Crypto World

Swift built its blockchain. It chose deposits over XRP

For fifteen years the loudest promise in crypto was that XRP would replace Swift. Not complement it, not plug into it, replace it: the slow, expensive, pre-funded machinery of correspondent banking swept away by a bridge asset that settles in seconds.

Summary

- Swift’s blockchain ledger went live with 17 major banks and chose tokenized deposits, not XRP.

- The system targets real-time liquidity management and cross-border settlement inside existing bank balance sheets.

- XRP rallied on the headline, but the architecture leaves no public bridge asset in the middle.

- The strongest XRP arguments rely on old artifacts, overlapping relationships, and optional future liquidity use cases.

- The launch weakens the original “XRP replaces Swift” thesis while leaving Ripple’s broader business intact.

It was the thesis that sold the token, filled the conference halls, and outlasted a five-year lawsuit.On July 9, 2026, Swift answered.

The network moved its own blockchain ledger into live operation with seventeen pioneer banks, among them Citi, HSBC, Wells Fargo, UBS, Standard Chartered, and MUFG. The build took nine months. The system runs 24 hours a day across six continents, coordinating cross-border payments on a shared ledger that eliminates the batch windows and cut-off times that made correspondent banking feel like a fax machine. It is, by any fair reading, Swift doing the thing everyone said Swift would never do: shipping blockchain settlement, at scale, with the incumbents, before the disruptor could take the market.

And the asset moving across it is tokenized bank deposits. Not XRP. Not any public token. Banks convert dollars and euros they already hold into digital claims and send those claims to each other directly. No third coin sits in the middle.

That is not a rumor, a leak, or an interpretation. It is the design, and it is the most consequential piece of information the XRP thesis has received since the SEC dropped its appeal.What followed was five days of the loudest argument the XRP community has had in years, conducted almost entirely over a resurfaced slide and a two-word post from a man who no longer works there. That argument is worth walking through, because the way it is being fought reveals more than the thing being fought over.

What Swift actually shipped

The details matter, because the gap between what was announced and what was believed became its own story within hours.

Swift confirmed that its blockchain-enabled shared ledger completed roughly nine months of development and testing and is ready for commercial use. The stated purpose is liquidity management: letting banks monitor and move tokenized deposits in real time, with visibility into cash positions across institutions. The system reportedly runs on Hyperledger Besu with Chainlink’s cross-chain interoperability protocol handling messaging between chains, though that stack detail comes from secondary reporting rather than a Swift technical disclosure and deserves the caveat.

The seventeen pilot banks are not a random sample. They are the tier-one institutions that XRP holders spent a decade naming as future Ripple customers. Citi. HSBC. Wells Fargo. UBS. MUFG. Standard Chartered. When Swift decided how money would move in a tokenized era, it convened exactly the banks the bridge-asset thesis was waiting on, and those banks agreed to test settlement using their own deposits.

The ledger’s economic function is worth stating plainly, because it is where the XRP question actually lives. Its purpose is to let banks see and move their own liquidity in real time across a shared record. Every participant reads the same state. Positions net continuously instead of at end of day. Cut-off times stop existing. Whatever else that is, it is a direct attack on the specific inefficiency that made a bridge asset attractive in the first place, executed by the party that owns the relationships.

Swift has also signaled where this goes next, describing an ambition to become a platform for programmable money and agentic commerce, payments that execute automatically when conditions are met without a human approving each one. That is not a defensive crouch. It is a network that watched the tokenization argument play out for a decade and decided to build the endgame itself.crypto.news covered the market’s immediate reaction, which was, revealingly, a rally. XRP rose on the news that Swift had built a system without it.

Why the rally happened

That reaction is the most interesting thing in this story, because it was not irrational. It was the product of a genuine ambiguity that both sides are now exploiting.

Two of the seventeen banks, Standard Chartered and UBS, already work with Ripple through custody or payment infrastructure on the XRP Ledger. Ripple Treasury entered Swift’s Certified Partner Program in April 2026. Swift’s broader payments framework names more than thirty institutions with existing Ripple relationships, a set that extends beyond the seventeen pilot participants, though the overlap has never been specified. Read those facts quickly and it looks like Ripple is inside the tent.

Then the artifacts arrived. A researcher operating as SMQKE resurfaced a Swift-branded slide that places Ripple explicitly in the middle of a payment flow, positioned between local bank and local bank. A widely shared clip features a former Swift insider, now linked to Euro Exim Bank, predicting XRP adoption within the network. The slide got called a mic-drop moment. The clip got called verbatim proof.

The rebuttal came just as fast and from a more credentialed source. Tom Zschach spent six years as Swift’s Chief Innovation Officer, running the network’s digital asset strategy. He answered the rumor with two words: not happening. A separate analyst urged followers to stop engaging with anyone claiming Swift currently uses XRP, on the grounds that the only public evidence shows adoption of ISO 20022 messaging standards, which is a data format, not an asset choice.

Both sides have a problem. Zschach left Swift earlier this year and has criticized Ripple for years, which makes his read informed but personal and not official policy. The slide is undated, resurfaced rather than leaked, and interpreted through a YouTube channel and an anonymous account. Neither is evidence in the sense that a production integration would be evidence.

What is not ambiguous is the ledger. Seventeen banks. Tokenized deposits. Live.

A decade of the banks saying no

The July 9 launch reads differently once you remember how long the question has been open, because the record is not one of banks failing to understand the pitch. It is one of banks understanding it precisely and declining.

Ripple’s original enterprise product was messaging: a way for banks to exchange payment instructions with better data and fewer errors than legacy rails. Banks bought that. Santander, SBI, Standard Chartered, and hundreds of others signed on across the late 2010s, and RippleNet became a real business. Then came the second ask, the one the token depended on: route your liquidity through XRP instead of pre-funding accounts. That ask went almost nowhere. The company’s own On-Demand Liquidity product reached a fraction of its partner base, and most institutions stayed on the messaging layer and never touched the asset, a divide crypto.news has documented at length across the XRP vertical.

The explanations offered for that gap were always circumstantial: regulatory uncertainty, the SEC lawsuit, accounting treatment, custody immaturity, market depth. Each was legitimate at the time. Each has since been resolved or substantially reduced. XRP is classified as a digital commodity. The lawsuit ended. Custody is a solved product sold by every major bank. Market depth is adequate for the ticket sizes involved.

So the circumstantial explanations have expired, and the behavior has not changed. When the constraints lift and the decision stays the same, the constraints were not the reason. That is the uncomfortable inference available on July 9 and it does not require believing anything bad about Ripple, only accepting that treasurers weighing a volatile bridge asset against a deposit token they issue themselves have a preference, and have had it for ten years, and just spent nine months building infrastructure that encodes it.

The thesis under the argument

Strip away the personalities and one real technical dispute remains, and it is worth stating precisely because it is the only part that could still cut Ripple’s way.

The bridge-asset argument was never about messaging. It was about nostro and vostro accounts, the pre-funded pools of foreign currency that banks must park in every destination country in order to settle. That trapped capital is the actual cost of correspondent banking, running to trillions globally, and it is the problem XRP was designed to solve: instead of pre-funding a lira account in Turkey, a bank buys XRP, sends it in seconds, and sells it into lira at the far end, freeing the capital that was sitting idle.

Ripple’s supporters argue that Swift’s upgrade is a front-end improvement that does not touch this. Tokenized deposits are still deposits. If a bank sends a tokenized dollar to a bank that needs lira, someone still has to bridge the currency pair, and a shared ledger does not conjure liquidity where none exists. On this reading, Swift built a faster pipe and left the plumbing problem intact, which is exactly the gap XRP was built for.

The counter is harder and mostly wins. A shared ledger with real-time visibility across seventeen tier-one banks changes the economics of pre-funding even if it does not abolish it, because the reason nostro balances are so large is uncertainty about position and timing. Netting improves. Buffers shrink. And critically, the tokenized-deposit model gives banks something a public bridge asset never could: settlement in an instrument they already issue, with no exposure to a volatile third token, no market-maker spread, and no question about who is liable when the price moves mid-transfer. The bridge asset solves trapped capital by introducing price risk and a dependency on a token’s liquidity. Banks have been consistent for a decade about which trade-off they prefer, and Swift just built infrastructure that encodes the answer.

There is one more asymmetry the bridge argument tends to skip. A tokenized deposit is a liability of a regulated bank, which means it arrives inside the legal and accounting framework treasurers already operate in. A bridge asset is a bearer instrument on a public ledger, which means somebody has to write a policy for holding it, mark it to market, explain it to an auditor, and answer for it when it gaps. That is not a technology problem and no amount of settlement speed fixes it. It is why the ODL conversion rate stayed low even in corridors where the math worked, and it is the quiet reason Swift’s design was always the likelier winner.

The honest version is that Swift’s ledger does not make XRP technically impossible as a liquidity leg. It makes it commercially unnecessary for the corridors that matter most, which is a slower and more final kind of defeat.

What the artifacts actually show

The evidentiary standard in this argument collapsed almost immediately, and it is worth being precise about what each item is, because the community is treating them as interchangeable.

The Swift-branded slide is the strongest bull artifact and the weakest form of evidence. It is undated. It was resurfaced by a researcher rather than released or leaked. Nobody has confirmed when it was produced, for what audience, whether it described a live integration or a hypothetical architecture, or whether it survived contact with a product decision. Corporate slide decks are full of vendors placed in diagrams during evaluation phases that ended in no. Even read maximally, the slide depicts Ripple as a connector or optional leg inside Swift-adjacent infrastructure, which is a substantially smaller claim than the thesis it is being used to defend.

Zschach’s post is the strongest bear artifact and is also not evidence. He is a former executive stating a personal view, months after departure, about an organization whose current architecture he no longer sets, and he has a documented history of criticizing Ripple. His read is well-informed. It is not policy.

The Euro Exim Bank thread is the strangest of the three. Its force comes from David Schwartz’s court testimony, where Ripple’s chief technology officer initially told regulators that the company’s primary customers were not banks, and later acknowledged failing to mention Euro Exim Bank as a bank customer using XRP. The XRP argument holds that this proves the asset is already in production use at the margins of traditional finance. It does prove that. It also concedes the scale: the reference case, cited in 2026 as evidence of bank adoption, is a trade finance specialist that nobody would mistake for a tier-one institution. If the strongest live example is Euro Exim Bank while the seventeen banks on Swift’s ledger are Citi, HSBC, and Wells Fargo, the argument has answered itself.

The pattern across all three is the same. The bull case runs on interpretation of artifacts. The bear case runs on a live system with named participants. Those are not the same kind of fact.

The case that this changes nothing for Ripple

Now the argument that Ripple’s defenders make, and it deserves a serious hearing, because on the corporate side it is largely correct.

Ripple never needed Swift. The company runs its own corridors, its own bank relationships with Santander and SBI, and its own dollar stablecoin. Ripple Prime, the institutional arm built out of the Hidden Road acquisition, has cleared more than $3 trillion across roughly 300 institutional clients. The company spent the last two years buying its way into prime brokerage, treasury software, and payments infrastructure, and none of that revenue routes through Swift or depends on Swift’s approval. A network that competes with Ripple’s messaging business building a better messaging business is a competitive fact, not an existential one.

The direction of travel also vindicates Ripple intellectually, which is not nothing. Swift spent years dismissing blockchain settlement and has now shipped 24/7 tokenized cross-border payments with an explicit roadmap toward programmable money and agentic commerce. That is Ripple’s thesis, delivered by Ripple’s incumbent. Being right about where finance was heading, and losing the contract anyway, is a real outcome, and Ripple’s supporters are entitled to point out that nobody was building this in 2015 except them.

Ripple is also still in the room. The Certified Partner Program membership is real. The Ripple-linked institutions inside Swift’s framework are real. Standard Chartered and UBS working with both is real. Nothing about the July 9 launch forecloses XRP serving as an optional liquidity leg for exotic corridors where no deep deposit market exists, which is precisely what the resurfaced slide depicts, and which was always the realistic ceiling for a bridge asset anyway.

And Ripple’s institutional business keeps compounding regardless. The XRP Ledger’s credit layer is in validator voting, an effort crypto.news examined in detail in its analysis o what on-chain credit means for XRP. SBI Digital Finance and Doppler announced institutional XRP lending infrastructure for Japan on July 13. Goldman Sachs sits atop the XRP ETF holder table with a $153.8 million position, a fact crypto.news reported when the funds crossed $1.53 billion. The company is fine. That was never the question.

Ripple in 2026 is a payments and prime brokerage conglomerate with a stablecoin, a pending bank charter, and billions in acquisitions behind it, and it would remain all of those things if XRP traded at fifty cents.

The case that it is the end of an argument

The question was always whether Ripple being fine does anything for XRP, and July 9 is the cleanest data point anyone has produced.

Here is the uncomfortable sequence. The bridge-asset thesis required banks to hold and route a volatile public token. The banks said no for a decade. XRP holders explained that the banks were slow, captured, and would come around once the technology proved itself and the regulatory fog lifted. The fog lifted: XRP is a digital commodity, the lawsuit is over, the appeals are dropped. The technology proved itself: Swift just deployed it. And at the exact moment both preconditions were satisfied, the seventeen largest banks in the world adopted tokenized settlement and chose deposits.That is not the banks being slow. That is the banks answering.

The market noticed even while the price rallied. Spot XRP ETFs recorded $7.29 million of net outflows on July 8, the largest single-day withdrawal since March. Open interest fell from $2.58 billion on July 5 to $2.33 billion on July 9 as traders closed positions instead of opening them. The long-to-short ratio slipped to 0.96, meaning bears slightly outnumbered bulls into the news. Retail bought the Swift headline. Institutions sold into it. When those two groups disagree about an institutional-adoption story, the institutions are usually the ones who read the announcement.

That divergence is the tell worth carrying forward. Price reacted to the word Swift appearing next to the word blockchain. Flow reacted to the architecture. Over any horizon longer than a week, flow wins.

The deeper problem is that this compounds with everything else already on the record. Most of Ripple’s bank partners use RippleNet for messaging and never touch the token. The XRP Ledger’s EVM sidechain, built to give XRP a DeFi economy, holds $25,741 and trades nothing. RLUSD, Ripple’s own product, has grown into a business while the ledger’s native asset has not. Each of these is survivable alone. Together they describe a pattern: every route by which value was supposed to reach XRP has been tested, and the value keeps arriving somewhere else.

Swift is the biggest of those tests because it was the original one. The thesis was not that XRP would find a niche. It was that XRP would become the settlement layer of global finance. That specific claim now has a specific answer, delivered by the specific institution the claim was about, using the specific banks the claim named.

What would have to be true for the bulls

Fairness demands stating the conditions under which the bear reading here is wrong, because they exist and they are not absurd.

Tokenized deposits only work between banks that hold each other’s currencies in size. The model is excellent for dollar-euro-sterling-yen, which is most of the volume and nearly all of the profit. It is useless for a Nigerian bank settling with a Philippine bank, where no deposit market exists in either direction and someone must still bridge. If tokenized deposit networks handle the deep corridors and a public bridge asset handles the long tail, XRP has a real business. It is a smaller business than the pitch, and it competes with stablecoins that carry no price risk, but it is real.

The second condition is agentic settlement. Swift has said it wants to be the platform for programmable money and machine-to-machine payments. Those flows are high-frequency, low-value, and permissionless by nature, which is the environment where a neutral public asset with a native ledger has genuine structural advantages over an interbank consortium. Ripple has been building directly at this, and if the agentic economy materializes at scale, the question reopens on different terms.

The third is time. Seventeen banks in pilot is not global adoption. Consortium infrastructure has failed before, repeatedly, and Swift’s ledger could stall in exactly the way that bank blockchain consortia have stalled since 2016. A pilot that quietly does not scale would leave the field open again. R3, Corda, Utility Settlement Coin, and a decade of bank consortia are a real precedent for exactly that failure mode, and Ripple has outlived most of them.

None of those conditions rescue the original claim. They describe a smaller, more plausible XRP: a liquidity instrument for corridors nobody else wants, and a settlement rail for machines. Which is a decent business, and is not what anyone bought.

The answer nobody wanted to hear

Fifteen years of argument reduced to a design document. Swift built the blockchain. It went live with the exact banks the thesis named. And it moves tokenized deposits, because banks would rather settle in money they issue themselves than in an asset whose price can move against them between the send and the receive.

The XRP community will spend this week debating a resurfaced slide and a former executive’s two-word post, and both of those things are more interesting than the ledger, and neither of them matters. The slide is undated. The executive is gone. The ledger is live.

What is left is the smaller question, the one that has quietly been the only real one for two years: not whether Ripple wins, because Ripple is winning, but whether anything Ripple wins reaches the token. On July 9 the largest institution in cross-border payments answered that question in the most expensive way available, by building the future and leaving XRP out of the blueprint.The thesis is not dead. It is just no longer a thesis about Swift.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Swift has not published a technical disclosure of the ledger’s full stack; the Hyperledger Besu and Chainlink CCIP details derive from secondary reporting. The Swift-branded slide discussed here is undated and was resurfaced by a third party, not released by Swift, and no party has confirmed its provenance or current status. Tom Zschach’s comments are his personal view and not Swift policy; he left the organization earlier in 2026. ETF flow, open interest, and long-to-short figures derive from SoSoValue and CoinGlass. Details reflect information current as of July 14, 2026, and are subject to change. Always do your own research.

Pi Network price has surged more than 13% to an intraday high of $0.083 after the Core Team confirmed a Protocol v25 upgrade for July 22, lifting retail sentiment around the battered token.

Summary

- Pi Network price surged over 13% after the Core Team scheduled its Protocol v25 upgrade.

- Rising open interest and a possible triple bottom supported PI’s rebound from record lows.

- Negative money flow and daily token unlocks could limit gains above $0.083.

According to data from crypto.news, Pi Network (PI) price traded near $0.082 at press time after rebounding from its July 14 record low around $0.071. The advance stood out as Ethereum, Solana, and other high-beta cryptocurrencies fell alongside a global technology-stock rout.

Protocol v25 and leveraged demand have fueled the rebound

Pi Network’s Core Team confirmed that Protocol v25 will improve network stability and add tools for more efficient, privacy-preserving smart contracts. The team also introduced a redesigned Mining App menu intended to simplify access to ecosystem features and applications. Pi Network’s announcement gave traders a dated catalyst after PI lost about 27% over the previous week.

Derivatives traders quickly increased their exposure. PI futures open interest rose to $10.73 million from $10.44 million a day earlier. Rising leverage, combined with thin order books, likely helped accelerate the move as bearish positions faced pressure above $0.080.

Meanwhile, Pi Network’s retail-heavy market structure helped the token move independently of large-cap altcoins. Global technology shares fell on July 17 as investors reduced leveraged exposure to semiconductor and AI stocks, while renewed Middle East tensions pushed oil prices higher.

U.S. initial jobless claims also dropped to 208,000 from 216,000, another sign of resilience in the labor market. Firm economic data can reduce the case for Federal Reserve rate cuts, a development that usually hurts speculative assets. PI’s network-specific catalyst outweighed that pressure during Friday’s session.

On the lower-time-frame chart, PI has formed three troughs around $0.073–$0.075, creating a possible triple bottom. The pattern requires a decisive close above its neckline near $0.082–$0.083. A confirmed breakout could open a move toward $0.086, where the chart shows the next short-term target.

According to trader Crypto With Gopal, buyers have repeatedly defended the same support zone.

“Support has held multiple times—now all eyes are on the breakout. Market sentiment is turning increasingly bullish.”

The daily chart presents a tougher test. PI remains inside a descending channel that has controlled price action since late April, while the Supertrend stays bearish at $0.101. A rebound toward that level would still leave the token beneath the channel’s upper boundary, now located around $0.108.

Weak money flow and token unlocks threaten the recovery

Chaikin Money Flow remains negative at approximately -0.15, which shows that capital outflows still exceed inflows despite Friday’s bounce. PI must push the indicator above zero and reclaim $0.101 before the daily chart supports a durable trend reversal.

Supply also remains a structural risk. PiScan data showed roughly 127.5 million PI scheduled to unlock over a 30-day period, equal to an average of about 4.25 million tokens per day. Continued releases could limit gains unless network activity creates enough demand to absorb the new supply.

A rejection from $0.083 would weaken the triple-bottom setup and return attention to $0.074. A daily close below that support would invalidate the recovery thesis and expose the record-low region near $0.071, with the descending channel allowing further losses toward $0.065.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

“The real prize is the yen side of onchain settlement, one of the most strategic positions in Asian finance over the coming decade, and that is exactly what SBI is building toward,” he added.

One technical limitation remains. JPYSC does not yet support withdrawals to external wallets.

“Regarding JPYSC, its use is currently limited to accounts within SBI VC Trade, and it does not yet support withdrawals to external wallets or remittances and settlements via public blockchains,” the spokesperson said.

For now, that limits JPYSC’s use outside SBI’s own platform. Investors cannot yet move the stablecoin to external wallets or use it to settle transactions across public blockchains.

Sota Watanabe, CEO of Startale Group, which works with SBI Holdings on JPYSC, said the company’s continued investment in digital assets reflects what he sees as growing institutional confidence in blockchain infrastructure.

“SBI Holdings’ continued commitment to digital assets likely signals confidence in the future architecture of global finance,” Watanabe told CoinDesk.

He said blockchain is increasingly being viewed as financial infrastructure rather than an emerging technology, adding that Japan is well-positioned to lead the sector due to its regulatory framework and financial institutions.

SBI expansion

SBI agreed to buy Tokyo-based cryptocurrency exchange Bitbank for around $289 million in June. The acquisition is expected to close in October, subject to regulatory approval. SBI previously acquired crypto exchange Bitpoint in 2022. The firm also led a $76 million Series C funding round for institutional exchange EDX Markets and a $25 million Series C round for crypto risk manager Gauntlet, the spokesperson said.

Crypto World

ether.fi Partners with Nexus Mutual to Protect Against ETH Slashing at Institutional Scale

[PRESS RELEASE – London, United Kingdom, July 17th, 2026]

ether.fi, the leading onchain neobank for digital asset management, has selected Nexus Mutual to provide crypto’s largest-ever ETH Slashing Cover. The cover protects ether.fi‘s validators against up to 15,000 ETH worth of slashing penalties.

As ether.fi continues to see rapid adoption from both retail and institutional audiences, securing industry-leading protection against slashing risk for ether.fi users is critical. Over the last year, ether.fi has been systematically strengthening their stack across infrastructure, risk management, operational security and real-time defense systems.

Since ether.fi operates one of the largest validator sets on Ethereum, slashing is a real tail risk for them. By working with Nexus Mutual, ether.fi has mitigated this with protection that kicks in to secure against validator losses. This cover was calculated to protect ether.fi in even the most extreme scenarios and represents more than all historical losses from ETH slashing combined.

“We’ve always believed the safest protocols will ultimately win. That’s why we’ve invested heavily in audits, operational security, staking architecture, and now the largest insurance program in the industry. We are excited to partner with Nexus Mutual to make this a reality,” said Mike Silagadze, Founder & CEO of ether.fi.

“We’ve known the ether.fi team since before it was ether.fi, and they’ve been focused on risk from day one. Covering their users for up to 15,000 ETH in slashing penalties is a historic step, and we’re proud they chose Nexus Mutual to take it with them,” said Hugh Karp, Founder of Nexus Mutual.

About ether.fi

ether.fi is the leading onchain neobank for digital asset management. With $6B+ in AUM across Cash (crypto card), Stake (restaking), and Liquid (liquid restaking derivatives), ether.fi has established category dominance in crypto neobanking. It’s the rare institutional-grade product built for consumer adoption.

About Nexus Mutual

Nexus Mutual is the first crypto insurance alternative. Since 2019, they have covered more than $7 billion against smart contract hacks, slashing, and other digital asset risks. As the industry leader, they have become a trusted partner for everyone from individuals to institutions to help manage onchain risk.

The post ether.fi Partners with Nexus Mutual to Protect Against ETH Slashing at Institutional Scale appeared first on CryptoPotato.

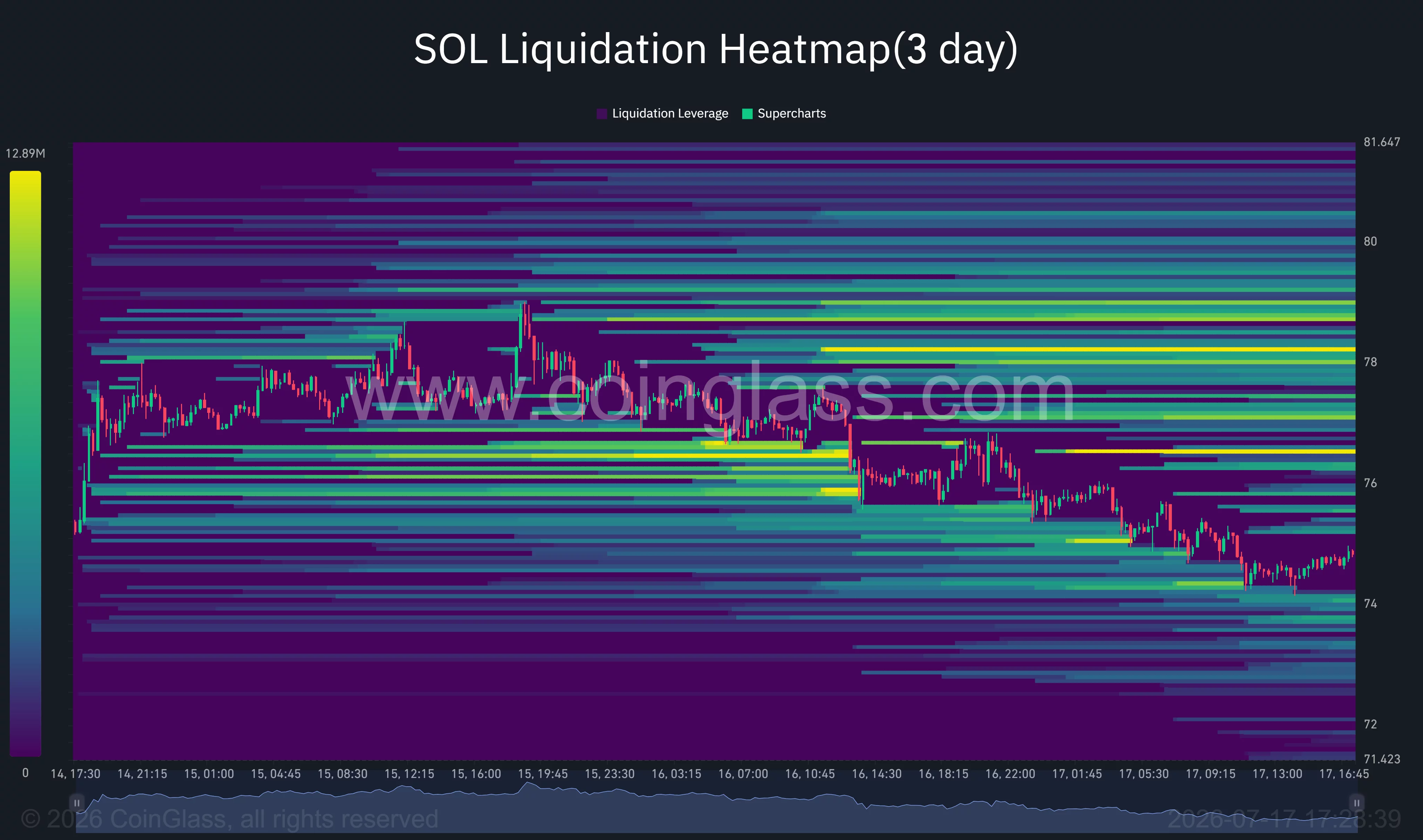

Solana price has fallen nearly 4% to about $74 after a rejection near $77, as a global technology sell-off and leveraged long liquidations have pushed traders toward caution.

Summary

- Solana price tests $74 support after losing its rising trendline and facing weak four-hour momentum.

- A recovery above $76.50 could trigger short liquidations and drive SOL toward $78–$80.

- Losing $74 would expose the daily Supertrend support at $69.60 and deepen downside risks.

According to data from crypto.news, Solana (SOL) price extended its decline on July 17 after failing to hold above the $76.50–$77 resistance area. Selling accelerated as semiconductor shares led losses across global markets, with Nasdaq 100 futures down 1.8%, Japan’s Nikkei 225 off 4%, and Taiwan’s benchmark plunging more than 6%.

The drop can partly be attributed to the rout due to doubts over stretched artificial intelligence valuations and leveraged retail positions.

Strong U.S. data added pressure on speculative assets. Initial unemployment claims fell to 208,000 from 216,000, while June retail sales rose 0.2%. The 10-year Treasury yield climbed toward 4.60%, and the dollar strengthened, raising the cost of holding high-beta assets such as Solana.

Institutional demand has provided only limited relief. U.S. spot Solana exchange-traded funds attracted $8.36 million on July 6, their strongest daily intake in almost two months, per data from SoSoValue. However, the inflow was not enough to prevent SOL from retreating from its early-July high near $83.

Solana price can rebound if bulls reclaim $76.50

On the 4-hour chart, SOL trades near $74.87 and has reached the lower Bollinger Band at $74.33. The middle band at $76.51 now serves as immediate resistance, while the upper band sits at $78.69. A 4-hour close above the midpoint would give buyers another chance to test the $78–$80 region.

Momentum remains weak but is approaching levels where relief rallies can develop. The 4-hour relative strength index has dropped to 36.58, below its signal average of 45.48 but still above the oversold threshold of 30. Price has also formed a sequence of lower highs since its July 4 peak near $83.

According to crypto analyst SatoshiOwl, SOL has reached a support area after breaking beneath an ascending trendline.

“Hold here and we could see a relief bounce back toward $78–$80. Lose it, and a deeper flush becomes much more likely.”

Ali Charts offered a longer-term counterpoint, noting that the TD Sequential indicator has produced a buy setup on Solana’s monthly chart. The analyst described it as a potential early warning of a macro trend change, although the monthly setup requires confirmation from shorter time frames.

The daily chart remains constructive above the Supertrend support at $69.62. Chaikin Money Flow stands at 0.03, which shows that capital flow is still marginally positive despite the latest sell-off. SOL must first recover the former horizontal support at $76.64 before the daily structure can improve.

CoinGlass’ three-day liquidation heatmap places the nearest large pools of leveraged positions above the market. Dense clusters sit near $76.50–$76.70, $78, and $78.70, making those levels possible price magnets if SOL rebounds. A move through $76.70 could liquidate short positions and accelerate a recovery toward $78.

A break below $74 would expose the $69.60 support zone

Downside risk will rise if SOL closes decisively below the $74–$74.30 area. The heatmap shows less concentrated liquidity immediately beneath the current price, leaving room for a quicker decline toward $72 before the daily Supertrend level near $69.62 comes into play.

A loss of $69.62 would invalidate the remaining bullish daily setup and expose the June recovery base between $64 and $66. Macroeconomic pressure could deepen that move if Treasury yields continue higher, technology shares extend their decline, or renewed U.S.-Iran tensions lift oil prices and reduce demand for risk assets.

For now, SOL remains caught between weak four-hour momentum and positive daily capital flow. Bulls need $76.50 back to target the liquidity stacked near $78–$80, while a failure to protect $74 would place the $69.60 trend support at risk.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

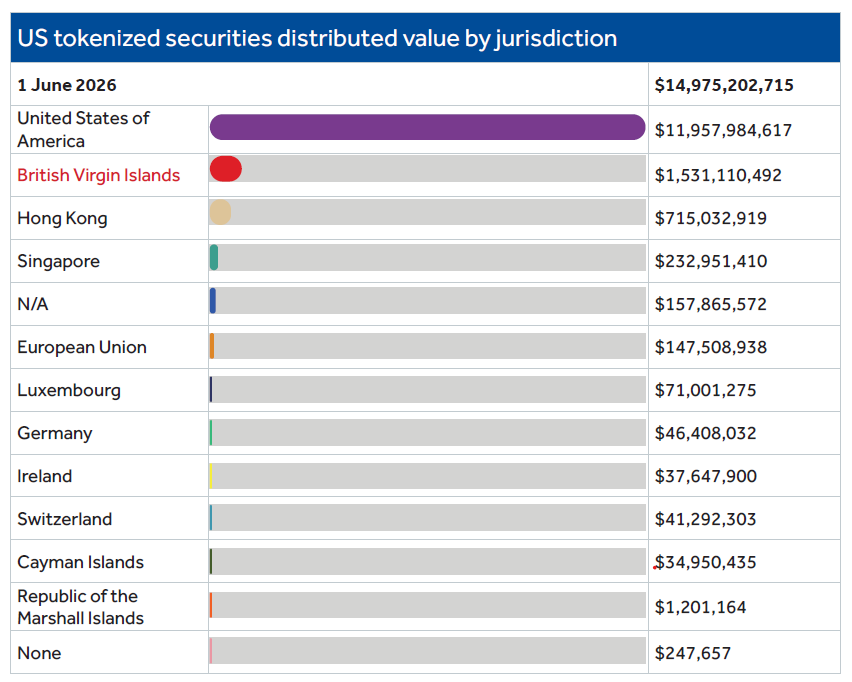

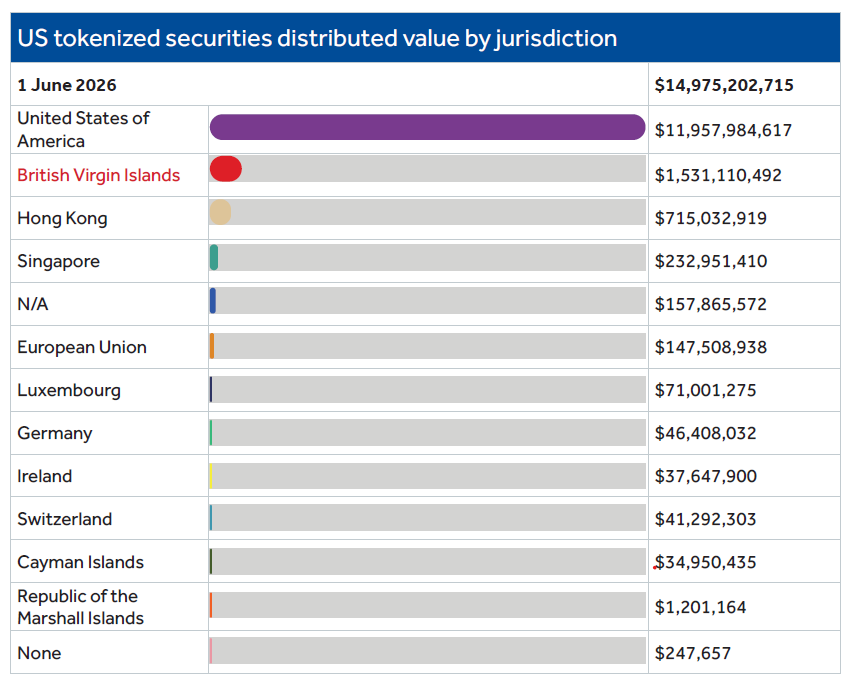

More than $1 out of every $10 of the world’s tokenized US Treasuries is issued by a company incorporated in the British Virgin Islands.

That places the small Caribbean territory behind only the United States as a key jurisdiction for the rapidly growing asset class, according to BVI Finance.

BVI Finance’s Destination Digital report in June found that BVI entities accounted for approximately $1.5 billion of the $14.98 billion global market for tokenized US Treasuries as of June 1.

A growing list of digital asset firms now call the British Virgin Islands home, including Kraken’s parent company, Payward, Bitstamp (recently acquired by Robinhood), 1inch and Bitfinex.

The territory boasts a stablecoin market cap of about $1.2 billion held in BVI-linked addresses and has roughly 28,000 stablecoin asset holders.

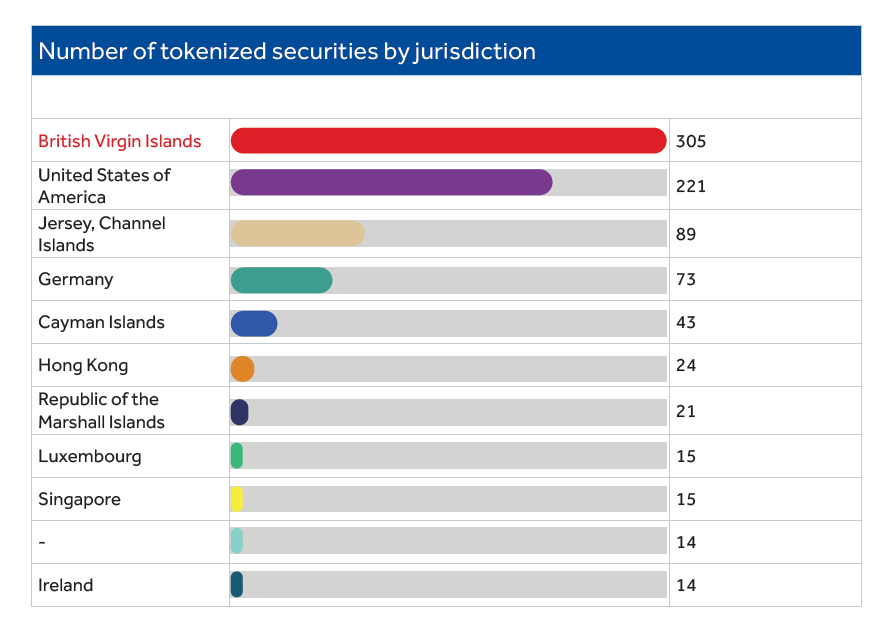

More than 25 virtual asset service providers (VASPs) have been approved under the BVI’s VASP regime, and, according to Bernstein Research, the Islands host 305 tokenized securities — the highest count for any single jurisdiction in the RWA.xyz dataset.

US tokenized securities distributed value by jurisdiction. Source: Destination Digital

The statistics suggest the Virgin Islands has become one of the world’s top crypto hotspots, but the reality is a little more nuanced.

Tokenized assets are designed to be borderless, and crypto projects often have the choice of which offshore jurisdiction to incorporate in.

In most cases, digital asset companies aren’t physically relocating to the Virgin Islands; they’re simply using the territory to incorporate legal entities, such as token issuers, treasury vehicles, holding companies or special purpose vehicles (SPVs).

Crypto companies aren’t just choosing BVI for tax reasons

Andrew Jowett, a partner at Appleby (BVI) Ltd who advises digital asset businesses on corporate structuring, told Cointelegraph that clients researching the BVI typically compare several jurisdictions, such as the Cayman Islands, United Arab Emirates, Singapore and Switzerland.

Despite long-held assumptions about offshore Caribbean tax havens, tax neutrality is no longer the primary driver.

Related: Dubai crypto market hits 50 licensed firms after new VARA approval

“The overriding factor for choosing the BVI has been digital asset regulation and not tax,” Jowett said. The British overseas territory does have attractive tax policies, and imposes no corporate income tax or capital gains tax on BVI companies.

But all the leading crypto hubs now have favorable crypto tax policies, meaning it’s no longer the deciding factor.

The Cayman Islands imposes no corporate income tax or capital gains tax, and the UAE has zero personal income tax or federal corporate tax on qualifying free zone entities.

“Tax neutrality is table stakes,” said Saeed Al-Marri, chief executive of digital asset infrastructure firm Ethra, which is incorporated in the BVI. He added that the BVI provides legal certainty and clarity, factors he said will determine which jurisdictions survive institutional adoption.

LTP is an institutional digital asset infrastructure provider that operates regulated entities in the BVI, Hong Kong, Australia and the UAE. Its founder and chief executive, Jack Yang, told Cointelegraph that while favorable taxation is relevant for cross-border structures, it is secondary to legal and regulatory certainty as tokenization moves further into institutional finance.

“A tax-neutral structure that cannot pass review by banks, custodians, auditors, investment committees, or regulators has limited practical value,” he said.

Number of tokenized securities by jurisdiction. Source: Destination Digital

Orest Gavryliak, chief legal officer at decentralized exchange aggregator 1inch, which is incorporated in the BVI, said that more and more decentralized finance (DeFi) protocols are choosing jurisdictions that provide predictable rules, rather than simply the lowest tax burden.

“Jurisdiction isn’t exactly becoming irrelevant, but its role is changing,” Gavryliak told Cointelegraph. “Protocols are increasingly weighing factors such as regulations, institutional credibility and long-term sustainability.”

Crypto hubs now compete on legal infrastructure

Jurisdictions vying to be “crypto hubs” like Singapore and the UAE increasingly compete via favorable legal infrastructure and licensing regimes, such as Singapore’s Payment Services Act and Dubai’s Virtual Assets Regulatory Authority (VARA) rulebooks.

The BVI introduced the Virtual Assets Service Providers Act (VASP Act) in 2023, overseen by the BVI Financial Services Commission (FSC).

Compared with many larger financial centers, it offers a speedy turnaround, responds to VASP applications within six weeks and aims to complete the review process within six months, according to BVI Finance and FSC guidance.

Jowett said beyond favorable tax regimes, clients prioritize “ease of launch” and efficient corporate structuring, which has long been part of the BVI’s appeal. Companies can be set up quickly, the legal framework is flexible, and ongoing reporting is generally lighter than in onshore jurisdictions.

Related: Cayman Islands Web3 foundations jump 70% as CARF reporting rules arrive

The Virgin Islands has also historically been favored because it offers more corporate confidentiality than many larger financial centers.

While BVI companies are still subject to anti-money laundering (AML) and know-your-customer (KYC) requirements, beneficial ownership information is held by registered agents rather than a public register, which reduces disclosure requirements.

British Virgin Islands. Source: Destination Digital

However, none of the companies interviewed by Cointelegraph cited tax neutrality or greater corporate confidentiality as deciding factors for incorporating in the BVI, pointing instead to legal certainty, regulatory clarity and corporate flexibility.

Incorporating, not physically relocating to the Virgin Islands

Yang told Cointelegraph that LTP does not employ full-time staff “on the ground.” Instead, the entity is overseen by its board and supported by staff from elsewhere in the LTP group.

The same distinction can be seen elsewhere in the industry. Kraken’s parent company, Payward, is incorporated in the BVI, but the exchange’s operations are primarily based in the United States, while 1inch’s team and operations are spread across multiple jurisdictions.

The BVI isn’t winning the race to attract glitzy headquarters or large-scale engineering teams. Instead, it has become the legal home for many digital asset businesses, while much of the work happens elsewhere. For jurisdictions competing to attract the industry, that just may be enough.

Magazine: Singapore isn’t a ‘crypto hub’ — it’s something better: StraitsX CEO

Japanese financial services group SBI Holdings has acquired a majority stake in Holdbuild, the parent company of Singaporean crypto platform Coinhako, after receiving regulatory approval from Singapore’s central bank.

The approval from the Monetary Authority of Singapore (MAS) enabled SBI to acquire company shares from existing shareholders through a capital injection, making Coinhako a consolidated subsidiary of SBI, the company announced on Thursday.

Coinhako holds a Major Payment Institution license under MAS through its subsidiary, Hako Technology Pte. Ltd. SBI announced its intent to acquire a majority stake in the Singaporean crypto exchange in February.

SBI said it plans to combine Coinhako’s customer base and regional network with its own financial services and digital asset businesses, including its JPYSC stablecoin initiative.

Related: Coinbase Ventures tops crypto VC list for H1 2026

Financial terms of the transaction were not disclosed. SBI did not immediately respond to Cointelegraph’s request for details on the deal.

The acquisition is part of SBI’s broader expansion in digital assets. Earlier this month, the company led a $76 million Series C funding round for institutional crypto exchange EDX Markets. It also shared plans to acquire Bitbank for $289 million, aiming to create one of Japan’s largest crypto exchanges.

SBI deepens crypto industry involvement in Asia

SBI described Singapore as a key hub in its digital asset strategy and said the acquisition would strengthen its presence in Southeast Asia. SBI said it plans to hold its first overseas branch managers’ meeting in Singapore this summer to strengthen its local business foundation.

SBI has accelerated its digital asset expansion in recent months through acquisitions, investments and tokenization initiatives. This week, the company partnered with Ondo Finance to bring tokenized Japanese stocks and integrate its JPYSC stablecoin for settlement and collateral.

In February, SBI and Startale Group unveiled Strium, a layer-1 blockchain focused on tokenized securities and real-world assets. The network is designed to support 24/7 trading, tokenized equity settlement and institutional financial applications as SBI expands its digital asset infrastructure across Japan and overseas markets.

Magazine: Dubai tops Asian crypto hubs, Taiwan passes crypto laws: Asia Express

XRP remains under pressure across both its USDT and BTC trading pairs, with the broader market structure still favoring sellers. While the token has managed to stabilize above nearby support on the dollar chart, its Bitcoin pair continues to print lower highs and lower lows, highlighting persistent relative weakness.

Ripple Price Analysis: The USDT Pair

The daily chart shows XRP trading around $1.08 after an extended decline within a well-defined descending channel. Although the asset has recently moved sideways instead of extending its losses, the broader trend remains bearish as it continues to trade below both the 100-day and 200-day moving averages. These levels are also sloping downward, reinforcing the prevailing negative momentum.

Following the sharp breakdown in June, XRP has established a consolidation range between the $1 support zone and the $1.25 resistance area. Buyers have repeatedly defended the lower boundary, but every recovery attempt has been rejected before reclaiming the declining 100-day moving average or breaking above the channel’s higher boundary, indicating that bullish momentum remains limited.

A breakout above the $1.25 resistance would be the first sign that buyers are regaining control and could expose the descending channel’s upper boundary as the next major hurdle. Until then, the broader structure continues to favor further downside, with a loss of the $1 support opening the door toward significantly lower demand zones.

The RSI is hovering near the neutral 50 level, reflecting the current balance between buyers and sellers after weeks of heavy selling pressure. However, without a decisive bullish breakout, the indicator does not yet suggest a meaningful shift in trend.

The BTC Pair

The XRP/BTC daily chart paints an even weaker picture. The pair has remained inside a long-term descending channel for nearly a year while consistently trading beneath both the 100-day and 200-day moving averages, highlighting sustained underperformance against Bitcoin.

After several failed recovery attempts during May and June, XRP/BTC has finally dropped below the key horizontal support around 1,720 sats. This level has repeatedly attracted buyers over the past few months, but each rebound has produced another lower high, signaling that selling pressure continues to dominate.

On the upside, the next important resistance sits around the 1,850 sats region, where previous support has turned into resistance. A move above this area would improve the short-term outlook, but the descending channel and the 200-day moving average near 2,000 sats remain the primary barriers to a broader trend reversal.

Meanwhile, the RSI remains below the midpoint, suggesting that momentum still favors the sellers. Unless XRP/BTC can reclaim key resistance levels and break its long-term bearish structure, the pair appears vulnerable to another test of the channel’s lower boundary, which is now located around 1,500 sats.

The post Ripple Price Analysis: Weakening XRP Momentum Raises Risk of a Sub-$1 Drop appeared first on CryptoPotato.

ECB’s Piero Cipollone said stablecoin adoption could erode bank deposits, but the digital euro will keep banks at the center of payments.

The part that rattles valuations is the license. K3 is open-weight, with the full model due for public release on July 27. Anyone will be able to download it, run it on their own hardware, and pay nobody.

Anthropic released Fable 5 last month, and OpenAI shipped GPT-5.6 a week ago, both closed and metered. The assumption underwriting hundreds of billions of dollars in AI infrastructure spending is that frontier capability stays scarce, expensive and American.

A free Chinese model at the top of a coding leaderboard is a direct argument against that.

Meanwhile, Moonshot’s domestic rivals took it worst, with Z.ai falling about 27% and MiniMax about 16%.

For crypto, the headwinds run through the tape rather than through anything onchain. Bitcoin has spent this entire week taking direction from semiconductors.

Last Friday, it rose 4% on the day South Korea’s Kospi jumped 8% and SK Hynix priced $26.5 billion of American depositary shares. This Friday, it fell because a model release in Beijing made the same trade look expensive.

There is, however, a more concrete exposure underneath.

Bitcoin miners have spent two years repositioning themselves as AI data center landlords, signing long-term leases with model developers on the assumption that demand for training and inference compute keeps rising.

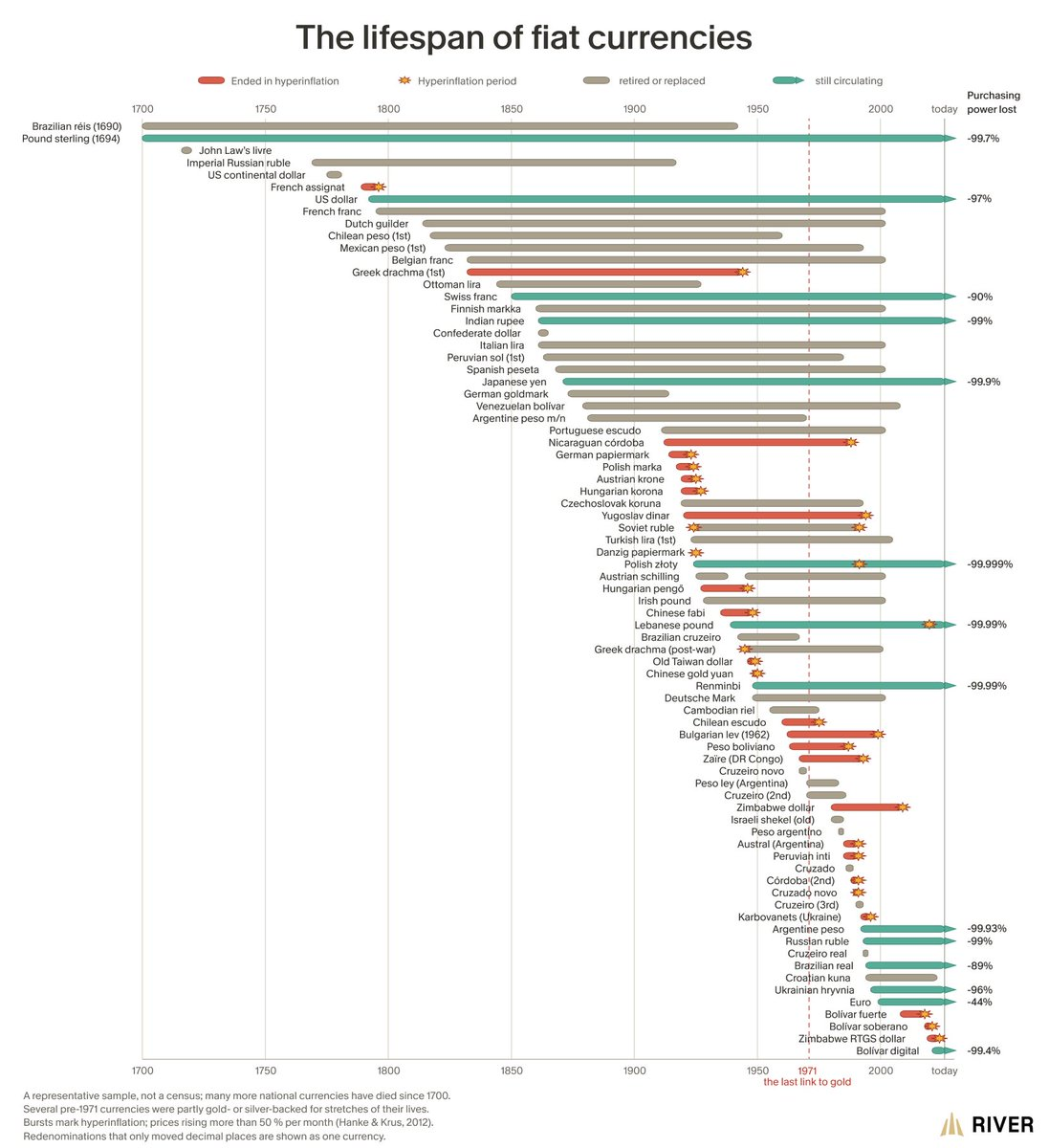

Michael Saylor is making the case for Bitcoin (BTC) with a history lesson. The MicroStrategy chairman shared River research tracking over 60 government currencies since 1700. His point is simple. Paper money keeps failing, and Bitcoin was built to fix that.

River, a Bitcoin financial services firm, published the chart this week. It claims the average fiat currency lasts just 27 years.

326 Years of Fiat History Behind Saylor’s Bitcoin Pitch

The chart tells a grim story. Dozens of currencies died in hyperinflation, defined by economists Steve Hanke and Nicholas Krus as prices rising by more than 50% in a month.

Germany’s papiermark (or Paper Mark) went that way in 1923. Hungary’s pengő followed in 1946, when prices doubled roughly every 15 hours. Zimbabwe’s dollar collapsed in 2008.

The survivors did not do much better. The US dollar has lost 97% of its buying power. The British pound is down 99.7%, and the Japanese yen 99.9%. Even the euro, the youngest and best performer, has lost 44% since 1999.

River is upfront about the chart’s limits. It calls the data a representative sample, not a census, and notes many pre-1971 currencies had partial gold backing. That year gets its own dashed line, marking when the dollar cut its final tie to gold.

“Fiat currency is the problem. Companies, institutions, securities, and technologies that strengthen Bitcoin are part of the solution. We can debate ideas without mistaking allies for enemies,” Saylor commented.

Follow us on X to get the latest news as it happens

Notably, Michael Saylor’s next-decade Bitcoin outlook calls the pioneer crypto a digital property whose strength lies in its base layer barely changing. He sees Bitcoin as scarce global capital for final settlement, not mainly for everyday payments.

His bigger bet is that Bitcoin will support a new financial system built on digital capital, credit, and money.

River Says Most Cryptocurrencies Fail the Same Test

River’s warning is not just about fiat. The firm says the average cryptocurrency does not even last a year. Nearly all of them fall to zero when priced in Bitcoin.

“All of these currencies suffer from the same problem: Centralized power and an infinite money supply. Bitcoin was designed to outlast all fiat currency,” the firm said in its post.

Meanwhile, not everyone agrees that Bitcoin’s design is settled. StarkWare CEO Eli Ben-Sasson recently challenged Bitcoin’s fixed cap, arguing lost keys will shrink the usable supply forever.

Chainalysis estimated that up to 3.79 million BTC were already unrecoverable by 2017. Supporters rejected his 4% issuance fix, since 95.5% of all Bitcoin now exists.

The market adds a twist to Saylor’s pitch. Bitcoin trades near $63,252, down about 47% in a year.

MicroStrategy still holds 843,775 BTC, the largest corporate stash, even after selling 3,588 BTC this month, its biggest sale since 2022.

History says fiat money fades. The coming months will test whether investors still believe Bitcoin is the escape.

The post MicroStrategy’s Saylor Pitches Bitcoin Bull Case With 300 Years of Fiat History appeared first on BeInCrypto.

XRP FED CHAIR LIVE NOW!!! CRYPTO PUMPS

First Reform UK police commissioner elected

Ready Capital Corporation (RC) Shareholder/Analyst Call Prepared Remarks Transcript

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat23 hours ago

NewsBeat23 hours agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Crypto World2 days ago

Crypto World2 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business1 day ago

Business1 day agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics2 days ago

Politics2 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Entertainment2 days ago

Entertainment2 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos3 days ago

News Videos3 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech3 days ago

Tech3 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Crypto World17 hours ago

Crypto World17 hours agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech3 days ago

Tech3 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Business1 day ago

Business1 day agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Sports2 days ago

Sports2 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos7 hours ago

News Videos7 hours agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

NewsBeat2 hours ago

NewsBeat2 hours agoRegistration is now open for March for Men with Kev 2026

-

Business13 hours ago

Business13 hours agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Tech4 days ago

Tech4 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

News Videos4 days ago

News Videos4 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Entertainment2 days ago

Entertainment2 days agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World3 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Crypto World16 hours ago

Crypto World16 hours agoClaude Fable 5 Slips to Second in AI Coding Leaderboard

You must be logged in to post a comment Login