–$68,300 may invite renewed selling pressure and retesting of lower support bands.

Investors should also monitor liquidity patterns and derivatives activity as they often foreshadow the next directional move. In addition, traders will be paying close attention to any shifts in macro sentiment or changes in the risk-on/risk-off appetite that can influence Bitcoin’s risk premium and its correlation with broader markets.

This ongoing narrative—between a fragile near-term bounce and the weight of higher-timeframe bears—will likely shape price action in the weeks ahead. As always, readers are advised to conduct their own research and consider how these developments fit their risk tolerance and investment horizon.

TLDR:

- BTC dominance has been ranging between 58% and 60% for months and is now approaching the critical 58% range low.

- Analyst CryptoCandy24x expects a rotation back to 60% or higher if BTC dominance holds firmly above the 58% boundary.

A CME gap at 70.1K remains unfilled, with analysts watching for a potential rejection that could push Bitcoin toward 66K. - Analyst maintains a short position, warning that Bitcoin’s structure stays bearish while price trades below the 71.4K level.

BTC dominance is nearing the 58% range low as Bitcoin’s price holds around $67,922, drawing attention from analysts across the market.

The metric has been cycling between 58% and 60% for months, and its latest move toward the lower boundary is happening alongside a key CME gap sitting at 70.1K.

Traders are now watching both developments closely, as the outcome of each could shape Bitcoin’s short-term price direction in the days ahead.

BTC Dominance Tests Critical Support at 58%

BTC dominance has been trapped in a defined range between 58% and 60% for several months. The metric has repeatedly rotated from the range high to the range low without breaking in either direction.

This prolonged consolidation has kept traders on alert for any sign of a decisive move. The current approach toward 58% is now putting that lower boundary under renewed pressure.

Analyst @cryptocandy24x noted that BTC dominance is once again approaching the range low near 58%. According to the analyst, if the current momentum holds, a rotation back toward the 60% range high is possible in the coming days.

However, this outlook only remains valid as long as BTC dominance holds above the 58% level. A confirmed breakdown below that mark would shift the bias in a different direction entirely.

A hold at 58% would suggest Bitcoin is maintaining its market share against altcoins. If dominance bounces from this level, it would align with the analyst’s expectation of a return toward 60% or higher.

On the other hand, a drop below 58% could signal growing altcoin strength across the broader market. The next few sessions will be telling as to which scenario plays out.

CME Gap at 70.1K Adds Pressure to Bitcoin’s Short-Term Outlook

While BTC dominance tests its range low, Bitcoin’s price is also facing a notable technical setup overhead. The CME closed at 70.1K, leaving a gap below the close that the market has yet to address.

Gaps of this nature have historically shown a strong tendency to get filled at some point. This makes the 70.1K level a significant reference point for traders planning their next moves.

Analyst @KillaXBT provided an update on how Bitcoin’s structure is developing around these key levels. The analyst noted that a push toward the CME gap, followed by a rejection, could lead to a retest of the 66K level next week.

KillaXBT also confirmed that the broader structure remains bearish while Bitcoin stays below 71.4K. The analyst noted they remain short and are tracking how price reacts at these zones.

A gap fill at 70.1K followed by a strong rejection would add more weight to the bearish case currently building. Traders are therefore watching for entry signals around that level ahead of any potential downside continuation.

The 66K area, meanwhile, stands as the next key support zone if selling pressure resumes. Until Bitcoin reclaims 71.4K, the market structure continues to favor the downside.

TLDR:

- Strategy has scaled its Bitcoin raises from hundreds of millions to over $1.8 billion per round in 2026.

- Five instruments, MSTR, STRK, STRF, STRD, and STRC, fund weekly Bitcoin purchases across investor profiles.

- Strategy recorded 12 consecutive weekly Bitcoin buys in 2026, regardless of short-term price movements.

- With 761,000 BTC held, Strategy still needs roughly 260,000 more coins to hit its one-million target by 2026.

Strategy has notably increased the pace of its Bitcoin accumulation through a series of larger and more frequent capital raises.

The company, led by Michael Saylor, has moved from occasional fundraising rounds to near-weekly capital deployments.

This shift has allowed Strategy to stack Bitcoin at a scale that few institutional players can match. The company currently holds over 761,000 Bitcoin and is targeting one million coins by the end of 2026.

Capital Raise Volume Grows From Millions to Billions

Between 2021 and 2023, Strategy raised capital through relatively modest and infrequent transactions. Convertible notes and occasional equity raises were the primary tools used during that stretch.

The amounts were in the hundreds of millions at most. The overall pace was slow compared to what the company would later execute.

That changed sharply heading into 2025 and 2026. Strategy began closing raises of $1 billion, $1.4 billion, and $1.8 billion in rapid succession.

The frequency moved from quarterly to weekly across that period. Crypto analyst Axel Bitblaze described the shift on X, calling Strategy “a bitcoin vacuum cleaner” that Saylor has carefully engineered.

The larger raises are now structured across five separate financial instruments. These are MSTR equity, STRK, STRF, STRD, and STRC.

Each instrument attracts a different type of investor within the capital stack. This design allows Strategy to pull in capital from a much wider pool of institutional and retail participants.

The broader result is a self-reinforcing system. As more investors seek yield or equity upside, more capital flows into Bitcoin purchases.

Bitblaze noted that Saylor has effectively built “a bitcoin-backed yield curve inside a single company.” Wall Street demand, therefore, converts directly and automatically into Bitcoin demand every single week.

Weekly Purchase Cadence Drives Steady Bitcoin Demand

Strategy recorded 12 consecutive weekly Bitcoin purchases throughout 2026 alone. Each purchase was funded through one or more of the five capital instruments currently in use.

The consistency of these buys has remained steady regardless of short-term price movements. No week was skipped even during periods of broader market uncertainty.

With 761,000 Bitcoin already on its balance sheet, Strategy still requires approximately 260,000 more coins to hit its one-million target.

That remaining demand translates into ongoing and predictable buying pressure across the market. The purchase timeline runs through the end of 2026. Price action along the way does not appear to alter the accumulation schedule.

Saylor recently posted the phrase “The Orange March Continues” across his social media channels. Analysts quickly read the statement as a signal of another imminent purchase.

Bitcoin was trading near $68,425 at the time. According to observers, the market had not yet priced in the anticipated move.

Strategy’s expanded capital raise program directly funds each new round of Bitcoin acquisitions. Larger raises mean larger and more frequent purchases moving forward.

The five-instrument structure ensures that investor demand across different risk profiles continues feeding the system.

For the broader Bitcoin market, this translates into a sustained and growing source of institutional buying pressure week after week.

Crypto World

Solana Head and Shoulders Breakdown Triggers Bearish Outlook Amid On-Chain Selling Pressure

TLDR:

- Solana confirms a head and shoulders breakdown, projecting downside toward the $70–$77 range.

- Market cap fell from $55B, signaling capital outflows and weakening investor confidence.

- On-chain data shows sustained realized losses, with daily selling pressure between $30M and $50M.

- Exchange outflows rose sharply, yet the price remains weak due to a lack of strong buyer demand.

Solana price analysis indicates a confirmed bearish reversal after a structured breakdown. Price action, declining market cap, and on-chain signals collectively point to sustained selling pressure in the near term.

Head and Shoulders Breakdown Signals Trend Reversal

Solana price has shown a clear head and shoulders formation after an extended uptrend. The pattern includes a defined left shoulder, a higher peak, and a lower right shoulder.

This structure typically signals exhaustion among buyers and a shift in trend direction. The neckline formed as a slightly ascending support level, reflecting earlier higher lows.

However, price action failed to hold this zone, leading to a decisive breakdown. This move confirmed a structural shift, with sellers gaining control of momentum.

Following the breakdown, Solana declined nearly 4% toward the $86 level. This move aligns with the expected reaction after a neckline breach.

The measured move projects a downside range between $70 and $77, based on the pattern’s height. $SOL has confirmed a head and shoulders breakdown.

If the price fails to reclaim this level, it may act as resistance. This scenario often accelerates selling pressure and reinforces the bearish outlook.

Market Cap and On-Chain Data Confirm Weakness

Solana’s network valuation peaked near $55 billion before entering a sharp decline phase. This drop reflects strong distribution activity and reduced participation. The initial decline around March 17 marked a turning point in sentiment.

Market cap fell rapidly, suggesting large holders exited positions. Afterward, the price entered a consolidation phase between $50 billion and $52 billion.

However, recovery attempts remained weak and formed lower highs. A further decline below $50 billion aligned with the neckline breakdown.

This confluence between price structure and capital flow strengthens the bearish case. Sustained weakness below this level may support the projected downside targets.

On-chain data adds another layer to the analysis. Net realized profit and loss shows continued selling at a loss since mid-February.

Daily losses range between $30 million and $50 million, indicating persistent pressure.Exchange flow data shows a shift, with outflows reaching 700,000 SOL after March 17.

This suggests reduced selling supply on exchanges. However, price has not responded positively, indicating weak demand.

Currently, Solana trades near $87.29, below key support at $88.02. A sustained move lower may expose the next support at $81.60. Resistance remains near $92.19, where buyers must regain strength.

Crypto World

The CLARITY Act Is Under Threat of Depayment Delay Although a Stablecoin Deal Is Being Made

Stablecoin Deal Is a Partial Victory

According to recent reports, the Senate leaders and the White House achieved a consensus on stablecoin yields. This move has resolved one of the major conflicts between crypto companies and banks. Thorn, however, said that the progress was good but still needs some work. Thorn pointed to the fact that a number of thorny issues may still delay the passage of the bill through Congress. These are the decentralization of finance monitoring, the security of the developers, and the regulatory framework. Furthermore, ethical considerations can also attract the attention in the process of further discussion.

The policy advisors of the US have noted that the negotiations are not over with the stablecoin issue. Participants of the discussions stated that the lawmakers should resolve the pending issues before the bill is completed. Besides, they characterized the new accord as a significant measure, as opposed to a solution.

Players in the industry have noted that there is a small legislative window in which the CLARITY Act should be passed. Kristin Smith of the Solana Institute told that the lawmakers should hope to pass it by August. In addition, she observed that the congressional timetable is even more restricted when there is greater activity in terms of election matters towards the end of the year. Senator Cynthia Lummis has proceeded to urge the bill to move forward quickly through the Congressional Banking Committee. She noted that the lawmakers would be able to pick the markup step during the Easter recess. Additionally, she has once again stated that timely passage is still relevant in developing the regulation of digital assets.

Mediators Prefer to have an Early Contact

The regional intermediaries have intervened to deliver messages between the two parties. Egypt, Qatar and the United Kingdom have relayed positions as part of early outreach activities. Furthermore, their contacts demonstrate that both Washington and Tehran are examining the possibility of the negotiations framework.Iran has already conveyed rigid terms of getting down to formal negotiations. These are a ceasefire, guarantees of new war and financial compensation. Moreover, the location of Tehran indicates the issues of security in the long term and economic recovery of the city following weeks of conflicts.

The US has also stipulated some conditions that the conflict will come to an end. They are terminated development of missiles during several years and imposed restrictions on the uranium enrichment. In addition to the above, Washington aims at containing the activities of Iran supporting regional factions aligned to its interests.President Donald Trump said that US forces have undermined the military capacity of Iran in the course of operations. He pointed out that there is massive destruction of missile systems among other assets. Therefore, the administration looks at the present development as a foundation of strategy change.

According to Trump, the US is contaminating with a possibility to reduce its military presence in the region. In addition, he associated this action to attainment of major goals against Iranian capabilities. This trend represents the shift of active operations to a diplomatic solution.Oil prices around the world have remained high because it is not clear that there will be a route to supply the product. The Strait of Hormuz is still impacting the market sentiment because it cannot move freely. As a result, the cryptocurrency market is on the alert due to geopolitical risks.The market has reacted to the shifting trends in the war. Prices improved due to the reports of relaxed sanctions of Iranian oil exports. But the volatility has not ended yet because investors are monitoring the military and diplomatic signs closely.

Risk-Off Drips throughout Markets

The world markets became risk-off when geopolitical tension escalated in the Middle East. Further, increasing uncertainty drove investors out of risky in the form of Bitcoin and Ethereum. Equities and commodities, too, reacted by this change, with a more extended response. Due to the oil infrastructure related disruptions in Iran, oil prices went up. Also, increased energy prices were an issue that was of concern to inflation and economic growth. Therefore, investors changed portfolios in order to minimize the exposure of risk sensitive assets.

New information published by the U.S. Bureau of Labor Statistics indicated that producer prices increased than anticipated in February. The Producer Price Index rose by 0.7% on a monthly basis and stood at 3.4% on an annual basis. Therefore, expectations for an interest-rate reduction have been undermined, as monetary risks of inflation still exist. Markets are concerned about the upcoming Federal Open Market Committee meeting. The traders assume that rates will be maintained between 3.50% and 3.75% in the near term. Nevertheless, the lack of clarity in the direction of policy has been promoting investment in crypto assets reduction among investors.

Chain data revealed that short-term Bitcoin owners transferred big amounts to exchanges. Over 48,000 BTC had been deposited in profit on exchanges within one day. This activity indicated that there is intensified selling pressure during the recent price rebounds. Short-term holders kept generating profits as Bitcoin moved to higher resistance levels. Besides, a good number of investors decided to sell off rather than to hold during volatility. This action decreased the upward movement and led to recurring pullbacks. At the report date, the price of Bitcoin was close to 72,229, a daily drop. Ethereum fell to approximately 2,235, although other currencies like XRP and BNB gained losses as well. Moreover, the general market environment continued to be sensitive, with sentiment remaining low.

Crypto World

BTC Miner Inflows to Binance Hit Lowest Levels Since June 2023 Amid Reduced Selling Pressure

TLDR:

- BTC miner inflows to Binance have dropped to their lowest monthly average since June 5, 2023.

- The U.S. ice storm forced miners to sell BTC to cover fixed costs despite reduced operations.

Combined miner inflows across all exchanges currently stand at approximately 4,381 BTC monthly. - Miners are estimated to hold 1.8 million BTC in reserve, making their behavior critical to watch.

BTC miner inflows to Binance have dropped to historically low levels in recent weeks. This follows a sharp spike recorded during the ice storm that struck the United States in late January and early February.

The monthly average now stands at approximately 4,316 BTC. Across all exchanges, the combined figure reaches 4,381 BTC. Analysts view this shift as a reduction in structural selling pressure from the mining cohort.

Ice Storm Forces U.S. Mining Pools to Liquidate BTC Holdings

Several large U.S.-based mining pools slowed down or halted operations during the storm. The extreme weather disrupted normal mining activity across affected regions.

However, fixed costs such as electricity, infrastructure, and operational expenses remained constant. This financial pressure pushed some miners to sell BTC in order to maintain liquidity.

On-chain analyst Darkfost noted the sharp rise in miner inflows during that period. The data showed a clear correlation between the weather event and increased BTC distribution to exchanges.

Miners facing reduced output still needed to cover ongoing operational costs. Selling into the market became the most practical solution for many affected operations.

The spike in inflows was a temporary reaction to an external shock. Once weather conditions normalized, mining activity gradually resumed across the United States.

With operations back online, the need to liquidate BTC eased considerably. The data confirms the increase was event-driven rather than structural.

This pattern is not uncommon when miners face unexpected downtime. External disruptions can quickly shift miner behavior from accumulation toward distribution.

When income drops but costs remain fixed, selling becomes the most immediate option available. The ice storm served as a clear example of how operational risk translates directly into market activity.

Miner Reserves and Reduced Selling Pressure Point to Market Stability

Since the storm subsided, BTC miner inflows have reversed sharply to the downside. The current monthly average of 4,316 BTC marks the lowest reading since June 5, 2023.

This decline points to miners retaining more BTC rather than routing it toward exchanges. Lower exchange inflows typically reflect reduced selling intent from this cohort.

According to Darkfost’s analysis, miners currently hold an estimated 1.8 million BTC in reserves. This represents a large supply pool that could enter the market under shifting conditions.

Any move to increase distribution from these reserves could generate considerable selling pressure. Monitoring miner behavior therefore remains a critical component of broader market analysis.

At present, the data suggests miners are in a conservative distribution phase. The reduction in exchange inflows across both Binance and the wider market supports this reading.

Miner-driven selling pressure appears relatively contained at this stage. This backdrop can support near-term price stability for BTC.

The trend requires continued monitoring as market conditions evolve. If BTC prices decline sharply, miners may resume higher distribution to manage cash flow.

Conversely, rising prices could encourage further holding. Miner inflow data remains one of the more reliable on-chain indicators for gauging supply-side pressure.

Musk says SpaceX and Tesla to build advanced chip factories in Austin

BTC Performance Driven By Individuals While Central Banks Drive Gold Price

What ‘SNL UK’ Can Do That The U.S. Version Can’t

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics2 days ago

Politics2 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech5 days ago

Tech5 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World23 hours ago

Crypto World23 hours agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos4 days ago

News Videos4 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World24 hours ago

Crypto World24 hours agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Crypto World2 days ago

Crypto World2 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Business6 days ago

Business6 days agoAustralian shares drop as Iran war enters third week

-

Crypto World6 days ago

Crypto World6 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Politics5 days ago

Politics5 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion6 days ago

Fashion6 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Tech3 days ago

Tech3 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Politics5 days ago

Politics5 days agoReal-time pollution monitoring calls after boy nearly dies

-

Crypto World4 days ago

Crypto World4 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

NewsBeat4 days ago

NewsBeat4 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business6 days ago

Business6 days agoMeta planning major layoffs as AI spending and automation reshape workforce

-

News Videos4 days ago

News Videos4 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Business4 days ago

Business4 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

-

Politics3 days ago

Politics3 days agoGender equality discussions at UN face pushbacks and US resistance

-

Entertainment6 days ago

Oscars reunite Rob Reiner supergroup of 17 stars for emotional tribute: Here's who appeared on stage

You must be logged in to post a comment Login