Crypto World

The slow-motion ‘bank run’ in private credit

Investors tried to pull $13 billion out of private credit funds this quarter. They got less than half. For many crypto investors, if the collapse of private credit continues, half could end up being a good outcome.

Seven private credit giants capped investor withdrawals this quarter, including Morgan Stanley, BlackRock, Apollo, Blue Owl, Cliffwater, Blackstone, and Ares. Oaktree almost joined that group, although it technically fulfilled its 8.5% in withdrawal requests by having parent Brookfield buy 1.7% of shares at the eleventh hour.

Private credit funds package up illiquid loans inside vehicles that typically go up, except during rare times of crisis, such as during a major war or mass job losses.

They also typically limit quarterly withdrawals to 5%, which is not a problem until many people want out, like they do now.

When more than 5% want to withdraw, everyone gets a haircut on their withdrawal request. At Apollo and Ares, 11% wanted out. Those funds returned less than half.

Crypto started joining the private credit bandwagon years ago, selling similar products in a different wrapper. Many stablecoin and altcoin treasury managers invest in private credit directly.

‘A quasi run on the bank’

Michael Saylor delivered a keynote at the Blockworks Digital Asset Summit on March 26, the same week Apollo and Ares gated withdrawals. He pitched his company’s dividend-paying stocks as competitors to private credit.

Saylor even called the multi-trillion dollar private credit crisis this year “a quasi-run on the bank.”

Worse, the same companies gating traditional private credit withdrawals are tokenizing private credit on blockchains. Apollo launched ACRED, a tokenized feeder into Apollo’s Diversified Credit Fund. A few months after that launch, Apollo’s partner Securitize had built sACRED, a derivative to goose yields even higher through risky decentralized finance (DeFi) protocols.

Holders can buy ACRED, deposit it into DeFi vaults, borrow stablecoins, buy more ACRED, and loop. Yields after looping, which are tantamount to risk, soared.

Securitize initially advertised daily redemption rights for ACRED holders, which was quite curious given that most private credit funds limit quarterly redemptions to 5%. Then, after crypto publication Unchained asked about the mismatch with the fund’s quarterly 5% cap, Securitize quietly removed daily liquidity rights.

Easier to buy, just as hard to sell

In other words, crypto tokenization changed the speed at which people could buy and add leverage. It did not change the speed at which they could sell.

Nor did crypto improve the most important characteristic of private credit: the deteriorating credit qualities of US borrowers who are suffering higher fuel prices, AI-induced job layoffs, wartime uncertainty, inflation, and rising costs of living.

Crypto sold versions of the same illiquid debt that investors cannot exit quickly in any environment, let alone the current “quasi run on the bank” reality.

By one analyst’s count, tokenized private credit surged from $25 million to $6 billion over the last year.

Read more: Bitcoin mortgages debut with 60% haircut and no margin calls

Using blockchain for private credit instruments merely extends leverage and the rehypothecation chain that amplifies losses in a market downturn.

Goldfinch, a DeFi protocol for undercollateralized real-world lending, has already suffered three defaults totaling $18 million. The most recent default wiped out more than 7% of its active loan book.

A bad loan is still a bad loan, even if a smart contract wraps it in a token.

Billions queued up to leave private credit

Apollo Debt Solutions, valued at about $15 billion, received redemption requests for 11.2% of its shares. It enforced a 5% cap and returned $730 million of $1.5 billion requested. Ares Strategic Income Fund faced 11.6% in requests and did the same.

Blackstone recorded a record 7.9% in requests totaling nearly $4 billion. It raised its cap to 7% and injected $400 million of its own capital. BlackRock’s $26 billion fund received $1.2 billion in requests. Cliffwater’s $33 billion fund saw the worst: 14% demanded back.

Across roughly a dozen funds, about $4.6 billion in investor capital remains trapped.

Blue Owl Capital is the poster child of the current crisis in private credit. The company permanently halted redemptions from its retail-focused Blue Owl Capital Corp II in February. Its stock has declined 42% since the start of the year and 60% over the past twelve months.

Smelling blood, a shark investor launched a tender offer for 6% of Blue Owl Capital Corp II at about 65 cents on the dollar.

“All you need is for the snowball to start rolling down the hill, and it has begun,” the investor said at a recent investment conference.

Crypto credit risks

Federal Reserve Chair Jerome Powell addressed private credit on March 30 at Harvard University. He called it a correction, not a systemic event.

Nonetheless, Powell’s contentious reassurance arrived the same week that DZ Bank, Germany’s second-largest lender, warned that private credit could trigger a chain reaction with severe negative effects for the US economy.

A record 63% of fund managers surveyed by Bank of America identified private equity and private credit as the most likely source of the next wave of systemic bankruptcies.

Default rates would tend to agree. The private credit default rate reached 5.8% through January 2026, the highest since Fitch’s index launched. Morgan Stanley forecasts it will climb to 8%, more than triple the historical average. UBS has warned that severe AI disruption to software borrowers could push defaults to 13%.

Software exposure is the fault line. About 26% of direct lending loans went to software companies. Many built business models on costly subscriptions that AI is now undermining. Blackstone’s flagship BCRED fund posted its first monthly loss in three years in February after marking down loans.

Wall Street spent years pitching private credit as institutional-grade yield, and crypto wanted to democratize and decentralize it. What they actually democratized and decentralized was the purchase of opaque, illiquid loans by retail investors with 5% quarterly redemption limits whose fund managers choose the valuations of their own assets with broad discretion.

As Protos has previously reported, this type of opacity in financial products is a feature, not a bug. Now those investors want their money back. The funds are returning less than half.

Powell says it is not systemic. About two thirds of private fund managers disagree.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

TLDR:

- The Cayman Islands officially holds $427 billion in U.S. Treasuries, but Fed research puts the true figure far higher.

- Fed researchers identified a $1.4 trillion undercount, making the Cayman Islands the largest foreign Treasury holder.

- Hedge funds domiciled in the Cayman Islands absorbed 37% of all net Treasury issuance between 2022 and 2024.

- Unlike central banks, hedge funds can exit Treasury positions rapidly, posing a risk to U.S. debt market stability.

The Cayman Islands, a Caribbean territory with just 90,000 residents, holds more U.S. Treasuries than Japan or China.

Federal Reserve researchers have found that official data undercounts the island’s actual holdings by $1.4 trillion. This discovery reshapes long-held assumptions about who finances American debt.

For decades, analysts pointed to Asian economic giants as the backbone of Treasury demand. The real picture, however, tells a different story entirely.

Hedge Funds Drive Cayman Islands’ Treasury Holdings Beyond Official Figures

Official records place Cayman Islands holdings at $427 billion, ranking it sixth among foreign holders. Japan leads on paper at $1.22 trillion, followed closely by China.

However, Fed researchers determined the official count misses over $1.4 trillion in actual Cayman-linked purchases.

The reason behind this gap is structural. The Cayman Islands serves as the legal domicile for roughly three-quarters of the world’s offshore hedge funds.

When those funds buy Treasuries, the purchases register under the Cayman Islands, regardless of where the fund managers actually operate.

Between 2022 and 2024, hedge funds domiciled there purchased $1.2 trillion in Treasury securities. That figure absorbed 37% of all net issuance during that period. As @BullTheoryio noted, that is nearly equal to what all other foreign investors combined purchased.

After the Fed’s adjustment, the Cayman Islands surpasses Japan, China, and the United Kingdom combined. This makes a nine-square-mile island the single largest foreign financier of U.S. government debt today.

Treasury Market Stability Faces Questions as Hedge Fund Exposure Grows

Central banks and sovereign wealth funds tend to hold Treasuries as long-term reserve assets. They rarely exit positions abruptly, even during periods of market stress. Hedge funds operate under an entirely different framework.

These funds carry leveraged positions and answer to performance mandates, not policy goals. They have no obligation to remain invested when market conditions shift against them. That difference matters greatly when the largest buyer controls such a large share of demand.

In April 2025, a sudden tariff announcement triggered simultaneous unwinding across multiple funds. That coordinated exit added pressure across the entire Treasury market at once. The event exposed just how quickly this pool of demand can reverse.

The Fed’s own paper concluded with a direct warning directed at analysts and policymakers. Researchers wrote that “data users should be aware that this major gap exists.” That single line carries weight given the scale of the miscounting involved.

The Cayman Islands’ GDP stands at $7 billion, yet funds registered there finance positions worth many times that figure overnight.

The concentration of leveraged, short-term capital in one jurisdiction now sits at the center of U.S. debt market dynamics.

Large Bitcoin investors are absorbing significant realized losses as the flagship cryptocurrency remains trapped in a prolonged sideways slump below $70,000.

According to on-chain data from Glassnode, wallets holding between 100 and 10,000 BTC are currently realizing daily losses of over $200 million based on a 7-day moving average. These large investors are often referred to as “whales” and “sharks.”

Bitcoin Slump Forces Major Holders Into Deep Losses

Notably, this pain is particularly acute among “Long-Term Holders.” This represents investors who acquired their coins more than six months ago near the peak of the previous rally.

The 30-day simple moving average of Long-Term Holder Realized Losses has climbed steadily since November 2025. This upward trend confirms that veteran investors are increasingly capitulating and selling at a loss.

While this flush-out of underwater buyers is a standard feature of bear-market resolutions, Glassnode analysts note it is not yet sufficient to call a bottom.

To signal the structural exhaustion that typically precedes a new bull cycle, selling pressure will likely need to decelerate to below $25 million in daily realized losses.

However, the chances of reaching that exhaustion point quickly seem slim, as the market is currently gripped by its most bearish sentiment in months.

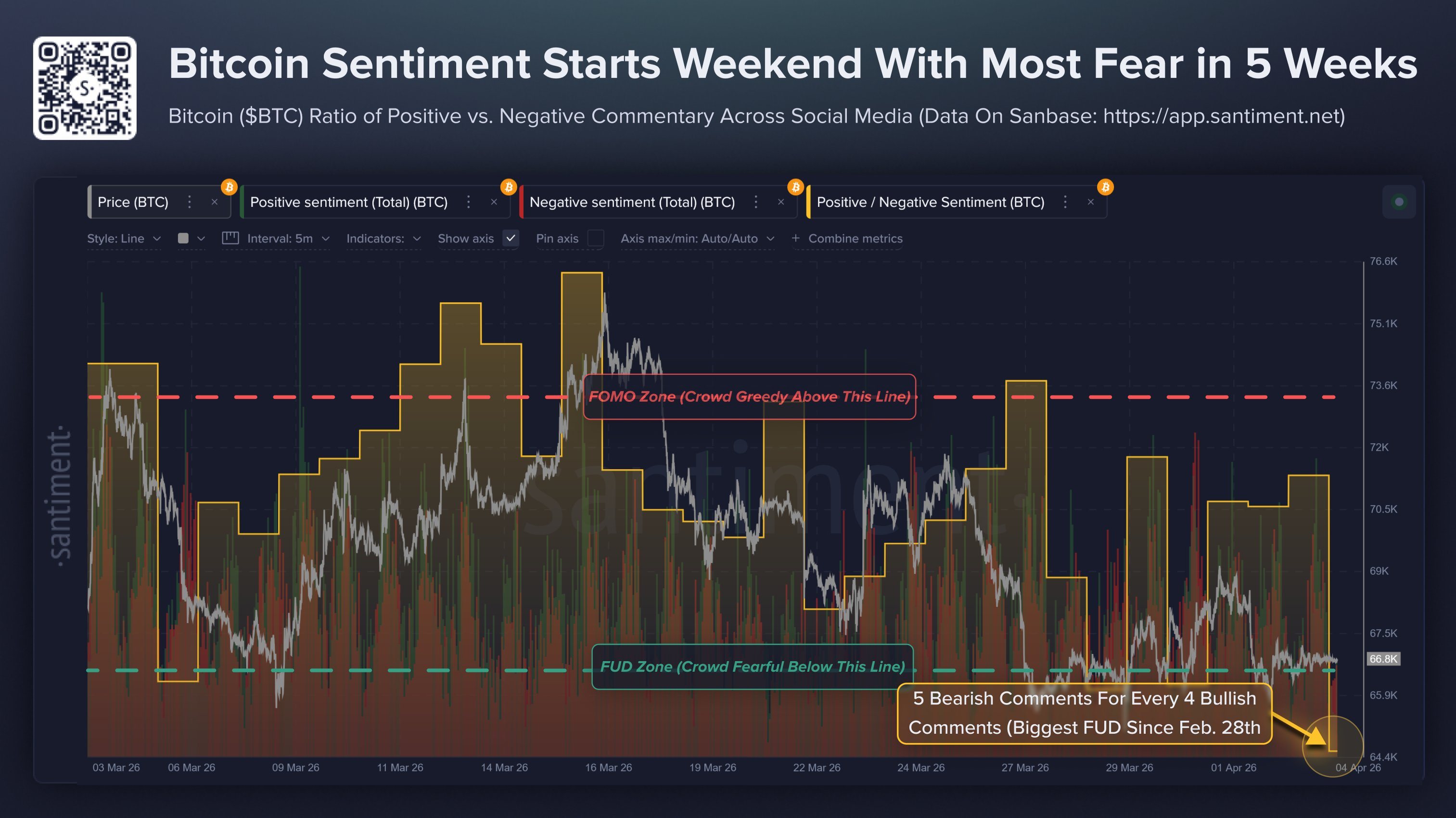

Blockchain analytics firm Santiment reports that fear, uncertainty, and doubt (FUD) have crept back into the community.

Citing data across social media platforms, including X, Reddit, and Telegram, Santiment noted that Bitcoin is seeing its highest bearish discussion ratio since late February.

The firm noted that BTC is showing a ratio of just 0.81 bullish comments per bearish one amid this extended period of stagnation.

With Bitcoin’s price hovering around $66,800, ongoing geopolitical tensions and domestic regulatory debates are fueling widespread pessimism.

Yet, Santiment pointed out that there is a silver lining for contrarian traders as markets typically move in the opposite direction of the crowd’s expectations.

Historically, this heightened fear has fueled price rebounds. This suggests the current market conditions could turn positive sooner than the broader community anticipates.

The post Bitcoin Whales Are Losing $200 Million Daily As Market Fear Rises appeared first on BeInCrypto.

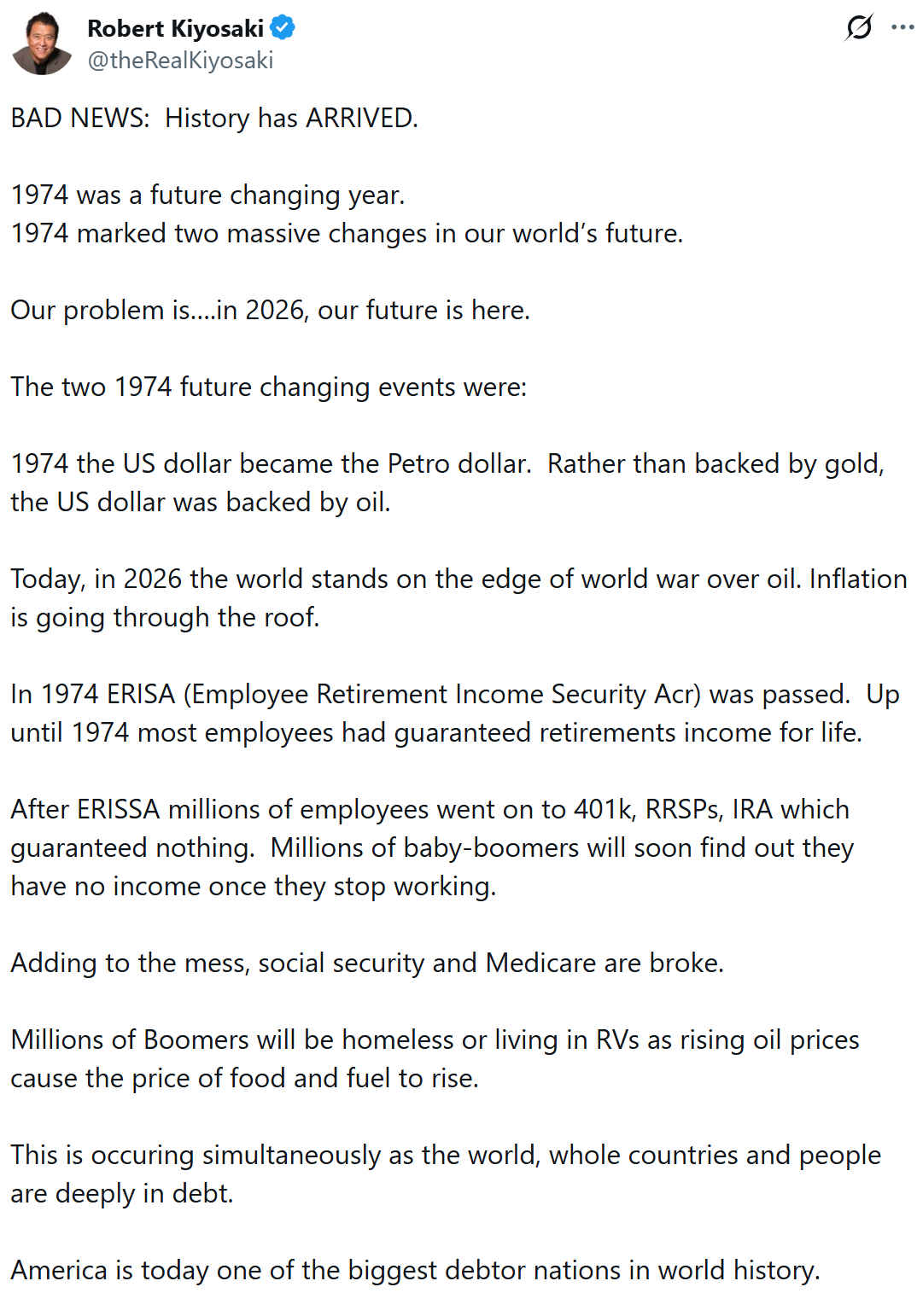

Robert Kiyosaki said current economic pressure reflects changes that began in the 1970s.

Summary

- Kiyosaki said 1974 policy shifts still shape debt, inflation, retirement pressure, and demand for Bitcoin.

- He warned baby boomers may face retirement income gaps as pensions gave way to market-based accounts.

- Santiment data showed Bitcoin bearish sentiment rose, while contrarian traders watched fear levels for reversal signs.

Robert Kiyosaki said 1974 marked a major shift in how money and retirement worked in the United States. In a post on X, he wrote that “the future created in 1974 has arrived” and tied today’s financial stress to policy changes from that period.

He connected that year to the petrodollar system and to changes in retirement planning. Kiyosaki said those changes helped shape the debt and inflation concerns now facing households and investors.

Kiyosaki also referred to the Employee Retirement Income Security Act and the wider move away from pension structures that paid workers for life. He said many workers now depend on market-based retirement accounts instead of guaranteed income after leaving work.

He warned that this shift placed more responsibility on individuals. In the same post, he wrote that “millions of baby-boomers will soon find out they have no income once they stop working,” linking that concern to long-term pressure on retirement security.

In addition, Kiyosaki repeated his long-running support for gold, silver, and Bitcoin. He described those assets as “real money” and said people should focus on financial education while looking at alternative stores of value.

His latest remarks follow similar warnings from recent months. Last month, he said a major financial “bubble burst” could send capital into scarce assets and push Bitcoin much higher. He also said Bitcoin could reach $750,000 within a year after such a crash.

Bitcoin sentiment turns more negative

At press time, Bitcoin traded near $66,826. Kiyosaki’s latest comments arrived as market sentiment around the asset weakened. Data from Santiment showed bearish discussion on social platforms rose to its highest level since late February.

The platform said the bullish-to-bearish comment ratio fell to 0.81, showing weaker confidence among traders. Santiment also said that extreme fear can sometimes act as a contrarian signal, with markets often moving against the crowd when negative sentiment grows too strong.

Crypto World

How Japan’s Surging Government Bond Yields Are Triggering a Global Liquidity Drain on Bitcoin

TLDR:

- Japan holds ¥390 trillion in JGBs — a 1% yield rise could trigger tens of trillions in unrealized losses.

- Japanese institutions are liquidating foreign risk assets, pulling global liquidity as capital returns home.

- Early 2026 saw $9.6 billion exit Bitcoin, with capital rotating into stablecoins amid rising rate pressure.

- Stablecoin supply near all-time highs signals sidelined capital that has yet to re-enter risk markets.

Rising Japanese government bond yields are quietly reshaping the global liquidity landscape in 2026. As yields climb, Japan’s largest domestic institutions face mounting pressure on their balance sheets.

This pressure triggers a chain of asset liquidations and capital repatriation that extends far beyond Japan’s borders.

Bitcoin, as a globally sensitive risk asset, is absorbing the consequences of this contraction. Understanding this dynamic is now essential for anyone tracking crypto market behavior.

How Rising JGB Yields Are Draining Global Liquidity

Japanese government bond yields have been rising steadily due to several converging macro forces. Policy normalization expectations from the Bank of Japan are a primary factor.

Persistent inflation and mounting fiscal expansion concerns are adding further upward pressure. Together, these forces are pulling bond prices lower across the curve.

Japan’s domestic institutions hold approximately ¥390 trillion in government bonds. Even a 1% rise in yields can produce tens of trillions of yen in unrealized losses.

Banks, insurers, and pension funds carry the heaviest exposure among domestic holders. These institutions are now being forced into difficult balance sheet decisions.

To manage growing losses, many institutions are liquidating risk assets abroad. Capital is being repatriated back to Japan at an accelerating pace.

Japan ranks among the world’s largest external investors, so these moves carry global weight. Each wave of repatriation effectively removes liquidity from international financial markets.

Data is already confirming this trend. Yen-denominated external credit has declined noticeably in recent months. This decline reflects the active withdrawal of Japanese capital from global markets. The essence of liquidity contraction is visible in these numbers, and Bitcoin is not immune to it.

Bitcoin Absorbs the Pressure as Deployed Liquidity Shrinks

Bitcoin’s sensitivity to global liquidity conditions makes it particularly vulnerable during this period. Historically, low-rate environments provided the fuel for Bitcoin’s price expansion cycles.

Rising rates reduce leverage across markets and suppress new demand from institutional participants. Japan’s climbing yields are directly contributing to this tightening dynamic.

Early 2026 data recorded approximately $9.6 billion flowing out of Bitcoin. Much of this capital rotated into stablecoins rather than leaving crypto markets entirely.

This rotation points to investors reducing risk exposure while staying positioned for re-entry. Higher rates appear to be the primary force behind this cautious capital movement.

Stablecoin supply data adds another layer to this picture. The “All Stablecoins (ERC20): Total Supply” chart has returned to near all-time highs.

This level shows that substantial capital remains parked and waiting on the sidelines. Yet this liquidity is not actively entering risk markets, reflecting a “liquidity exists but is not deployed” condition.

Analysts now argue that Bitcoin can no longer be tracked through on-chain metrics alone. Rates, foreign exchange movements, and global credit flows must be part of the analysis framework.

Japan’s rising JGB yields have become a central variable in understanding Bitcoin’s macro environment. Liquidity contraction originating in Tokyo is now a force felt across global crypto markets.

The crypto industry is confronting a paradox: an explosion in the number of tokens, paired with stagnating overall value. Industry observers say the surge in supply is outpacing the demand and usefulness of the assets, raising what one founder calls an existential challenge for the sector.

In a stream of posts on X, Michael Ippolito, co-founder of Blockworks, highlighted a stark divergence between the proliferation of tokens and the value they generate. “The average coin is only slightly higher than where it was in 2020 and down about 50% since 2021,” he wrote, underscoring how a larger token universe has not translated into commensurate gains for holders. He also noted that median token returns have fallen sharply, with most assets down roughly 80% from their peaks, suggesting gains have become concentrated in a narrow group of large-cap tokens while the broader market lags.

Ippolito argues the root cause is supply: a rapid expansion in token issuance has minted a vast number of assets even as total market capitalization remains mostly flat. “We created a ton of new assets and still total market cap is flat,” he said, warning that value dilution across a growing token pool undermines the industry’s fundamentals.

Key takeaways

- Token inflation is projected to outpace value generation, diluting investor returns as the number of assets multiplies against a relatively flat market cap.

- Prices and on-chain fundamentals have diverged since 2021, with on-chain revenue lifting only modestly while token prices fail to follow.

- Public commentary from prominent investors echoes concern that token issuance dynamics threaten broader ecosystem credibility and long-term relevance.

- Capital allocation appears to be shifting away from newly issued tokens toward publicly listed crypto firms, with the majority of token launches trading below their generation event prices.

Token prices break from fundamentals

Beyond the expansion of assets, observers note a weakening link between on-chain activity and market prices. In 2021, token valuations tended to track protocol revenues and usage. More recently, even as some networks have reported renewed revenue generation, prices have not mirrored that momentum. This decoupling, according to Ippolito, signals waning investor confidence in tokens as reliable vehicles for capturing value.

Arthur Cheong, founder and CEO of DeFiance Capital, echoed the sentiment, urging the industry to address the token conundrum. In a post on X, Cheong argued that if the market remains concentrated around a small handful of assets like Bitcoin and Ether, the broader ecosystem risks losing relevance. The sense of urgency around realigning token economics with price remains a recurring theme among influential investors.

Capital shifts from tokens to stocks

New research adds a practical dimension to the conversation: capital is rotating away from fresh token launches and toward publicly listed crypto companies. A February report from DWF Labs found that over 80% of token projects traded below their token generation event (TGE) price, with typical losses ranging from 50% to 70% within roughly three months. The study details a pattern where peaks occur within the first month after launch, followed by sustained selling pressure and overhang from airdrops and early investor unlocks that depress subsequent price action.

Andrei Grachev of DWF Labs framed the finding as structural rather than cyclical, suggesting that the dynamics of token issuance—especially post-launch unlocks—continue to weigh on price trajectories even for projects with active products or protocols.

Broader implications for the market

Taken together, the observations point to a market that must reconcile a rapidly expanding asset universe with a comparatively stable or shrinking value base. If the industry cannot restore alignment between token fundamentals and price, the appeal of tokens as value-bearing instruments could wane, risking broader adoption and investment interest. The conversation is reframing token issuance practices, with voices in the ecosystem calling for tighter economics, improved utility, and more disciplined distribution models to prevent perpetual dilution.

As the debate unfolds, market participants will be watching several key developments: whether new tokens adopt more conservative supply schedules or unique value accrual mechanisms, how regulators and auditors respond to proliferation and complex unlock patterns, and whether investors increasingly favor tokenized representations tied to real-world use cases or established crypto firms over speculative launches.

For readers seeking direction, the coming quarters will reveal whether the industry can re-anchor token prices to tangible fundamentals or whether concentration in a few dominant assets will persist, leaving many projects competing for marginal gains in a crowded field.

Watch next for how token issuers adapt to this critique, whether capital rotates further toward crypto-listed equities or continues to seek merit across the broader asset class, and what, if any, policy or market-driven reforms emerge to restore alignment between innovation and value.

Bitcoin added downside BTC price warnings as Binance order-book data showed multiple investor classes selling coins into the weekend.

Bitcoin (BTC) circled $67,000 on Sunday as traders warned of hidden BTC price weakness.

Key points:

-

Bitcoin Bollinger Bands demand a volatile BTC price breakout after a slow weekend.

-

A trader predicts a move lower thanks to weak support and exposed downside wicks.

-

Sideways price action comes as sellers step up into the end of the week.

Bitcoin trader waits for sweep of sub-$60,000 lows

Data from TradingView showed volatility cooling over the weekend, with BTC/USD acting within an increasingly narrow range.

On four-hour time frames, the Bollinger Bands volatility indicator constricted — a classic signal that a sharp move up or down was due.

In their latest analysis, pseudonymous trader LP bet on bears winning the battle.

“Looking back at previous cycles, bottoms were formed after multiple sweeps of the lows, forcing capitulation before a reversal,” a post on X read.

“In contrast, this cycle has been doing the opposite, consistently sweeping the highs, making it difficult to enter short positions while leaving the lows exposed and building liquidity below.”

LP said that sweeping local lows, including February’s wick below $60,000, was “likely just a matter of time.”

“When that breakdown eventually happens, watch the behavior closely. If price starts repeatedly sweeping the lows, making it psychologically difficult to enter longs, that’s when a true bottom is more likely forming,” they concluded.

Whales “buying dips and selling rips” on BTC

Continuing, Keith Alan, cofounder of trading resource Material Indicators, flagged unusual selling activity despite flat BTC price action.

Related: Bitcoin ‘done’ with 85% crashes, says Cathie Wood amid new $34K target

Uploading a chart of Binance order-book liquidity and volume by investor class, Alan highlighted a bot using time-weighted average price (TWAP) to distribute BTC on Friday.

“The vertical orange line represents the smallest order class with a TWAP bot selling $18M in an hour,” he explained.

“That’s exponentially more than their normal $3M-$5M daily volume in 1 hr. That ain’t retail!”

Whales, Alan added, were “buying dips and selling rips” with Bitcoin still trapped in a range.

Earlier, Cointelegraph reported on further threats to Bitcoin bulls, including resurgent US dollar strength.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Bitcoin (BTC) traded near $66,749 at press time, while market activity stayed muted across major digital assets.

Summary

- Bitcoin traded near $66,749 as low volatility and weak liquidity kept traders watching for moves.

- Analyst Michaël van de Poppe said Bitcoin may sweep liquidity before a fast recovery upward.

- EGRAG CRYPTO said past Bitcoin cycle bottoms often reached the 1.618 Fibonacci zone before rebounding.

The asset was down slightly in the past 24 hours, while seven-day gains stood at 0.81%. Daily trading volume reached $19.67 billion.

That price action came during a period of weak movement in the market. Analysts tracked a narrow range in Bitcoin and pointed to low activity across the wider crypto sector. Altcoins also showed soft volume and thinner liquidity during the same period.

Analysts track a possible end to the squeeze

Crypto analyst Michaël van de Poppe said volatility on Bitcoin’s four-hour chart had dropped to its lowest level since the broader breakdown. He said the market was nearing the end of a volatility squeeze that usually does not last much longer under similar conditions.

Van de Poppe also said altcoins showed the same pattern, with low volatility, low volume, and low liquidity. Despite the geopolitical backdrop, he wrote that he would not expect a much deeper move lower and instead saw a possible liquidity sweep followed by a quick recovery, “most likely during next week already.”

Crypto market commentator EGRAG CRYPTO pointed to longer-term chart structure. He said past Bitcoin cycle bottoms repeatedly reached the 1.618 Fibonacci level before the market formed a base.

He described that level as an area where fear often peaks and accumulation starts. The post framed that view as a structure-based reading rather than a reaction to short-term headlines. The account also urged traders to focus on charts and numbers instead of outside narratives.

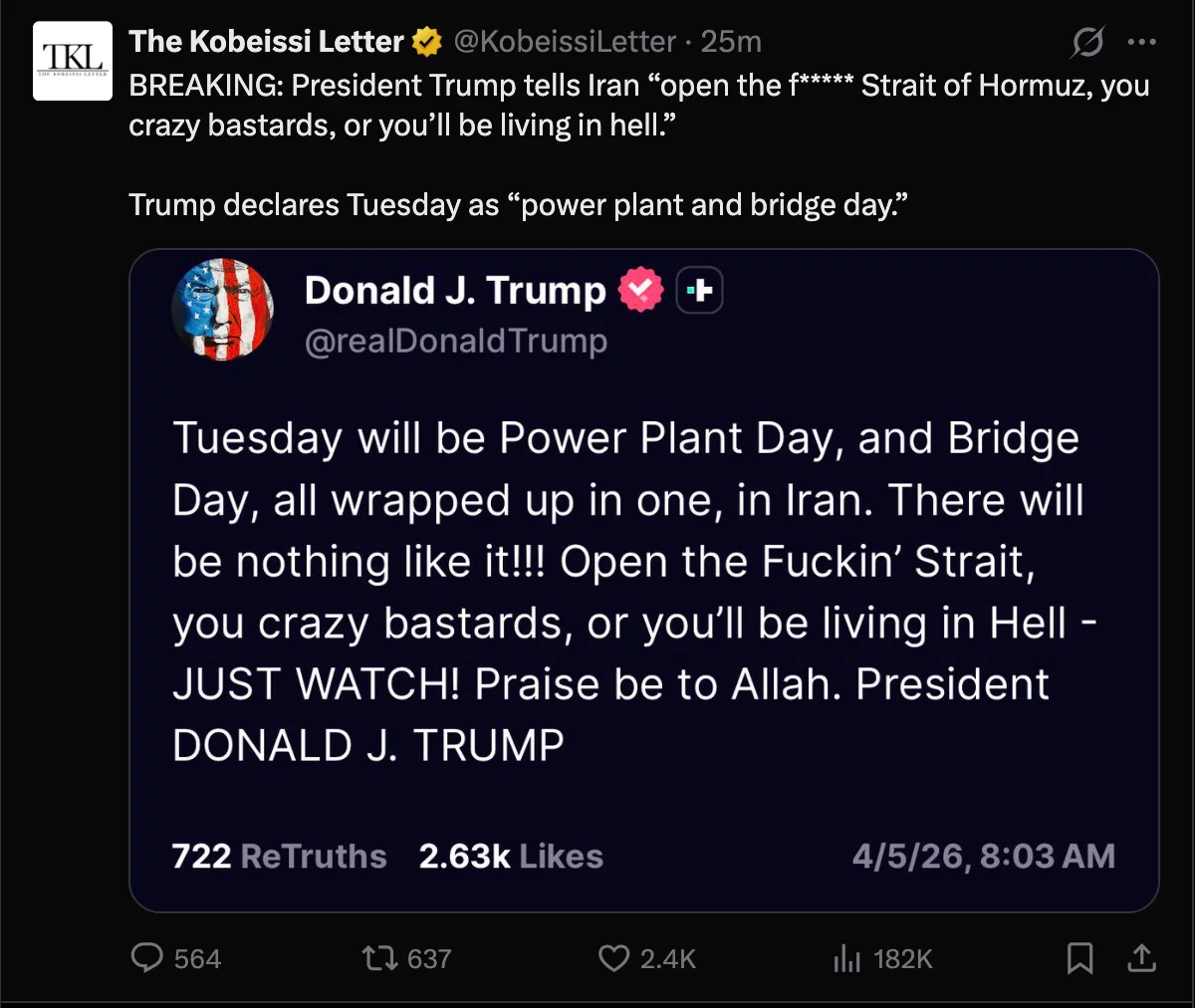

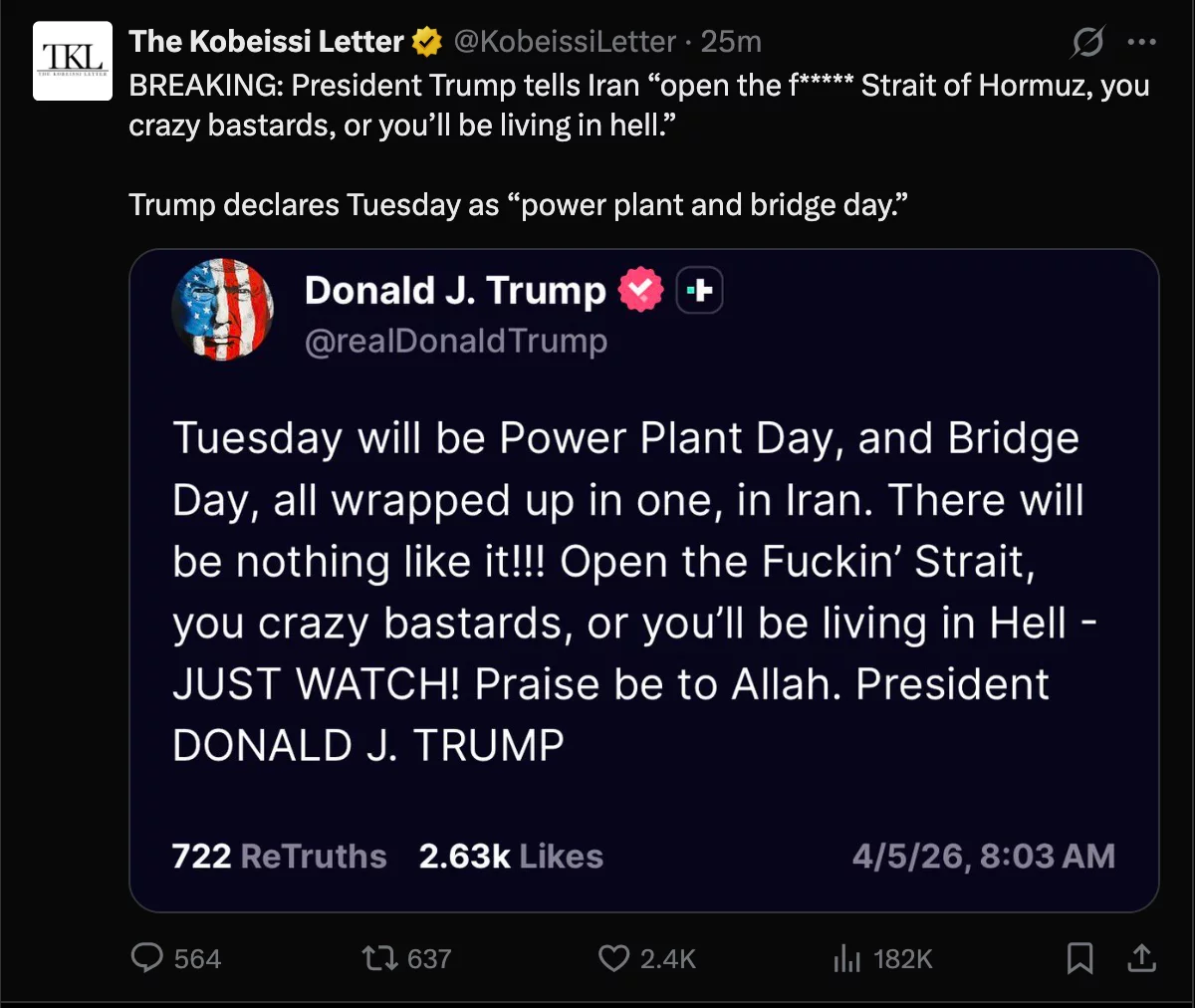

At the same time, traders watched new posts from The Kobeissi Letter about comments attributed to Donald Trump on Iran and the Strait of Hormuz.

The account also said Trump planned a news conference with the US military at 1 PM ET on Monday. Those headlines added another layer of caution for crypto traders.

Rich Dad Poor Dad author Robert Kiyosaki has argued that the economic shifts set in motion more than five decades ago are now unfolding, advocating for Bitcoin and gold while warning against rising debt, inflation and retirement risks.

In a Saturday post on X, Kiyosaki pointed to 1974 as a turning point that reshaped both money and retirement systems. He argued that the United States’ move toward a petrodollar framework, alongside policy changes affecting pensions, laid the foundation for today’s financial pressures.

“The future created in 1974 has arrived,” Kiyosaki wrote, linking current inflation and geopolitical tensions around energy to the dollar’s evolution after the end of the gold standard era. He also mentioned the passage of the Employee Retirement Income Security Act, which introduced new rules for pension plans and coincided with a broader shift toward market-based retirement savings.

According to Kiyosaki, that transition replaced guaranteed lifetime income for many workers with systems such as 401(k)s and similar accounts, placing more risk on individuals. “Millions of baby-boomers will soon find out they have no income once they stop working,” he warned.

Related: Rich Bitcoin traders lost $337M daily in first quarter of 2026

Kiyosaki supports Bitcoin, gold as “real money”

Kiyosaki reiterated his long-standing view that individuals should focus on financial education and consider alternative stores of value. He said he continues to favor assets such as gold, silver and Bitcoin, which he describes as “real money.”

Last month, Kiyosaki warned that a major financial “bubble burst” could be approaching, arguing that such a crisis may trigger a sharp rally in scarce assets like Bitcoin (BTC). He suggested Bitcoin could reach $750,000 within a year of the crash.

His view is tied to the expansion of global money supply, which historically has driven demand for limited assets. During the 2020–2021 period, rising liquidity coincided with strong gains in stocks and real estate. Kiyosaki expects a similar dynamic after a downturn, also forecasting that gold could surge significantly.

Related: ‘Rich Dad, Poor Dad’ author says ‘pin is near’ on TradFi ‘bubble burst:’ Predicts $750K Bitcoin

Bitcoin bearish sentiment spikes

Meanwhile, bearish sentiment around Bitcoin has climbed to its highest level since late February, according to data from crypto analytics platform Santiment. The ratio of bullish to bearish comments across major social platforms has dropped to 0.81, reflecting a noticeable lack of optimism among market participants.

Despite the negative tone, Santiment suggested this could be a contrarian signal. Historically, markets tend to move against crowd expectations, meaning elevated fear and uncertainty may precede a price recovery.

Magazine: Bitcoin 85% crashes ‘done,’ CLARITY Act speculation mounts: Hodler’s Digest, Mar. 29 – April 4

TLDR:

- Every crypto cycle since 2017 has produced one dominant chain or narrative that rewarded early participants.

- The 2022 collapse of LUNA and FTX proved that capital preservation matters more than chasing the hottest trend.

- By 2025, nations began stacking Bitcoin as a reserve asset, shifting the buyer profile beyond retail investors.

- Entering 2026 with no clear winner yet, history points to a new season forming before most participants notice it.

Each crypto market cycle has produced a clear winner — until the next one arrived. Observers tracking blockchain trends over the past decade have noted a recurring pattern: capital, attention, and momentum rotate between chains and narratives.

Understanding these cycles has separated profitable participants from those who stayed focused on yesterday’s opportunities. The question entering 2026 is which season comes next.

Bitcoin and Ethereum Set the Foundation for Rotating Chain Dominance

Crypto market cycles began taking shape as early as 2017, when Bitcoin led the charge. Retail investors who simply held BTC through that period came out ahead.

The following year, Ethereum captured that momentum through the ICO boom, making it the dominant chain of 2018.

The bear market of 2019 offered a different kind of lesson. Bitcoin moved from $3,400 to $13,000 and back within a single year. Altcoins largely sat out. Surviving that period came down to patience and conviction rather than active trading.

Then 2020 introduced DeFi, and Ethereum rewarded on-chain participants generously. Protocols like YFI, AAVE, and UNI generated returns that traditional markets could not match.

Solana followed in 2021, establishing itself as a credible alternative to Ethereum and running hard across the board.

As analyst Jeremy noted on X, “Every chain has its season. Most people only notice after it’s over.” That observation holds true across each of these periods. The rotation was visible in hindsight, though rarely obvious in real time.

2022 Through 2026 Reflects the Shift Toward Institutional and National Narratives

The 2022 cycle stands apart from the rest. No single chain won. LUNA collapsed by May, and FTX followed in November.

The market rewarded caution over speculation that year. Those who avoided both disasters preserved enough capital to participate in the next cycle.

Bitcoin reasserted itself in 2023, quietly. Ordinals introduced a new use case directly on the Bitcoin base layer. Meanwhile, the ETF approval narrative built steadily while much of the market was still recovering from 2022.

Solana returned in 2024, this time through meme coins. The Pump.fun platform became the symbol of that era. Jeremy cited one trader who turned $72,000 into $30 million within three days on a meme coin. That kind of return drew a new wave of participants to the Solana ecosystem.

By 2025, the narrative moved beyond retail entirely. Nations began accumulating Bitcoin as a reserve asset. That shift in buyer profile changed the dynamics of the market in a way that previous cycles had not seen.

Entering 2026, no dominant chain or narrative has emerged yet. According to Jeremy, “The next season is loading.” Those positioned ahead of the cycle stand to benefit most.

A six-month intelligence operation preceded the $270 million exploit of Drift Protocol and was carried out by a North Korean state-affiliated group, according to a detailed incident update published by the team earlier on Sunday.

The attackers first made contact around fall 2025 at a major crypto conference, presenting themselves as a quantitative trading firm looking to integrate with Drift.

They were technically fluent, had verifiable professional backgrounds, and understood how the protocol operated, Drift said. A Telegram group was established and what followed were months of substantive conversations around trading strategies and vault integrations, interactions that are standard for how trading firms onboard with DeFi protocols.

Between December 2025 and January 2026, the group onboarded an Ecosystem Vault on Drift, held multiple working sessions with contributors, deposited over $1 million of their own capital, and built a functioning operational presence inside the ecosystem.

Drift contributors met individuals from the group face to face at multiple major industry conferences across several countries through February and March. By the time the attack launched on April 1, the relationship was nearly half a year old.

The compromise appears to have come through two vectors.

A second downloaded a TestFlight application, Apple’s platform for distributing pre-release apps that bypasses App Store security review, which the group presented as their wallet product.

For the repository vector, Drift pointed to a known vulnerability in VSCode and Cursor, two of the most widely used code editors in software development, that the security community had been flagging since late 2025, where simply opening a file or folder in the editor was sufficient to silently execute arbitrary code with no prompt or warning of any kind.

Once devices were compromised, the attackers had what they needed to obtain the two multisig approvals that enabled the durable nonce attack CoinDesk detailed earlier this week. Those pre-signed transactions sat dormant for more than a week before being executed on April 1, draining $270 million from the protocol’s vaults in under a minute.

The attribution points to UNC4736, a North Korean state-affiliated group also tracked as AppleJeus or Citrine Sleet, based on both on-chain fund flows tracing back to the Radiant Capital attackers and operational overlap with known DPRK-linked personas.

The individuals who appeared in person at conferences were not North Korean nationals, however. DPRK threat actors at this level are known to deploy third-party intermediaries with fully constructed identities, employment histories, and professional networks built to withstand due diligence.

Drift urged other protocols to audit access controls and treat every device touching a multisig as a potential target. The broader implication is uncomfortable for an industry that relies on multisig governance as its primary security model.

But if attackers are willing to spend six months and a million dollars building a legitimate presence inside an ecosystem, meet teams in person, contribute real capital, and wait, the question is what security model is designed to catch that.

Jody McIntyre asks damages from MP who called him a Jew hater

The Financial Freedom STRATEGY Nobody Teaches (Infinity Investing)

Clothes won’t smell ‘stale and nasty’ after washing if you stop making 1 common mistake

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business3 days ago

Business3 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment6 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech6 days ago

Tech6 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World5 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech6 days ago

Tech6 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Business3 days ago

Business3 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Sports16 hours ago

Sports16 hours agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech6 days ago

Tech6 days agoApple will hide your email address from apps and websites, but not cops

-

Sports5 days ago

Sports5 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech5 days ago

Tech5 days agoEE TV is using AI to help you find something to watch

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech5 days ago

Tech5 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion6 days ago

Fashion6 days agoThe Best Spring Trends of 2026

-

Tech5 days ago

Tech5 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Sports6 days ago

Sports6 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Crypto World7 days ago

Bitcoin’s Six-Month Losing Streak: What On-Chain Data Says About the Market’s Next Move

-

Politics6 days ago

Politics6 days agoBBC slammed for ignoring author of The Fraud

You must be logged in to post a comment Login