Crypto World

The Best Trade of the Week Wasn’t Crypto or Gold, It Was Your Morning Coffee

One of the best trades of the week, was not Bitcoin or gold. It was sitting in your kitchen.The arabica coffee price jumped 16.19% on Monday, its biggest single-day gain this century, closing at a 5.5-month high. Robusta contracts climbed 8.83% to a five-month peak in the same session.

The move lifted coffee futures roughly 43% above their early June low near 239 cents per pound. Harvest delays in Brazil, shrinking exchange stocks, and El Nino risks fueled the rally.

Neither the crypto majors nor gold’s record run came anywhere near that one-day move.

Why the Coffee Price Is Surging After Brazil Harvest Delays

According to Barchart, September arabica gained 48.75 cents on Monday, its largest one-day advance since at least 2000. The spark came from Brazil, the world’s biggest coffee producer.

Consultancy Safras & Mercado reported that Brazil’s 2026/27 harvest was 52% complete as of July 1. That lags last year’s 60% and the five-year average of 55%.

Weather adds pressure. Somar Meteorologia recorded no rain in Minas Gerais, Brazil’s top arabica region, in the week through July 5. Meanwhile, forecaster Rural Clima warned that rains expected in mid-July could prove “detrimental” to crops.

Inventories point the same way. ICE arabica stocks fell to a 2.25-year low of 366,756 bags on Monday. In addition, a stronger Brazilian real discourages exports, and farmers are reportedly withholding beans.

El Nino threatens next season too. NOAA sees a 67% probability of a record “Super El Nino,” which could disrupt the September and October flowering that shapes Brazil’s 2026/27 crop.

The bearish case has not vanished, however. The USDA still projects a record 71.9 million-bag Brazilian crop, and Rabobank recently raised its arabica surplus estimate to 9.5 million bags. Those figures pushed arabica to a 19-month low just four weeks ago.

The reversal since then suggests the market abandoned that surplus story. Coffee also joined a broader commodity bid, with gold holding above $4,000 per ounce this month.

Coffee Futures Break Out of a Descending Channel on the Weekly Chart

The weekly chart shows a clean breakout from the descending parallel channel that guided prices lower from the October 2025 top. Price escaped the pattern in late June and now trades near 343 cents.

The rally has already pierced the 0.5 Fibonacci retracement at 339.5 cents. That level derives from the move between the June low at 238.7 and the October 2025 high at 440.26.

The next barrier stands at the 0.618 retracement of 363.26 cents. It overlaps a supply zone between 363 and 375 that rejected prices repeatedly in 2025. Therefore, this area remains the most important long-term resistance.

Rising weekly volume accompanied the breakout, which suggests genuine buying pressure rather than a thin short squeeze. If bulls stall, the reclaimed zone between 308 and 318 cents should provide first support.

Daily Chart and RSI Breakout Put 370 Cents in Sight

The daily chart confirms the momentum. Price broke above the March 24 swing high at 318.8 cents, a level that coincides with the 0.382 Fibonacci retracement. The year’s largest volume bars accompanied the move.

The next target sits at 370.65 cents, the swing high from late January. It rests just above the 0.618 retracement, creating a tight resistance cluster between 363 and 370. On Tuesday, the contract cooled 2.4% to around 341 cents, still holding the 0.5 level.

Momentum indicators tell a similar story. The daily RSI broke above a descending resistance line that capped it from February 2025, with rejections in August and September 2025 validating that trendline. The indicator now reads near 75.

Such a reading signals strong bullish conviction but also overbought conditions. Historically, similar levels preceded short-term cooling phases, in line with Tuesday’s pullback. Recent positioning data already showed capital rotating into hard assets before the breakout.

The structure stays bullish while the coffee price holds above 315 to 319 cents on a closing basis. A daily close back below that zone would mark the record rally as a squeeze, while a break through 363 to 370 would open the road to 397 and the psychological 400 cents.

For investors comparing commodities into year-end, coffee just forced its way onto the list.

The post The Best Trade of the Week Wasn’t Crypto or Gold, It Was Your Morning Coffee appeared first on BeInCrypto.

Decentralized finance (DeFi) analytics platform Zapper announced it will shut down next month, becoming the latest crypto platform to fold amid a market downturn.

In a post to X on Wednesday, Zapper CEO Seb Audet said Zapper’s website, mobile app and API services would shut down on Aug. 3, marking the end of a seven-year run after receiving backing from the likes of billionaire investor Mark Cuban in 2021.

“We evaluated a number of different options, pursued some to the fullest extent possible, and came to the realization that an orderly wind down is the best course of action,” Audet said.

While Zapper didn’t share the reasons behind its decision to shut down, Audet hinted in a response that the shutdown was due to falling demand, stating: “At the end of the day, the market decides.”

Cointelegraph reached out for comment but didn’t receive an immediate response.

Source: Zapper

Zapper adds to a growing list of crypto platforms that have shut as crypto market sentiment has sunk to near all-time lows and venture capital funding has become harder to secure.

Cardano-based analytics platform TapTools made a similar decision to shut down in June, as did Bitcoin-focused DeFi platform Botanix a week later, citing weak demand for Bitcoin DeFi.

SBI’s crypto unit, decentralized email service Dmail, and nonfungible token marketplaces like Nifty Gateway and Rodeo have also sunset operations this year amid a broader fall in NFT activity.

Related: Yield Guild Games cuts 35 staff, shuts game publisher to focus on AI

Zapper was founded in 2019 and put itself on the map by winning one of Kyber’s DeFi Hackathon events later that year, which helped it raise a $1.5 million seed round.

It also raised $15 million in a Series A funding round in May 2021, led by Framework Ventures, with Cuban, Coinbase Ventures and the Ashton Kutcher-founded Sound Ventures also contributing.

Crypto traders use platforms like Zapper to track token prices, follow DeFi trends and discover new protocols. Zapper also allowed traders to connect their wallets to monitor positions, manage liquidity pools and yield farms and learn about upcoming airdrops.

Audet said the Zapper team scaled its product to over 2 million monthly active users and oversaw more than $13 billion in processed transactions at its peak.

However, Zapper has experienced major setbacks throughout its journey, including in April 2025, when it suffered a social engineering attack. The breach allowed attackers to temporarily hijack the platform’s domain and redirect unsuspecting users to a malicious page embedded with phishing traps.

Securing VC funding has become a challenge

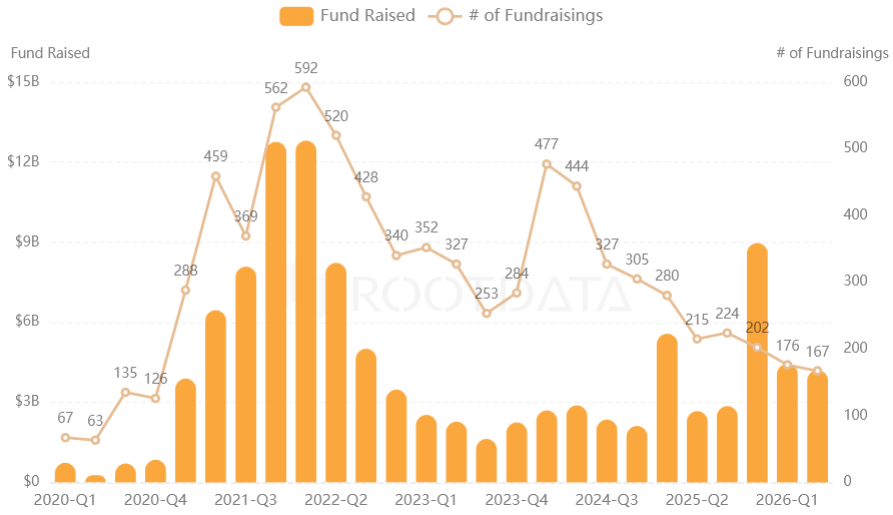

While crypto VC funding increased 57.6% year-on-year to $4.21 billion in the second quarter, the spread of capital has become far more concentrated, with the overall deal count having now fallen nine times over the last 10 quarters, according to RootData’s VC dashboard.

Quarterly change in crypto VC funding and deal count since Q1 2020. Source: RootData

Features: From Bitcoin critics to blockchain believers: The 5 biggest crypto backflips

OpenAI has secured U.S. government clearance for its GPT-5.6 model, removing a key regulatory hurdle as traders turn their attention to the company’s pre-IPO perpetual futures market.

Summary

- OpenAI has received U.S. approval to launch GPT-5.6, clearing a major regulatory hurdle ahead of its wider rollout.

- Traders are closely watching OPENAI-PERP contracts as the GPT-5.6 approval fuels pre-IPO valuation expectations.

- SoftBank’s latest investment and OpenAI’s Jalapeño AI chip add to investor focus ahead of any future IPO.

Axios first reported that the U.S. Department of Commerce has granted general permission for OpenAI to roll out GPT-5.6, paving the way for a wider release of ChatGPT and its API as early as Thursday.

The approval follows a review by the Commerce Department’s Center for AI Standards and Innovation, which evaluated the frontier AI model under a voluntary agreement signed by President Donald Trump that gives regulators up to 30 days to assess advanced AI systems before public deployment.

During the review process, OpenAI stationed a dedicated technical team in Washington, D.C., to answer regulators’ questions directly, a step Axios described as unusual. The company is preparing three GPT-5.6 variants for launch: Sol as the flagship model, Terra as a balanced option, and Luna as a lower-cost, faster version.

Approval removes a key uncertainty for OpenAI traders

With the regulatory review complete, attention has quickly turned to OpenAI’s pre-IPO perpetual futures, which already trade on crypto platforms including Coinbase and Binance.

As crypto.news previously reported, Coinbase introduced OPENAI-PERP through its Everything Exchange initiative in June, allowing eligible non-U.S. users to gain exposure to OpenAI’s private-market valuation through perpetual futures settled in USDC. The contracts have no expiration date and are designed to convert automatically if OpenAI eventually lists its shares publicly.

The latest approval gives traders a fresh catalyst to price into those contracts because GPT-5.6 is expected to become the company’s next flagship commercial release. Even so, Coinbase has warned that OpenAI’s eventual IPO price could still end up as much as 25% above or below the perpetual futures price at the time of listing.

Industry data cited by CryptoQuant points to growing interest in pre-IPO crypto products. According to the analytics firm, trading volume across the sector climbed to $12 billion in June 2026 from just $2 million in March.

Crypto.news previously noted that the infrastructure for trading OpenAI and Anthropic pre-IPO futures has already been established, allowing markets to react immediately to company-specific developments such as regulatory approvals.

OpenAI continues building its AI business ahead of any listing

Recent corporate developments have added to investor attention surrounding OpenAI. Earlier this month, as crypto.news reported, SoftBank Group completed a second $10 billion investment in the company, moving the Japanese conglomerate closer to fulfilling its previously announced $30 billion follow-on commitment.

OpenAI has also continued investing in its own infrastructure. Last month, chief executive Sam Altman introduced Jalapeño, the company’s first custom-built AI chip developed with Broadcom.

According to OpenAI, the processor is optimized for inference workloads powering products such as ChatGPT, Codex, and future AI agents, reducing the company’s dependence on third-party hardware suppliers.

Still, enthusiasm around pre-IPO contracts has not always translated into immediate gains. Crypto.news previously reported that Anthropic’s pre-IPO perpetual futures fell 7% within 24 hours of their Coinbase debut despite strong interest in the company.

By contrast, the SpaceX pre-IPO market generated heavy retail participation before its public listing, with the stock later opening about 13% above its IPO price, providing an example that OpenAI traders are now watching closely as GPT-5.6 moves toward public release.

The Bank of England has reaffirmed that its work on a potential digital pound has remained independent despite claims that political lobbying may have influenced its approach.

Summary

- Bank of England Governor Andrew Bailey said Nigel Farage did not influence the central bank’s policy on a potential digital pound.

- Bailey’s letter, reported by The Guardian, said no CBDC policy changes followed his meeting with Farage on cryptocurrencies.

- Farage continues to face parliamentary scrutiny over crypto-linked gifts as the Bank of England advances digital pound research.

Bailey says CBDC policy remained independent

According to The Guardian, Bank of England Governor Andrew Bailey said the central bank did not alter its position on a potential central bank digital currency after meeting Reform UK leader Nigel Farage.

The newspaper reported that Bailey made the comments in a letter written after the meeting, which covered several topics, including cryptocurrencies.

In the letter obtained by The Guardian, Bailey reportedly said the Bank of England is capable of identifying attempts to influence its policymaking. He also wrote that no policy changes had resulted from Farage’s interventions after the meeting.

Bailey’s response came after Farage publicly said he had discussed cryptocurrencies with the governor. According to The Guardian, Bailey confirmed the meeting took place but rejected any suggestion that the conversation affected the Bank’s work on a digital pound.

Farage has repeatedly criticized central bank digital currencies, arguing they could increase financial surveillance. He previously said he would “rather go to prison” than live under such a system, a position he has maintained while opposing the proposed digital pound.

Farage faces scrutiny as digital pound research continues

Separately, Farage has resigned as the Member of Parliament for Clacton and will contest a by-election while parliamentary investigations into his financial declarations continue.

During an X livestream on Tuesday, Farage said he stepped down so local voters could decide whether he should continue representing the constituency instead of waiting for the outcome of the investigations.

Farage said he had “done nothing wrong” and maintained that he had not broken any laws or misused public money. He also confirmed that the UK parliamentary standards commissioner is investigating two matters involving gifts he received from crypto billionaire Christopher Harborne and George Cottrell, who has a previous fraud conviction and has been linked to a crypto casino.

According to Farage, the money provided by Harborne was an unconditional gift that would be used to pay for his personal security because of threats and attacks against him. He said seeking re-election would allow voters in Clacton to judge his actions directly.

Meanwhile, The Guardian reported that the UK’s National Crime Agency is investigating several transactions involving other senior Reform UK figures over suspected money laundering. The report did not say that Farage was part of that investigation.

While those political developments continue, the Bank of England has kept its digital pound project under review. In a recent update, the central bank said no decision has been made on whether to introduce a digital pound and added that any launch would require further analysis and public consultation.

Earlier this year, the Bank of England began a six-month pilot involving 18 companies to test how tokenized assets could be settled using central bank money. According to the central bank, the program is designed to examine settlement technology as officials continue evaluating whether a digital pound would have a role in the UK’s financial system.

Crypto exchanges now let you trade Tesla, gold, oil, and even pre-IPO companies like SpaceX and OpenAI as perpetual futures, around the clock, with leverage, without owning a single share. This guide explains how RWA perpetuals work, how a contract tracks an asset the blockchain cannot see, what happens when the stock market closes and the perp does not, and the real risks behind the most ambitious expansion perps have ever attempted.

Summary

- RWA perps bring crypto-style perpetual futures to off-chain assets like stocks, commodities, currencies, and private companies.

- These contracts provide price exposure only, not ownership, dividends, votes, or any claim on the underlying asset.

- The oracle is the core risk layer because it decides what off-chain price the contract tracks and what price can liquidate traders.

- Closed-market gaps make stock and commodity perps structurally different from crypto perps that trade against live spot markets 24/7.

- RWA perps are best understood as trading and hedging instruments, not long-term substitutes for owning stocks or tokenized shares.

The most traded instrument in crypto has started eating the rest of finance. Perpetual futures, the leveraged, never-expiring contracts that dominate crypto volume, are no longer limited to Bitcoin and Ethereum: on a growing list of venues you can now open a leveraged position on Tesla stock at 3 a.m. on a Sunday, short gold from a self-custodied wallet, or trade contracts tracking companies like SpaceX, OpenAI, and Anthropic that have never listed on any stock exchange at all. Coinbase’s rollout of pre-IPO perpetuals on exactly those names made headlines this month, and decentralized venues have quietly listed perps on US equities, indices, foreign exchange, and commodities for over a year.

These instruments are called RWA perpetuals, perps on real-world assets, and they represent something truly new: synthetic, around-the-clock, globally accessible exposure to assets that live entirely outside crypto, delivered through contracts that never touch the underlying. No shares are bought, no gold is vaulted, no barrel of oil changes hands. The entire construction rests on a price feed and a payment mechanism, which is either an elegant triumph of financial engineering or a stack of risks wearing a stock ticker, depending on which part of it you are looking at.

This guide explains RWA perps from first principles: what they are and how they differ from ordinary crypto perps and from tokenized stocks, the oracle machinery that lets a blockchain track an off-chain price, the strange problems that arise when a 24/7 contract tracks a market that closes on weekends, the pre-IPO frontier where perps track companies with no public price at all, the legal battle over what these contracts even are, and the honest risk list anyone should read before trading equity exposure inside a crypto venue.

Perps in one paragraph, and what changes with RWAs

A perpetual future is a derivative contract that lets a trader take a leveraged long or short position on an asset’s price and hold it indefinitely, because unlike a traditional future it never expires. Its price is tethered to the real asset’s price by the funding rate, a recurring payment between longs and shorts that nudges the contract back toward the underlying whenever it drifts: trade above the reference price and longs pay shorts, encouraging selling; trade below and shorts pay longs. Margin collateralizes the position and liquidation closes it if losses approach the margin posted. If any of that machinery is unfamiliar, the full plain-English guide to perps, funding, and liquidations is the place to start, because everything below assumes it.

Now change one word. A Bitcoin perp tracks an asset that trades on the same rails, around the clock, with deep on-chain and exchange price sources. An RWA perp tracks an asset that trades somewhere else entirely: a stock on Nasdaq, gold in London, oil in futures pits, a currency in the interbank market. The contract mechanics are identical, the same funding rate, the same margin, the same liquidation engine, but the reference price now comes from outside crypto, through an oracle, from a market with its own opening hours, holidays, halts, and corporate events. Every distinctive property of RWA perps, good and bad, flows from that single change. The trader gets exposure to Apple without a brokerage account, without owning shares, without market-hours restrictions, and without the venue holding any Apple at all; the trade-off is that the entire product is only as good as the price feed and the venue’s handling of the moments when the real market is dark.

It is worth separating RWA perps cleanly from their tokenized cousins, because the two are constantly conflated. A tokenized stock is a claim: somewhere, an issuer holds real shares and mints tokens representing them, with custody, redemption, and dividend questions attached. An RWA perp is not a claim on anything; it is a bet settled in stablecoins whose size happens to be indexed to a stock’s price. You cannot redeem a perp for a share, you receive no dividends, and you own nothing except a margin position. The perp’s advantage is precisely that it needs no custody chain, no share purchases, and no issuer, which is why perps on real-world assets scaled faster than tokenized versions of the same assets; its limitation is that it delivers only price exposure, nothing else a share provides.

The oracle problem: teaching a blockchain the price of Tesla

A blockchain cannot see Nasdaq. Every RWA perp therefore depends on an oracle, infrastructure that fetches off-chain prices and delivers them on-chain, and the oracle design is the single most important line in any RWA perp’s documentation, because it determines what price you are liquidated against.

Serious implementations layer defenses. Prices are pulled from multiple independent sources, exchange feeds, institutional data providers, aggregators, and combined into an index price so no single source can be spoofed. The contract then computes a mark price, typically a smoothed or median-filtered version of the index, and it is the mark price, not the last trade on the venue itself, that drives liquidations, so a momentary wick on the perp’s own order book cannot cascade positions. Funding is computed from the gap between the perp’s trading price and the index. All of this mirrors crypto-perp best practice; the RWA twist is that equity and commodity data is licensed, paywalled, and published on the real market’s schedule, so oracles for stocks tend to involve professional data vendors and update rules for what to publish when the source market is closed.

The failure modes are exactly what you would guess. A stale feed liquidates traders against yesterday’s price; a manipulated thin source poisons the index; a decimal error in one vendor’s print, without median filtering, becomes a mass liquidation event. These are not hypotheticals in DeFi’s history, oracle failures are among its most reliably recurring disasters, and the diligence question for any RWA perp venue is boringly specific: how many sources, what aggregation, what staleness rules, and what happened the last time one input misbehaved.

When the market sleeps and the perp does not

Here is the genuinely novel problem RWA perps introduced, one crypto perps never had: the underlying market closes. Nasdaq trades six and a half hours a day, five days a week; the perp trades every hour of every day. For roughly two-thirds of the perp’s life, there is no live reference price at all.

What happens in the gap is price discovery in reverse. During market hours, the perp follows the stock. Overnight and on weekends, the perp becomes the only live market for that exposure, and it drifts on crypto-native flows, news, and speculation, anchored only by traders’ expectations of where the stock will open. Then comes Monday’s open, and the stock either validates the weekend perp price or gaps away from it, at which point funding and arbitrage violently reconcile the two. Traders who study these venues have observed that weekend equity-perp prices function as a real-time forecast of Monday’s open, which is fascinating for researchers and dangerous for the overleveraged: a position that survives the whole weekend can be liquidated in the first minute of the cash session when the reference price jumps to reality.

Corporate actions add a second layer of housekeeping crypto never needed. Stocks split, pay dividends, get halted, and get delisted. A 10-for-1 split must be handled by adjusting the contract or the index, or every position would instantly show a 90% move; dividends create predictable price drops the perp must account for, typically through funding adjustments, since perp holders receive no dividend; a trading halt in the underlying leaves the oracle publishing nothing while the perp keeps trading. Every serious RWA-perp venue has written rules for each event, and the difference between venues is largely the quality of those rules, which nobody reads until the day they matter.

Where RWA perps trade, and how the peg holds in practice

The venue landscape splits along the same centralized-versus-decentralized line as the rest of crypto, with the decentralized side, unusually, having led. On-chain perp exchanges pioneered equity and forex perps because listing a new market there requires an oracle feed and a risk parameter file, not a licensing negotiation: Hyperliquid, the dominant on-chain perp venue with roughly 70% of decentralized open interest, lists perps across crypto, US equities, indices, foreign exchange, and commodities, and peers like dYdX and GMX cover overlapping ground. The centralized side arrived with 2026’s regulatory thaw, Coinbase’s CFTC-supervised perp products and pre-IPO contracts being the landmark, and carries the opposite trade-offs: eligibility gating and custody of your margin, in exchange for regulated recourse and deeper fiat integration. The decentralized share of total perp open interest has climbed to roughly 13.5% from under 4% a year earlier, and RWA listings are a visible driver, because the assets people most want to trade at 3 a.m. are precisely the ones whose official markets are closed.

It is worth dwelling on how the peg actually holds for an RWA perp, because the mechanism is subtler than for crypto perps. With a Bitcoin perp, arbitrageurs enforce the peg directly: if the perp trades rich, they short it and buy spot Bitcoin, a riskless-ish basis trade available around the clock. With a stock perp, the spot leg is only available during market hours, so during the trading day the peg is enforced by the same basis arbitrage, brokerage account on one side, perp on the other, and it holds tightly. Overnight, the arbitrage is unavailable, and the only tether is the funding rate pushing against crowd positioning plus traders’ willingness to fade a drift they expect the open to punish. The result, visible in the data, is a peg that breathes: tight during cash sessions, loose and expectation-driven outside them, snapping taut at each open. Traders who internalize that rhythm stop being surprised by it; funding on equity perps also inherits the rhythm, often resetting sharply around opens as the reconciliation happens.

One further mechanical note: margin and settlement on RWA perps are almost universally in stablecoins, which means a trader’s collateral is exposed to stablecoin risk on top of position risk, and profits on a Tesla short arrive as USDC, not as anything resembling a brokerage balance. The entire experience is crypto-native from margin to settlement; only the price is borrowed from the outside world.

The frontier: perps on companies with no price

The strangest members of the family are the pre-IPO perpetuals, contracts tracking private companies, SpaceX, OpenAI, Anthropic, that have no exchange-listed price to reference at all. Here the oracle question becomes almost philosophical: what does the contract track? In practice, venues construct reference prices from private-market data, secondary-share transaction reports, disclosed funding rounds, and administrator judgment, published as an index that updates far less frequently and far less verifiably than any stock feed. The funding mechanism then tethers the perp to that constructed number.

The appeal is obvious and real: exposure to the most coveted private companies on earth has historically been reserved for venture funds and accredited insiders, and a perp democratizes at least the price bet. The caveats deserve equal billing. The reference price is an estimate with wide error bars, not a market print; liquidity in these contracts is thin relative to major perps; the gap between a private valuation and an eventual IPO price can be enormous in either direction; and a trader is ultimately taking positions against a number a small set of parties assembles. It is the frontier, with everything that word implies, and its emergence within regulated American venues in 2026 says as much about the regulatory moment as about the product.

What the law says a perp is

That regulatory moment is its own story, because RWA perps sit precisely on the fault line American law is redrawing. Perpetual futures spent a decade as an offshore product, and 2026 is the year they came onshore: the CFTC approved US-regulated perpetual contracts, Coinbase secured routes to offer perp-style products to eligible American customers, and equity and pre-IPO perps followed. Immediately, the definitional fight began, most visibly in litigation between CME and the CFTC over what legally distinguishes a perpetual from the dated futures the incumbent exchanges have licensed for decades. The answer matters commercially, an instrument classified one way slots into existing licensing regimes and another way does not, and it matters for RWA perps most of all, because a perp on a stock brushes against securities law in ways a perp on Bitcoin does not. The broader classification architecture being decided in Congress, mapped in this publication’s guide to the pending market-structure law, will determine which agency’s rules these products ultimately live under, and traders should treat the current arrangements as provisional. Meanwhile the traditional-finance side is converging from the other direction, with the DTCC piloting tokenized versions of the very equities these perps synthesize, a pincer movement whose endpoint, real assets and synthetic exposure sharing on-chain rails, is visible even if its timeline is not.

A brief sizing note grounds all of this. Perpetual futures as a class did roughly $61 trillion of volume in 2025 with daily totals routinely above $100 billion, several multiples of spot; RWA contracts are a young single-digit share of that machine, growing from a base near zero two years ago. The scale of the host explains the stakes: even a modest share of perp flow migrating to equity and commodity tickers represents volume that rivals mid-sized national stock exchanges, arriving on rails no securities regulator designed.

Who actually uses RWA perps

The user base sorts into recognizable types, and knowing them clarifies what the product is for. The largest group is access-constrained traders: people in jurisdictions without cheap brokerage access to US equities, for whom a perp on an index or a mega-cap is the first practical route to that exposure at all, leverage aside. The second is the crypto-native hedger: a fund or treasury holding volatile crypto that wants to offset macro exposure, short an index against a token portfolio, hedge dollar strength through forex perps, without opening brokerage relationships and moving capital across the fiat border. The third is the weekend and event trader, using the perp’s always-open market to position around news that breaks when exchanges are closed, earnings leaks, geopolitical shocks, Sunday-night macro, accepting gap risk in exchange for being early. The fourth is the basis and funding trader, harvesting the structural spreads between the perp, the underlying, and the calendar of opens and closes, the professionals for whom the peg’s breathing rhythm is not a hazard but the product itself.

What the list conspicuously lacks is the buy-and-hold investor, and that is the honest boundary of the instrument. A perp position pays funding indefinitely, carries liquidation risk permanently, and confers no ownership; holding one for months as a stock substitute is almost always dominated by simply owning the stock or its tokenized form. RWA perps are a trading and hedging instrument that happens to wear equity tickers, not an investment product, and most of the grief in the category comes from users who mistook one for the other.

The honest risk list

Everything above condenses into a short list anyone should hold against the marketing.

First, you own nothing. An RWA perp delivers price exposure, not shares, dividends, votes, or any claim; in a venue insolvency you are an unsecured creditor of a margin balance. Second, the oracle is the product; a perp on Tesla is really a perp on someone’s Tesla price feed, and its integrity ceiling is the feed’s. Third, the closed-market gap is a structural hazard: weekend positions carry reconciliation risk at every open, and leverage that feels safe on Saturday can be fatal at 9:30 on Monday. Fourth, all the ordinary perp dangers apply at full strength, funding costs that erode crowded positions, liquidation mechanics that work exactly as brutally here as everywhere else, and thin order books where large orders suffer meaningful execution costs. Fifth, the legal ground is actively shifting, and products available today may be restructured, restricted, or geofenced tomorrow.

Against those risks stands what RWA perps genuinely deliver: the first globally accessible, always-open, self-custodial route to price exposure on the world’s most important assets, with shorting and leverage included, no brokerage gatekeeping, and settlement in stablecoins. That is not a small thing, and it explains why volume has arrived faster than infrastructure maturity. The sensible posture is the one perps have always demanded, respect the leverage, know your liquidation price, read the contract specifications, and add the RWA-specific habits: check the oracle design, check the corporate-actions policy, and never carry a weekend position sized for a market that cannot gap.

The larger meaning of the category is worth one closing paragraph. RWA perps are the first instrument through which crypto’s market structure, rather than its assets, went global: what is being exported is not a coin but a way of trading, continuous, self-custodial, leverage-native, and settled in stablecoins, applied to the underlyings the rest of the world already cares about. Whether that export ends with crypto venues capturing equity flow, or with traditional exchanges adopting perpetual mechanics and around-the-clock sessions to repatriate it, and the incumbents’ own moves toward continuous clearing suggest the second path is live, the direction of convergence is set. The trader’s edge, for now, lies in understanding both worlds at once: the perp machinery crypto built, and the market-hours, corporate-actions, oracle-fed reality of the assets it has annexed.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Perpetual futures are high-risk leveraged instruments and you can lose your entire margin. Product availability and regulation vary by jurisdiction and are changing rapidly as of July 8, 2026. Always do your own research.

Frequently asked questions

What is an RWA perpetual in simple terms?

An RWA perpetual is a crypto-style perpetual futures contract whose price tracks a real-world asset, a stock, a commodity, a currency, or even a private company, instead of a cryptocurrency. It lets you take a leveraged long or short position on that asset’s price, around the clock, without owning it, with the contract kept in line by funding payments against an oracle-delivered reference price.

How is an RWA perp different from a tokenized stock?

A tokenized stock is a token backed by real shares held somewhere by an issuer, a claim you can in principle redeem. An RWA perp is backed by nothing; it is a margin bet whose payoff is indexed to the asset’s price. Perps offer easier leverage, shorting, and no custody chain; tokenized stocks offer actual ownership economics like dividends. They solve different problems and carry different risks.

Do I receive dividends from a stock perp?

No. Perp holders own no shares and receive no dividends, votes, or corporate rights. Venues typically account for dividends through index or funding adjustments so that the predictable price drop on the ex-dividend date does not unfairly transfer money between longs and shorts, but no dividend is ever paid to you.

What happens to my stock perp when the market is closed?

The perp keeps trading. With no live reference price, it floats on traders’ expectations of where the stock will reopen, effectively becoming a forecast market. When the real market opens, the reference price jumps to reality and funding and arbitrage pull the perp into line, which can be violent if news broke during the closure. Overleveraged weekend positions are the classic casualty.

How can there be a perp on a private company like SpaceX?

The venue constructs a reference price from private-market data such as secondary transactions and funding rounds, and the perp’s funding mechanism tethers the contract to that constructed index. It provides otherwise unavailable exposure, with the major caveat that the reference price is an estimate rather than a market print, updated less often and less verifiably than any stock feed.

Are RWA perps legal in the United States?

The landscape shifted in 2026 as the CFTC approved US-regulated perpetual contracts and major venues brought perp-style products onshore, including equity and pre-IPO contracts for eligible customers. Classification disputes are active, including litigation over how perps differ from dated futures, and pending market-structure legislation will shape the final rules, so availability depends on venue, product, and jurisdiction and should be verified rather than assumed.

What is the biggest risk specific to RWA perps?

The oracle and the closed-market gap. Your position is marked and liquidated against a constructed reference price, so feed quality is everything, and when the underlying market is closed the perp can drift far from where the asset will actually reopen. Both risks come on top of the standard perp dangers of leverage, funding costs, and liquidation.

Can I get liquidated while the stock market is closed?

Yes. The perp trades and marks positions continuously, so a weekend move in the perp’s mark price can liquidate you before the underlying market ever opens. Equally, a position can survive the weekend and be liquidated instantly at the open when the reference price gaps. Sizing for the gap, not for the calm, is the core discipline.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

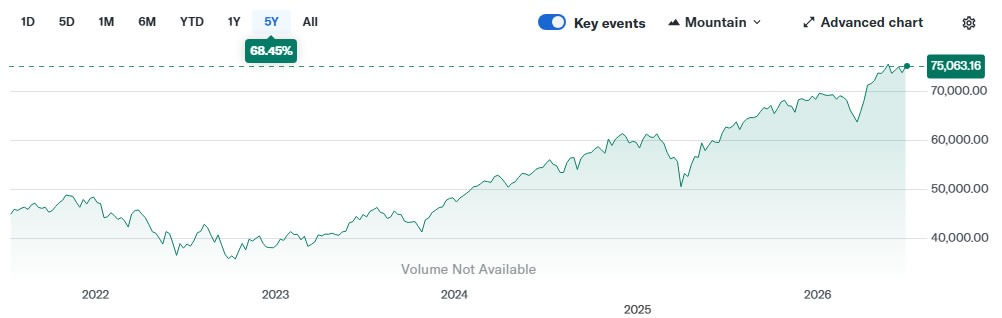

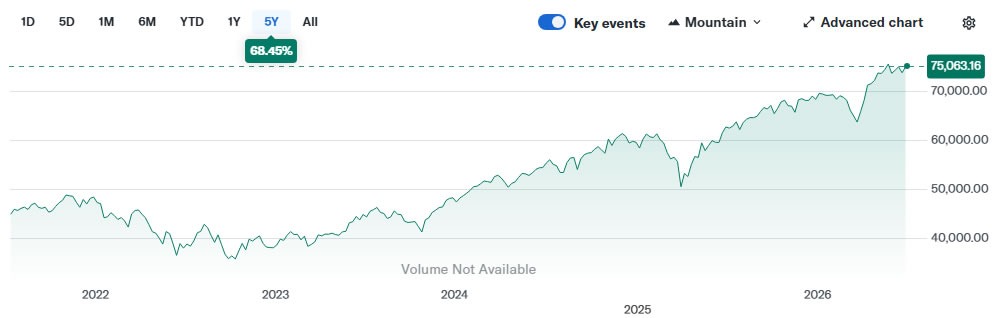

Whether crypto ultimately benefits from a new liquidity push from the Federal Reserve may depend less on any direct policy support for digital assets and more on how policymakers react if US markets face a sustained downturn. Analysts speaking to Cointelegraph argue that if the Fed concludes it must “break decades of precedent” to defend equities, the resulting shift in liquidity expectations could improve conditions for risk assets—potentially including Bitcoin and other mainstream cryptocurrencies.

The debate comes as the US equity market has risen sharply in recent years. According to the article, the market has grown by 68% over the past five years and added roughly $6 trillion in value so far this year, even as critics have warned that rapid expansion can be followed by a serious correction. In that scenario, one proposal gaining attention is the Fed supporting equities through purchases tied to exchange-traded funds, an approach that would mark a meaningful escalation in the Fed’s traditional toolkit.

Key takeaways

- Analysts suggest a Fed response to a major equity drawdown could include support mechanisms such as ETF buying, which would be a significant departure from past practice.

- Even without direct central-bank involvement, crypto prices are still described as heavily influenced by US dollar liquidity, real interest rates, and broader risk sentiment.

- Policy actions that signal a “floor” under risk assets could compress the risk premium investors demand for volatile assets like Bitcoin.

- Central-bank bond-market interventions in past crises (including COVID-era ETF purchases) are cited as precedent for how liquidity backstops can alter market behavior.

- However, multiple analysts also note that high inflation may limit how aggressively the Fed can “print money,” leaving other tools on the table.

If equities get defended, liquidity could spill over

Cointelegraph reports that US equities are often treated as deeply embedded in the fabric of the economy—through household portfolios, pensions, and corporate financing. HashKey Group senior researcher Tim Sun told Cointelegraph that the US stock market is “deeply embedded in American household balance sheets, the pension system, corporate financing capabilities, and the structural dynamics of fiscal revenue.”

That structural exposure matters because it raises the political and economic stakes of a prolonged bear market. Cointelegraph also cites Balchunas’s claim that 58% of Americans own stocks, arguing that pressure to avoid extended market weakness could become “very powerful.”

Balchunas further said on Tuesday that the Fed could decide to “break decades of precedent” by buying equity ETFs to support the stock market. The underlying idea is that the Fed might choose a mechanism designed to stabilize liquidity when traditional channels appear to be failing—an approach that could improve risk appetite across the asset class spectrum.

From COVID-era ETF buying to a possible equity backstop

The article points to prior Fed actions during crisis periods to support the claim that central-bank liquidity interventions can become a template. In 2020, the Fed purchased corporate bond ETFs as part of its broader effort to restore liquidity to frozen credit markets during the COVID-19 shock. The article says those measures involved the Fed acquiring $8.7 billion worth of ETFs, helping limit economic damage while credit markets struggled.

Balchunas is described as suggesting that the Fed may be more likely to replicate an “ETF buyer of last resort” posture in future downturns. In the report’s framing, the shift would not necessarily be aimed at crypto—rather, it would be aimed at equities and credit, with digital assets benefiting as secondary effects through changing liquidity and risk conditions.

Cointelegraph also notes that central banks in China and Japan have used indirect equity ETF purchases via authorized intermediaries funded by public resources. While those are not US policy, Balchunas argues the approach is operationally feasible, and that the US could eventually follow if equity stabilization becomes urgent enough.

Why crypto is described as a dollar-liquidity trade

Even if the Fed never targets cryptocurrencies, Sun argues that macro forces still dominate crypto pricing. He told Cointelegraph that a prolonged, severe bear market would “do far more than just erode investor wealth,” adding that it would likely shock consumer spending, compromise pension stability, slow corporate credit expansion, and dent tax revenues.

In that context, cryptocurrencies may not be directly shielded by policy, but the article stresses that their market behavior remains tied to broader financial variables. Sun said crypto’s macro pricing is fundamentally linked to US dollar liquidity, real interest rates, and equity market risk sentiment.

Bitget Wallet chief operating officer Alvin Kan echoed the linkage, telling Cointelegraph that historically, once the Fed takes steps that support risk assets—through rate cuts, balance-sheet expansion, or even targeted ETF purchases—crypto has tended to enter a medium-to-long-term uptrend. He compared such conditions to the 2021 period, when risk appetite returned and capital rotated into high-beta assets.

The report frames this as a change in investor expectations rather than a direct “policy promise” for crypto. As another quoted view within the article describes, when market participants believe there is an effective policy floor under risk assets, the risk premium demanded for highly volatile assets should compress—creating a more favorable environment for Bitcoin and broader crypto exposure.

Limits on Fed action and the tools that remain

Not all analysts see the Fed’s options as unlimited. Jeff Mei, the operating chief of BTSE, told Cointelegraph that while a downturn could prompt action, it’s difficult to envision the Fed “printing more money” given that inflation remains high. In his view, the central bank can still respond using other tools, even if large-scale money creation becomes politically or economically constrained.

This matters for traders and investors because the market impact of any Fed response may depend on what form it takes. A shift toward liquidity provision that calms rates and improves risk sentiment could help crypto, but the direction and magnitude of that benefit likely hinge on the specific policy mechanism and how quickly markets interpret it as credible.

Kan’s comments, as relayed in the article, suggest that a structural backstop for macro conditions could strengthen crypto’s role as both a growth and diversification asset in a world of expanding global liquidity. At the same time, Mei’s caution highlights that high inflation could slow or reshape the policy path, leaving the market to watch not just whether equities are supported, but how and with what instruments.

For now, the key thing readers should monitor is whether policymakers move from general easing expectations to concrete actions that explicitly stabilize equities—especially any steps involving ETF-related mechanisms—and how quickly those signals translate into improved dollar liquidity and lower risk premia across the broader market.

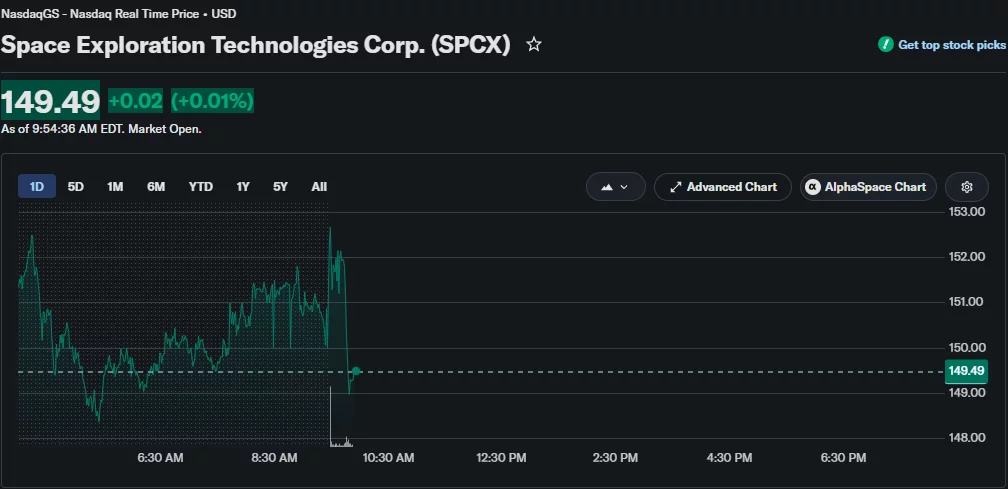

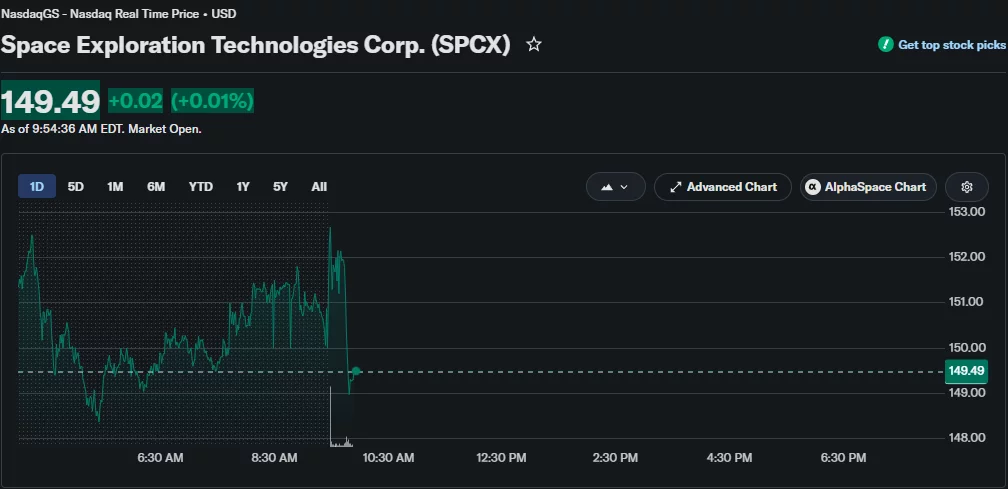

SpaceX has transferred Bitcoin for the first time in six months, while its newly listed SPCX shares have fallen more than 25% from recent highs despite joining the Nasdaq-100.

Summary

- SpaceX moved Bitcoin for the first time in six months, though the transfer was worth only $88.

- SPCX shares have fallen more than 25% despite the company’s fast-tracked Nasdaq-100 inclusion.

- JPMorgan estimates the index addition could drive about $4.3 billion in passive fund buying.

According to Arkham Intelligence, a wallet linked to Elon Musk’s SpaceX moved just $88 worth of Bitcoin on July 8, ending a six-month period without on-chain activity. Although the transfer was tiny, it quickly fueled speculation across crypto markets because the company’s wallets have historically remained inactive for long periods.

Arkham Intelligence data showed that SpaceX still holds about 18,712 BTC, worth roughly $1.16 billion at current prices. The receiving wallet now contains 614 BTC valued at about $38 million. The blockchain analytics platform also showed that the company’s previous major transfer involved more than 1,016 BTC worth nearly $100 million.

Why did a small Bitcoin transfer attract attention?

While the latest transaction involved only a nominal amount, it arrived after a series of larger Bitcoin sales by corporate treasury holders. Strategy, MARA Holdings, Nakamoto Holdings, and Sequans Communications have all disclosed Bitcoin sales in recent weeks.

Last week, Strategy announced a Bitcoin sale worth about $216 million, adding to investor sensitivity around transfers from large institutional wallets.

Past activity has also added to the attention. Arkham Intelligence data indicates that outflows from SpaceX to unidentified wallets accelerated around the crypto market decline on Oct. 10 last year before slowing as the company’s attention turned toward its public listing.

Meanwhile, Bitcoin traded above $62,000 but remained nearly 2% lower on the day as geopolitical tensions weighed on risk assets. The decline followed renewed U.S.-Iran strikes, while President Donald Trump questioned whether the cease-fire between the two countries would hold after both sides exchanged fresh attacks.

Why has SPCX remained under pressure despite Nasdaq-100 inclusion?

Selling pressure has continued in SpaceX shares even after the company secured a place in the Nasdaq-100. SPCX closed 6.83% lower at $149.47 on Tuesday after touching an intraday low of $148.86, leaving the stock below its IPO debut price and more than 25% below levels seen about a month ago. Premarket trading on Wednesday showed the shares edging up 0.49%.

Nasdaq confirmed that SpaceX qualified for accelerated inclusion under revised eligibility rules that allow certain large newly listed companies to enter the Nasdaq-100 much sooner than previously permitted. The company officially joined the benchmark before the opening bell on July 7, making it one of the fastest IPOs to enter the technology-focused index.

According to JPMorgan, the index addition is expected to generate roughly $4.3 billion in compulsory buying by passive exchange-traded funds and other index-tracking portfolios that must rebalance their holdings to match the Nasdaq-100. Even with that expected inflow, investors continued taking profits after the stock’s strong rally following its market debut.

Wall Street has nevertheless remained constructive on the stock. As previously reported by crypto.news, analysts at Morgan Stanley, Goldman Sachs, and Citigroup have initiated coverage on SpaceX with higher valuation targets.

Morgan Stanley has taken the most bullish stance, assigning a $300 price target while arguing that the company’s long-term growth prospects remain intact despite the recent pullback.

Stablecoins are increasingly showing up at the heart of tokenized finance, not just as short-term trading tools. In a report released by Binance Research, stablecoin-settled perpetual contracts tied to traditional financial assets generated more than $1.1 trillion in trading volume in the first half of 2026—highlighting how on-chain dollar instruments are being used to mirror parts of TradFi through crypto.

Binance Research also points to a broader shift in behavior among exchange users: stablecoins are becoming long-term portfolio holdings rather than assets held only for brief trading windows. That dual role—derivatives settlement and everyday value storage—helps explain why stablecoin activity is rising alongside the market’s size.

Key takeaways

- Binance Research reports stablecoin-settled TradFi-linked perpetual contracts topped $1.1 trillion in first-half 2026 volume.

- Those TradFi perpetuals accounted for roughly 11% of all crypto perpetual trading volume in the first five months of 2026, per Binance Research.

- Binance data cited in the report shows stablecoins are moving from “temporary” trading assets toward longer-term holdings (with stablecoin-heavy portfolios becoming far more common).

- Stablecoin usage for cross-border transfers is accelerating in Latin America, where transfer-user share on Binance rose to 38% in 2026 from 17% in 2025.

- Overall stablecoin market capitalization is around $311 billion, with payment-related activity supported by recent record transaction volumes tracked by Visa’s Allium dashboard.

Derivatives settlement moves closer to TradFi

One of the clearest signals from Binance Research is that stablecoins are increasingly being used as settlement rails for perpetual contracts linked to traditional financial assets. These “TradFi perpetuals” are designed to give traders exposure to assets familiar from conventional markets, while using crypto infrastructure and stablecoin settlement.

According to Binance Research, this segment expanded to roughly 11% of total crypto perpetual trading volume across the first five months of 2026. The first-half 2026 figure—over $1.1 trillion in stablecoin-settled TradFi perpetual trading—suggests the category is no longer a niche experiment and has become a meaningful slice of derivatives activity.

The practical implication for traders and market makers is that stablecoins are becoming less optional in derivatives routing. Instead of merely being a quote asset or temporary buffer, they are increasingly embedded in how positions are effectively settled and maintained.

Stablecoins shift from trading fuel to portfolio core

Binance Research argues the stablecoin story is not only about derivatives. It says stablecoins are increasingly used as longer-term stores of value, with measurable changes in how exchange users allocate their holdings.

The report states that 30% of Binance exchange users now hold more than half of their portfolios in stablecoins, up from 4% in 2020. This is a large behavioral change, suggesting that many participants are treating stablecoins as a default “base” for account value—whether for risk management, quick deployment into trades, or keeping capital positioned on-chain without exposure to higher volatility assets.

For investors and traders, the takeaway is that stablecoins may be playing an increasingly structural role in liquidity and capital allocation. If more participants keep a stablecoin-heavy allocation, it can affect how quickly liquidity appears across markets and how sensitive exchange order books are to broader market swings.

Payments momentum and record transaction volumes

Beyond exchange behavior and derivatives, the report frames stablecoins as part of a wider payment and settlement ecosystem. DefiLlama data cited in the article shows global stablecoin market capitalization is roughly $311 billion, up from about $254 billion a year earlier.

Visa’s Allium-powered stablecoin dashboard adds another layer to the activity picture. According to Visa’s dashboard figures referenced in the article, adjusted stablecoin volume reached a record $1.79 trillion in June—exceeding the previous high set in February. The combination of a higher market cap and stronger transaction activity points to demand that is not limited to speculative trading.

For readers, this matters because stablecoin growth that is supported by transaction throughput is generally more resilient than growth driven solely by short-lived leverage cycles. When payment rails and settlement demand rise, stablecoins can become more tightly linked to real usage patterns.

Latin America becomes a focal point for transfer adoption

Binance Research also highlights a geographic shift in stablecoin usage for cross-border payments, with Latin America standing out. The report says the region’s share of Binance stablecoin transfer users more than doubled to 38% in 2026 from 17% in 2025, attributing the change to growing demand for faster and lower-cost international transfers.

The report’s findings align with broader marketplace signals. A report highlighted in the article from Bitso—an exchange based in Mexico City—found that US dollar-pegged stablecoins represented 40% of crypto asset purchases on its platform in 2025. That share surpassed Bitcoin’s 18% for the first time, suggesting stablecoins are increasingly the gateway asset for purchases and on-chain value conversion in the region.

Industry participants have also framed stablecoin payments as an opportunity set beyond the traditional US-to-Mexico remittance corridor. The article notes that in May, Claudia Wang, a former Bybit executive, estimated remittance corridors outside the US-to-Mexico market represent a $112 billion opportunity for stablecoin issuers.

Traditional players appear to be moving in parallel. In May, Western Union launched its USDPT stablecoin on the Solana network for cross-border payments. Later, MoneyGram launched its MGUSD stablecoin on the Stellar network for remittances using its consumer app, expanding the set of on-chain rails available to customers.

Taken together, these developments reinforce the idea that stablecoins are increasingly treated as payments infrastructure, not just speculative tokens. As adoption concentrates in regions with strong remittance demand, competitive pressure may shift toward reliability, coverage, fee efficiency, and user onboarding—areas where crypto-native rails can compete directly with legacy systems.

Looking ahead, investors and builders should watch whether stablecoin usage keeps deepening beyond trading venues—especially in high-throughput payment corridors like Latin America—and whether derivatives growth continues at a similar pace as market structure evolves. The key open question is how quickly stablecoin-settled TradFi perpetuals and real-world transfer flows can reinforce each other in sustained volume.

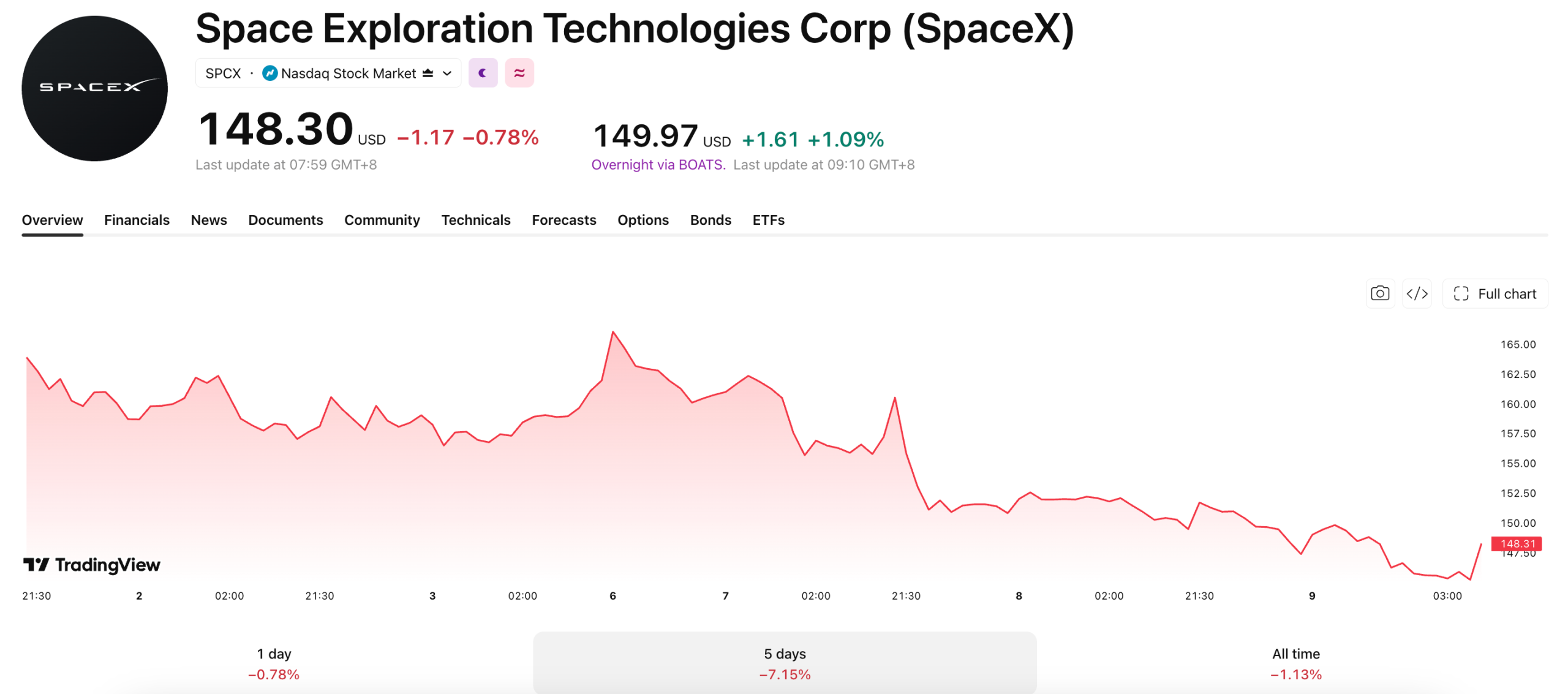

SpaceX (SPCX) shares have fallen as much as 35% from their post-IPO peak of $225.64. The drop came just days after the company joined the Nasdaq-100, as heavy selling offset forced index buying.

The stock closed at $148 on July 8, below its $150 debut price for a second straight session. That erased nearly all the gains SpaceX made since its record June 12 listing.

A Sell-The-News Pattern for SPCX

SpaceX’s Nasdaq-100 inclusion required index-tracking funds to buy shares, even though the company keeps a small public float. That mechanical demand did not stop investors from selling into the news.

This is a familiar pattern, as Palantir saw the same thing happen after it joined the Nasdaq-100 in late 2024. Its shares dropped about 25% over the following weeks.

A Trillion-Dollar Valuation Under Pressure

The pullback still leaves SpaceX with a market capitalization near $1.9 trillion. The company posted about $18.7 billion in revenue in 2025, up about 33% year over year. That puts its valuation at roughly 100 times sales.

Starlink drove much of that growth. SpaceX’s satellite internet unit generated more than $11 billion in 2025, about 61% of total revenue. It remains the main support for the company’s trillion-dollar valuation.

SpaceX still lost money last year. The company reported a $4.9 billion net loss in 2025 and $4.3 billion more in the first quarter of 2026. Heavy spending on its xAI artificial intelligence unit and on Starship development continues to weigh on cash flow.

Wall Street has largely stayed bullish since the Nasdaq-100 inclusion. Morgan Stanley, Bernstein, RBC, and UBS all initiated coverage with buy-equivalent ratings. MoffettNathanson took a neutral stance, and CFRA recommended that investors sell.

Starlink’s profit growth may determine how much further the stock can fall. Investors will likely watch whether that business can outpace SpaceX’s mounting AI and rocket-development costs.

The post SpaceX Stock Falls 35% From Peak Even After Nasdaq-100 Inclusion appeared first on BeInCrypto.

Crypto markets could benefit from increased liquidity if the US central bank steps in to support the $75 trillion equity market in a bear market, as it is “too big and too important to fail,” according to analysts.

The US equity market has grown by 68% over the past five years and has added roughly $6 trillion in market value so far this year. However, analysts and experts, such as goldbug Peter Schiff, have warned that years of rapid growth could be setting up the market for a major correction.

Such a correction could see the Fed “break decades of precedent” and buy equity ETFs to support the stock market, Balchunas said on Tuesday, while other analysts said the resulting move to increase liquidity could set up an environment for cryptocurrencies to benefit.

“Once the Fed steps in, rate cuts, balance-sheet expansion, even targeted ETF purchases, crypto has historically entered a medium-to-long-term uptrend, similar to what we saw in 2021, as risk appetite returns and capital rotates back into high-beta assets,” Bitget Wallet chief operating officer Alvin Kan told Cointelegraph.

Stocks deeply embedded in American households

Balchunas said that 58% of Americans own stocks, so “the political pressure to keep stocks out of a prolonged bear market is going to be very powerful.”

In 2020, the Fed bought corporate bond ETFs during COVID-19 to act as a “buyer of last resort” to restore liquidity to frozen credit markets. The unprecedented move saw it acquire $8.7 billion worth of ETFs, which helped to limit economic damage from the pandemic.

“I think there’s a good chance the Fed will buy equity ETFs in the next major downturn to support [the] market, and it will be common practice going forward,” said Balchunas.

Related: Crypto turns ‘contrarian bet’ as AI stocks draw investor attention: Bitwise

Central banks in China and Japan currently use indirect equity ETF purchases via authorized intermediaries with public funds to boost liquidity, and America could follow, he added.

“This is just one byproduct of the ‘Nothing Stops This Train’ monetary supply explosion and debt extravaganza sweeping the world, but especially in the US, which at this point feels irreversible.”

US stock market cap growth over the past five years, as measured by the Wilshire 5000 Total Market Index. Source: Yahoo Finance

Crypto remains tied to dollar liquidity

HashKey Group senior researcher Tim Sun said that a prolonged, severe bear market “would do far more than just erode investor wealth — it would directly shock consumer spending, compromise pension stability, stall corporate credit expansion, and dent tax revenues.”

While cryptocurrencies will not receive direct backing from the central bank, “their macro pricing remains fundamentally tied to US dollar liquidity, real interest rates, and equity market risk sentiment,” Sun added.

“Once market participants are convinced that a policy floor effectively underpins risk assets, the risk premium demanded for highly volatile assets will compress. As a result, Bitcoin and mainstream crypto assets are poised to benefit significantly from improving liquidity expectations and a broader revival in risk appetite.”

Bitcoin has underperformed US stock markets this year. Source: Google Finance

Strong incentive to backstop major drawdowns

“This structural backstop supports a more resilient macro backdrop, and that’s ultimately bullish for crypto’s role as a growth and diversification asset in a world of expanding global liquidity,” Kan said.

Meanwhile, Jeff Mei, the operating chief of BTSE, told Cointelegraph that in the event of a downturn, “it’s difficult to see the Fed printing more money to stimulate it, given that inflation is still high. However, there are other tools they can deploy to take action.”

Features: The biggest blockchain upgrades still to come in 2026

The de-escalation in the Middle East appears to be threatened severely as US President Donald Trump just said the memorandum of understanding (MoU) with Iran ‘is over.’

Most assets opened for trading now reacted with immediate volatility: oil prices rocketed, while BTC dipped below $62,000.

The report from CNN cited Trump, who said he believes the MoU with Iran is over after both parties failed to reach a permanent deal and resumed the airstrikes against each other across the region.

Recall that the Islamic Revolutionary Guard Corps said it responded to a wave of US attacks by launching its own against American military targets in Bahrain and Kuwait. It added that its military has targeted an air base in Bahrain hosting US forces.

The United States began its assault earlier and reimposed sanctions on Iranian oil sales as ‘punishment’ for attacks on ships near the Strait of Hormuz.

Speaking at the ongoing NATO summit in the Turkish capital Ankara, Trump added that he doesn’t want to reengage with Tehran for additional peace talks after the failure of the previous rounds.

As mentioned above, USOIL jumped immediately after the news went live, going to $75 for the first time since June 22. It had fallen below $67,50 just days ago as the markets priced in the war de-escalation.

As it typically happens when there are new attacks in the Middle East, bitcoin headed in the opposite direction. The asset had peaked above $64,000 earlier but began to gradually lose value after the initial attacks.

However, Trump’s worrisome message sent it further south, as the cryptocurrency dipped below $62,000 minutes ago.

The post Oil Soars, Bitcoin Plunges as Trump Declares Iran MoU ‘Is Over’ appeared first on CryptoPotato.

Smithsonian head says White House report unfairly characterized US history museum

DeFi Dashboard Zapper to Shut Down After 7 Years

BREAKING: Real Reason Why Sami Zayn Won And Lost The Undisputed WWE Championship In 9 Days

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

WOW XRP BREAKOUT! ALTCOIN SEASON INCOMING?! #xrp #crypto #bitcoin in

The Only 6 Accounts You Will EVER Need #finance #wealth #money #tyler

Here’s What Different Amounts Of Money Gets You In NYC Vs The World! #fyp #nyc #money #chicago

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: High Hopes

-

NewsBeat4 days ago

NewsBeat4 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Fashion2 days ago

Fashion2 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics6 days ago

Politics6 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World5 days ago

Crypto World5 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

News Videos2 days ago

News Videos2 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech2 days ago

Tech2 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Business2 days ago

Business2 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Crypto World7 days ago

Crypto World7 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World2 days ago

Crypto World2 days agoSK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World4 days ago

Crypto World4 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos2 days ago

News Videos2 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech4 days ago

Tech4 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Crypto World5 days ago

ESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

-

NewsBeat7 days ago

NewsBeat7 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business6 days ago

Business6 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World6 days ago

Crypto World6 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos3 days ago

News Videos3 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Sports1 day ago

Sports1 day agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Crypto World6 days ago

Crypto World6 days agoAlibaba bans Claude Code over alleged backdoor security concerns

You must be logged in to post a comment Login